Sample Category Title

Yen Inches Upward as Japan’s CPI Fuels March BoJ Hike Talks

Japanese Yen found modest strength in Asian session today, lifted by stronger than expected consumer inflation data from Japan. At the same time, two-year yield climbed to its highest point since 2011 while Nikkei is steady. The data intensified speculations around BoJ's move to abandon its negative interest rate policy. Almost all economists are expecting a rate hike in the first half of the year, with April still tagged as the most probable timing. However, the CPI raises the chance of an expedited move in March.

Despite today's recovery, it's premature to declare bullish reversal for Yen. BoJ Governor Kazuo Ueda has indicated that, even with the shift away from negative rates, the monetary policy stance will remain accommodative, and any tightening efforts are expected to unfold gradually. Additionally, the prospect of other major central banks, such as Fed, postponing policy easing could maintain a significant yield gap, thereby restraining any potential Yen rally.

In other market developments, Euro is trading as the week's standout performer for, followed by Swiss Franc and Sterling. New Zealand Dollar finds itself lagging at the bottom, with market participants keenly awaiting RBNZ's rate decision tomorrow. Australian Dollar, alongside the Dollar, shows weakness, whereas Canadian Dollar and Yen are mixed.

Technically, EUR/USD is now pressing medium term channel resistance after yesterday's strong rebound. The notable support from 55 D EMA is a near term bullish sign. The overall favored case is that correction from 1.7062 has completed with three waves down to 1.6127. Break of 1.6671 resistance will strengthen this bullish case, and target a retest on 1.7062 high next.

In Asia, at the time of writing, Nikkei is down -0.21%. Hong Kong HSI is down -0.48%. China Shanghai SSE is up 0.55%. Singapore Strait Times is down -0.91%. Japan 10-year JGB yield is up 0.010 at 0.700. Overnight, DOW fell -0.16%. S&P 500 fell -0.38%. NASDAQ fell -0.13%. 10-year yield rose 0.039 to 4.299.

ECB's Lagarde highlights wage dynamics in inflation outlook

In a speech delivered at the European Parliament overnight, ECB President Christine Lagarde emphasized the significant role of wage pressures. According to Lagarde, wage pressures "remain strong" across the region, anticipated to be an "increasingly important driver of inflation dynamics" in the coming quarters.

This shift towards wage-driven inflation comes as the contribution of profits, previously a significant factor in domestic cost pressures, begins to wane. Importantly, Lagarde pointed out that labor cost increases are being "partly buffered by profits", preventing a full pass-through to consumer prices.

Lagarde also touched on the risks associated with second-round effects, a concern for economies dealing with inflation. She reassured that ECB's current restrictive monetary policy, combined with a notable decline in headline inflation and well-anchored longer-term inflation expectations, serves as a "safeguard against a sustained wage-price spiral".

Looking ahead, Lagarde expects continued deceleration in inflation rates as the effects of previous shocks diminish and tighter financing conditions exert downward pressure.

Fed's Schmid counsels patience, preemptive policy shifts unnecessary

Kansas City Fed President Jeffrey Schmid emphasized a cautious approach to adjusting Fed's monetary policy. With inflation persistently above the target, coupled with tight labor markets and strong demand, Schmid argues there is "no need to preemptively adjust the stance of policy."

His stance highlights a preference for a measured response, suggesting that "the best course of action is to be patient," a sentiment that underscores the importance of observing the economy's reaction to the already implemented policy tightening measures. He urged to wait for "convincing evidence that the inflation fight has been won."

Schmid also addressed the current state of high inflation, indicating that "we are not out of the woods yet." He pointed out that recent reductions in inflation have primarily resulted from decreases in energy and goods prices, thanks to the rebalancing of oil markets and the healing of supply chains.

Core inflation in Japan eases to 2%, but surpasses expectations

Japan's CPI core (all items ex food) slowed from 2.3% yoy to 2.0% yoy, above expectation of 1.9% yoy. This marks the third consecutive month of decline, reaching the lowest level in 22 months and aligning precisely with BoJ's inflation target of 2%.

The headline CPI also saw a decrease, moving from 2.6% to 2.2% yoy. Nevertheless, CPI core-core (ex-food and energy) showed only modest improvement, edging down from 3.7% to 3.5% yoy.

A significant factor contributing to the overall CPI's decline a -12.1% yoy drop in energy prices, resulting from government interventions to mitigate utility bills through subsidies for oil wholesalers. In contrast, food prices saw 5.9% yoy increase, while accommodation fees surged by 26.9% yoy.

The latest inflation data should fortify the argument for BoJ to terminate its negative interest rate policy soon. However, the decisive factor for the exact timing—be it March or April—hinges on the forthcoming wage negotiations between large enterprises and unions scheduled for March 13.

Looking ahead

Germany Gfk consumer sentiment and Eurozone M3 money supply will be released in European session. Later in the day, US will release durable goods orders, house price index and consumer confidence.

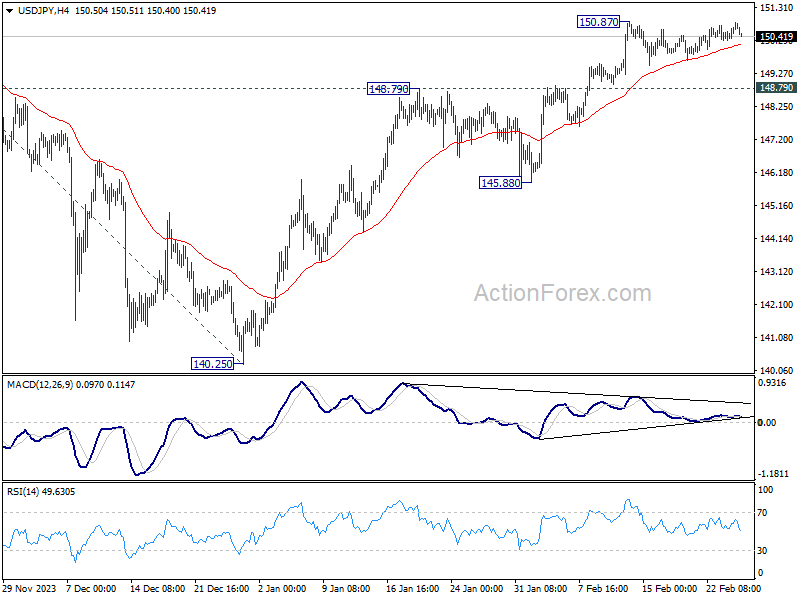

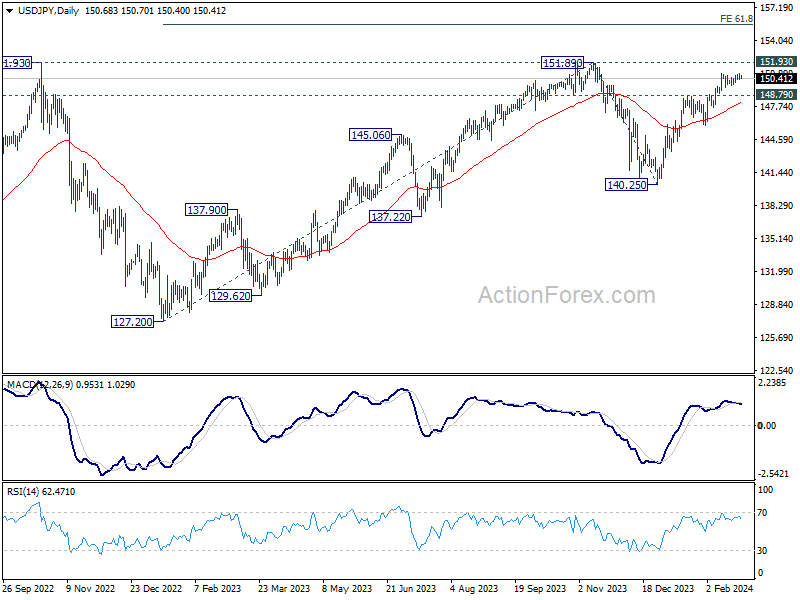

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.39; (P) 150.61; (R1) 150.94; More...

USD/JPY retreats mildly ahead of 150.87 resistance as consolidation continues. Intraday bias remains neutral and outlook is unchanged. In case of deeper retreat, downside should be contained by 148.79 resistance turned support to bring rebound. On the upside, break of 150.87 will resume 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Jan | 2.20% | 2.60% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Jan | 2.00% | 1.90% | 2.30% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Jan | 3.50% | 3.70% | ||

| 00:01 | GBP | BRC Shop Price Index Y/Y Jan | 2.50% | 2.90% | ||

| 07:00 | EUR | Germany Gfk Consumer Confidence Mar | -29 | -29.7 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 0.20% | 0.10% | ||

| 13:30 | USD | Durable Goods Orders Jan | -4.40% | 0.00% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Jan | 0.30% | 0.50% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI y/y Dec | 6.00% | 5.40% | ||

| 14:00 | USD | Housing Price Index M/M Dec | 0.10% | 0.30% | ||

| 15:00 | USD | Consumer Confidence Feb | 114.9 | 114.8 |

Gold Price Faces Uphill Task, Bitcoin Rallies

Key Highlights

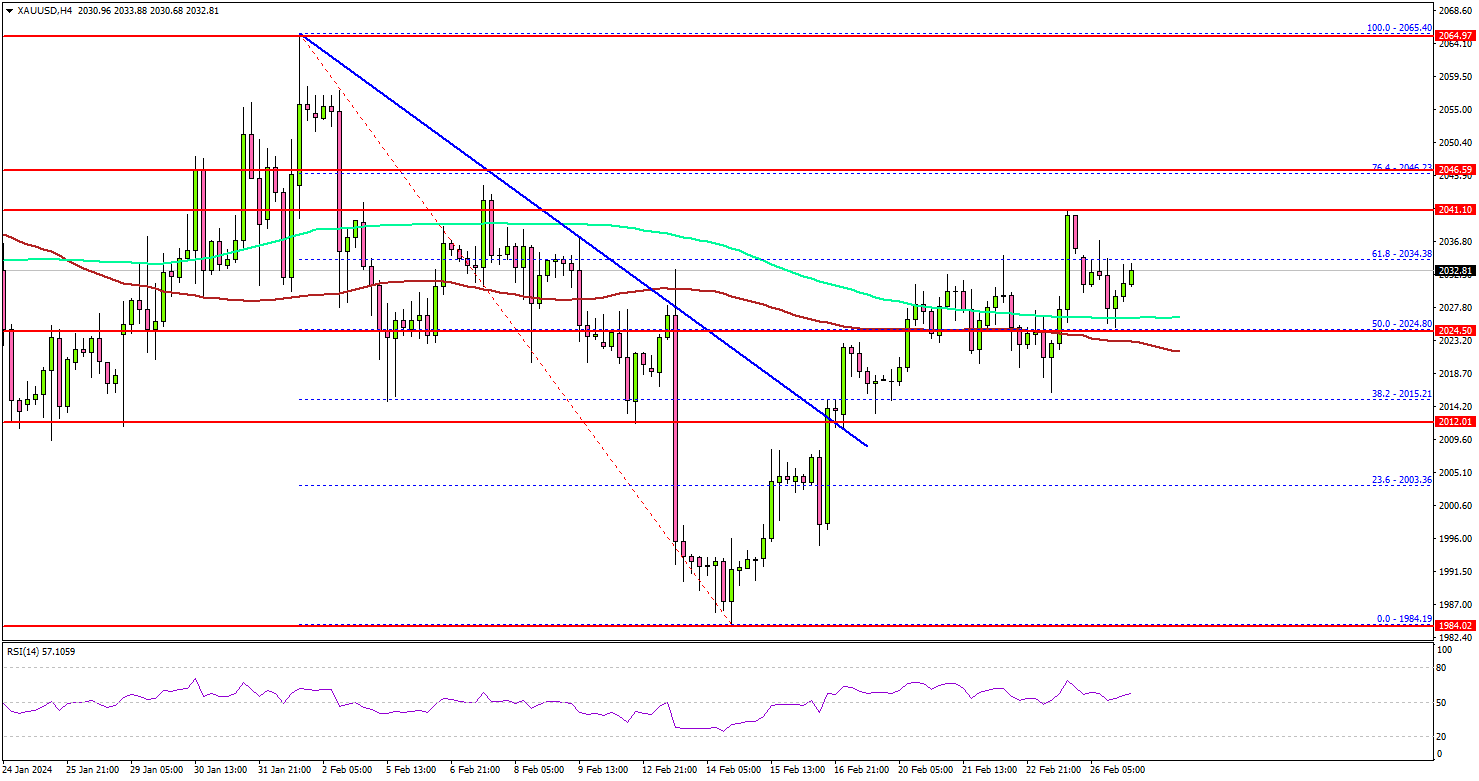

- Gold is attempting a fresh increase above the $2,020 resistance.

- It broke a key bearish trend line with resistance at $2,012 on the 4-hour chart.

- EUR/USD is showing a few positive signs above the 1.0780 resistance.

- Bitcoin prices surged over 10% and climbed toward $58,000.

Gold Price Technical Analysis

Gold prices started a fresh increase from the $1,985 support against the US Dollar. The bulls cleared the $2,000 resistance to start a decent recovery wave.

The 4-hour chart of XAU/USD indicates that the price settled above the $2,015 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

Besides, it broke a key bearish trend line with resistance at $2,012 on the same chart. There was a spike above the 61.8% Fib retracement level of the downward move from the $2,065 swing high to the $1,984 low.

On the upside, the price is facing hurdles near the $2,040 level. An upside break above the $2,040 level could send the price toward the $2,046 resistance. It is close to the 76.4% Fib retracement level of the downward move from the $2,065 swing high to the $1,984 low.

The next major resistance is near the $2,050 level, above which Gold could test $2,065. Any more gains might send it toward $2,080.

Initial support is near the $2,020 level or the 100 Simple Moving Average (red, 4 hours). The first major support sits at $2,012. Any more losses might call for a move toward the $1,985 level in the coming days.

Looking at EUR/USD, the pair is showing a few positive signs above 1.0780, but the bulls face many hurdles above 1.0850.

Economic Releases to Watch Today

- US Housing Price Index for Dec 2024 (MoM) - Forecast +0.3%, versus +0.3% previous.

- US Durable Goods Orders for Jan 2024 – Forecast -4.8% versus 0% previous.

Core inflation in Japan eases to 2%, but surpasses expectations

Japan's CPI core (all items ex food) slowed from 2.3% yoy to 2.0% yoy, above expectation of 1.9% yoy. This marks the third consecutive month of decline, reaching the lowest level in 22 months and aligning precisely with BoJ's inflation target of 2%.

The headline CPI also saw a decrease, moving from 2.6% to 2.2% yoy. Nevertheless, CPI core-core (ex-food and energy) showed only modest improvement, edging down from 3.7% to 3.5% yoy.

A significant factor contributing to the overall CPI's decline a -12.1% yoy drop in energy prices, resulting from government interventions to mitigate utility bills through subsidies for oil wholesalers. In contrast, food prices saw 5.9% yoy increase, while accommodation fees surged by 26.9% yoy.

The latest inflation data should fortify the argument for BoJ to terminate its negative interest rate policy soon. However, the decisive factor for the exact timing—be it March or April—hinges on the forthcoming wage negotiations between large enterprises and unions scheduled for March 13.

Fed’s Schmid counsels patience, preemptive policy shifts unnecessary

Kansas City Fed President Jeffrey Schmid emphasized a cautious approach to adjusting Fed's monetary policy. With inflation persistently above the target, coupled with tight labor markets and strong demand, Schmid argues there is "no need to preemptively adjust the stance of policy."

His stance highlights a preference for a measured response, suggesting that "the best course of action is to be patient," a sentiment that underscores the importance of observing the economy's reaction to the already implemented policy tightening measures. He urged to wait for "convincing evidence that the inflation fight has been won."

Schmid also addressed the current state of high inflation, indicating that "we are not out of the woods yet." He pointed out that recent reductions in inflation have primarily resulted from decreases in energy and goods prices, thanks to the rebalancing of oil markets and the healing of supply chains.

ECB’s Lagarde highlights wage dynamics in inflation outlook

In a speech delivered at the European Parliament overnight, ECB President Christine Lagarde emphasized the significant role of wage pressures. According to Lagarde, wage pressures "remain strong" across the region, anticipated to be an "increasingly important driver of inflation dynamics" in the coming quarters.

This shift towards wage-driven inflation comes as the contribution of profits, previously a significant factor in domestic cost pressures, begins to wane. Importantly, Lagarde pointed out that labor cost increases are being "partly buffered by profits", preventing a full pass-through to consumer prices.

Lagarde also touched on the risks associated with second-round effects, a concern for economies dealing with inflation. She reassured that ECB's current restrictive monetary policy, combined with a notable decline in headline inflation and well-anchored longer-term inflation expectations, serves as a "safeguard against a sustained wage-price spiral".

Looking ahead, Lagarde expects continued deceleration in inflation rates as the effects of previous shocks diminish and tighter financing conditions exert downward pressure.

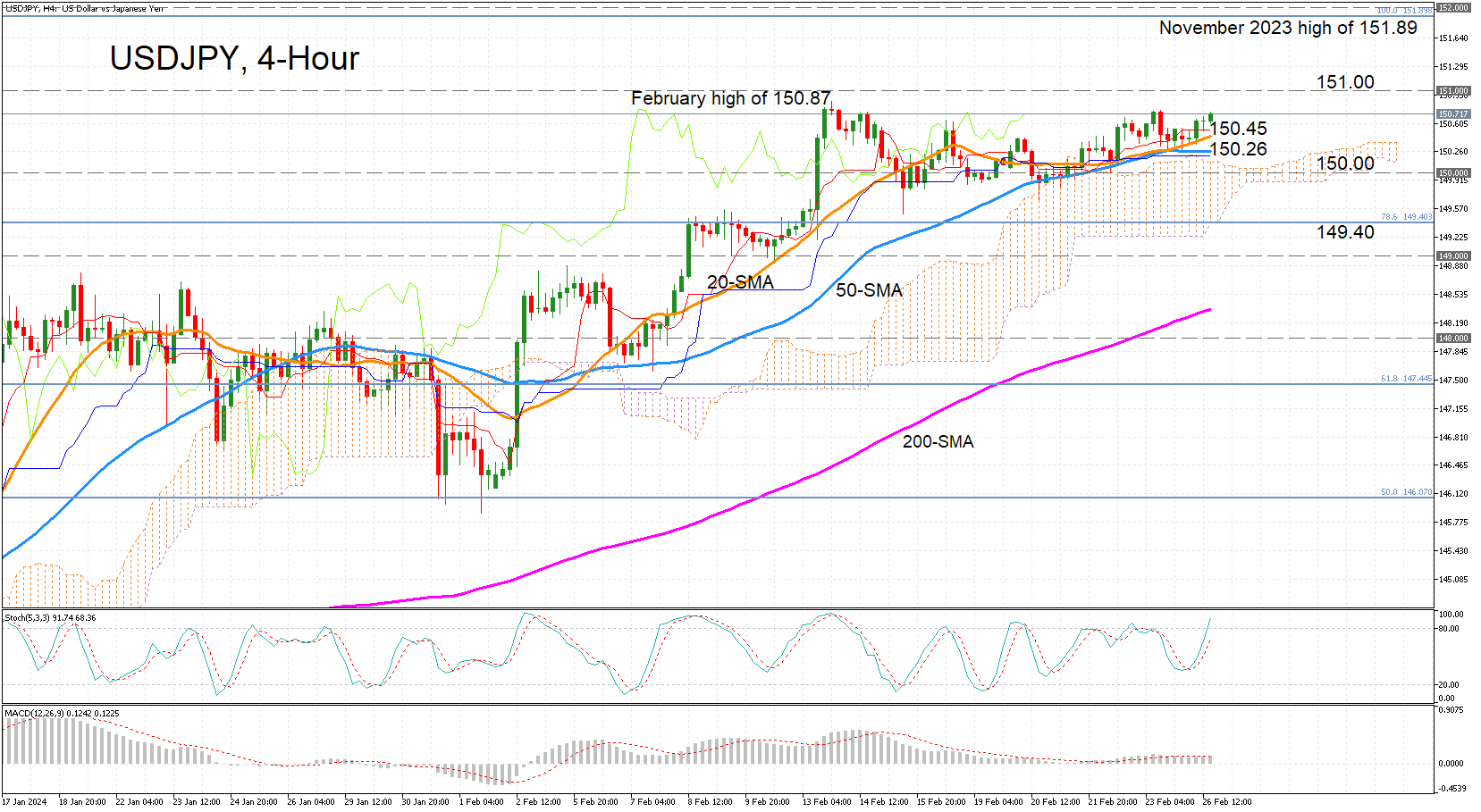

USDJPY Maintains Weak Positive Bias as Bulls Tread Carefully

- USDJPY is barely holding onto upside momentum

- Stiff support propping up the bulls but neutral shift may be unavoidable

USDJPY is slowly crawling back up towards the February 13 peak of 150.87 after a mild pullback. But despite the tight range of the past two weeks and a strong immediate support zone, the bullish forces may not yet be powerful enough to drive the price to fresh highs.

The stochastics have only just turned positive after today’s rebound in the 4-hour chart, while the MACD is flat and is being capped by its red signal line.

An attempt to break above the 150.87 peak is plausible in the short term. However, the real challenge is overcoming the 151.00 level. Clearing this hurdle would put the pair on track to retest the November 2023 top of 151.89 and aim for the 152.00 handle.

To the downside, there is plenty of support that makes it difficult for the bears to pose a significant imminent threat. The 20-day simple moving average (SMA) is the first line of defence at 150.45, followed by the 50-day SMA at 150.26. Slightly lower lies the Kijun-sen line at 150.21, which has flatlined just above the top of the Ichimoku cloud. Should these walls collapse, there’s likely to be further support at the psychologically important 150.00 level.

However, by this point, the near-term bias would have switched to neutral as the price would have already entered the Ichimoku cloud. So, the focus would then quickly turn to the 78.6% Fibonacci retracement of the November-December downleg at 149.40, after which there would be a high risk of slipping below the cloud.

Summing up, USDJPY urgently needs to make a significant push towards the 151.00 area, otherwise it risks being stuck in a consolidation mode. Yet, in the bigger picture, the bullish structure should be safe as long as the price avoids a drop below the 78.6% Fibonacci.

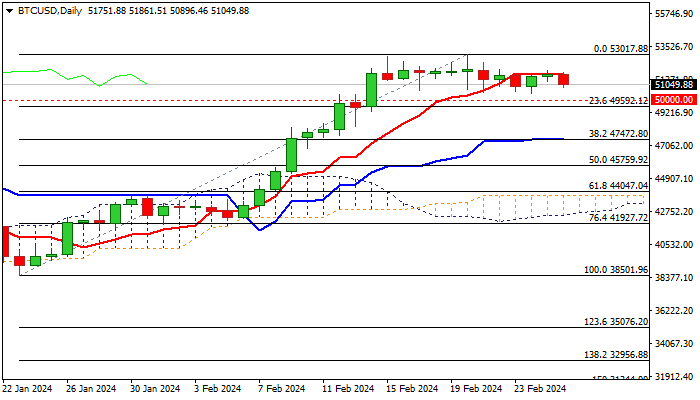

Bitcoin – Bulls Taking a Breather for Consolidation/Limited Correction

Bitcoin eases on Monday, shifting focus towards the floor of near-term consolidation range (50500) established after larger bulls started to run out of steam and left fresh multi-month peak at 53017 (Feb 20).

Early signal of an uptrend’s stall and subsequent correction has been generated from daily RSI bearish divergence and strongly overbought weekly studies.

Last week’s action ended in red Doji candlestick after a four weeks of continuous advance, contributing to initial signals of reversal.

Deeper drop and violation of psychological 50000 support would lead to formation of reversal pattern on weekly chart and further weaken near-term structure for deeper correction.

Broader uptrend remains firmly in play and suggests that limited correction should precede fresh push higher, with extension below 50000 to be contained above 47500 zone (near Fibo 38.2% of 38501/53017 / daily Kijun-sen) to mark a healthy correction and offer better levels to rejoin larger bullish market.

Res: 51600; 52500; 53085; 54330

Sup: 50500; 50000; 48310; 47500

Sunset Market Commentary

Markets

US President Trump easily beat his remaining contender in the Republican primaries, Nikki Haley, in her home state South Carolina this weekend. He cements his grip over the GOP and is gearing up for a duel against President Biden (?) in November elections. We assumed that Trump momentum and USD momentum would go hand in hand, but there’s little evidence of that so far. The reasoning is that a Trump election victory implies a hawkish foreign policy stance against the likes of China (CNY), Europe (EUR), Mexico (MXN),… Irrespective of domestic policies, USD could be by default winner if other currencies lose out in anticipation of another 4-yr term for The Donald. The trade-weighted greenback extends its correction lower today with DXY currently changing hands near 103.75 from an open just below 104. First support (last week’s low) stands at 103.43 with the 103-area providing more backing. EUR/USD rises from 1.0820 to currently 1.0860. The absence of eco data and central bank speeches warns against overinterpreting today’s action. German Bunds underperform US Treasuries with German yields 3 to 4 bps higher across the curve whereas US yields are almost unchanged. European stock markets tread water near last week’s cycle highs. Slovak debt agency Ardal announced the launch of its first syndicated deal of the year later this week (likely tomorrow). They will do a new 10-yr benchmark. YTD, they already raised the significant amount of €3.46 bn via regular auctions, which is a significant amount of this year’s projected funding need of (at least) €10bn.

Later this week, attention turns to PCE deflators in the US (Thursday), the Fed’s preferred inflation gauge. Despite strong expected m/m readings (0.3% headline, 0.4% core), the yearly figures should have eased further in January, be it only gradually (especially for the core gauge). CPI’s earlier this month, if any, suggest upside risks. February CPI in the euro area (Friday, after national readings in the run-up) could drop to 2.5% y/y even as monthly prices may jump a 0.6%. Strong negative base effects (which last through April) are the reason why. Similarly, core inflation is set for a drop sub 3%. Aside from some price data, the US manufacturing ISM is on tap on Friday. The latter is seen extending the bottoming out process that started in November (49.5 from 49.1) on inventory rebuilding and with some export partners showing new (export) momentum.

News & Views

The head of the World Trade Organization said trade volumes last year have probably fallen short of the 0.8% forecast made in October. Speaking during the WTO’s 13th biennial conference in Abu Dhabi, Ngozi Okonjo-Iweala added that the 3.3% projection made for 2024 (before the war between Hamas and Israel) may be too optimistic as well. She said that while global commerce proved resilient through the pandemic, is it now performing weaker than expected amid economic headwinds and a shift towards protectionism. While the US and India are “doing quite well”, the WTO president said demand is sluggish across most other major economies. Supply for its part is constrained by wars and climate-related problems including drought that is slowing down shipping through the Panama Canal.

European agricultural ministers urge the EU to increase the €60bn per year Common Agricultural Policy (CAP) subsidy scheme, the Financial Times reported quoting Ireland’s McConalogue and Belgium’s Clarinval. Calls for that are growing along with European-wide farmer protests which have flared up again today a.o. in Brussels. The CAP accounts for about a third (some €390bn) of the €1.21tn common budget (2021-2027). Increasing the amount either requires heated discussions about a shift in priorities or increase national contributions to obtain a larger budget. The latter is no easy task given how stretched government finances already are currently. Aside from more funds, farmers also demand a relaxation in environmental regulations and ask for several trade deals to be reconsidered, saying they allow cheap imports to undercut prices for domestic producers.

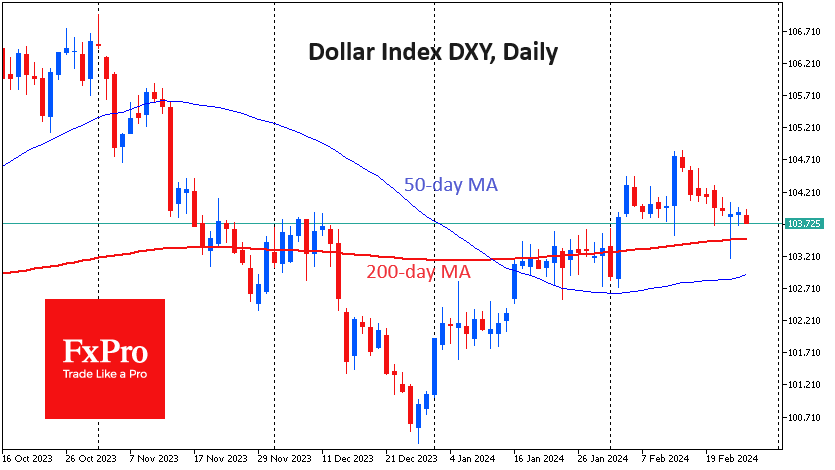

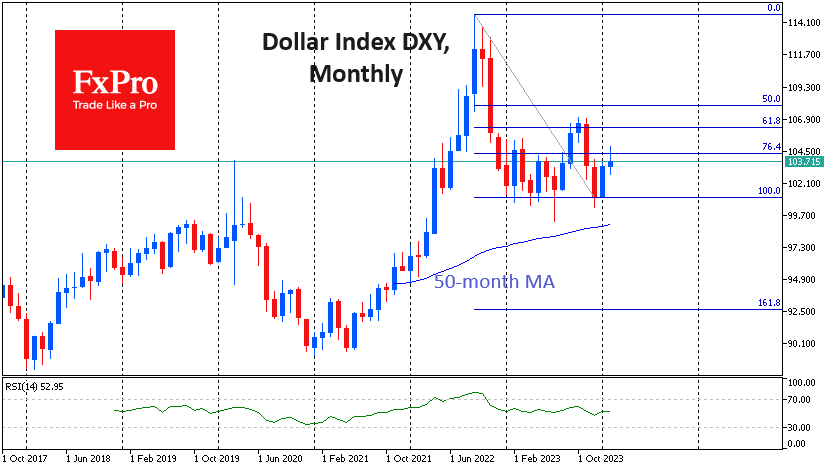

Time for the Dollar to Choose a Trend

The Dollar Index is giving up positions painfully slowly. It is under pressure for the ninth session in a row, but at the same time, the market is unable to accelerate or break this downtrend. Individual currency pairs are now testing critical local levels. The ability to finally break through them could set the trend for the coming weeks.

The Dollar Index has fallen from a high of 104.85 on February 14th to 103.7. This level was strong resistance from late November to early February. It could now act as support. This is also a historically important level for the Dollar Index as it was the peak in March 2020, which took 26 months to overcome.

It is logical to expect increased volatility in this area as this is where global trend selection takes place. A decisive move lower will open a quick path to last year’s lows around 100.0. Approaching these levels will make the main scenario a further multi-month decline in the US currency, with a final target in the 90.0-92.5 range.

The ability to develop an offensive from these levels would demonstrate the strength of the dollar bulls after the pause. In this case, the DXY could quickly return to last year’s October-November highs near106.8. This, in turn, should be followed by a recovery of the dollar to multi-year highs towards 114.5-115.0.

Keeping the dollar in balance this week rests on the shoulders of the 10 FOMC members who are scheduled to speak this week. On the macro data front, the market will be watching Thursday’s Personal Income and Expenditure and PCE price indices.

On the technical front, the EURUSD, AUDUSD, and USDCHF are all trading around their 200-day moving averages, the GBPUSD is trading around its 50-day MA, and the USDJPY is approaching 151 level, where the pair made a brutal multi-week bearish reversal in October 2022 and November 2023.