Sample Category Title

Inflation Still Matters for ECB

- The eurozone inflation report for February on the menu this week

- Most ECB members worry about the growth outlook after the mixed PMIs

- The euro continues to suffer again against the pound

- German CPI will be published on Thursday; Eurozone on Friday 10:00 GMT

With global stock markets attracting lots of interest due to their consecutive all-time highs, the countdown to the March 7 ECB meeting has commenced. This gathering is considered to be a key one as, apart from the overall rhetoric that could shape market expectations, the updated quarterly staff projections could lay the path for a more accommodative monetary policy stance for the rest of 2024.

The usual “quiet period” for ECB members has started with both the hawks and the doves trying to set the basis for the upcoming closed-doors discussion in Frankfurt. Most members agree that the next move will probably be a rate cut but there is an open debate on the actual announcement date. The doves are pushing for a move as early as possible, even in March, while the hawks preach patience.

The weak growth outlook creates worries at the ECB

Since price stability is the ECB's only target, this week’s inflation report will be closely scrutinized. However, there appears to be a growing concern, especially among ECB doves, about the growth outlook. Last year was a challenging one with the eurozone avoiding technical recession on the back of the stronger Italian and Spanish growth levels. In the meantime, German growth remains a serious problem for the ECB.

The preliminary PMI surveys for February, which were released last week, probably depict accurately the current mixed growth picture across the euro area states. The French PMI figures managed to produce sizeable upside surprises with the manufacturing component jumping to an 11-month high.

On the contrary, the German PMI manufacturing survey disappointed as it dropped again with the recent farmers’ protests probably impacting heavily on this result. Nevertheless, it remains at an extremely low level, confirming the current weak economic momentum in Germany, after a very weak 2023, possibly amplified by the 2024 budget shenanigans.

German and eurozone CPIs are expected to ease further

Returning to inflation and the preliminary CPI report for February will be published this week. On Thursday, we will get the German and French figures with the eurozone aggregate print coming on Friday. The German headline CPI is expected to further slow to 2.6% year-on-year change, which if confirmed, will be the lowest annual increase since June 2021, almost three years ago.

Similarly, the eurozone headline CPI figure is seen dropping to 2.5%, cancelling out the last two months’ pickup in inflation. More importantly, the focus would be on the core indicator as this has proved stickier lately. Economists are looking for a 2.9% print, a level that is unlikely to please certain ECB doves looking for a rate move as early as in March.

Should inflation confirm expectations, the ECB doves will try to get an agreement at the March meeting on the date of the first rate cut. However, stronger inflation this week along with the weak growth outlook means that stagflation will continue to describe the current eurozone situation. This will most likely deepen the developing rift in the ECB ranks as the hawks will most likely resist any rate cut discussion.

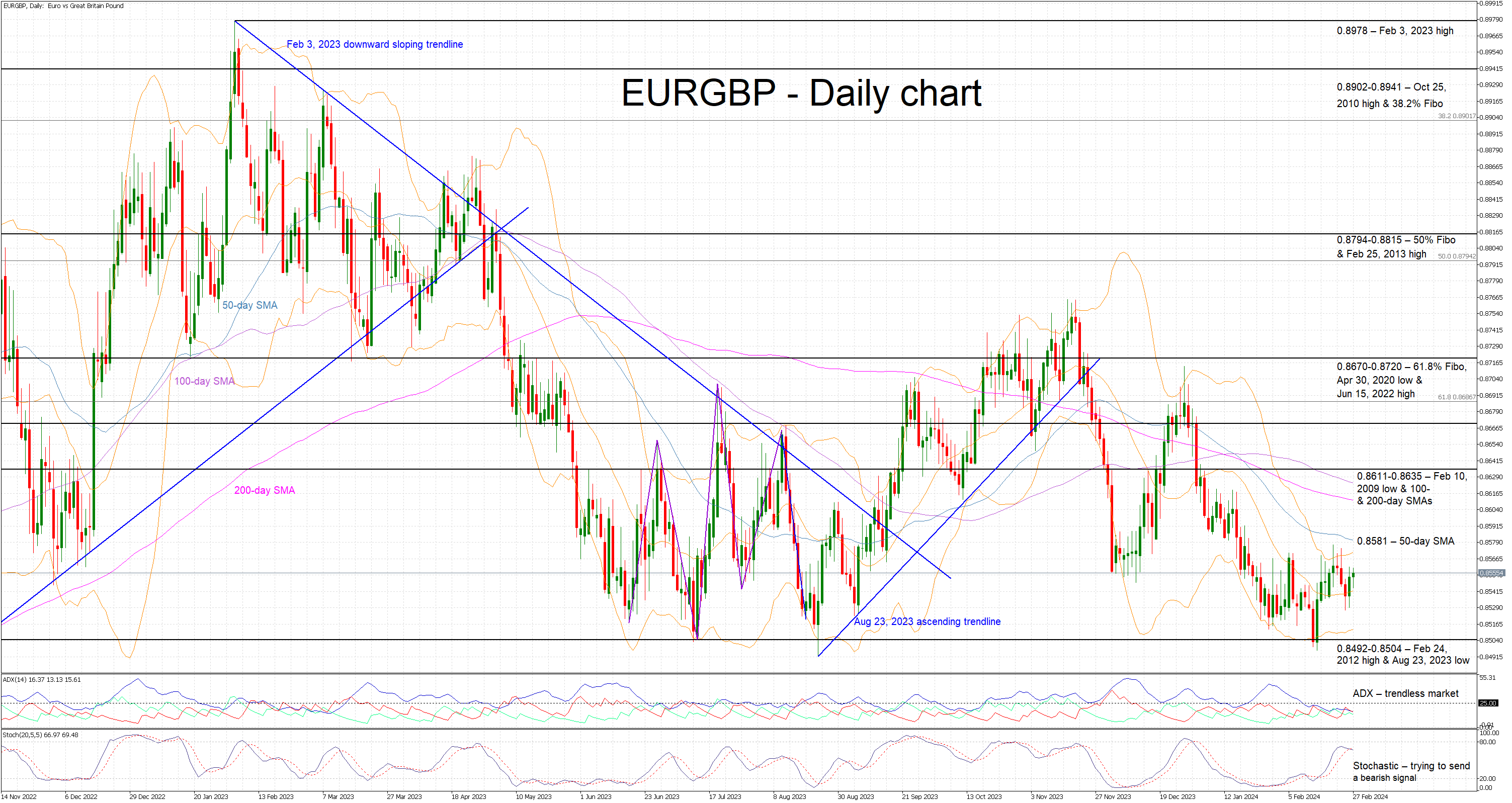

Euro remains on the backfoot against the pound

Last week’s data releases highlighted the fact that there is an economic divergence developing between the UK and the eurozone. This is also depicted in the euro/pound pair remaining near its 2024 low and validating the recent bearish trend.

A stronger set of inflation figures this week could lead the euro/pound pair higher with the 0.8581 level being the first plausible target. On the flip side, a plethora of downside surprises could reignite the market expectation for a more aggressive rate cut cycle by the ECB. Such an outcome could increase the current downside pressure with euro/pound moving lower and potentially retesting the recent 0.8497 low.

EURJPY Falls Slightly After Meeting 3-Month High

- EURJPY creates bullish tendency in short- and long-term timeframes

- RSI indicates potential downside retracement

EURJPY is retreating somewhat after the aggressive buying interest towards the three-month high of 163.70. The price has been developing an upward trend since the rebound off the 153.15 support level confirming the bullish bias in the short- and long-term pictures.

Technically, the RSI indicator is pointing slightly down after it jumped above the 70 level; however, the MACD oscillator is still pointing to strengthening momentum above its trigger and zero lines.

If the market extends its upside move above the previous high, then it may reach the 164.30 resistance, taken from the peak on November 16. Surpassing this line, there is lot of room until the next resistance line at 170.00, registered in May 2008, so traders need to be cautious for the psychological levels between 164.00 and 170.00.

On the flip side, a bearish move could find immediate support at 161.85 ahead of the 20-day SMA at 161.25. Even lower, the market may retest the near-term rising trend line near the 160.25 barricade. A successful attempt to break beneath this line could open the way for a negative correction until the 50-day SMA at 159.65 and the long-term ascending trend line at 158.00.

To sum up, EURJPY seems bullish in all timeframes and only a drop beneath the 200-day SMA at 157.75 may change this outlook to bearish.

NZIER forecasts no further RBNZ hike, eyes mid-2025 cuts

In its latest Quarterly Predictions, NZIER noted there are "signs of further easing in inflation pressures" in New Zealand. But the pivotal question for RBNZ is whether this easing is "occurring at a fast enough pace" to bring inflation back to target band of 1-3%.

"Based on the balance of risks, we expect "no further OCR increases in this cycle," NZIER said.

Highlighting the New Zealand economy's "resilience," NZIER acknowledges the potential for inflation to persist above RBNZ's target, suggesting a "cautious approach" from the central bank, gearing towards understanding the "lag effects of the monetary policy tightening" already implemented.

Meanwhile, NZIER forecasts RBNZ OCR cuts to start mid-2025, "once it is confident it has reined in inflation sufficiently to keep it around the 2 percent inflation target mid-point over the coming year."

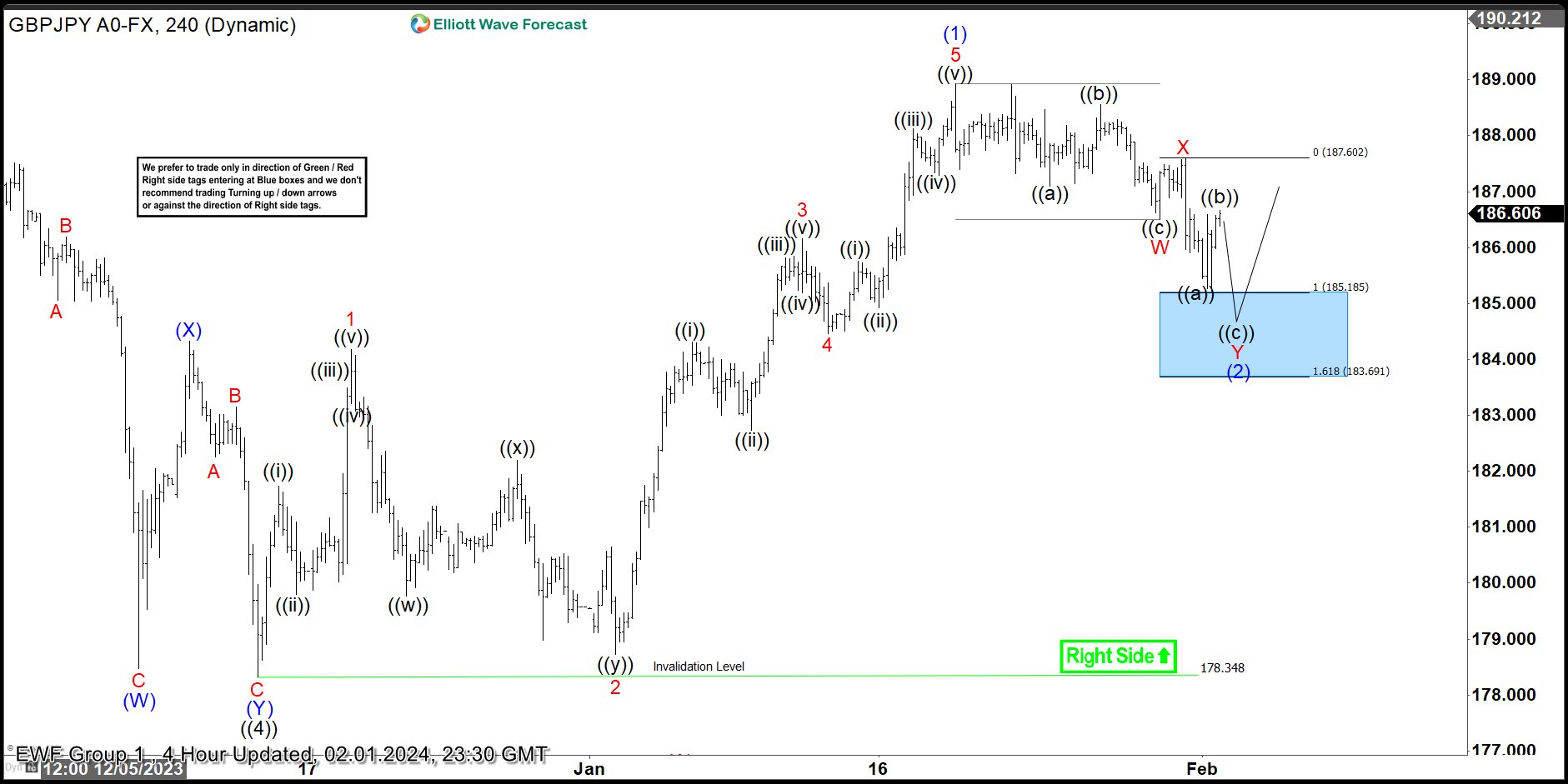

GBPJPY Perfect Reaction Higher From Blue Box Area

In this technical blog, we will look at the past performance of the 4-hour Elliott Wave Charts of GBPJPY. In which, the rally from 13 December 2023 low unfolded as an impulse sequence and called for an extension higher to take place. Therefore, we knew that the structure in GBPJPY should remain supported & extend higher. So, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

GBPJPY 4-Hour Elliott Wave Chart From 2.01.2024

Here’s the 4-hour Elliott wave Chart from the 2/01/2024 update. In which, the rally to 188.93 high-ended wave (1) & made a pullback in wave (2). The internals of that pullback unfolded as Elliott wave double correction where wave W ended in 3 swings at 186.49 low. Then a bounce to 187.60 high-ended wave X & started the next leg lower in wave Y towards 185.18- 183.69 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

GBPJPY Latest 4-Hour Elliott Wave Chart From 2.26.2024

This is the latest 4-hour Elliott wave Chart from the 2/26/2024 update. In which the pair is showing a strong reaction higher taking place, right after ending the double correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. Since then the pair has already seen a break above 188.93 high confirming the next extension higher.

Another Solid String Would Further Cement the Idea of First Fed Cut in July

Markets

A news-poor trading session yesterday didn’t prevent German yields from rebounding sharply after Friday’s setback. A belated reaction to the hawkish ECB talk or simply repositioning ahead of the end of month and/or critical data later this week? Either way, changes varied between 7.1-8.1 bps across the curve. US Treasuries outperformed, adding 1.9 to 3.6 bps. A dual US auction went smooth in the 2-y tenor but printed mixed in the 5-y. Most major equity indices eased from (record) highs. The euro traded stronger, helped higher by narrowing interest rate differentials. EUR/USD extended the mid-February recovery to 1.0851. DXY (trade-weighted dollar index) suggested some overall USD weakness was in play as well, declining to 103.827. USD/JPY continues to hover near recent highs north of 150. JPY is looking increasingly vulnerable for a sharp sell-off. If the dollar doesn’t come to the rescue, then the Bank of Japan has to. This morning’s higher-than-expected inflation numbers (see below) offer a (tiny) bit of respite. The BoJ’s core gauge (excluding food but including oil products) eased to 2% in January. That measure is expected to jump higher in February as energy subsidies distorted last year’s m/m (-0.6%) reading to the downside. Sterling lost ground throughout the session though within the technical barriers. EUR/GBP gained to 0.8554.

The eco calendar still has something to offer after the Japanese CPI numbers. The US takes center stage with durable goods orders, house price data, some regional business sentiment indicators and consumer confidence (Conference Board). Their importance for trading would have been bigger if it weren’t for the other important data that’s scheduled for release later this week (including PCE deflators and manufacturing ISM). But if anything, another solid string would further cement the idea of a first Fed cut in July rather than June. That should provide a solid floor beneath US yields. The 2-y yield is nearing the first resistance in the 4.80% region but we don’t expect that level to break. The 10-y tenor is looking at 4.40%. The dollar should soon find some support as well (EUR/USD 1.0862/1.0865), especially if equities continue to struggle for direction after they are no longer flanked by (mostly stellar) earnings releases. Several central bankers have and will hit the wires in the meantime. Kansas Fed’s Schmid in Asian dealings sees no need to preemptively adjust policy and said he’s in no hurry to halt the balance-sheet runoff. Sticking to the subject of monetary policy, the Hungarian central bank is bound to cut rates today. The jury’s out whether the MNB will stick to 75 bps to ensure forint stability or capitalize the stronger disinflation and scale up to 100 bps.

News & Views

National Japanese inflation data slowed less than hoped in January. Headline CPI declined from 2.6% Y/Y to 2.2% (vs 1.9% consensus) with the CPI ex fresh food gauge – the BoJ’s favorite – down to 2% Y/Y from 2.3% (vs 1.9% forecast). Another core gauge that excludes fresh food and energy slowed to 3.5% Y/Y from 3.7% (vs 3.3%). A jump in prices of foreign technical travel packages skewed today’s outcome as it turns out that the base of comparison for this series was January 2020, not 2023. The ministry of internal affairs and communications said that they had stopped surveying the prices for the past three years due to the difficulties in collecting stable price data following the onset of Covid. Japanese bond yields are nevertheless slightly higher this morning with the 2-yr yield at the highest level since early 2011. The Japanese yen fails to profit and remains in dire straits north of USD/JPY 150.

US President Biden said in NBC’s “Late Night with Seth Meyers” that there was an agreement in principle for a ceasefire between Israel and Hamas during Ramadan in the Gaza Strip (March 10 – April 9). In exchange, more hostages would be released. It would also allow for Palestinians to evacuate from the southern city of Rafah. The next phase in the war is expected to be an Israelian ground move into this city. US President Biden hopes that a temporary ceasefire would help change the dynamic towards a two-state solution. There has been no official reaction from Israel yet. PM Netanyahu vowed to destroy Hamas and so far rejected the two-state solution idea.

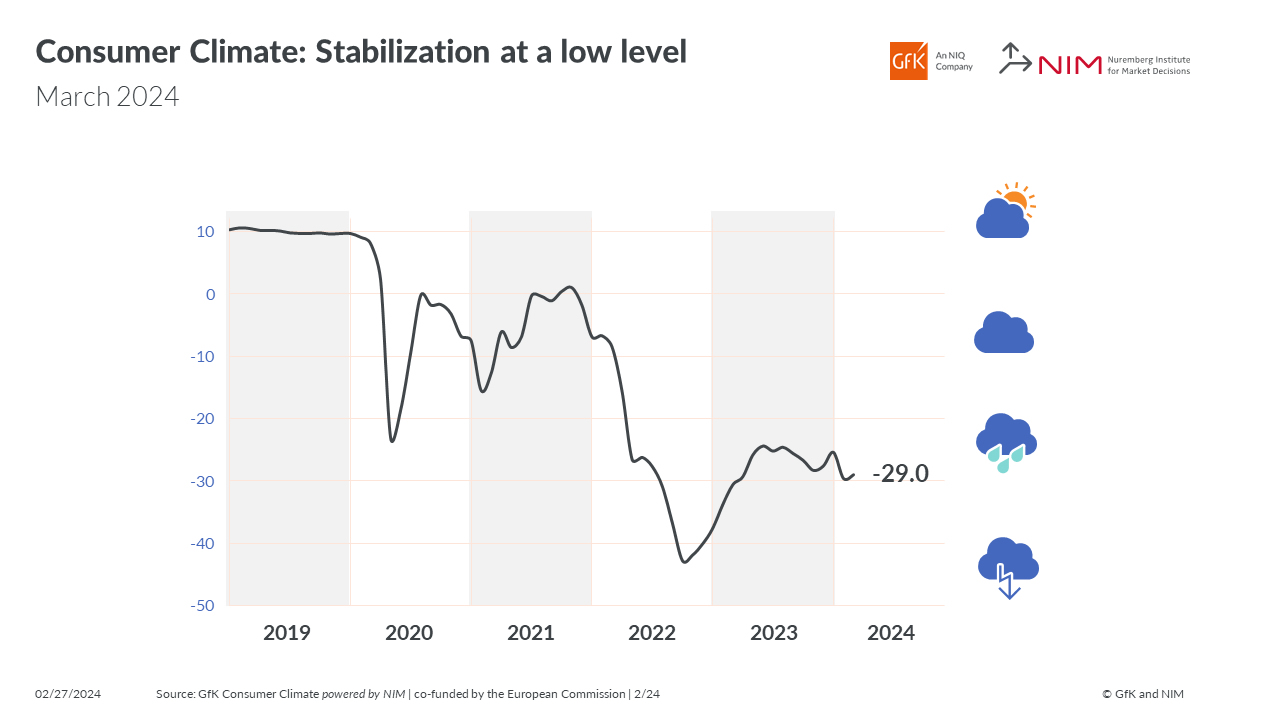

Germany’s Gfk consumer sentiment rises slightly to -29

Germany Gfk Consumer Sentiment for March ticked up from -29.6 to -29.0, matched expectations. In February, economic expectations rose from -6.6 to -6.4. Income expectations improved notably from-20.0 to -4.8. Willingness to buy fell from -14.8 to -15.0. Willingness to save jumped from 14.0 to 17.4.

Rolf Bürkl, a consumer expert, highlighted the prevailing uncertainty among consumers, driven by persistently high prices and dimming economic projections for Germany. German government's downgrade of its growth forecast for 2024 from an initial 1.3% down to a mere 0.2% underscores the challenges ahead.

Calm Before the Data

European and American stocks kicked off the week with a pause, as investors took a breather after sending major stock indices in these regions to record highs. The Stoxx 600, the S&P500 and Nasdaq 100 all retreated from an ATH level on Monday. MAMAA stocks were down around 1%, Amazon – which had it first day at Dow Jones Industrial index fell 0.15% whereas Nvidia managed to eke out a small gain.

It feels like there is a moment of calm and silence in the aftermath of major tech earnings, investors will decide whether this rally deserves to continue higher straight away. The week brings some important economic data on the table. The US will release its latest growth and inflation updates this week. And favourable data – meaning resilient but not abnormally strong growth, coupled with softening inflation, would allow the market bulls to surf on the ‘goldilocks’ wave. If that’s the case, we could see the stock market rally continue, and to broaden to sectors other than the technology stocks. The equal weigh S&P500 index could make an attempt to catch up the technology-heavy S&P500. If not, if growth is resilient, but inflation ticks higher in a way that’s concerning for the Federal Reserve (Fed) expectations, we could see profit taking and a downside correction across major US indices, and selling could spill over to the other major stock markets.

But there are concerns regarding – not the strength of the US growth, but inflation’s trajectory. US economic is expected to have grown 3.3% in Q4 – lower than the 5% printed a quarter earlier but still a very strong growth for an economy that has experienced the most aggressive rate hiking cycle of its modern history. And the core PCE – which excludes food and energy prices – is expected to jump by most in a year. Three and six-month inflation – which both fell below the Fed’s 2% target recently- are also expected to spike above this 2% level. An uptick in inflation is not good news for the Fed doves, who already dropped the expectation that the Fed would cut rates by March, and then by May, and now they are trimming the June cut expectations. The expectation of a June Fed cut is given around 60% chance before this week’s inflation figures are released. This probability was around 70% just yesterday.

US GDP data is due Wednesday, inflation on Thursday. And before that, today, we will have an insight on the durable goods orders, house prices and the Richmond Fed manufacturing index. Voila.

The US 2-year yield is just around the 4.70%, the 10-year yield is a touch below the 4.30% level. Yesterday’s 2 and 5-year US auctions both settled at higher yields, as supply was heavy both in government and corporate bond sales. Vanguard’s intermediate-term treasury ETF saw the biggest weekly inflow on record as investors continued to scale back their Fed cut expectations fearing that a hotter-than-expected inflation read this week could spoil the market mood. Softening Fed expectations caused outflows from short and ultra-long term bonds to medium-term papers.

And speaking of inflation, inflation in Japan fell to a 22-month low. The Bank of Japan (BoJ) is in no rush to hike the rates this April. The USDJPY is getting comfortably near the 150 level, as the Nikkei 225 consolidates near ATH levels.

In commodities, US crude saw support near the 100-DMA yesterday, but appetite remains insufficient to push the price of a barrel to and above the $80pb level. Nat gas futures remain under pressure as investors remain reluctant to buy the dip even near the current oversold levels. Iron ore prices, on the other hand, fell to the lowest levels since November – a warnings regarding China’s inability to boost its property sector despite stimulus.

Inflation in Japan Surprises to the Topside

In focus today

In the euro area, we look out for the January monetary aggregates and lending data. We focus on the lending data as there have recently been signs of a rebound in loan growth and the credit impulse. A rebound in the credit impulse will be key for the euro area growth outlook in 2024.

In Hungary the central bank will announce its policy rate. The market consensus is a rate cut of 100bps from 10.0% to 9.0%.

Overnight the Reserve Bank of New Zealand will announce its cash rate decision. We expect an unchanged rate decision, but markets are pricing in a 25% chance of an additional rate hike - 9 months after the latest one.

In the US the republican primary elections head to Michigan.

Economic and market news

What happened over night

In Japan core CPI rose 2.0% y/y in January (cons.: 1.9%, prior: 2.3%). It marked the 22nd straight month in which inflation matched or exceeded the Bank of Japan's target. Core CPI excludes fresh food. Stripping away both fresh food and energy, CPI rose 3.5% y/y in January (cons.: 3.3%, prior: 3.7%). Hence, the release supports the case for the BoJ to end its negative interest rate policy. The next key release to look for in Japan is the first tally of the spring wage negotiations set to be released on 15 March. It will likely provide pivotal clues about whether Japan will experience another year with significant broad-based wage increases. Our base case remains that the BoJ will exit its yield curve control and end its negative interest rate policy at the April meeting.

What happened yesterday

Sweden cleared the final hurdle to join NATO after the Hungarian parliament as the last member state approved Sweden's accession to the defence alliance.

ECB's Stournaras sounded relatively hawkish on monetary policy. He said that he expects the first rate cut to be in June, but that he does not think the ECB should wait longer than that. He also said that any monetary policy adjustments must be gradual and that he is against abrupt changes in monetary policy. The hawkish tone is surprising since Stournaras is known to be one of the most dovish members of the ECB.

In the US we also heard some hawkish tones from Fed's Schmid who remained focused on the threat of high inflation and therefore is in no rush to lower interest rates. This is in line with other Fed members who have the over past few weeks have spoken about keeping policy rates at the current level until they are more confident that inflation is heading towards the 2% target.

The US Congress is under pressure to move forward on spending bills to avoid a partial government shutdown in five days. Nevertheless, a group of conservative hardliners in the House have repeatedly blocked legislation. In the Senate, the republican leader McConnell said that the republicans in the Senate are not going to shut down the government, but he does not control the members of the House.

Regarding the Israel-Hamas conflict, US president Biden said that he hopes for a ceasefire to start by next Monday as the parties seem to be nearing each other in a deal in negotiations in Qatar. Early Tuesday Biden said that Israel had agreed not to engage in military activity during the Ramadan.

Equities: Global equities were lower yesterday in an uneventful session with no major macro news to set the direction. Despite equities being lower we still saw cyclicals outperforming led by consumer discretionary, tech and industrials. It is worth nothing that small caps were doing good and hence there are no signs of negative shift in sentiment but rather some wait-and-see mode ahead of bigger macro events later this week. In US yesterday, Dow -0.2%, S&P 500 -0.4%, Nasdaq -0.1% and Russell 2000 +0.6%. Asian markets are mixed this morning with Chinese A-shares outperforming. Futures are lower in both Europe and US.

FI: Global bond yields rose on Monday ahead of European inflation data as well as comments from Federal Reserve members and mixed demand at yesterday's record-size auction of 5Y US Treasuries. The US treasury sold USD 64bn in the 5y benchmark yesterday with a bid-to-cover of 2.4 relative to 2.3 at the previous auction. Furthermore, the US Treasury also sold USD 63bn in the 2Y segment. 10Y US treasuries rose some 3bp, while the 10Y German government bond yields increased some 7bp.

FX: Yesterday's session marked a rather quiet start to the week. Generally, pro-cyclical currencies are still benefiting from the aftermath of last week's rally in global equities, favouring scandies, EUR, and GBP, while the USD trades on the back foot, causing EUR/USD to consolidate in the 1.08-1.09 range. A stronger-than-expected Japan January CPI print added some support to the JPY. Overnight, we expect an unchanged rate decision from the Reserve Bank of New Zealand (RBNZ).

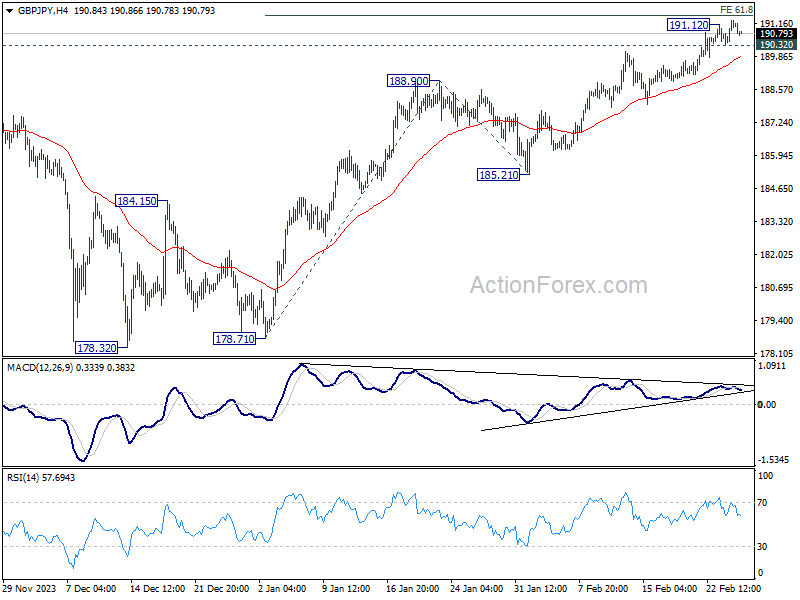

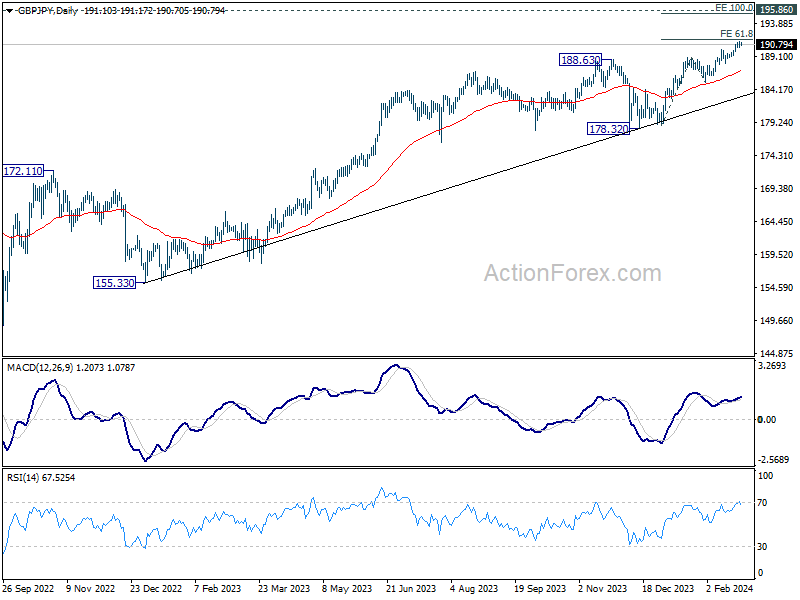

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.57; (P) 190.95; (R1) 191.55; More...

Intraday bias in GBP/JPY is back on the upside with breach of 191.12 temporary top. Firm break of 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50 will extend larger up trend to 100% projection at 195.40. On the downside, however, break of 190.32 minor support will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.83; (P) 163.27; (R1) 163.99; More...

EUR/JPY's rally resumed by breaking 163.45 temporary top and intraday bias is back on the upside. Further rally would be seen to 164.29 high. Firm break there will resume larger up trend. On the downside, below 1`62.55 minor support will turn bias back to the downside for deeper pullback first.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).