Sample Category Title

Forex and Cryptocurrency Forecast

EUR/USD: Awaiting a Turbulent Week

Recall that Monday, 27 May was a holiday in the US. However, on Tuesday, dollar bulls took control, and the DXY Index started to rise, bolstered by a significant increase in the US Consumer Confidence Index (from 97.5 to 102.0 against a forecast of 96.0). Consequently, EUR/USD moved southward.

Pressure on the euro was also due to expectations that the European Central Bank (ECB) is likely to cut the key interest rate by 25 basis points (bps) from 4.50% to 4.25% at its meeting on 06 June. This intention was confirmed by the head of the Bank of Finland, Olli Rehn, who stated on Monday that he considered it timely to transition to dovish rhetoric in June. Similar opinions were expressed by his colleague François Villeroy de Galhau, head of the Bank of France, and on Tuesday, 28 May, by Robert Holzmann, head of the Bank of Austria.

Unlike the dovish stance of European officials, representatives of the Federal Reserve (Fed) take a more stringent position and want to ensure that US inflation is steadily moving towards the 2.0% target.

Recall that the report released on 15 May by the US Bureau of Labour Statistics (BLS) showed that the Consumer Price Index (CPI) decreased from 0.4% to 0.3% month-on-month (m/m) against a forecast of 0.4%. Year-on-year, inflation also fell from 3.5% to 3.4%. Retail sales demonstrated an even stronger decline, dropping from 0.6% to 0.0% m/m (forecast was 0.4%). These data indicated that although inflation is resisting in some areas, it is generally declining. If previously market participants expected the first rate cut at the end of 2024 or even early 2025, after the publication of this data, talks about a possible Fed rate cut already this autumn resumed. Before the release of the preliminary US GDP data, the probability of a rate cut in September was 41%.

The report published on Thursday, 30 May by the Bureau of Economic Analysis showed that, according to preliminary data, US economic growth in Q1 slowed significantly to an annualized rate of 1.3%, below the forecast of 1.6% and Q4 2023's figure of 3.4%.

Experts attribute the weak GDP growth at the beginning of this year mainly to the dynamics of consumer spending. In Q1, consumer spending increased by 2.0%, not the previously expected 2.5%. The US Department of Commerce's revised data also changed the assessment of the Core Personal Consumption Expenditures (PCE) index, which excludes energy and food prices. At the end of Q1, the figure was 3.6%, not 3.7%. Analysts believe that this decline in all indicators was caused by a combination of factors: the depletion of funds accumulated by the population during the COVID-19 pandemic, the Fed's cycle of monetary tightening, and restrained income growth.

Against this backdrop, the dollar weakened slightly, and EUR/USD moved north. It received another bullish impulse after Eurostat presented on Friday, 31 May, a preliminary estimate of inflation in the Eurozone, which accelerated for the first time this year. Thus, the annual growth rate of consumer prices (CPI) in May was 2.6% compared to 2.4% in April, the lowest since November last year. The consensus forecast expected inflation to accelerate only to 2.5%. Core inflation (CPI Core), which excludes energy and food prices, also increased from 2.7% in April to 2.9% in May (forecast was 2.8%). This was a wake-up call for investors who had hoped that the ECB would not only cut rates once this year but continue to do so.

Towards the end of the working week, market attention focused on US consumer market data. According to the Bureau of Economic Analysis, inflation in the country, measured by the Personal Consumption Expenditures (PCE) Price Index, remained stable in April at 2.7% y/y. The Core PCE, which excludes volatile food and energy prices, rose by 2.8% y/y, matching the forecast. Other report details showed that personal incomes rose by 0.3% m/m in April, while personal spending increased by 0.2%.

After these data, the DXY Dollar Index was under slight pressure, and EUR/USD received a third bullish impulse. However, it did not last long, and ultimately, after all these fluctuations, EUR/USD returned to the Pivot Point of the last two and a half weeks, finishing at 1.0848. Regarding the analysts' forecast for the near future, as of the evening of 31 May, all of them (100%) voted for the dollar to strengthen. This forecast is understandable given the expected ECB decision on a rate cut on 06 June. But what if it doesn't happen? Or perhaps this forecast has already been priced into the market? In that case, instead of the dollar strengthening, we could see the opposite reaction.

All trend indicators on D1 are 100% green, while only 50% of oscillators are green, with 15% red and 35% neutral-grey.

The nearest support for the pair lies in the 1.0830-1.0840 zone, followed by 1.0800-1.0810, 1.0725-1.0740, 1.0665-1.0680, 1.0600-1.0620. Resistance zones are in the regions of 1.0880-1.0895, 1.0925-1.0940, 1.0980-1.1010, 1.1050, 1.1100-1.1140.

The upcoming week seems to be very eventful and volatile. On Monday, 03 June, and Wednesday, 05 June, the US Manufacturing and Services PMI data will be released. On 04, 06, and 07 June, there will be a slew of statistics from the US labour market, including Friday's crucial data on the unemployment rate and the number of new non-farm jobs (NFP). The most turbulent day of the week, however, is likely to be Thursday, 06 June. On this day, retail sales data for the Eurozone will be released first, followed by the ECB meeting. The market will be focused not only on the ECB's rate decision but also on the subsequent press conference and comments on future monetary policy.

GBP/USD: Foggy Times, Foggy Forecasts

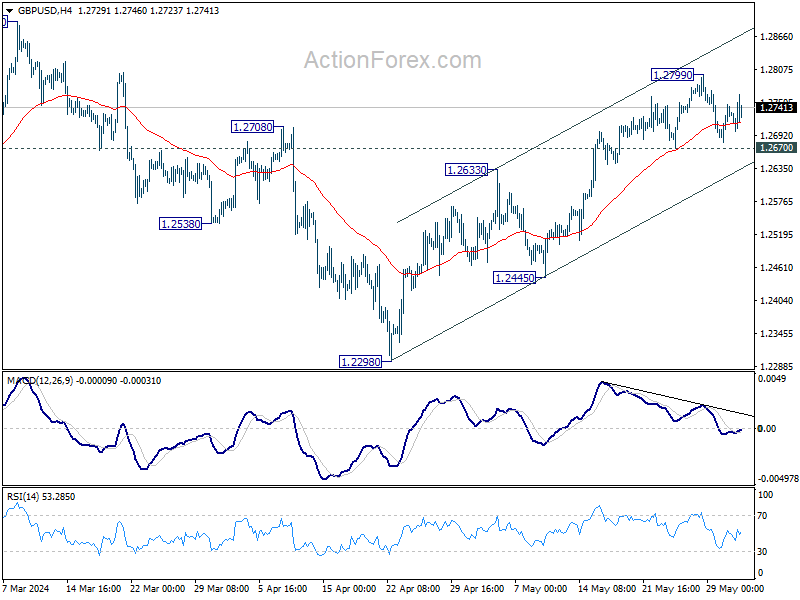

We've previously written that the prospects for the British currency, as well as the national economy, look rather foggy. The Business Activity Index (PMI) showed a decline, and not just it. Much of the pessimism is related to the sharp drop in retail sales in April, which fell by 2.7% y/y compared to the previous growth rate of 0.4%. Additional uncertainty comes from the fact that snap parliamentary elections are scheduled for 04 July. Prime Minister Rishi Sunak stated that "economic instability is just the beginning." This sounds frightening, doesn't it? If this is just the beginning, what lies ahead? Surprisingly, despite this situation, the pound has been strengthening since 22 April. During this period, GBP/USD rose by 500 points and on 28 May recorded a local maximum at the round figure of 1.2800.

Regarding the timing of the Bank of England's (BoE) interest rate cut, everything also seems as foggy as the Thames mist. JP Morgan (JPM) analysts, while adhering to their forecast for a rate cut in August, warn that "the risks have clearly shifted towards a later reduction. The question now is whether the Bank of England will be able to ease its policy at all this year." Goldman Sachs, Deutsche Bank, and HSBC strategists have also adjusted their rate cut forecasts, moving the date from June to August.

GBP/USD ended the week at 1.2741. Economists at Singapore's United Overseas Bank (UOB) believe that the current strengthening of the British currency has ended. UOB considers that over the next 1-3 weeks, "the pound is likely to trade with a downward bias, but a more significant pullback would require breaking below 1.2670. On the other hand, if the pound breaks above 1.2770 (the 'strong resistance' level), it would indicate that it will likely trade within a range rather than pulling back lower."

The median forecast of analysts for the near term is as follows: 75% voted for the pair to move south, while the remaining 25% voted for a northward movement.

As for technical analysis, unlike the experts, all 100% of trend indicators and oscillators on D1 point north, although 15% of the latter signal overbought conditions. If the pair continues to fall, support levels and zones are at 1.2670-1.2700, 1.2575-1.2600, 1.2540, 1.2445-1.2465, 1.2405, 1.2300-1.2330. If the pair rises, it will encounter resistance at levels 1.2760, 1.2800-1.2820, 1.2885-1.2900.

No significant economic statistics are scheduled to be released in the UK next week.

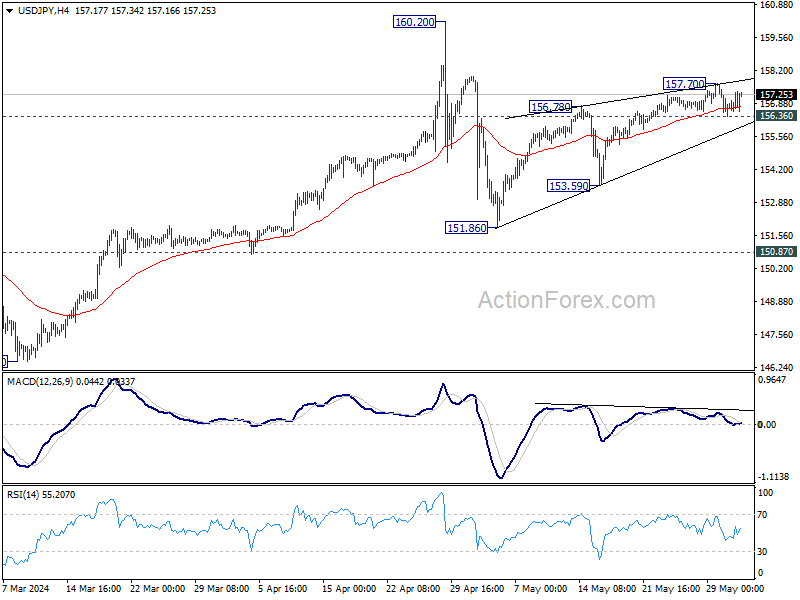

USD/JPY: A Very Calm Week

The past week was surprisingly calm for the yen. USD/JPY moved within a super-narrow sideways channel of 156.60-157.00 for the first half of the week, but then, amid US data and Japanese macro statistics, the trading range expanded slightly to 156.36-157.70. Compared to the price swings at the end of April and early May, it's hard to believe this is the same currency pair. Interestingly, Japanese financial authorities have not officially confirmed whether they conducted intensive yen purchases on 29 April and 1 May to support its exchange rate. However, Bloomberg reports that comparing deposits at the Bank of Japan suggests that around ¥9.4 trillion ($60 billion) might have been spent on these currency interventions, a new monthly record for such financial operations.

However, if this $60 billion helped, it was only slightly – the dollar has already recovered half of its losses. Since interest rates in the US and Europe have not yet decreased, and the yen rate remains extremely low at 0.1%, officials from the Ministry of Finance and the Bank of Japan (BoJ) are trying to buy time until this gap starts to narrow. Comments from BoJ board member Seiji Adachi, who stated on 30 May that the Japanese central bank leaders could raise the interest rate, provided some support for the yen. However, the question of when this might happen remains open, and officials are reluctant to answer. In his traditional speech on Friday, 31 May, Japan's Minister of Finance, Shunichi Suzuki, reiterated that exchange rates should reflect fundamental indicators and that he would respond appropriately to excessive movements.

On Friday, 31 May, a block of important macroeconomic statistics on the state of the Japanese economy was released. The Consumer Price Index (CPI) in Tokyo showed that inflation rose to 2.2% y/y in May. In April, this figure was at 1.8%, matching a 26-month low. Core inflation in Tokyo also rose to 1.9% from 1.6% y/y, and the CPI excluding volatile food and energy prices increased from 1.8% to 2.2% y/y. (It should be noted that inflation in Tokyo is usually higher than the nationwide figures, which are published three weeks later. Therefore, the Tokyo CPI is a preliminary but not final indicator of inflation dynamics at the national level.)

The current rise in inflation could increase confidence in future BoJ monetary policy tightening. However, the fear of low inflation and a sharp yen appreciation deters the BoJ from raising the interest rate and narrowing the gap with other major global currencies' rates. A strong yen would harm national exporters. The decline in industrial production, which fell by -0.1% in April both month-on-month and year-on-year, does not encourage borrowing costs to rise.

The last note of the week for USD/JPY was struck at 157.25. United Overseas Bank (UOB) analysts believe that in the next 1-3 weeks, "the dollar has the potential for growth, but given the weak upward momentum, any advancement is likely to be slow. The 157.50 level might be difficult to overcome, and resistance at 158.00 is unlikely to be reached in the near future."

Speaking of the average forecast of experts, only 20% indicate a southward direction, while the remaining 80% adopt a neutral position and look east. Technical analysis tools show no such doubts or disagreements. Thus, 100% of trend indicators and oscillators on D1 point north, with 15% already in the overbought zone. It should be noted that if the green/north color of the indicators for the euro and the British pound indicates their strengthening, in the case of the yen, it conversely indicates its weakening. Therefore, traders may find it interesting to pay attention to the EUR/JPY and GBP/JPY pairs, whose dynamics have been impressive lately.

The nearest support level is in the area of 156.25-156.60, followed by zones and levels at 155.50-155.90, 153.10-153.60, 151.85-152.35, 150.80-151.00, 149.70-150.00, 148.40, 147.30-147.60, 146.50. The nearest resistance is in the 157.40 zone, followed by 157.70-158.00, 158.60, and 160.00-160.20.

No significant events or publications regarding the state of the Japanese economy are expected next week.

CRYPTOCURRENCIES: Bullish and Bearish Ethereum Prospects

For the second week, market participants' attention has been focused on the main altcoin. On 23 May, the US Securities and Exchange Commission (SEC) approved 19b-4 applications from eight issuers of spot exchange-traded funds based on Ethereum. (According to JP Morgan experts, this was dictated not by a desire to support digital assets but by a political decision aimed at supporting Joe Biden ahead of the US presidential elections.) Whatever the true reason for this regulatory move, everyone is now interested in where Ethereum prices will go.

The newborn ETH-ETFs can only start trading after the SEC approves the S-1 applications. According to Bloomberg analyst James Seyffart, this could take "weeks or months," although it is very likely to happen in mid-June. According to DeFiance Capital CEO Arthur Cheong, Ethereum's price could rise to $4,500 even before trading begins. CCData analysts believe that within 100 days of the launch of ETH-ETFs, the price could reach $5,000 per coin. This forecast is based on linear regression and the price statistics of bitcoin after the launch of spot BTC-ETFs. CCData's analysis assumes that inflows into similar Ethereum funds will be at least 50% of inflows into Bitcoin-ETFs, which means about $3.9 billion over a 100-day period.

Popular analyst Lark Davis has forecasted future growth for bitcoin to $150,000 and Ethereum to $15,000, explaining such a sharp price increase by the emerging market dynamics. The main reason for growth, Davis also cites spot BTC-ETFs, to which ETH-ETFs will now join. This will further fuel the cryptocurrency market's enthusiasm. Currently, spot BTC-ETFs hold 1,002,343 coins (≈ $68 billion), which is about 5% of the circulating supply of the flagship asset. Davis believes this impressive figure clearly indicates growing recognition of cryptocurrency and interest from institutional investors, especially from the US.

Strike CEO Jack Mallers predicts that during the ongoing bull rally, bitcoin could reach $250,000 and possibly rise in price to $1 million. On a podcast with Pomp Investments founder Anthony Pompliano, Mallers explained his bold forecast by stating that bitcoin is still at an early stage of development. According to him, the bond market is currently facing problems, so central banks may inject a significant amount of liquidity into the financial system to stabilize it. This liquidity influx will trigger an increase in the value of risky assets, including the leading cryptocurrency.

Jack Mallers disagrees with the notion that bitcoin is a bubble or a tool for speculation. The asset is becoming increasingly popular among financial giants on Wall Street, and its limited supply of 21 million coins makes BTC highly resistant to inflation, unlike fiat currencies and gold. "Bitcoin can be called the hardest form of money – thanks to the fixed issuance schedule and halvings every four years. The release rate of new coins gradually decreases, thereby increasing bitcoin's long-term value," argued the Strike CEO.

Analysts from financial investment company Motley Fool also target a six-figure number. They suggested that bitcoin's rate could rise to $400,000 and possibly even reach $1 million. The reason, which has been mentioned many times, is the influx of money from institutional investors through spot ETFs. Motley Fool analysts noted that more and more pension funds and hedge funds, managing multi-billion dollar sums, are entering the bitcoin market. Thanks to cryptocurrency ETFs, they can easily include bitcoin (and soon Ethereum) in their investment portfolios.

According to analysts, around 700 investment companies have already invested in such funds. Nevertheless, the share of institutional investors in bitcoin-ETFs is currently only about 10% of the total. Motley Fool estimates that if financial institutions invest about 5% of their assets in bitcoin, the market capitalization of the first cryptocurrency could exceed $7 trillion, which explains its forecasted rate of $400,000.

Considerably less optimism was heard in the forecast of Bloomberg senior analyst Mike McGlone. According to him, bitcoin's volatility leaves it trailing gold and the US dollar in investment appeal. Furthermore, he believes that stocks will soon crash amid the expected recession, but BTC will suffer even more than the stock market. McGlone emphasized that the Tether (USDT) stablecoin, pegged to the US dollar, typically trades twice as much per day as bitcoin. "I can access the US dollar anywhere in the world from my phone using Tether. Tether is the number one trading token. It's the number one cryptocurrency for trading. It's the dollar. The whole world has moved to the dollar. Why? Because it's the least bad of all fiat currencies," the Bloomberg expert stated.

While Mike McGlone merely downgraded bitcoin's attractiveness, Cardano founder Charles Hoskinson simply buried it. He equated bitcoin to a religion and stated that the industry has outgrown its dependence on it. According to Hoskinson, "the industry no longer needs bitcoin to survive." He pointed out critical threats to the leading cryptocurrency, including insufficient adaptability and dependence on the Proof-of-Work algorithm.

Franklin Templeton analysts, on the contrary, consider L2 protocols, along with Ordinals, Runes, and DeFi primitives, as one of the main drivers of bitcoin's innovation revival. Strike CEO Jack Mallers defended the first cryptocurrency. According to him, the Lightning Network, created for instant and cheap transactions, a second-layer solution based on the BTC blockchain, can further increase the demand for the first cryptocurrency. Mallers believes that thanks to this, bitcoin can be used for everyday purchases, such as paying for a cup of coffee. Former BitMEX CEO Arthur Hayes called the native token of the Cardano blockchain (ADA) "dog shit" due to its low use in protocols.

As of the time of writing this review on the evening of Friday, 31 May, ADA is trading at 0.45 USD per coin, while bitcoin and Ethereum are faring significantly better: BTC/USD is trading at $67,600, and ETH/USD at $3,790. The total cryptocurrency market capitalization is $2.53 trillion ($2.55 trillion a week ago). The Bitcoin Fear & Greed Index remained almost unchanged over 7 days, staying in the Greed zone at 73 points (74 a week ago).

It should be noted that ETH/USD failed to break through the $4,000 resistance this past week. The local maximum was recorded on Monday, 27 May, at $3,974. The lack of an immediate pump is explained by the fact that everyone who wanted to buy Ethereum in anticipation of the SEC's historic decision already did so. Meanwhile, according to some analysts, there is a high probability that immediately after the launch of the long-awaited spot exchange funds, Ethereum will enter a deep drawdown, similar to what happened in January with bitcoin. Then, over 12 days, it fell by 21%.

One of the key reasons for BTC's drawdown at that time was the unlocking of GBTC fund assets from Grayscale, which was converted into a spot fund from a trust. It began losing investments daily at a rate of $500 million. It is possible that something similar could happen with Ethereum, where Grayscale's ETHE fund holds $11 billion worth of ETH. As soon as this fund is converted into a spot fund and its assets are unlocked, short-term investors might start taking profits, potentially causing ETH/USD to fall to the strong support zone of $2,900-3,200.

Pessimists among bearish factors also cite the uncertain legal status of the altcoin, as the SEC has not yet clearly defined whether ETH is a commodity or a security. Additionally, the regulator has many complaints about the staking program.

Staking is a way to earn cryptocurrency by "locking" a certain amount of coins in a wallet on the Proof of Stake (PoS) algorithm to support the network. In return, the user receives rewards in the form of additional coins. According to Wall Street legend Peter Brandt, "the biggest disasters in the cryptocurrency sphere that are yet to happen will be related to staking." The expert noted that such assets as Ethereum are often rented out to earn such income, often in the form of interest, which strongly reminds him of collapsed financial pyramids. As staking becomes more widespread, Brandt warned, it could attract increased attention from central banks, treasuries, and other authorities. This could lead to tighter regulation, significantly altering the crypto space and potentially resulting in the cessation of staking and bankruptcies for those involved.

Swiss Franc Outperforms as Global Inflation Data Lack Lasting Impact on Forex

Inflation data were the key drivers in the forex markets last week, though they failed to produce any sustained movements across major currencies. Australian Dollar rallied following robust CPI figures, yet its gains were limited by the prevailing risk-off sentiment in the region.

Similarly, Euro received a modest boost after unexpected acceleration in inflation, but traders remained cautious, opting to wait for the upcoming ECB rate decision and economic projections before making significant bets. In US, PCE inflation data provided relief to stock investors, contributing to stabilization of risk sentiments that subsequently placed pressure on the Dollar.

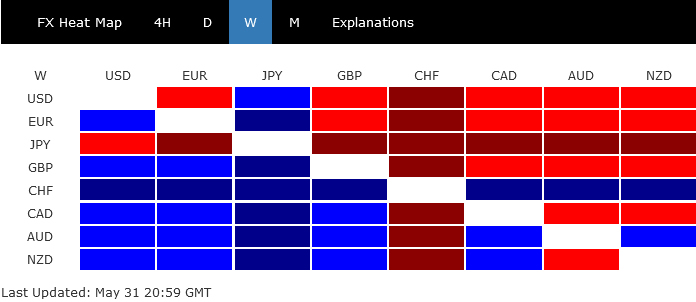

In terms of performance rankings, Swiss Franc dominated as the most impactful mover, significantly bolstered by SNB's intervention signals. Australian and New Zealand Dollars rounded out as the next strongest. Conversely, Japanese Yen was the weakest, though it stayed above its near-term support against most counterparts. Dollar and Euro trailed as the second and third weakest, respectively, while British Pound and Canadian Dollar closed the week with middling performances.

Swiss Franc Rises as SNB Fires Warning Shot on Intervention

Swiss Franc ended as the standout performer in currency markets last week, primarily driven by SNB Chair Thomas Jordan's emphatic remarks concerning the currency's weak exchange rate. Jordan's comments, which effectively served as a "warning shot" to the markets, signaled reduced tolerance for further weakness in the Franc.

Jordan, speaking at an event in Seoul, highlighted a weaker Franc remains the most likely catalyst for rising inflation in Switzerland. He suggested that SNB might intervene in the currency markets by selling foreign currencies to counteract this trend.

Additionally, robust Swiss GDP data also played a role in recalibrating market expectations of more policy easing by SNB in the near term. Probability of another rate cut in June is now perceived to be around 40%, a significant reduction from the over 65% chance seen at the beginning of May.

Despite the potential for more near-term rebound in the Franc, upside potential appears relatively limited. This is partly because SNB's primary concern is preventing excessive depreciation rather than aggressively driving up the exchange rate. Additionally, interest rate differential between SNB and other major central banks is expected to remain wide, given that persistent inflation is a global issue.

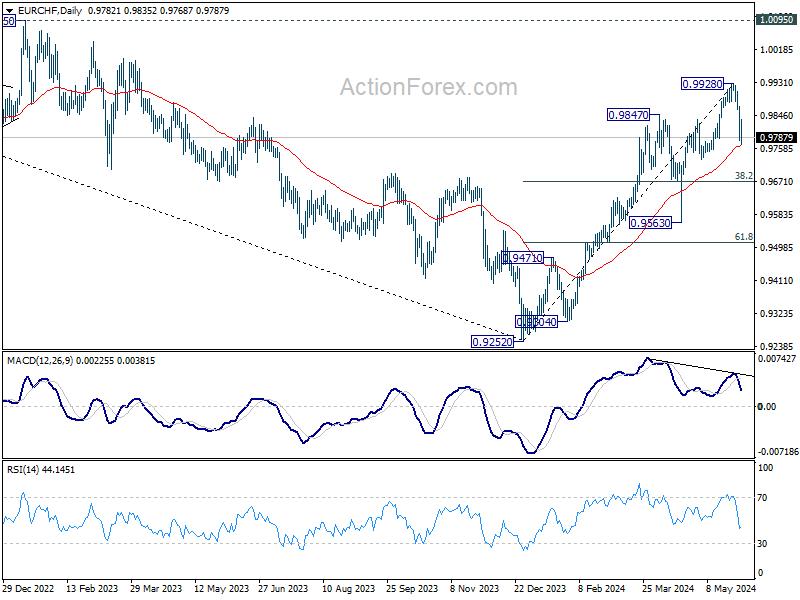

Taking a look at EUR/CHF, bearish divergence condition in D MACD argues that 0.9928 might already be a medium term top. Price actions from there are currently seen as developing into a correction to the up trend from 0.9252 only. Sustained break of 55 D EMA (now at 0.9765), will bring deeper fall to 38.2% retracement of 0.9252 to 0.9928 at 0.9670. Strong support should be seen there to bring rebound to set the range for the corrective pattern.

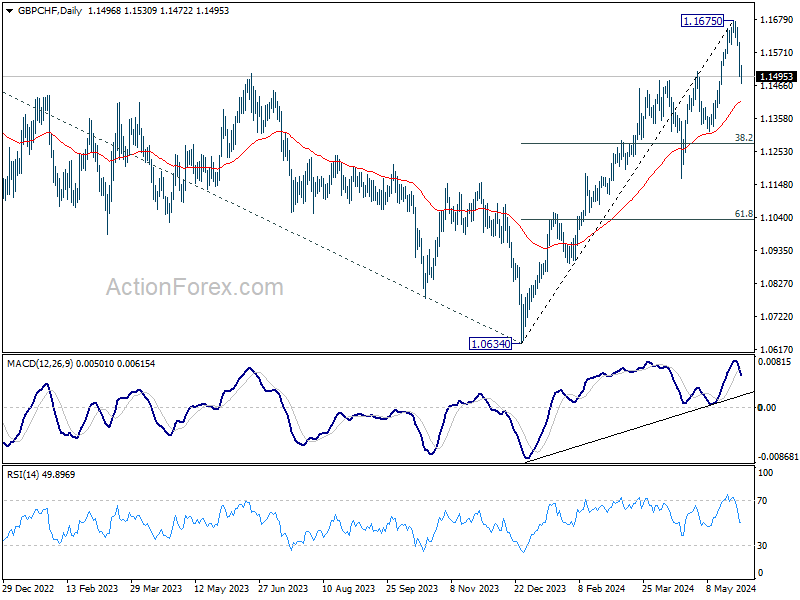

GBP/CHF has been as little stronger than EUR/CHF recently. But overall development in Franc still favors that a medium term is formed at 1.1675. Fall from there, as a correction to up trend from 1.0634, could extend to 55 D EMA (now at 1.1414) and possibly below. But strong support is expected from 38.2% retracement of 1.0634 to 1.1675 at 1.1277 to bring rebound.

Euro Struggles for Traction Despite Surging Inflation Figures

Euro had a temporary uplift following release of May's inflation data, which indicated reacceleration in both headline and core figures within the Eurozone. Despite this, the currency's momentum quickly dissipated, leaving Euro languishing at the lower end of the performance spectrum among major currencies.

ECB remains poised to lower interest rates by 25 basis points at its upcoming meeting this Thursday. This adjustment will bring deposit rate to 3.75% and main refinancing rate to 4.25%.

Initially, a significant portion of financial analysts, as polled in a recent Reuters survey, anticipated ECB would enact two additional rate cuts later this year, in September and December. However, the market's expectations have shifted post-inflation data, now forecasting a total of slightly more than 50 bps in cuts for the year, suggesting only two rate reductions.

Market participants appear to be adopting a cautious stance, opting to withhold larger bets until ECB releases its new economic projections alongside the rate decision. This forthcoming information will likely play a critical role in shaping future market movements and monetary policy expectations.

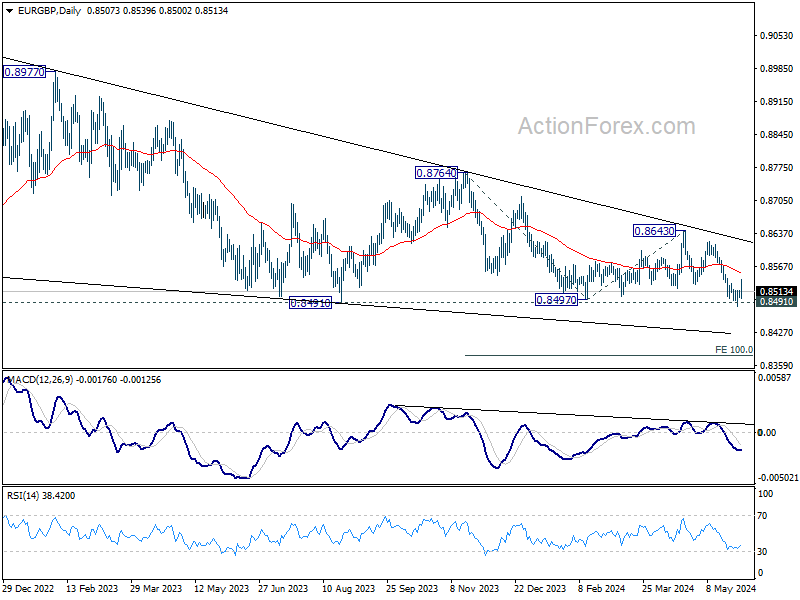

EUR/GBP recovered after breaching 0.8491 key support briefly, but upside is so far limited. Further decline will remain in favor as long as 55 D EMA (now at 0.8553) holds. Decisive break of 0.8491/7 will resume larger down trend to 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

Aussie Climbs Modestly Amid Uncertainty Over RBA's Next Steps

Australian Dollar stood out as one of the stronger performers last week, buoyed by unexpected acceleration in headline inflation. Notably, RBA's favored metric, trimmed mean inflation, which excludes volatile items such as petrol, also showed an uptick. However, its gains were tempered by a prevailing risk-off mood, particularly noticeable within the region.

In its recent meeting minutes, RBA disclosed that a rate hike was on the table in May, though it ultimately decided to maintain rates. Currently, Warren Hogan, Chief Economic Advisor at Judo Bank, stands alone in anticipating a rate hike in June, asserting it as the "only option" in light of the government's inaction on price control. Additionally, there is a prevailing sentiment that RBA could be just "one bad inflation report" away from deciding to increase rates.

Contrarily, major banks continue to forecast a rate cut as the next move, with Westpac expecting a "forward-looking" RBA to initiate cuts in November. Market traders, on the other hand, have significantly dialed back their expectations for a rate cut, now foreseeing a possible easing only by December 2025—a delay from the previously anticipated cut in May next year.

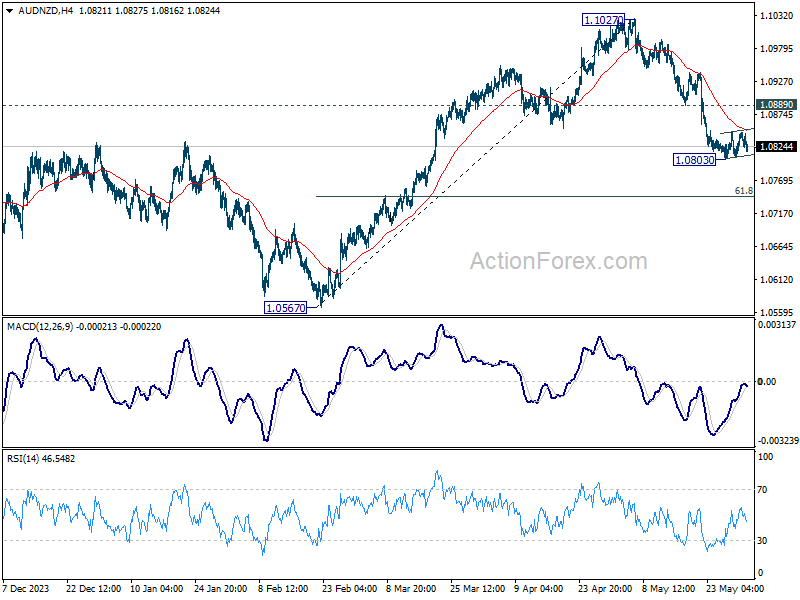

Even against Kiwi, Aussie's recovery was lackluster. With 55 4H EMA intact, fall from 1.1027 is expected to resume sooner rather than later. Break of 1.0803 will target 61.8% retracement of 1.0567 to 1.1027 at 1.0743 and below.

Steady US Inflation Data Calms Markets

In the US, April's PCE data, which indicated that both headline and core inflation rates remained unchanged from previous months, has provided a sense of relief to investors. This stability alleviates concerns about re-acceleration of inflation that might trigger further tightening by Fed. Currently, investors are accepting a balanced 50/50 probability that Fed will begin cutting interest rates in September. Any data supporting this move in the coming weeks could bolster risk sentiment weigh on the greenback.

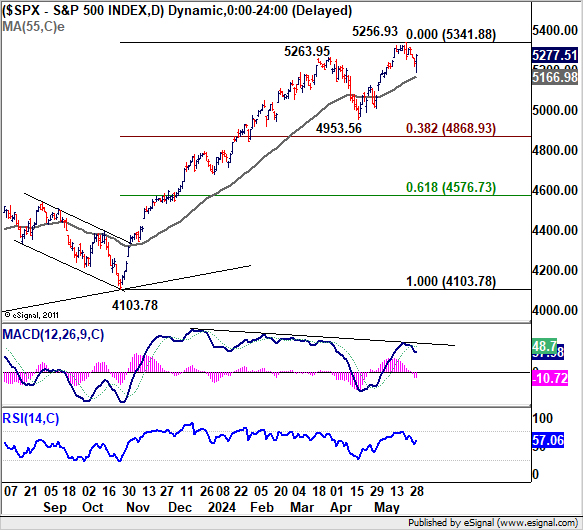

In the stock markets, while DOW's correction was steep, S&P 500 and NASDAQ have been resilient. For now, S&P 500's pull back from 5256.93 looks more likely a near term correction than not. Another rally through 5256.93 to resume the larger up trend is still in favor.

However, sustained break of 55 D EMA (now at 5166.98) will indicate that it's already correcting the whole rise from 4103.78. Deeper fall would then be seen back towards 4953.56, and possibly below.

Dollar index struggled in tight range around flat 55 D EMA last week. On the downside, firm break of 104.08 will resume the fall from 106.51. More importantly, that would argue that whole rebound from 100.61 has completed with three waves up to 106.51. In this case, deeper fall would be seen to 102.35 and possibly below..

Nevertheless, strong bounce from current level will retain near term bullishness. Break of 105.74 resistance will argue that rise from 100.61 is ready to resume through 106.51 to 107.34 resistance.

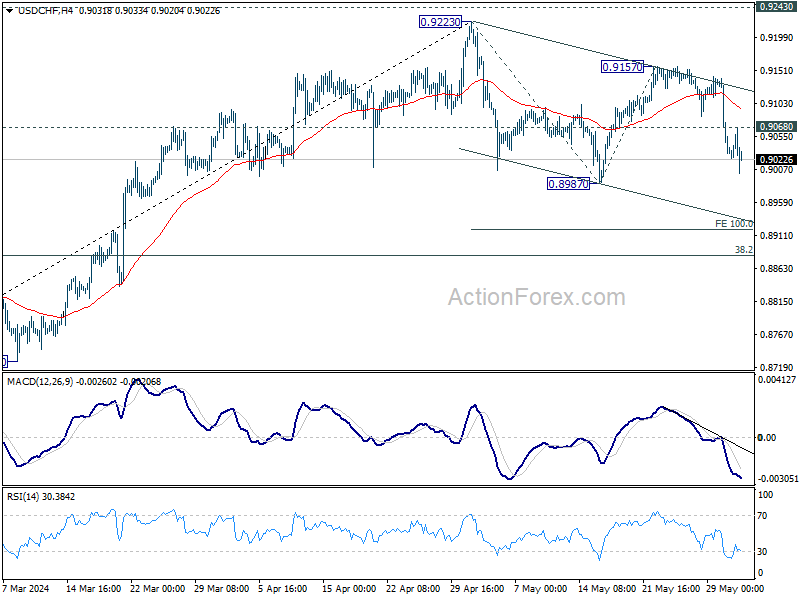

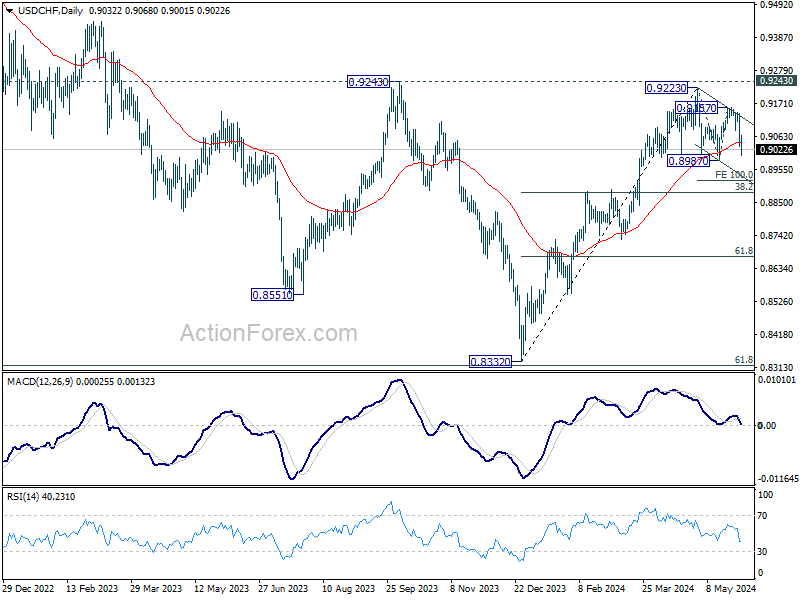

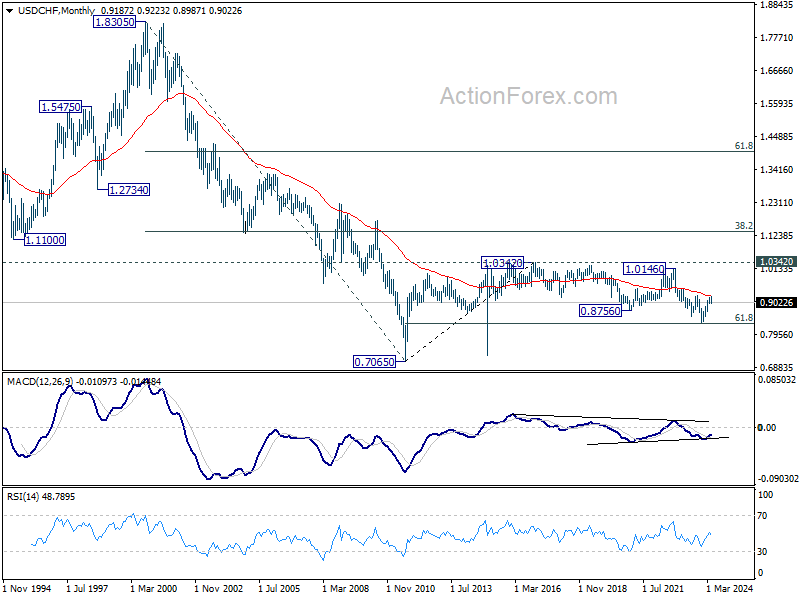

USD/CHF Weekly Outlook

USD/CHF's steep decline last week suggests that rebound from 0.8987 has completed at 0.9157. Initial bias stays on the downside this week for 0.8987. Firm break there will resume the fall from 0.9223 to 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.9065 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

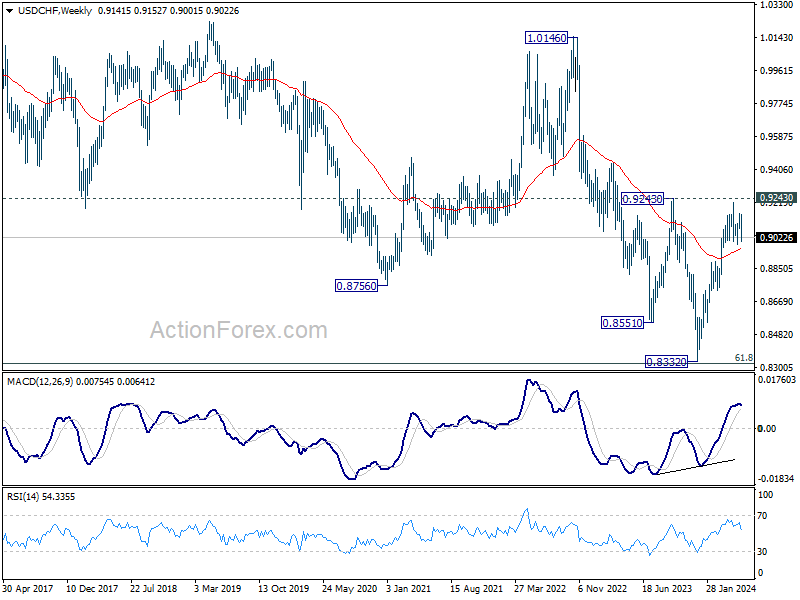

In the long term picture, price action from 0.7065 (2011 high) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Strong rebound from 61.8% retracement of 0.7065 to 1.0342 (2016 high) will start the third leg as a medium term rally. But there will be no sign of long term reversal until firm break of 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

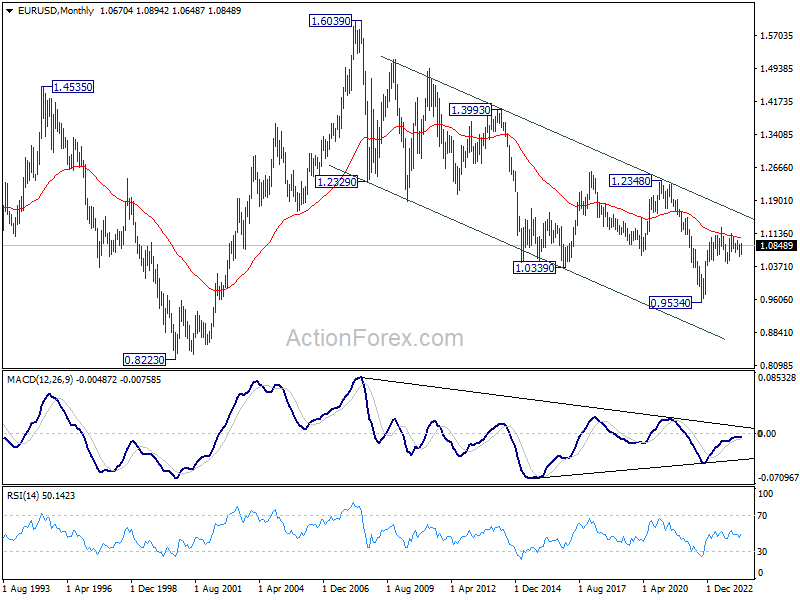

EUR/USD Weekly Outlook

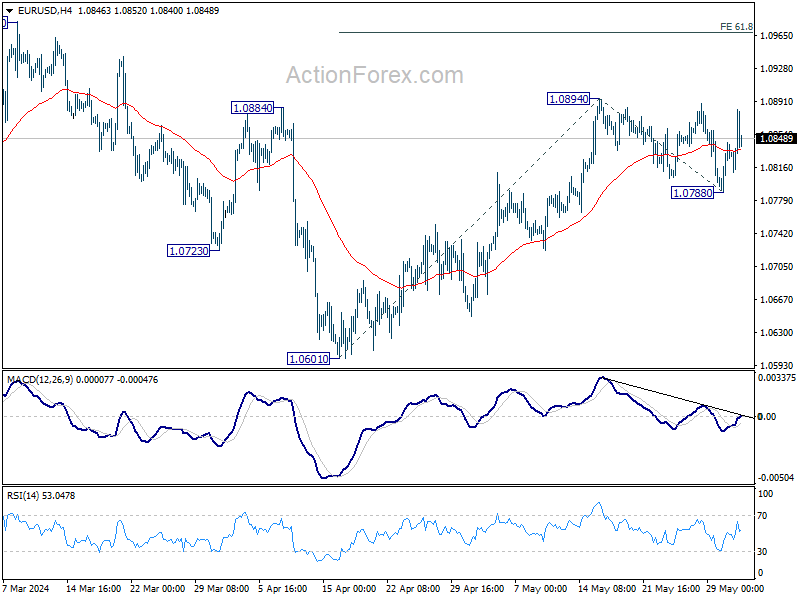

EUR/USD dipped to 1.0788 last week but quickly recovered. Initial bias remains neutral this week first. On the upside, firm break of 1.0894 will resume whole rally from 1.0601, and target 61.8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. For now, risk will stay on the upside as long as 1.0788 support holds, in case of retreat.

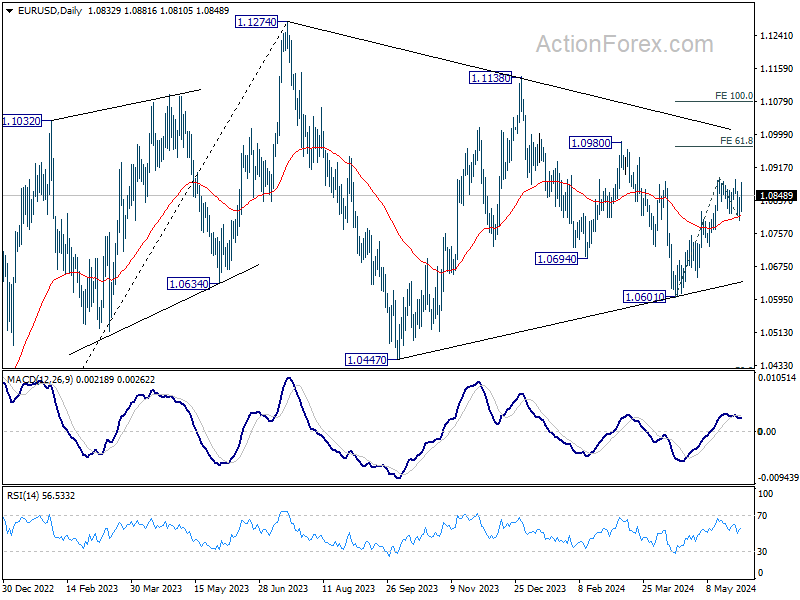

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

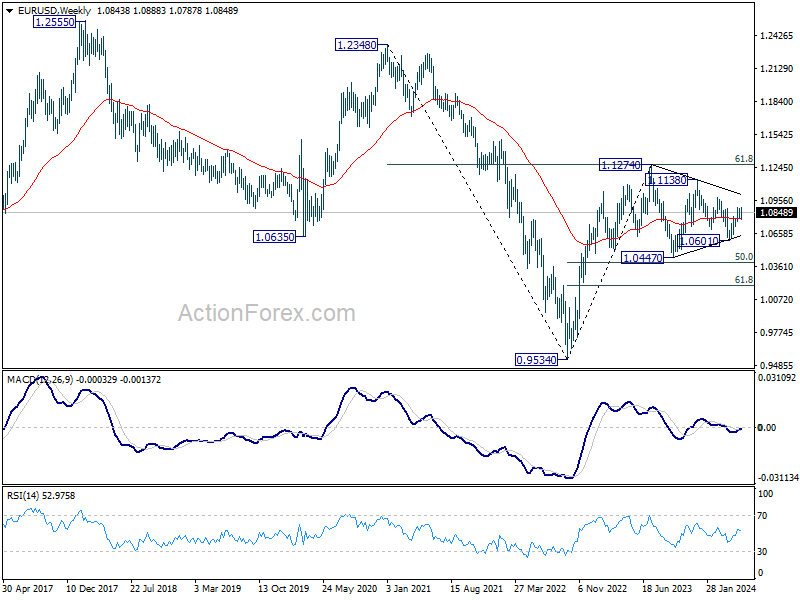

In the long term picture, a long term bottom is in place at 0.9534 on bullish convergence condition in M MACD. It's still early to call for bullish trend reversal with the pair staying inside falling channel in the monthly chart. Nevertheless, sustained trading above 55 M EMA (now at 1.1030) and break of 1.1274 resistance will raise the chance of reversal and target 1.2348 resistance for confirmation.

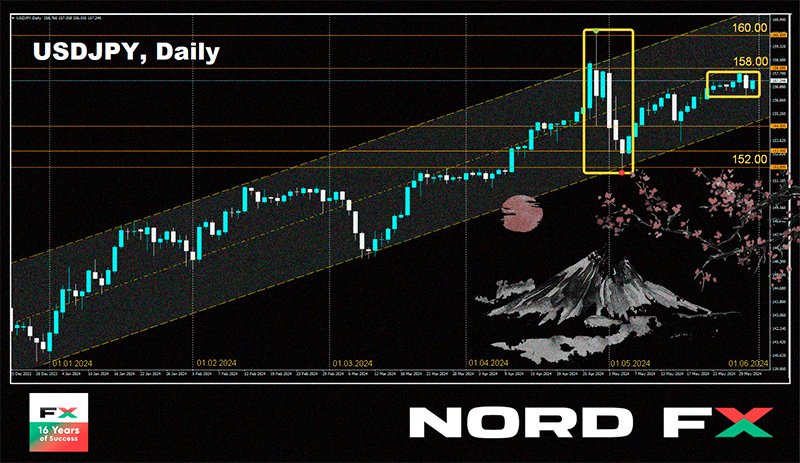

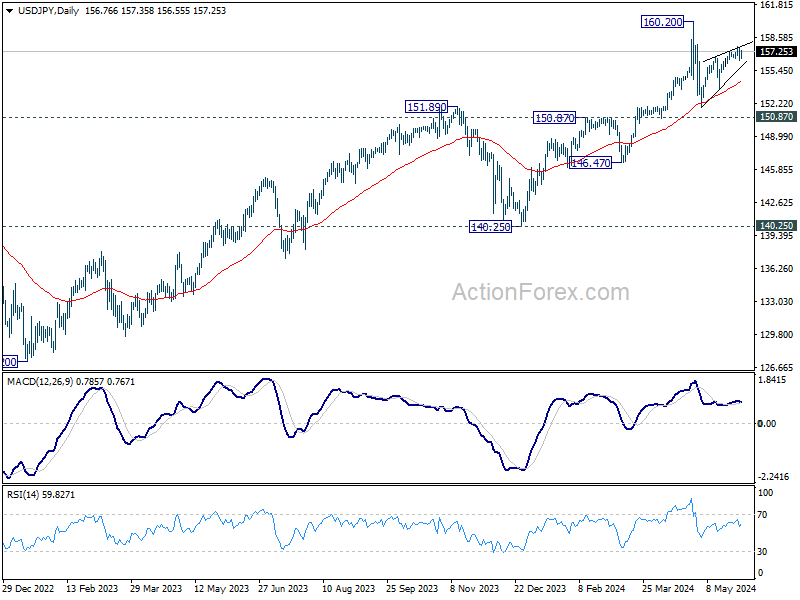

USD/JPY Weekly Outlook

USD/JPY turned sideway after edging higher to 157.70 last week. Initial bias remains neutral this week first. Decisive break of 156.36 will confirm short term topping at 157.70, on bearish divergence condition in 4 H MACD. Intraday bias will be back on the downside for 153.59 support. Firm break there will target 151.86 and below as the third leg of the corrective pattern from 160.20.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

In the long term picture, as long as 140.25 support holds, up trend from 75.56 (2011 low) is still in progress. Next target is 138.2% projection of 75.56 (2011 low) to 125.85 (2015 high) from 102.58 at 172.08.

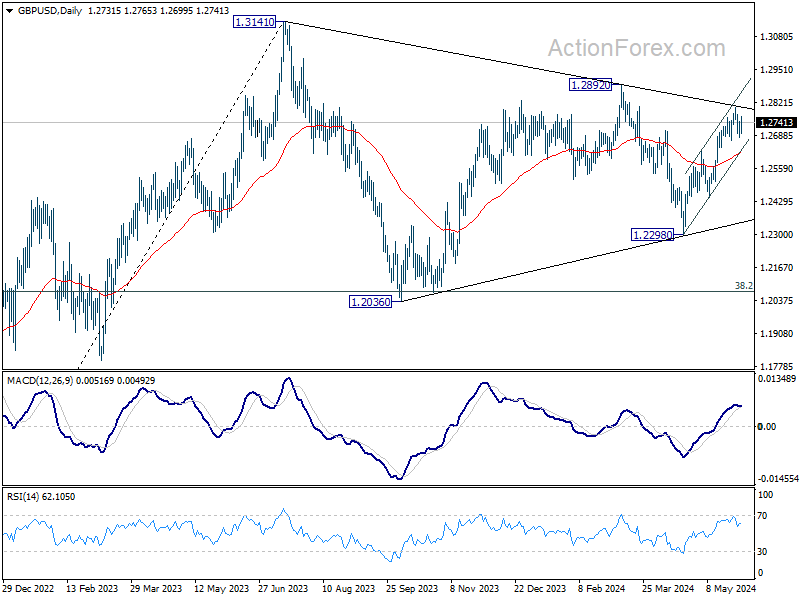

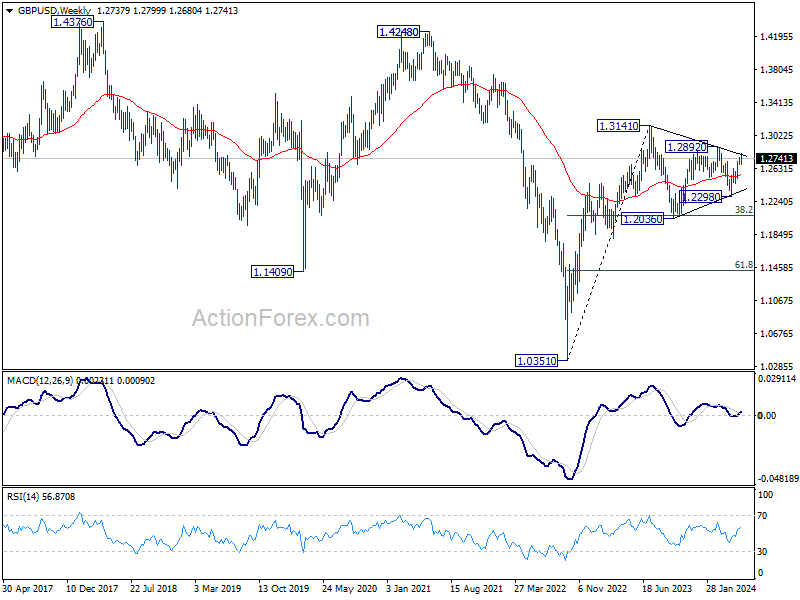

GBP/USD Weekly Outlook

GBP/USD edged higher to 1.2799 last week but turned sideway since then. Initial bias stays neutral this week and more range trading could be seen. Further rise is expected as long as 1.2670 support holds. Above 1.2799 will resume the rally from 1.2298 and target 1.2892 resistance. However, break of 1.2670 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

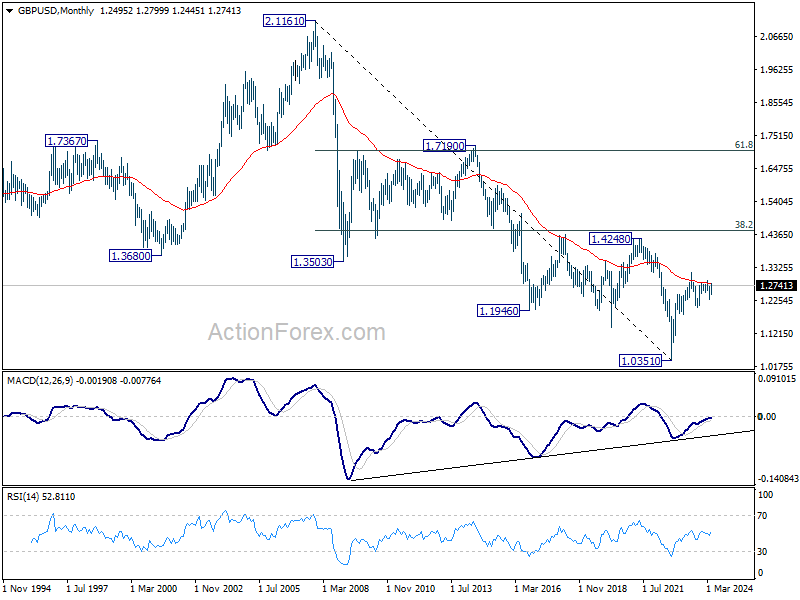

In the long term picture, a long term bottom should be in place at 1.0351 on bullish convergence condition in M MACD. But momentum of the rebound from 1.3051 argues GBP/USD is merely in consolidation, rather than trend reversal. Range trading is likely between 1.0351/4248 for some more time.

USD/CHF Weekly Outlook

USD/CHF's steep decline last week suggests that rebound from 0.8987 has completed at 0.9157. Initial bias stays on the downside this week for 0.8987. Firm break there will resume the fall from 0.9223 to 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.9065 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

In the long term picture, price action from 0.7065 (2011 high) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Strong rebound from 61.8% retracement of 0.7065 to 1.0342 (2016 high) will start the third leg as a medium term rally. But there will be no sign of long term reversal until firm break of 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

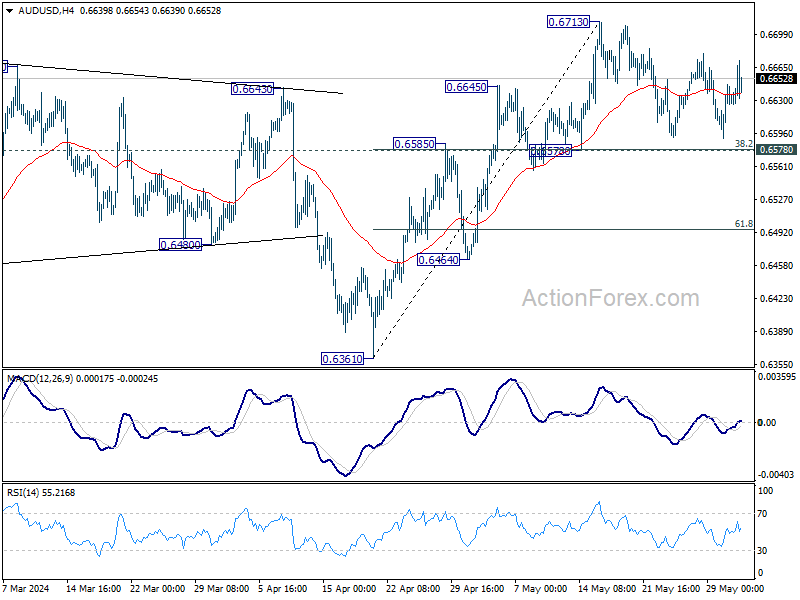

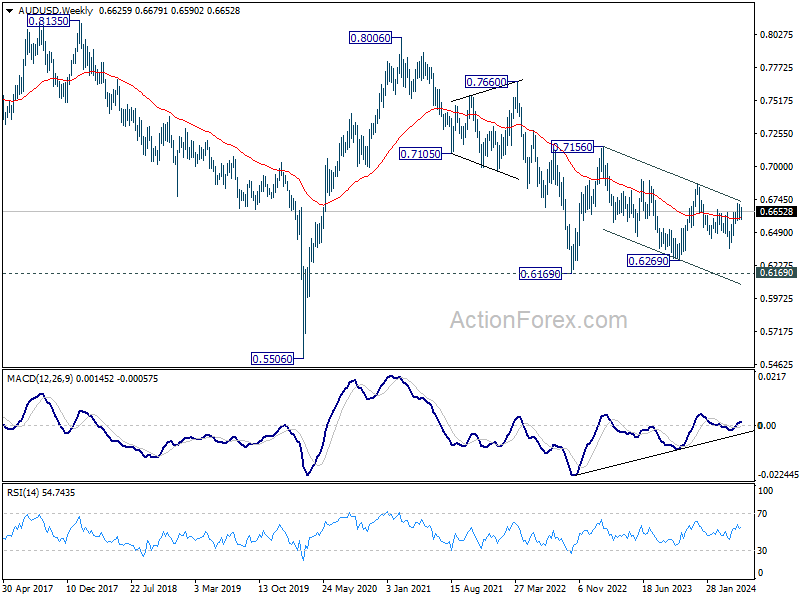

AUD/USD Weekly Report

AUD/USD stayed in sideway trading below 0.6713 last week and outlook is unchanged. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

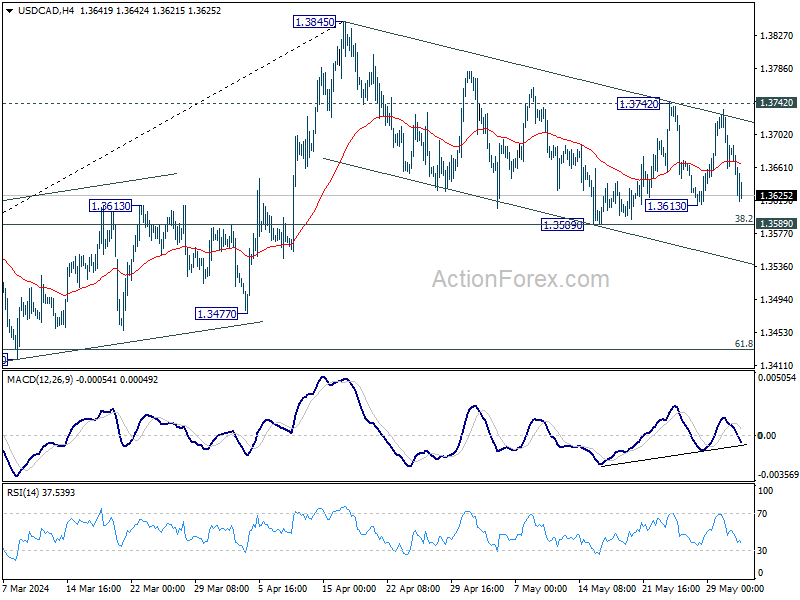

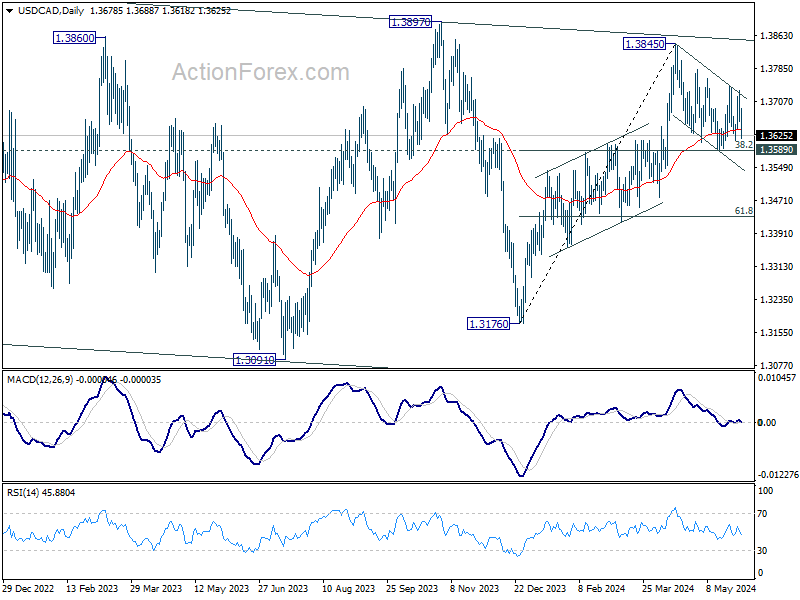

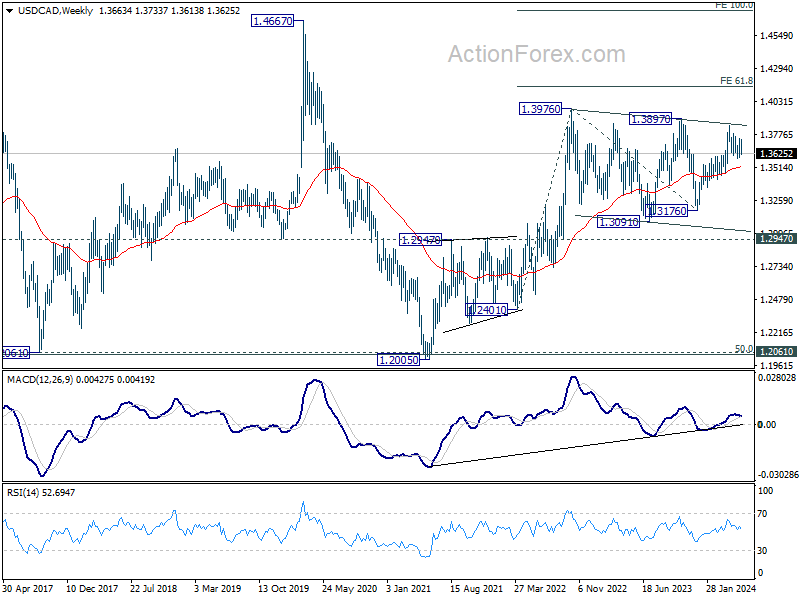

USD/CAD Weekly Outlook

USD/CAD gyrated in range of 1.3589/3742 last week and outlook is unchanged. Initial bias remains neutral this week. On the upside, break of 1.3742 resistance will revive the case that correction from 1.3845 has completed at 1.3589. Intraday bias will be back on the upside for retesting 1.3845. On the downside, firm break of 1.3589 support will argue that whole rise from 1.3176 has completed at 1.3845 already. Fall from 1.3845 should then resume to 61.8% retracement of 1.3176 to 1.3845 at 1.3432.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

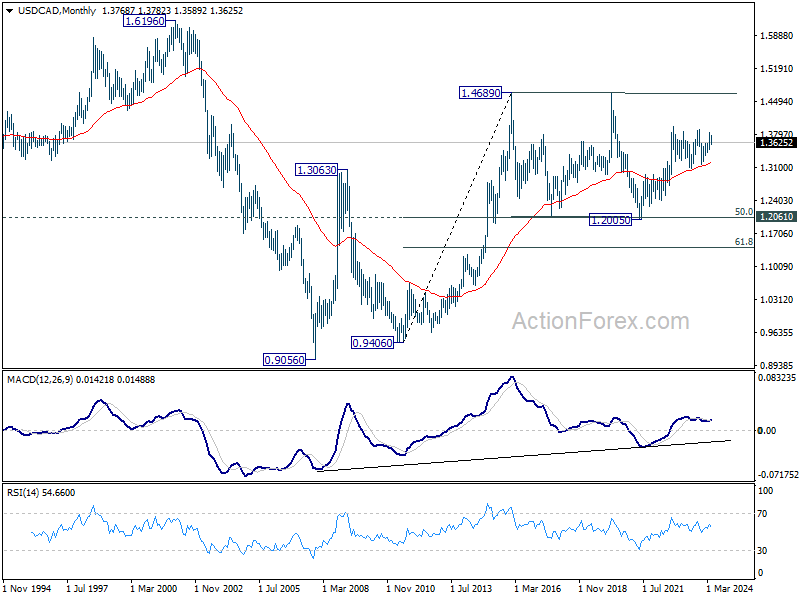

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

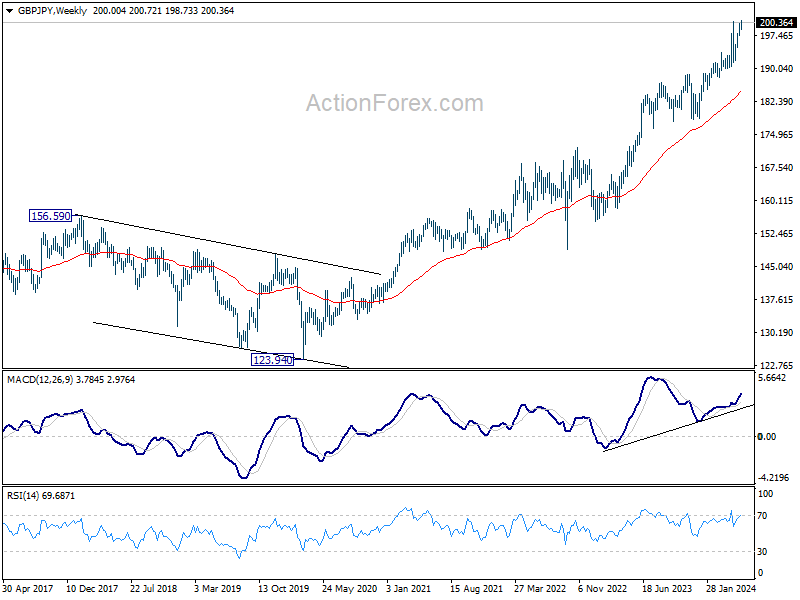

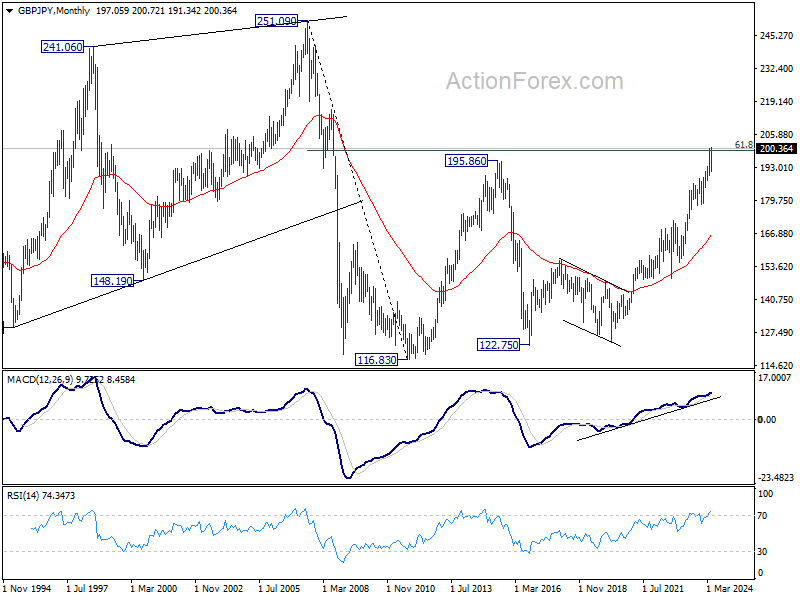

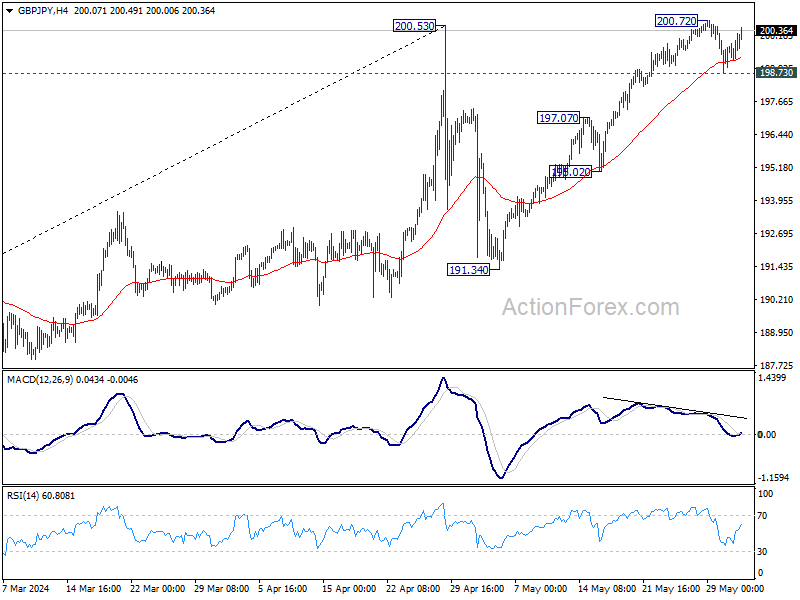

GBP/JPY Weekly Outlook

GBP/JPY dipped to 198.73 last week after edging higher to 200.72. But it quickly recovered. Initial bias is neutral this week first. On the upside, decisive break of 200.53/72 will confirm larger up trend resumption. On the downside, below 198.73 will turn bias to the downside for 197.07 resistance turned support instead.

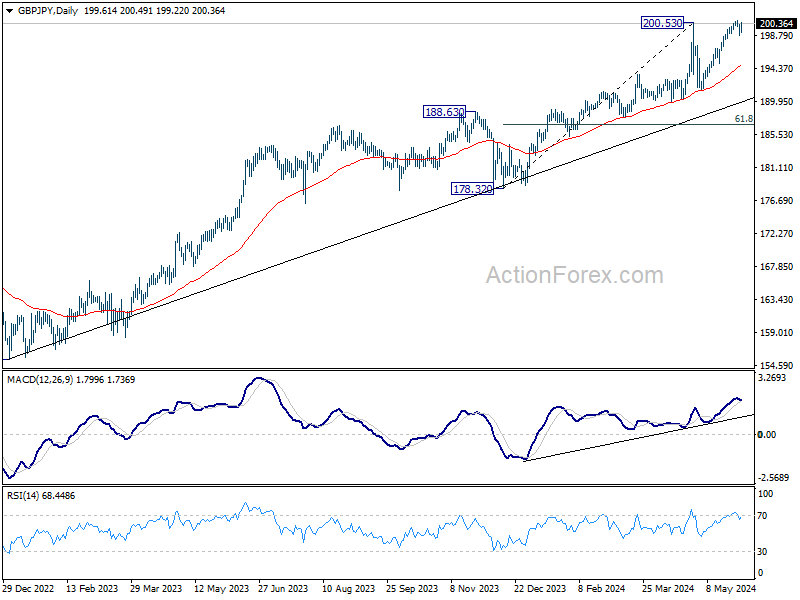

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 185.06) holds, price actions from there is seen as correcting the rise from 178.32 only. That is, larger up trend is expected to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Focus is now on 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80. Decisive break there would pave the way back to 251.09 in the long term.