Sample Category Title

UK CPI slows to 3.9% yoy in Nov, core CPI down to 5.1% yoy

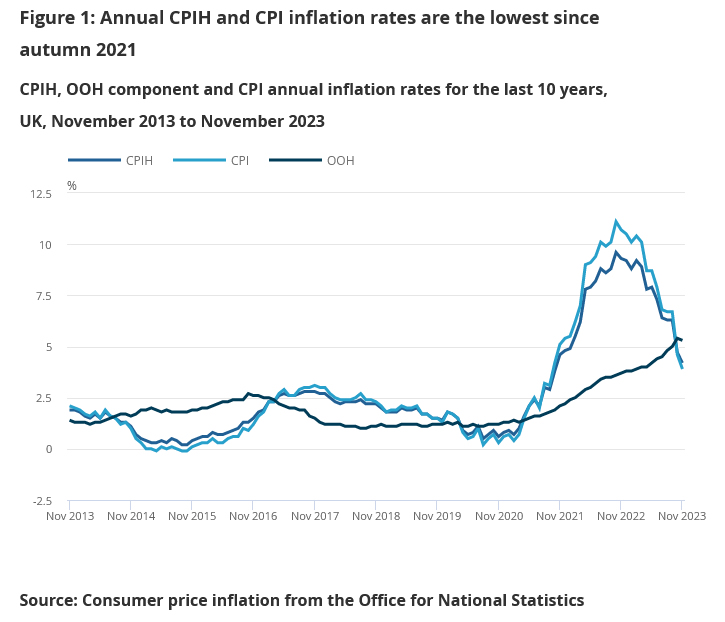

UK CPI slowed from 4.6% yoy to 3.9% yoy in November, below expectation of 4.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 5.7% yoy to 5.1% yoy, below expectation of 5.5% yoy. CPI goods fell from 2.9% yoy to 2.0% yoy. CPI services also fell from 6.6% yoy to 6.2% yoy.

ONS noted, "The easing in the annual inflation rates reflected downward contributions from eight divisions, most notably transport, recreation and culture, and food and non-alcoholic beverages. There were no divisions with large offsetting upward effects."

On a monthly basis, CPI was down -0.2% mom, below expectation of 0.2% mom rise.

Rate Cut Optimism Continues to Lift Risk Sentiment

In focus today

This morning, the Danish statistics office will release the consumer confidence indicator for December. In November, consumer confidence improved, although sentiment was still overall negative at -10.3. The labour market is still going strong, and inflation was low in November. Given the high expected wage growth, consumers' purchasing power is increasing. This is positive for consumer confidence, and we think it will improve again in December.

Today, we closely follow the EU meeting regarding a new set of fiscal policy rules in the EU. The EU economy and finance ministers will hold an informal videoconference to discuss the fiscal rules. This is likely the last chance to get a deal on a new set of rules before the self-imposed year-end deadline. Read more about the negotiations on fiscal rules in Euro Area Research - New fiscal rules in the EU - aligning theory and practice?, 29 November.

In the US, existing home sales for November and Conference Board consumer survey for December will be released.

Looking at the central bank calendar, ECB's Lane and Riksbank's Thedeen are scheduled to speak.

The 60 second overview

Fed speak: The Fed's Goolsbee and Bostic continued to push back on the notion of imminent rate cut talks yesterday even if both underscored the recent positive developments on inflation. Goolsbee noted that 'market has gotten ahead of themselves' while Bostic reminded that there 'is not going to be urgency' in easing the current restrictive policy stance. Barkin was more optimistic, as he described the retreat in inflation as 'remarkable', which contrasts his more cautious comments heard in late November. We still think that the Fed is going to cut rates for the first time in March, but given the recent easing in financial conditions and that there are few signs of a clear cooling in economic momentum, we think the Fed will opt for a relatively gradual rate cutting pace of 4x25bp in 2024 (market prices in a total of 145bp of cuts).

PBoC: The People's Bank of China left the 1 and 5 year Loan Prime Rates (LPR) unchanged overnight, which was widely anticipated after it made no changes to the Medium-term Lending Facility (MLF) rate last Friday. Loan Prime Rates are the key reference rates for business loans and mortgages. As both economic data and the outlook for new stimulus remain mixed, we stick to our 'muddling through' scenario for China, with no boom but also no signs of an imminent bust. We expect Chinese GDP to grow by 4.5% in both 2024 and 2025.

Equities: Global equities were higher (again) yesterday. Fed officials are trying to push back against rate cut expectations for next year, but investors are not listening. They have decided that rate cuts are coming and that means less monetary headwinds and cheaper financing. Russell 2000 was up by almost 2% yesterday, which was not surprising with the soft-landing and lower yields dominating. Energy doing well as oil prices are higher, not due to lower yields but rather as the Red Sea conflict is escalating. Materials also outperforming as industrial metals have grinded higher lately. Major indices in US yesterday, Dow +0.7%, S&P 500 +0.6%, Nasdaq +0.7% and Russell 2000 +1.9%. The positive sentiment is continuing in Asia this morning with both Kospi and Nikkei 225 up more than 1.5% despite lacklustre trade data out of Japan. US and European futures both in green this morning as well.

FI: The markets keep ignoring comments from the Federal Reserve officials that rate cuts will be gradual and limited and inflation needs to decline further such that the "battle against inflation" can be declared to be "won". Hence, the 10Y US Treasury yield is testing the 4%-level and the US curve flattened from the long end, which is not what we see during the start of a rate cutting cycle.

FX: In Scandies, NOK/SEK closed higher for the fifth consecutive session, hand in hand with relative yields on the back of Norges Bank's surprise hike. On Tuesday, the cross traded above 0.99 for the first time since early November. In majors, GBP and AUD were among the outperformers both in response to hawkish central bank comments. Meanwhile, the USD continues to trade on the back foot after Fed/Powell refrained from pushing back on rates pricing last week and as such fuelled further risk on. EUR/USD took another step higher and is seemingly having its eyes on the 1.10 handle.

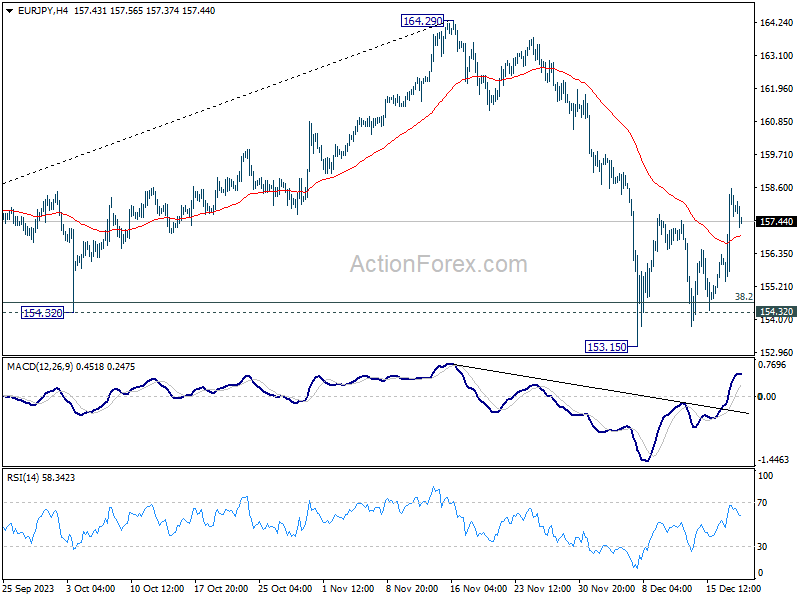

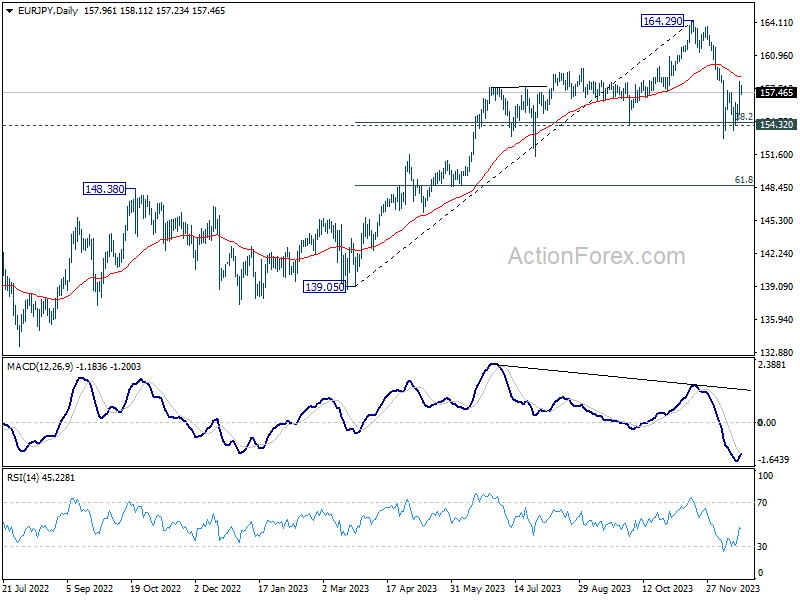

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.04; (P) 157.30; (R1) 159.22; More..

Intraday bias in EUR/JPY stays on the upside for the moment. Rebound from 153.15 should target 55 D EMA (now at 158.97). On the downside, break of 153.15 will resume whole fall from 164.39 to 61.8% retracement of 139.05 to 164.29 at 148.69.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

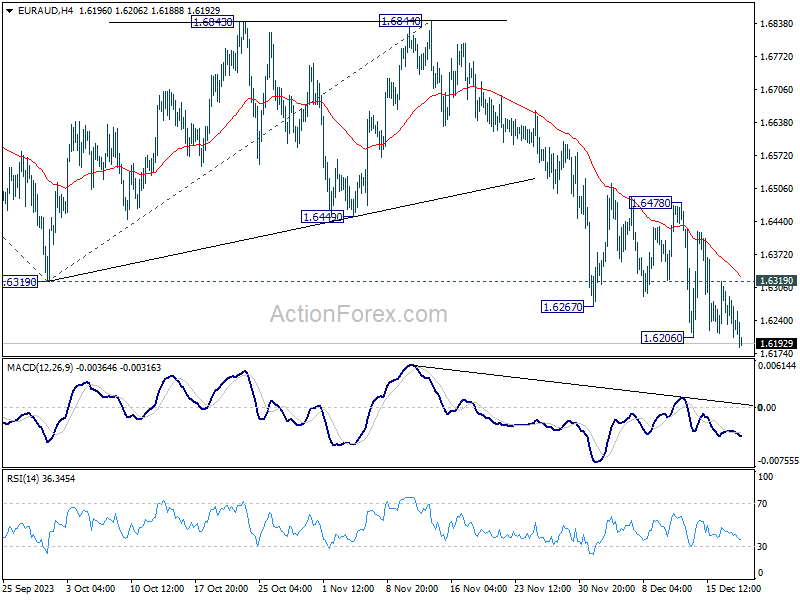

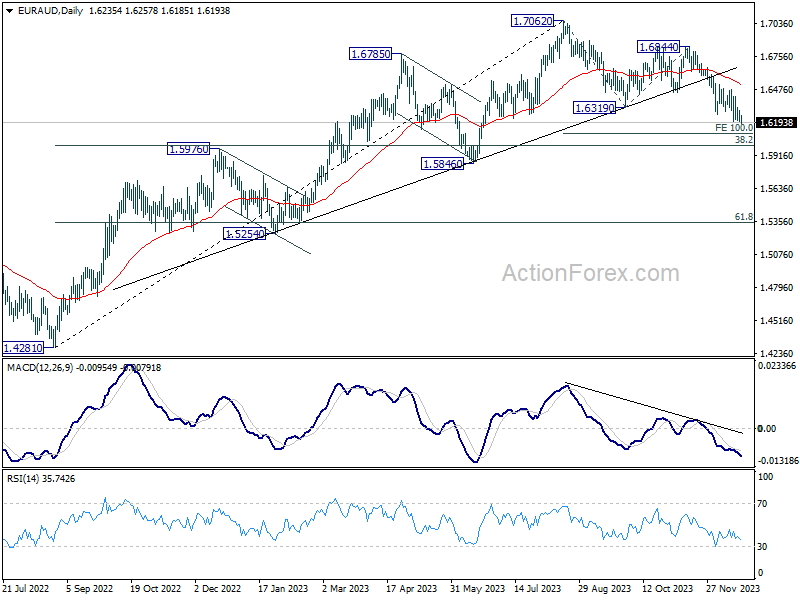

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6197; (P) 1.6248; (R1) 1.6289; More...

EUR/AUD's decline resumed by breaking 1.6206 and intraday bias is back on the downside. Current fall from 1.7062 should now target 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106. On the upside, above 1.6319 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.6478 resistance holds.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9432; (P) 0.9461; (R1) 0.9483; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9402 could extend further. But still, deeper decline is expected with 0.9543 resistance intact. On the downside, firm break of 0.9407 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325. However, sustained break of 0.9543 will bring further rally back to 0.9683 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

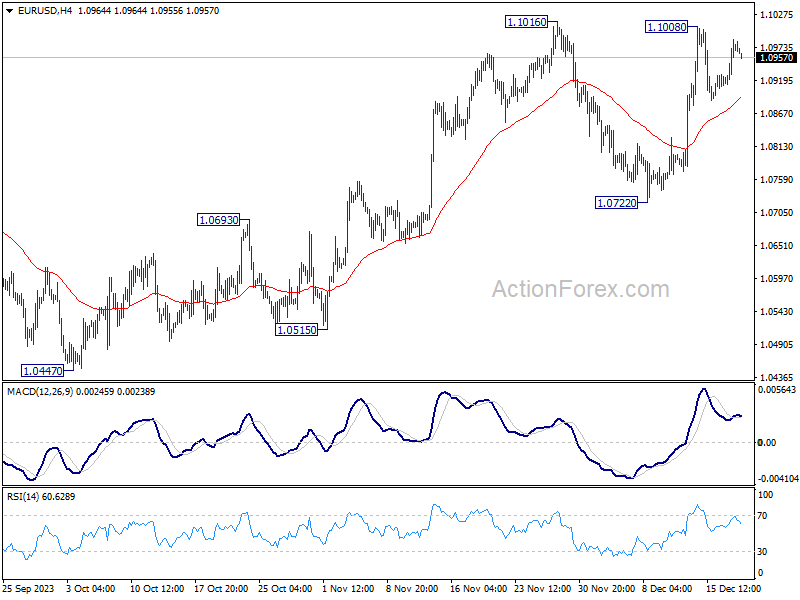

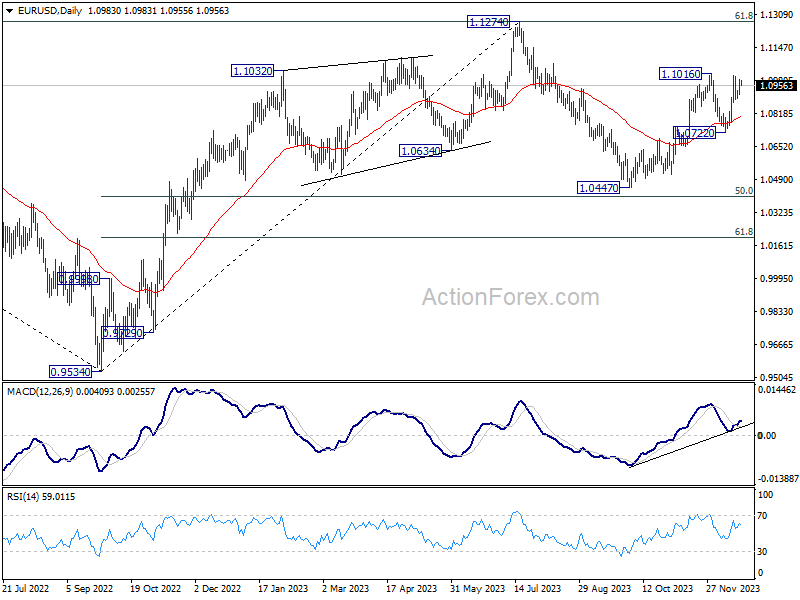

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0935; (P) 1.0961; (R1) 1.1007; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen below 1.1008. Further rally is expected as long as 1.0722 support holds. On the upside, break of 1.1016 will resume the whole rise from 1.0447 to retest 1.1274 high.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

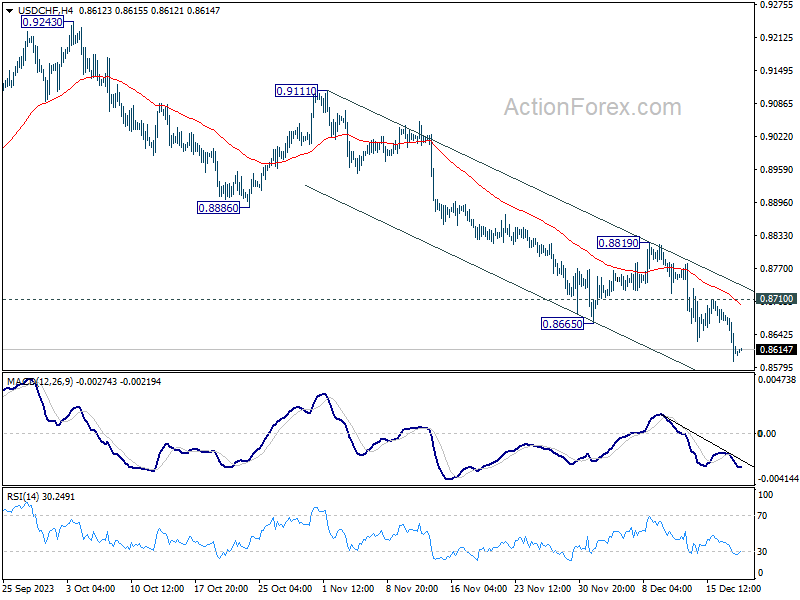

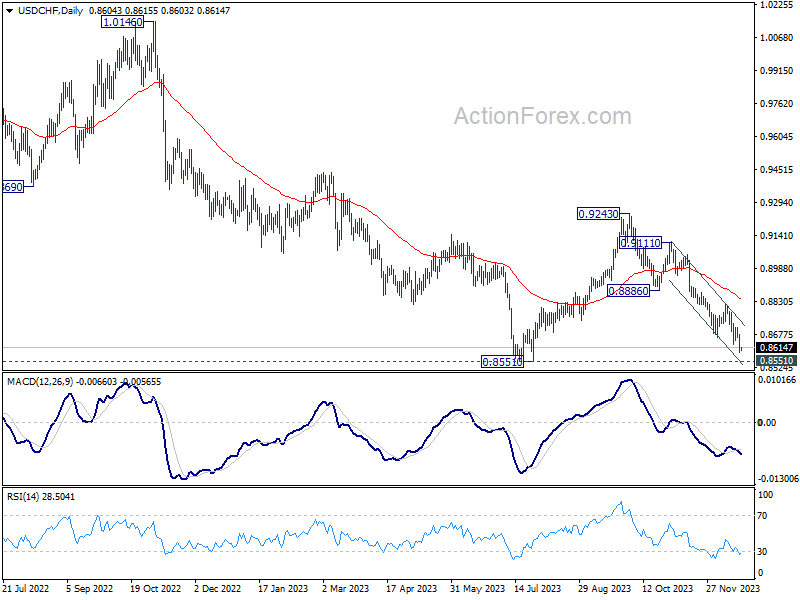

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8573; (P) 0.8630; (R1) 0.8667; More....

Intraday bias in USD/CHF remains on the downside for the moment. Current fall from 0.9243 should target 0.8551 key support next. On the upside, above 0.8710 minor resistance will turn intraday bias neutral again first. But outlook will remain bearish as long as 0.8819 resistance holds.

In the bigger picture, price actions from 0.8551 are currently seen as a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Strong support should be seen 0.8551 to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243.

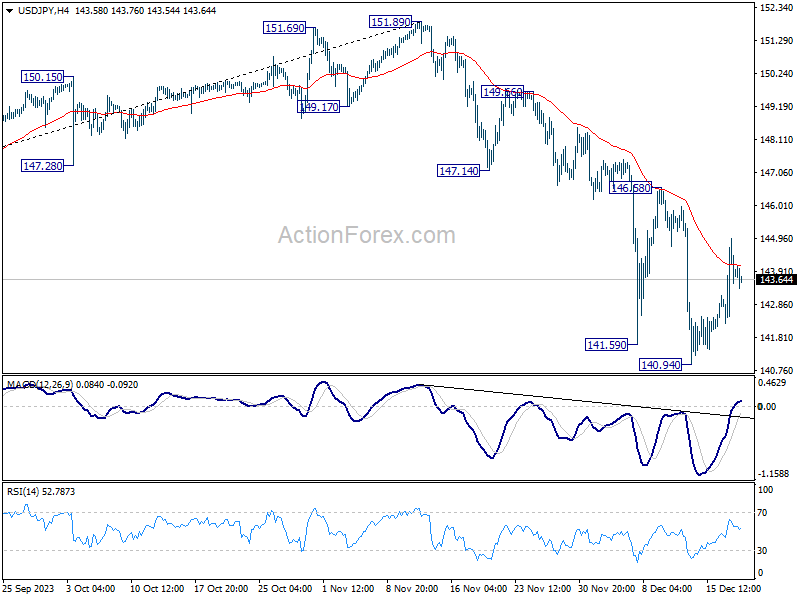

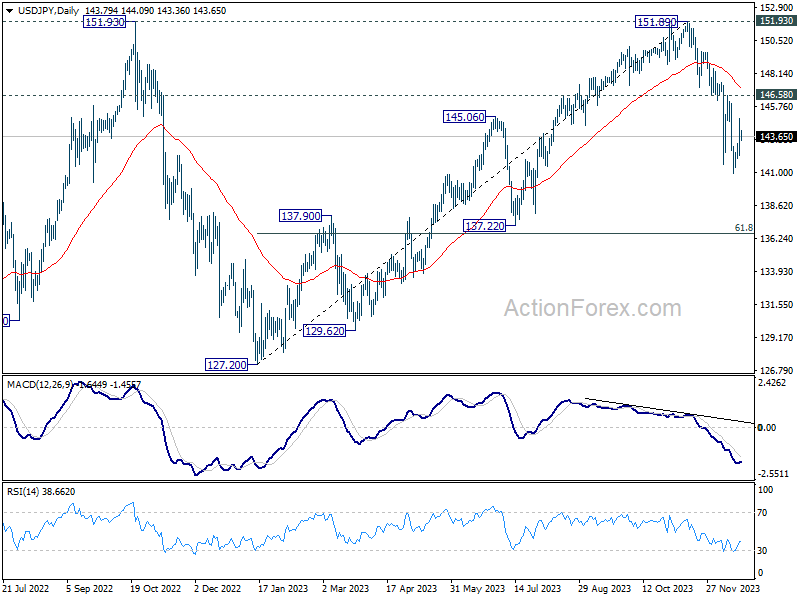

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.41; (P) 143.68; (R1) 145.12; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. Upside of current recovery should be limited below 156.48 resistance to bring another decline. Firm break of 140.94 will resume the whole fall from 151.89. Next target will be next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

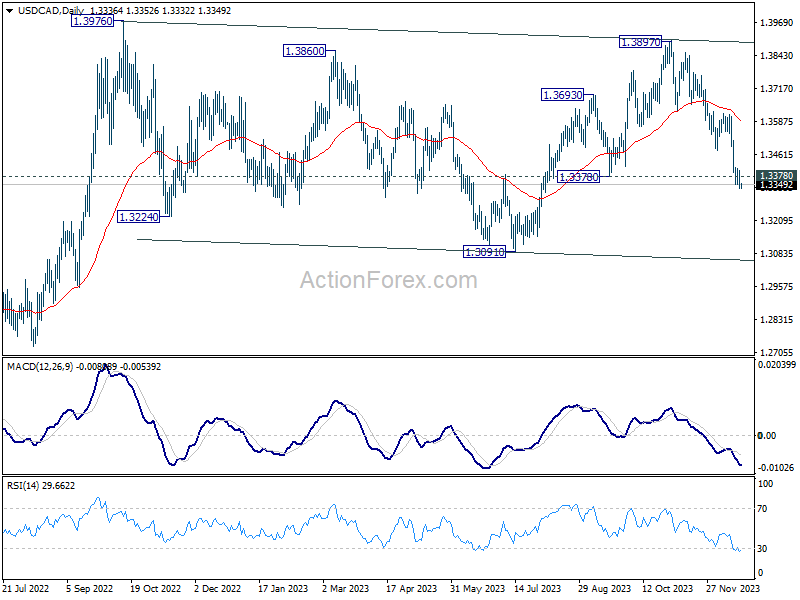

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3309; (P) 1.3356; (R1) 1.3381; More...

Intraday bias in USD/CAD stays on the downside for the moment. Sustained trading below 1.3378 will extend the fall from 1.3897 to retest 1.3091 support next. On the upside above 1.3408 minor resistance will turn intraday bias neutral again. But risk will stay on the downside as long as 1.3479 support turned resistance holds.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

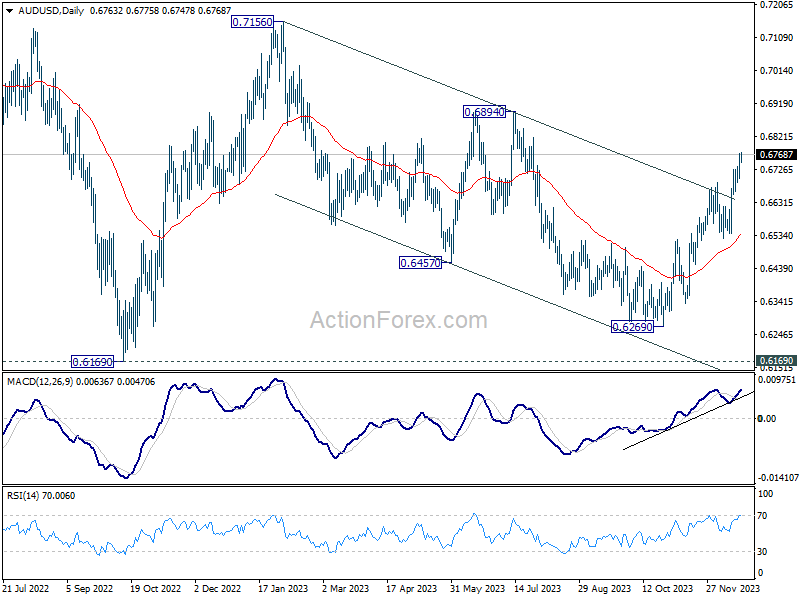

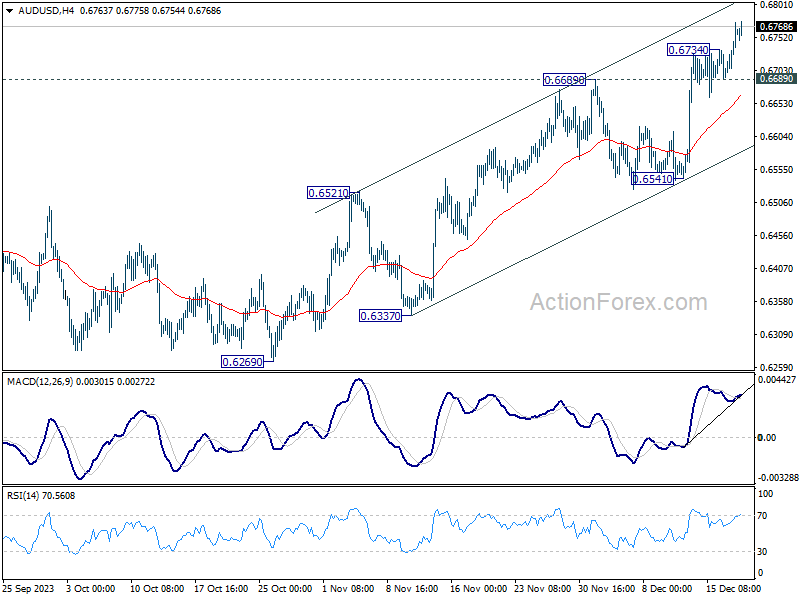

AUD/USD Daily Report

Daily Pivots: (S1) 0.6718; (P) 0.6746; (R1) 0.6792; More...

AUD/USD's rally resumed after brief retreat and intraday bias is back on the upside. As noted before, fall from 0.7156 could have completed with three waves down to 0.6269. Further rise should be seen to 0.6894 resistance first. Sustained break there will target 0.7156 next. On the downside, below 0.6689 minor support will turn intraday bias neutral for consolidations again. But outlook will remain mildly bullish as long as 0.6541 support holds, in case of retreat.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.