Sample Category Title

FX Interventions Do Not Change a Currency’s Fundamental Course

Markets

The Fed kept the policy rate stable at the 5.25%-5.50% range yesterday. The statement did feature some changes, including that “In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.” It also announced that the Fed will reduce the pace of QT in Treasuries from $60bn to $25bn while keeping the $35bn cap in MBS. The “lack of further progress” translated in chair Powell saying it’s going to take longer to gain the confidence that inflation is indeed back on track towards target. In terms of policy rates, it boils down in keeping them at the current level for a little while longer. That’s exactly what markets have been repricing for in recent months. Some in the outskirts of the market even began contemplating about rate hikes again. Powell noted it was unlikely that the next move would be an increase. Minutes later he did say that “In terms of peak rate, […] I think the data will have to answer that question for us.” Turning to those data, yesterday’s was a mixed bag. The April ADP job report (192k with an upward revision to March) was stronger than expected. But the manufacturing ISM unexpectedly dipped in contraction territory again (49.2) while price pressures in the sector intensified sharply. Yields finished the session lower in technically irrelevant trading. Daily changes varied between -3.5 bps (30y) to -7.5 bps (2y). The dollar lost ground against the euro (EUR/USD 1.0712) though we should add that this happened in holiday-thinned European trading (Labor Day). It was also partially a spillover from what is a presumed FX intervention by Japanese officials in late US dealings. USD/JPY dropped sharply from 158 to an intraday low of 153.04 before closing at 154.57. US stock markets swung from gains of up to 1.75% (Nasdaq) in volatile trading.

The Japanese yen is once again in the spotlights during Asian dealings, erasing about half of yesterday’s gains and confirming that FX interventions do not change a currency’s fundamental course. Stocks in the broad region trade mixed with few news stories to guide them. The dollar and euro trade balanced while yields in the US ease less than 2 bps. The economic calendar contains the (outdated) Q1 productivity numbers and unit labor costs. The jobless claims give us the usual weekly look on the labour market. All in all we don’t think it’ll trigger big swings ahead of tomorrow’s US services ISM and the payrolls report. We may see German bonds outperform in core markets as they catch up with the US yesterday but we wouldn’t draw any firm conclusions from that. Technical trading could keep EUR/USD oscillating around the 1.07 big figure as it has been doing for the last couple of sessions.

News & Views

The US Treasury released its quarterly refunding statement yesterday. Since August 2023, Treasury has significantly increased issuance sizes for nominal coupon and FRN securities. Based on current projected borrowing needs, Treasury does not anticipate needing to increase them further for at least the next several quarters. Actual auction sizes remain steady for the May-July period at their April (peak) level of $69bn, $58bn, $70bn and $44bn for 2-yr, 3-yr, 5-yr and 7-yr sales. The longer tenors follow the same rhythm as in the Fed-Apr period implying higher auction sizes in the first month (cumulative $83bn for 10-yr, 20-yr & 30-yr in May vs $74bn in June & July). Treasury expects to increase the 4-, 6-, and 8-week bill auction sizes in the coming days to ensure sufficient liquidity to meet one-week cash needs around the end of May. Over the course of July, auction sizes will reach the highs from February and March. Finally, Treasury announced the launch of a buyback program. They aim to end up with operation sizes of maximum $30bn per quarter across buckers for liquidity support.

Rating agency Moody’s raised the outlook on Brazil’s Ba2 rating from stable to positive. Improved growth prospects with upside potential over the medium and long term are one reason. Moody’s expects growth to average around 2% in coming years. Second, structural reforms over successive administrations support policy effectiveness with institutional guardrails reduce policy uncertainty. Finally, gradual fiscal consolidation may lead to a stabilization of the debt burden. A new fiscal framework limits the increase in real primary spending to 70% of the increase in real revenues in the previous year.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut and has broad backing. EMU disinflation will continue in April and bring headline CPI (temporarily) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets come to terms with that, pushing yields up.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective. Upcoming CPI readings and a resilient economy/labour market will continue to prevent the Fed to cut rates fast nor deep. September at the earliest, but December is more likely. US yields, especially at the front end, could catch a breather after the recent sharp repricing, but their bottom is well protected.

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the previous YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a technical break. Last year’s low at 1.0494 looks vulnerable.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

Powell Did Not Shake Markets

In focus today

Today offers a light schedule in terms of tier-1 data releases.

Most global markets that were off yesterday due to the International Labour Day are back today.

In the US, we will keep an eye out for the preliminary Q1 productivity data. Surprisingly strong productivity growth contributed to the US economy's stellar performance in 2023, but its persistence remains uncertain. We also receive the initial jobless claims figure.

Swedish PMIs for April are released at 9:30 CET. In the last release, Manufacturing PMI reached expansionary ground once again at 50.0 for the first time since June 2022. New orders increased to 50.9, thus adding up to an increase of 2.6 in the aggregated Manufacturing PMI for Q1 2024, mainly driven by new orders in the export sector. We anticipate that the positive trend continues in today's release.

Economic and market news

What happened overnight

In Japan, authorities appeared to have intervened in FX markets, as the yen took a sharp upwards turn against the dollar (USDJPY) from around 157 to 153 in less than 45 minutes. The suspected intervention came after the dollar had been weakening some on the back of the Fed's decision to leave rates unchanged and Fed chairman Powell's subsequent remarks (read more below). As of this morning the USDJPY is trading around 156.

Asian markets have reacted to yesterday's Fed decision by trading a bit mixed with Shanghai and South Korea slightly down, and Australia, Japan, and Hong Kong in the Green.

US futures for major indices are all trading up as of this morning with Nasdaq futures in front having gained around 0.6%. S&P500 and Dow Jones futures are not far behind trading about 0.5% and 0.4% up respectively.

What happened yesterday

In the US, the Fed left interest rates unchanged as was widely expected amongst market participants. In its press release, the FOMC announced that from June onwards it will reduce its monthly quantitative tightening (QT) programme for US Treasuries to USD25bn from the previous USD60bn a month. It left its cap on reducing its holdings of Mortgage-Backed Securities unchanged at USD35bn a month.

At the press conference, Powell provided few new clues on the policy outlook but emphasized that the Fed continues to see its policy having a restrictive effect on demand. As such he made it clear the Fed remains in a good place with its current policy. However, the Fed needs more confidence on inflation returning to target before deciding on a rate cut. Yet, he said it is unlikely that the next move would be a hike.

Markets initially reacted in a dovish manner sending both the dollar and long yields down. However, this reaction mostly faded later, and both the dollar and 10Y UST yields ended little changed from pre-meeting levels. Read more in Research US - Fed review - Maintaining easing bias, 2 May.

The ISM manufacturing figure for April fell more than expected coming in at 49.2 vs. consensus expectations of 50.0. The month prior it stood at 50.3, and the drop was driven especially by new orders which dropped to 49.1 from 51.4 the month prior.

The ADP jobs report showed slightly stronger jobs growth in the private sector than what was expected posting 192k additional jobs for April, and an upwards revision to the March figure of 24k. Tomorrow we will be looking out for the jobs report where we expect 200k additional non-farm jobs created in April.

The JOLTs job opening numbers pointed to fewer job openings than expected, as such lending support to the narrative of a cooling labour market. There was a total of 8.488mn job openings in March, and the ratio of job openings to unemployed jobseekers declined to 1.32, the lowest seen since the initial Covid-shock hit the economy in 2020. The February figure saw a very slight upward revision of around 50k.

In the Quarterly Refinancing Announcement (QRA) the US Treasury said issuance is going to be concentrated in the 2Y-5Y segment as well as in T-Bills. They also announced that auction sizes would remain unchanged "at least for the next several quarters". Guidance is thus overall unchanged from January, just as expected.

In Europe, most markets were out due to International Labour Day, however those that remained opened traded mostly in the red with for instance the FTSE100 dropping 0.28%. Market movements.

Happy Apple Day

The Federal Reserve (Fed) decision yesterday was… interesting. As expected, the Fed kept its rates unchanged and said that they are not confident to cut the interest rates as inflation has started to show signs of heating up. Jerome Powell reassured that the Fed’s next move will unlikely be a rate hike. That was a relief. Then, the Fed said that it will start tapering QT. It sounded like ‘the rates must stay longer in the oven but taste this – in the meantime’.

The market reaction to the decision was mixed. The stocks first gained then erased losses. The S&P500 closed the session down by 0.34%. The treasury yields fell. The 2-10year portion of the yield curve remains inverted, mind you, since summer 2022. Maybe – but just maybe – we will finally see recession arrive to the US? Note that the latest GDP print in the US surprised by a sharp slowdown to 1.6%, from above 3% printed a quarter earlier, and down from 5% printed the quarter before that. Interest rate swaps still price in one rate cut for 2024, sometime by the year end.

Data-wise, the ADP report came in stronger than expected yesterday with 192K new private job additions in April compared to around 180K expected by analysts, but job openings further fell and the ISM manufacturing PMI fell into the contraction zone while price pressures continued to rise. US oil inventories on the other hand jumped more than 7-mio barrels according to yesterday’s EIA data. All eyes are on the official jobs data due tomorrow.

The cocktail of no-rate-cut-in-horizon from the Fed, soft economic data, rising price pressures and rising US oil inventories sent the barrel of US crude below the $80pb level. News that the US and Saudi Arabia are working on a new pact to help ease tensions in the Middle East strengthens the bears’ hands as well. Note that yesterday’s decline pushed the barrel of crude into the medium-term bearish consolidation zone and paves the way for deeper losses. Next support is seen at $78pb – the 100-DMA.

In the FX, the US dollar eased yesterday, but a part of the move was explained by the sharp fall in the USDJPY which tanked from 157.50 to 153 within minutes, fueling speculation that the Bank of Japan (BoJ) certainly has its fingers behind the move. The USDJPY is back above 155 this morning, but this time, the downside correction was certainly big enough to clear speculative longs and give the holders of short yen positions cold feet. The BoJ has drawn the red line at the 160 level this week, saying no one goes above. Let’s see if enough traders are willing to challenge that view.

Elsewhere, the EURUSD rebounded past the 1.07 level, while Cable settled above 1.25. The USDCHF continues its steady ascent on the back of the growing divergence between the Fed – unable to cut rates because of rising inflation and the SNB – well positioned to cut rates again thanks to subdued price pressures. Gold sees support at $2284 – the minor 23.6% Fibonacci retracement on October to April rebound. Softer US yields, rising inflation, ambiguous direction for equities and uncertain geopolitical landscape should keep appetite robust near the $2300 support.

Chips and cannabis

Amazon gained more than 2% yesterday as its cloud business grew more than expected in Q1 thanks to AI. AMD fell more than 9%, as the company gave a weak outlook for game chip demand and Super Micro Computer tumbled 14% as earnings missed lofty expectations. Fears regarding a slowdown in chip demand pulled Nvidia nearly 4% down, while Micron Technology fell almost 3%. Happily, Qualcomm rebounded 4% in the afterhours trading on solid forecast for the current period.

Cannabis stocks, which were flying high on Tuesday following the US decision to reclassify marijuana as a less dangerous drug, fell yesterday. Beyond the short-term volatility, the reclassification will have a concrete positive impact on pot companies’ profit margins through tax breaks, hence the sector could see a sustainable growth following the decision. I don’t think that we will see another bubble in pot stocks – similar to the one we saw in 2018 and again in 2021, but having exposure to a Marijuana ETF – like YOLO – wouldn’t hurt.

Apple day

Apple is due to report Q1 results today after the bell. Expectations are soft given that Apple’s Chinese business got a major hit in Q1 as competitors increased their market share against the giant Apple. The chances are that, the actual results won’t blow anybody’s mind.

What investors now expect is plans and projects regarding how Apple will integrate AI into its devices and catch up with its AI delay. Good news is, because Apple is not seen as a cutting-edge technology company – but also a luxury brand – any promising step in AI could get a decent leverage from the company’s high brand value. Therefore, if investors are convinced that Apple’s got a robust AI plan, we could see a positive reaction to otherwise weak quarterly results. Pricewise, Apple is down by 15% since the December peak, and near the major 38.2% Fibonacci retracement on ytd selloff. Either it will stay in the positive trend and attempt a rebound, or it will sink into the medium-term bearish consolidation zone.

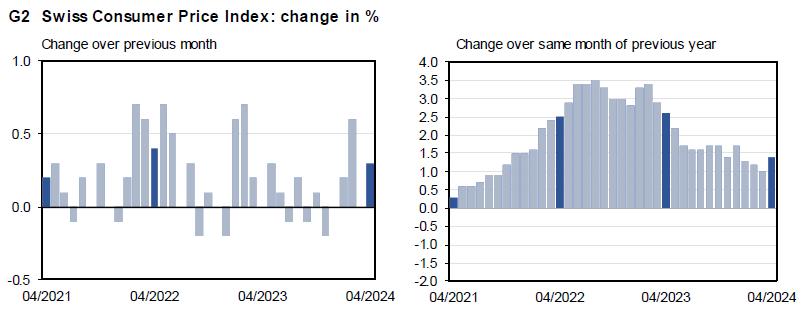

Swiss CPI rises to 1.4% yoy in Apr, above expectations

Swiss CPI rose 0.3% mom in April, above expectation of 0.2% mom. CPI core (excluding fresh and seasonal products, energy and fuel) rose 0.4% mom. Domestic products prices rose 0.1% mom. Import products prices rose 1.1% mom.

Over the 12 month period, CPI accelerated from 1.0% yoy to 1.4% yoy, above expectation of 1.1% yoy. CPI core increased from 1.0% yoy to 1.2% yoy. Domestic products price growth rises from 1.7% yoy to 2.0% yoy. Imported products prices contraction lessened from -1.3% yoy to -0.4% yoy.

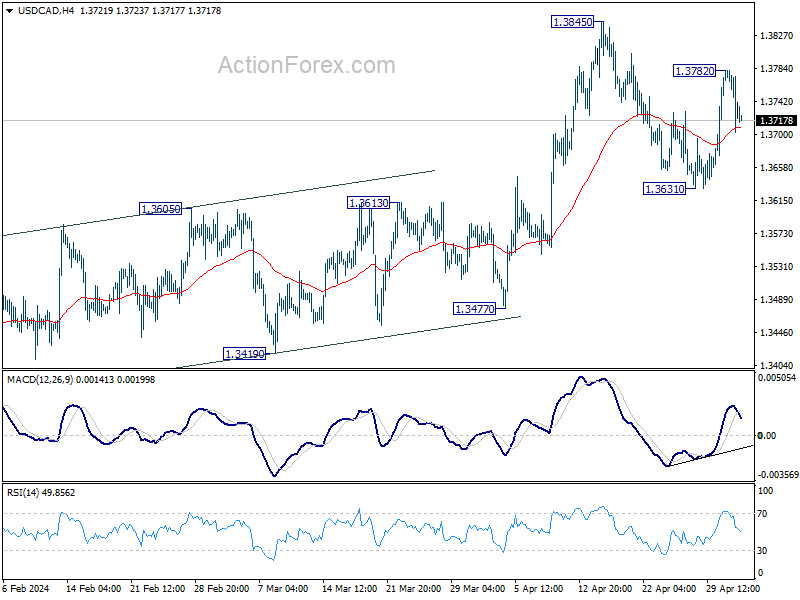

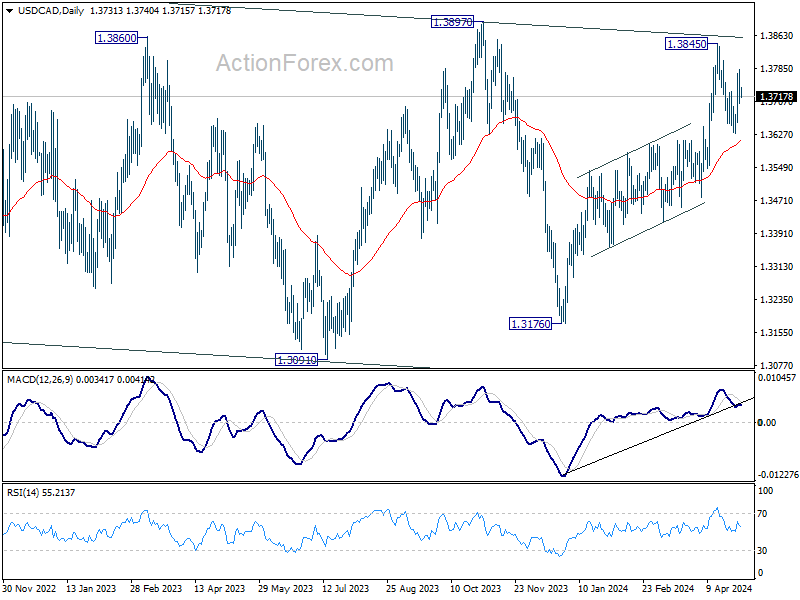

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3700; (P) 1.3742; (R1) 1.3779; More...

Intraday bias in USD/CAD is turned neutral again with current retreat. On the upside above 1.3782 will target 1.3845 resistance first. Firm break there will resume larger rise from 1.3176 towards 1.3976 key resistance next. On the downside, break of 1.3631 will extend the fall from 1.3845. Sustained trading below 55 D EMA (now at 1.3615) will argue that whole rise from 1.3176 has completed already.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

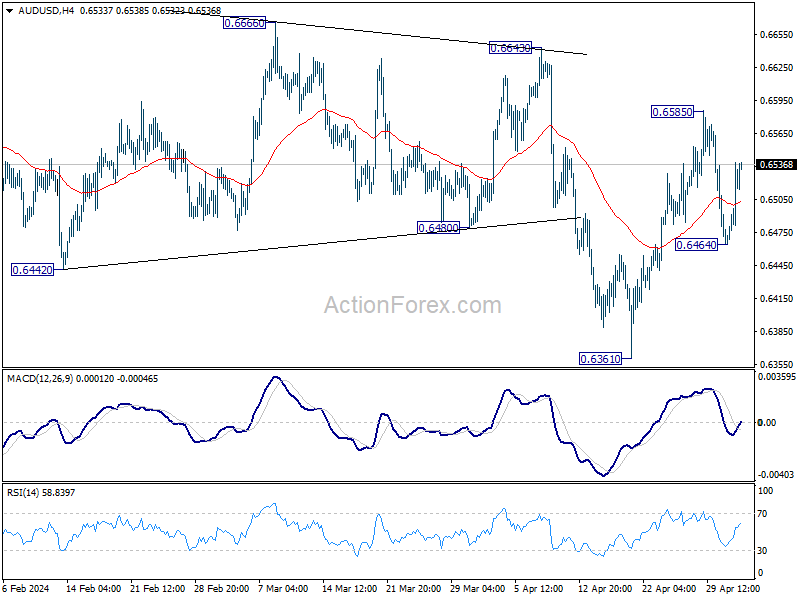

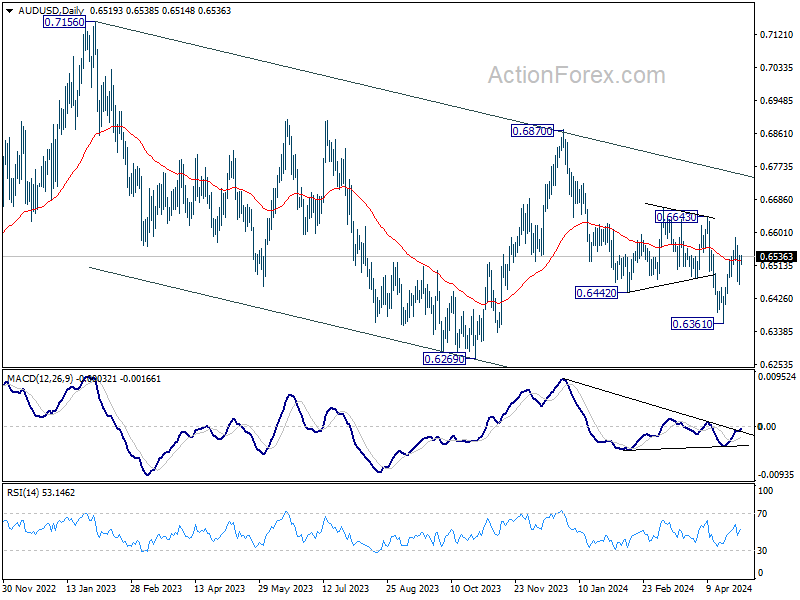

AUD/USD Daily Report

Daily Pivots: (S1) 0.6479; (P) 0.6509; (R1) 0.6554; More...

Intraday bias in AUD/USD is turned neutral again with current recovery. On the upside, break of 0.6585 resistance will resume the rebound from 0.6361. That would also affirm the case that fall from 0.6870 has completed. Further rally would be seen to 0.6643 resistance next. Nevertheless, break of 0.6464 will bring deeper fall back to retest 0.6361 low.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

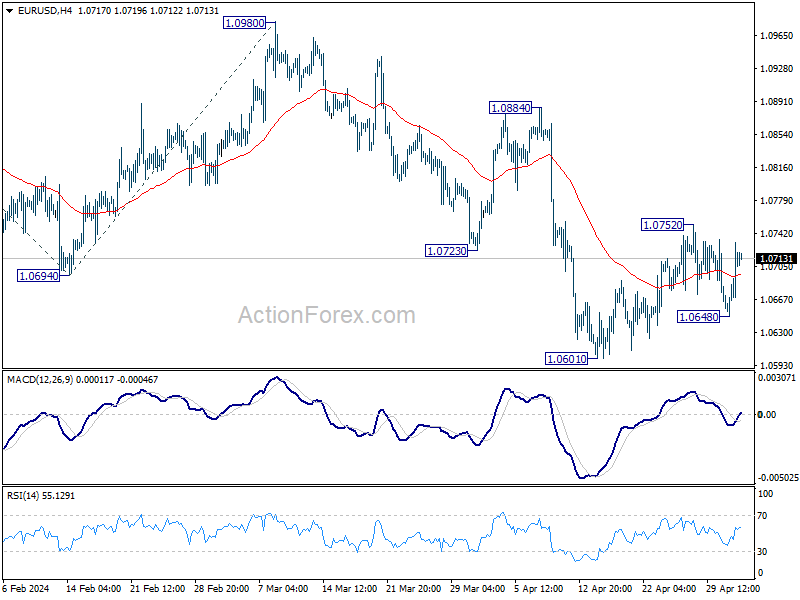

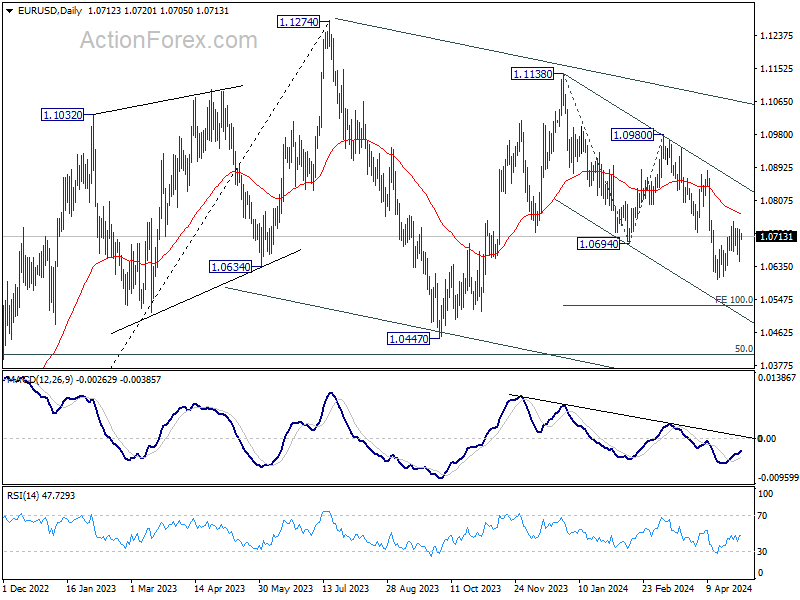

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0664; (P) 1.0699; (R1) 1.0748; More...

Intraday bias in EUR/USD is turned neutral against with current recovery. On the upside, break of 1.0752 will resume the rebound from 1.0601. Sustained trading above 55 D EMA (now at 1.0770) will argue that fall from 1.0980 has completed. On the downside, though, break of 1.0648 will retain near term bearishness and bring retest of 1.0601 low first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

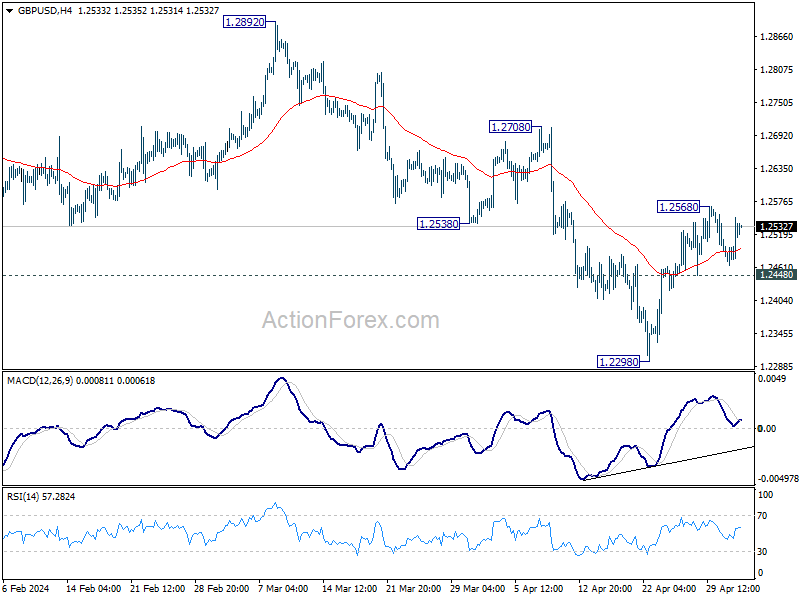

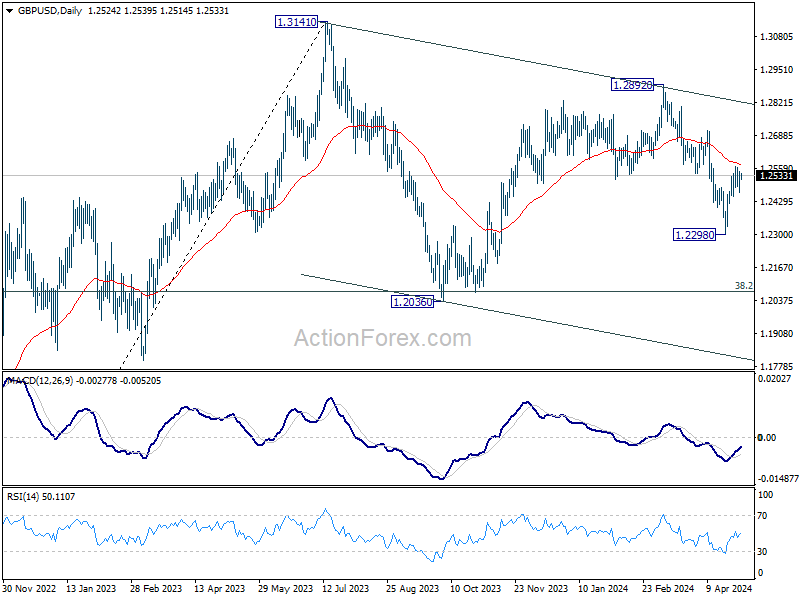

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2481; (P) 1.2516; (R1) 1.2564; More...

Range trading continues in GBP/USD and intraday bias remains neutral. On the upside, above 1.2568 will resume the rebound from 1.2298 to 55 D EMA (now at 1.2578). Sustained break there will argue that fall from 1.2892 has completed already, and bring further rise to this resistance. Nevertheless, on the downside, break of 1.2448 minor support will indicate that rebound from 1.2298 has completed, and turn bias back to the downside for this low.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

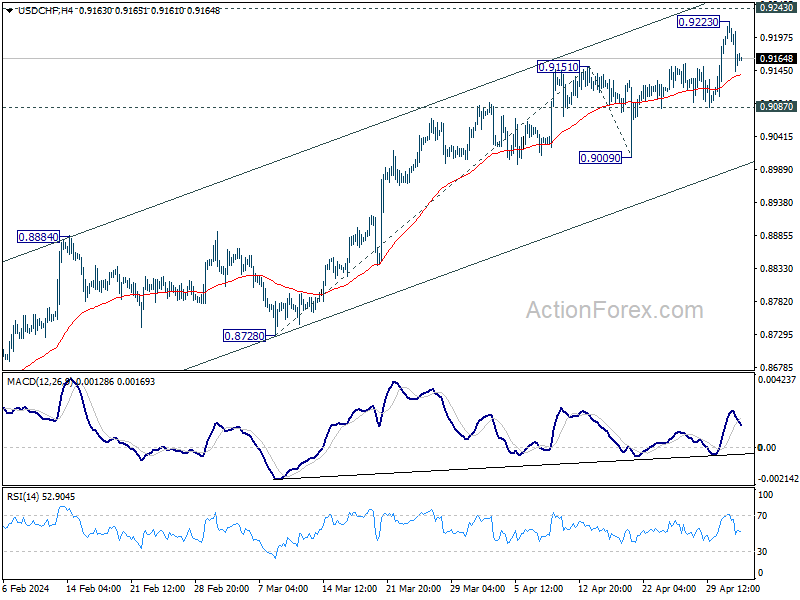

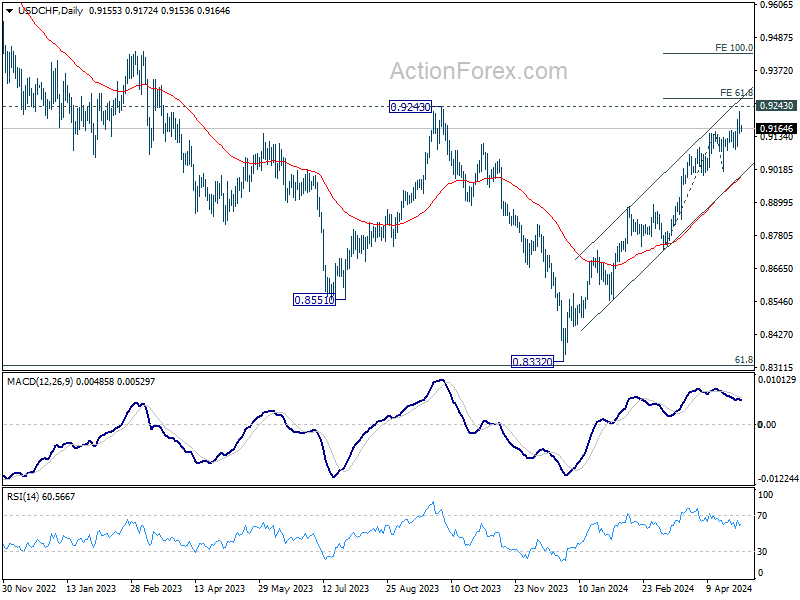

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9176; (R1) 0.9207; More....

USD/CHF retreated after rising to 0.9223 and intraday bias is turned neutral first. Further rally is in favor as long as 0.9087 support holds. On the upside, above 0.9223 will resume larger rally to 0.9243 resistance, and 61.8% projection of 0.8728 to 0.9151 from 0.9009 at 0.9270. However, firm break of 0.9087 will indicate rejection by 0.9243 and turn bias back to the downside 0.9009 support instead.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8884 resistance turned support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

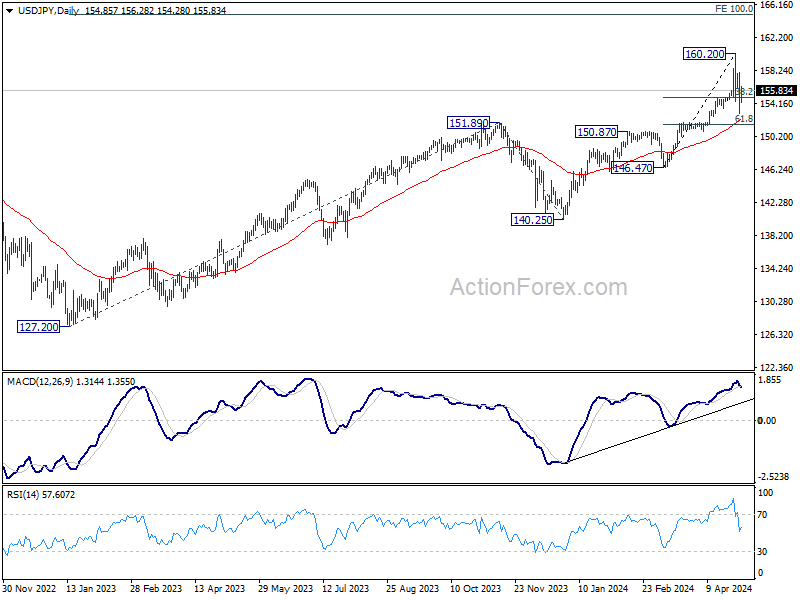

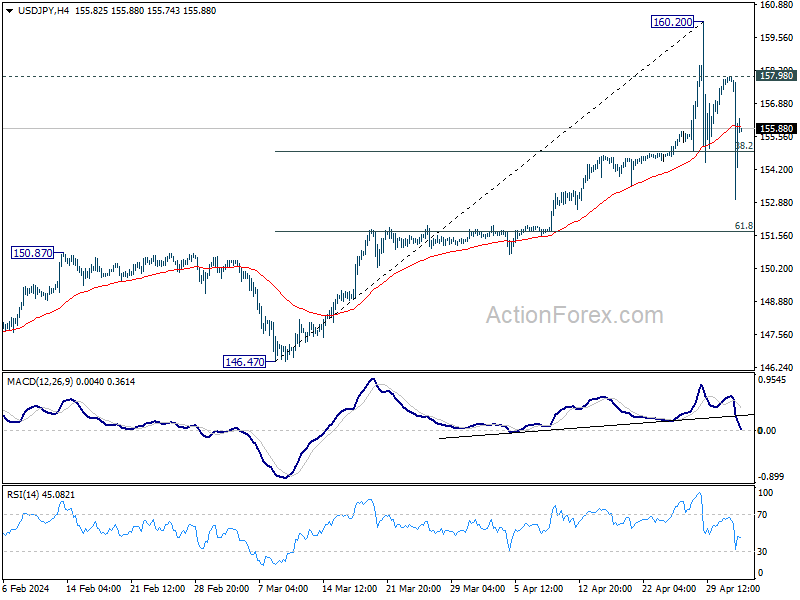

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.27; (P) 155.13; (R1) 157.26; More...

USD/JPY's correction from 160.20 short term top extended with another dip to 152.99, but quickly recovered again. For now, risk will be mildly on the downside as long as 157.98 resistance holds. Deeper pullback would be seen to 55 D EMA (now at 152.25), and possibly further to 61.8% retracement of 146.47 to 160.20 at 151.71. But strong support should be seen from 150.87 to bring rebound.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.