Sample Category Title

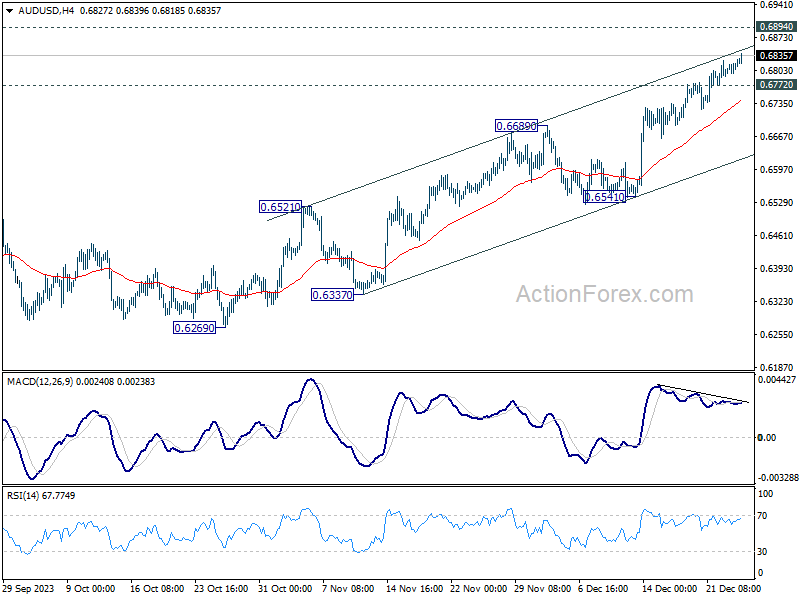

AUD/USD Daily Report

Daily Pivots: (S1) 0.6801; (P) 0.6815; (R1) 0.6837; More...

AUD/USD's rally from 0.6269 continues today and hits as high as 0.6839 so far. Intraday bias remains on the upside for 0.6894 resistance first. Sustained break there will target 0.7156 next. On the downside, below 0.6772 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 0.6689 resistance turned support holds, in case of retreat.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

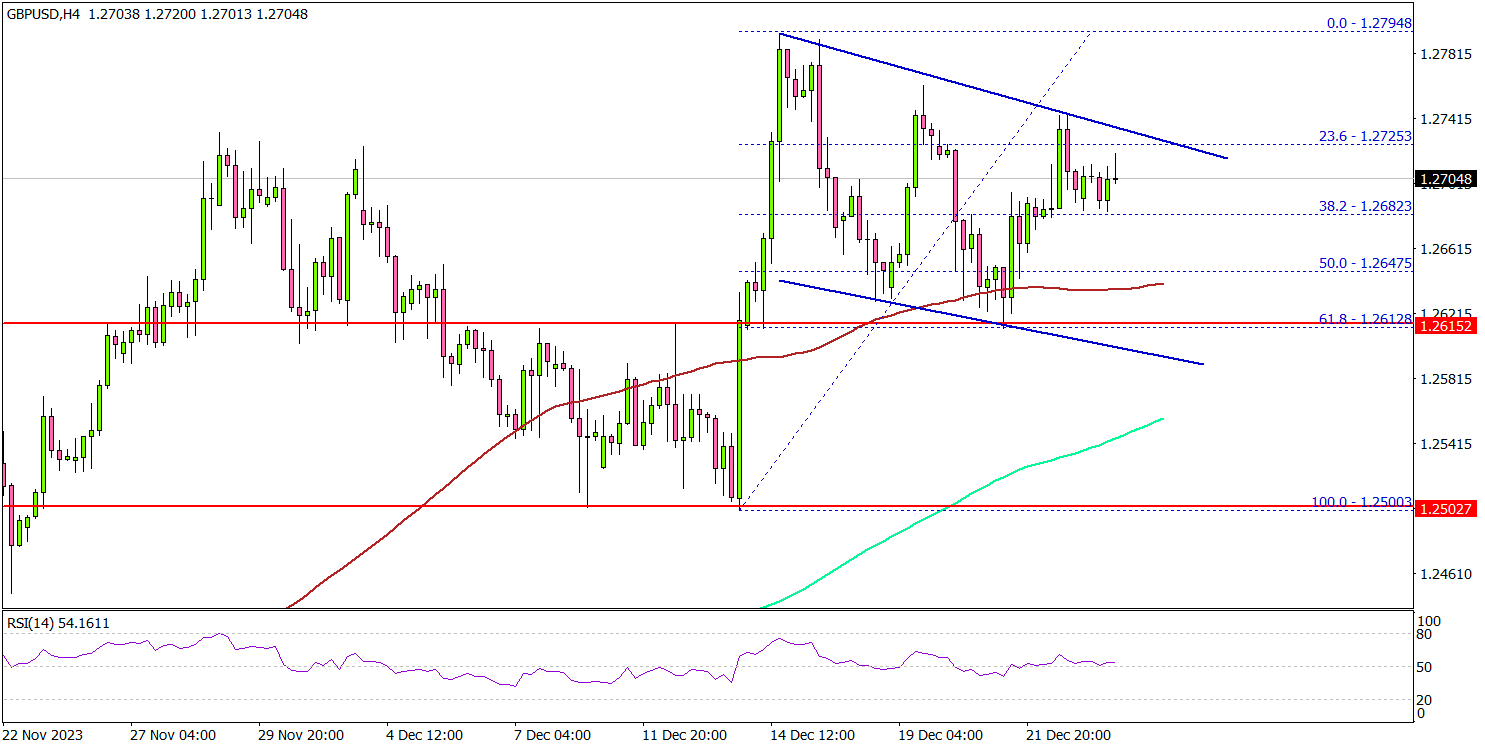

GBP/USD Seems Primed For More Gains Above 1.2800

Key Highlights

- GBP/USD is eyeing more gains above the 1.2750 level.

- A major bullish flag is forming with resistance near 1.2725 on the 4-hour chart.

- EUR/USD is gaining bullish momentum above the 1.0980 zone.

- Oil prices could gain pace for a move toward the $78 level.

GBP/USD Technical Analysis

The British Pound formed a base above the 1.2600 zone against the US Dollar. GBP/USD climbed higher above the 1.2650 level to set the pace for more gains.

Looking at the 4-hour chart, the pair settled above the 1.2650 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

The pair is now following a major bullish flag with resistance near 1.2725 on the same chart. If the bulls push the pair above the flag resistance, there could be a sharp increase. The next key resistance is near the 1.2800 level.

A close above the 1.2800 zone could open the doors for more upsides. The next stop for the bulls might be 1.2850. Any more gains might call for a drift toward the 1.2880 level.

If there is a downside correction, the pair might find bids near the 1.2650 level. The next major support is 1.2600, below which the pair might decline and test 1.2540. Any more losses might send the pair toward the 1.2400 support.

Looking at EUR/USD, the pair is trading in a positive zone and the bulls could soon aim for a move toward the 1.1200 zone.

Economic Releases

- Richmond Fed Manufacturing Index for Dec 2023 - Forecast -7, versus -5 previous.

BoJ’s Dec meeting highlights lack of urgency in tightening

Summary of Opinions of BoJ's December 18-19 meeting revealed a prevailing view among the board members on a lack of urgency in tightening monetary policy. The consensus was that delaying the decision to tighten poses minimal risk. This general sentiment indicates BoJ's preference for a measured approach, prioritizing stability and sufficient data before considering changes.

The summary acknowledged that the sustainable and stable achievement of price stability target, set at 2%, is not yet certain. In considering whether to end the negative interest rate policy and yield curve control framework, the board stressed the importance of confirming a virtuous cycle between wages and prices.

To reach the 2% inflation target sustainably, one member noted that "growth momentum in nominal wages needs to strengthen further". It's also noted that wage growth has not kept pace with inflation. And, even with potentially higher wage hikes in the spring, the risk of inflation significantly surpassing 2% remains "low". Current policy approach does not risk "falling behind the curve" in response to inflation dynamics.

The summary also noted that acknowledged that the need to "rapidly tighten monetary policy is small". At the same time, "the cost incurred if this risk materializes would be significant."

BoJ’s Ueda: Policy adjustment possible with strengthened wage-price relationship

BoJ Governor Kazuo Ueda, in a speech yesterday, acknowledged that while the probability of achieving the central bank's price target is gradually increasing, it is still not high enough to justify a change in the current monetary policy.

Ueda highlighted, "The likelihood of Japan's economy getting out of the low-inflation environment and achieving our price target is gradually rising, though the likelihood is still not sufficiently high at this point."

The Governor pointed out the significant uncertainties surrounding economic and price conditions both domestically and internationally. He emphasized the importance of observing how firms' wage- and price-setting behaviors evolve in response to these conditions.

Ueda also mentioned that "we will likely considering changing policy," if there is significant strengthening of the virtuous cycle between wages and prices, leading to a sustainable and stable likelihood of achieving BoJ's price target.

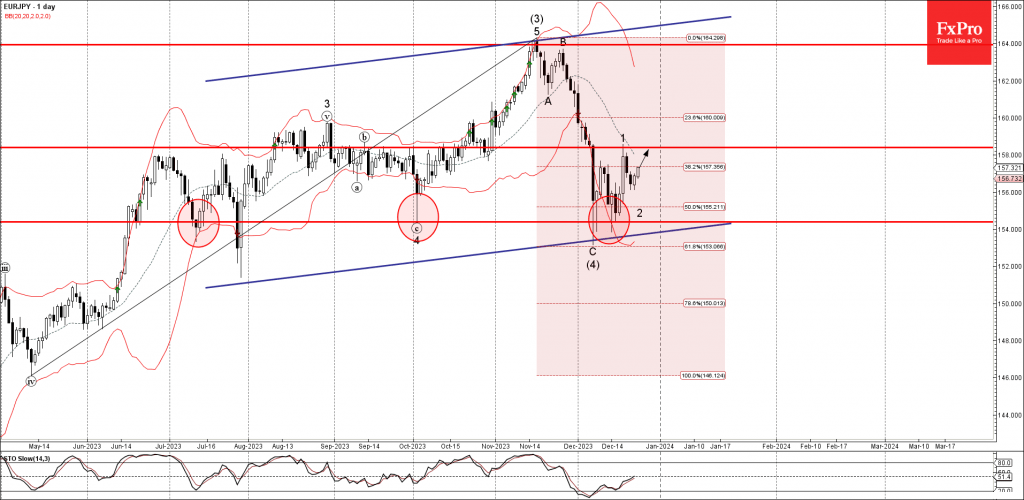

EURJPY Wave Analysis

- EURJPY rising inside impulse wave (5)

- Likely to reach resistance level 158.40

EURJPY rising inside the intermediate upward impulse wave (5), which started earlier from the major support level 154.40 (which has been reversing the price from July).

The support level 154.40 was additionally strengthened by the 50% Fibonacci correction of the upward impulse from May and by the support trendline of the daily up channel from July.

Given the clear daily uptrend, EURJPY currency pair can be expected to rise further to the next resistance level 158.40 (top of the earlier minor impulse wave 1).

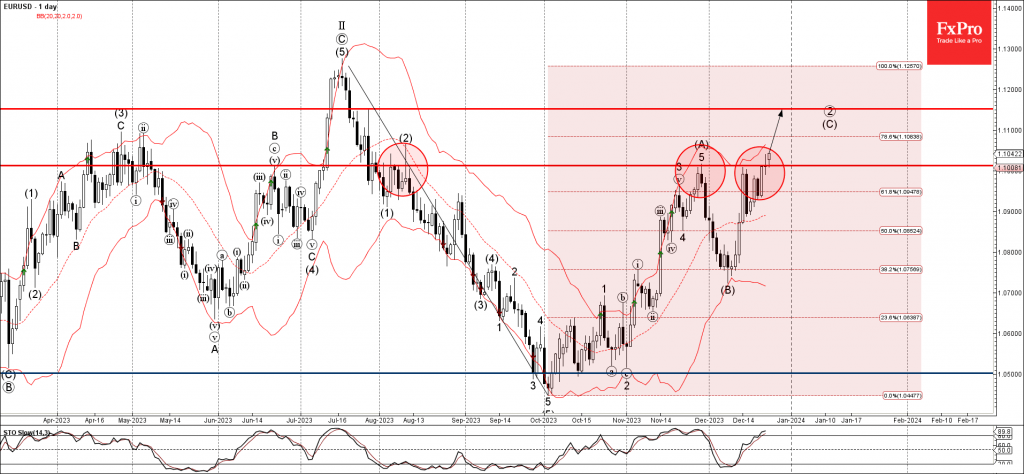

EURUSD Wave Analysis

- EURUSD broke resistance level 1.1015

- Likely to reach resistance level 1.1150

EURUSD currency pair broke the resistance level 1.1015 (which has been reversing the price from August).

The breakout of the resistance level 1.1015 accelerated the active medium-term impulse wave (C) from the start of December.

Given the prevailing bullish euro sentiment, EURUSD currency pair can be expected to rise further to the next resistance level 1.1150 (target price for the completion of the active impulse wave (C)).

Canadian Dollar Posts Another Strong Week

- Canadian GDP remains flat for a second straight month

- PCE Price Index eases

The Canadian dollar is showing limited movement on Tuesday. In the European session, USD/CAD is trading at 1.3248, down 0.14%. Canadian banks are closed for a holiday, which means it should remain an uneventful day for the Canadian dollar. As there are no Canadian events this week, US releases could have a magnified impact on the movement of the Canadian dollar.

The Canadian dollar posted a second consecutive winning week, with gains of 0.83%. The Canadian dollar has sparkled in December, climbing 2.2% in both November and December.

Canada’s GDP stalls agaon

Canada’s economy remains stagnant as GDP was flat in October for a second straight month. This was below the market consensus of 0.2%. The silver lining was retail sales, which jumped 1.2%, the sharpest pace of growth since January. The preliminary estimate for November stands at 0.1%. GDP in the third quarter came in at -0.3%, and Canada will have to post positive growth in Q4 to avoid a recession, which technically is two consecutive quarters of negative growth.

The US wrapped up last week with the PCE Price Index, the Federal Reserve’s preferred inflation indicator. The headline reading fell to 2.6% y/y in November, down from a downwardly revised 2.9% in October and lower than the market consensus of 2.8%. The core rate eased to 3.2%, down from a downwardly revised 3.4% and lower than the market consensus of 3.3%.

The numbers are an encouraging sign for the Federal Reserve and support the case for rate cuts next year. However, personal spending and income were higher than expected and could temper these expectations. Personal income edged up to 0.4% m/m in November, up from an upwardly revised 0.3% in October and matching the consensus estimate. Personal spending gained 0.2%, up from a downwardly revised 0.1% and shy of the consensus estimate of 0.3%.

Fed Chair Powell has pencilled in three cuts in 2024 but the markets have priced in up to six cuts. Investors have priced in a rate cut in January at 14%, up from 8% a week ago, according to the CME’s FedWatch tool.

USD/CAD Technical

- USD/CAD tested support at 1.3262 earlier

- There is resistance at 1.3262 and 1.3289

2023 In Review: A Look Back At The Highlights Of The Year

The year 2023 commenced after two years of economic uncertainty and heavy inflation across Europe and North America, home to leading financial markets, with major currencies such as the euro and the US dollar, and financial hubs including London, New York, Chicago, Frankfurt, and Toronto.

These continents, where major stock exchanges operate and the S&P 500, NASDAQ, and FTSE 100 indices represent the top stocks of the top listed companies in Britain and the US, witnessed a dynamic interplay of economic recovery, inflation challenges, and policy adjustments.

The European and North American economies had spent 2023 recovering from a sustained period of inflation and cost of living issues (Britain and mainland Europe), and in the US, yet more bank collapses and a close call with state insolvency as the US Government had to raise the debt ceiling to stop it defaulting on its existing commitments, highlighting the country's huge national debt.

Inflation did decline during 2023, but central bank policy on both sides of the Atlantic favoured continued increases in interest rates, despite the US inflation going down from 11% in mid-2022 to around 3.1% now, and the British inflation rate is 3.9% now whereas it was also in double figures during 2022. Now, we move on to looking at specific markets.

Indices – S&P Is The Stellar Performer

With regard to indices, the outright performer during the course of this year has been the S&P 500, which has managed to achieve a return of approximately 24% year-to-date, which is a remarkable increase over its usual average of approximately 10%.

As far as global indices are concerned, this stellar performance from the companies whose listed stocks are included in the S&P 500 index puts it in second place globally, with only the Nasdaq 100 Index having outshone it. However, it is worth noting that Japan's Nikkei 225, whilst not considered one of the top performers by many analytical publications, has done well with a gain of 26.35% year-to-date. Thus, depending on the rankings referred to, the S&P 500 ranks between second and third place in terms of annual performance - but the point is that it has more than doubled its annual average in 2023.

What is fascinating about this is that just seven companies, those being Apple, Google's parent Alphabet, Meta Platforms (formerly Facebook), Microsoft, NVIDIA, Amazon.com, and Tesla, had driven the S&P 500 index to its stratospheric growth during the first six months of 2023.

What a contrast to the previous year's tech stock doldrums!

The High Volatility of the Oil Market

In commodities markets, international relations, politics, and, in the case of the past two years, wars in regions with oil-producing significance are historically major factors causing market volatility.

Just almost two years on from the beginning of the war between Ukraine and NATO allies and Russia, which is an OPEC+ country and one of the world's largest suppliers of energy products, there is now another war, this time in the Middle East which involves Israel backed by Western NATO allies, with oil-producing nations such as Iran being in the background.

With such instability in the geopolitical sphere, oil prices have been volatile this year. There was notable volatility all year in oil markets; however, by mid-October 2023, the war in the Middle East had caused oil prices to climb to $94 a barrel.

It also reignited fears among oil traders and economists that markets could breach the $100 a barrel mark.

This did not happen, and prices slowed again. By the beginning of December, the focus was on whether oil-producing countries would scale back production a bit more in order to bolster demand.

These volatile peaks this year have been sudden and shorter-lived than in 2022 when they were noticeably longer. In mid-2022, it was entirely possible to pull into a fuel station in France and pay 2.20 euros for a litre of unleaded fuel!

Tech Stocks – The Enthusiasm Is Back

2023 heralded a return to the forefront of tech stocks. This was reflected heavily in the strident performance of the S&P 500 index in the United States; however, when looking at the entirety of US-listed technology stocks, which are largely listed on New York's Nasdaq exchange, it would be fair to call 2023 the year of an absolute resurgence. Nasdaq Composite gained over 40% in value year-to-date.

This performance has overshadowed the period of time during 2021 and 2022 when somewhat risky entries into the Nasdaq listings by SPAC companies were de rigueur, and the ensuing year of 2022 was a year of total decline in tech stocks.

This has reversed, and Nasdaq's performance in 2023 demonstrates a return to favour of tech stocks, and not one mention of the four-letter acronym SPAC has been uttered for almost two years now. Stability, it seems, is back on track.

The bricks-and-mortar FTSE100 index in the United Kingdom has once again demonstrated that institutional stability gained by the tracking of age-old blue-chip corporations listed on the London Stock Exchange is a bastion of buoyancy. There are a series of financial services giants included in the FTSE 100, along with engineering stalwarts, housebuilders, entertainment and retail conglomerates and scientific corporations.

Perhaps rather surprisingly, Hargreaves Lansdown, Britain's largest retail financial services company, was deleted from the FTSE 100 index in the last quarter of 2023. However, the index itself has performed with average results this year.

The euphoric surge of 2021, when it reached 7,000 points for the first time, was not replicated in 2023, and despite some degree of celebration when it approached 8,000 during the earlier part of 2023, this was short-lived and never replicated.

Stability and steadiness are the order of the day when it comes to Britain's stock markets. It is a different animal to the US tech sector, and far more grey suit, and less Silicon Valley.

Australian Dollar: Association With Commodities?

Now we move to currencies, and whilst on the subject of commodities, we can start with the Australian dollar.

During the first month of 2023, there was a steady rise in AUD/USD and many traders considered at the time that AUD/USD was going to be considered one of the most preferred currency pairs for traders in the commodities market, which makes sense given Australia's highly important mining and mineral extraction industry which trades its raw materials on Australia's commodities markets.

Toward the end of this year, the AUDUSD was moderately volatile. The AUDUSD pair moved from its high point in early 2023 of 0.71 on the 26th of January through a series of moderate spikes but an overall downward move during the second half of the year, resting at 0.63 on the 3rd of October.

The Cable - Volatility Is Back

The GBPUSD pair, often referred to as 'The Cable,' has been very volatile this year, which is interesting given that both the US and Britain have been faced with similar economic matters such as fighting inflation, post-lockdown debts, and energy price increases far beyond the percentage of retail price inflation. Just in the past month alone, the GBPUSD went from 1.25 to 1.27. These currencies are often not volatile at all. Thus, a movement of a few cents in either direction is a matter to consider when measuring the market sentiment.

EURUSD: Similar Policies, Different Movements

The EURUSD pair has experienced higher and lower moments during the course of this year, and despite the European Union member states having experienced similar challenges and been subject to similar geopolitical matters as the United States and Britain, there has been some movement between the euro and the US dollar.

By mid-July, during the height of summer, the EURUSD pair was up to 1.12, which is a considerable uptick from the low point of 1.05 at which it began the year. Interestingly, the European Central Bank had held off from making interest rate increases during 2022, something that was being watched very closely, whilst the US and British monetary policy was staunchly in favour of continued increases.

Of course, the ECB ultimately gave way and did increase rates, but far less frequently than its Anglosphere counterparts, whose major currencies are traded against the euro.

Overall, the European economy has done quite well during 2023, and the energy-related matter of natural gas supplies being in jeopardy due to political sanctions appears to have largely resolved itself. As the final two weeks of 2023 are in swing, the EURUSD stands at 1.09, which is not as high as the summer but a little higher than its low entry in January this year.

Bank Demises – Business As Usual

In the US, there have been a few economic issues that have dented investors' and economic analysts' confidence. The aforementioned bank-related toxicity in which some large, well-established banks became insolvent was a major event of 2023.

Silicon Valley Bank collapsed after 50 years in business, and the surrounding contagion saw the end of some smaller regional banks like First Republic Bank, which got mopped up by JPMorgan after its demise.

Credit Suisse, one of the world's largest Tier 1 investment banks, with a substantial market share in interbank FX currency dealing, finally went bankrupt, and whilst that is a Swiss bank, the effect of its demise was mostly felt on Wall Street. Oddly, the US dollar has not been too adversely affected by these catastrophes, despite them following a similar set of circumstances to the ones that caused the global financial crisis in 2008/2009.

This time, the news passed, and the US dollar has remained very strong. There has been absolutely no talk of the world's reserve currency being usurped by another major, even during the period earlier this year when the country had to increase its debt ceiling to be able to continue to service its national debt, which is higher than the United Kingdom's national debt in terms of percentage debt to GDP ratio, and with the UK having had no such issue in servicing its commitments.

Overall, the US dollar has held up very well indeed over not just 2023 but also previous years, despite lockdowns, involvement in wars, and spiralling national debt. It is clear that the hard-working nature of the American public has kept productivity high.

Monetary Policy: Interest Rate Hikes Blighted 2023

Almost absolutely unified in terms of monetary policy, the Bank of England and the US Federal Reserve have been continuing to increase interest rates even during a period in which inflation is decreasing. There has been some talk of stopping the interest rate increases, but this has not yet materialised. The cost of maintaining existing commitments for large corporations has increased due to having to service loans at higher rates, but as is clear from the stock market performance of larger, well-capitalised corporations, this has not hampered their performance at all.

Britain has lived through Brexit-related wranglings and the shortest prime ministerial term in history, whereas the US lived through almost going bankrupt. Despite the media sensationalism, however, both countries are in overall good shape as far as everyday life is concerned for most people.

Volatility in the currency markets appears to be originating from news-driven trading, which is perhaps why it is so sudden and changeable.

It's been a fascinating year. A year of rebuilding the economy from bizarre policy and a year of battling global headwinds. What will 2024 bring?

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/JPY Yawns after BoJ CPI Slips

- BOJ Core CPI falls to 2.5%

- BoJ’s Ueda hints at possible shift in policy

The Japanese yen is showing little movement on Tuesday. In the European session, USD/JPY is trading at 142.39, down 0.04%.

BoJ Core CPI drops more than anticipated

Japanese inflation indicators have been heading lower. Last week, Core CPI, which excludes fresh food but includes fuel costs, dropped in November from 2.9% to 2.5%. On Tuesday, the Bank of Japan’s Core CPI index followed suit and declined to 2.7% in November, down from 3.0% in October.

Core inflation may have dropped in November, but it has exceeded the BoJ’s 2% target for well over a year and speculation is high that the central bank will shift policy and lift interest rates from negative territory, perhaps in early 2024. Such a move would mark a sea change in monetary policy, after decades of negative rates.

We have seen that tweaks to the yield curve control program have triggered sharp movement from the yen, and it’s a safe bet that a shift in rate policy would send the yen flying higher. BoJ policy meetings have become market-moving events and every comment from a senior BoJ official has the potential to shake up the currency markets.

BoJ Governor Ueda has hinted that the economy is slowly moving towards the BoJ target, but the central bank wants to see stronger wage growth before it considers inflation to be sustainable. The BoJ has insisted that current inflation is being driven by cost-push factors and is not sustainable. On Monday, Ueda said that he would consider shifting policy if the “cycle between wages and prices intensifies” but added that there was no specific timing to changing the Bank’s ultra-loose policy.

The US wrapped up last week with the PCE Price Index, the Federal Reserve’s preferred inflation indicator. The headline reading fell to 2.6% y/y in November, down from a downwardly revised 2.9% in October and lower than the market consensus of 2.8%. The core rate eased to 3.2%, down from a downwardly revised 3.4% and lower than the market consensus of 3.3%.

The numbers are welcome news for the Fed and support the case for rate cuts next year. Fed Chair Powell has pencilled in three cuts in 2024 but the markets have priced in up to six cuts. Investors have priced in a rate cut in January at 14%, up from 8% a week ago, according to the CME’s FedWatch tool.

USD/JPY Technical

- USD/JPY is putting pressure on resistance at 142.55. Above, there is resistance at 142.78

- There is support at 142.34 and 142.11