Sample Category Title

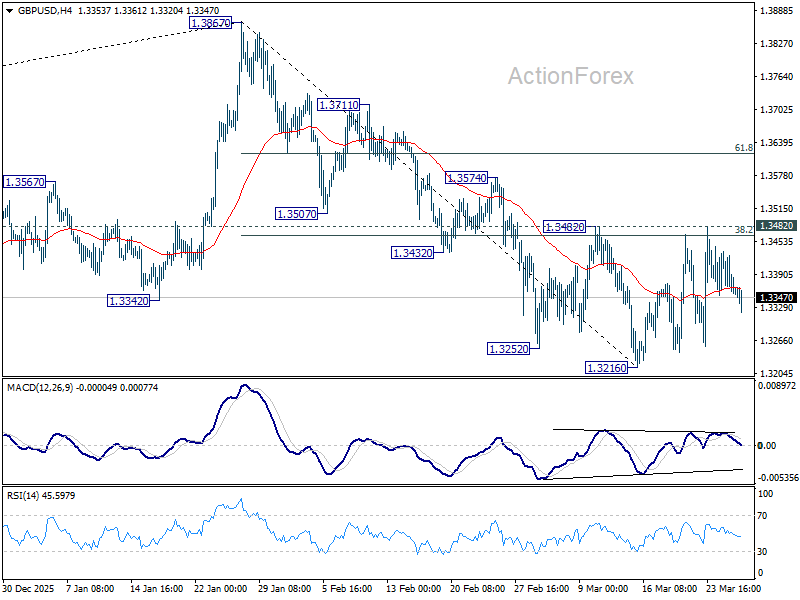

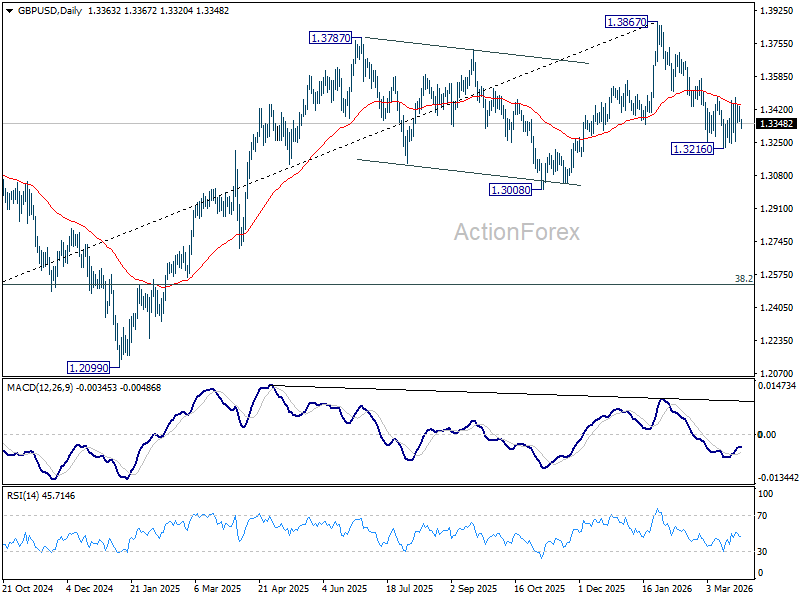

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3336; (P) 1.3386; (R1) 1.3415; More...

GBP/USD dips mildly today but stays in established range. Intraday bias stays neutral at this point. With 1.3482 resistance intact, further decline is in favor. On the downside, below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

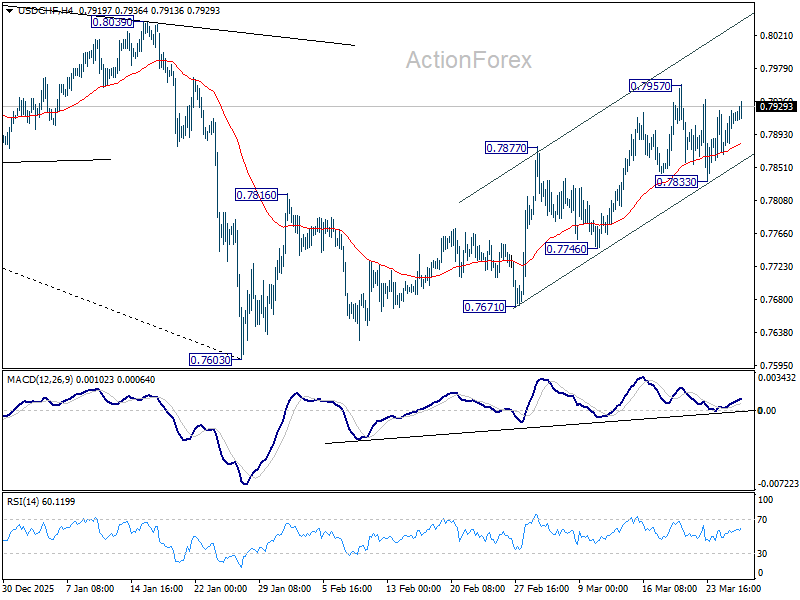

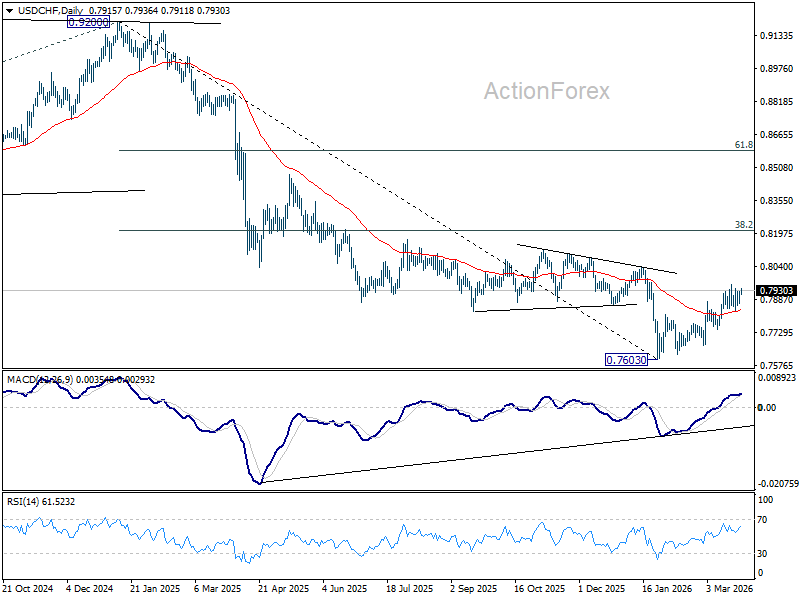

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7882; (P) 0.7904; (R1) 0.7939; More….

USD/CHF recovered today but stays below 0.7957. Intraday bias stays neutral at this point. As noted before, rise from 0.7603 should be correcting whole decline from 0.9200. Above 0.7957 will target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. This will remain the favored case as long as 0.7746 support holds.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

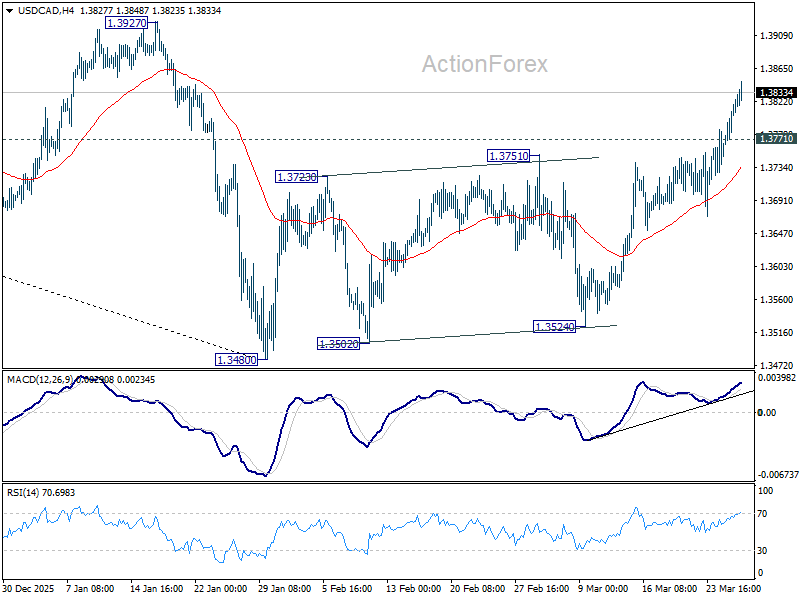

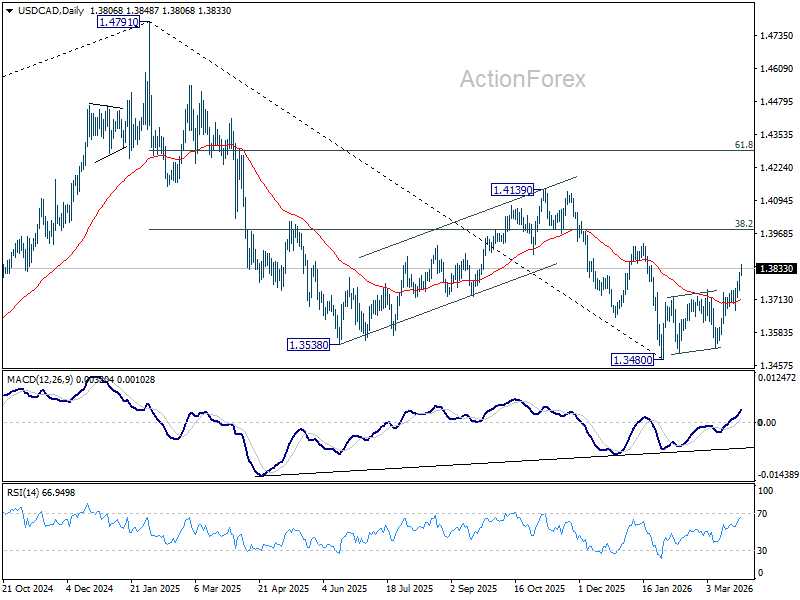

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3766; (P) 1.3794; (R1) 1.3838; More...

Intraday bias in USD/CAD remains on the upside for the moment. Rebound from 1.3480 is seen as correcting the whole down trend from 1.4791 and should target 1.3927 resistance, or probably further to 38.2% retracement of 1.4791 to 1.3480 at 3981. On the downside, below 1.3771 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

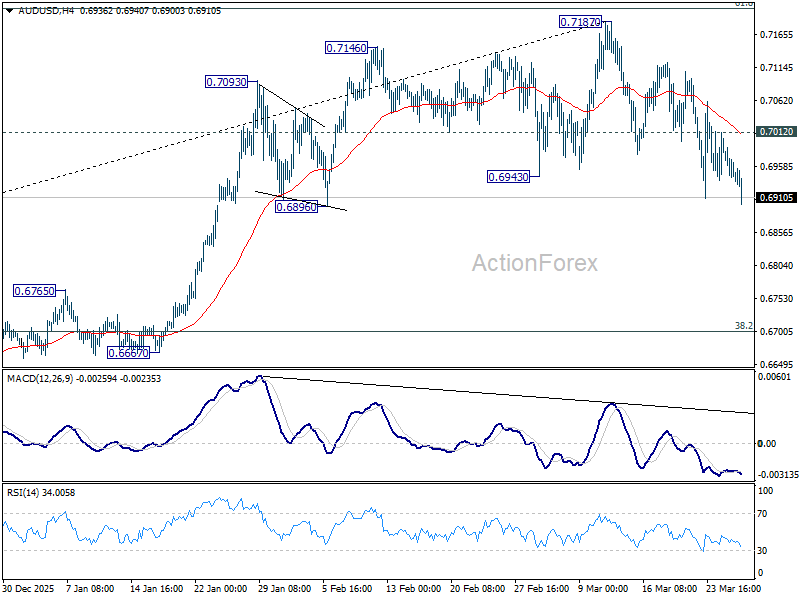

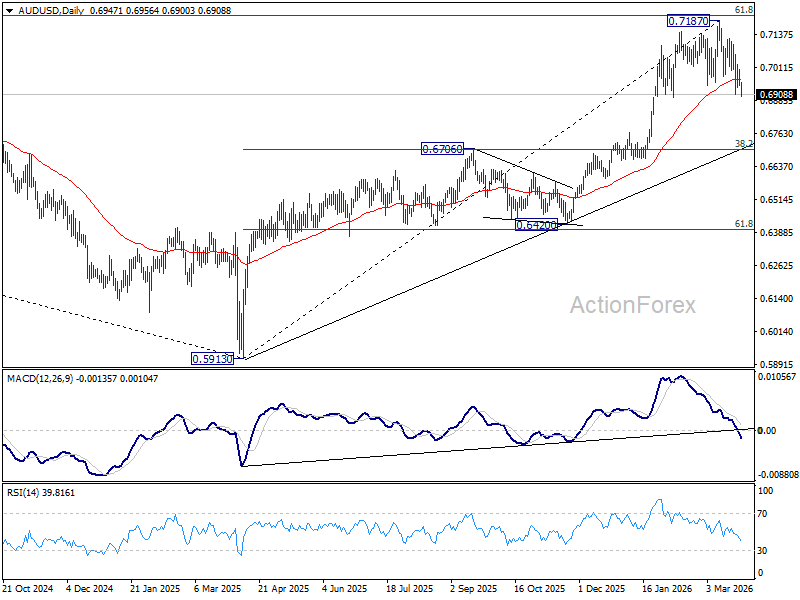

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6925; (P) 0.6965; (R1) 0.6987; More...

AUD/USD's fall from 0.7181 extends lower today and the development should now confirm rejection by 0.7206 key fibonacci resistance. The decline is see as correcting whole up trend from 0.5913. Intraday bias is now on the downside for 38.2% retracement of 0.5913 to 0.7187 at 0.6700. On the upside, though, above 0.7012 minor resistance will turn intraday bias neutral again first.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

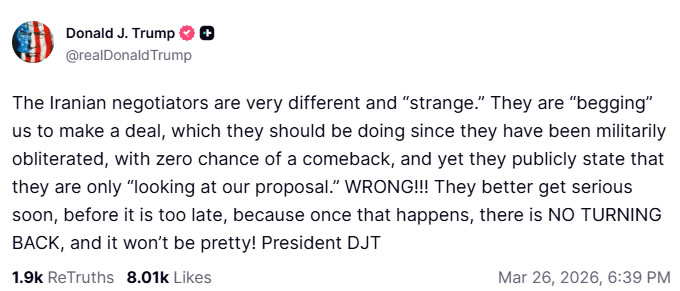

The $120 Canary: Markets Price Weekend Escalation, Dollar Rallies on Trump Ultimatum

Risk aversion has returned to global markets following a high-stakes ultimatum from US President Donald Trump, signaling a breakdown in the 15-point Iran negotiation. As Brent crude rebounds above $105, the focus has shifted to the Saturday, March 28 expiration of the five-day strike pause. Trump’s shift from "productive talks" to warnings of "military obliteration" suggests the diplomatic off-ramp has hit a brick wall, sparking a broad rally in Dollar. The $120 Brent level as the critical "canary in the coal mine"; a move toward this target in the next 48 hours would signal that markets have fully discounted a weekend military escalation.

The latest social media activity from the White House reveals a significant amount of strategic anxiety. While a confident leader typically allows diplomatic results to speak for themselves, the public labeling of Iranian negotiators as "strange" and "begging" suggests an attempt to narrate a reality that is not yet visible on the ground.

If Iran were truly in a position of desperation, the U.S. would likely not need to issue an all-caps ultimatum on social media. Instead, the rhetoric implies that the 15-point proposal—which includes maximalist demands such as the dismantling of Iran’s nuclear program—has hit a functional brick wall.

The most alarming development for the markets is the phrase "NO TURNING BACK." This shift in tone coincides perfectly with the looming expiration of the five-day strike pause set for this Saturday. Earlier in the week, the administration was promoting "productive talks," but the transition to "it won't be pretty" indicates that the window for a peaceful off-ramp is rapidly closing. This serves as a direct warning to Tehran that the U.S. is prepared to transition from limited, surgical strikes to targeting critical energy infrastructure or initiating ground operations.

A truly "calming" diplomatic post would have focused on the progress of the 15 points or the mutual benefits of a regional peace. Instead, this latest communication focused on total military obliteration, reminding Iran they have "zero chance of a comeback."

Markets are now actively front-running a weekend escalation. The $120 level in Brent crude is the single most important metric to watch; if oil marches toward that target tomorrow, it is a clear signal that the market has completely discounted the "negotiation" narrative and is bracing for a significant military event on Saturday night or Sunday.

In the currency markets, Dollar is the strongest performer on the day so far, supported by both safe-haven demand and the repricing of interest rate expectations. Yen and Swiss Franc are both also benefiting mildly from renewed risk aversion. In contrast, commodity currencies are underperforming, with Aussie and Kiwi leading losses, while Sterling is also pressured. Loonie has managed to hold relatively better, supported by the rebound in oil prices, while Euro also positions in the middle.

In Europe, at the time of writing, FTSE is down -1.41%. DAX is down -1.69%. CAC is down -1.11%. UK 10-year yield is up 0.125 at 4.901. Germany 10-year yield is up 0.085 at 3.047. Earlier in Asia, Nikkei fell -0.27%. Hong Kong HSI fell -1.89%. China Shanghai SSE fell -1.09%. Singapore Strait Times fell -0.34%. Japan 10-year JGB yield rose 0.02 to 2.274.

BoE’s Breeden: 'Lackluster' Growth is the UK’s Disinflationary Shield

Bank of England Deputy Governor Sarah Breeden is betting on the UK’s weak economy to absorb the latest global energy shock. She argues that "rising slack" in the labor market and weak pricing power make a wage-price spiral "less likely," allowing the BoE to stay sidelined. Read more.

ECB's 'Option April': Nagel Warns Against Shying Away from Pre-emptive Hikes

Bundesbank President Joachim Nagel signaled that an April rate hike is now a live option following the conflict-induced energy spike in Iran. Warning that the Governing Council should not "shy away" from pre-emptive action, Nagel shifted the market’s focus toward the risk of a "secondary" inflation surge in wages and services. Read more.

RBA Warns of 'Restrictive' Shift: Why Rising Neutral Rates and Petrol Shocks Could Trigger More Hikes

Assistant Governor Christopher Kent just delivered a sobering update on the RBA’s path forward. While global uncertainty usually cools rates, the "Supply Shock" from the Middle East is having the opposite effect—pushing Neutral Rates higher and keeping the pressure on Australian households. Read more.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6925; (P) 0.6965; (R1) 0.6987; More...

AUD/USD's fall from 0.7181 extends lower today and the development should now confirm rejection by 0.7206 key fibonacci resistance. The decline is see as correcting whole up trend from 0.5913. Intraday bias is now on the downside for 38.2% retracement of 0.5913 to 0.7187 at 0.6700. On the upside, though, above 0.7012 minor resistance will turn intraday bias neutral again first.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

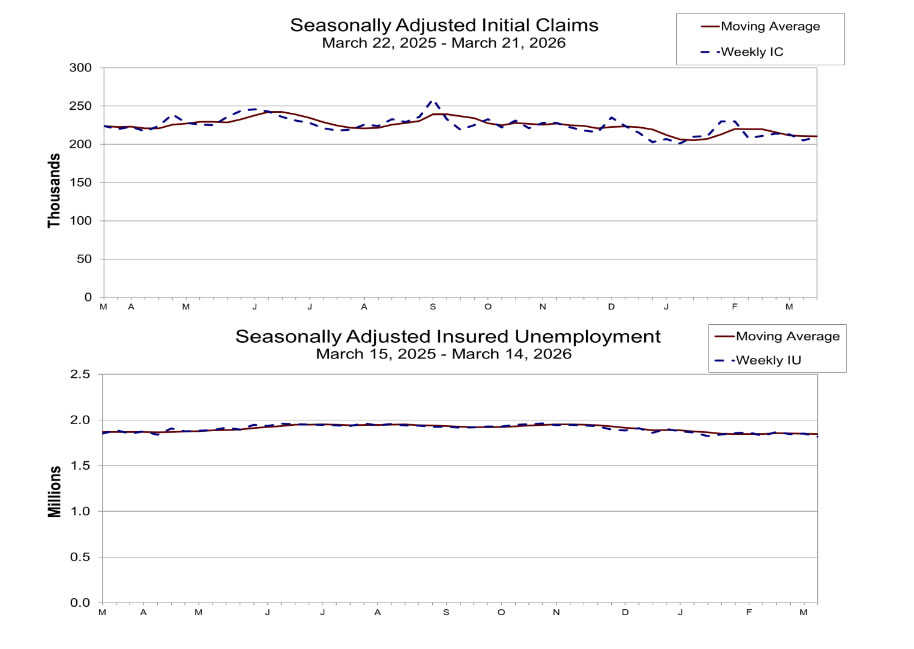

US initial jobless claims rise to 210k, vs exp 211k

US initial jobless claims rose 5k to 210k in the week ending March 21, slightly below expectation of 211k. Four-week moving average of initial claims fell -250 to 210.5k.

Continuing claims fell -32k to 1.819m in the week ending March 14, lowest since May 25, 2024. Four-week moving average of continuing claims fell -2k to 1.847m, lowest since October 5, 2024.

BoE’s Breeden: ‘Lackluster’ Growth is the UK’s Disinflationary Shield

Bank of England Deputy Governor Sarah Breeden argued today that "second-round effects" from the Iran energy shock are less likely to take root in the UK. Citing rising slack in the labor market and a lackluster outlook for economic activity, Breeden suggested that diminished pricing power for firms and workers acts as a natural buffer against a wage-price spiral.

Speaking at an event today, Breeden offered a measured assessment of the UK’s inflationary trajectory in the wake of Middle East tensions. Rather than signaling an immediate policy tightening, she pointed to the underlying fragility of the UK economy as a protective factor. Breeden noted that the outlook for activity was "lackluster" even before the recent energy spike, suggesting that the economy is already in a state of weakened demand that prevents higher costs from being easily passed on to consumers.

"All of that means that firms and workers are likely to have less pricing power, less wage bargaining power," Breeden explained. This assessment hinges on the idea that the UK’s cooling labor market will prevent the "wage-price feedback loop" that typically follows a commodity shock.

Additionally, Breeden explicitly stated that it is "not wise to act" before the Monetary Policy Committee has sufficient information, noting that the Bank expects to learn a "chunk more" by the time of the April decision.

The Dusk of the Petrodollar Age

- Iran insists on control of the Strait of Hormuz and is demanding compensation.

- The US withdrawal from the Middle East could mark the beginning of the end of the petrodollar era.

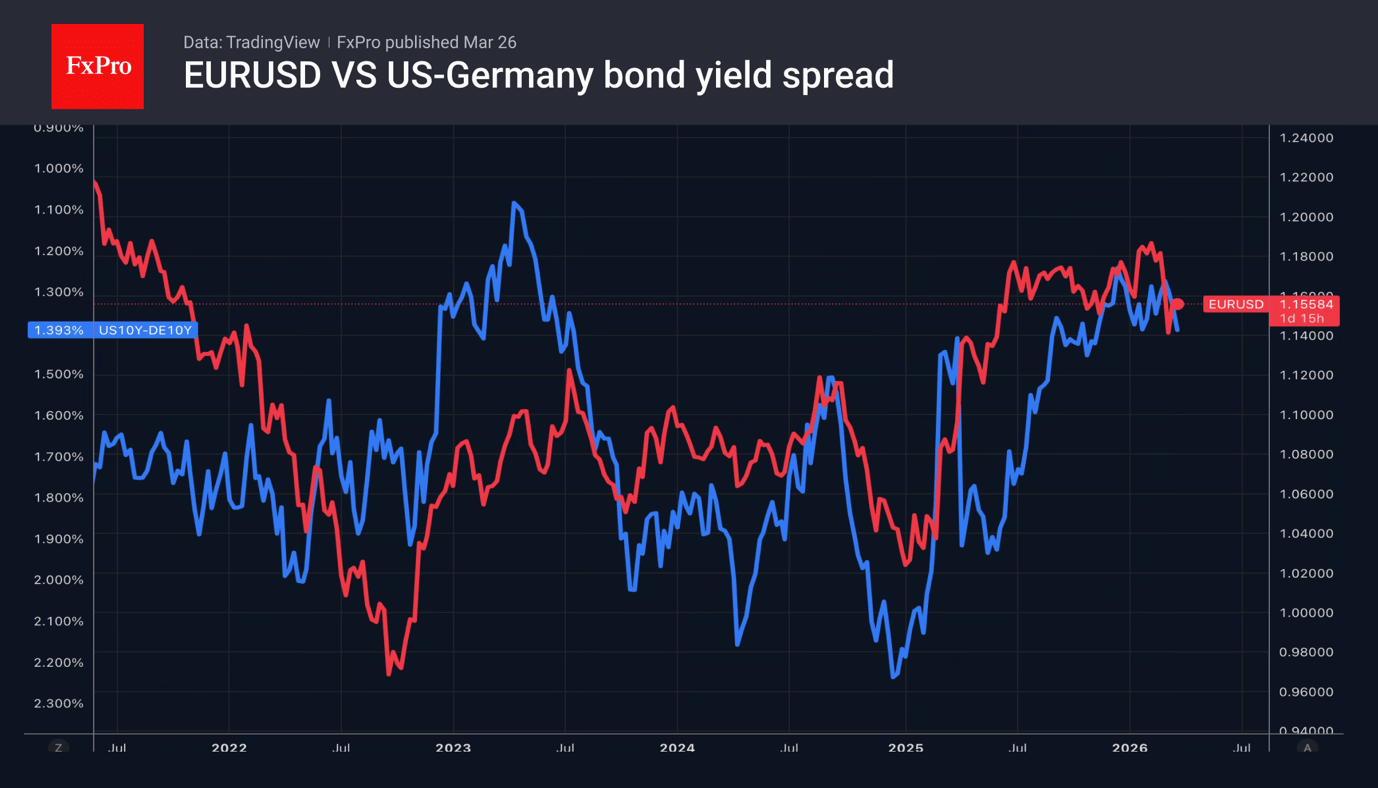

Rising oil prices, triggered by Iran’s rejection of Donald Trump’s 15-point plan, have sent the EURUSD lower. Tehran does not consider itself to have lost the war and is putting forward its own demands. This does not look like a capitulation by Iran, which means the armed conflict is likely to continue, a development that is positive for the US dollar in the near term.

Morgan Stanley describes the USD rally as a bull trap, pointing out that the oil crisis is a temporary phenomenon, whilst divergence in monetary policy always works. The futures market indicates a 64% probability of rates remaining unchanged until the end of the year and a 32% chance of a hike. This is a dramatic shift from the start of the year, when speculators were betting on 2–3 rate cuts by year-end. Nevertheless, the ECB is expected to deliver up to three rate hikes by the end of the year, which should favour the euro against the dollar.

However, it must be understood that without a resolution to the fuel crisis caused by the armed conflict in the Middle East, there is no point in discussing monetary policy divergence. It is by no means certain that the ECB will raise rates, no matter how much Christine Lagarde speaks of determination in the fight against inflation and bringing it back to the 2% target.

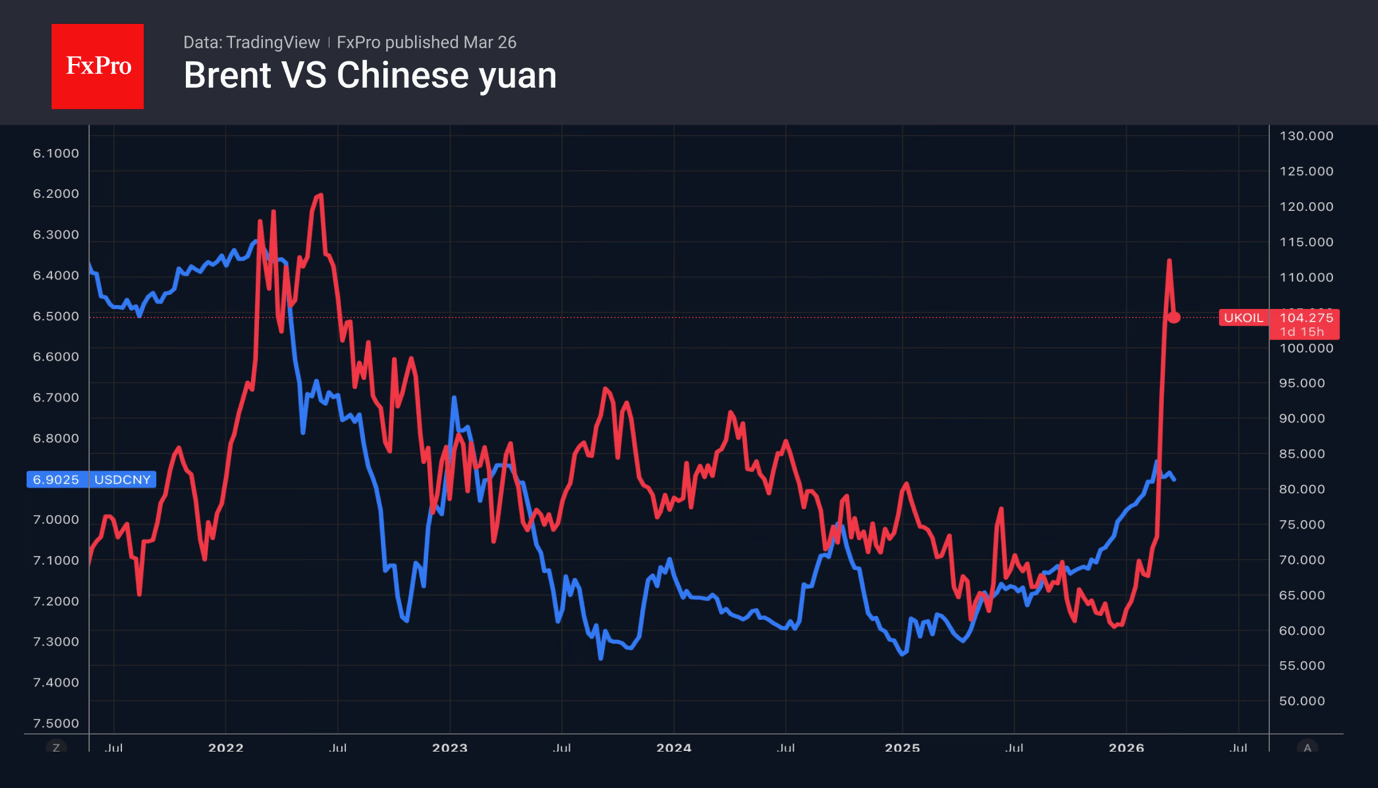

Far from everyone is convinced that the continuation of the conflict will, in the medium to long term, lead to a depreciation of the euro against the dollar. Deutsche Bank believes that a protracted conflict in the Middle East carries the risk of a shift from the petrodollar to the petro-yuan. The concept first emerged in 1974, when Saudi Arabia agreed to sell oil for US dollars and channel its foreign trade surplus into dollar-denominated assets in exchange for US security guarantees. Riyadh now sells four times as many barrels to China as it does to the United States.

Tehran’s continued control of the Strait of Hormuz and the fact that most of Iran’s oil is supplied to China suggest that the transition to the petro-yuan is a matter for the foreseeable future. At the same time, the dollar’s loss of its role as the settlement currency for black gold could undermine its other privileges, particularly its status as the primary reserve asset.

GBP/USD Eyes Middle East: Details Matter to the Market

GBP/USD traded at 1.3364 on Thursday. The pair declined over the previous two sessions and is now showing signs of a tentative recovery amid expectations of a possible de-escalation in the Middle East conflict.

The US has reportedly presented Iran with a 15-point settlement plan following discussions about a potential month-long truce. However, Iran has rejected participation in negotiations, stating that US diplomacy cannot be trusted.

In the UK, February inflation figures matched expectations. Headline CPI held steady at 3%, while core inflation edged up slightly to 3.2% against a forecast of 3.1%. However, the data had limited impact on the market, as it reflected conditions prior to the latest escalation in the Middle East.

Against the backdrop of lower oil prices, investors are revising their expectations for Bank of England policy. The market is now pricing in fewer than two rate hikes before year-end, with total expected tightening estimated at approximately 68 basis points, down from nearly 75 basis points previously.

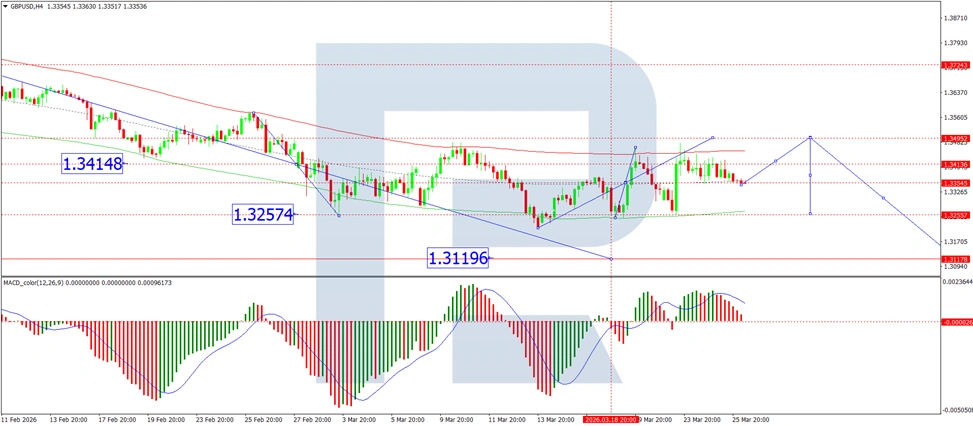

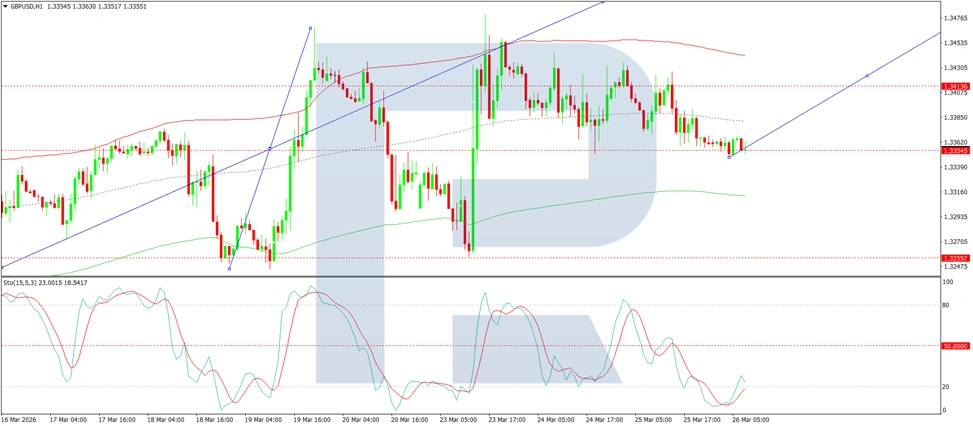

Technical analysis

On the H4 GBP/USD chart, the market is forming a broad consolidation range around 1.3354, currently extending up to 1.3434. A decline to 1.3255 is expected in the near term, followed by the formation of a new consolidation range. An upside breakout would pave the way for a continuation wave to 1.3494, while a downside breakout would suggest further movement to 1.3119. Technically, this scenario is confirmed by the MACD indicator, whose signal line is above zero and pointing firmly downwards.

On the H1 chart, the market has formed a compact consolidation range around 1.3355. A downside breakout has initiated a wave structure extending to 1.3255. Should this level be breached, further downside towards 1.3125 is likely. Conversely, an upside breakout from the range could trigger a growth wave to 1.3494. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 20 and pointing firmly downwards.

Conclusion

GBP/USD is navigating competing forces amid short-term volatility driven by geopolitical headlines. While tentative signs of a potential US–Iran truce have offered some relief to markets, Iran’s rejection of negotiations underscores the fragility of hopes for de-escalation. Meanwhile, UK inflation data – though in line with forecasts – has been largely overlooked given its pre-escalation timeframe. Lower oil prices have prompted markets to scale back expectations for Bank of England tightening, offering modest support for sterling. With technical indicators pointing to continued consolidation and the Middle East situation remaining fluid, the pair’s near-term direction will likely hinge on further geopolitical developments.

Chart Alert: Gold (XAU/USD) Bearish Trend Resumes Below $4,620 as Stagflation and Oil Strength Weigh

Key takeaways

- Bearish trend intact despite rebound: Gold (XAU/USD) plunged 15% to a 4-month low before a 12% rebound, but the bounce is likely a dead cat bounce, with another bearish leg expected.

- Stagflation & oil strength driving downside risk: Rising WTI crude oil supports a stagflation backdrop, increasing interest rate pressures, and the opportunity cost of holding gold, reinforcing a negative correlation and downside bias.

- Key technical levels signal further weakness: Breach below $4,440 on Gold (XAU/USD) may trigger a move toward $4,099 and lower, while only a break above $4,620 would invalidate the bearish outlook.

Since 19 March, Gold (XAU/USD) has staged the expected bearish impulsive down move sequence and plummeted by 15% to print a 4-month low of $4,099 on Monday, 23 March 2026, supported by the “stagflation fear” macro factor.

Thereafter, the previous yellow metal staged a rebound of 12% to hit an intraday high of $4,603 on the backdrop of “TACO” optimism that the US White House Administration is looking to end the month-long US-Iran war, in turn, allowing passage to reopen in the Strait of Hormuz, the global oil flow choke point.

Right now, intermarket and technical analyses are pointing to another leg of bearish impulsive down move for Gold (XAU/USD), likely the end of the 12% corrective rebound, aka dead cat bounce from Monday’s low.

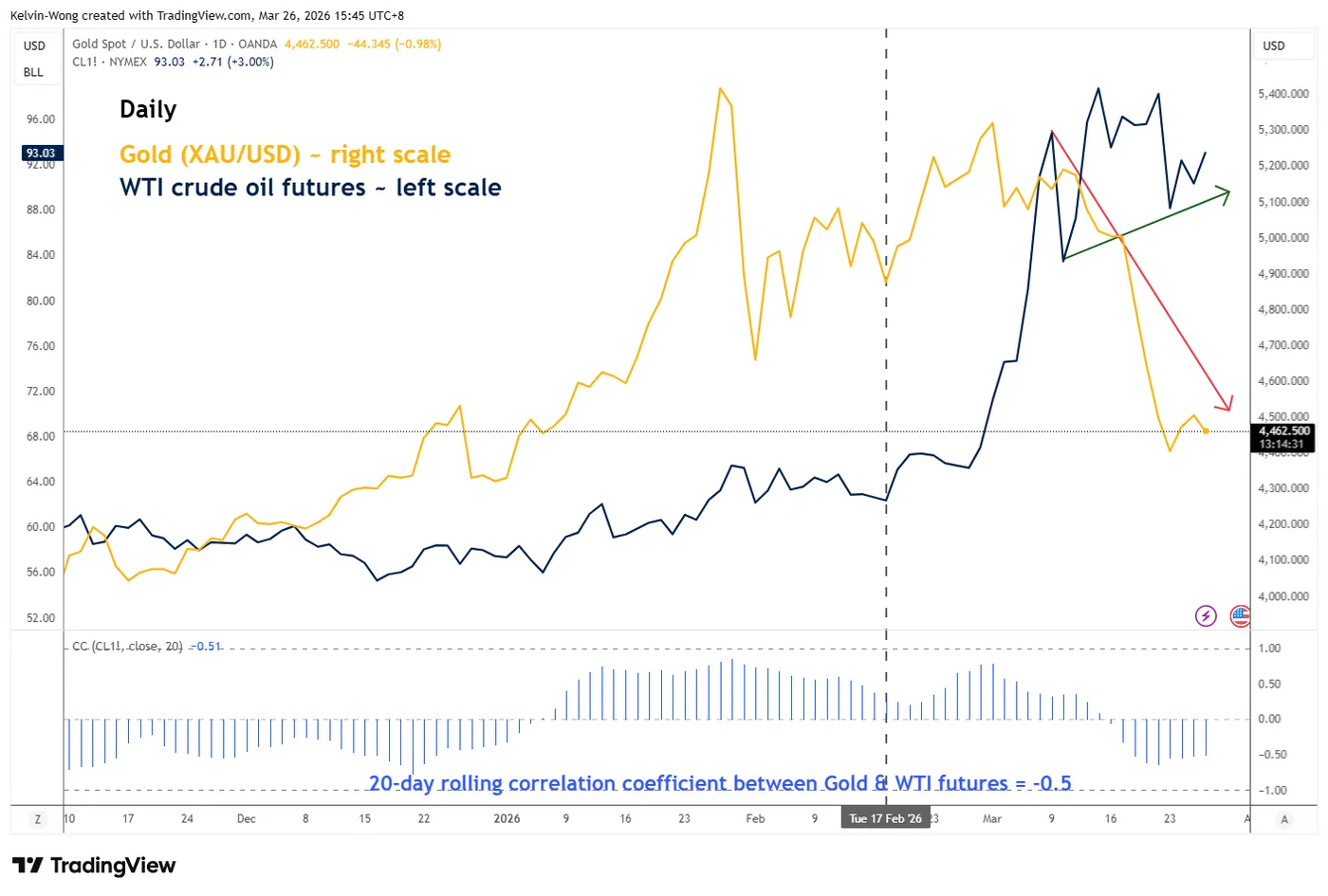

A firmer WTI crude oil supports further weakness in Gold (XAU/USD)

Fig. 1: Gold (XAU/USD) & WTI crude oil futures indirect correlation as of 26 Mar 2026 (Source: TradingView)

Fig. 2: West Texas Oil CFD minor trend as of 26 Mar 2026 (Source: TradingView)

The macro connection between WTI crude oil and Gold is stagflation risk.

Higher oil prices via supply side shock (closure of the Strait of Hormuz leads to a lesser oil supply globally, in turn, also creating a second-order effect of lower aggregate demand as input costs of finalized goods and services get more expensive).

Hence, stagflation is a deadly combination of higher prices and lower economic growth prospects in later stages. A challenging environment for central bankers as they cannot easily implement expansionary monetary policies to counter and anticipate the second-order demand destruction in a stagflation environment.

Therefore, central banks are likely to adopt a “wait and see” approach, and some “inflation-fighting” central banks may turn cautiously hawkish and start to implement an interest rate hike cycle.

Gold, being a non-interest income-bearing asset, will incur higher opportunity costs as interest rates rise globally, in turn, triggering a negative feedback loop into the price actions of Gold.

Since 17 February 2026, the movement of WTI crude oil futures has an indirect correlation with Gold (XAU/USD), and its 20-day rolling correlation coefficient stands at -0.5 at this time of writing (see Fig.1).

The recent pull-back in the West Texas Oil CFD (a proxy of the WTI crude oil futures) due to “TACO jaw bowing” has managed to find support at its rising 20-day moving average.

West Texas Oil CFD’s medium-term uptrend phase remains intact, a clearance above $93.70 key near-term resistance may see a further push up to retest the $102.25 intermediate range resistance in the first step (see Fig. 2).

Gold (XAU/USD) - End of corrective rebound, start of new bearish leg

Fig. 3: Gold (XAU/USD) minor trend as of 26 Mar 2026 (Source: TradingView)

Watch the $4,620 key short-term pivotal resistance on Gold (XAU/USD). A break below the $4,440 key near-term support (downside trigger level) may set off another bearish impulsive down move sequence to retest $4,167/4,099 before exposing the next supports at $4,007 and $3,936/3,886 (also a Fibonacci extension) (see Fig. 3).

On the other hand, a clearance and an hourly close above $4,620 invalidate the bearish scenario for an extension of the corrective rebound towards the $4,737/4,775 key medium-term pivotal resistance zone.

Key elements to support the bearish bias on Gold (XAU/USD)

- The hourly RSI momentum indicator has staged a bearish breakdown below its key ascending trendline support.

- The recent 12% rebound seen in Gold (XAU/USD) from its 23 March 2026 low has stalled close to the 50% Fibonacci retracement of the prior impulsive down move from the 10 March 2025 high to 23 March 206 low.