Sample Category Title

Sentiment Stabilizes after FOMC, Yen Jumps Again on Alleged Strategic Intervention

Markets sentiment in the US stabilized overnight, responding positively to Fed Chair Jerome Powell's less hawkish-than-anticipated remarks in the post-FOMC press conference. DOW closed slightly up, while S&P 500 and NASDAQ saw mild losses only. Treasury yields and Dollar both fell in response to these developments. Key takeaways from Powell's address include a clear stance against further policy tightening, soothing market fears of another rate hike. The focus remains firmly set on the timing and pace of rate cuts, which would be heavily dependent on incoming economic data.

Japanese Yen surged dramatically again, purportedly due to intervention by Japanese authorities. This move was strategically timed to capitalize on Dollar's weakness post-FOMC, during a period of low liquidity. Japan's chief currency diplomat, Masato Kanda, remained tight-lipped about the intervention, stating that details would be released at the end of the month. While this intervention has not reversed Yen's downtrend, it seems to be setting the stage for prolonged range trading, with 160 against Dollar acting as a strong psychological floor.

Overall in the forex markets, Canadian Dollar is currently the week's weakest performer, followed by New Zealand Dollar and Swiss Franc. In contrast, Yen leads as the strongest, followed by Sterling and the Euro. Dollar is mixed, caught between post-FOMC sell-off pressures and market readjustments, while Australian Dollar has shown recovery, buoyed by the broader risk sentiment improvement.

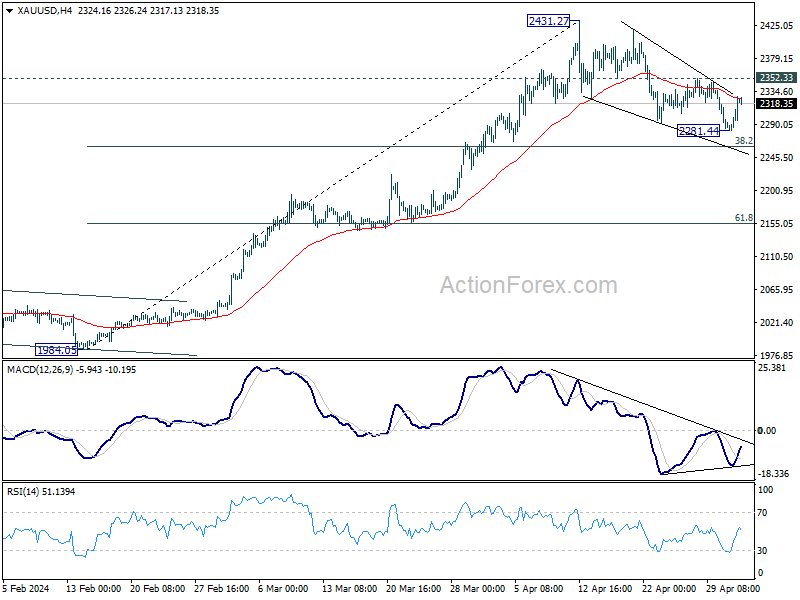

Technically, Gold's corrective fall from 2431.27 extended to 2281.44 but quickly recovered. It's possible that this correction has completed as a five-wave descending triangle pattern. Also, considering bullish convergence condition in 4H MACD, break of 2352.33 resistance will strengthen this case, and bring stronger rally through 2431.27 high to resume the larger up trend.

In Asia, at the time of writing, Nikkei is down -0.09%. Hong Kong HSI is up 2.21%. China is on holiday. Singapore Strait Times is up 0.27%. Japan 10-year JGB yield is down -0.0003 at 0.896. Overnight, DOW rose 0.23%. S&P 500 fell -0.34%. NASDAQ fell -0.33%. 10-year yield fell -0.091 to 4.595.

10-year yield dips as Fed Powell rules out rate hike

US markets expressed a sign of relief overnight followed as Fed Chair Jerome Powell's less hawkish than feared stance at the post-FOMC press conference. Major stock indexes closed mixed while treasury yields dipped with Dollar.

Most importantly, Powell characterized the current interest rate level as "sufficiently restrictive," and indicated that it is "unlikely that the next rate move will be a hike." Instead, Powell delineated the future monetary policy path as a decision between "cutting" and "not cutting" interest rates, depending on economic data.

This stance comes in the wake of stronger-than-expected inflation data since the beginning of the year, leading Powell to acknowledge that it would "take longer than previously expected" for Fed to be confident that inflation is on a steady decline toward the 2% target. policymakers to become comfortable that inflation will resume the decline towards 2%."

"If we did have a path where inflation proves more persistent than expected, and where the labor market remains strong but inflation is moving sideways and we're not gaining greater confidence, well, that would be a case in which it could be appropriate to hold off on rate cuts," Powell said. "There are paths to not cutting and there are paths to cutting. It's really going to depend on the data."

More on FOMC:

- First Cut by Fed is September at the Earliest

- May FOMC: Stalling in Inflation Leaves FOMC Stalling for Time

10-year yield closed down -0.0910 at 4.595 in reaction to FOMC. Technically, another rise could still be seen as long as 4.568 support holds. But even in this case, TNX should continue to lose upside momentum ahead of 4.997 high. Meanwhile, break of 4.568 will indicate that it's at least in a near term pullback towards 55 D EMA (now at 4.408.

BoC nears interest rate cuts as inflation eases, says Macklem

BoC Governor Tiff Macklem, at a Senate committee testimony, indicated that Canada is edging closer to conditions that would allow for easing monetary policy. "The short answer is we are getting closer," he affirmed.

Inflation in Canada has moderated effectively, remaining under 3% since January and aligning with the central bank's forecasts. This stabilization is expected to persist through the first half of 2024, with key core measures of consumer prices showing a consistent downward trend.

"We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained," Macklem explained.

Furthermore, Macklem addressed the impact of fiscal policy on the economic outlook, noting that recent governmental fiscal plans are unlikely to significantly alter the Bank's projections for the economy or inflation.

Looking ahead

Swiss CPI, retail sales, and PMI manufacturing will be released in European session. Eurozone will release PMI manufacturing final. Later in the day, US will release trade balance, jobless claims, non-farm productivity, and factor orders. Canada will also publish trade balance.

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.27; (P) 155.13; (R1) 157.26; More...

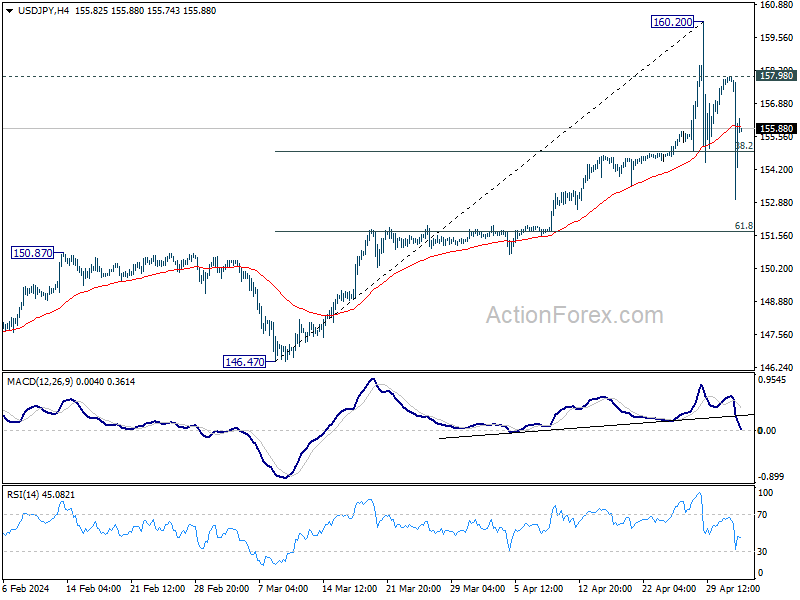

USD/JPY's correction from 160.20 short term top extended with another dip to 152.99, but quickly recovered again. For now, risk will be mildly on the downside as long as 157.98 resistance holds. Deeper pullback would be seen to 55 D EMA (now at 152.25), and possibly further to 61.8% retracement of 146.47 to 160.20 at 151.71. But strong support should be seen from 150.87 to bring rebound.

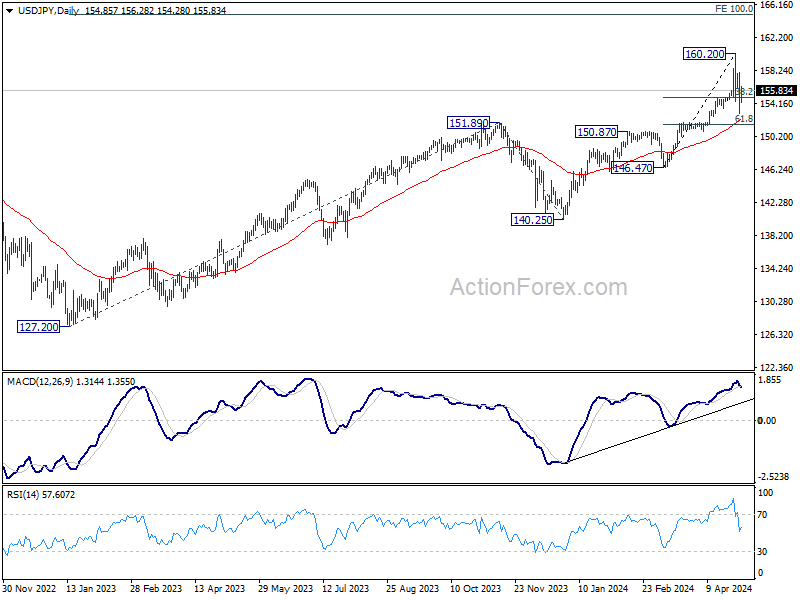

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | -0.20% | 14.90% | 15.90% | |

| 23:50 | JPY | Monetary Base Y/Y Apr | 2.10% | 1.70% | 1.60% | |

| 23:50 | JPY | BoJ Meeting Minutes | ||||

| 01:30 | AUD | Building Permits M/M Mar | 1.90% | 3.20% | -1.90% | -0.90% |

| 01:30 | AUD | Trade Balance (AUD) Apr | 5.02B | 7.37B | 7.28B | 6.59B |

| 05:00 | JPY | Consumer Confidence Apr | 38.3 | 39.5 | 39.5 | |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | 0.20% | -0.20% | ||

| 06:30 | CHF | CPI M/M Apr | 0.20% | 0.00% | ||

| 06:30 | CHF | CPI Y/Y Apr | 1% | |||

| 07:30 | CHF | Manufacturing PMI Apr | 45.8 | 45.2 | ||

| 07:45 | EUR | Italy Manufacturing PMI Apr | 49.8 | 50.4 | ||

| 07:50 | EUR | France Manufacturing PMI Apr F | 44.9 | 44.9 | ||

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 42.2 | 42.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.6 | 45.6 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 0.70% | |||

| 12:30 | CAD | Trade Balance (CAD) Mar | 1.0B | 1.4B | ||

| 12:30 | USD | Trade Balance (USD) Mar | -69.3B | -68.9B | ||

| 12:30 | USD | Initial Jobless Claims (Apr 26) | 212K | 207K | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.80% | 3.20% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | 3.20% | 0.40% | ||

| 14:00 | USD | Factory Orders M/M Mar | 1.60% | 1.40% | ||

| 14:30 | USD | Natural Gas Storage | 68B | 92B |

Elliott Wave Analysis: 7 Swing Correction in Gold (XAUUSD)

Short Term Elliott Wave View on Gold (XAUUSD) suggests that rally from 11.13.2023 low is unfolding as a 5 waves impulse. Up from 11.13.2023 low, wave 1 ended at 2146.79 and dips in wave 2 ended at 1973.13. The metal extended higher in wave 3 towards 2431.78. Pullback in wave 4 is unfolding in a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 2323.86 and wave (b) ended at 2417.89.

Wave (c) lower ended at 2291.26 which completed wave ((w)) in higher degree. The metal then bounced in wave ((x)) with internal subdivision as a zigzag. Up from wave ((w)), wave (a) ended at 2337.31 and wave (b) ended at 2304.90. Wave (c) higher ended at 2352.76 which completed wave ((x)) in higher degree. The metal has turned lower in wave ((y)) with internal subdivision as a zigzag. Down from wave ((x)), wave (a) ended at 2281.3 and wave (b) ended at 2328.29. Near term, as far as pivot at 2352.76 high stays intact, expect the metal to extend lower. Potential target lower is 100% – 161.8% Fibonacci extension of wave ((w)). This area comes at 2124.1 – 2211 where buyers can appear.

Gold (XAUUSD) 60 Minutes Elliott Wave Chart

XAUUSD Elliott Wave Video

https://www.youtube.com/watch?v=2z3DY_oHHg4

BoC nears interest rate cuts as inflation eases, says Macklem

BoC Governor Tiff Macklem, at a Senate committee testimony, indicated that Canada is edging closer to conditions that would allow for easing monetary policy. "The short answer is we are getting closer," he affirmed.

Inflation in Canada has moderated effectively, remaining under 3% since January and aligning with the central bank's forecasts. This stabilization is expected to persist through the first half of 2024, with key core measures of consumer prices showing a consistent downward trend.

"We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained," Macklem explained.

Furthermore, Macklem addressed the impact of fiscal policy on the economic outlook, noting that recent governmental fiscal plans are unlikely to significantly alter the Bank's projections for the economy or inflation.

Gold Price Could Restart Increase Above This Resistance

Key Highlights

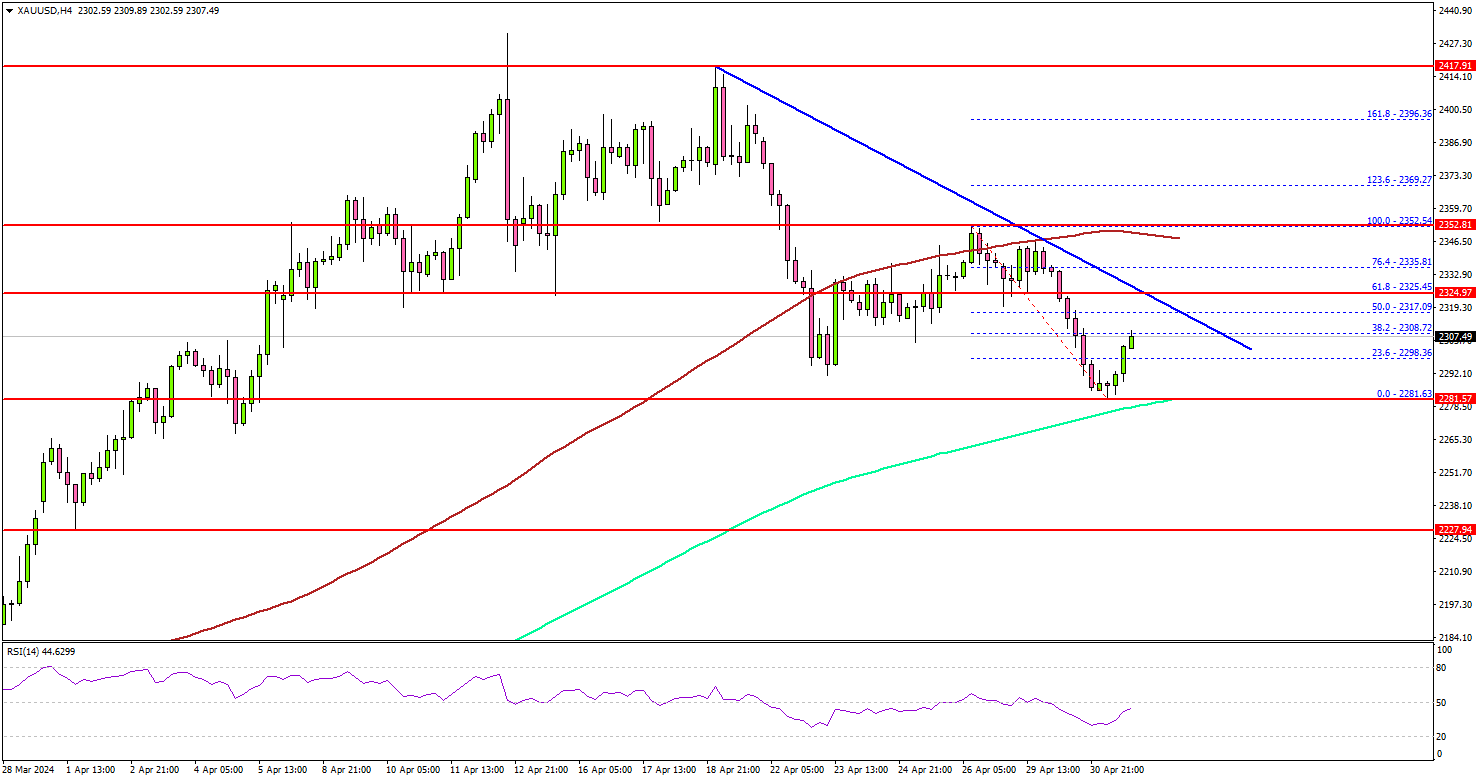

- Gold started a downside correction and traded below $2,350.

- A connecting bearish trend line is forming with resistance at $2,325 on the 4-hour chart.

- Oil prices extended losses but remained stable above $80.00.

- Bitcoin price traded to a new weekly low below $60,000.

Gold Price Technical Analysis

Gold prices started a downside correction from the $2,431 high against the US Dollar. It traded below the $2,400 and $2,365 support levels.

The 4-hour chart of XAU/USD indicates that the price even broke the $2,325 support and settled below the 100 Simple Moving Average (red, 4 hours). However, the bulls are now active above the $2,280 support and the 200 Simple Moving Average (green, 4 hours).

The price is now consolidating losses, with an immediate resistance at $2,318. The first major resistance is now forming near connecting bearish trend line at $2,325.

The main resistance is now forming near $2,350 and the 100 Simple Moving Average (red, 4 hours), above which the price could accelerate higher toward $2,395.

On the downside, the 200 Simple Moving Average (green, 4 hours) is the key at $2,280. A downside break below the $2,280 support might call for more downsides. The next major support is near the $2,250 level. Any more losses might send Gold prices toward $2,220.

Looking at Bitcoin, there was a strong decline, and the bears were able to push the price below the $60,000 and $58,500 support levels.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for March 2024 - Forecast 42.2, versus 42.2 previous.

- Euro Zone Manufacturing PMI March 2024 – Forecast 45.6, versus 45.6 previous.

- US Initial Jobless Claims - Forecast 212K, versus 207K previous.

10-year yield dips as Fed Powell rules out rate hike

US markets expressed a sign of relief overnight followed as Fed Chair Jerome Powell's less hawkish than feared stance at the post-FOMC press conference. Major stock indexes closed mixed while treasury yields dipped with Dollar.

Most importantly, Powell characterized the current interest rate level as "sufficiently restrictive," and indicated that it is "unlikely that the next rate move will be a hike." Instead, Powell delineated the future monetary policy path as a decision between "cutting" and "not cutting" interest rates, depending on economic data.

This stance comes in the wake of stronger-than-expected inflation data since the beginning of the year, leading Powell to acknowledge that it would "take longer than previously expected" for Fed to be confident that inflation is on a steady decline toward the 2% target. policymakers to become comfortable that inflation will resume the decline towards 2%."

"If we did have a path where inflation proves more persistent than expected, and where the labor market remains strong but inflation is moving sideways and we're not gaining greater confidence, well, that would be a case in which it could be appropriate to hold off on rate cuts," Powell said. "There are paths to not cutting and there are paths to cutting. It's really going to depend on the data."

More on FOMC:

- First Cut by Fed is September at the Earliest

- May FOMC: Stalling in Inflation Leaves FOMC Stalling for Time

10-year yield closed down -0.0910 at 4.595 in reaction to FOMC. Technically, another rise could still be seen as long as 4.568 support holds. But even in this case, TNX should continue to lose upside momentum ahead of 4.997 high. Meanwhile, break of 4.568 will indicate that it's at least in a near term pullback towards 55 D EMA (now at 4.408).

First Cut by Fed is September at the Earliest

Current and expected risks warrant the FOMC holding off on the first cut until September and then carefully assessing lingering inflation risks as each subsequent step is taken. A low of 3.375% is expected for fed funds mid-2026, a modestly contractionary rate.

Following a run of data pointing to inflation being more persistent, the updated views of Chair Powell and the FOMC were eagerly awaited. In the event, the tone of their guidance was balanced, with the FOMC again emphasising they will decide meeting by meeting on the appropriate timing of rate cuts. Very clear in Chair Powell’s remarks though is that they need to see a number of months of good progress on inflation before considering a cut. Given recent momentum, the additional three months of data to come ahead of the July meeting are unlikely to be enough. We now see September as the most probable timing for the first cut, followed by one cut per quarter until June 2026, when we see the fed funds rate troughing at a modestly contractionary 3.375%.

The FOMC is not ignoring the recent momentum in inflation. In the statement, the Committee noted in “recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective” and that they do “not expect it will be appropriate to reduce the target range until [they have] gained greater confidence that inflation is moving sustainably toward 2 percent”. However, Chair Powell made clear in the press conference that they still expect inflation will move down over the year. The current stance of policy is deemed “sufficiently restrictive” and the labour market coming into balance. From this guidance and other comments in the press conference, it is evident the Committee is focused on when to cut, not whether.

In gauging the most likely timing of a first cut and the pace thereafter, the persistence of activity and labour market momentum will prove key. Our baseline view is that momentum holds up around trend for activity and above zero for job growth. Wages growth will remain solid with risks skewed upwards. Recall also that most US borrowers are insulated from rate hikes and household wealth is still rising. If our baseline view on the economy plays out, the FOMC are likely to take their time easing policy. The persistence of this economic resilience, and so pricing pressure, also favours our baseline view of a one cut per quarter profile over two years.

Conversely, if the labour market suddenly deteriorates, with employment contracting and the unemployment rate rising materially above 4.0%, then expectations for wages and demand will sour. This would justify an earlier and potentially more rapid policy easing. While this should be seen only as a risk scenario, it cannot be ruled out completely. Business surveys such as the ISMs have, on average, been pointing to net job losses for the past six months.

Jumping ahead and considering our forecast end point for this cycle of 3.375%, two points are worthy of note. First, we do expect FOMC policy to be effective in bringing inflation back around target and so see a material easing over the period, a cumulative 200bps. But second, Westpac continues to see need for restrictive policy into the medium-term, with 3.375% materially above the FOMC’s longer run end point of 2.6%. We expect modestly restrictive policy will be needed into the medium-term because supply-side inflationary pressures evident across the economy, most notably in rents and house construction costs, are likely to persist. Further, with the continuing support to demand from highly expansionary fiscal policy, regardless of which party wins, investment is also likely to be sustained across the economy and with it demand for resources and financial capital.

The latter point is important for both Treasury yields and the US dollar. Over the course of the next two years, we forecast the US 10-year yield will retreat to around 4.0% as inflation declines. But that level is expected, on average, to prove the low point. We see the 10-year yield edging higher during 2026. The result is a swing in the cash/10-year spread from around -80bps to +60bps at end-2025 and rising. Underlying this view is also a belief that, irrespective of which party wins in November’s elections, the US fiscal position is unlikely to improve in coming years and will instead remain at risk of deteriorating further.

For the US dollar, while the extraordinary support from actual and expected rate differentials has abated somewhat in 2024, with the ECB and Bank of England now expected to cut sooner than the FOMC and likely by a similar amount over two years, aid for the US dollar from this factor is expected to remain at or above-average over the period. Around the time of November’s elections, policy expectations should also be constructive for US growth. Consequently, we have flattened out our US dollar profile, seeing DXY only edge lower from the 105–107 range recently traded to 103.5 end-2024 and 99.0 end-2025. Some further weakening is likely in 2026, but it is more probable that the US dollar will remain above long-run average levels than break through.

These developments have implications for Australian financial benchmarks as well. While our own fiscal situation is a stark contrast to the US, this means Australia’s 10-year is likely to trade in line with the US 10-year over the period and into the medium-term, rather than at a premium as in the past. We therefore regard the 4.0% level as a floor for yields in Australia as well, even as policy rates fall. We also continue to expect the Australian dollar to largely track the US dollar, averaging USD0.66 through June and September quarters before beginning to edge higher from December quarter (USD0.67). Through 2025, a 4 cent appreciation is expected to USD0.71 and in 2026 there is reason to believe further modest appreciation will be seen. To this profile, risk appetite and the persistence of inflation are set to remain downside risks. Most of this is a USD story, though; the outlook for Australia’s trade-weighted index remains a continuation of a broadly stable level, as it has been for the past decade.

May FOMC: Stalling in Inflation Leaves FOMC Stalling for Time

Summary

As was widely expected, the FOMC left the fed funds target range unchanged at 5.25%-5.50% at the conclusion of its May meeting. It was evident, however, that the Committee believes inflation's return to its 2% objective likely has a somewhat longer and uncertain journey ahead. In the post-meeting statement, the Committee noted that "in recent months, there has been a lack of further progress" toward its 2% inflation goal. This setback in obtaining confidence that inflation is on a sustainable path back to 2% reinforces our view that any reduction to the fed funds rate remains at least a couple of meetings away.

The Committee announced that it will slow the pace of quantitative tightening (QT) starting on June 1. The monthly cap for Treasury security redemptions was reduced from $60 billion to $25 billion, while the monthly redemption cap for mortgage-backed securities (MBS) was left unchanged at $35 billion. The slow-but-don't-stop approach to balance sheet runoff is an attempt to keep normalizing the size of the Fed's balance sheet without creating money market stresses like the ones that occurred in September 2019. The move to a slower pace of QT was well-telegraphed by the Committee, and the outlook for the federal funds rate will be far more critical to determining the level and shape of the yield curve in the months ahead, in our view.

Lack of Progress on Inflation Keeps FOMC on Hold

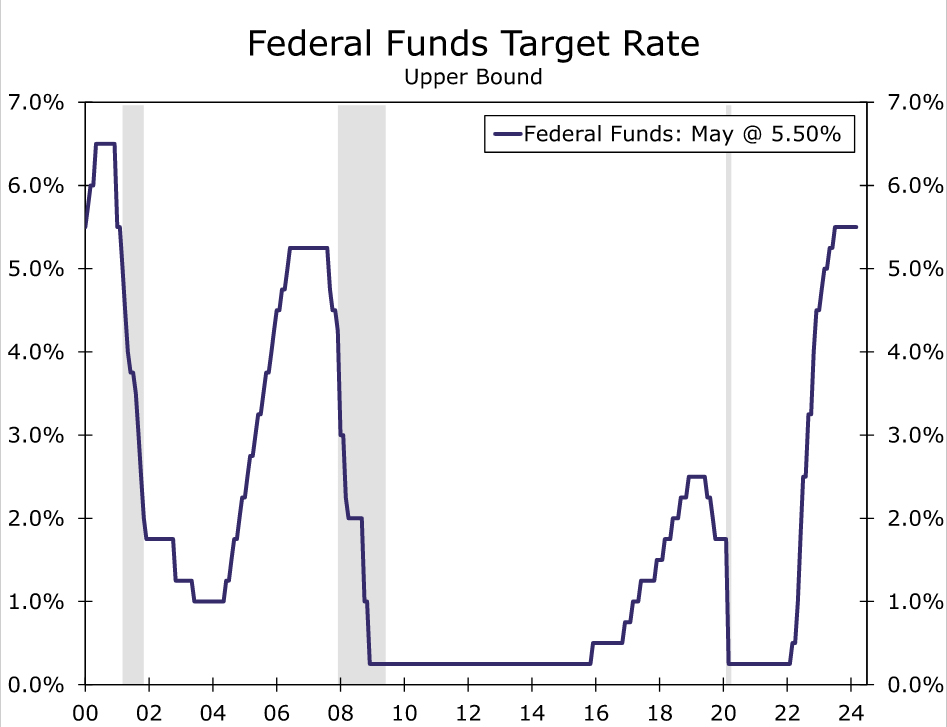

As universally expected, the Federal Open Market Committee (FOMC) voted unanimously at its meeting today to leave the target range for the federal funds rate unchanged at 5.25%-5.50%, where it has been maintained since last July (Figure 1). As is typical for the April/May FOMC meeting, the Committee did not release a Summary of Economic Projections, which contains the so-called "dot plot," at the conclusion of this meeting. Therefore, market participants need to infer the FOMC's intentions from its post-meeting statement and from the Q&A session in Chair Powell's press conference. In our view, these data points suggest the Committee is not in any rush to cut rates, a message that was delivered by numerous Fed officials in the weeks leading up to today's meeting (see our recent "Flashlight" report for further discussion.)

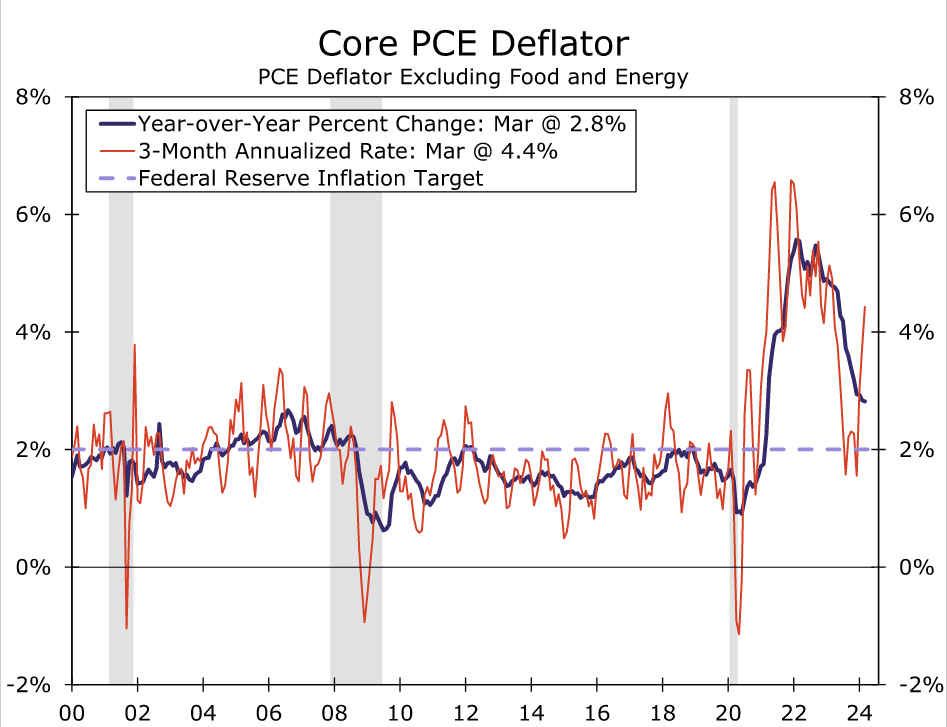

In that regard, the FOMC continues to have an upbeat assessment of the real economy. The post-meeting statement noted once again that "economic activity has continued to expand at a solid pace," that "job gains have remained strong" and that "the unemployment rate has remained low." Furthermore, the Committee continues to acknowledge that "inflation has eased over the past year," although the statement noted for the first time that "there has been a lack of further progress toward the Committee's 2 percent inflation objective." As shown in Figure 2, the year-over-year rate of core PCE inflation, which the FOMC considers to be the best measure of the underlying rate of consumer price inflation, has receded from more than 5% in 2022 to 2.8% in March. However, core PCE prices have shot up at an annualized rate of 4.4% over the past three months. To paraphrase recent Fed speakers, the FOMC will need greater "confidence" that inflation is returning to 2% on a sustained basis before it feels comfortable cutting its target range for the federal funds rate. In our view, the Committee will not have that confidence until the September 18 FOMC meeting, at the earliest.

In Chair Powell's post-meeting press conference, he noted that it likely will take longer than originally thought to get that confidence. Notably, he backed off any reference to the potential timing of a rate reduction in his prepared remarks, no longer stating that "it will likely be appropriate to begin dialing back policy restraint at some point this year" (emphasis ours). Yet he also noted that he believes it is "unlikely" that the FOMC will need to hike again and that policy remains restrictive. On balance, the recent data appear to have pushed the FOMC away from the precipice of rate cuts but still very comfortable with a wait and see approach.

Slow-But-Don't-Stop for QT

Although the Committee kept its primary policy tool, the federal funds rate, unchanged at today's meeting, the FOMC did announce some changes to its balance sheet runoff program. The Committee announced that it intends to slow the decline in its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The monthly redemption cap for mortgage-backed securities (MBS) was left unchanged at $35 billion. The new caps will be effective starting June 1.

The logic for slowing runoff is fairly straightforward: the ultimate “equilibrium” size of the Fed's balance sheet is uncertain, and a prudent risk management policy calls for a slow-but-don't-stop approach as the Fed feels out the optimal size for its balance sheet. The minutes from the last FOMC meeting noted that “slower runoff would give the Committee more time to assess market conditions as the balance sheet continues to shrink.” Powell reiterated in his press conference that slowing the pace of runoff will help ensure a "smooth transition" and "reduce the possibility that money markets experience stress." We think the new pace of runoff will continue through at least year-end 2024.

Fed stands pat, acknowledge lack of progress in disinflation

Fed keeps interest rate unchanged at 5.25-5.50% as widely expected.. In the accompanying statement. Fed noted that there has been a " lack of further progress" recently on lowering inflation towards target.

Meanwhile, FOMC emphasized that "The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent."

Full statement below:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; Loretta J. Mester; and Christopher J. Waller.

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; Loretta J. Mester; and Christopher J. Waller.