Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0960; (P) 1.0986; (R1) 1.1038; More...

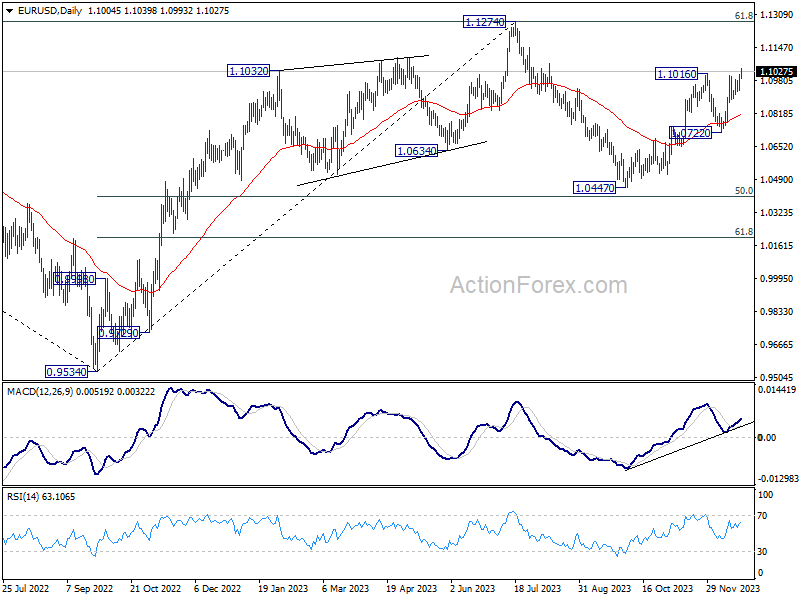

EUR/USD's rally from 1.0447 resumed by breaking through 1.1016 resistance. Intraday bias is back on the upside. Further rally should be seen to retest 1.1274 high. Strong resistance should be seen from there to limit upside, at least on first attempt. On the downside, below 1.0929 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.0722 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

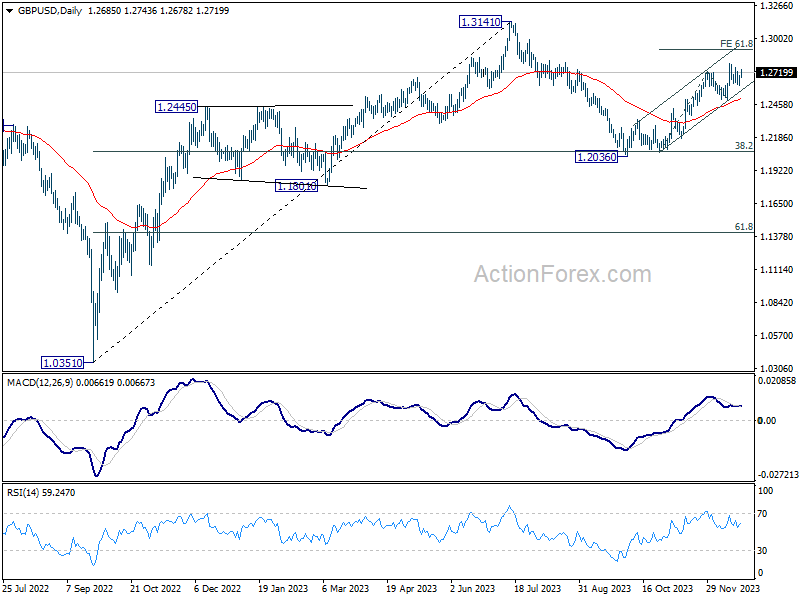

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2636; (P) 1.2666; (R1) 1.2720; More...

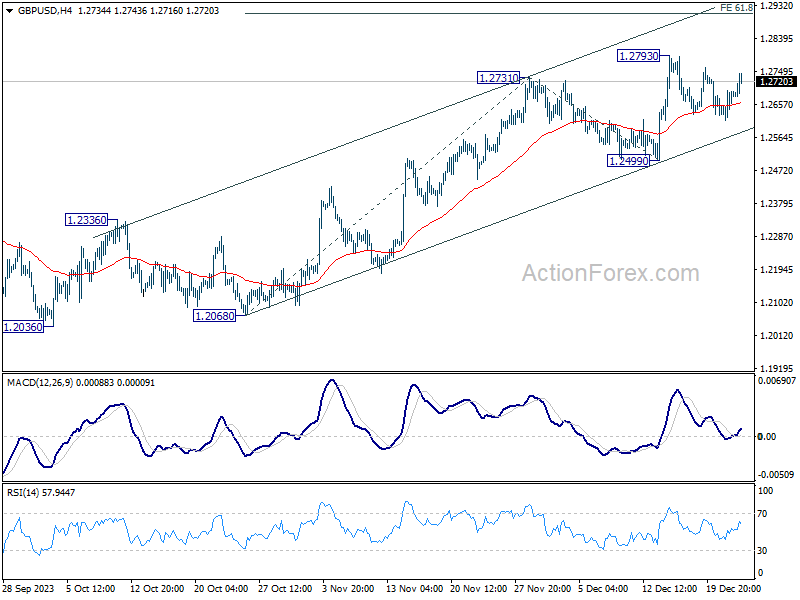

GBP/USD is still bounded in range below 1.2793 and intraday bias remains neutral at this point. Further rally is still expected as long as 1.2499 support holds. . On the upside, firm break of 1.2793 will resume the rally from 1.2036. Next target is 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

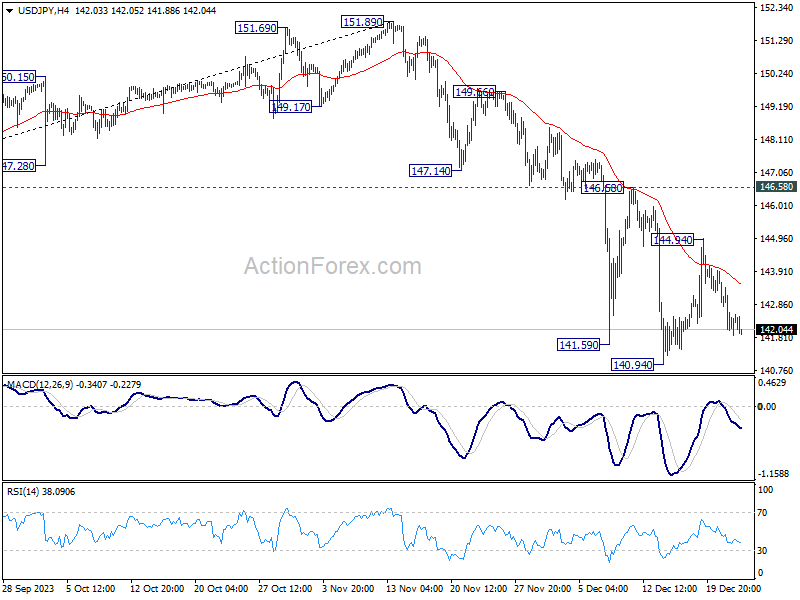

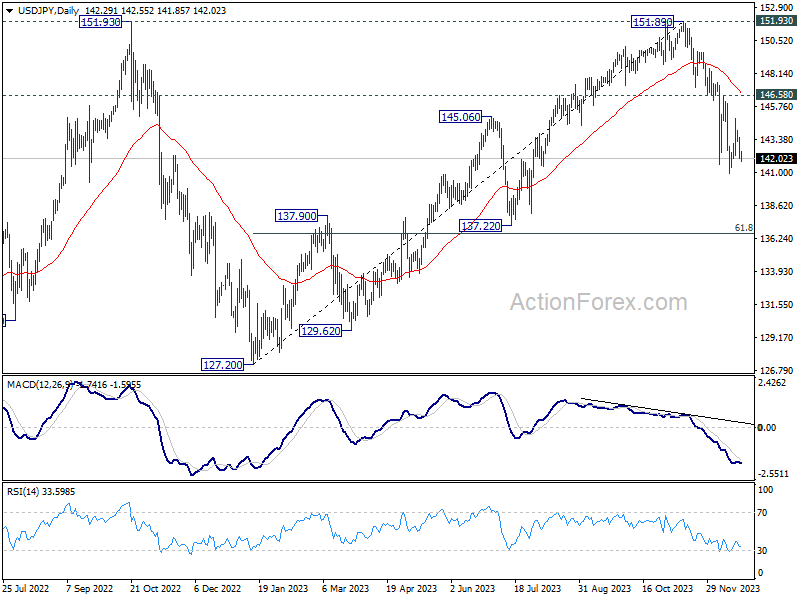

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.57; (P) 142.60; (R1) 143.14; More...

USD/JPY is still bounded in consolidation from 140.94 and intraday bias stays neutral. Also, outlook will remain bearish as long as 146.58 resistance holds. Firm break of 140.94 will resume the whole fall from 151.89. Next target will be next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

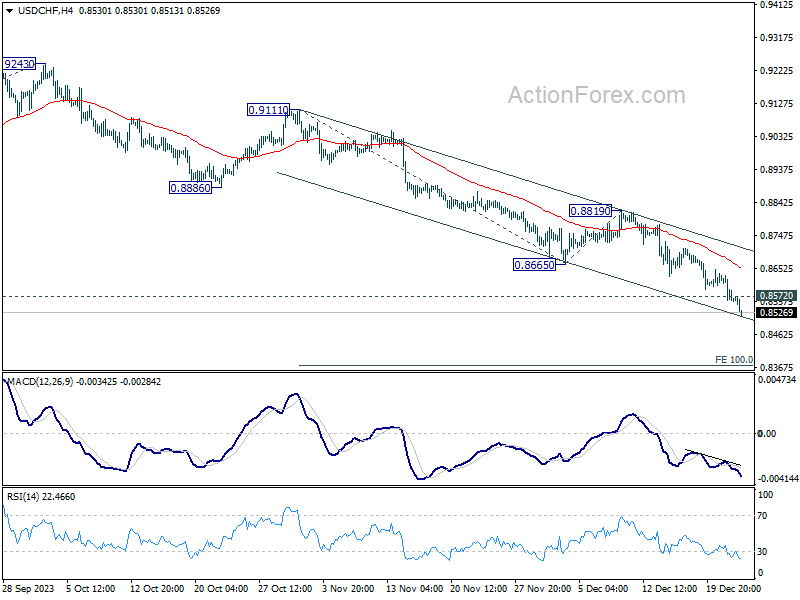

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8536; (P) 0.8587; (R1) 0.8614; More....

USD/CHF's decline continues today and falls through 0.8551 support without noticeable recovery. Longer term down trend is resuming. Intraday bias remains on the downside for 100% projection of 0.9111 to 0.8665 from 0.8819 at 0.8373 next. On the upside, above 0.8572 minor resistance will turn bias neutral and bring consolidations first. But risk will stay on the downside as long as 0.8665 support turned resistance holds.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

Dollar Falters on Soft PCE Inflation Data, Sterling Rises on Retail Sales

Fresh selloff is seen in Dollar in early US session after lower than expected headline and core PCE inflation readings. While another month of progress might still be insufficient to prompt Fed for an early rate cut, at least, things are heading in the right direction. The greenback is set to end as the worst performer for the week. The only question is whether it could stage a recovery against Yen in the final ours to climb one position up.

Sterling was lifted by stronger than expected retail sales data today, but it's still lagging behind others for the week, just performing better against Dollar and Yen. Swiss Franc is currently the leader, followed by Aussie and Kiwi. Canadian Dollar is mixed, and GDP disappointment is certainly giving no help.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 0.16%. CAC is up 0.16%. Germany 10-year yield is up 0.0003 at 1.964. UK 10-year yield is down -0.0332 at 3.502. Earlier in Asia, Japan 10-year JGB yield rose 0.0333 to 0.626. Nikkei rose 0.09%. Hong Kong HSI fell -1.69%. China Shanghai SSE fell -0.13%. Singapore Strait Times rose 0.89%.

Merry Christmas to our readers. We'll be back on December 27.

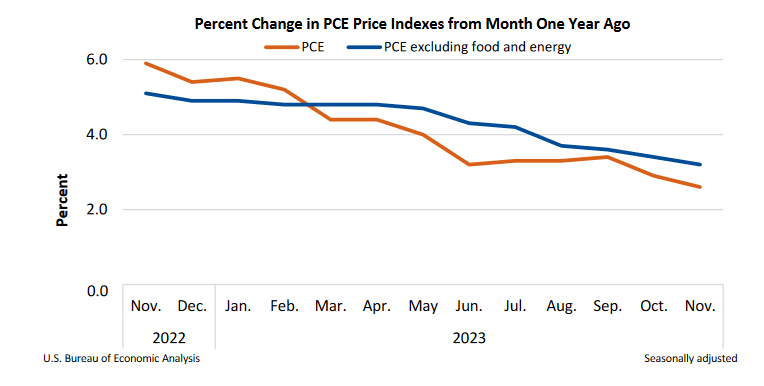

US PCE slows to 2.6% in Nov, core PCE down to 3.2%, miss expectations

US personal income rose 0.4% mom or USD 81.6B in November, matched expectations Personal spending rose 0.2% mom or USD 46.7B, below expectation of 0.3% mom.

PCE price index fell -0.1% mom, below expectation of 0.0% mom. Core PCE price index (excluding food and energy)rose 0.1% mom, below expectation of 0.2% mom. Goods prices fell -0.7% mom while services prices rose 0.2% mom. Foods prices decreased -0.1% mom and energy prices decreased -2.7% mom.

From the same month a year ago, PCE price index slowed from 3.0% yoy to 2.6% yoy, below expectation of 2.9% yoy. Core CPI price index fell from 3.4% yoy to 3.2% yoy, below expectation of 3.4% yoy. Goods prices fell -0.3% mom while services prices rose 4.1% yoy. Foods prices rose 1.8% yoy and energy prices decreased -6.0% yoy.

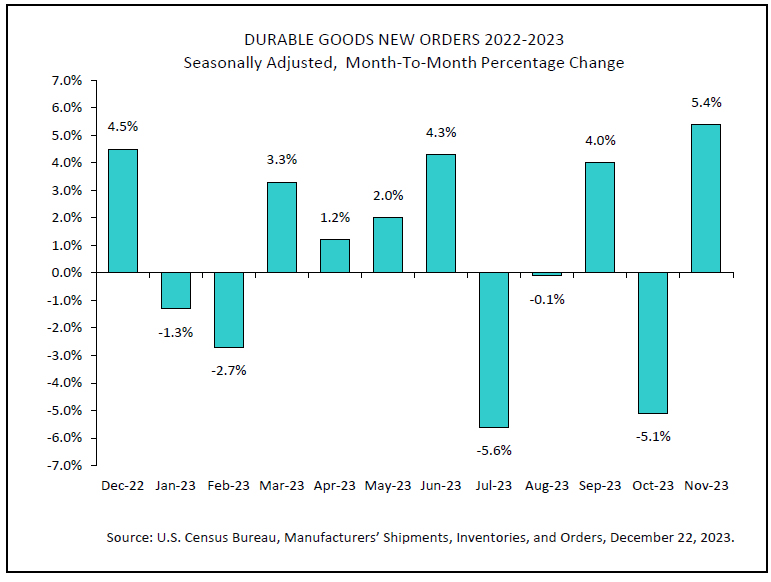

US durable goods orders rises 5.4% in Nov, ex-transport up 0.5%

US durable goods orders rose 5.4% mom to USD 295.4B in November, above expectation of 2.7% mom. Ex-transport orders rose 0.5% mom to 187.6B, above expectation of 0.2% mom. Ex-defense orders rose 6.5% mom to USD 279.6B. Transportation equipment rose 15.3% mom to USD 107.8B.

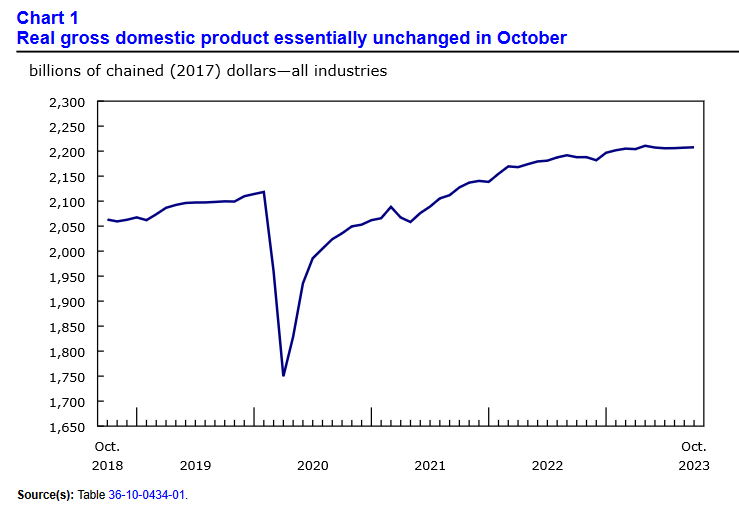

Canada GDP unchanged for the third month in Oct

Canada's GDP was essentially unchanged for a third consecutive month in October, below expectation of 0.2% mom growth. Services producing industrial edged by 0.1% mom while goods-producing industries were essentially unchanged. The 20 industrial sectors evenly split between increases and decreases.

Advance information indicates that GDP rose 0.1% mom in November.

UK retail sales volumes rises 1.3% mom in Nov, sales value up 1.0% mom

UK retail sales volumes (quantity bought) rose 1.3% mom in November, well above expectation of 0.4% mom. Ex-automotive fuel sales values rose 1.3% mom. Over the year, sales volumes rose 0.1% yoy while ex-fuel sales volume rose 0.3% yoy.

Sales value (amount spent) rose 1.0% mom, 3.8% yoy. Ex-fuel sales value rose 1.2% mom, 5.7% yoy.

Japan's CPI core slows to 2.5% yoy, but services inflation hit three-decade high

Japan's core CPI, which excludes fresh food, decreased from 2.9% yoy to 2.5% yoy in November, marking the lowest level since July 2022. Despite this deceleration, inflation remains above BoJ's target of 2% for the twentieth consecutive month, indicating persistent inflationary pressures.

All-items CPI also experienced a slowdown, dropping from 3.3% yoy to 2.8% yoy. Additionally, core-core CPI, which excludes both fresh food and energy, showed a slight decrease from 4.0% yoy to 3.8% yoy.

Notably, goods inflation saw a significant reduction, declining from 4.4% yoy to 3.3% yoy. In contrast, service inflation showed an acceleration, rising from 2.1% yoy to 2.3% yoy. This increase in service inflation is the sharpest in three decades, dating back to October 1993, if the effects of past consumption tax hikes are excluded.

Energy prices, a key factor in inflation calculations, dropped by -10.1% yoy. Japanese government's subsidies to reduce fuel costs played a role in tempering inflation rates. Without these subsidies, core CPI would have seen an increase of around 3%, according to the ministry.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8536; (P) 0.8587; (R1) 0.8614; More....

USD/CHF's decline continues today and falls through 0.8551 support without noticeable recovery. Longer term down trend is resuming. Intraday bias remains on the downside for 100% projection of 0.9111 to 0.8665 from 0.8819 at 0.8373 next. On the upside, above 0.8572 minor resistance will turn bias neutral and bring consolidations first. But risk will stay on the downside as long as 0.8665 support turned resistance holds.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Nov | 2.80% | 3.30% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Nov | 2.50% | 2.50% | 2.90% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Nov | 3.80% | 4.00% | ||

| 23:50 | JPY | BoJ Minutes | ||||

| 07:00 | GBP | Retail Sales M/M Nov | 1.30% | 0.40% | -0.30% | 0.00% |

| 07:00 | GBP | GDP Q/Q Q3 F | -0.10% | 0.00% | 0.00% | |

| 07:00 | GBP | Current Account (GBP) Q3 | -17.2B | -13.1B | -25.3B | -24.0B |

| 13:30 | CAD | GDP M/M Oct | 0.00% | 0.20% | 0.10% | 0.00% |

| 13:30 | USD | Personal Income M/M Nov | 0.40% | 0.40% | 0.20% | 0.30% |

| 13:30 | USD | Personal Spending Nov | 0.20% | 0.30% | 0.20% | 0.10% |

| 13:30 | USD | PCE Price Index M/M Nov | -0.10% | 0.00% | 0.00% | |

| 13:30 | USD | PCE Price Index Y/Y Nov | 2.60% | 2.90% | 3.00% | |

| 13:30 | USD | Core PCE Price Index M/M Nov | 0.10% | 0.20% | 0.20% | 0.10% |

| 13:30 | USD | Core PCE Price Index Y/Y Nov | 3.20% | 3.40% | 3.50% | 3.40% |

| 13:30 | USD | Durable Goods Orders Nov | 5.40% | 2.70% | -5.40% | |

| 13:30 | USD | Durable Goods Orders ex Transport Nov | 0.50% | 0.20% | 0.00% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec F | 69.4 | 69.4 | ||

| 15:00 | USD | New Home Sales Nov | 0.690M | 0.679M |

Canada GDP unchanged for the third month in Oct

Canada's GDP was essentially unchanged for a third consecutive month in October, below expectation of 0.2% mom growth. Services producing industrial edged by 0.1% mom while goods-producing industries were essentially unchanged. The 20 industrial sectors evenly split between increases and decreases.

Advance information indicates that GDP rose 0.1% mom in November.

US durable goods orders rises 5.4% in Nov, ex-transport up 0.5%

US durable goods orders rose 5.4% mom to USD 295.4B in November, above expectation of 2.7% mom. Ex-transport orders rose 0.5% mom to 187.6B, above expectation of 0.2% mom. Ex-defense orders rose 6.5% mom to USD 279.6B. Transportation equipment rose 15.3% mom to USD 107.8B.

US PCE slows to 2.6% in Nov, core PCE down to 3.2%, miss expectations

US personal income rose 0.4% mom or USD 81.6B in November, matched expectations Personal spending rose 0.2% mom or USD 46.7B, below expectation of 0.3% mom.

PCE price index fell -0.1% mom, below expectation of 0.0% mom. Core PCE price index (excluding food and energy)rose 0.1% mom, below expectation of 0.2% mom. Goods prices fell -0.7% mom while services prices rose 0.2% mom. Foods prices decreased -0.1% mom and energy prices decreased -2.7% mom.

From the same month a year ago, PCE price index slowed from 3.0% yoy to 2.6% yoy, below expectation of 2.9% yoy. Core CPI price index fell from 3.4% yoy to 3.2% yoy, below expectation of 3.4% yoy. Goods prices fell -0.3% mom while services prices rose 4.1% yoy. Foods prices rose 1.8% yoy and energy prices decreased -6.0% yoy.

Yen Steady as Japanese Inflation Dips

- Japanese core inflation falls to 2.5%, as expected

- US to release PCE Price Index on Friday

The Japanese yen is showing little movement on Friday. In the European session, USD/JPY is trading at 142.03, down 0.06%.

Japanese core inflation eases to 2.5%

Japan’s Core CPI, which excludes fresh fuel but includes fuel costs, dropped to 2.5% in November, matching the consensus estimate. This was down from the October gain of 2.9% and marked the lowest reading since July 2022. Still, it was the twentieth consecutive month that the core rate has exceeded the Bank of Japan’s target of 2%. The headline figure dropped to 2.8%, down from 3.3% in October.

The yen shrugged off the drop in inflation, taking a breather after surging 1% a day earlier. The sharp gains were driven by the third-estimate US GDP for Q3, which came in at 4.9%, lower than the second estimate of 5.2%. The drop in GDP was driven by weaker consumer spending, but the economy remains strong, as the 4.9% gain was the highest level since Q4 2021.

The BoJ released on Friday the minutes of its October 31 meeting, when the central bank unexpectedly tweaked its yield curve control (YCC) program. The yen took a bath and fell 1.78% on the day of the meeting, as the markets viewed the move as a step by the BoJ’s to phasing out its ultra-easy monetary policy. The minutes indicated that board members were divided on whether the BoJ should make clear that the tweak was not a step towards ending YCC, or should the Bank “not strongly deny” that the tweak could lead to an end of YCC. The debate highlights that board members are well aware that a shift in policy can have a significant impact on the currency markets, as was evident with the yen’s plunge following the October meeting.

The US wraps up the week with the PCE Price Index, which is considered the Federal Reserve’s preferred inflation indicator. The headline and core readings are expected to remain unchanged in November, at 0.2% and 0%, respectively. Recent inflation readings have had a strong impact on the movement of the US dollar, and that could be the case later today if the headline or core rate readings are wide of the estimates.

USD/JPY Technical

- USD/JPY has support at 141.57 and 141.03

- There is resistance at 142.60 and 143.14

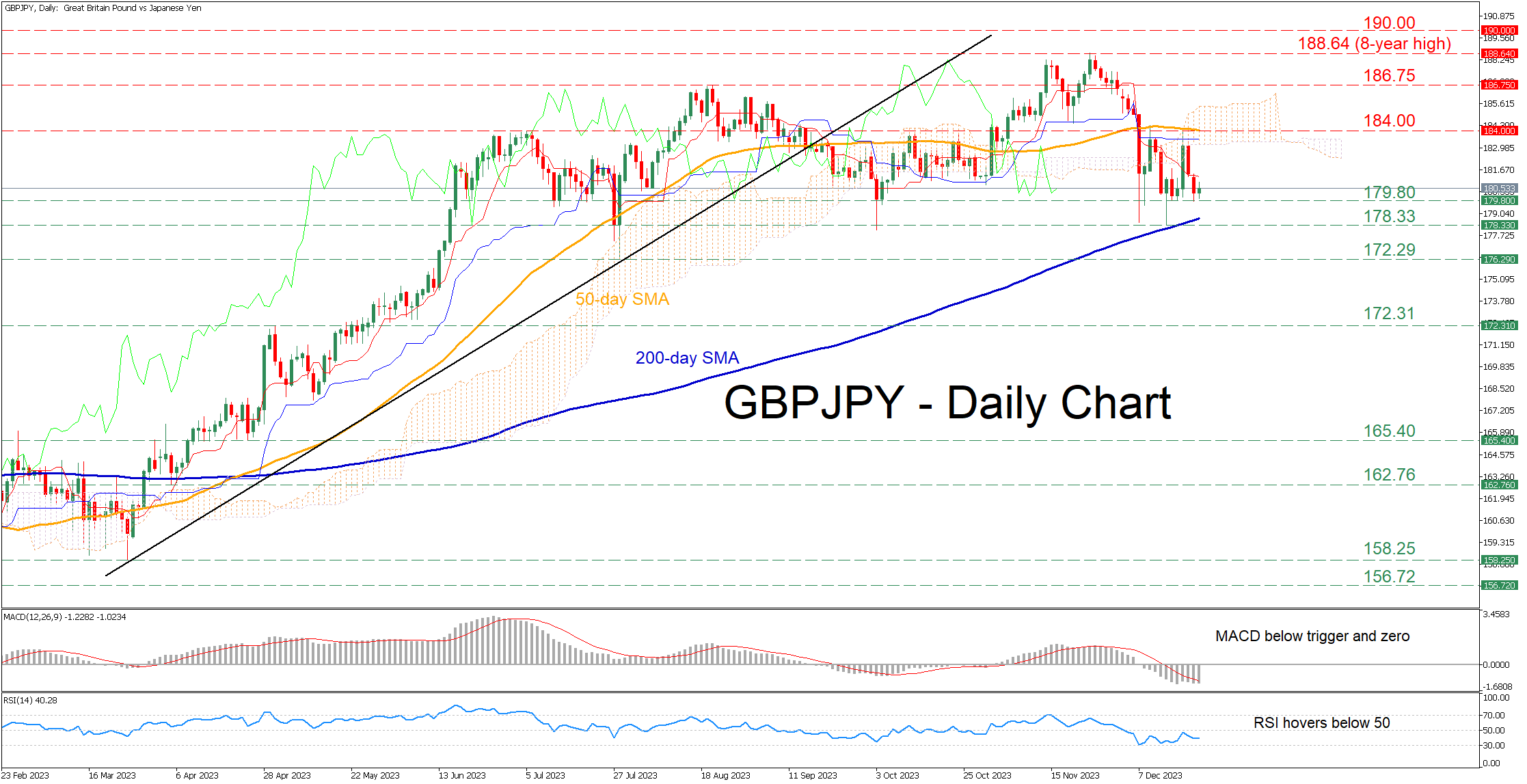

GBPJPY Rotates Lower After Rejection at 50-day SMA

- GBPJPY moves without direction in the past two weeks

- The 50- and 200-day SMAs curb upside and downside, respectively

- RSI and MACD are deep in their negative zones

GBPJPY had been in a prolonged uptrend since January, posting an eight-year high of 188.64 on November 24 before experiencing a pullback. In the short-term, the pair is undergoing a period of rangebound trading, with its 50- and 200-day simple moving averages (SMAs) defining its neutral pattern.

Considering that the short-term oscillators remain tilted to the downside, the price could inch lower to test the recent support of 179.80. If that hurdle fails, the spotlight could turn to the December bottom of 178.33, which also held strong in October and lies very close to the 200-day SMA. Even lower, the July low of 172.29 might cap the pair’s downside.

Alternatively, should the pair reverse back higher, immediate resistance could be met at the 50-day SMA of 184.00, which rejected two upside attempts in December. Piercing through that wall, the price may challenge the August high of 186.75. A violation of that region could open the door for the eight-year peak of 188.64.

In brief, GBPJPY retains a muted tone in the past few sessions as the efforts to escape its range in both directions have been disproved. Is the pair already in a consolidation phase?