Sample Category Title

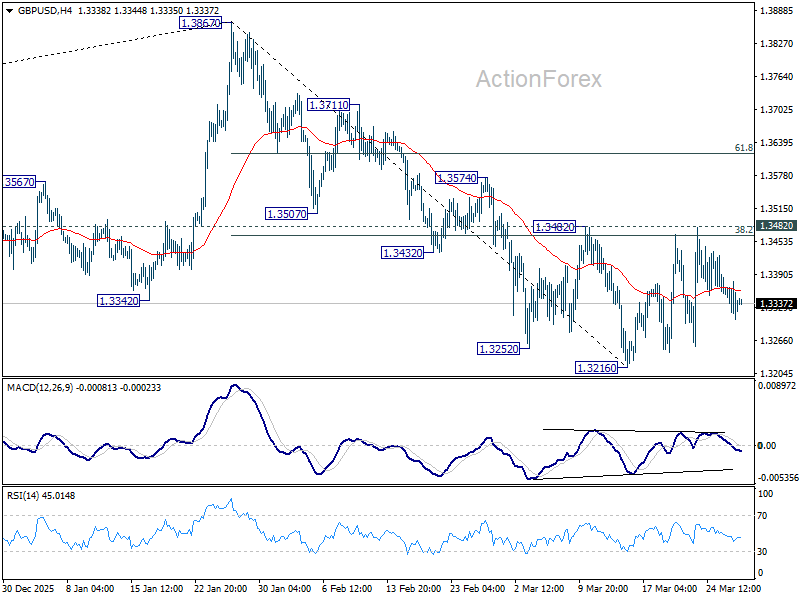

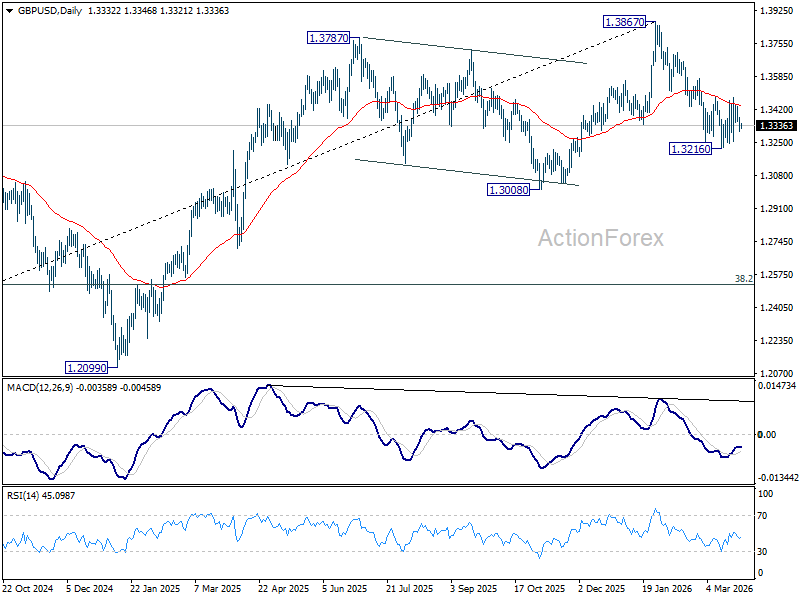

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3301; (P) 1.3340; (R1) 1.3369; More...

Range trading continues in GBP/USD and intraday bias remains neutral. With 1.3482 resistance intact, further decline is in favor. On the downside, below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

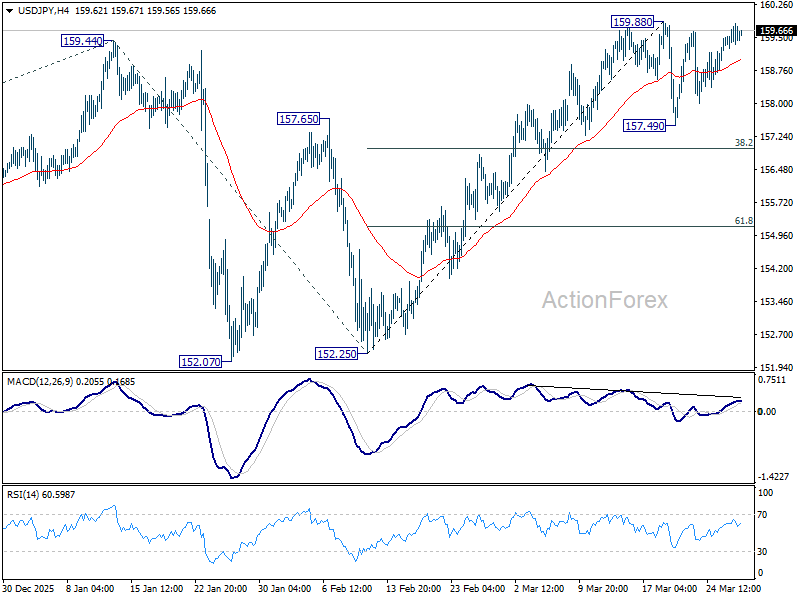

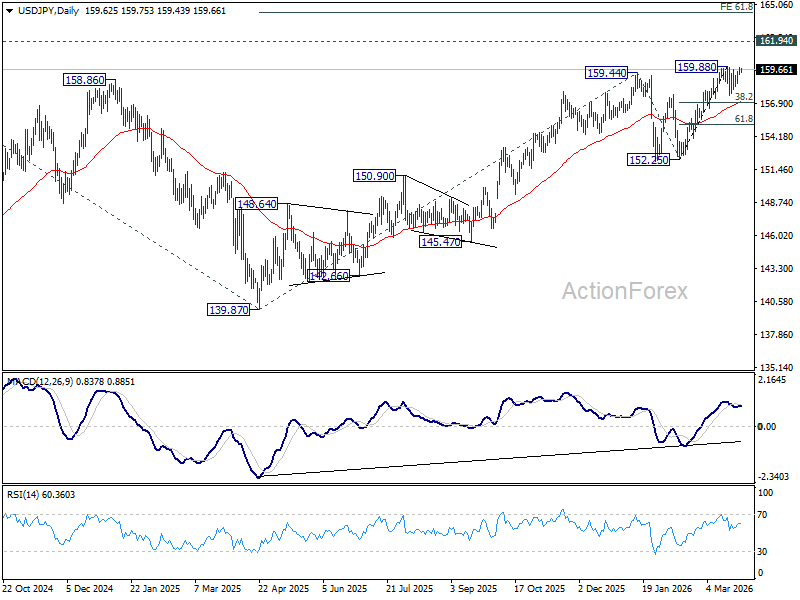

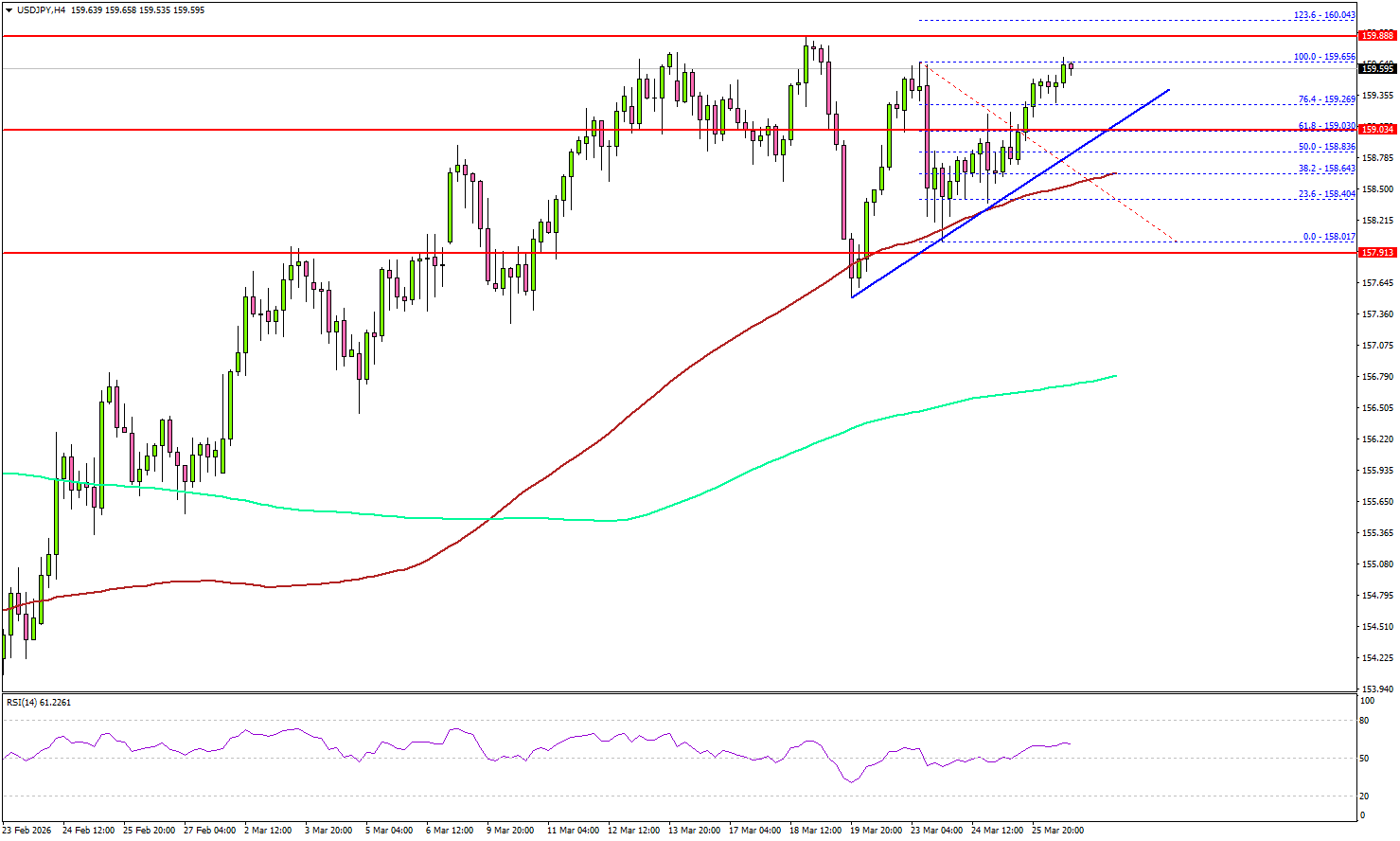

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.42; (P) 159.64; (R1) 159.98; More...

Range trading continues in USD/JPY and intraday bias stays neutral. Consolidation from 159.88 could extend with another falling leg. But in that case, downside should be contained by 38.2% retracement of 152.25 to 159.88 at 156.96 to bring rebound. On the upside, break of 159.88 will target a test on 161.94 high.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7924; (P) 0.7942; (R1) 0.7972; More….

Immediate focus is now on 0.7957 resistance in USD/CHF as rebound from 0.7833 extends. Firm break there will resume the rise from 0.7603, as correction to the downtrend from 0.9200, and target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rise is expected as long as 0.7833 support holds, in case of another retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

Iran Strike Pause: Slow-Boil Inflation Nightmare Scenario Keeps Dollar on Top

The latest 10-day extension of the Iran strike pause by US President Donald Trump might act as a “relief valve”, preventing a freefall in stocks. But it has also created a "slow-boil" inflation trap that is forcing a dramatic global monetary policy reversal. Contrary to providing a sentiment boost, Trump’s extension is paralyzing equity markets—preventing both a final capitulation and a meaningful recovery. This fundamental deadlock is keeping Dollar firmly at the top of the weekly performance table.

The "nightmare scenario" currently haunting global central banks is the transition from first-round to second-round inflationary effects. Typically, policymakers "look through" volatile energy spikes, but oil hovering at $105 for weeks is a different beast. It is high enough to infiltrate every layer of the economy—from plastics and transport to fertilizer—but not "explosive" enough to cause the immediate demand collapse that would naturally cool the market. This "slow boil" is exactly what leads manufacturers and logistics firms to stop absorbing costs and start passing them on to the final consumer.

The shift in rhetoric from the world’s most influential central banks has been swift. Bundesbank President Joachim Nagel, a noted hawk, has pivoted from discussing potential rate cuts to a 25bps "insurance hike" in April to protect the ECB's 2% target. Similarly, the Fed’s trajectory has undergone a massive reversal; after starting the year with expectations for multiple cuts, the market now assigns a near 50% chance of a rate hike in 2026.

As long as the Iran war drags on, the likelihood of inflation becoming entrenched grows, leaving central banks with no choice but to tighten.

Ultimately, Trump’s 10-day "relief valve" is a double-edged sword for investors. While it prevents a total market capitulation today, it also kills any appetite for "dip buying." Professional investors remain on the sidelines, paralyzed by the uncertainty of whether April 7 brings a diplomatic resolution or a regional energy war. This will keep the risk markets pressured, at least in the short term.

In the currency markets, this has solidified a clear hierarchy: Dollar and Sterling are the dominant beneficiaries, while growth-sensitive currencies like the Australian and New Zealand Dollars remain at the bottom of the pile.

In Asia, at the time of writing, Nikkei is down -0.12%. Hong Kong HSI is up 0.68%. China Shanghai SSE is up 0.70%. Singapore Strait Times is up 0.64%. Japan 10-year JGB yield is up 0.099 at 2.373. Overnight, DOW fell -1.01%. S&P 500 fell -1.74%. NASDAQ fell -2.38%. 10-year yield rose 0.088 to 4.416.

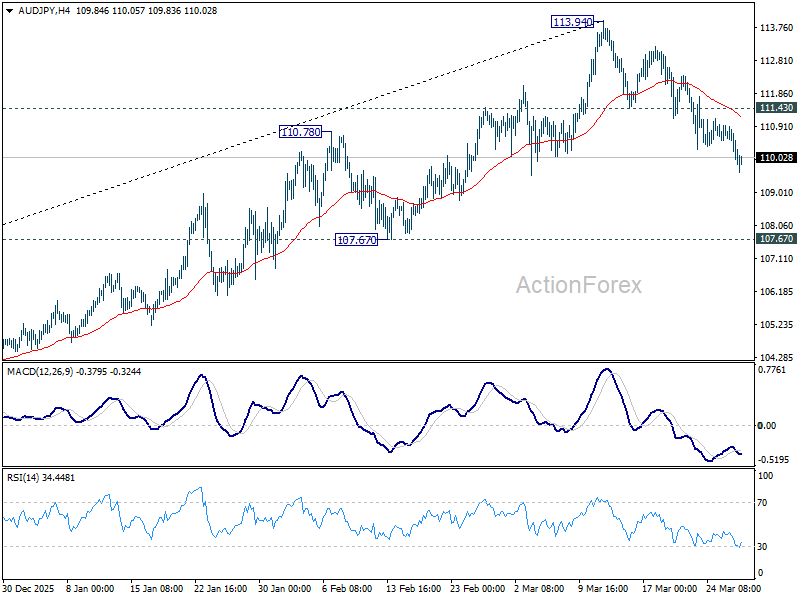

Stagflation Trap Could Tie RBA's Hawkish Hand, and Send AUD/JPY to 103

AUD/JPY is under pressure as rising geopolitical risks and surging energy and fertilizer costs create a stagflation threat for Australia. While markets still price a May RBA hike, growing concerns over a growth slowdown are raising doubts about further tightening. As expectations shift, the cross is at risk of a deeper correction toward the 103 level. Read More.

Fed Shifts Focus Back to Inflation as Officials See Labor Market in Balance

Federal Reserve officials are shifting focus back to inflation as the labor market is increasingly seen as balanced. Jefferson, Barr, and Cook warn that rising energy prices could push inflation higher and risk becoming entrenched if sustained. With policymakers prioritizing inflation risks over growth concerns, expectations for rate cuts are being pushed back, reinforcing a higher-for-longer outlook. Read More.

Oil Not a Simple Boost as BoC Rogers Flags Inflation and Growth Risks

Oil is no longer a clear tailwind for the Canadian Dollar, as Bank of Canada’s Carolyn Rogers warns that the latest energy surge is lifting inflation while weighing on growth. While higher oil prices support export income, rising costs are squeezing households and businesses, raising concerns about demand and investment. Read More.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7924; (P) 0.7942; (R1) 0.7972; More….

Immediate focus is now on 0.7957 resistance in USD/CHF as rebound from 0.7833 extends. Firm break there will resume the rise from 0.7603, as correction to the downtrend from 0.9200, and target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rise is expected as long as 0.7833 support holds, in case of another retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

USD/JPY Advances, Bulls Aim for Break Toward New Highs

Key Highlights

- USD/JPY started a fresh increase above 158.80 and 159.00.

- A bullish trend line is forming with support at 159.00 on the 4-hour chart.

- EUR/USD failed to clear the 1.1620 resistance zone and trimmed gains.

- Gold prices are again moving lower and might revisit $4,200.

USD/JPY Technical Analysis

The US Dollar remained supported above 158.00 against the Japanese Yen. USD/JPY regained traction and climbed above 158.80.

Looking at the 4-hour chart, the pair settled well above 158.80, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair cleared the 76.4% Fib retracement level of the downward move from the 159.65 swing high to the 158.01 low.

On the upside, the pair is now facing sellers near 159.80. The first major resistance sits at 160.00 or the 1.236 Fib extension level of the downward move from the 159.65 swing high to the 158.01 low.

A close above 160.00 could open the doors for gains above 160.80. In the stated case, the bulls could aim for a move to 162.00.

If there is no upside break above 160.00, the pair might start a fresh decline. Immediate support is seen near 159.00. The first key support sits at 158.80. A close below 158.80 might call for heavy losses. In the stated case, it could even revisit 157.50 in the coming days.

Looking at Gold, the price is signaling a fresh decline, and there are chances of a drop toward the $4,200 level.

Upcoming Key Economic Events:

- Fed's Barkin speech.

- Fed's Daly speech.

- Fed's Paulson speech.

Stagflation Trap Could Tie RBA’s Hawkish Hand, and Send AUD/JPY to 103

AUD/JPY’s selloff is accelerating as renewed risk aversion combines with a growing “stagflation trap” that is undermining the Reserve Bank of Australia’s hawkish outlook. While markets still price around a 72% chance of a May rate hike, surging energy and fertilizer costs are increasingly seen as a drag on growth rather than a simple inflation boost. As expectations begin to shift, the cross is at risk of a deeper medium-term correction toward the 103 region.

The broader backdrop is turning more defensive. Escalation risks in the Middle East remain elevated, with mixed messaging from US President Donald Trump—from ultimatums to extended pauses—failing to provide clarity. Rather than calming markets, the developments have prolonged uncertainty, keeping oil prices elevated and risk sentiment fragile.

This risk-off tone is weighing directly on the Aussie as AUD/JPY has emerged as one of the clearest expressions of this shift, with the pair among the biggest movers this week and downside momentum building.

At the same time, markets are reassessing the RBA’s policy path. The central bank’s March 17 hike was delivered on a narrow 5–4 split, already signaling internal divisions. While expectations for another hike in May remain firm, confidence in that outcome is becoming more fragile as new risks emerge.

The key issue is Australia's heavy reliance on imported refined fuels. Sustained Brent prices above 100 are feeding through into higher transport and business costs, raising inflation while simultaneously weighing on growth—a classic stagflation setup. The fertilizer shock adds extra pressure. Australia sources over 40% of its fertilizer imports from the Middle East, particularly Urea. With disruptions around the Strait of Hormuz, Urea prices have surged more than 30% in March, sharply increasing input costs for the agricultural sector. This threatens to squeeze farm margins and reduce output, while pushing food prices higher.

Taken together, these dynamics are complicating the RBA’s policy calculus. Inflation pressures argue for tightening, but the growth hit from rising costs and uncertainty raises the risk that further hikes could exacerbate the slowdown. Some market participant could start to speculate whether the balance could tilt toward a pause in May.

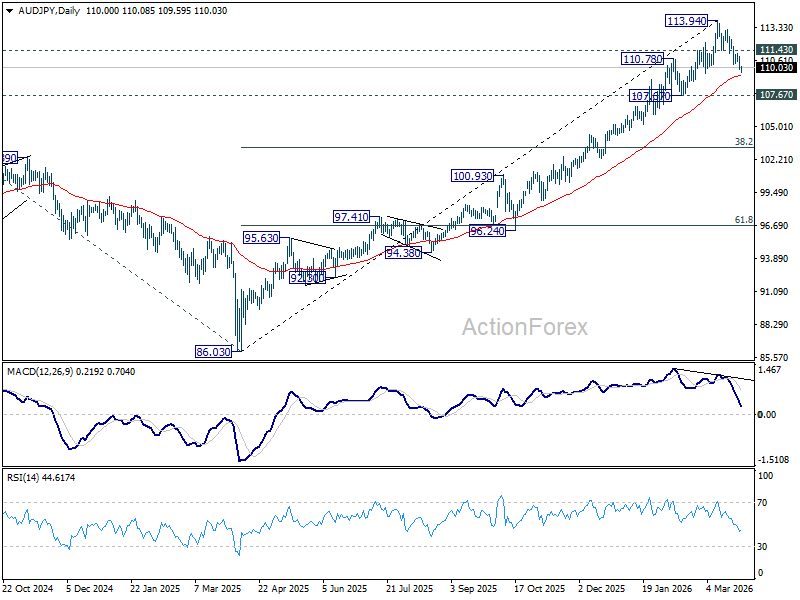

Technically, AUD/JPY is showing signs of a medium-term top, with bearish divergence visible in D MACD. The break of 110 level leaves it vulnerable, with immediate focus on the 55 D EMA (now at 109.31). Sustained trading below this level would open the door for a deeper pullback to 107.67 support next.

Decisive break of 107.67 will confirm that AUD/JPY is already correcting whole up trend from 86.03 (2025 low) and bring deeper decline to 38.2% retracement of 86.03 to 113.94 at 103.27.

Conversely, a strong rebound from current levels and a break above 114.30 would suggest the uptrend remains intact, though this scenario appears less likely as macro headwinds build.

Fed Shifts Focus Back to Inflation as Officials See Labor Market in Balance

Federal Reserve officials are signaling a shift in priorities, with the labor market increasingly viewed as “in balance” while inflation risks regain prominence. Comments from Philip Jefferson, Michael Barr, and Lisa Cook highlight a subtle but important pivot: employment conditions are no longer the primary concern, as attention turns back to rising price pressures driven by the Middle East energy shock.

Vice Chair Jefferson said he expects overall inflation to rise in the near term, reflecting higher energy prices stemming from the conflict. He emphasized that the duration of the shock will be critical—short-lived disruptions may only affect the economy for a quarter or two, but sustained increases in oil prices could have more material implications for both inflation and growth.

Governor Barr added that the key risk is a shift in "inflation expectations", which could lead to more entrenched price dynamics. He emphasized the importance of assessing how long energy prices remain elevated, with prolonged shocks posing a greater threat to both inflation and the broader economy.

Separately, Governor Cook further reinforced the message, stating that while overall risks are balanced, inflation risks are "greater right now:. This marks a clear change in emphasis, as policymakers prioritize containing inflation over responding to potential growth weakness.

Meanwhile, the labor market is seen as "balanced". Officials pointed to low hiring and downside risks, suggesting that while employment conditions are stable for now, they could weaken if shocks intensify.

Overall, the comments reflect a return to inflation vigilance. Rate cuts are being delayed, and while policy remains on hold for now, the balance of risks has shifted.

Oil Not a Simple Boost as BoC Rogers Flags Inflation and Growth Risks

Oil is no longer a clean positive for Canada, as a Bank of Canada official warn that the latest energy shock also risks fueling broader inflation rather. Senior Deputy Governor Carolyn Rogers said in a speech it is "too early to assess the impacts of the war on growth", but made clear that higher oil prices will bring both benefits and costs.

While stronger energy prices could lift export income, Rogers emphasized that the same shock will squeeze consumers and businesses through higher costs, while tighter financial conditions and elevated uncertainty weigh on spending and investment. This highlights a growing dilemma for policymakers, where the traditional growth boost from oil is increasingly offset by demand destruction risks.

Rogers warned that the recent rise in energy prices will push inflation higher in the near term, with the key risk being second-round effects spreading into other goods and services. With the policy rate held at 2.25% last week, the BoC is in a wait-and-see mode but stands ready to respond.

The Epic Blunder of Fighting the Last War

The Middle East conflict is not Venezuela, or Russia’s invasion of Ukraine, or COVID. Policymakers should not use “the last war” as a template for the current one.

- The Middle East conflict and the resulting fuel crisis are not the same as previous crises and should not require COVID-style policy responses such as work-from-home mandates. Governments and other decision-makers need to avoid the temptation to “fight the last war”. Nor should they fall into the trap of “we must do something, and this is something”, when that something is ill-suited to the current problem.

- The focus should instead be on the key issue for the world economy: how the conflict maps into energy-supply disruption via the closure of the Strait of Hormuz and/or damage to oil and gas infrastructure in other Gulf states. Time is almost up on our initial assumption that the Strait would be closed for about a month, so we will shortly update our baseline forecast to reflect this. But the Strait is a time-limited source of leverage for Iran. At some point, third-party countries will respond to the damage being done to them; already some tankers are being allowed through.

- This is a significant shock to the economy and a challenging situation for public policy. For the next few weeks, though, the appropriate monetary policy response is “wait and see”. The current crisis is not (yet) a financial crisis or a pandemic requiring immediate, potentially out-of-cycle, action. And conditions could be quite different in a month’s time. Domestic conditions will continue to shape the RBA’s decisions at its regular meetings.

“Fighting the last war” is a common cognitive trap: trying to make a current crisis fit a past one. We saw attempts to make COVID fit the GFC template by expecting borrower distress despite massive fiscal support and, in some quarters, to make the AI boom fit the COVID template of sudden mass job losses, at least in the US.

The current conflict in the Middle East is producing plenty of examples of this behaviour, again misguided. The US/Israel attack has not gone the same way as the US intervention in Venezuela, nor are the implications like those of Russia’s invasion of Ukraine. The geographic pinch-point of the Strait of Hormuz shapes both the energy-price implications and the military ones. The context also differs significantly: the world is not emerging from a pandemic, with macroeconomic policy highly expansionary and other supply chains already disrupted.

The domestic context in Australia also differs in important ways, particularly the ceiling on east coast wholesale gas prices introduced after the 2022 episode. We are also four years further along with solar and battery installation. These changes mean that, for Australia, this is mostly an issue of fuel prices and availability, rather than electricity (as in 2022–23).

In addition, the current conflict bears little resemblance to the COVID pandemic, so policy responses should differ. We were surprised that work-from-home mandates have been seriously proposed. A fuel shortage is not a respiratory virus, and there is no reason to prevent or discourage workers from attending their workplace if they commute by foot, bicycle or public transport. Better responses would be to expand public transport coverage and frequency, encourage carpooling (including more extensive transit lanes), and cancel non-essential government travel. Only if those policies fail, or fuel shortages become so extreme that critical workers need to be prioritised, would WFH become an appropriate response.

Likewise, businesses are not facing a sudden loss of income as the community goes into lockdown. Income support measures should therefore be much more targeted, if they are needed at all.

The main similarity to the pandemic is stockpiling, as people fear downstream supply disruptions. Policy responses to address this make more sense than mandating work-from-home. Options include publicising the restocking of petrol stations that had run out of some fuels, as well as measures already taken such as temporary changes to fuel standards and the oil-for-gas supply deal with Singapore.

A kinetic war between US/Israel and Iran could drag on without necessarily having its current dramatic impact on global energy markets. For the rest of the world, the key issues are closure of the Strait of Hormuz and actual or threatened damage to gas and other civilian infrastructure in non-combatant Gulf states. But closure of the Strait is a time-limited source of leverage for Iran. At some point, third-party countries will respond to the damage being done to them; already some tankers are being allowed through.

The immediate issue for the global and Australian economies is fuel availability. Higher prices will curb demand, but periods of localised unavailability will be especially disruptive.

The implications for macroeconomic policy depend on the broader effects on inflation and growth. The RBA was already hiking rates ahead of the outbreak of the conflict. Demand growth had picked up a little more sharply than they, or we, had expected. And with the economy no longer running with significant spare capacity as in the 2010s, even small upside demand or downside supply shocks show up in prices rather than being absorbed. More frequent policy adjustments should therefore be expected.

As highlighted by the RBA’s counterparts at the RBNZ, policymakers should ordinarily try to look through the first-round, fuel-specific impacts on inflation from a shock like this. Second-round effects such as higher transport and materials costs flowing through to other prices may, however, require a response. A lift in inflation expectations is also a watch point. But if the supply-disruption element of the conflict fades over the next month or so, these effects will also be short-lived. While the forthcoming update to our baseline forecast is more severe than this, the risks around it are two-sided. It will therefore pay to wait to see which scenario plays out ahead of the May meeting. A May rate hike is still on the cards for pre-existing domestic reasons, but pre-judging the second-round effects on inflation, and the need for any hikes beyond the next one, is a much less secure strategy.

In particular, we do not expect an out-of-cycle RBA decision. These are rare: the last one was in March 2020, just ahead of lockdown, and the one before that was in 1997, both to cut rates. Even during the GFC, there were no out-of-cycle policy decisions. The decision tree facing the RBA also does not require one. May seems a long way away, but by then either things will have de-escalated, or the war will have escalated, drawn in Gulf states and worsened energy supply. De-escalation would see some of the inflationary shock soon moderate, weakening the case for further policy tightening. Escalation would be an even larger negative shock to global growth than we are already facing, but also inflationary. With the Board already split on the need to hike expeditiously, we see neither the need, nor the appetite, to bring forward that decision in either scenario. This is not COVID, and we do not expect policymakers to act like it is.

Cliff Notes: A Fork in the Road

Key insights from the week that was.

In Australia, February’s CPI came in slightly below expectations, headline inflation ticking down to 3.7%yr from 3.8%yr, while trimmed mean inflation held steady at 3.3%yr. Constructive elements of the detail included: dwelling purchases posting its smallest increase in ten months; a below-expectations annual increase in education prices; and lower childcare costs, the result of increased take-up of the Childcare Subsidy following the introduction of the three-day guarantee. There were also a couple of upside surprises, however, most notable were clothing and some food-related categories. The impact from electricity rebates has also now abated, bringing reported electricity prices back into line with actual prices.

The net result is that the inflationary pulse Australia was experiencing prior to the current surge in fuel prices was marginally softer than expected. While fuel will undoubtedly boost headline inflation from March, the trimmed mean pulse is likely to hold above but near the top of the target range through 2026. For a detailed view of how each state’s economy is positioned to weather coming headwinds, see our latest Coast-to-Coast report.

The Q1 Westpac-ACCI Survey of Industrial Trends meanwhile showed that the long-awaited improvement in manufacturing conditions is finally materialising, the Actual Composite rising to 59.3 – a strong expansionary read. Underpinning the move was a surge in output growth, another solid lift in new orders and, encouragingly, a rise in employment and overtime. Note though, this survey was largely completed before the onset of the Middle East conflict. Australian manufacturing’s acute exposure to fuel and energy costs is likely to see a partial reversal in Q2 and a degree of apprehension over the outlook.

Offshore, data released was inconsequential. The preliminary March S&P Global PMIs for the major advanced economies unsurprisingly pointed to softer momentum and heightened inflationary pressures in the initial weeks of the Middle East conflict. FOMC members Bowman and Waller meanwhile were focused more on labour market weakness than inflation, though they felt it prudent to wait-a-while to assess the implications of the current conflict for price risks.

Regarding the state of the Middle East conflict, equity markets took solace in news the White House had been involved in initial intermediated discussions over the path to a ceasefire, although uncertainty over who in Iran’s leadership will take the lead in any formal negotiations has kept participants guessing on both the timing and potential success of these initiatives. The overnight extension of the 5-day reprieve for Iranian energy infrastructure by President Trump to 10 days is a positive step towards fruitful negotiations, however.

Iran’s military actions have also been relatively contained this week, and safe passage through the Strait of Hormuz has been provided to several ships, consistent with prior communications from Iranian officials that ships operated by countries not involved in the conflict are free to transit if Iran’s conditions are met. It is not clear if this includes a payment of up to US$2 million per shipment as previously telegraphed. If Iranian authorities hold to this guidance, China’s fleet and vessels from other non-aligned countries such as Malaysia (a key supplier to Australia who reportedly reached an agreement with Iran overnight) could slowly reduce the current global deficiency in crude and LNG supply, even if the US/Israel and Iran continue military actions against one another. The key risk remains the intentional, or unintentional, destruction of production and/or logistics facilities, turning a temporary loss of supply into an enduring one. The duration of this conflict and lost supply matters a great deal to both the persistence of global consumer inflation and the policy outlook.