Sample Category Title

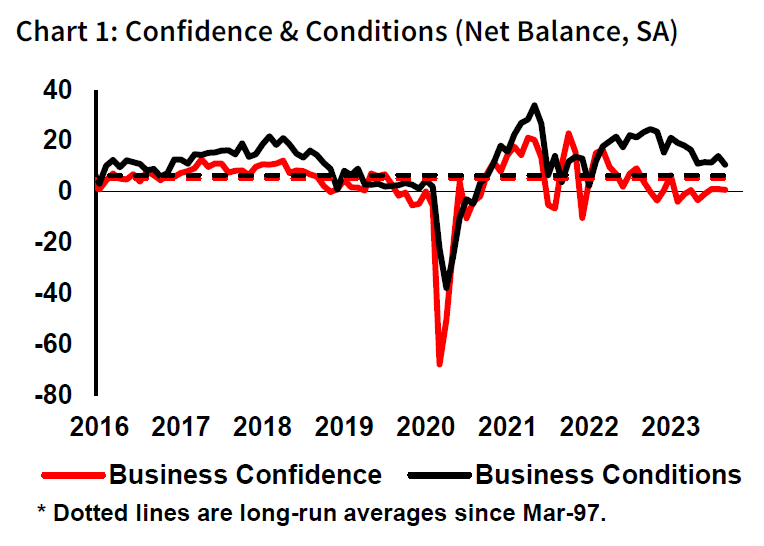

Australian NAB business confidence unchanged at 1, declining conditions and easing price pressures

Australia NAB Business Confidence for September remained stable at a level of 1. Meanwhile, a decline was observed in Business Conditions, which slid from 14 to 11. A deeper dive into the components reveals trading conditions receding from 19 to 16, profitability conditions from 14 to 8, and employment conditions registering a dip from 10 to 8.

Notably, growth in labor costs saw a deceleration, moving from a 3.2% quarterly rate down to 2.0%. Additionally, purchase costs experienced a slowdown from 2.9% to 1.8%. Both final product prices and retail prices exhibited moderated growth rates, with the former decelerating from 1.7% to 1.0% while the latter remained unchanged at 1.8%.

NAB Chief Economist Alan Oster remarked, "the economy has remained in reasonable shape through the middle of the year." He went on to note the +1 index points underscores that firms are somewhat ambivalent regarding their future prospects, with views split evenly regarding the outlook.

However, there was a silver lining in the inflation scenario. Oster highlighted that "the survey showed some positive signs for inflation with cost pressures and price growth easing in the month."

Even though the imminent Q3 CPI release is anticipated to reflect strong inflation for the quarter, Oster noted, "the September survey results suggest the momentum of some of the key cost pressures driving inflation may have started to step back in a welcome sign for the broader inflation outlook."

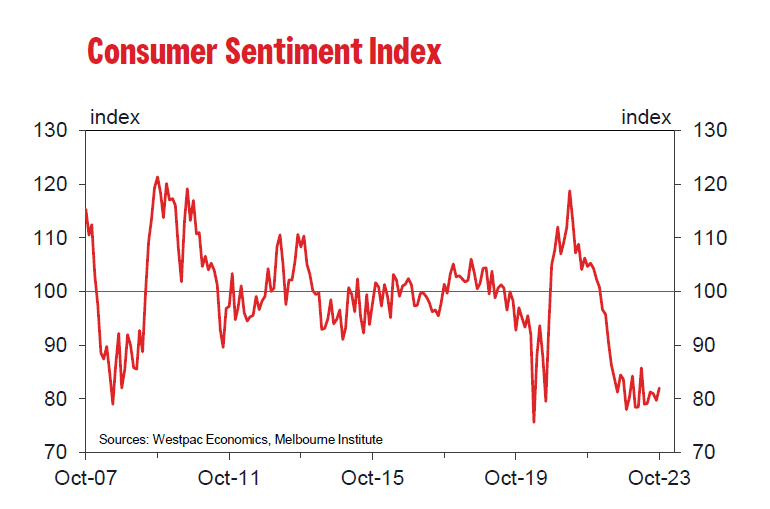

Australian consumer sentiment ticks up to 82, but interest rates concerns linger

Australia's Westpac Consumer Sentiment Index showed a positive move, climbing 2.9% from 79.7 to 82 in October. Despite the uptick, a score of 82 still paints a subdued picture, correlating with a decline in per capita spending.

One of the more pressing concerns for consumers remains the prospective upward movement in mortgage interest rates. The post-October RBA decision survey indicated that 63% of consumers anticipate mortgage interest rates to climb in the forthcoming year. This figure marks a substantial rise from 52.3% in September. N

Notably, however, these numbers don't match the heightened concerns recorded when RBA was in an active rate-hiking mode, where readings ranged between 70-80%. Meanwhile, optimism for a rate cut next year has dwindled; only 7% of consumers now hold that expectation, down from 15% the previous month.

The upcoming November 7 meeting of RBA is earmarked as a significant event, with a revised set of forecasts to accompany the Statement on Monetary Policy.

Westpac shared their viewpoint on the evolving situation: "While the RBA may need to revise its near-term forecasts for headline inflation up, on its own this will probably not be enough to trigger a further rate rise."

The September quarter CPI, slated for release on October 25, is now in sharp focus. Westpac added, "If, however, there are further surprises in the September quarter CPI, due October 25, the next few meetings could be a little more live than the one in October."

BoE’s Mann highlights concerns over extended inflation duration

BoE MPC Catherine Mann emphasized the significance of the duration of inflation in guiding her future policy decisions.

Mann pointedly remarked, "Going forward, a very important ingredient for my decision-making is the duration of inflation, and how long it is exceeding target."

The MPC member expressed concerns that prolonged inflation above the target could lead to a "drift" in medium-term expectations. Monetary policy "has to be more aggressive, because it has to address both a drift in expectations as well as the actual inflation above target," Mann further elaborated.

Mann also warned of the challenges that could arise if inflation remains persistently above the target. "If inflation gets embedded for longer above target, then getting it to target is going to require more policy action for longer and that I'd rather not have to do because people become backward looking," she said.

In the context of future economic shocks, Mann anticipates an "upward bias" in inflation, suggesting that a higher neutral rate of interest is "a very plausible outcome."

Fed’s Jefferson on the balance between rising yields and monetary policy

Fed Vice Chair Philip Jefferson shared in a speech overnight the insights onchallenges posed by rising real long-term Treasury yields. He pointed out the complexities faced by policymakers when determining the direction of monetary policy amidst such changes.

Jefferson stated, "In part, the upward movement in real yields may reflect investors' assessment that the underlying momentum of the economy is stronger than previously recognized and, as a result, a restrictive stance of monetary policy may be needed for longer than previously thought."

However, he was quick to add a caveat, underscoring the nuances associated with interpreting yield movements. Jefferson added, "But I am also mindful that increases in real yields can arise from changes in investor's attitudes toward risk and uncertainty."

Jefferson assured his approach would be comprehensive and adaptive. "I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy," he noted.

Vice Chair's will weight the "totality of incoming data in assessing the economic outlook and the risks surrounding the outlook".

Highlighting the delicate equilibrium that is to be maintained, Jefferson encapsulated the current scenario as a "sensitive period of risk management." Here, the dichotomy lies in "balance the risk of not having tightened enough, against the risk of policy being too restrictive."

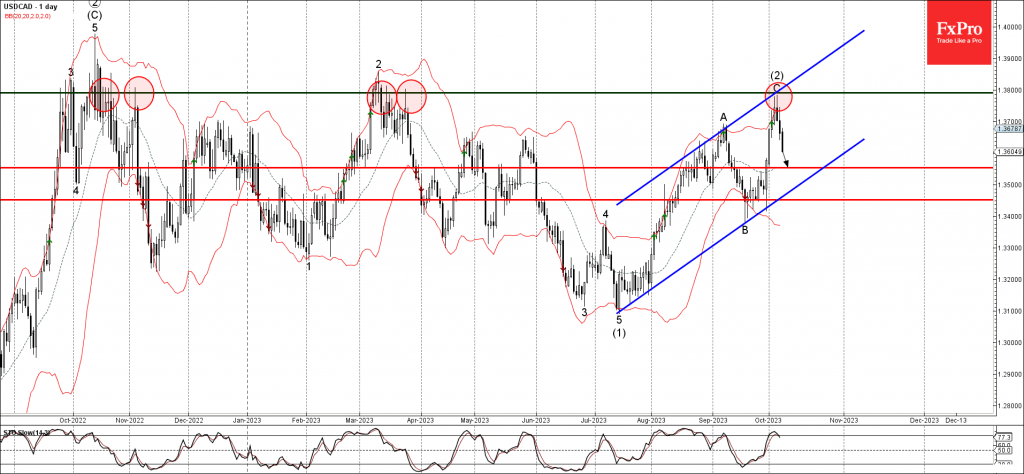

USDCAD Wave Analysis

- USDCAD reversed from resistance level 1.3800

- Likely to fall to support level 1.3555

USDCAD currency pair recently reversed down from the resistance level 1.3800 (which has been reversing the price from October of 2022), coinciding with the upper daily Bollinger Band and the resistance trendline of the daily up channel from July.

The downward reversal from the resistance level 1.3800 stopped the c-wave of the earlier intermediate ABC correction (3) from the start of July.

Given the strength of the resistance level 1.3800 and the still overbought daily Stochastic, USDCAD can be expected to fall further toward the next support level 1.3555.

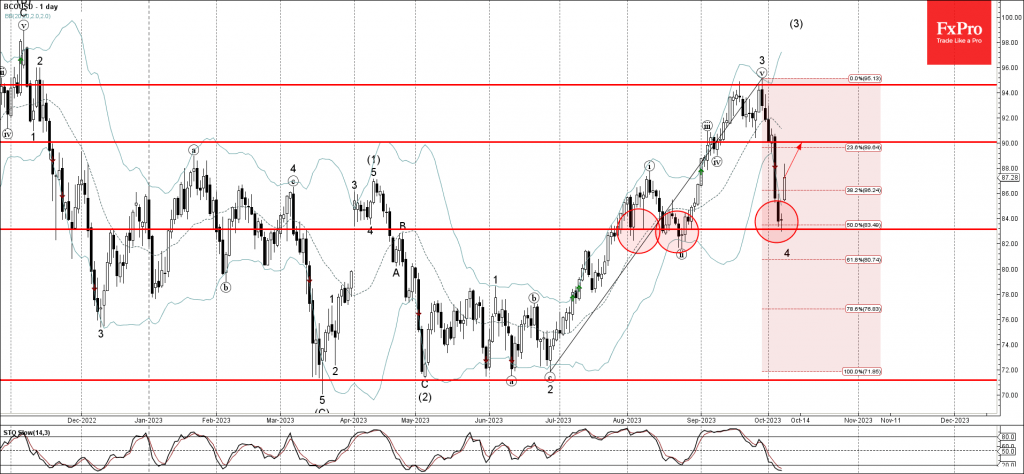

Brent Crude Oil Wave Analysis

- Brent crude oil reversed from support level 83.15

- Likely to rise to resistance level 90.00

Brent crude oil recently reversed up from the support level 83.15 (which has been repeatedly reversing the price from the start of August), coinciding with the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from June.

The upward reversal from the support level 83.15 is currently forming the daily candlesticks reversal pattern Morning Star Doji.

Given the still oversold daily Stochastic, Brent crude oil can be expected to rise further toward the next resistance level 90.00.

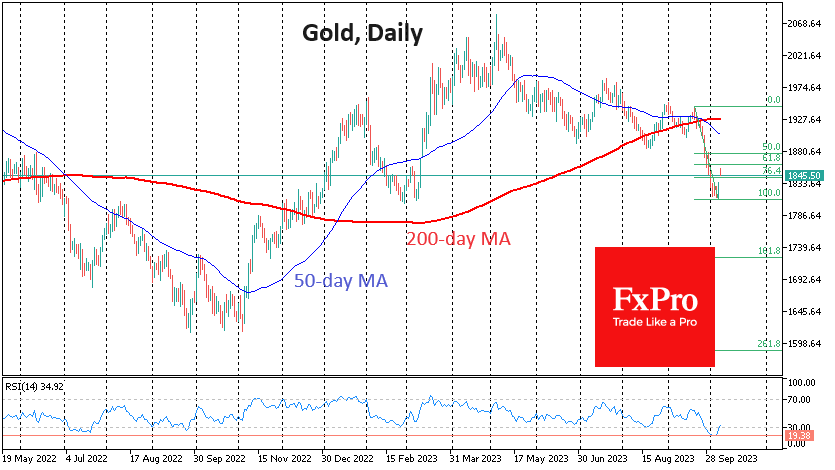

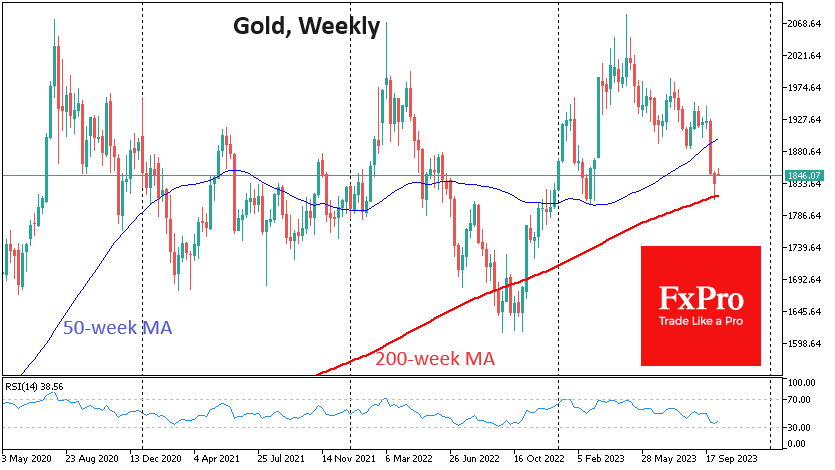

Gold Not Too Cold Right Now

Gold climbed close to $1855 per troy ounce in early trading on Monday and stabilised in a relatively narrow range of $1845-1853 during the European session. The rise from Friday’s lows of $1810 resulted from a combination of three factors. However, they all appear to be short-term and promise the evolution of an interesting situation.

Gold came into last Friday’s session having built up an impressive oversold condition, losing almost every day since the 20th, falling 7% to a low near $1810. This sell-off has taken the daily RSI to 19, an extremely oversold level last seen in July 2015. An asset is considered oversold when the RSI falls below 30, and a reading below 20 is a rare event that at least a short-term bounce has always followed.

Gold buying on Friday was supported by rising risk appetite in equity markets as tepid wage growth figures accompanied robust employment data. As a result, US bond yields fell on expectations that the Fed would avoid further policy tightening.

On Monday, gold opened with a gap higher on the back of clashes between Israel and Hamas. However, the latest move is more of a knee-jerk reaction to the news than a sustained, extended move. Still, gold bullion is hardly the quickest and easiest way to protect capital from war these days: transferring wealth into another currency or bank is much easier and more efficient.

We should, therefore, be prepared for the recent rally in gold to be reinforced by short-term profit-taking, which will only encourage the bears.

The classic Fibonacci retracement pattern suggests a potential upside to $1862, or 61.8% of the original downside amplitude. However, today’s top coincides with the rally we saw in gold in late February and early March. Very soon after, the market turned to a new round of declines.

The triumph of the bears was then prevented by the crisis in regional banks in the US, which led to a rush into gold and the major cryptocurrencies. The 50-week moving average was the technical support at the time. Now, the 200-week moving average is taking on the role of support.

Gold may make another attempt to break below $1810 in the coming days. We could see a quick fall to $1760 if the bears succeed.

At the same time, we cannot completely rule out the possibility that gold will start to look attractive to long-term buyers from these levels, having begun another gentle climb.

UK100 – Gives Up Earlier Gains in Risk-Averse Trade

- UK100 outperforming buoyed by energy stocks

- Risk aversion weighing on broader markets

- Sideways trend remains in tact

We’re seeing a little more risk-aversion in the markets at the start of the week which is understandable considering the unfortunate events in Israel over the weekend.

The surprise attack by Hamas has fueled concerns about further instability in the Middle East which could in turn disrupt oil flows at a time when the market is already extremely tight and prices are high.

It’s quite natural in these circumstances for investors to take a risk-averse approach while they gain a better understanding of what the knock-on effects will be – for example with the WSJ claiming that the attack was aided by Iran – and what that will ultimately mean for the global economy.

It comes at a time when there is already enormous uncertainty over the global economy going into 2024 with most central banks likely done with monetary tightening but some still warning of more to come.

If economies aren’t already in or heading for recession, further hikes could tip them over the edge, and that has been weighing heavily on stock markets. We’ll hear from a wide array of central bankers over the course of this week which will be particularly interesting in light of Friday’s jobs report and ahead of this week’s US CPI data.

FTSE still stuck in sideways pattern

The UK100 is outperforming its counterparts in Europe this morning, with energy stocks naturally performing well amid higher oil and gas prices.

UK100 Daily

Source – OANDA on Trading View

That said, it’s given up earlier gains to trade relatively flat on the day. From a technical standpoint, it found support again last week around the ascending trendline it temporarily traded below in August, with 7,400 also acting as a barrier to the downside.

But there’s still no clear trend forming – up or down – with the index still seemingly trapped in a sideways pattern, largely over the last five months between 7,400 and 7,700.

Fed’s Logan suggests elevated term premiums might ease pressure on tigthening

Dallas Fed President Lorie Logan pointed out the role of higher term premiums, noting their impact on term interest rates. "Higher term premiums result in higher term interest rates for the same setting of the fed funds rate, all else equal".

Logan elaborated on this delicate interplay, stating, "If long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed funds rate."

Further expanding on this, Logan remarked, "Thus, if term premiums rise, they could do some of the work of cooling the economy for us, leaving less need for additional monetary policy tightening."

This suggests a potential offsetting force; should term premiums rise, the economy could experience a natural cooling, thereby alleviating some of the pressure on Fed to intervene.

However, Logan also emphasized the importance of understanding the root causes behind shifts in long-term interest rates. "To the extent that strength in the economy is behind the increase in long-term interest rates, the FOMC may need to do more."

Inflation, as has been the case for many months, remains a focal point of concern. Logan made it abundantly clear that inflation hovering above comfort levels is a significant risk. "Inflation remains too high, the labor market is still very strong, and output, spending, and job growth are beating expectations," she acknowledged.

High inflation, according to Logan, is the predominant risk that requires meticulous attention. "We cannot allow it to become entrenched or reignite," she warned.

Logan's remarks also encapsulated a vigilant and adaptive approach to monetary policy. "I will be carefully evaluating both economic and financial developments to assess the extent of additional policy firming that may be appropriate to deliver on the FOMC's mandate," she affirmed.