Sample Category Title

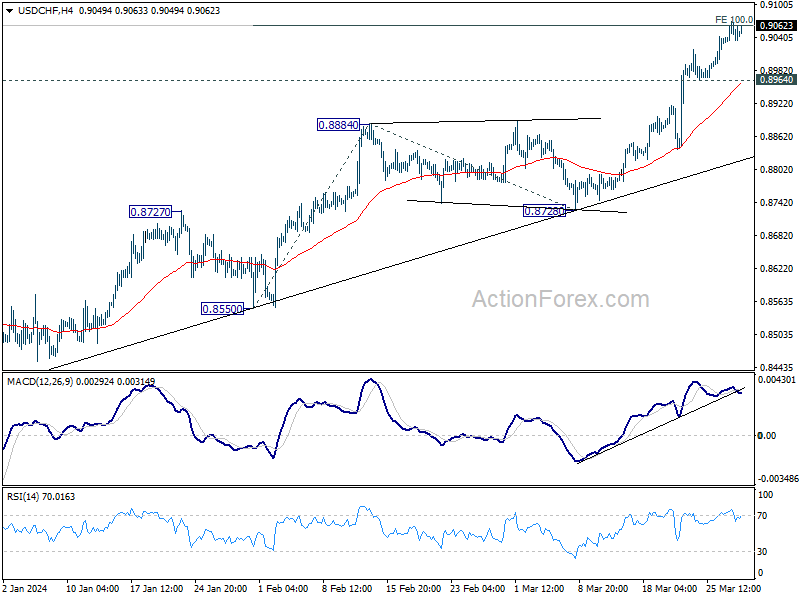

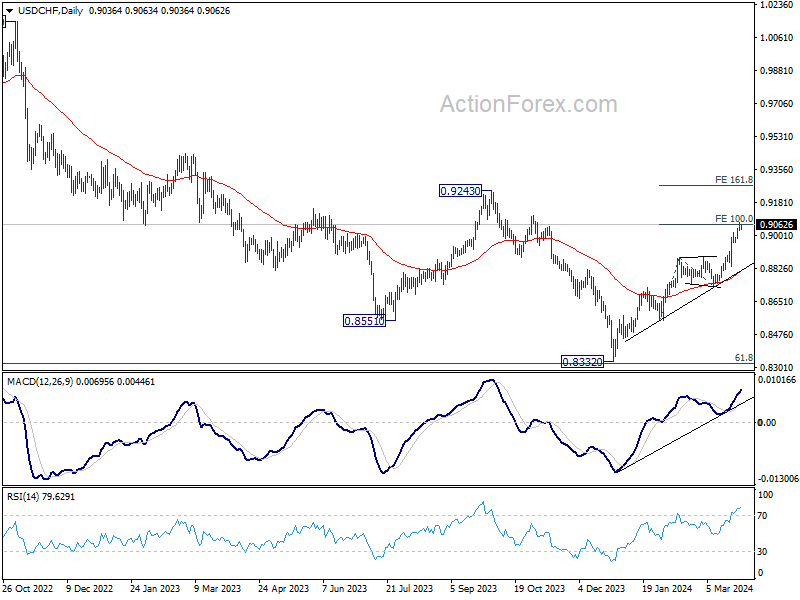

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9019; (P) 0.9046; (R1) 0.9064; More....

Intraday bias in USD/CHF remains on the upside at this point. Sustained trading above 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062 will target 0.9243 key medium term resistance next. On the downside, below 0.8964 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 0.8884 resistance turned support holds.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

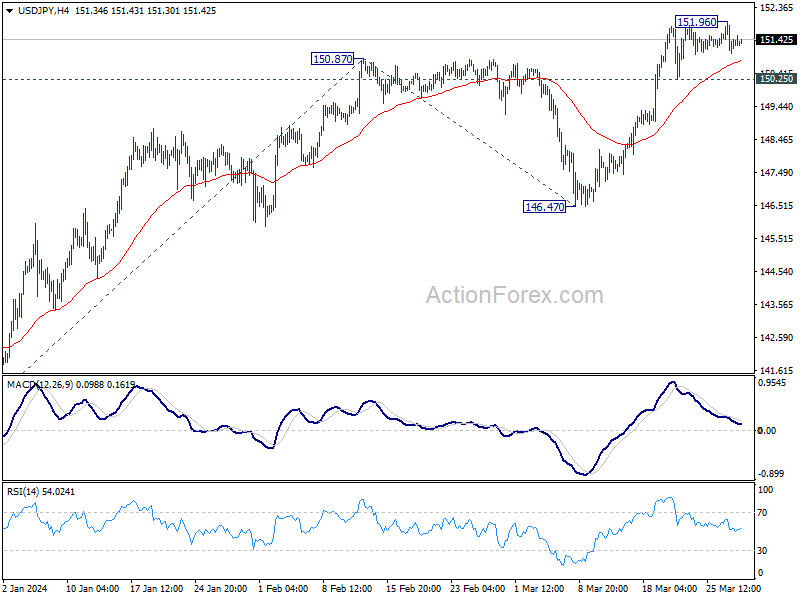

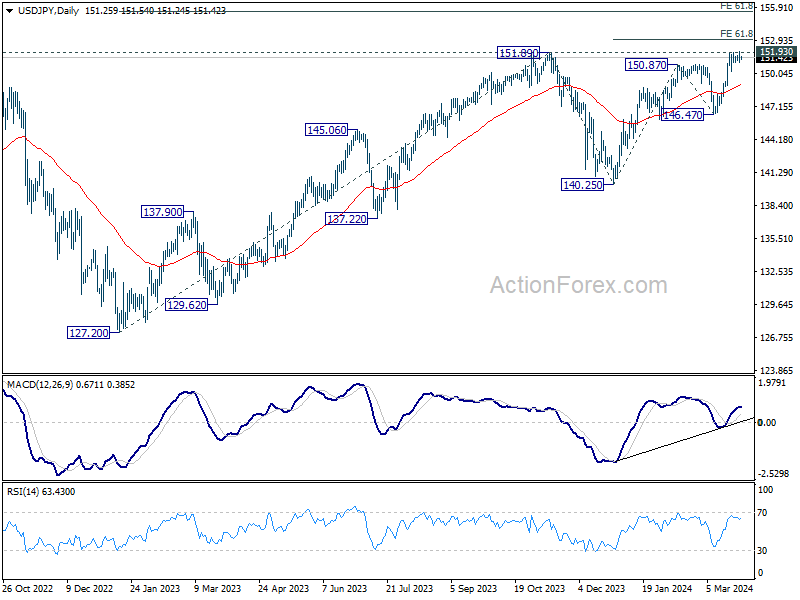

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.91; (P) 151.44; (R1) 151.85; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, break of 150.25 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.01). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

Something Must Give

European stocks renewed record on Wednesday, the US dollar consolidated gains and the S&P500 stocks got a late-session boost. Yesterday’s price action pointed at a possible end-of-quarter portfolio rebalancing as the session saw the laggards of the quarter like Apple and Tesla gain, and the stars like Microsoft and Nvidia retreat. Nvidia fell 2.5% yesterday. Goldman Sachs warned that the pension funds are likely to sell $32bn worth of equities as part of rebalancing. That could have a slowing impact on the equity rally, although the rebalancing act will hardly change the overall market trend given that there is a sizeable amount of cash waiting to flow into equities and bonds. The only thing that investors need is the Federal Reserve (Fed) rate cut dream to stay alive for the June meeting. And for now, that’s the case. Activity on Fed funds futures gives around 64% chance for a June rate cut.

But note that, this probability was around 75% last week and it’s coming lower as many investors think that the Fed won’t be able to cut the rates with robust growth and bumpy inflation. And indeed, the US latest GDP update is due today and is expected to confirm an above 3% growth for the US economy in the last quarter of last year, down from almost 5% printed a quarter earlier. These levels don’t call for an imminent Fed cut. This is perhaps why the US dollar is not willing to give back gains despite a relatively dovish Fed stance. The US dollar index is up by around 1% since the Fed plotted 75bp cut for this year and said that it will also start slowing the pace of QT.

Something must give.

- Either the US dollar should weaken because the Fed is expected to cut three times this year with the first cut due in June - in which case we could continue to see the stock market laggards catch up with the leaders of the past quarters and capital to flow into the other-than-tech sectors as well. And in case of policy easing – as predicted - appetite should also broaden to small and mid cap stocks, to EM funds and to commodities.

- Or the US dollar should continue its recovery on the back of robust data and a pullback in Fed cut expectations, in which case we should see the stocks give back strength.

But both a strong dollar and a stock rally is not sustainable in Q2.

Eurozone economies under pressure, but ECB determined to fight inflation

Higher interest rates and the energy crisis are taking a toll on Eurozone economies. Germany is expected to rise 0.1% this year – it’s more a stagnation than a rise. Slowing Eurozone economies and gloomy growth outlook for the next quarters back a June rate cut from the European Central Bank (ECB), yes, but the ECB says that it won’t commit to other rate cuts beyond June, before making sure that inflation is on a solid path toward the 2% policy target. And indeed, inflation numbers from Spain confirmed a rebound in consumer prices in March as the government continued to remove support that helped tempering the otherwise-unbearable rise in energy prices. So yes, the last mile in reaching the 2% inflation goal is not a given for the European countries either. And that’s certainly why the EURUSD holds ground near the 1.08 level – it’s because the ECB looks determined to continue fighting inflation. But a robust GDP and a hot inflation report could break the back of the EURUSD bulls.

Sumo fight

The sumo fight between the Japanese officials and the yen bears remains intense as the yen bears are testing the Japanese nerves near the 152 level. The threat of FX intervention slows the yen selloff at the current levels, but we saw in the past that the post-intervention effects remain limited when the market is turbocharged with opposite direction trades. Therefore, any pullback in the USDJPY – due to the threat of intervention or intervention – could remain short-lived. A hint of further policy tightening is certainly more effective than costly and barely effective FX threats.

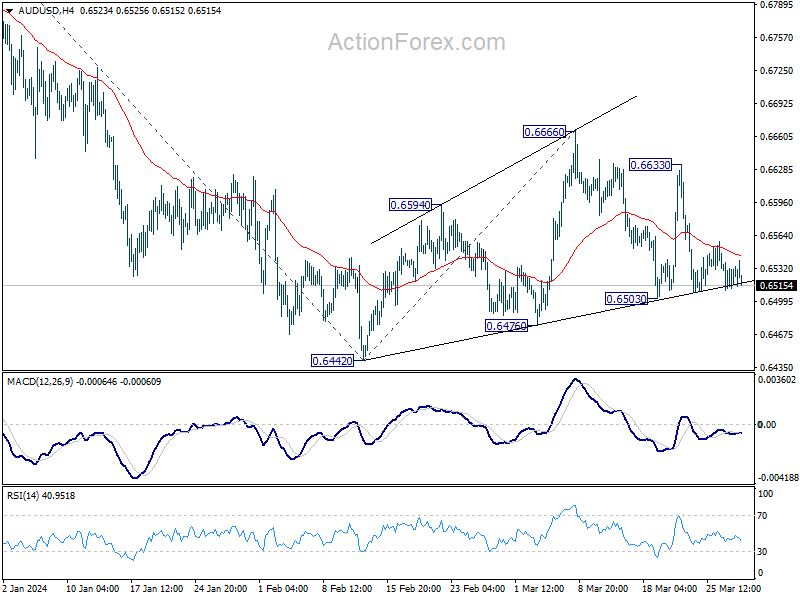

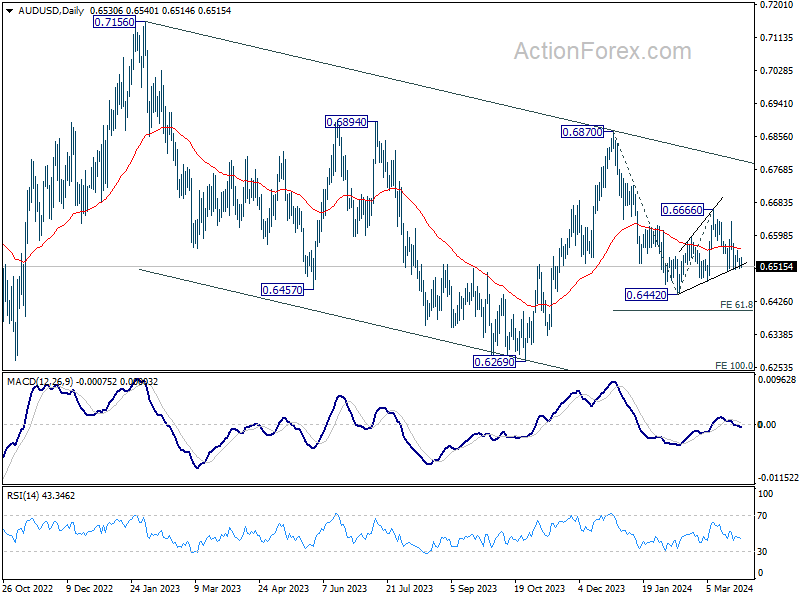

AUD/USD Daily Report

Daily Pivots: (S1) 0.6518; (P) 0.6529; (R1) 0.6545; More....

Intraday bias in AUD/USD remains neutral and outlook is unchanged. Risk will remain on the downside as long as 0.6633 resistance holds. Firm break of 0.6503 support will indicate that larger fall from 0.6870 is ready to resume, and turn bias to the downside for 0.6442 low. For now, risk will stay on the downside as long as 0.6633 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

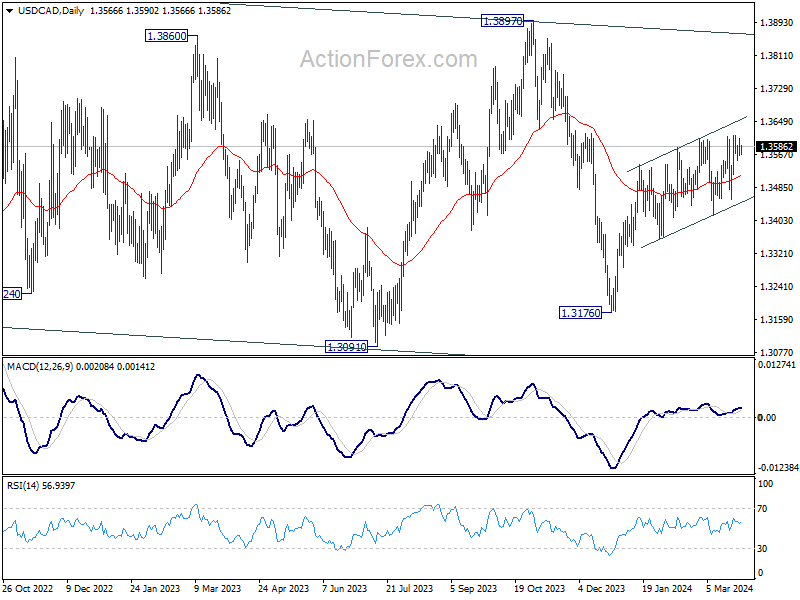

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3552; (P) 1.3580; (R1) 1.3595; More...

Outlook in USD/CAD is unchanged and intraday bias remains neutral. On the upside, decisive break of 1.3612 resistance will resume whole rise from 1.3176 towards 1.3897 resistance. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

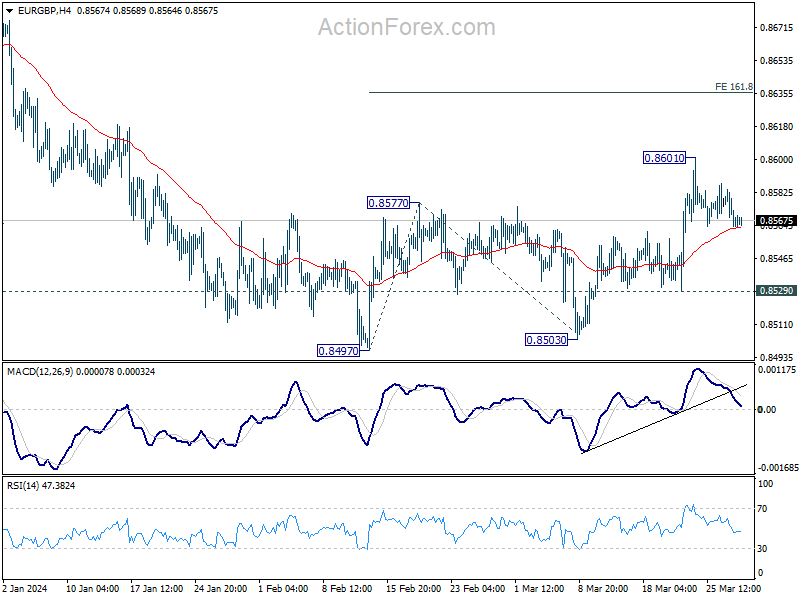

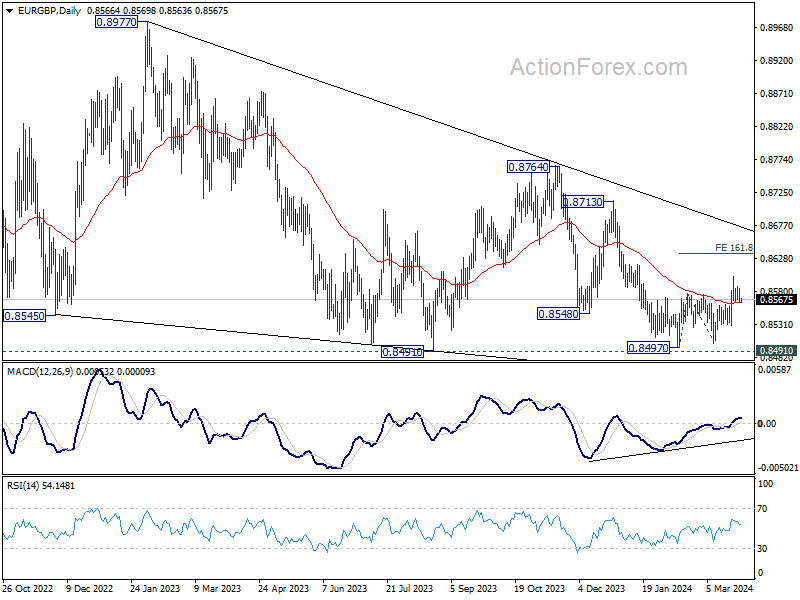

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8559; (P) 0.8572; (R1) 0.8579; More...

Intraday bias in EUR/GBP remains neutral for the moment. With 0.8529 support intact, further rally is in favor. Rebound from 0.8497 is seen as at least correcting the fall from 0.8764. Above 0.8601 will target 161.8% projection of 0.8497 to 0.8577 from 0.8503 at 0.8632.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

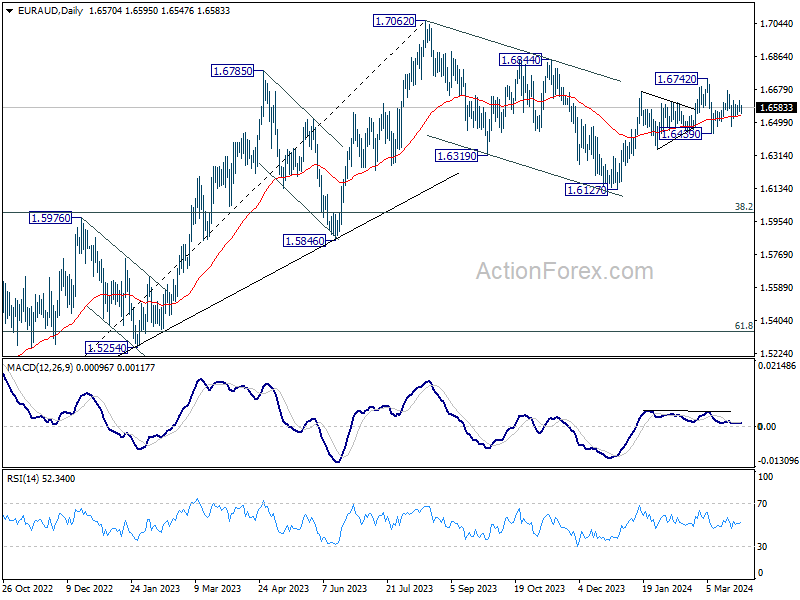

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6547; (P) 1.6585; (R1) 1.6608; More...

EUR/AUD is extending consolidation from 1.6742 and intraday bias stays neutral. Near term outlook will remain cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

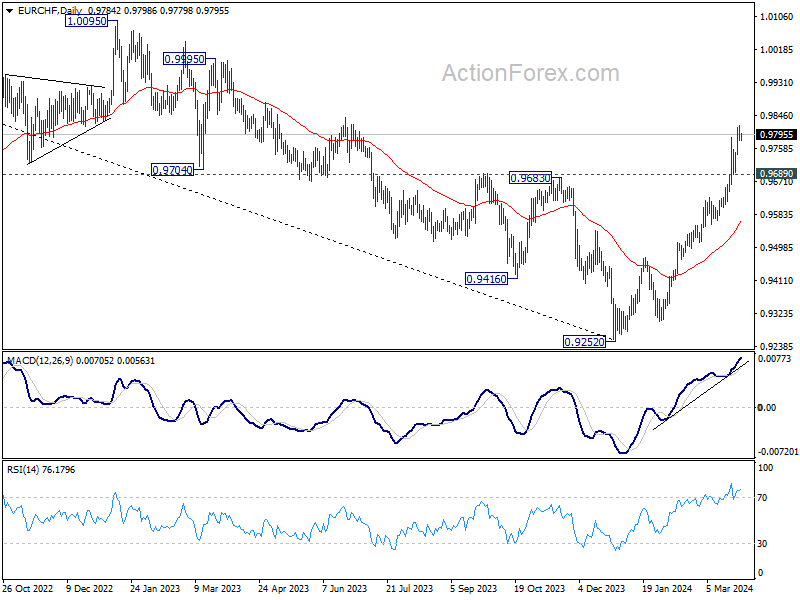

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9771; (P) 0.9796; (R1) 0.9810; More..

Intraday bias in EUR/CHF remains on the upside for the moment. Rise from 0.9252 is in progress towards 1.0095 key resistance next. On the downside, break of 0.9689 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9535) holds.

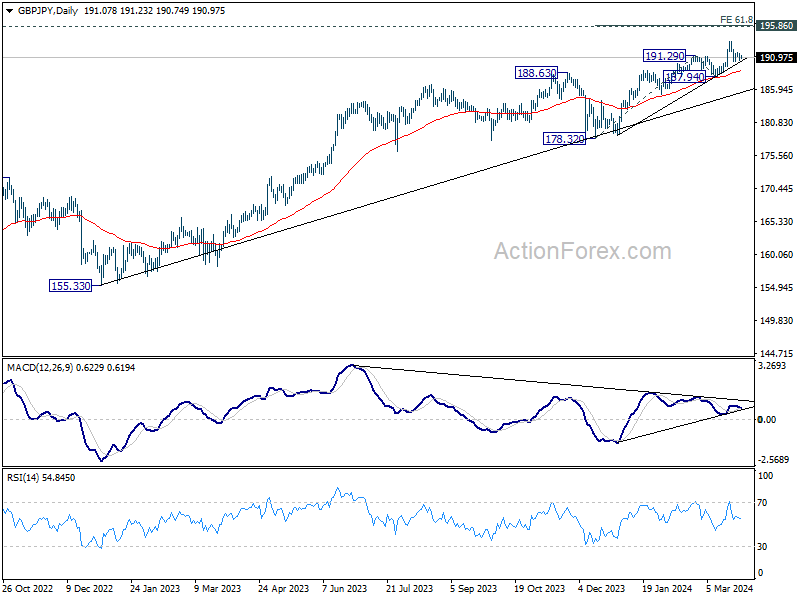

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.59; (P) 191.07; (R1) 191.62; More.....

Intraday bias in GBP/JPY remains neutral as consolidation continues below 193.51. Outlook will stay bullish as long as 187.94 support holds. On the upside, break of 193.51 will resume larger up trend to 61.8% projection of 178.32 to 191.29 from 187.94 at 195.95, which is close to 195.86 long term resistance.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

Cliff Notes: Opinions on the State of the Economy

Key insights from the week that was.

This week, Westpac surveys provided insight into both the current conditions and outlook faced by consumers and manufacturers. The Monthly CPI Indictor and job vacancies subsequently provided more evidence of the persistence of Australia’s disinflationary trend.

Westpac-MI Consumer Sentiment's March survey signalled that consumers remain very concerned over their family finances, with headline confidence 16% below average at 84.4, little changed from 2023’s average of 80.9. Unsurprisingly, the underlying pulse of nominal retail sales remains weak and ‘time to buy a major household item’ assessments from the Westpac-MI suggests this trend will persist for some time.

Elements of the survey are showing tentative signs of promise though. The RBA’s more balanced commentary looks to have had a positive impact, as evinced by the rise in sentiment between those surveyed before the policy meeting (79.3) and after (94.9). Westpac-MI mortgage rate expectations also eased. That said, few consumers believe rate cuts are imminent.

The Q1 Westpac-ACCI Survey of Industrial Trends provided a timely perspective on the state of the economy from the perspective of manufacturers. Respondents were deeply pessimistic on the general business outlook, a view reinforced by the deterioration in new orders (from flat to declining) and a corresponding fall in output in the quarter. In response to a prolonged period of acute cost pressures over 2022 and 2023, manufacturers are reporting a reduction in both overtime and employment in 2024. The sector is keenly awaiting a less restrictive policy stance. Though, as rate cuts are likely to proceed slowly from September, it may be some time before manufacturers feel material benefit.

At least the other data released this week was consistent with steady progress towards the RBA’s inflation goal.

The Monthly CPI Indicator rose a benign 0.2% in February, leaving the annual rate unchanged at 3.4%yr for a third consecutive month. Trimmed Mean inflation ticked a little higher, from 3.8%yr to 3.9%yr; though the headline index excluding volatile items and holiday travel managed to move lower, from 4.1%yr to 3.9%yr.

Services inflation was a focus as this month’s release provided the quarterly update on prices in this category of spending, giving an idea of the risks surrounding the Q1 CPI report. We view these risks as balanced, the lift in services inflation (3.7%yr to 4.2%yr) due to a stronger increase in education costs being largely offset by softer electricity and holiday travel prices (both monthly surveys). Hence, we have retained our forecast of 0.7% (3.4%yr) for Q1 CPI and continue to expect inflation to reach the top of the target range by the end of the year.

On the labour market, job vacancies were reported to have fallen 6.1% between November and February, a pace of decline more in line with the average seen in the middle of 2022. The survey was consistent with other data. Labour demand is moderating in response to the broadening economic slowdown, but there remains a substantial ‘overhang’ of vacancies relative to pre-pandemic levels. This is in line with our expectation for a continued deceleration in jobs growth through 2024, albeit while avoiding outright national declines in employment. On the labour market, Chief Economist Luci Ellis’ essay this week explores productivity dynamics during and after the pandemic.

Offshore, markets took a breather in the absence of top-tier data.

In the US, total durable goods orders rose 1.4% in February thanks to orders for new non-defence transport equipment, particularly aircraft. Elsewhere in manufacturing, conditions are much weaker, core goods shipments and orders only marginally higher year-to-date.

The March regional Fed surveys also point to downside risks for activity ahead. The Richmond Fed Index declined to –11, with pessimism in new orders and the order backlog of note, while the Dallas Fed index fell to –14.4. The Dallas Fed’s ‘average employee work week’ and employment components point to businesses in the region dealing with softening demand by cutting hours instead of laying off staff. Expectations of a soft landing should limit downside risks for employment over the year ahead.