Sample Category Title

Currency Markets an Ocean of Calm

Markets

US Treasury yields ease a few more bps in the wake of yesterday’s FOMC policy meeting. Markets were bracing for a hawkish surprise from chair Powell following a string of higher-than-expected inflation readings and ongoing economic resilience. Its absence pushed rates up to 7 bps lower at the front with additional losses of some 2 bps today. The 5% psychological mark in the 2y tenor is being left alone for the time being. Longer maturities swapped minor losses for gains as US investors started joining and going into some second tier eco data that eventually didn’t move any significant barriers. Tomorrow’s services ISM and April payrolls report on the other hand do have the potential to do so. First quarter unit labor costs jumped from 0% in 2023Q4 to 4.7% amid a sharp slowdown in productivity from 3.5% to 0.3%. Initial jobless claims again came on to the strong side of expectations, stabilizing at 208k vs a small uptick to 211k expected. German Bunds slightly outperformed Treasuries in a catch-up move after taking the day off on Wednesday. Rates drop between 0.4 and 1.7 bps across the curve but trade off the intraday lows.

Currency markets are an ocean of calm. The euro loses a few ticks against an equally unconvincing dollar. EUR/USD is testing the 1.07 big figure. The Japanese yen almost fully pared morning losses of a percent or more following an alleged intervention by Japanese officials in late US dealings yesterday. Guestimates amount to JPY 3.5tn on top of the JPY 5.5tn spent Monday. USD/JPY is currently changing hands just south of 155. Sterling put up base camp again around EUR/GBP 0.855. Elsewhere, the Czech crown trades (EUR/CZK 25.08) unchanged after the central bank cut rates by the expected 50 bps to 5.25%. At the presser later today, markets will be keen to spot hints for a slower cutting pace going forward.

News & Views

At the end of last year and early this year, inflation in Switzerland slowed faster than expected. This allowed the Swiss National Bank to reduce its policy rate from 1.75% to 1.50% at the March meeting. However, the decline in inflation came to a halt last month. Headline inflation printed at an above consensus 0.3% M/M and 1.4% Y/Y (was 0.0% m/m and 1.0% in March). Core inflation also reaccelerated to 1.2% Y/Y from 1.0%. According to the Swiss Federal Statistical Office, the monthly increase was, amongst others due to rising prices for international package holidays and air transport. Furniture and furnishings also recorded a price increase, as did petrol. In contrast, prices for hotels and supplementary accommodation decreased, as did those for gas. Contrary to what was often the case of late, the rise in inflation was mainly driven by higher prices for goods (+0.6% M/M) rather than services (+0.1% M/M). Despite the higher than expected April increase, inflation still holds comfortably in the 0%-2.0% inflation target band. Markets lowered the probability of an additional 25 bps cut in June to slightly more than 50%. The Swiss franc rebounded from about EUR/CHF 0.9815 this morning to 0.9765 currently.

The OECD in updated forecasts indicates that the outlook on the global economy has started to brighten. Global growth was revised higher for this year to 3.1% compared to 2.9% expected in February. The impact of tighter monetary conditions continues but global activity is proving relatively resilient, inflation is falling faster than initially projected and private sector confidence is improving. Supply and demand imbalances in labour markets are easing, with unemployment remaining at or close to record lows, real incomes have begun to turn up as inflation eases and trade growth has turned positive. However, developments continue to diverge across countries, with softer outcomes in Europe and most low-income countries, offset by strong growth in the United States and many large emerging-market economies. The overall macro policy mix is expected to stay restrictive, with real interest rates declining only gradually and mild fiscal consolidation in most countries over the next two years. Annual consumer price inflation in the G20 economies is projected to ease gradually, declining to 3.6% in 2025 from 5.9% in 2024. By the end of 2025, inflation is projected to be back on target in most major economies.

Graphs

EUR/CHF: Swiss franc rebounds after hotter than expected inflation reduces market bets for further SNB cutting

Czech 2y swap yield. CNB cut by 50 bps to 5.25%. Markets now await the presser for clues on potential slower pace.

Brent oil ($/b) struggles to recover from a (technically driven) gap sub $85

S&P500 looking for direction as sell-on-upticks pattern still holds for now

USD/CHF Makes a Temporary Reversal After Swiss Inflation Jumps

Swiss CPI figures released earlier today came out above expectations, at 1.4%, leading to a reversal of some recent losses for the Swiss franc against other currencies. Observing the USD/CHF pair, we notice a significant intraday drop that appears to be an impulsive move down from a new high. Ideally, this trend could drive the pair even lower, possibly toward the 0.9 area where new support might be found. The reason is wave C of a potential ABC flat formation. So, despite current sell-off, we still believe that the higher degree trend will resume at some point, perhaps within the next week or so.

Canada’s Trade Accounts Register a $2.3 Billion Deficit in March

Canada’s merchandise trade balance swung to a $2.3 billion deficit in March, while February's surplus was revised lower to $476 million.

Exports, which fell by 5.3% in March, gave back most of last month's hefty gain. The contribution to the decline was broad-based, with 9 of 11 sectors falling. Gold and other metal exports continue to swing the headline number, falling by 32.5% month-on-month (m/m). Exports of energy products (-4.9% m/m) and exports of motor vehicles and parts (-6.3% m/m) also contributed to the slide.

Meanwhile, total imports also fell (-1.2% m/m) in March with 7 of 11 product sectors seeing declines. Imports of electronic and electrical equipment fell by 8.1% m/m in March after a sizeable gain last month. Further contributing to the decline was a decrease in metal ores and non-metallic mineral imports (-27.9% m/m), which was partially offset by a 10.8% m/m gain in metal and non-metallic mineral imports.

In volume terms, imports rose by 0.6% in the first quarter while exports were effectively flat.

Canada's trade surplus with the United States narrowed from $8.5 billion in February to $6.5 billion in March.

Key Implications

Before the release of the March trade data, export activity was shaping up to be a decent tailwind to Q1 growth. However, volatility stemming from trade in gold and other metal sectors combined with revisions to last month's data suggest trade may turn out to be a net drag in the first quarter. This is meaningful as it puts downside risk to the most updated forecasts for first quarter GDP growth–including the Bank of Canada's newly revised projections of 2.8%.

March's data pours cold water on the prospects of a sustained upturn in external demand, as export volumes pulled back sharply. Imports, a barometer for domestic demand, suggests the Canadian consumer is holding up moderately well despite the slight decline in March import volumes. However, over the near term we would expect imports to moderate further as spending patterns weaken over the coming months.

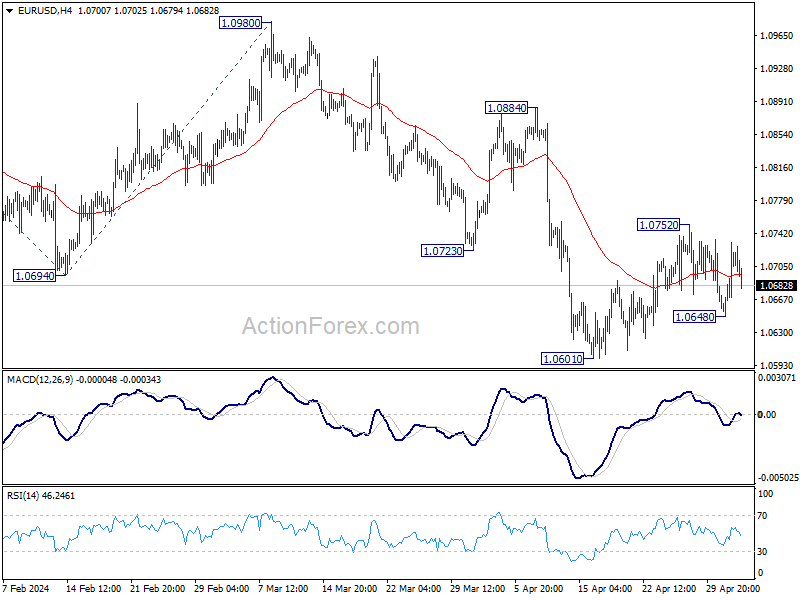

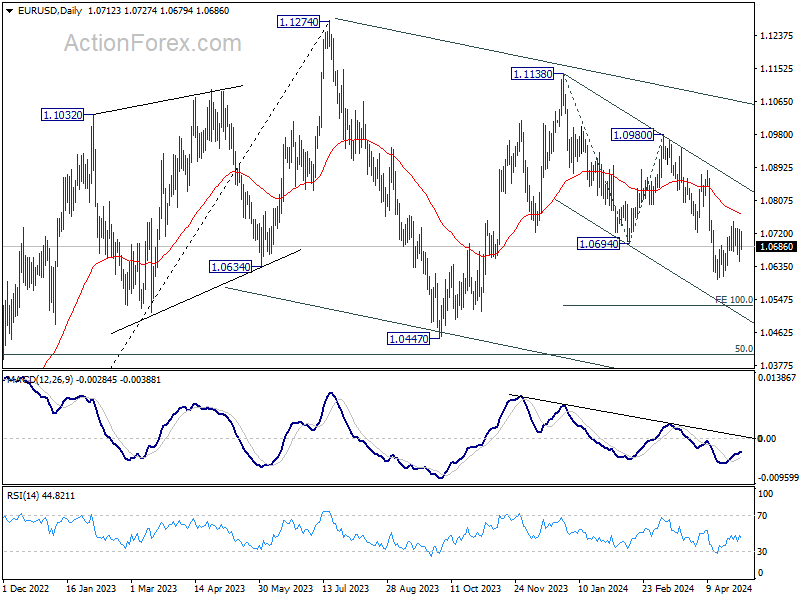

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0664; (P) 1.0699; (R1) 1.0748; More...

Intraday bias in EUR/USD remains neutral as range trading continues. On the upside, break of 1.0752 will resume the rebound from 1.0601. Sustained trading above 55 D EMA (now at 1.0770) will argue that fall from 1.0980 has completed. On the downside, though, break of 1.0648 will retain near term bearishness and bring retest of 1.0601 low first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

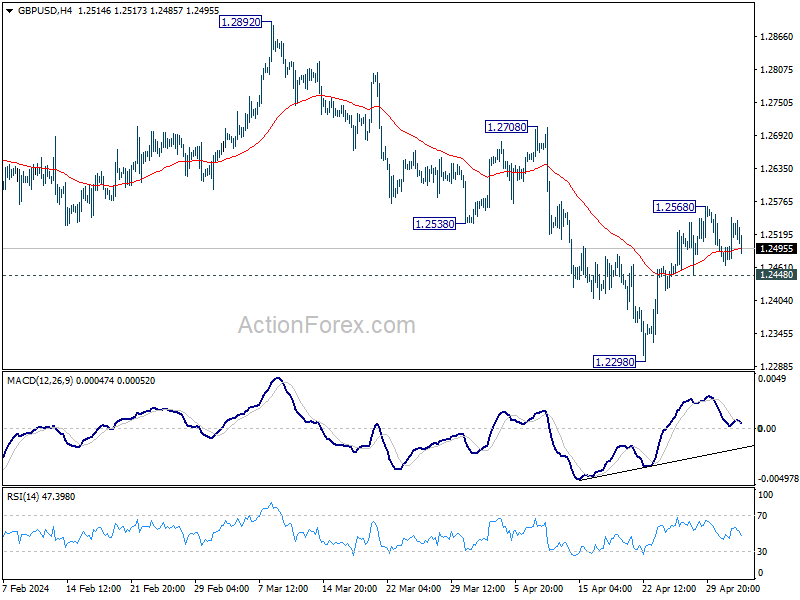

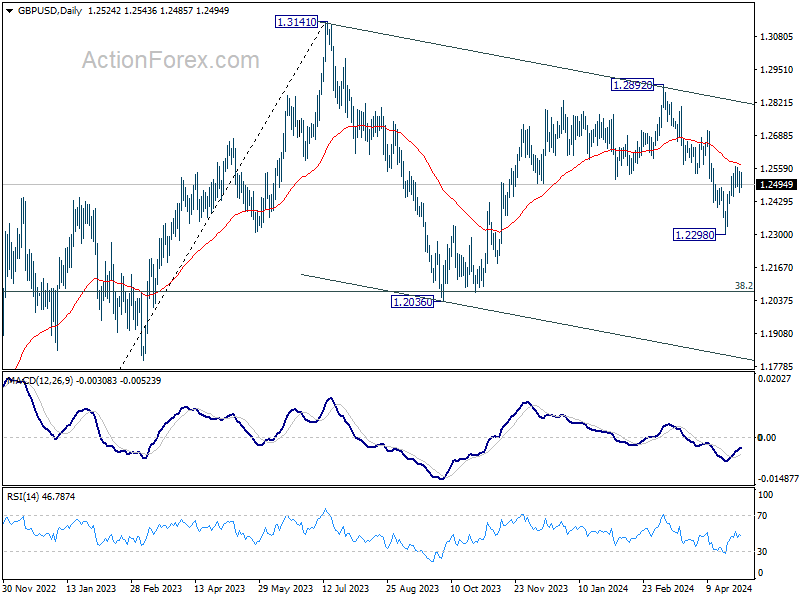

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2481; (P) 1.2516; (R1) 1.2564; More...

Intraday bias in GBP/USD remains neutral as range trading continues. On the upside, above 1.2568 will resume the rebound from 1.2298 to 55 D EMA (now at 1.2578). Sustained break there will argue that fall from 1.2892 has completed already, and bring further rise to this resistance. Nevertheless, on the downside, break of 1.2448 minor support will indicate that rebound from 1.2298 has completed, and turn bias back to the downside for this low.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

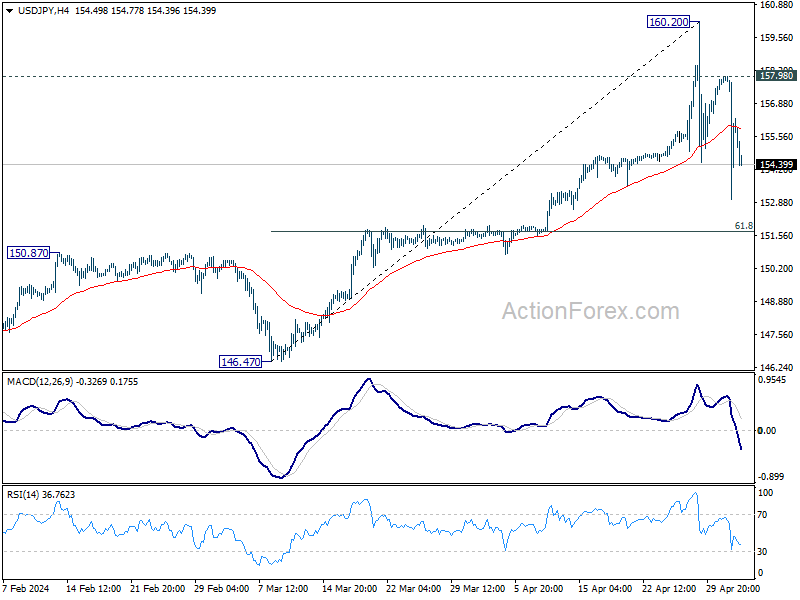

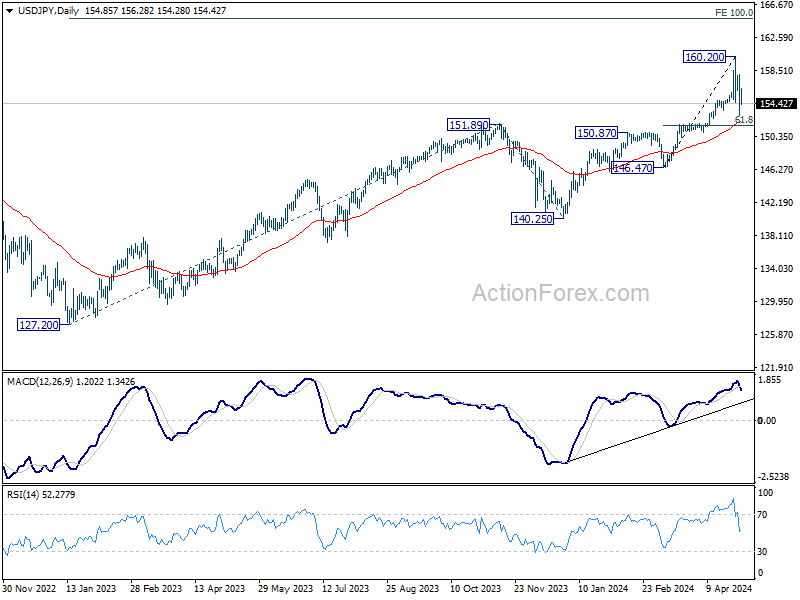

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.27; (P) 155.13; (R1) 157.26; More...

No change in USD/JPY's outlook as correction from 160.20 is in progress. Risk will stay on the downside as long as 157.98 resistance holds. Deeper pullback would be seen to 55 D EMA (now at 152.25), and possibly further to 61.8% retracement of 146.47 to 160.20 at 151.71. But strong support should be seen from 150.87 to bring rebound.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

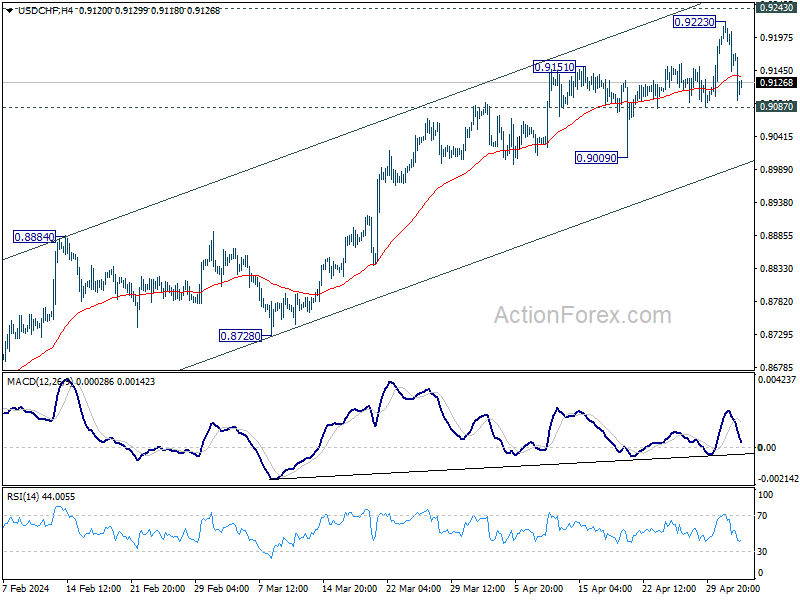

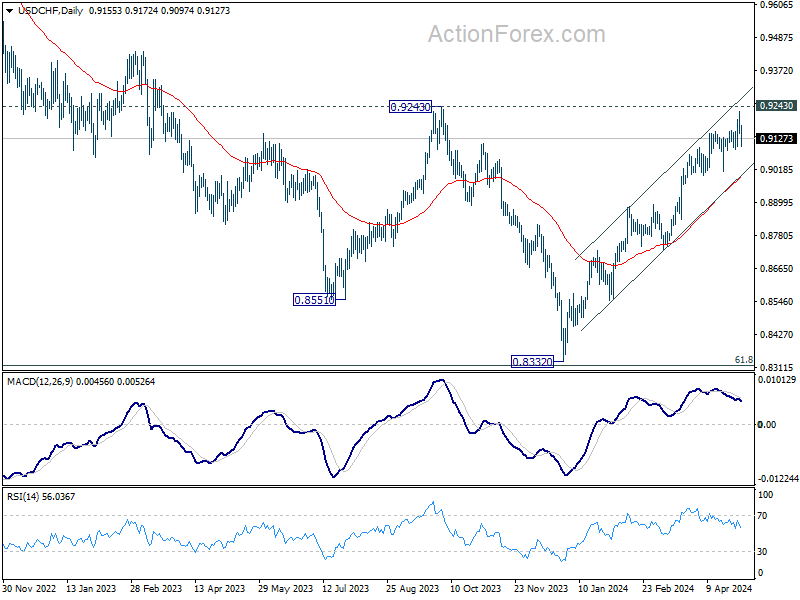

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9176; (R1) 0.9207; More....

Intraday bias in USD/CHF remains neutral for the moment. Further rally is still in favor as long as 0.9087 support holds. On the upside, above 0.9223 will resume larger rally to 0.9243 resistance. Decisive break there will carry larger bullish implication. However, firm break of 0.9087 will indicate rejection by 0.9243 and turn bias back to the downside 0.9009 support instead.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8884 resistance turned support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Swiss Franc Rebounds on Strong Inflation Data, Yen Standing Tall

Swiss Franc saw a significant rebound in European session, driven by stronger-than-expected inflation figures for April. Despite this upside surprise, inflation remained within SNB's target range of 0-2% for the eleventh consecutive month. Currently, economists are still largely anticipating a further 25 basis point rate cut by SNB in June, which would adjust the policy rate to a more neutral level of 1.25%. However, these expectations could be subject to change should inflation figures for May indicate acceleration again.

Meanwhile, Japanese Yen continues to dominate as the strongest currency for the week, bolstered by significant spikes on Monday and Wednesday. Despite Japan's top currency diplomat Masato Kanda refraining from confirming any market interventions, reports suggest that as much as JPY 3.5T may have been deployed in market operations on Wednesday. This speculation has solidified 160 mark as a firm ceiling for USD/JPY for now. We're are now keenly waiting to see if upcoming US non-farm payroll data tomorrow might trigger further pullback in USD/JPY.

In other parts of the currency markets, Swiss Franc trails only behind the Yen in strength for the week, with Sterling ranking third. On the flip side, Canadian Dollar is lagging as the weakest performer, followed by New Zealand Dollar and Australian Dollar. Dollar and the Euro are positioned in the middle.

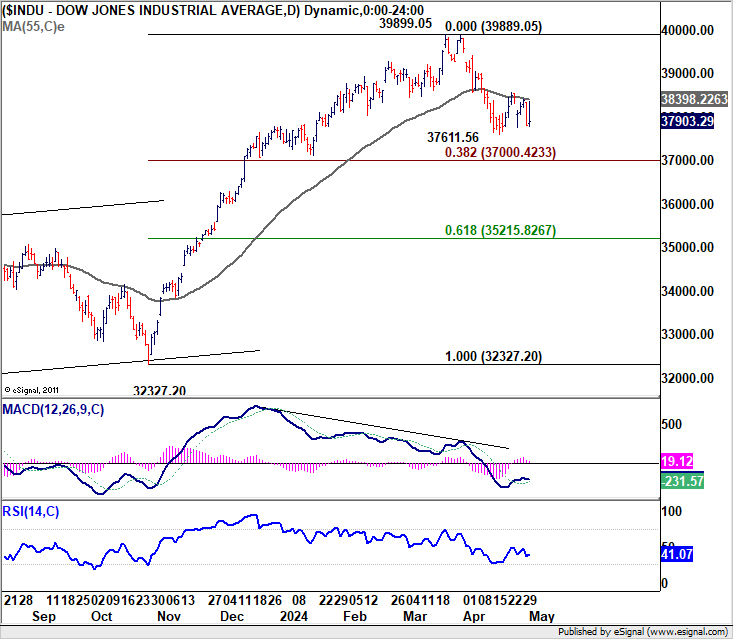

Technically, near term outlook in DOW remains bearish as it's firmly capped by 55 D EMA. The first question for the rest of the week would be on whether correction from 39899.05 would resume through 37611.56. The second question is, if #1 realizes, how would DOW reaction to 38.2% retracement of 32327.20 to 39889.05 at 37000.42. That would set the tone on risk sentiment for the rest of the quarter.

In Europe, at the time of writing, FTSE is up 0.45%. DAX is up 0.18%. CAC is down -0.63%. UK 10-year yield is down -0.0398 at 4.334. Germany 10-year yield is down -0.009 at 2.577. Earlier in Asia,Nikkei fell -0.10%. Hong Kong HSI rose 2.50%. China was on holiday, Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.0101 to 0.906.

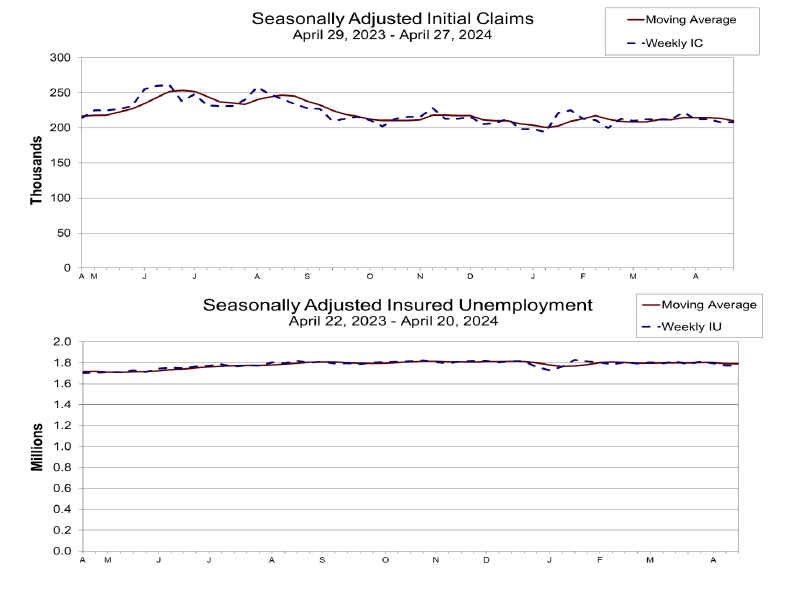

US initial jobless claims unchanged at 208k, vs exp 212k

US initial jobless claims was unchanged at 208k in the week ending April 27, lower than expectation of 212k. Four-week moving average of initial claims fell -3.5k to 210k. Continuing claims was unchanged at 1774k in the week ending April 20. Four-week moving average of continuing claims fell -4k to 1779k.

Also released IS trade deficit widened slightly from USD -68.9B to USD -69.4B, versus expectation of US -69.3B. Nonfarm productivity rose 0.3% in Q1, versus expectation of 0.8%. Unit labor costs rose 4.7% in Q1 versus expectation of 3.2%.

Canada trade balance recorded CAD -2.3B deficit, versus expectation of USD 1.0B surplus.

Eurozone PMI manufacturing finalized at 45.7, deepens recession despite bright spots in Spain and Netherlands

Eurozone's manufacturing sector remains entrenched in recession as April's PMI figures highlight ongoing challenges and disparities within the region. The overall Manufacturing PMI for the Eurozone was finalized at 45.7, a slight decrease from March's 46.1.

Among the member states, Greece led with a PMI of 55.2, though it marked a three-month low for the country. Spain and the Netherlands exhibited positive trends, with Spain reaching a 22-month high at 52.2 and the Netherlands achieving a 20-month high at 51.3. Conversely, major economies like Germany, France, and Italy continued to struggle. Germany's PMI slightly improved to a two-month high of 42.5, and France's was a three-month low at 45.3, despite a slight uptick from the flash estimate.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted the manufacturing sector is prolonging its drawn-out recession into April." He highlighted the significant downturn in new orders, which he described as "a rapid decline unmatched in speed over the past four months and devoid of international support." De la Rubia also pointed out the concerning trends in the capital goods sector, which is usually a bellwether for broader industrial health but has been "hit particularly hard" in the current cycle.

Spain stands out as an anomaly within the Eurozone, continuing to demonstrate economic resilience with sustained growth in its manufacturing sector. This divergence is notable, especially against the backdrop of more subdued economic performances in other major Eurozone economies like Germany, France, and Italy, which have failed to gain similar momentum.

Swiss CPI rises to 1.4% yoy in Apr, above expectations

Swiss CPI rose 0.3% mom in April, above expectation of 0.2% mom. CPI core (excluding fresh and seasonal products, energy and fuel) rose 0.4% mom. Domestic products prices rose 0.1% mom. Import products prices rose 1.1% mom.

Over the 12 month period, CPI accelerated from 1.0% yoy to 1.4% yoy, above expectation of 1.1% yoy. CPI core increased from 1.0% yoy to 1.2% yoy. Domestic products price growth rises from 1.7% yoy to 2.0% yoy. Imported products prices contraction lessened from -1.3% yoy to -0.4% yoy.

Also from Switzerland, retail sales fell -0.1% yoy in March, versus expectation of 0.2% yoy rise. PMI manufacturing fell sharply from 41.4, well below expectation of 45.8.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9176; (R1) 0.9207; More....

Intraday bias in USD/CHF remains neutral for the moment. Further rally is still in favor as long as 0.9087 support holds. On the upside, above 0.9223 will resume larger rally to 0.9243 resistance. Decisive break there will carry larger bullish implication. However, firm break of 0.9087 will indicate rejection by 0.9243 and turn bias back to the downside 0.9009 support instead.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8884 resistance turned support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | -0.20% | 14.90% | 15.90% | |

| 23:50 | JPY | Monetary Base Y/Y Apr | 2.10% | 1.70% | 1.60% | |

| 23:50 | JPY | BoJ Meeting Minutes | ||||

| 01:30 | AUD | Building Permits M/M Mar | 1.90% | 3.20% | -1.90% | -0.90% |

| 01:30 | AUD | Trade Balance (AUD) Apr | 5.02B | 7.37B | 7.28B | 6.59B |

| 05:00 | JPY | Consumer Confidence Apr | 38.3 | 39.5 | 39.5 | |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | -0.10% | 0.20% | -0.20% | |

| 06:30 | CHF | CPI M/M Apr | 0.30% | 0.20% | 0.00% | |

| 06:30 | CHF | CPI Y/Y Apr | 1.40% | 1.10% | 1.00% | |

| 07:30 | CHF | Manufacturing PMI Apr | 41.4 | 45.8 | 45.2 | |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 47.3 | 49.8 | 50.4 | |

| 07:50 | EUR | France Manufacturing PMI Apr F | 45.3 | 44.9 | 44.9 | |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 42.5 | 42.2 | 42.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.7 | 45.6 | 45.6 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | -3.30% | 0.70% | ||

| 12:30 | CAD | Trade Balance (CAD) Mar | -2.3B | 1.0B | 1.4B | |

| 12:30 | USD | Trade Balance (USD) Mar | -69.4B | -69.3B | -68.9B | |

| 12:30 | USD | Initial Jobless Claims (Apr 26) | 208K | 212K | 207K | 208K |

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.30% | 0.80% | 3.20% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 4.70% | 3.20% | 0.40% | |

| 14:00 | USD | Factory Orders M/M Mar | 1.60% | 1.40% | ||

| 14:30 | USD | Natural Gas Storage | 68B | 92B |

US initial jobless claims unchanged at 208k, vs exp 212k

US initial jobless claims was unchanged at 208k in the week ending April 27, lower than expectation of 212k. Four-week moving average of initial claims fell -3.5k to 210k.

Continuing claims was unchanged at 1774k in the week ending April 20. Four-week moving average of continuing claims fell -4k to 1779k.

USD/JPY Slides – Did Tokyo Intervene?

It has been a remarkable week for the yen, which has exhibited sharp swings throughout the week.

The Japanese yen fell as much as 1% earlier and on Thursday but has pared most of those losses. USD/JPY has risen 0.38% to 155.19 at the time of writing.

In the Asian session, the yen fell as low as 157.55 but then recovered to precisely 153. The reason for the swing is unclear but there are strong suspicions that Japan’s Ministry of Finance (MoF) ordered another round of intervention. Japan’s top currency official, Masota Kanda, refused to comment on whether Japan had intervened. Kanda was also mum about whether there was intervention on Monday, when the yen spiked and fell below the 160 level before recovering.

Money market movements indicate that the MoF did intervene on Monday, selling as much as $35 billion to prop up the yen. The yen’s swings Monday and today could signal that the MoF has targeted 160 as its “line in the sand” for intervention.

Fed holds rates, US dollar slips

There was no surprise from the Federal Reserve which maintained the benchmark rate in the target range of 5.25% to 5.50% on Wednesday. This marked a six straight pause, as Fed Chair Powell was clear that high inflation has delayed rate cuts. The rate statement said that inflation had fallen in the past year but there was a lack of progress towards the 2% inflation target in recent months. At a press conference, Powell said that the Fed was not yet confident that inflation was falling closer to the target.

Consumer inflation has been moving higher and the US economy remains surprisingly strong, which has complicated the Fed’s plan to provide relief to households by lowering rates. Still, the Powell said the next rate move was unlikely to be a hike, which sent the US dollar broadly lower against the majors on Wednesday. The yen soared as much as 3.2% against on the dollar after the rate announcement and closed on Wednesday with gains of 2%.

USD/JPY Technical

- USD/JPY is testing resistance at 155.13. Above, there is resistance at 157.26

- There is support at 152.27 and 150.14