Sample Category Title

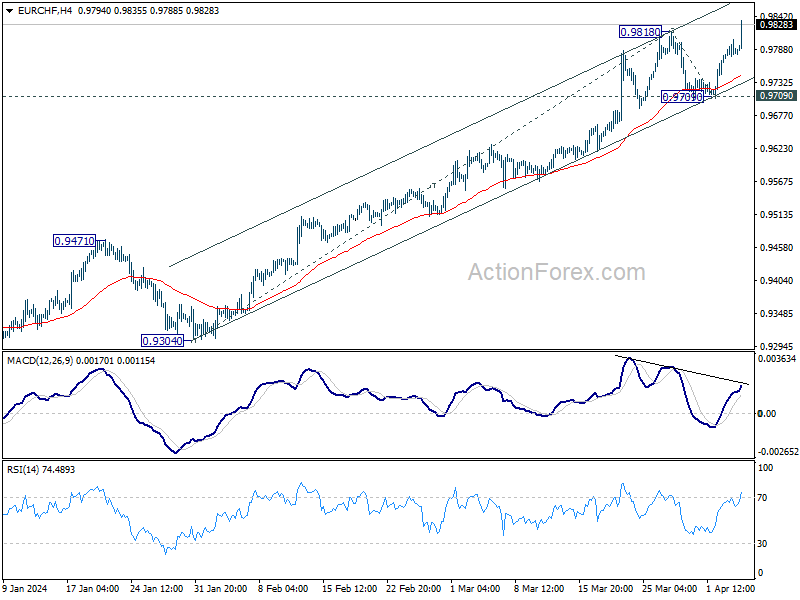

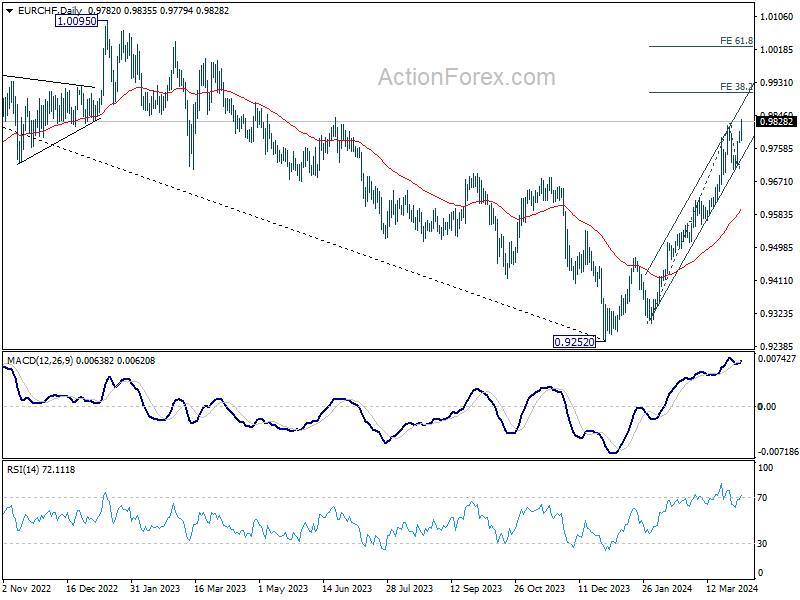

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9766; (P) 0.9786; (R1) 0.9804; More...

EUR/CHF's rally resumed by breaking through 0.9818 resistance and intraday bias is back on the upside. Current rally from 0.9252 would target 38.2% projection of 0.9304 to 0.9818 from 0.9709 at 0.9905. For now, break of 0.9709 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9599) holds.

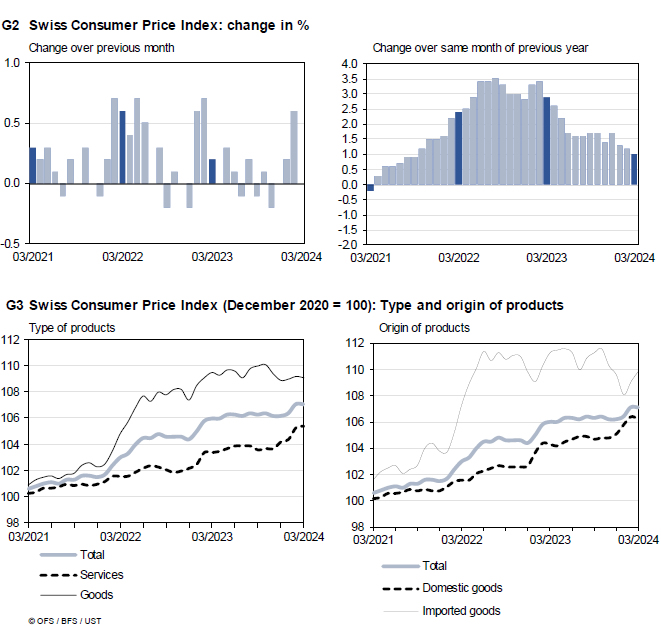

Swiss CPI falls to 1% yoy in Mar, misses expectations

Swiss CPI was flat month-over-month in March, below expectation of 0.3% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices fell -0.2% mom. Imported products pries rose 0.7% mom.

Over the 12-month period, CPI slowed from 1.2% yoy to 1.0% yoy, below expectation of 1.4% yoy. Core CPI slowed from 1.1% yoy to 1.0% yoy. Domestic products prices slowed from 1.9% yoy to 1.8% yoy. Imported products prices fell from -1.0% yoy to -1.3% yoy.

ISM-Inspired Treasury Gains Went Hand-in-hand With Profit Taking on USD Long

Markets

It’s been a rollercoaster ride for US Treasuries so far this week. (Easter) Monday’s consensus-beating, growth-signaling, manufacturing ISM triggered a fierce sell-off. The move continued on Tuesday with rallying oil prices (Brent $90/b; see news & views) continuously adding pressure. Technical support levels (YTD sell-off low) avoided even steeper losses on Tuesday together with a tougher risk climate. The natural drift south re-emerged yesterday even as lower-than-expected March CPI figures (2.4% Y/Y headline; 2.9% Y/Y core) cement the case for a 25 bps June ECB policy rate cut. A stronger March US ADP employment report (+184k) initially did the trick for UST’s. The mirror image in yield terms was a first stay above 4.4% (10-yr) since the end of November last year. Markets were on the edge of clearcut technical breaks, but the March services ISM and Fed Chair Powell’s speech dented enthusiasm. The ISM declined from 52.6 to 51.4 (vs 52.8 consensus). Details showed accelerating business activity (57.4 from 57.2) and strong new (export) orders. Firms shed jobs at a slower pace (48.5 from 48). However, the slowest increase in four years in prices paid (53.4 from 58.6) drew most attention. The ISM warned not to read too much into this move because of rising fuel costs. They release nevertheless proved to be the intraday turning point in yesterday’s trading session with US Treasuries gradually erasing losses afterwards. This comeback gained even more traction after Powell’s comments on the outlook. He stuck with his view that recent data do not materially change the overall picture which continues to be one of solid growth, a strong but rebalancing labor market and inflation moving down to 2% on a sometimes bumpy path. The Fed is still on track to lower the policy rate at some point this year, but Powell still needs greater confidence that inflation is moving sustainably down towards 2% suggesting that the central bank has time to let incoming data guide the decision. The well-known tune without additional hawkish accents were sufficient for US Treasuries to move all the way back to opening levels. Daily changes on the US yield curve ranged between -1.6 bps (2-yr) and +1.2 bps (30-yr). German yield changes varied between +1.4 bps (2-yr) and -0.9 bps (30-yr). This morning, we see US Treasuries drifting south again. The eco calendar contains several speeches from Fed members and weekly jobless claims. The final say – also on potential technical breaks – will be for US payrolls tomorrow and US CPI inflation next week Wednesday.

The dollar already bumped into resistance on Tuesday (DXY YTD high at 105; USD/JPY 152; EUR/USD low 1.07). The ISM-inspired Treasury gains went hand-in-hand with some profit taking on USD long positions. DXY fell from 104.70 towards 104.25 with EUR/USD closing at 1.0836 from an open at 1.0770. Main European and US markets stock markets ended with gains of up to 0.5%.

News & Views

OPEC+ yesterday decided to keep its policy of supply cuts unchanged. About 2mn b/d of output cuts will be prolonged until the next meeting in June (1st). The committee welcomed pledges from Iraq and Kazakhstan to achieve full conformity as well as to compensate for overproduction and from Russia that its voluntary adjustments in Q2 will be based on production instead of exports. Countries with outstanding overproduction in Q1 will submit detailed compensation plans by April 2024. The Committee will closely assess market conditions and noted readiness of participants to take additional measures at any time. The oil price yesterday extended its rebound with Brent crude almost touching the $90/b barrier as investors see a further tightening of the supply-demand balance.

The second round of the Slovak presidential elections take place this weekend. After an undecided first round, a final run-off takes place between Peter Pellegrini, an ally of Prime Minister Fico and Ivan Korcok, who disagrees with the euro-sceptic stance of PM Fico and Pellegrini. Korcok surprisingly won the first rate (42.5% of votes) with Pellegrini securing 37%. Most recent polls show that the outcome might be a very close call between the two contenders, with surveys showing no statistically relevant difference between support for the two contenders.

Euro, Sterling Bears Bulldozed by Fed Doves

Federal Reserve (Fed) Chair Jerome Powell reiterated yesterday that the Fed is not in a rush to cut rates but that it will cut sometime this year and that the recent jump in inflation didn’t ‘materially’ change their policy outlook. The latter was enough to send the market higher with joy.

On the data front however, the data painted another picture. The ADP printed 184’000 new private job additions in the US – higher than expected, while the ISM non-manufacturing activity expanded – with however lower-than-expected employment and price components (supportive of dovish Fed). Yet, earlier this week, the ISM’s manufacturing index jumped into the expansion zone and prices accelerated faster, and the Atlanta Fed’s GDPNow forecasts points at a first quarter growth of 2.8%.

The Fed may not feel in a hurry to cut rates, but investors think that it should be if it doesn’t want to be part of the November’s election story. So the challenge is big: either the Fed will cut by early summer and take the risk of seeing inflation pick up further into the year end, or it will wait until after the election and take the risk of imposing an otherwise unnecessary pressure on the economy. To make things easy, we will say that the data will decide. But the markets don’t react fully to the data when the Fed members continue to keep the dovish talk on the table. And those who tell otherwise go unheard. Fed’s Raphael Bostic said that he expects just one rate cut this year – after the election. Did anyone hear that?

The US 2-year yield eased yesterday as Powell stressed out that the recent rise in inflation doesn’t ‘materially’ change the way the Fed sees things – three rate cuts this year as per their latest dot plot – and the 10-year yield eased to 4.36%. The US dollar index sharply retreated and the S&P500 rebounded. Semiconductors came under pressure after a strong earthquake hit Taiwan and brought TSM to halt its operations on the island. But TSM said it will resume operations quickly as their critical tools have not been damaged.

Up next, investors will be watching the weekly jobless claims and job cuts as they wait for Friday’s jobs data.

Euro, sterling bears bulldozed by Fed doves

The sharp decline in the US dollar sent the EURUSD sharply higher yesterday. The pair made a quick move to 1.0845 after testing the 1.0740 level at the start of the week/quarter. But fundamentally, the data was supportive of the euro bears. Inflation in the Eurozone eased more than expected and the unemployment rate remained steady at 6.5% versus an improvement to 6.4% expected by analysts. The data clearly cemented the expectation of a June rate cut from the European Central Bank (ECB), but couldn’t give the euro bears enough leverage to fight back the US dollar shorts.

Across the channel, the Bank of England (BoE) doves are also gaining the upper hand on the Fed. According to Bloomberg, the probability of a BoE rate cut stood at 67% yesterday, versus just 57% for the Fed. But you couldn’t see that pricing on Cable chart, where the pair rebounded in a sharp move due to the US dollar weakness. But keeping the economic data in perspective, it makes more sense selling the tops in both the euro and sterling against the greenback than buying the dips.

Oil, Gold gain

US crude’s rally accelerated after clearing the $85pb level, the barrel of US crude traded at $86.50pb after OPEC confirmed to maintain supply cuts in place. The US oil inventories on the other hand jumped more than 3 mio barrels last week. Note that we could’ve seen a test of the $85pb resistance and a correction because the extension of OPEC cuts were already made public, and because US oil inventories rose more than expected, but the market decided to carry the oil rally higher, confirming that the trend is strongly on the bulls’ side. As such, oil rally certainly has more room to extend toward the $88-90pb range. We could see minor downside correction due to overbought levels.

In precious metals, gold exceeded the $2300 yesterday on the back of softer US dollar and the falling US yields. Some investors seek refuge in the safe-haven gold as the geopolitical scene remains tense and the sustainability of the equity rally is questioned. But note that trend and momentum indicators warn that gold has been bought too rapidly in a too short period of time and that the overbought conditions could trigger a minor downside correction. But the trend remains gold traders’ friend.

Rate Decision in Poland

In focus today

- In the euro area, we receive February PPI data.

- In Poland, the Polish central bank wraps up its two-day monetary policy meeting. We expect an unchanged policy rate at 5.75%, in line with consensus.

- In Switzerland, inflation for March is published at 8.30 CET.

- In Sweden, Riksbank Minutes are released 09.30 CET. Hopefully, we will receive information about the individual preferences of board members about the timing of the first rate cut. Also, Riksbank Governor Bunge speaks 13.30 about the corporate bond market.

- In Japan, we get the third wage tally from the biggest labour union, Rengo. We will look for further clues to what extent, wage growth in big business has rubbed off on the SME segment.

Economic and market news

What happened yesterday

In the US, the ADP employment report came in higher than expected at 184k (cons: 148k). The Leisure & Hospitality sector accounted for the largest share of job gains (+63k), supporting the narrative of a supply-driven recovery. On the other hand, ISM services came in below expectations, printing 51.4 (cons: 52.7). Sub-components painted a mixed picture as business activity remains upbeat, but leading new orders and prices indices declined. The employment index remains below 50, as was the case in the manufacturing report as well.

Moreover, Fed Chair Powell emphasized that the Fed's task of bringing down inflation was "not yet complete," stressing the necessity for additional data confirming sustainable progress toward the 2% target before cutting rates. Regarding recent data, Powell remarked that it did not "materially change the overall picture." The Fed Chair also announced that the Fed would initiate a new review of its monetary policy framework this year.

In the euro area, HICP inflation declined in March to 2.4% y/y (cons: 2.5%), while core inflation declined to 2.9% y/y (cons: 3.0%). Service inflation remains sticky around 4.0% for the fifth consecutive month, while core goods inflation continues lower. Overall, the print is positive news for the ECB, however we continue to believe that the ECB will wait until the June meeting before delivering its first rate cut. For instance, the timing of Easter seems to have impacted inflation less than expected in March, and since Easter also spans April, we could see some effects in the April print.

Euro area unemployment rate was unchanged in February at 6.5% following an upward revision of the January number to 6.5% from 6.4%. Hence, the labour market is still very strong despite the stagnating economy.

Yesterday, we published a research piece on euro area productivity growth compared to the United States. The chronic underperformance of euro area productivity growth compared to the US over the past three decades is glaring. We expect weak euro area productivity relative to the US to continue. Continued weak productivity implies a structurally lower EUR/USD and lower ECB policy rates. For more details, see Research euro area: Euro area productivity will keep falling behind, 3 April.

In commodities, OPEC+ signalled that it would keep its oil output policy unchanged and further work on improving compliance, while Brent crude crept closer to USD90/bbl. Additionally, gold prices reached an all-time high around USD2300.00 per troy ounce during yesterday's session.

Equities: Global equities were higher yesterday as two sets of pleasant inflation-related data temporarily calmed the fear of overheating, and bond yields flatlined. However, energy and materials still outperformed as these sectors are the biggest beneficiaries of improved manufacturing outlook and higher goods related prices. In the US yesterday, Dow -0.1%, S&P 500 +0.1%, Nasdaq +0.2% and Russell 2000 +0.5%. The positive manufacturing-related sentiment has carried over to Asia this morning with Japan and South Korea higher while China is standing out on the negative side. European and US futures are higher this morning.

FI: Long-end EGB rates ended close to unchanged in yesterday's session, but the volatility throughout the day was relatively significant. The 10Y Bund yield dipped to 2.36% following the European inflation figures, but the upward US ADP surprise reversed the situation in the afternoon. The level closed unchanged at 2.39%, in line with a largely unchanged 10Y UST yield at 4.36%. The pricing of ECB cuts in 2024 was unchanged at close to 90bp throughout the day.

Spain will tap the 5Y-15Y nominals segment and the 15Y linker, while France will tap in the 5Y+ nominals space. Finland is also active with tap auctions in the 10Y and 20Y segments.

FX: EUR/USD remained relatively stable in yesterday's session until the weaker-than-expected ISM services data initiated lower US rates and a broadly weaker USD, causing EUR/USD to rise to around 1.08. After a very poor March, NOK FX has been off to a strong start to the month with EUR/NOK falling from (close to) 11.80 down to the 11.60-level, driven by the rise in oil prices and the weaker USD. Akin to NOK, SEK strengthened during yesterday's session following the slightly softer US data. EUR/CHF continued its climb higher briefly breaching the 0.98 mark with markets eying the inflation data out this morning.

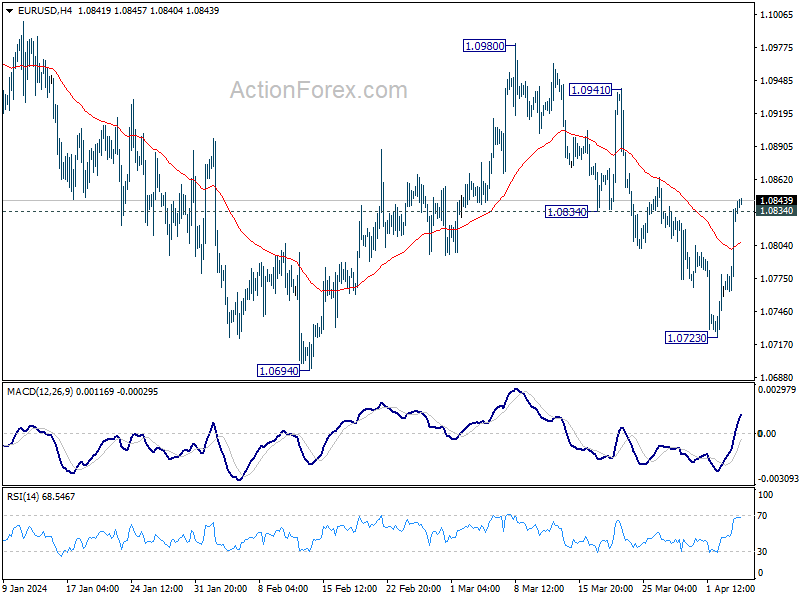

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0812; (R1) 1.0861; More...

Break of 1.0834 support turned resistance argues that fall from 1.0980 has completed with three waves down to 1.0723. Rise from there is currently seen as the third leg of the corrective pattern from 1.0694. Intraday bias is back on the upside for 1.0941/0980 resistance zone. On the downside, though, below 55 4H EMA (now at 1.0807) will bring retest of 1.0694/0723 support zone instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

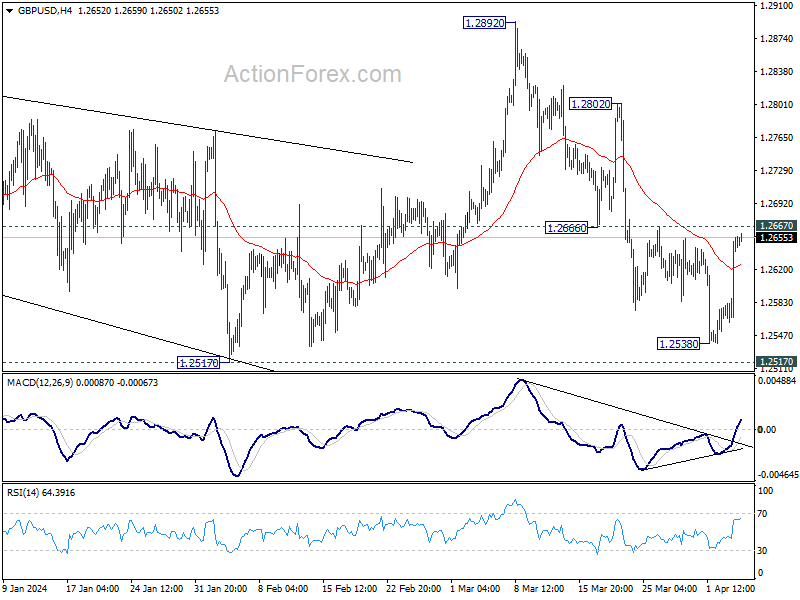

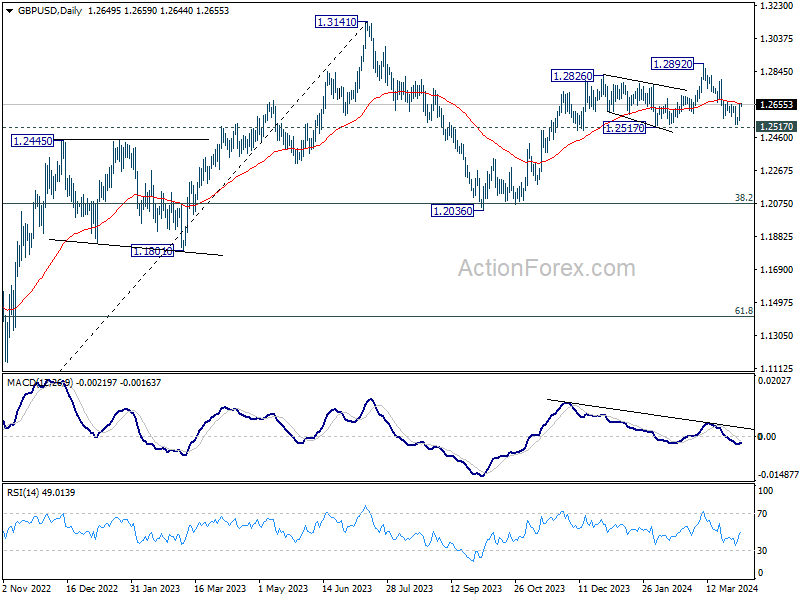

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2624; (R1) 1.2685; More...

Intraday bias in GBP/USD stays neutral first, and risk remains on the downside with 1.2667 resistance intact. Below 1.2538 will target 1.2517 structural support. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish. However, firm break of 1.2667 will turn bias back to the upside for stronger rebound towards 1.2802/2892 resistance zone instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

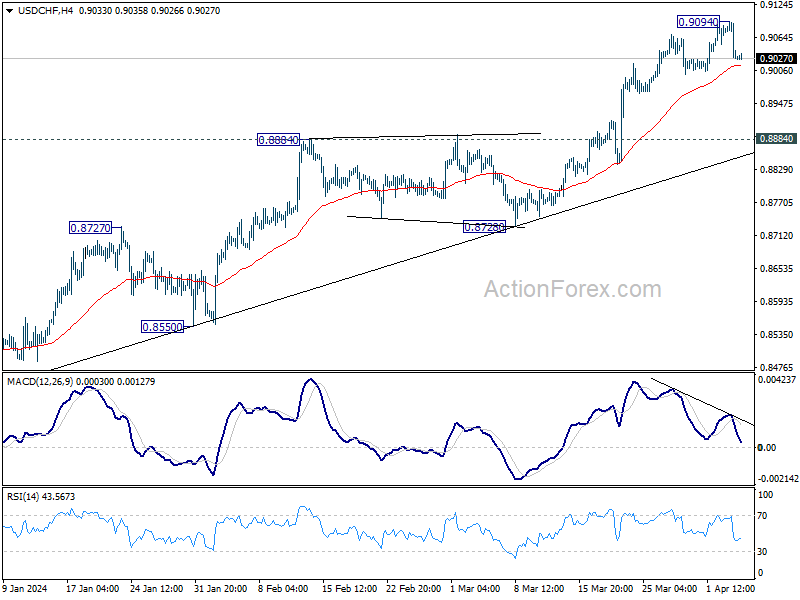

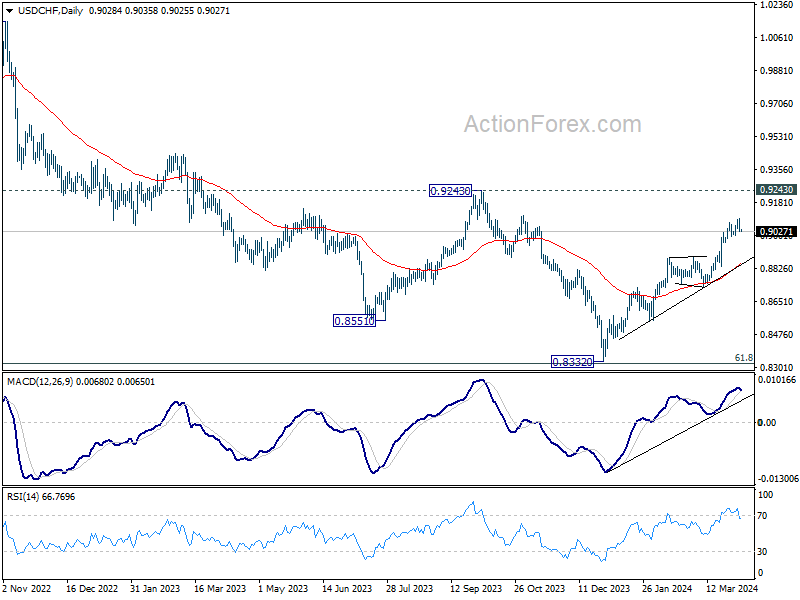

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9005; (P) 0.9050; (R1) 0.9074; More....

Intraday bias in USD/CHF is turned neutral with current retreat. On the downside, break of 55 4H EMA (now at 0.9016) will bring deeper pullback. But downside should be contained by 0.8884 resistance turned support to bring rebound. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

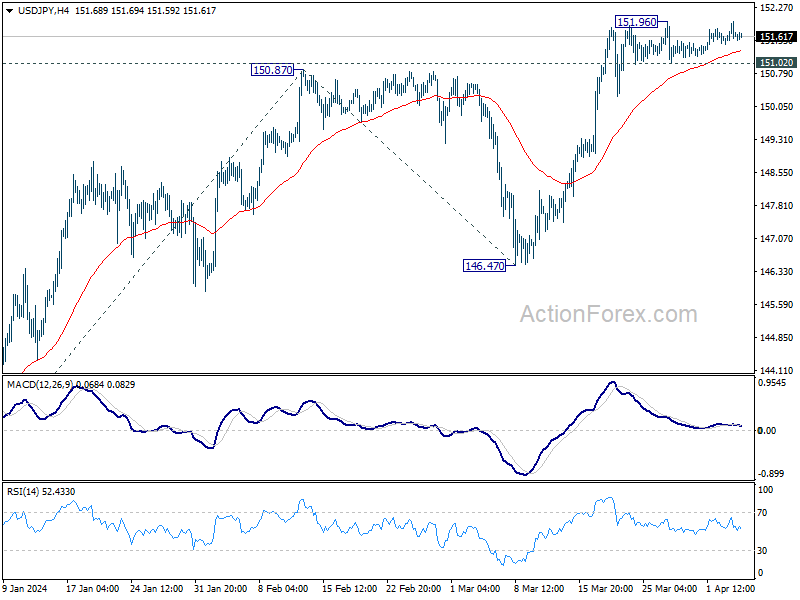

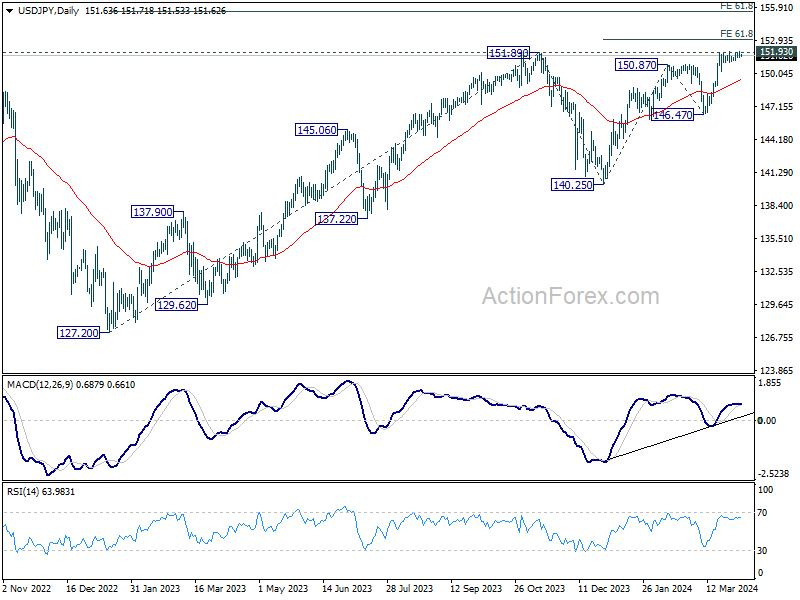

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.44; (P) 151.70; (R1) 151.96; More...

Intraday bias in USD/JPY remains neutral for the moment as range trading continues. On the downside, break of 151.02 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.51). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3496; (P) 1.3543; (R1) 1.3573; More...

Range trading continues in USD/CAD and intraday bias stays neutral at this point. On the upside, decisive break of 1.3612 resistance will resume whole rise from 1.3176 towards 1.3897 resistance. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.