Sample Category Title

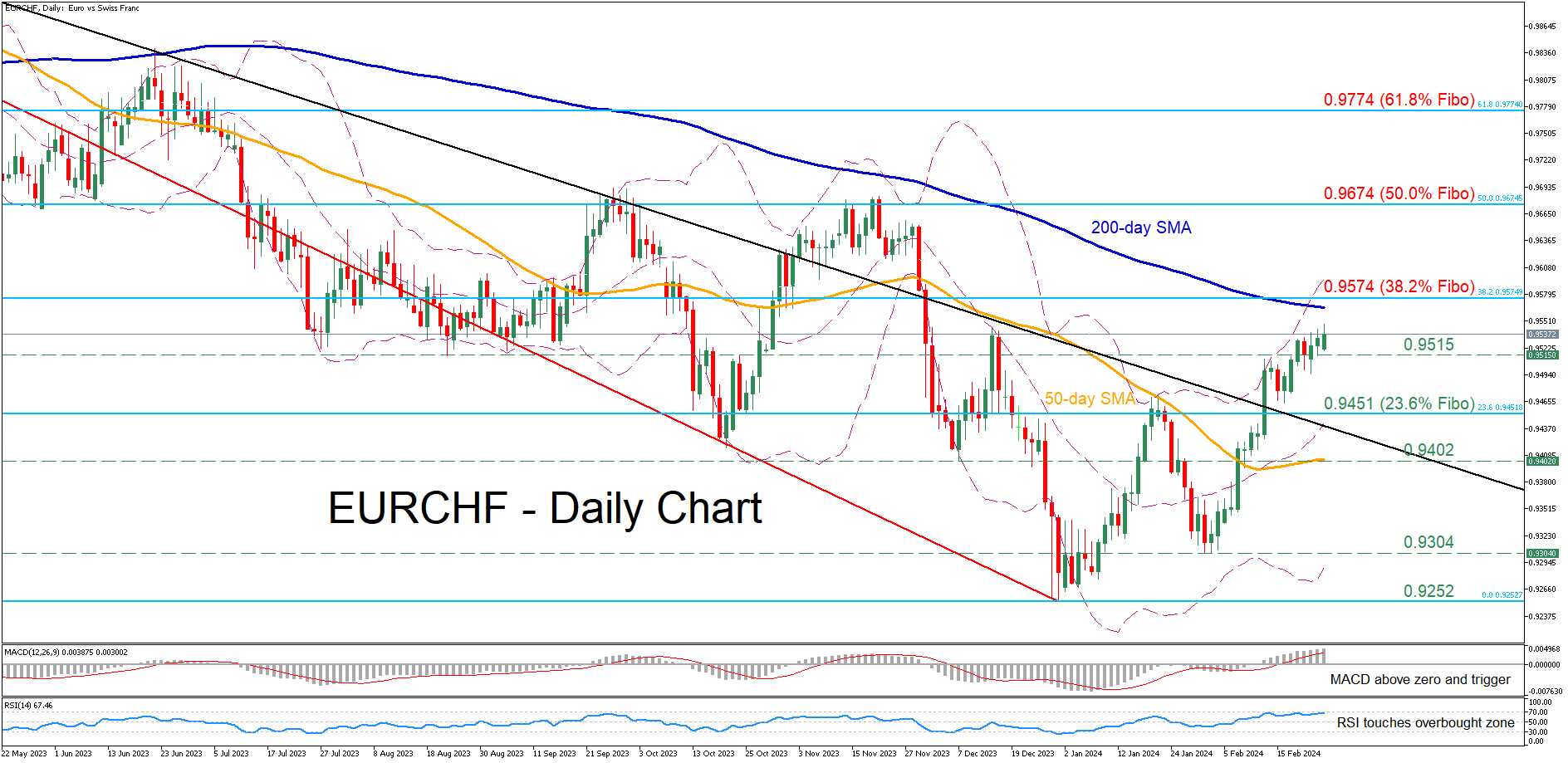

EURCHF Extends Advance Towards 200-Day SMA

- EURCHF extends recovery to a fresh 2-month high

- Breaks above trendline and eyes 200-day SMA

- Momentum indicators approach overbought levels

EURCHF has been in a downtrend since the beginning of 2023, dropping to an all-time low of 0.9252 on December 29. However, the pair has been staging a rebound in 2024, violating the downward sloping trendline that connects its lower highs in the past year and posting a fresh two-month peak on Monday.

Should the pair resume the recovery and jump above the 200-day simple moving average (SMA), immediate resistance could be met at 0.9574, which is the 38.2% Fibonacci retracement of the 1.009-0.9252 downleg. Claiming that zone, the price may test the 50.0% Fibo of 0.9674, a region that held strong both in September and November. Further upside attempts could stall at the 61.8% Fibo of 0.9774.

Alternatively, if the pair experiences a pullback, the August support of 0.9515 could prove to be a tough barrier for the bears to overcome. Sliding beneath that floor, the price might descend towards the 23.6% Fibo of 0.9451. A violation of that region could set the stage for the December support of 0.9402, which overlaps with the 50-day SMA.

In brief, EURCHF has been in a recovery mode since the beginning of the year, but the long-term downtrend remains intact. Therefore, a break above the 200-day SMA is needed for the bulls to regain some confidence about a full-scale reversal.

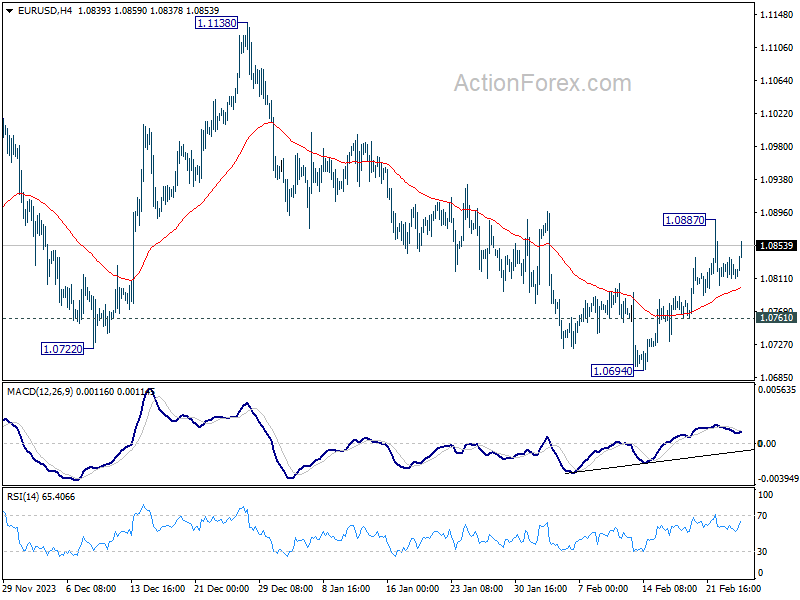

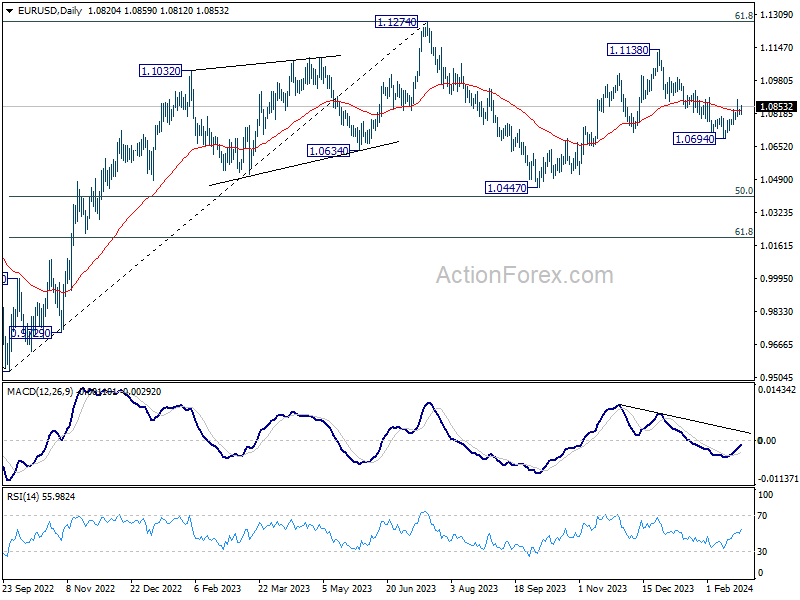

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0809; (P) 1.0824; (R1) 1.0836; More...

EUR/USD is staying in range below 1.0887 and intraday bias remains neutral. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0831) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. . However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

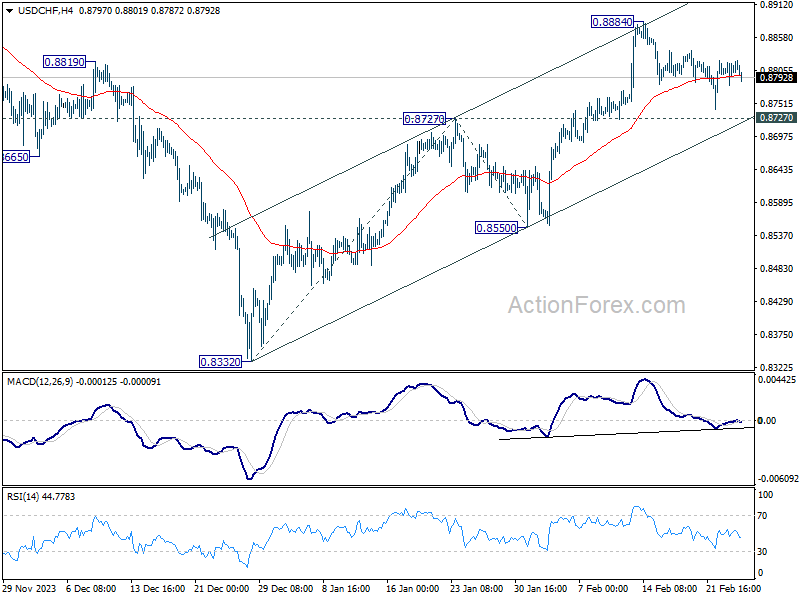

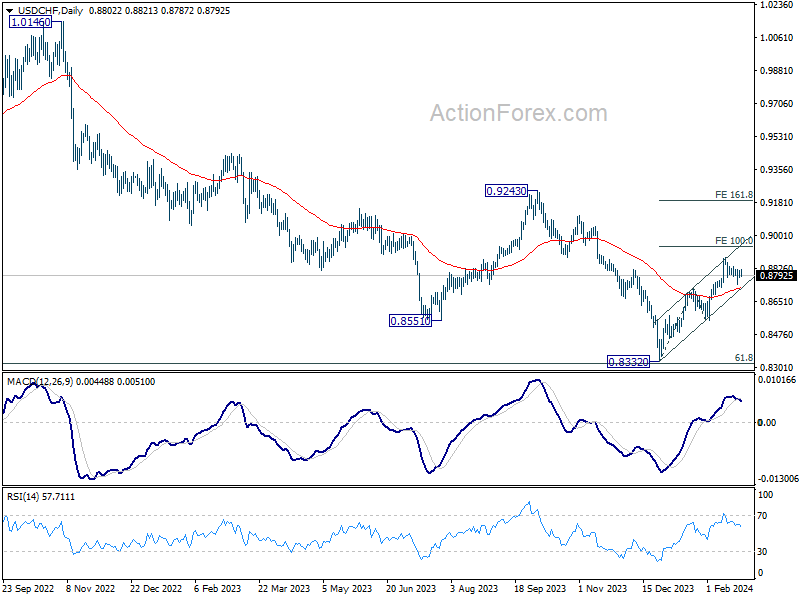

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8788; (P) 0.8804; (R1) 0.8827; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8884 is extending. With 0.8727 resistance turned support intact, further rally is expected. On the upside, above 0.8884 will resume the rally from 0.8332 to 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

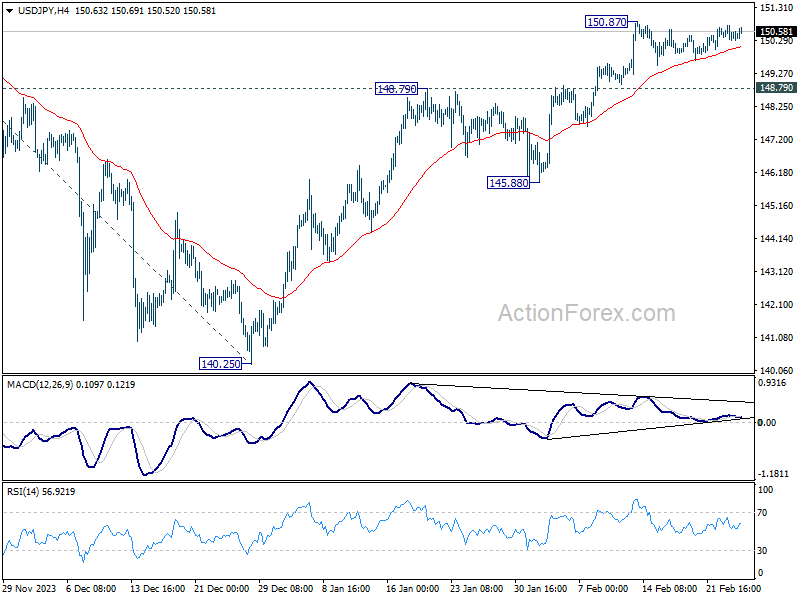

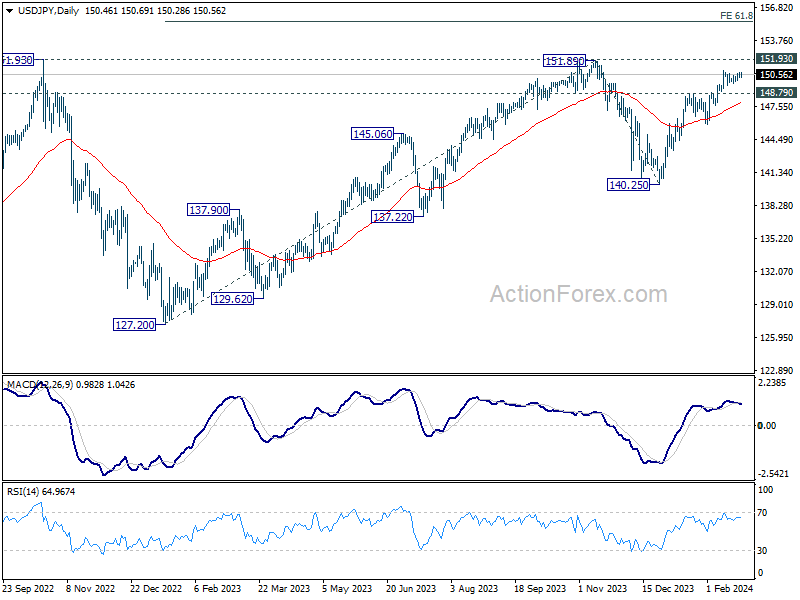

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.28; (P) 150.52; (R1) 150.76; More...

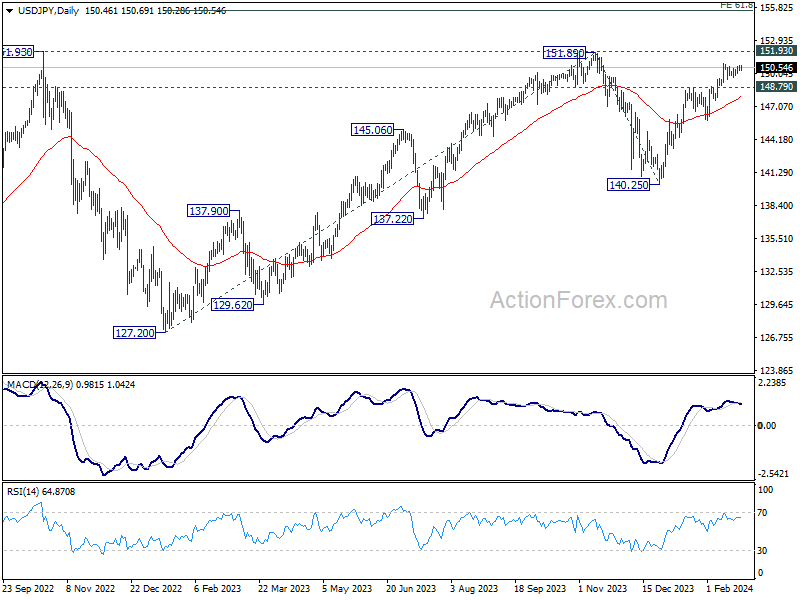

USD/JPY is staying in range below 150.87 and intraday bias remains neutral. In case of another retreat, downside should be contained by 148.79 resistance turned support to bring rebound. On the upside, break of 150.87 will resume 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg

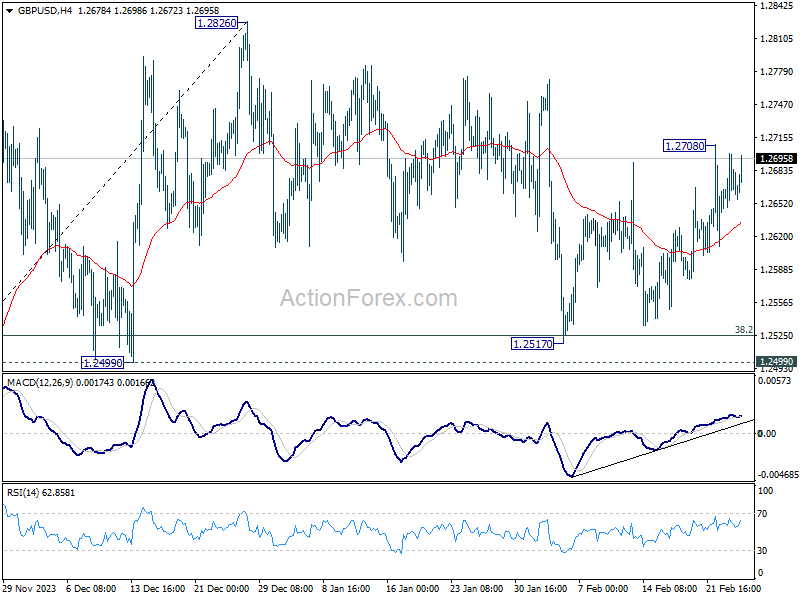

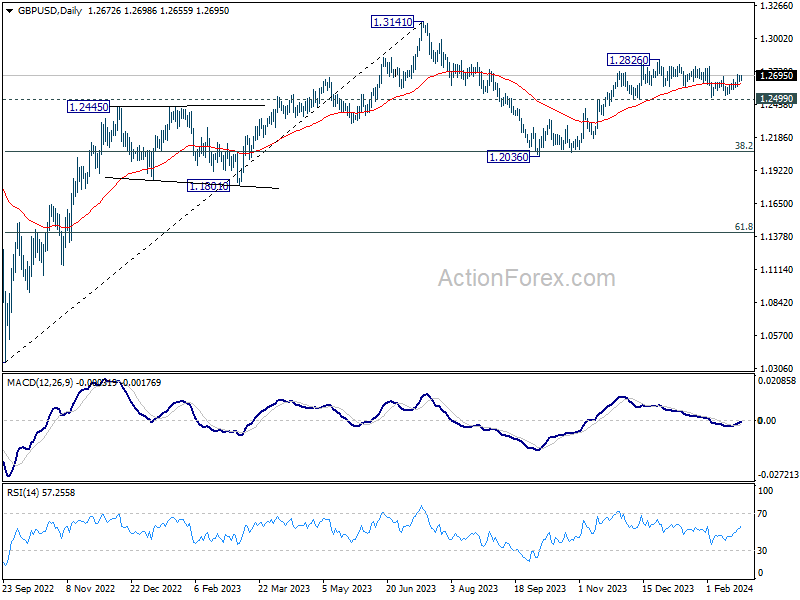

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2674; (R1) 1.2699; More...

GBP/USD is still capped below 1.2708 temporary top and intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Euro Gains Traction as Markets Eye Japan CPI, Commodity Currencies Lag

The global financial markets are overall very quiet today, marked by a noticeable absence of significant economic data releases or impactful news. Euro emerges as the frontrunner, leading European majors higher, while Yen sees a slight dip in anticipation of Japan's CPI data set to be released tomorrow. Commodity currencies are on the weaker side, particularly highlighted by New Zealand Dollar's early sell-off. Dollar, meanwhile, is mixed as it awaits new drivers that could provide fresh momentum.

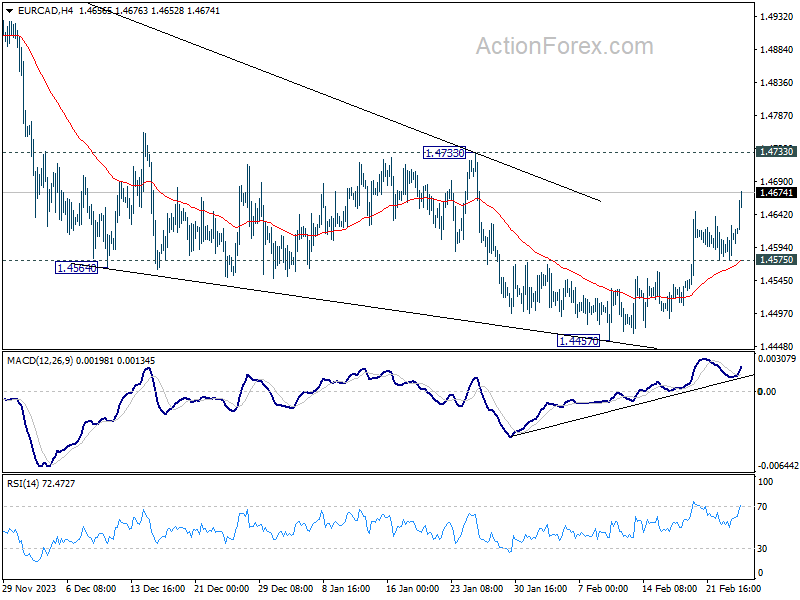

Technically, EUR/CAD's rebound from 1.4457 resumed today and it's on track to test 1.4733 resistance. Corrective fall from 1.5041 is seen as completed with three waves down. Rise from 1.4155 is probably resuming. Sustained break of 1.4733 will strengthen this bullish case and target 1.5041 resistance next. This will now remain the favored case long as 1.4575 support holds.

In Europe, at the time of writing, FTSE is down -0.28%. DAX is up 0.07%. CAC is down -0.34%. UK 10-year yield is up 0.0114 at 4.051. Germany 10-year yield is up 0.016 at 2.385. Earlier in Asia, Nikkei rose 0.35%. Hong Kong HSI fell -0.54%. China Shanghai SSE fell -0.48%. Singapore Strait Times fell -0.43%. Japan 10-year yield fell -0.0305 to 0.691.

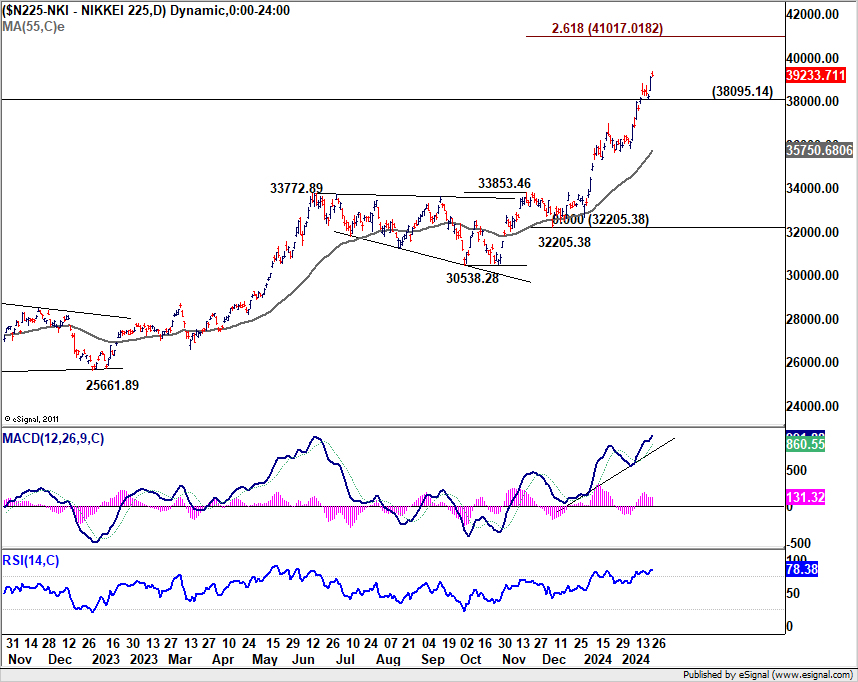

Nikkei reaches new heights as Yen declines before Japan's CPI

Nikkei index surged to new record today, signaling robust appetite for risk among Japanese investors, while Yen faces downward pressure, in particular against European majors. Consumer inflation data is in the spotlight in the upcoming Asian session.

Core CPI, which excludes food prices, is forecasted to decelerate from 2.3% to 1.8% in January, below BoJ's 2% target for the first time in nearly two years. However, for the BoJ, the crucial figure lies in the core-core CPI (excluding both food and energy), which is awaited to see if it will decelerate from December's 3.7%.

Governor Kazuo Ueda has consistently highlighted the significance of the outcomes from this year's annual wage negotiations as a pivotal factor in determining the timeline for phasing out the negative interest rate policy.

With large businesses scheduled to conclude wage talks with unions on March 13, just days before BoJ's next meeting on March 18-19, March is seen by some as a candidate for a rate hike. Yet, April, with the availability of new economic projections, remains a more plausible window for such policy adjustments.

However, any unexpected strength in the inflation report could fuel speculation about an earlier rate hike.

USD/JPY has been losing much momentum after breaking 150 handle. Threat of intervention by Japan could be a major factor keeping USD/JPY bulls from aggressive buying. Nevertheless, rally from 140.25 is still in tact as long as 148.79 support holds. But the path to 151.89/93 resistance zone would be slow.

As for Nikkei, it should be rather undeterred by the inflation data. Near term outlook will stay bullish as long as 38095.14 support holds. Next target is 40k psychological level, or even further to 261.8% projection of 30538.28 to 33853.46 from 32205.38 at 41017.01.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2674; (R1) 1.2699; More...

GBP/USD is still capped below 1.2708 temporary top and intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 2.10% | 2.40% | 2.40% | |

| 15:00 | USD | New Home Sales M/M Jan | 685K | 664K |

Nikkei reaches new heights as Yen declines before Japan’s CPI

Nikkei index surged to new record today, signaling robust appetite for risk among Japanese investors, while Yen faces downward pressure, in particular against European majors. Consumer inflation data is in the spotlight in the upcoming Asian session.

Core CPI, which excludes food prices, is forecasted to decelerate from 2.3% to 1.8% in January, below BoJ's 2% target for the first time in nearly two years. However, for the BoJ, the crucial figure lies in the core-core CPI (excluding both food and energy), which is awaited to see if it will decelerate from December's 3.7%.

Governor Kazuo Ueda has consistently highlighted the significance of the outcomes from this year's annual wage negotiations as a pivotal factor in determining the timeline for phasing out the negative interest rate policy.

With large businesses scheduled to conclude wage talks with unions on March 13, just days before BoJ's next meeting on March 18-19, March is seen by some as a candidate for a rate hike. Yet, April, with the availability of new economic projections, remains a more plausible window for such policy adjustments.

However, any unexpected strength in the inflation report could fuel speculation about an earlier rate hike.

USD/JPY has been losing much momentum after breaking 150 handle. Threat of intervention by Japan could be a major factor keeping USD/JPY bulls from aggressive buying. Nevertheless, rally from 140.25 is still in tact as long as 148.79 support holds. But the path to 151.89/93 resistance zone would be slow.

As for Nikkei, it should be rather undeterred by the inflation data. Near term outlook will stay bullish as long as 38095.14 support holds. Next target is 40k psychological level, or even further to 261.8% projection of 30538.28 to 33853.46 from 32205.38 at 41017.01.

US Dollar Eyes PCE Inflation Data After CPI Scare

- Core PCE price index to be crucial for markets amid sticky inflation fears

- Income and consumption to be watched too as US economy stays hot

- But can further upside surprises boost the dollar on Thursday, 13:30 GMT

Will PCE gauge ease or fuel inflation worries?

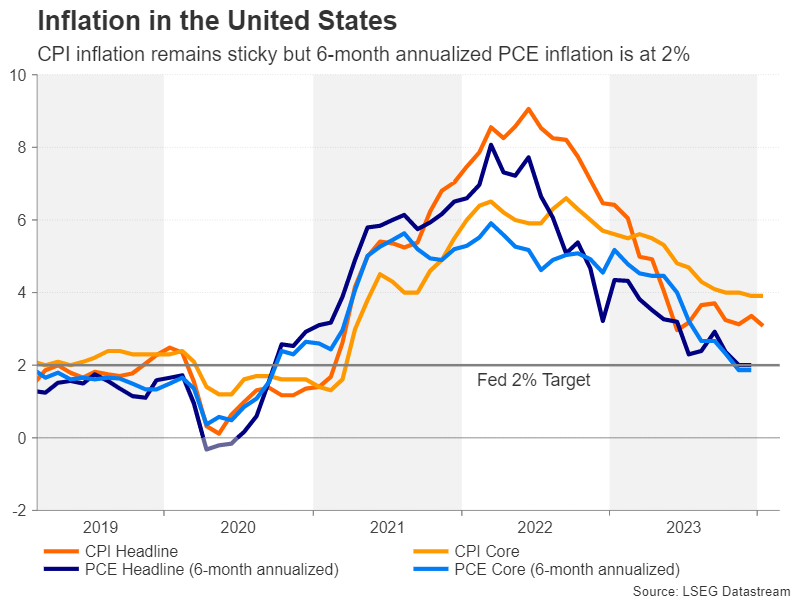

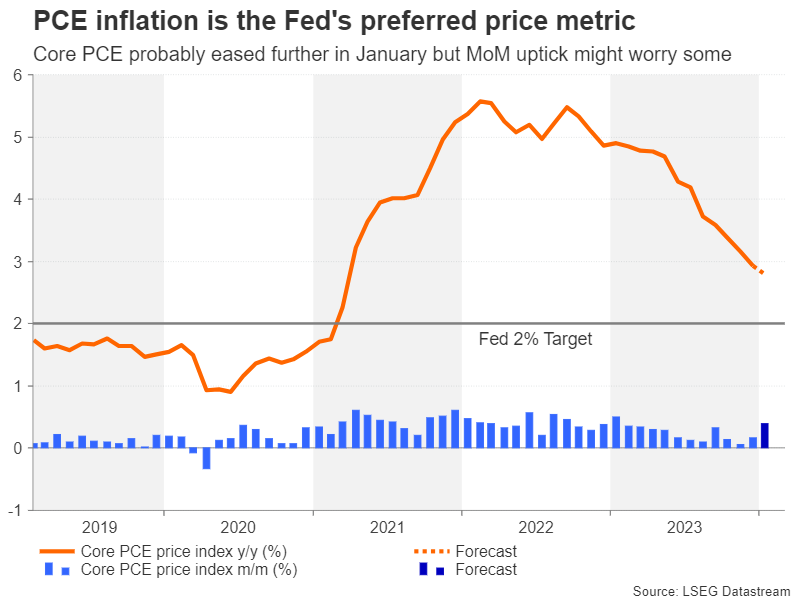

Even though the Fed has made great progress in its bid to bring inflation in the US under control, the next phase to get it all the way down to 2% is proving to be a little more difficult. The CPI measure of inflation has been stuck above 3.0% for some time now and core CPI was unchanged at 3.9% in January.

The inflation picture according to the Fed’s preferred PCE measure has been somewhat more encouraging lately, particularly when focusing on the six-month annualized rate. The headline PCE price index stood bang on the Fed’s 2.0% target in December and the core PCE price index was at 1.9% by this metric. However, the year-on-year rates still have some ground to cover and came in at 2.6% and 2.9%, respectively, in December.

For January, the core PCE price index is forecast to have cooled slightly lower to 2.8%, although the month-on-month rate is projected to have picked up to 0.4%. A stronger-than-expected reading, particularly in the month-on-month rate, would likely further stoke fears about high inflation rearing its ugly head again.

The big repricing

The recent run of upbeat indicators out of the world’s largest economy has put markets in a spin, prompting a sharp rethink on the expected Fed rate path. Markets were pricing almost seven rate cuts for this year at one point in January. A month later, those dovish bets have been scaled down to less than four cuts.

On the bright side, investors are now better aligned with the Fed’s thinking, although there is still some repricing to go as the Fed’s latest dot plot predicted three 25-bps rate cuts in 2024. Any further upside surprises in the inflation data following the CPI and PPI beats have the potential to spark some volatility across the major asset classes, including bonds and equities.

Can the dollar extend its uptrend?

Treasury yields have been steadier lately but could resume their rally if there’s another hotter-than-expected inflation print. A jump in yields could be enough to inject some life into the US dollar, which has been drifting lower over the past 10 days, even against the beleaguered yen.

The pair has been struggling to advance past the 150 level, losing momentum as it approaches the November peak of 151.92 yen. A strong PCE report might be what it takes to jumpstart the stalled uptrend and push the dollar to a new high above 152 yen.

However, there are significant downside risks too for the greenback in the event of a miss in the core PCE price index. Whilst there are signs that the dollar’s latest upswing is running out of steam, it has nevertheless rebounded by around 2.5% against a basket of currencies this year and by more than 6% against the yen. A selloff could therefore stretch at least until the 50-day moving average in the 146.60 region if it turns into a negative correction.

Slowing consumption could be a good thing

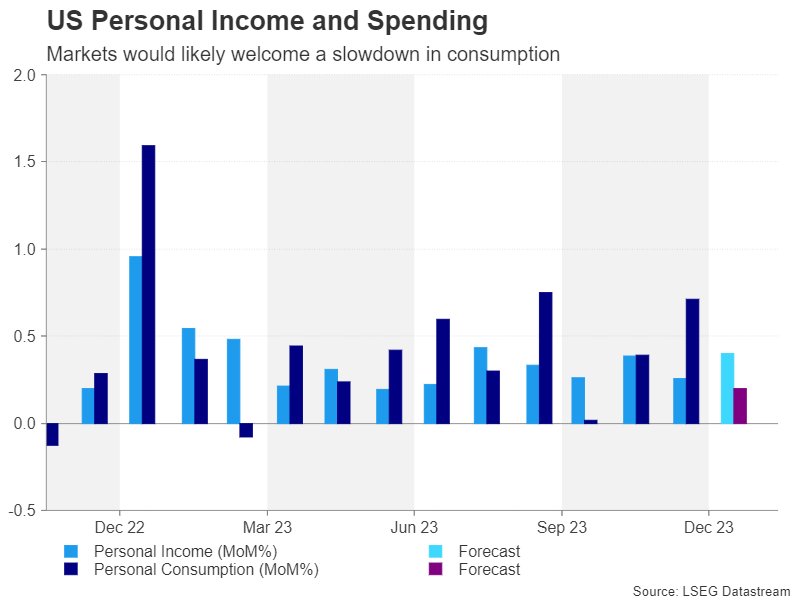

Investors will also be watching the latest numbers on personal income and personal consumption that will be released alongside the PCE price indices. Personal income is expected to have increased by 0.4% m/m in January versus 0.3% in December. More importantly, personal consumption is forecast to have risen at a more moderate pace of 0.2% in January after surging by 0.7% in December.

A slowdown in consumer spending could ease concerns about an overheating economy and so would likely be welcomed by equity markets, though not so much by the dollar. However, markets would not react as positively if there’s a sudden deterioration in consumption as investors are positioned for a soft landing in the US economy. Anything that questions that view would weigh on risk sentiment.

Also coming up

In other data due this week, durable goods orders for January will be watched on Tuesday, along with the consumer confidence index for February. On Wednesday, the second estimate of Q4 GDP might attract some attention, though no change is anticipated to the advance estimate of 3.3% annualized growth.

Closing the week on Friday will be the ISM manufacturing PMI for Friday. It’s expected that manufacturing activity improved slightly in February, with the PMI edging up to 49.5.

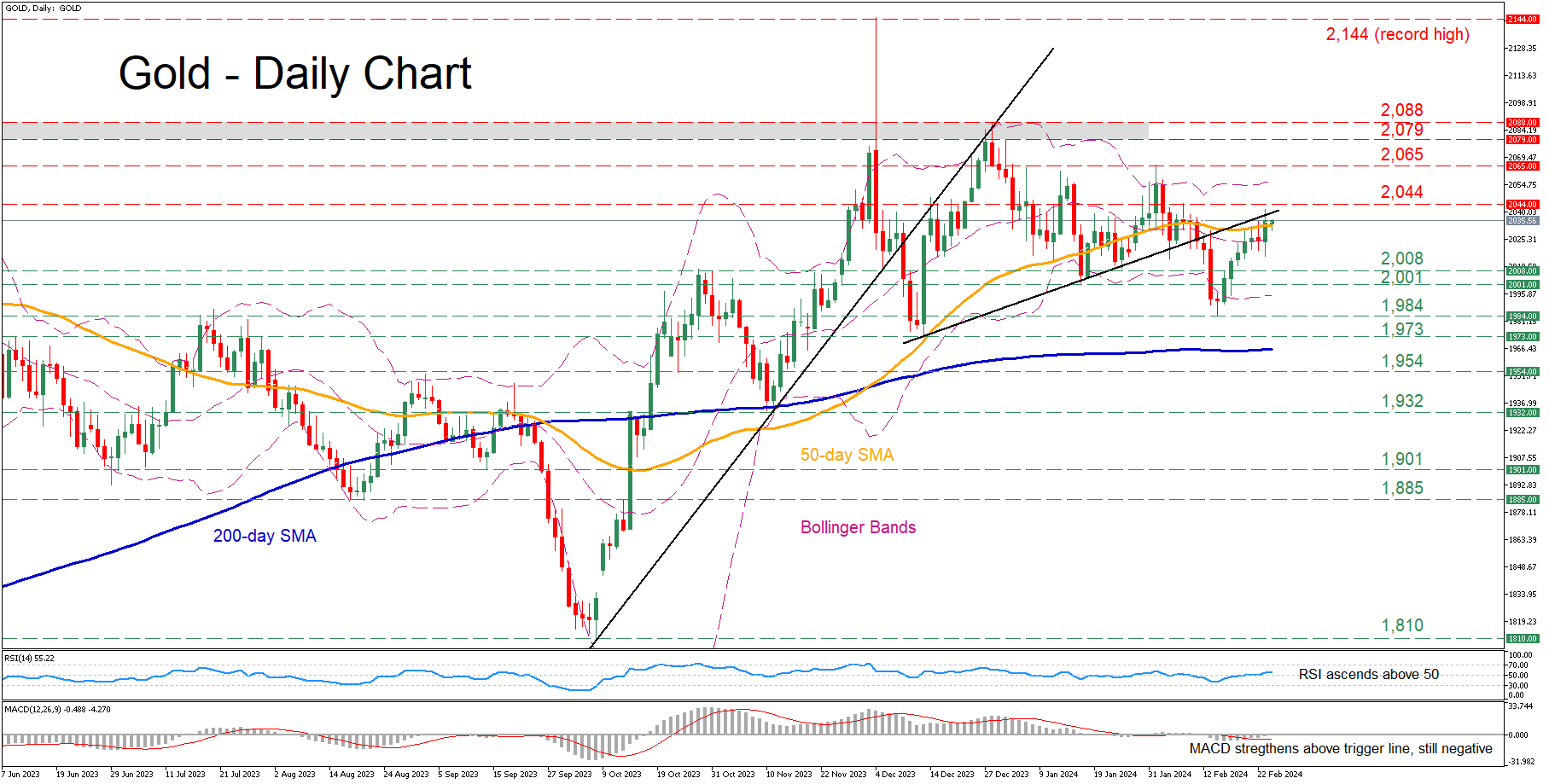

Gold Battles With 50-day SMA

- Gold rebounds strongly from its 2024 low

- Challenges 50-day SMA and ascending trendline

- Momentum indicators turn neutral-to-positive

Gold has been regaining ground in the past few sessions, following its bounce off the 2024 bottom of 1,984. Although the price has recouped a significant part of its losses, it has currently stalled at the congested region that includes the 50-day simple moving average (SMA) and the ascending trendline that connects the higher lows since December.

Should bullish pressures persist, bullion could challenge the 2,044 hurdle, which acted as resistance both in December and February. Failing to halt there, the price may advance towards the February high of 2,065. An upside violation of that zone could open the door for the crucial 2,079-2,088 range.

Alternatively, if the price reverses back lower, the January support zones of 2,008 and 2,001 could act as the first lines of defence. Further declines might then cease around the 2024 bottom of 1,984. Even lower, the December low of 1,973 could provide downside protection.

In brief, gold has been in a recovery mode in the past two weeks, but the 50-day SMA has been repeatedly curbing its upside. Hence, a break above the latter is needed for the price to extend its rebound towards all-time highs.

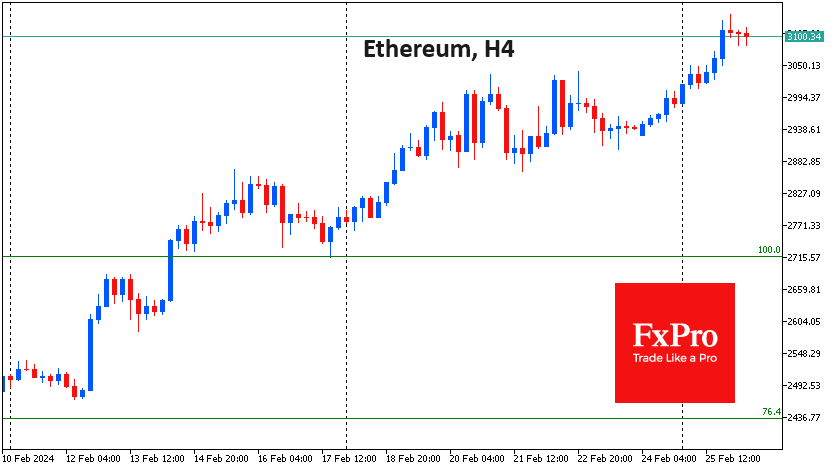

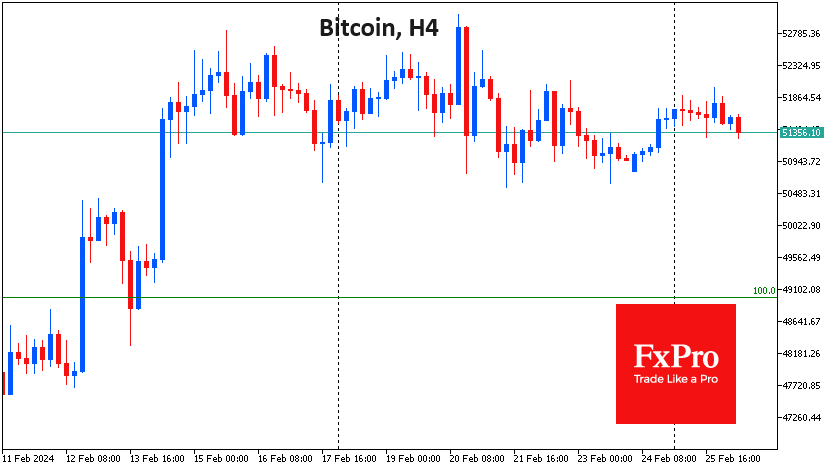

Ethereum as Crypto Growth Driver

Market picture

The crypto market settles at a $2 trillion cap level, up 0.8% on the day. Altcoins are once again driving growth, while the first coin is flat, losing 0.5% in 24 hours, and Ethereum is up 2.5%. BNB adds just under 2%, enjoying a resurgence of interest in cryptocurrency trading. XRP and Cardano both lose 1%, dragging the market back down.

Bitcoin and Ethereum are the cryptocurrencies of choice for institutional speculators. Their obvious trade right now is betting on the approval of spot ETFs on ETH. Speculators are cautiously locking in profits in BTC, which has previously rallied on the same theme.

Remember that Ethereum’s market capacity is smaller than Bitcoin’s, which has a three times bigger market cap. This means that the price is more sensitive to changes in sentiment. Ethereum has gained 40% in 30 days, the best performance among the top 10 coins.

News background

About 90% of the bitcoins purchased by spot ETFs have gone to Coinbase’s custodial platform, its CEO Brian Armstrong said. He stated that the exchange’s custody service has accumulated more than $36 billion in BTC. The growing ETF market suggests that institutional capital is seriously considering bitcoin as one of the most reliable assets.

If the US SEC does not approve a spot Ethereum ETF in May 2024, it will do so by mid-2025, said attorney Scott Jonsson. Bloomberg analyst James Seyffarth believes the SEC won’t take as long to process Ethereum ETF applications as it did with BTC, as a significant portion of the applications could be based on Bitcoin ETFs. S&P Ratings expects the SEC to approve applications to launch the ETF in May.

The court approves a $4.3 billion payment by Binance exchange to the US Department of Justice as part of a plea deal. According to the signed agreement, the platform agreed to take significant steps to ensure continued compliance with US laws.

According to CryptoSlam, total sales of non-replaceable tokens (NFTs) on the Solana network have surpassed $5 billion, with 43 million NFT transactions. The Solana blockchain has more than 2.2 million buyers and 1.6 million sellers of NFTs.

Internet forum Reddit invests surplus funds in Bitcoin and Ethereum. The cryptocurrency investment strategy started back in 2022.