Sample Category Title

Sunset Market Commentary

Markets:

The Israel-Hamas conflict dominates headlines today, but the market impact is constraint for now. With Japan and the US closed, traded volumes are low though, suggesting to wait at least tomorrow’s action before drawing firm conclusions. (Slight) risk aversion is the obvious undertone today. Main European stock markets lose 0.5% to 1%. The dollar is the preferred currency with EUR/USD currently trading at 1.0540 compared to last week’s close at 1.0583. Negative risk sentiment helps the Japanese yen to put its foot against the greenback with the pair going nowhere around 149.10. Oil prices spike higher with Brent crude currently near $88/b compared to last week’s close at $84.5/b. Bullion ends a dismal run bouncing off YTD lows around $1825/ounce to $1862 at the moment. German Bund yields correct 4.6 bps (5-yr) to 1.3 bps (30-yr) lower across the curve. Today’s only data point – German industrial production figures for August – printed near consensus at -0.2% M/M and -2% Y/Y. Production in industry excluding energy and construction was up by 0.5% M/M due to a rebound in the car industry. 10-yr yield spread changes vs Germany widen by up to 4 bps for Italy. The Italian spread reached a new YTD high at 207 bps, approaching the December top at 217 bps. Italy’s departing central bank governor Visco touched on the issue in an FT interview. He warned the Meloni government – who performed better than many feared according to him – to listen to market concern about the long-term potential growth rate of the economy. He explains the increase in the debt ratio towards 140% of GDP mainly by that dismal growth. Obviously, Italian spreads are rising against a background of higher risk-free rates, significant budget deficits, worries about rising interest rate expenses and the lack of ECB backing. Finally, we retain comments from Dallas Fed Logan who partly echoed SF Fed Daly last week. She argued that higher term risk premiums could do some of the work of cooling the economy, leaving less need for additional monetary policy tightening. On the other hand, “to the extent that strength in the economy is behind the increase in long-term interest rates,” the central bank may need to tighten more. Later this week, attention turns to the US Treasury’s mid-month refinancing operation with 10-yr Note and 30-yr Bond sales on Wednesday and Thursday, the IMF’s update to the global economic outlook, the ECB’s consumer expectations survey (Wednesday), minutes of the FOMC (Wednesday) and ECB (Thursday) meetings, US September CPI inflation figures (Thursday) and the start of Q3 earnings with Blackrock, Citigroup, JP Morgan Chase and Wells Fargo & Co (Friday).

News & Views:

The Hungarian trade balance again recorded a surplus of €708mn in August. Exports of goods were 0.5% higher M/M while imports declined 0.9% M/M. Compared to the same month last year €-denominated exports declined 1.5% but imports were 19% lower. YTD, the country succeeded a € 5 630mn surplus compared with a deficit of €5,644mn over the same period in 2022. The improvement in the country’s external position is an important factor for the National Bank of Hungary as it supports domestic financial stability, including the value of the forint, allowing for monetary policy normalization. On the other hand, government data published this morning showed that the country reached a government budget surplus in September of only HUF 33,7bn .The cumulative deficit YTD still stands at HUF 3 299bn. Last week, the government upwardly revised its budget deficit target for this year to 5.2% from 3.9%. The forint weakens from the EUR/HUF 386.5 area at the close last week to EUR/HUF 388.5 currently on the global risk-off sentiment.

The Bank of Israel announced a program to sell up $30bn in FX reserves “in order to moderate volatility in the shekel exchange rate and to provide the necessary liquidity for the continued proper functioning of the markets”. In addition to the $30bn program, and as necessary, the Bank will provide liquidity to the market through swap mechanisms of up to $15bn. Despite the announcement, the shekel remains under pressure against the dollar. It trades at USD/ISL 3.9325 compared to levels near USD/ILS 3.85 at the end of last week. The currency now trades at the weakest level against the dollar since early 2016.

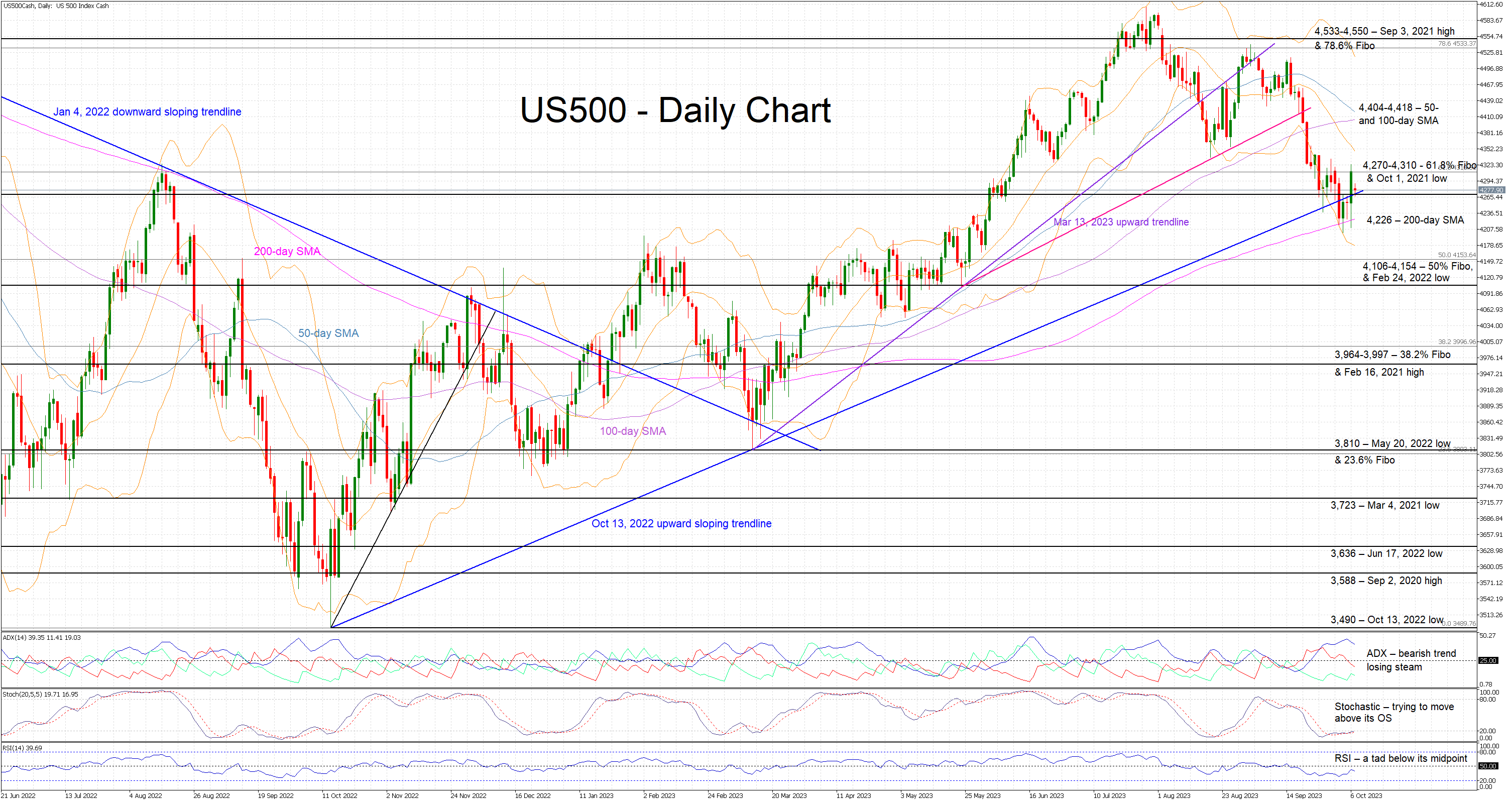

US 500 Cash Index Digests Developments

- The US 500 cash index jumped decisively higher on Friday

- The index bounced off the October 13, 2022 trendline

- The momentum indicators could be close to supporting a reversal

The US 500 cash index is trading sideways today, a much quieter session amidst the Columbus Day holiday. Market participants have the chance to digest Friday’s performance, when the US 500 index managed to successfully bounce off the long-term October 13, 2022 ascending trendline, and developments elsewhere.

The focus has understandably turned to the momentum indicators for an indication on the next leg in the US 500 cash index. The Average Directional Movement Index (ADX) appears to have peaked, and it is gradually edging lower. Similarly, the RSI has jumped higher, and it is currently trading a tad below its midpoint. More importantly, the stochastic oscillator is preparing to move aggressively above its oversold territory. This could be the signal the bulls have been expecting in order to regain market control.

Should the bulls appear determined to recoup part of their recent losses, they could try to stage a move towards the 4,404-4,418 area set by the 50- and 100-day simple moving averages (SMAs). Higher, they could retest the 4,533-4,550 range that is defined by the 78.6% Fibonacci retracement level and the September 3, 2021 high.

On the flip side, should the bears decide to fight the current upleg, they could try to finally break the 4,270-4,310 area, which is populated by the 61.8% Fibonacci retracement level of the January 4, 2022 – October 12, 2022 downtrend and the October 1, 2021 low. They could then come up against the 200-day SMA at 4,226, which, if broken, will open the door for a more protracted sell-off towards 4,106-4,154 range.

To conclude, the US 500 cash index bulls enjoyed Friday’s rally but for this move to have legs, they will probably need ample support from the momentum indicators.

Euro Slips as German Industrial Production Declines

- German Industrial Production declines for fourth straight month

The euro has started the week with losses. In the European session, EUR/USD is trading at 1.0527, down 0.57%.

Germany’s industrial production declines

German industrial production declined in August by 0.2%, following a revised -0.6% reading in July and shy of the consensus estimate of -0.1%. This marked a fourth straight decline, pointing to a prolonged slump in the production sector. There was some good news last week as factory orders rose 3.9% in August, but the outlook remains difficult. The manufacturing sector has been stuck in a downturn, with the September Manufacturing PMI coming in at 39.6, which indicates a sharp contraction (the 50 level separates contraction from expansion).

Germany has traditionally been the locomotive of the eurozone, but the largest economy in the bloc is a shadow of its former self. The economy was flat in the second quarter and the economy may have contracted in Q3. The German economy is getting squeezed by high interest rates, weak consumer consumption and falling exports.

US nonfarm payrolls sizzle

US nonfarm payrolls surprised to the upside, with a massive increase of 336,000 in September. This crushed the market consensus of 170,000 and the upwardly revised August reading of 227,000. The unemployment rate remained at 3.8%, compared to the market consensus of 3.7%. Wage growth decelerated in September – from 0.3% to 0.2% m/m and from 4.3% to 4.2% y/y. This is another sign that inflation is easing.

The blowout nonfarm payrolls led to the Fed futures market increasing the odds of a rate increase before the end of the year, which currently stands at 31%, according to the CME FedWatch tool. The Fed has been signalling that rates will remain “higher for longer” and traders appear to be listening to the Fed’s message.

EUR/USD Technical

- EUR/USD is testing support at 1.0545. Below, there is support at 1.0489

- 1.0641 and 1.0697 are the next resistance lines

EUR/USD Faces Downward Pressure Amid Rising Geopolitical Tensions

The principal currency pair, EUR/USD, is experiencing a decline as the week commences, predominantly driven by heightened risk aversion in the market. As of Monday morning, the currency pair's quotations are closely aligned with the 1.0552 mark.

A major contributor to the current sentiment is the escalating conflict between Arabian and Israeli forces. This geopolitical uncertainty has prompted investors to adopt a cautious stance, aiming to sidestep potential complications arising from the conflict.

Economic statistics unveiled in the US on Friday presented a mixed picture. The nation's unemployment rate steadfastly remained at 3.8%. Contrarily, non-farm payrolls demonstrated a robust uptick, registering an increase of 336,000, substantially surpassing the anticipated 171,000. The average hourly earnings metric retained its prior growth trajectory, with a month-on-month rise of 0.2%.

The employment sector's performance seemingly provides the US Federal Reserve with sufficient justification to proceed with interest rate hikes. However, consumer spending appears to be decelerating. Contrary to projections of an 11.7 billion USD increase, the US consumer lending volume dwindled by 15.6 billion USD.

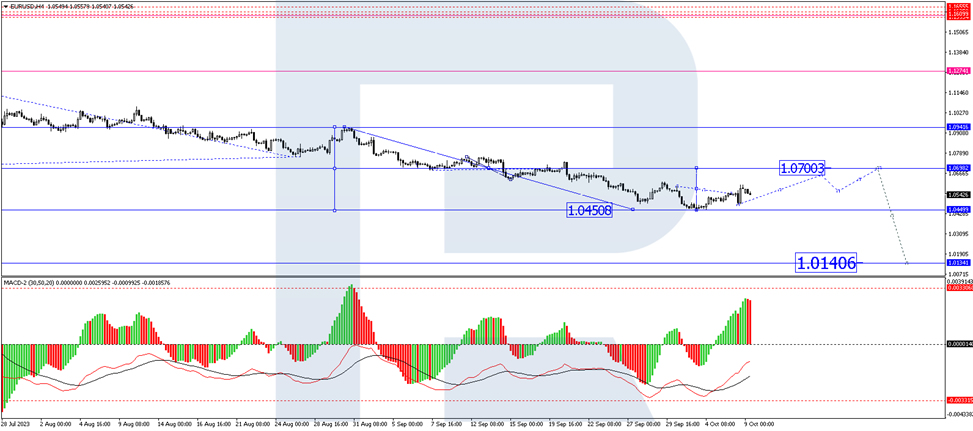

EUR/USD technical analysis

On the EUR/USD H4 timeframe, the market achieved the local target of the bearish wave at the 1.0450 juncture. As of the present moment, a corrective wave culminating at 1.0599 has been realized. The currency pair is now poised for a dip to the 1.0520 level, with indications suggesting the formation of a consolidation range around this point. A breach of this range to the upside could potentially propel the currency pair to the 1.0700 mark. Once this level is attained, a subsequent bearish wave targeting 1.0140 may ensue. The Moving Average Convergence Divergence (MACD) offers technical corroboration for this outlook, with its signal line entrenched below the zero mark, exhibiting a sharp upward trajectory, and poised for fresh peaks.

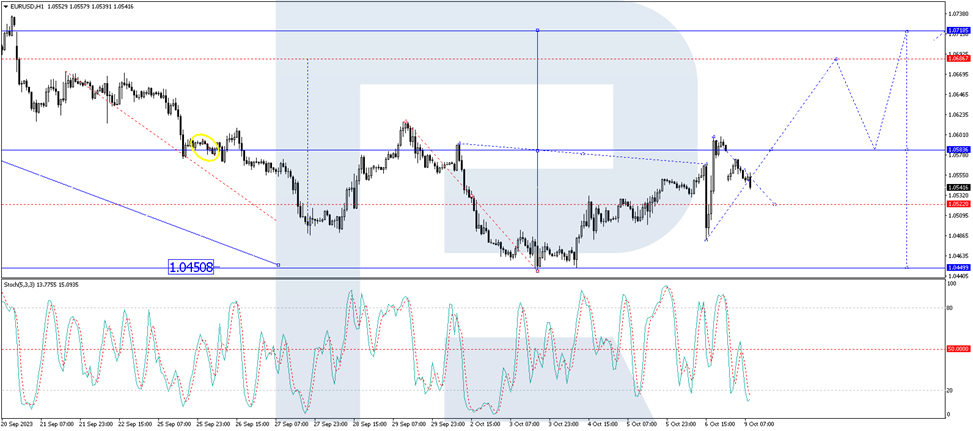

On the H1 timeframe for EUR/USD, an ascent towards 1.0599 has been charted. The market is currently undergoing a correctional phase targeting the 1.0520 mark. Upon completion of this correction, the potential for a bullish wave reaching 1.0700 emerges. This scenario gains validation from the Stochastic oscillator, which currently trades below the zero level but anticipates a climb to the 50-mark. A successful breach of this level could potentially drive the oscillator to the 80-mark.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0513; (P) 1.0556; (R1) 1.0630; More...

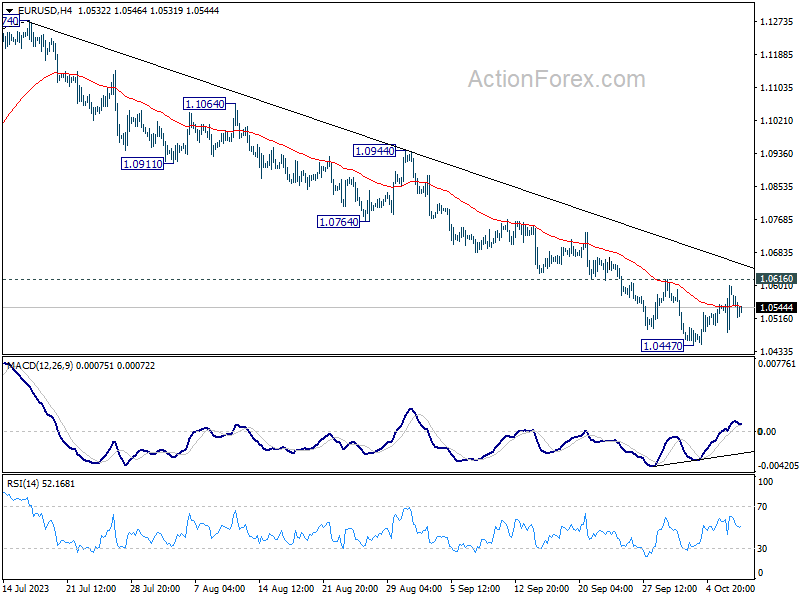

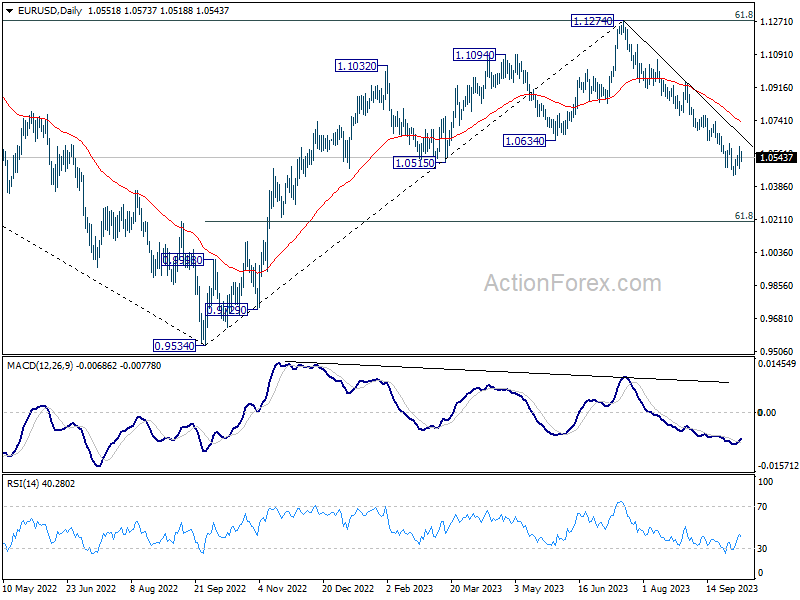

EUR/USD is staying in consolidation from 1.0447 and intraday bias remains neutral at this point. On the upside, firm break of 1.0616 resistance will confirm short term bottoming, and turn bias back to the upside for stronger rebound. Nevertheless, rejection by 1.0616 will retain near term bearishness. Break of 1.0447 will resume the fall from 1.1274 to 1.0199 fibonacci level next.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0730) holds, in case of rebound.

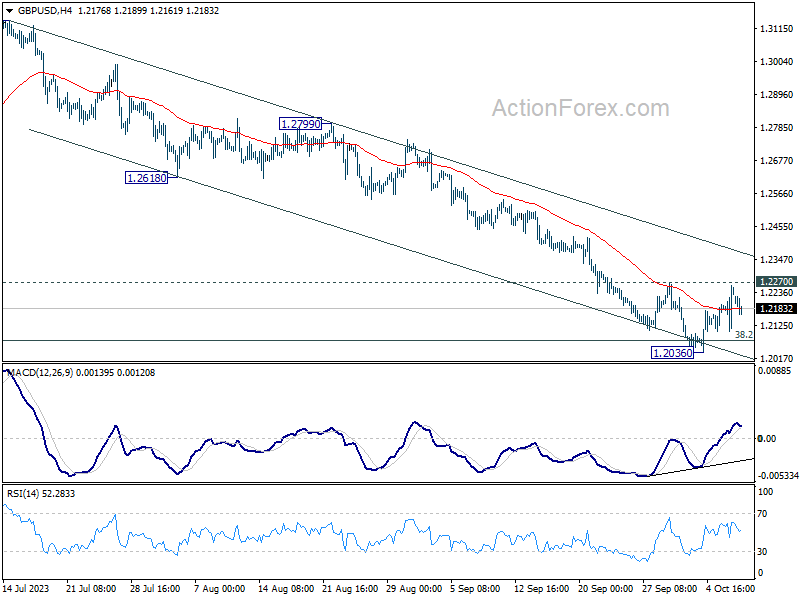

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2143; (P) 1.2202; (R1) 1.2298; More

Intraday bias in GBP/USD remains neutral as consolidation from 1.2036 is still extending. On the upside, firm break of 1.2270 resistance will confirm short term bottoming. Intraday bias will be back to the upside for stronger rebound. Nevertheless, rejection by 1.2270 will retain near term bearishness. Decisive break of 1.2075 fibonacci level would carry larger bearish implication and target 1.1801 support next.

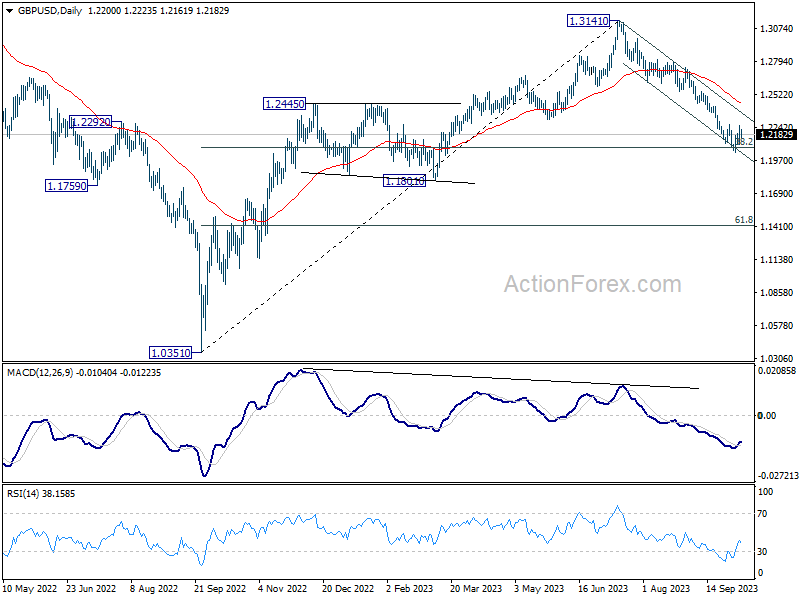

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2446) holds, in case of rebound.

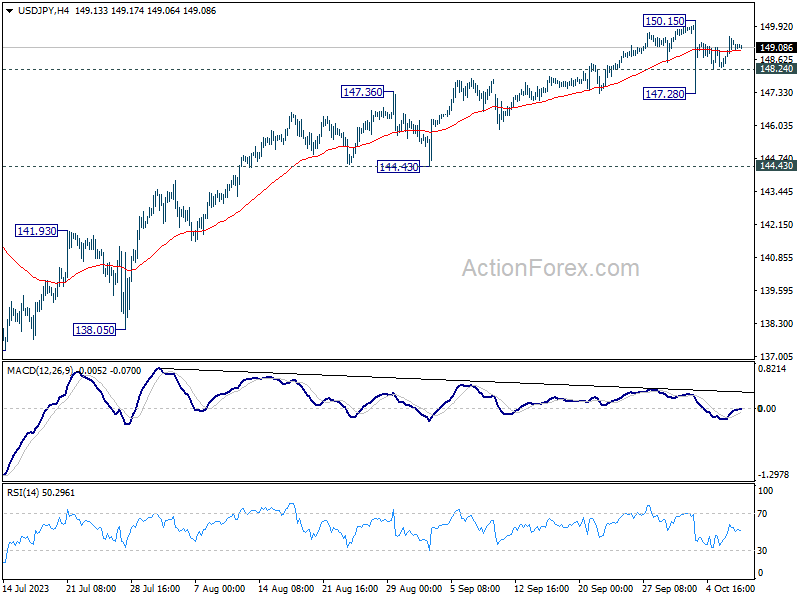

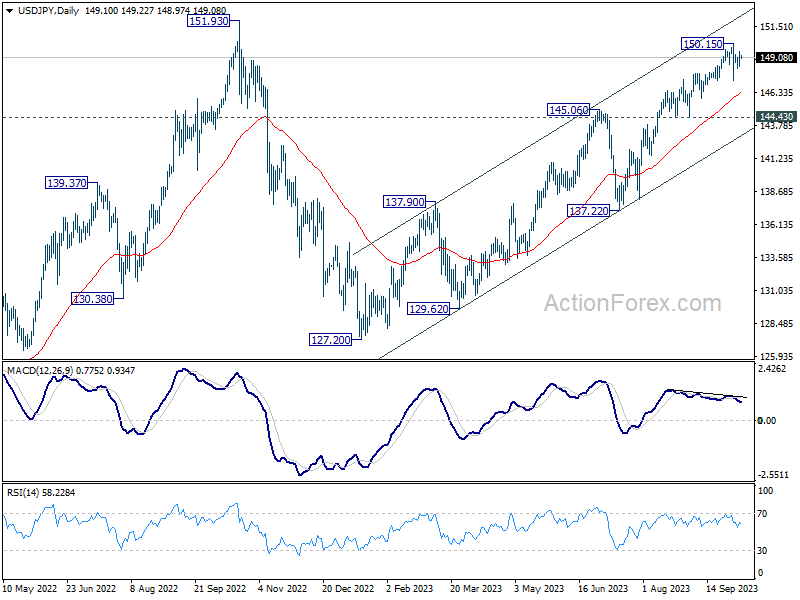

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.58; (P) 149.06; (R1) 149.76; More...

USD/JPY is extending the consolidation form 150.15 and intraday bias stays neutral for the moment. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

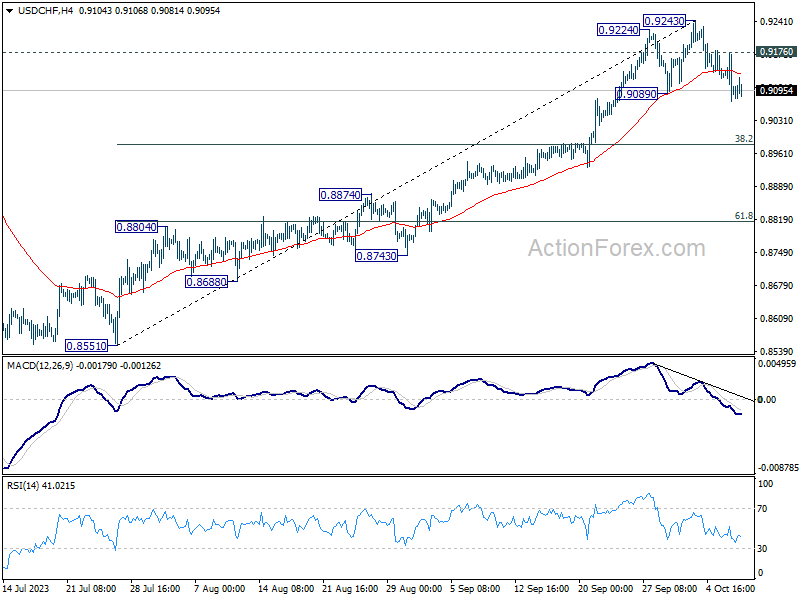

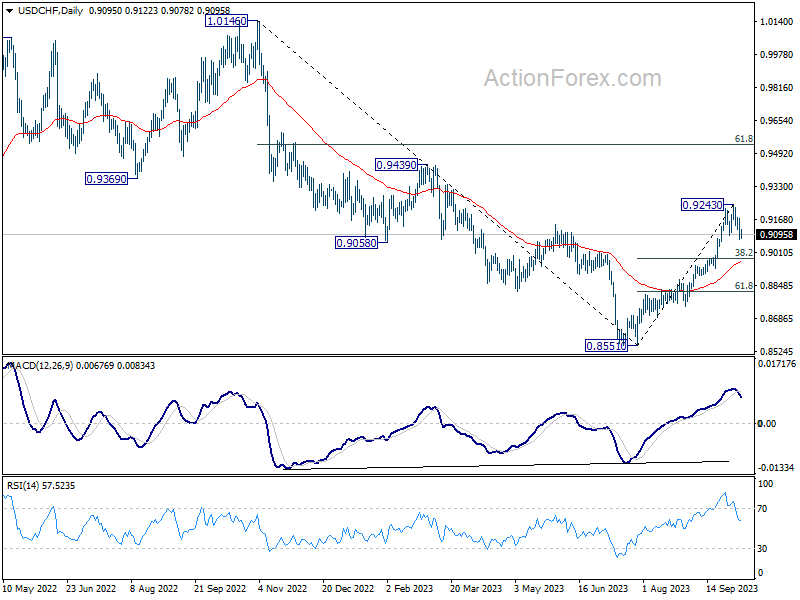

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9056; (P) 0.9116; (R1) 0.9159; More....

No change in USD/CHF's outlook as intraday bias stays mildly on the downside. Correction from 0.9243 would target 38.2% retracement of 0.8551 to 0.9243 at 0.8979. On the upside, though, above 0.9176 minor resistance will turn bias back to the upside for retesting 0.9243.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8967) holds, even in case of deep pullback.

Middle East Tensions Elevate Safe Havens, But Gains in Yen and Franc Restrained

The global financial markets are responding with caution to the rising tensions in the Middle East. However, this sentiment is tempered and contained, with significant shifts and trends yet to be firmly established. European stock markets are reflecting a subdued sentiment, with DAX and CAC registering modest declines, and FTSE remaining mostly flat.

The anticipated lower opening in US futures, while bond markets are on holiday, might offer more substantial market movements. However, if geopolitical tensions don't escalate further, focus will likely shift back to the economic calendar. Key events slated for this week include release of US inflation data, FOMC minutes, and UK's GDP figures.

In the currency markets, risk aversion is driving demand for safe-haven currencies. Notably, Yen and Swiss Franc have emerged as the day's top performers. However, their gains that can be characterized as limited for the time being.

Euro and Sterling are currently underperforming, partly driven by soft investor sentiment data for the former. Nonetheless, their downturn is not significantly steeper than that of Australian and New Zealand Dollars.

On the flip side, Canadian Dollar is showcasing strength, buoyed by the resilience in WTI oil prices, which have managed to sustain today's rebound. Amidst these movements, Dollar finds itself in a neutral territory, prolonging its consolidation phase from last week's peak.

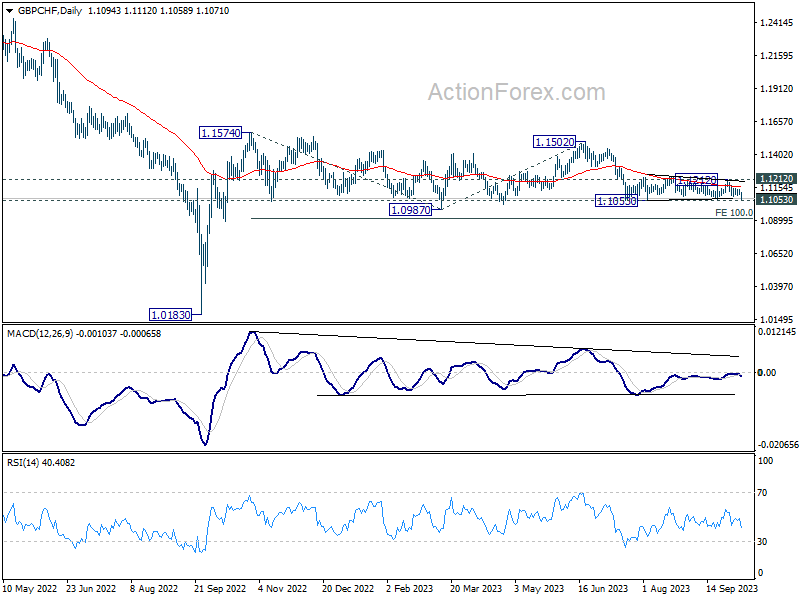

From a technical perspective, GBP/CHF is back eyeing 1.1053 support with today's decline. Decisive break there will confirm resumption of the fall from 1.1502. That would likely resume the whole decline from 1.1574 . Next target should be 100% projection of 1.1574 to 1.0987 from 1.1502 at 1.0915, even if the fall from 1.1574 is a corrective pattern. With UK GDP release on the horizon for Thursday, it remains to be seen if downside breakout will materialize before the crucial data point.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is down -0.77%. CAC is down -0.50%. Germany 10-year yield is down -0.0341 at 2.854. Earlier in Asia, Japan was on holiday, Hong Kong HSI rose 0.18% on half-day trading. China Shanghai SSE closed won -0.44%, back from week-long holiday. Singapore Strait Times lost -0.25%.

Eurozone Sentix fell to -21.9, current situation hits rock bottom in a year

Investor confidence in Eurozone appears to be staying on shaky ground, as evidenced by the dip in Sentix Investor Confidence from -21.5 to -21.9 for October. While this decline was milder than the anticipated drop to -24.0, it still casts a shadow on the economic climate of the region.

The more granular aspects of the report offer a mixed picture. Current Situation Index slipped from -22.0 to a low of -28.0, a trough not seen since November 2022. Conversely, Expectations Index, which forecasts sentiments for the coming six months, exhibited a rally, climbing from -21.0 to -16.8, marking its zenith since April.

Sentix noted, "The economic situation in the Eurozone remains difficult." While the uptick in Expectations Index could provide a glimmer of hope, Sentix tempers this optimism by clarifying that it "does not yet indicate a turnaround." Instead, it might simply imply a slowing down in the waning momentum.

Additionally, Sentix noted investors perceive ECB as somewhat hamstrung in its ability to intervene. The bank's typical proactive stance in assisting a faltering economy is "not yet discernible."

Shifting focus to Germany, the data presents a narrative akin to Eurozone. The Overall Investor Confidence experienced a minor lift, moving from -33.1 to -31.1. Yet, this was counterbalanced by Current Situation Index, which not only fell from -38.3 to -39.5 but also reached its nadir since July 2020. On a positive note, Expectations Index saw a boost, rising from -27.8 to -22.3.

ECB's de Guindos urges caution on oil prices amid enormous geopolitical uncertainties

ECB Vice-President Luis de Guindos highlighting the "enormous uncertainty" that geopolitical tensions are injecting into the financial markets and the broader economy, in light of the heightened conflicts between Israeli and Hamas forces in Gaza.

"The macroeconomic environment is subject to enormous uncertainty." He further stressed the heightened unpredictability by noting, "Nobody knows what is going to happen in the future," particularly in light of the recent events over the weekend.

De Guindos still anticipates a downturn in both headline and core inflation. However, he urged stakeholders to remain vigilant. His concerns stemmed mainly from "the evolution of oil prices, the depreciation of the euro and the evolution of unit labor costs".

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9056; (P) 0.9116; (R1) 0.9159; More....

No change in USD/CHF's outlook as intraday bias stays mildly on the downside. Correction from 0.9243 would target 38.2% retracement of 0.8551 to 0.9243 at 0.8979. On the upside, though, above 0.9176 minor resistance will turn bias back to the upside for retesting 0.9243.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8967) holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany Industrial Production M/M Aug | -0.20% | -0.10% | -0.80% | -0.60% |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Oct | -21.9 | -24 | -21.5 |

Mighty Dollar Turns to US Inflation Data and Fed Minutes

- Dollar stabilizes ahead of FOMC minutes and US inflation report

- Inflation expected to cool further - is the Fed done raising rates?

- Minutes due at 18:00 GMT Wednesday, inflation 12:30 GMT Thursday

Dollar sizzles

The US economy continues to display impressive resilience. Economic growth accelerated over the summer and is projected to have reached an annualized 4.9% in the third quarter according to the Atlanta Fed GDPNow model, as consumers continue to spend and the labor market remains in great shape.

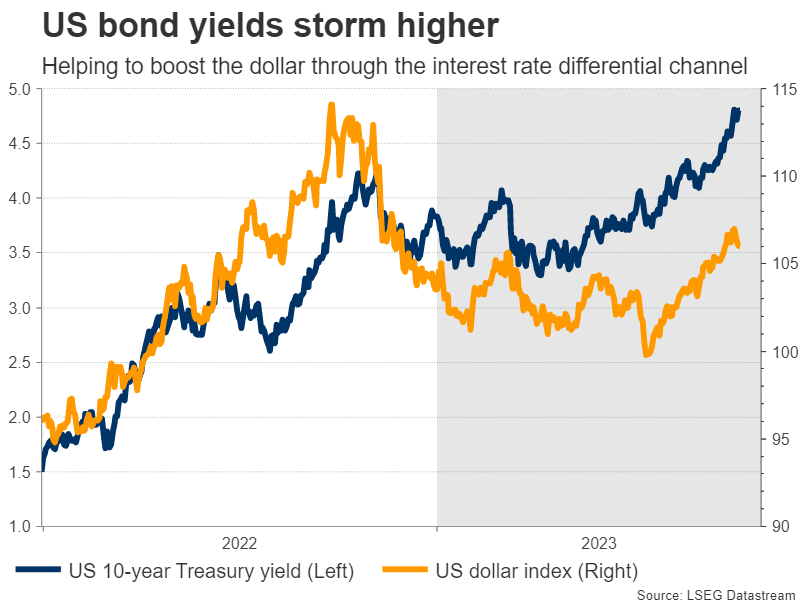

With the economy not slowing down, the Fed has adopted the view that interest rates will need to remain higher for a longer period of time to defeat inflation. This notion coupled with a sharp increase in debt issuance to fund budget deficits has pushed US bond yields to their highest levels since the financial crisis, turbocharging the US dollar.

Interest rate differentials have essentially widened in the dollar’s benefit, as US yields have risen much more aggressively than foreign ones. And with the Treasury set to continue flooding the markets with newly-issued bonds this quarter, this upside pressure will likely persist for some time.

Beyond all this, the dollar has also benefited from the worsening outlook for other currencies. The euro has been haunted by recession concerns, the British pound is grappling with a weaker labor market and fragile risk sentiment in the markets, while the yen has been devastated by the Bank of Japan’s refusal to raise interest rates.

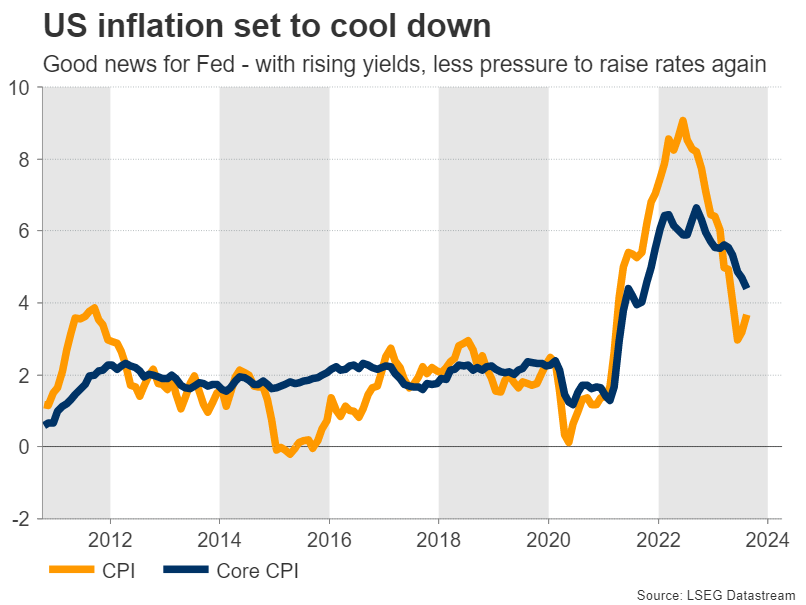

Inflation set to cool

Turning to the upcoming releases, inflation as measured by the CPI is anticipated to have lost steam on a yearly basis. The headline CPI rate is seen at 3.6% in September from 3.7% previously, while the core rate that excludes food and energy prices is expected to have declined to 4.1% from 4.3% previously.

Ahead of this dataset, the Fed will release the minutes of its September meeting, where the Committee refrained from raising interest rates but revised its implied rate path higher, fueling the ‘higher for longer’ narrative. Investors will dissect the minutes for more insights into this discussion.

The two main questions are whether the Fed will raise rates one final time this year and how long interest rates will remain at such high levels. Markets are still pricing in a 35% probability for the Fed to hike rates again by December.

However, that is highly unlikely, as the bond market has already done the heavy lifting for the Fed. The recent spike in long-dated US yields has the same effect as raising interest rates several times, so monetary policy has already been tightened lately. As such, there’s less pressure on the Fed to act again.

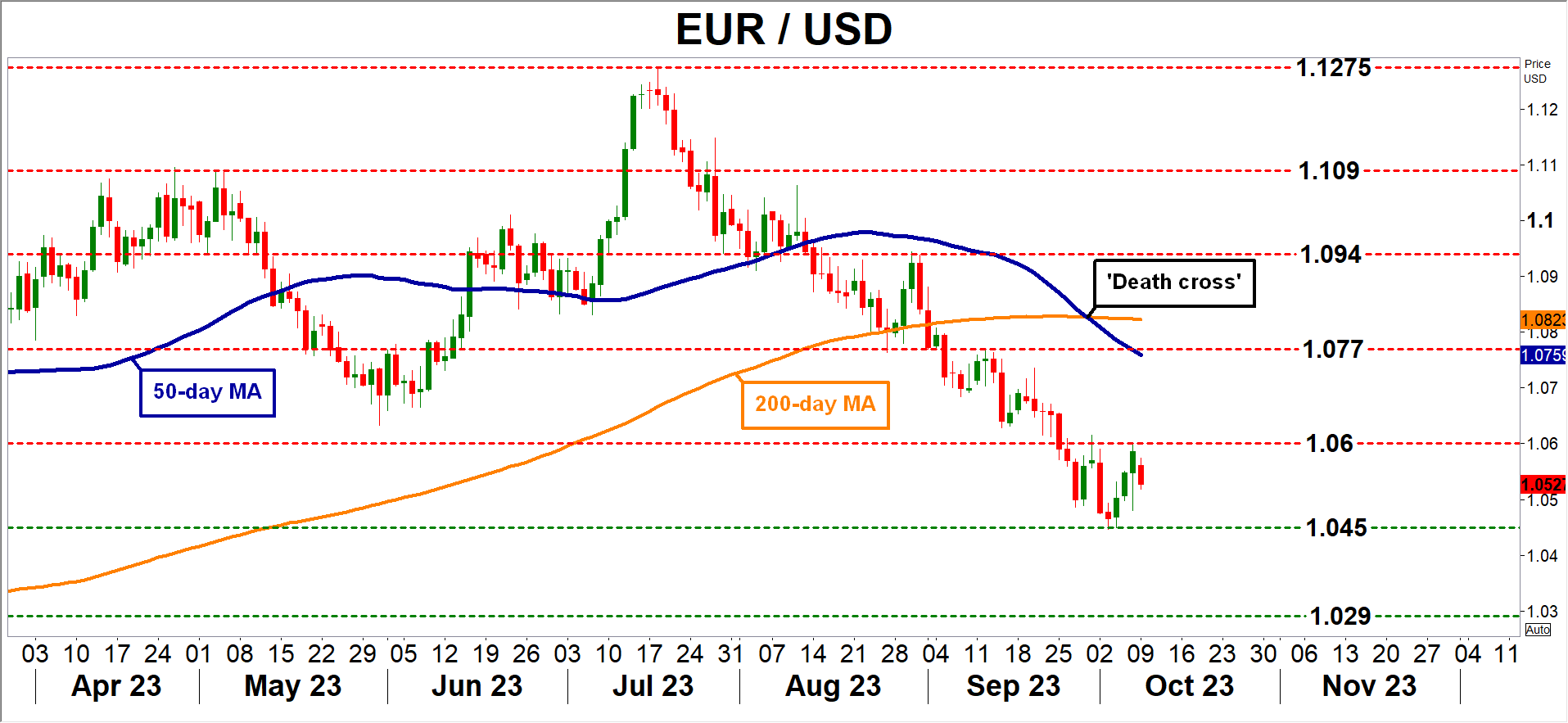

Dollar outlook and key levels

All told, the US dollar offers the ‘full package’ at this stage - the highest real rates among the major economies, the strongest economic growth, and safe haven qualities thanks to its reserve currency status. The US economy has been shielded by the government’s massive deficit spending, which has simultaneously safeguarded growth and pushed yields higher.

In contrast, there’s little to suggest the slowdown in Europe or China is approaching its conclusion. Leading indicators continue to paint a gloomy picture for both economies and stimulus measures have been scarce. Hence, the theme of American exceptionalism remains intact for now.

The charts tell the same story as a ‘death cross’ has formed in euro/dollar, with the 50-day moving average crossing below the 200-day one. That’s usually a negative sign. The most important level to watch on the downside is the recent low near 1.0450, while on the upside, any advances could stall around the 1.0600 region.