Sample Category Title

NFIB Small Business Optimism Index Pulls Back in September

NFIB's Small Business Optimism Index fell 0.5 points to 90.8 in September, coming broadly in line with market expectations for a moderate decline. September’s reading marks the 21st consecutive month below the historical average of 98.

Four of the ten subcomponents pulled back the month, five improved and one remained unchanged. Sizable declines were recorded in two indicators: expectations about an improvement in the economy (down 6 points to -43%) and expected credit conditions (down 4 points to -10%).

The labor market data was somewhat more upbeat. The net share of businesses planning to increase employment rose one point to 18%, while the share of firms with unfilled job openings rose 3 points to 43%, reversing the decline in the month prior. Quality of labor concerns fell back one point, with 23% of business owners identifying this as their top business problem. Inflation concerns held flat, also at 23%.

The share of firms increasing compensation held steady at 36%, while 23% of firms indicated that they planned to increase compensation, only partially reversing the 5 point gain in the month prior. The share of businesses 'raising' average selling prices held flat at 30% (up seven points from the cyclical trough in April), while the share of firms 'planning’ to raise average selling prices rose two points for the second month in a row to 29%.

Key Implications

After some improvement in early summer, small business confidence appears to be souring again, with the mild decline in September marking the second consecutive pullback in the headline confidence measure. Despite this, labor market indicators continue to flash green, with job openings and plans to increase employment both ticking higher in September, and quality of labor concerns remaining top of mind. This echoes the theme of continued resilience in the U.S. labor market observed in the latest payrolls report.

Businesses continue to boost compensation to attract workers. While the share of firms increasing and planning to increase worker compensation has come off their pandemic peaks, both measures remain elevated near their pre-pandemic levels. Meanwhile, the share of firms raising and planning to raise average selling prices are still above pre-pandemic highs, and have come off their cyclical troughs recently. These elements highlight the upside threat to inflation, with the Fed expected to keep its foot on the monetary policy brakes, and perhaps press them a bit harder over the near-term.

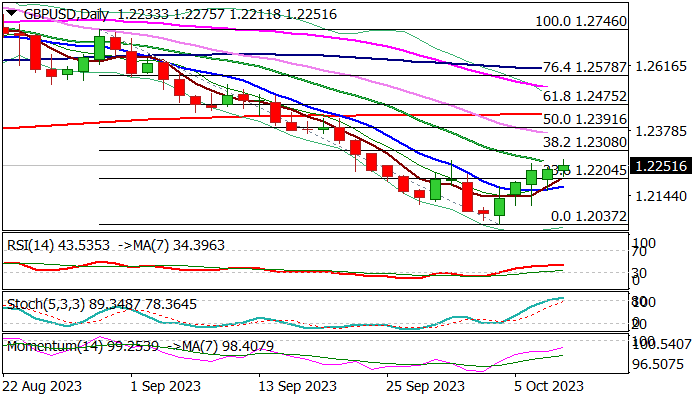

GBP/USD: Fresh Bulls Hold Grip But Need More Work to Signal Reversal

Cable rose to the highest in nearly two weeks on Tuesday, keeping in play near-term recovery which extends into fifth straight day.

Softer tone in the most recent comments from US policymakers, added to fresh but still limited risk appetite, keeping the pound underpinned for now.

Bulls probe through falling 20DMA (1.2252) with close above here to strengthen near-term structure for attack at pivotal Fibo barrier at 1.2308 (38.2% retracement of 1.2746/1.2037 downleg), violation of which would generate initial reversal signal.

On the other hand, caution is still required, as daily studies are still predominantly in bearish configuration (MA’s / momentum) and also turning overbought, warning that recovery may start running out of steam.

Dip-buying remains favored above 10DMA (1.2174) but expect the downside to be vulnerable while 20DMA caps.

Res: 1.2252; 1.2275; 1.2308; 1.2355.

Sup: 1.2204; 1.2174; 1.2105; 1.2052.

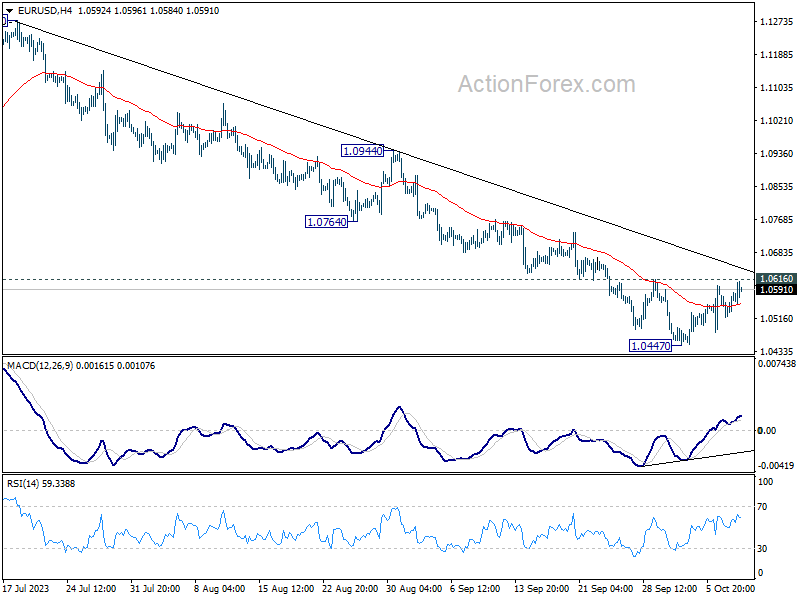

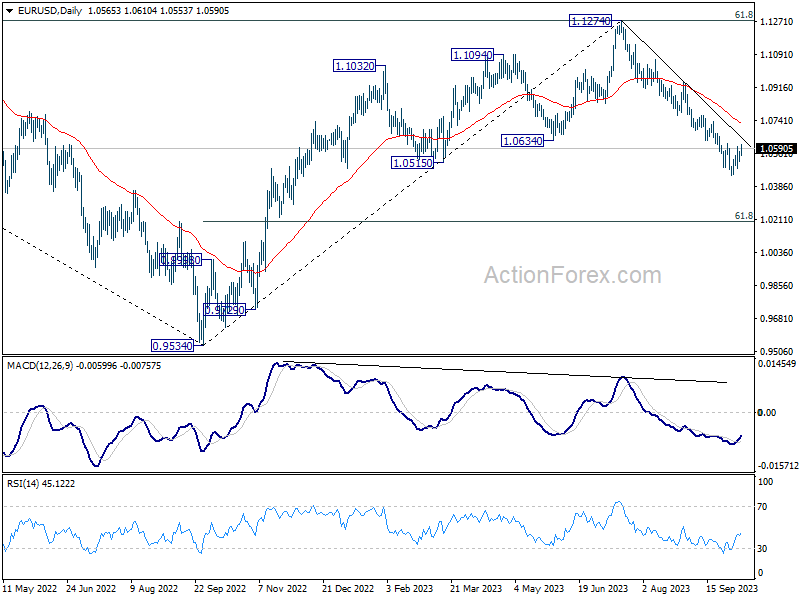

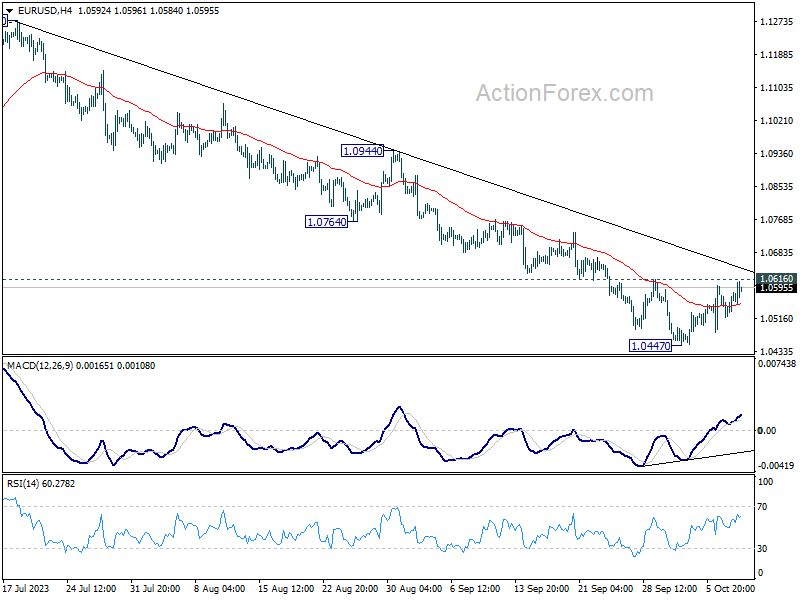

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0533; (P) 1.0554; (R1) 1.0587; More...

Intraday bias in EUR/USD remains neutral at this point. On the upside, firm break of 1.0616 resistance will confirm short term bottoming, and turn bias back to the upside for stronger rebound. Nevertheless, rejection by 1.0616 will retain near term bearishness. Break of 1.0447 will resume the fall from 1.1274 to 1.0199 fibonacci level next.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0725) holds, in case of rebound.

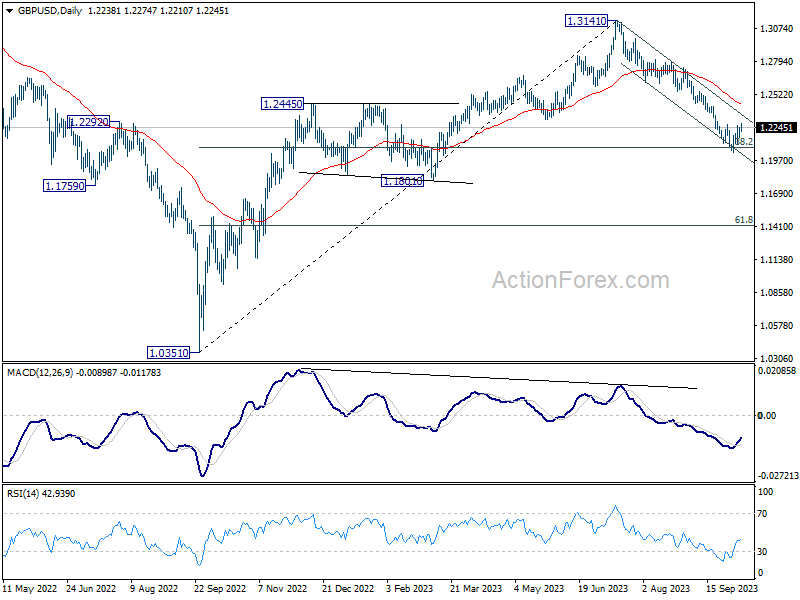

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2185; (P) 1.2215; (R1) 1.2266; More

Intraday bias in GBP/USD remains neutral for the moment. On the upside, firm break of 1.2270 resistance will confirm short term bottoming. Intraday bias will be back to the upside for stronger rebound. Nevertheless, rejection by 1.2270 will retain near term bearishness. Decisive break of 1.2075 fibonacci level would carry larger bearish implication and target 1.1801 support next.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2440) holds, in case of rebound.

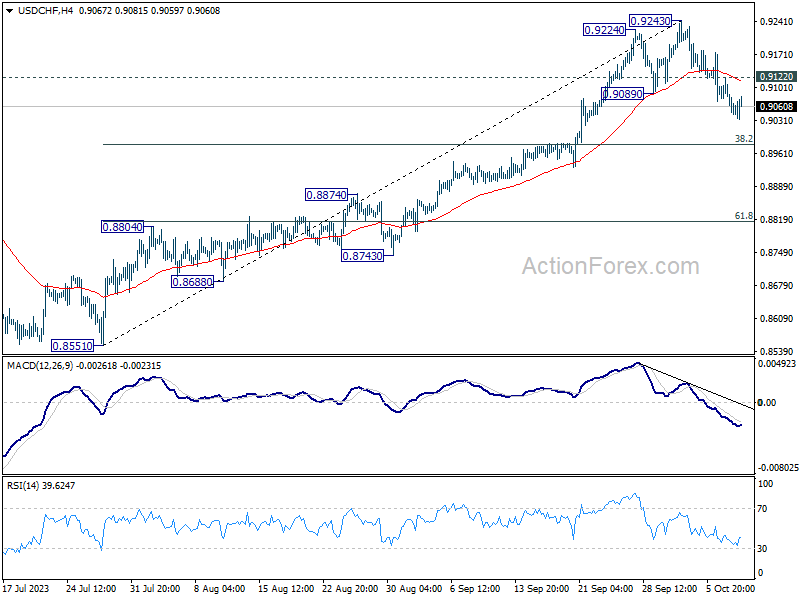

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9036; (P) 0.9080; (R1) 0.9111; More....

Intraday bias in USD/CHF stays on the downside for the moment. Corrective fall from 0.9243 could extend further to 38.2% retracement of 0.8551 to 0.9243 at 0.8979. On the upside, above 0.9122 minor resistance will turn intraday bias neutral first. But risk of another fall will remain as long as 0.9243 resistance holds.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8969) holds, even in case of deep pullback.

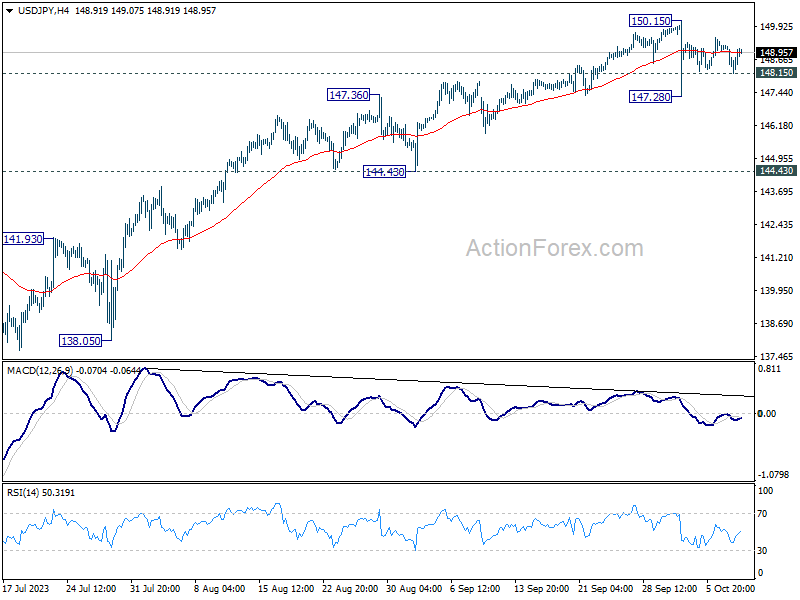

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.22; (P) 148.73; (R1) 149.02; More...

USD/JPY recovers further today but stays well below 150.15 resistance. Intraday bias remains neutral for the moment. Consolidation from 150.15 is still extending. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Yen Faces Pressure As Nikkei Soars, EUR/USD Eyeing Near Term Resistance

Yen is facing renewed selling pressure today as the development coincides a remarkable rebound in Nikkei and pullback in 10-year JGB yield. The notable rally in Nikkei, marking its largest single-day surge in nearly a year, is pivotal, signifying the potential of an extended risk-on sentiment in Japan that could correlate with a further depreciation of Yen.

Meanwhile, commodity currencies are not spared. Canadian, Australian, and New Zealand Dollar are also on the losing end, albeit their losses are contained within the previous day's range. Euro, on the other hand, is notably gaining traction, outpacing both the Sterling and the Swiss Franc, as all European majors strength.

Dollar presents a mixed bag, restrained partly by a retreat in US benchmark yield. Market participants are likely adopting a wait-and-see approach, with the CPI data slated for release later in the week being a significant determinant of Dollar's directional bias.

In the technical realm, EUR/USD will be in focus in the current session as recovery from 1.0447 extends. Firm break of 1.0616 will argue that the pair has already bottomed in the short term. Furthermore, sustained trading above the near term falling trend line will trigger stronger rally back to 1.0764 support turned resistance, even as a correction to the decline from 1.1274. If materializes, this could be accompanied by broad based decline in the greenback too, probably except versus Yen.

In Europe, at the time of writing, FTSE is up 1.63%. DAX is up 1.54%. CAC is up 1.47%. Germany 10-year yield is up 0.054 at 2.830. Earlier in Asia, Nikkei rose 2.43%. Hong Kong HSI rose 0.84%. China Shanghai SSE dropped -0.70%. Singapore Strait Times 1.03%. Japan 10-year JGB yield fell -0.0285 to 0.774.

Middle East strife indirectly spurs Nikkei to largest gain in 11 mths

Japan's Nikkei index surged by 2.43% upon reopening after a long weekend, logging the largest single day gain in 11 months. Conventional wisdom might suggest that heightened geopolitical tensions typically dampen investor sentiment. However, the dynamics observed in the Japanese market unfold a contrasting narrative.

The ascendancy in Nikkei is attributed, in part, to significant gains witnessed in the oil sector. Oil explorer Inpex saw an impressive 8.6% spike, while Japan Petroleum Exploration soared by 10.7%. These gains align with the rally in oil prices globally, stimulated by the escalating conflict in the Middle East.

The unexpected positive response of Japanese stocks to the geopolitical unrest has fueled a debate among market observers. Some argue that the intensifying situation in the Middle East might lead to reconsideration on Fed's policy path. There's a burgeoning perspective that Fed might hold off on further rate hikes, given the potential economic uncertainties injected by the conflict.

Technically, today's rebound in Nikkei argues that corrective pattern from 33772.89 (Jun high), could have completed with three waves down to 30487.67. That came after drawing support from 38.2% retracement of 25661.89 to 33772.89 at 30674.48. Next focus is 55 D EMA (now at 32149.24) Sustained trading above there will solidify this bullish case and target retesting 33772.89 high.

ECB's Villeroy: We're not at similar situation to Kippur War

In an interview with franceinfo radio, ECB Governing Council member Francois Villeroy de Galhau affirmed that the current interest rates, pegged at a historical high of 4% after ten consecutive hikes, are positioned at a "good level". Furthermore, Villeroy added that the prevailing economic climate doesn't warrant additional rate hikes.

However, Villeroy didn't mince words when expressing his apprehensions about the escalating oil prices. The surge in prices this week can be attributed to potential disruptions in supply, catalyzed by the military confrontations between Israel Palestinian Islamist group Hamas. Such geopolitical tensions have historically influenced global oil prices. A notable instance from the past is the 1973 Yom Kippur War, which had a significant bearing on oil price dynamics.

Addressing this historical context, Villeroy remarked, "I don't think that we are today in a similar situation (as the Kippur War) but we must of course remain very vigilant." He went on to underscore that such events amplify the existing economic uncertainty.

Australian consumer sentiment ticks up to 82, but interest rates concerns linger

Australia's Westpac Consumer Sentiment Index showed a positive move, climbing 2.9% from 79.7 to 82 in October. Despite the uptick, a score of 82 still paints a subdued picture, correlating with a decline in per capita spending.

One of the more pressing concerns for consumers remains the prospective upward movement in mortgage interest rates. The post-October RBA decision survey indicated that 63% of consumers anticipate mortgage interest rates to climb in the forthcoming year. This figure marks a substantial rise from 52.3% in September.

Notably, however, these numbers don't match the heightened concerns recorded when RBA was in an active rate-hiking mode, where readings ranged between 70-80%. Meanwhile, optimism for a rate cut next year has dwindled; only 7% of consumers now hold that expectation, down from 15% the previous month.

The upcoming November 7 meeting of RBA is earmarked as a significant event, with a revised set of forecasts to accompany the Statement on Monetary Policy.

Westpac shared their viewpoint on the evolving situation: "While the RBA may need to revise its near-term forecasts for headline inflation up, on its own this will probably not be enough to trigger a further rate rise."

The September quarter CPI, slated for release on October 25, is now in sharp focus. Westpac added, "If, however, there are further surprises in the September quarter CPI, due October 25, the next few meetings could be a little more live than the one in October."

Australian NAB business confidence unchanged at 1, declining conditions and easing price pressures

Australia NAB Business Confidence for September remained stable at a level of 1. Meanwhile, a decline was observed in Business Conditions, which slid from 14 to 11. A deeper dive into the components reveals trading conditions receding from 19 to 16, profitability conditions from 14 to 8, and employment conditions registering a dip from 10 to 8.

Notably, growth in labor costs saw a deceleration, moving from a 3.2% quarterly rate down to 2.0%. Additionally, purchase costs experienced a slowdown from 2.9% to 1.8%. Both final product prices and retail prices exhibited moderated growth rates, with the former decelerating from 1.7% to 1.0% while the latter remained unchanged at 1.8%.

NAB Chief Economist Alan Oster remarked, "the economy has remained in reasonable shape through the middle of the year." He went on to note the +1 index points underscores that firms are somewhat ambivalent regarding their future prospects, with views split evenly regarding the outlook.

However, there was a silver lining in the inflation scenario. Oster highlighted that "the survey showed some positive signs for inflation with cost pressures and price growth easing in the month."

Even though the imminent Q3 CPI release is anticipated to reflect strong inflation for the quarter, Oster noted, "the September survey results suggest the momentum of some of the key cost pressures driving inflation may have started to step back in a welcome sign for the broader inflation outlook."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.22; (P) 148.73; (R1) 149.02; More...

USD/JPY recovers further today but stays well below 150.15 resistance. Intraday bias remains neutral for the moment. Consolidation from 150.15 is still extending. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Oct | 2.90% | -1.50% | ||

| 23:50 | JPY | Current Account (JPY) Aug | 1.63T | 2.41T | 2.77T | |

| 00:30 | AUD | NAB Business Conditions Sep | 11 | 13 | ||

| 00:30 | AUD | NAB Business Confidence Sep | 1 | 2 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Sep | 49.9 | 53.2 | 53.6 | |

| 08:00 | EUR | Italy Industrial Output M/M Aug | 0.20% | -0.60% | -0.70% | -0.90% |

| 10:00 | USD | NFIB Business Optimism Index Sep | 90.8 | 91.5 | 91.3 | |

| 14:00 | USD | Wholesale Inventories Aug F | -0.10% | -0.10% |

Middle East strife indirectly spurs Nikkei to largest gain in 11 mths

Japan's Nikkei index surged by 2.43% upon reopening after a long weekend, logging the largest single day gain in 11 months. Conventional wisdom might suggest that heightened geopolitical tensions typically dampen investor sentiment. However, the dynamics observed in the Japanese market unfold a contrasting narrative.

The ascendancy in Nikkei is attributed, in part, to significant gains witnessed in the oil sector. Oil explorer Inpex saw an impressive 8.6% spike, while Japan Petroleum Exploration soared by 10.7%. These gains align with the rally in oil prices globally, stimulated by the escalating conflict in the Middle East.

The unexpected positive response of Japanese stocks to the geopolitical unrest has fueled a debate among market observers. Some argue that the intensifying situation in the Middle East might lead to reconsideration on Fed's policy path. There's a burgeoning perspective that Fed might hold off on further rate hikes, given the potential economic uncertainties injected by the conflict.

Technically, today's rebound in Nikkei argues that corrective pattern from 33772.89 (Jun high), could have completed with three waves down to 30487.67. That came after drawing support from 38.2% retracement of 25661.89 to 33772.89 at 30674.48. Next focus is 55 D EMA (now at 32149.24) Sustained trading above there will solidify this bullish case and target retesting 33772.89 high.

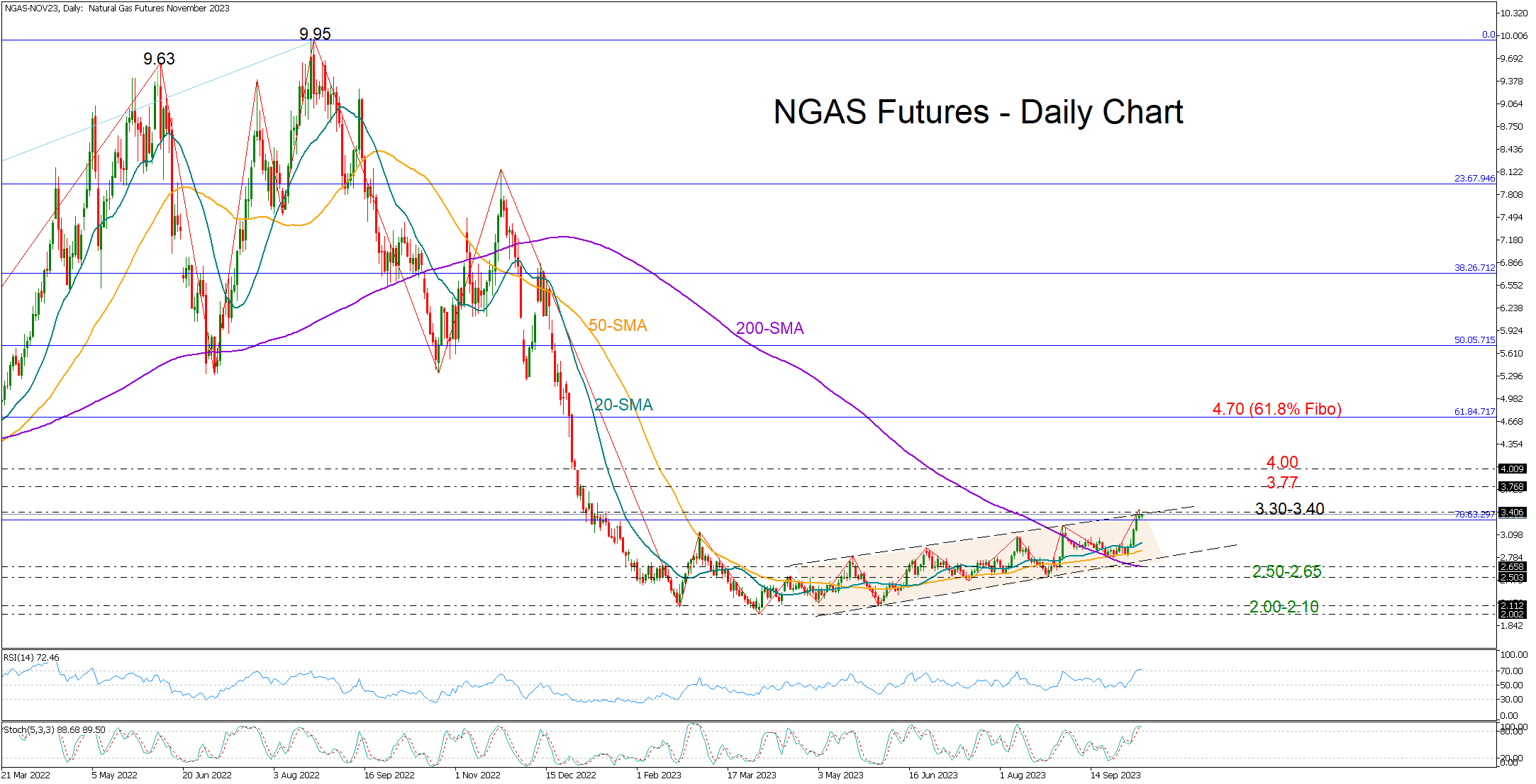

Will Natural Gas Futures Shift to a Bull Market?

- Natural gas futures reach caution area

- Market structure sends encouraging signals

Natural gas futures (November delivery) have been gently trending up since April’s 32-month lows, marking new higher highs and higher lows at a soft pace.

The recent upturn in the price brought the January 2023 resistance territory of 3.40 under the spotlight. Interestingly, this is where the bulls faced confluence at the end of October 2020 before they cracked that wall and staged an impressive rally to 6.44 in June 2021.

Monday's candlestick, with a small body at the top of an upward channel, has raised concerns about an upcoming bearish wave. Note that the RSI and the stochastic oscillator have entered overbought waters.

Yet, the positive crossings of the short and long-term SMAs show an upward trend forming.

The 78.6% Fibonacci retracement of the 2020-2022 uptrend is currently buffering downside pressures around 3.30. If that floor stays firm, with the price ascending above the channel too, resistance could next emerge somewhere between 3.77 and the 2023 high of 4.00. A successful battle there could activate new buying orders up to the 61.8% Fibonacci of 4.70.

Alternatively, a slide below 3.30 could see a test of the 20- and 50-day SMAs, while the channel’s lower band and the 200-day SMA could reject any declines towards the 2.50 base. Should the latter give way, the bears may re-challenge the 2023 floor of 2.10-2.00 with scope to expand the downtrend to the 2020 base of 1.50.

In a nutshell, natural gas futures could experience some profit taking in the short-term following a week of gains. As regards the market trend though, there are signs of improvement.

AUD/USD Drifting After Mixed Confidence Data

- Australian consumer confidence rebounds, business confidence eases

- Fed members say higher bond yields could cool inflation

The Australian dollar is unchanged on Tuesday, trading at 0.6412.

Australian consumer confidence rebounds, business confidence ticks lower

Australia’s Westpac consumer confidence index rebounded in October with a 2.9% gain to 82, up from 79.7 in September. This was the highest level in six months, but consumer confidence remains deep in pessimistic territory, below the neutral 100 level. The survey found that consumers remain concerned about high inflation and the possibility of higher interest rates. The latter is somewhat surprising, as the Reserve Bank of Australia has held rates for four straight months, but nevertheless, consumers are wary about further rate hikes.

The Westpac survey found that family finances remain under pressure, which dovetails with the Reserve Bank of Australia’s finance stability report, which found a large number of households are experiencing stress over their mortgage payments.

Australia’s NAB Business Confidence came in at 1 in September, unchanged after the August reading was revised from 2 to 1. Business conditions eased in August to 11, down from 14, with the employment sub-index component declining.

The RBA has paused four straight times and the futures markets have priced in another pause at the November 7th meeting at 95%. At the meeting earlier this month, RBA Governor Bullock said that additional rate hikes were a possibility, but the markets are viewing this as lip service in order not to lose credibility in the event that the central bank unexpectedly raises rates.

With no major US releases until Wednesday, the focus has been on Fedspeak, with a host of Fed members making public statements early in the week. On Monday, Fed members Jefferson and Logan said the spike in long-term bond rates could mean less of a need for the Fed to raise rates. The reason is that borrowing had become more expensive and inflation could ease without the Fed needing to raise rates.

US 10-year yield rates rose as high as 4.8% last week, a 16-year high, compared to 4.0% in July. Higher yields on Treasuries have led to an increase in other borrowing costs, including mortgages and consumer loans. This could put the Fed’s hopes for a soft landing in jeopardy and are providing support for the Fed to hold rates until next year. The odds of a rate hike before the end of 2023 have fallen to 27%, compared to 39% just one week ago, according to the CME FedWatch Tool.

AUD/USD Technical

- 0.6372 is a weak support line. Below, there is support at 0.6338

- There is resistance at 0.6458 and 0.6531