Sample Category Title

Down Under Central Bank Low Down

Summary

- At their respective monetary policy meetings this week, central banks in Australia and New Zealand remained relatively comfortably on hold.The Reserve Bank of Australia (RBA) held its Cash Rate at 4.10%, while the Reserve Bank of New Zealand (RBNZ) held its Official Cash Rate at 5.50%.

- For Australia, the RBA said that the economy is experiencing below-trend growth and that inflation is still expected to return to the 2-3 percent target range over its forecast period. While the RBA maintains a mild tightening bias, so long as growth stays sluggish and wage and price inflation keep trending in a favorable direction, we still think the current 4.10% policy rate will prove to be the peak for this cycle.

- The RBNZ said interest rates are constraining economic activity and reducing inflationary pressure. The central bank gave no clear signal of further tightening, but did hint that interest rates might have to remain at an elevated level for a more sustained period of time.

- Against a backdrop of overall resilient U.S. activity and higher U.S. yields, we view an on-hold RBA and RBNZ as consistent with some further Australian and New Zealand dollar downside in the months ahead. We target a low for AUD/USD around $0.6100, and a low for NZD/USD around $0.5700, by end Q1-2024.

Reserve Bank of Australia Still Watching, Still Waiting

The Reserve Bank of Australia (RBA) held its Cash rate at 4.10% at this week's monetary policy announcement, an outcome that was widely expected. Notably, the RBA made very few changes in its accompanying statement which, in our view, suggests the central bank will remain on hold for the foreseeable future. Among the salient points from the RBA's announcement, the central bank said:

- Inflation is too high and will remain so for some time yet.

- Higher interest rates are helping to establish a more sustainable balance between supply and demand in the economy, and holding rates steady provides further time to assess the impact of past monetary tightening.

- Australian growth was a little stronger than expected in the first half of the year, but the economy is still experiencing below-trend growth which is expected to continue for a while.

Recent data are consistent with inflation returning to the 2-3 percent target range over its forecast period with output and employment continuing to grow. - Significant uncertainties around the outlook include the persistence of services inflation, an uncertain outlook for Australian household consumption, and challenges for the Chinese economy, including the real estate sector.

In terms of future guidance, the RBA said "some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks. In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labor market."

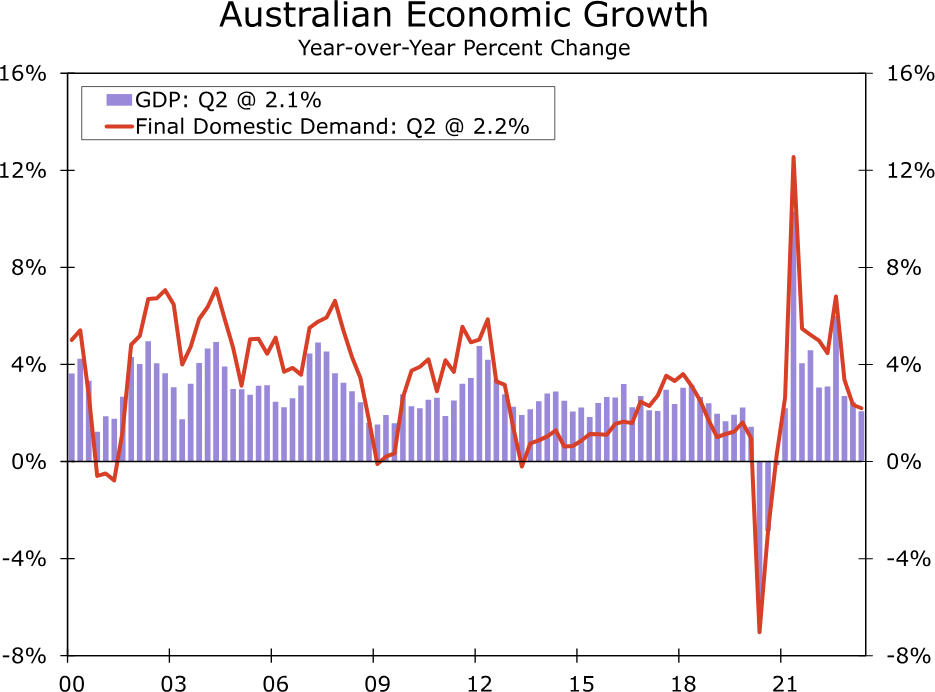

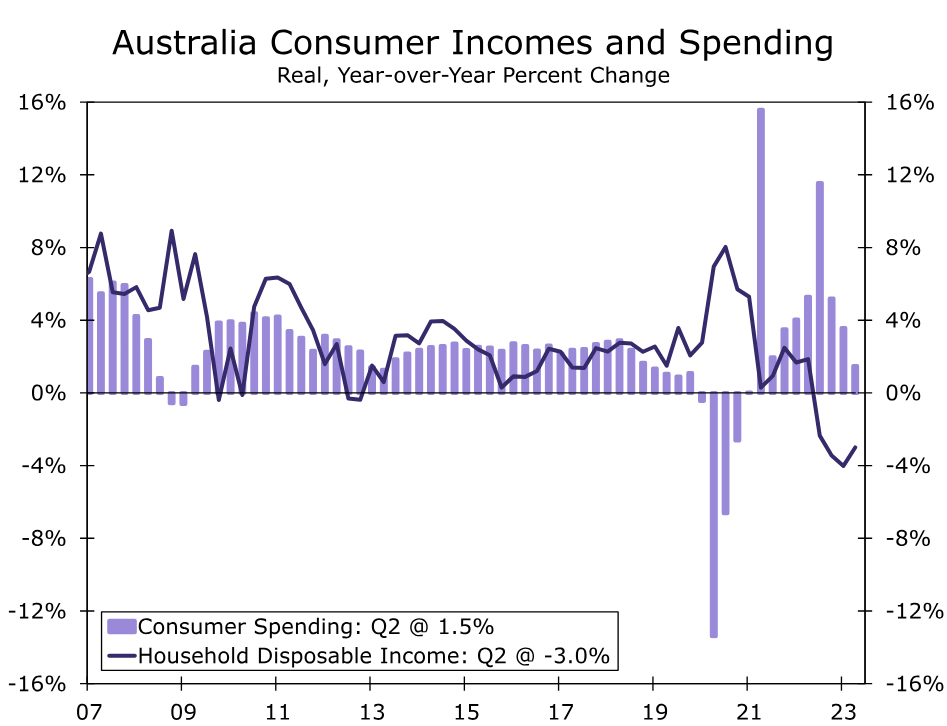

However, while the RBA maintained a mild tightening bias, at the current juncture we do not forecast any further rate hikes and believe the current policy rate of 4.10% will be the peak for this cycle. With respect to economic growth, recent indicators appear consistent with ongoing below-trend growth. Australian GDP grew just 0.4% quarter-over-quarter in both Q1 and Q2 of this year. To be sure, growth in final domestic demand was somewhat stronger at 0.7% per quarter. Over the past year, however, both overall GDP and final domestic demand have grown by just over 2%, which is subdued by historical standards. Notwithstanding a jump in August employment (driven largely by part-time jobs) and a rise in the September manufacturing and services PMIs, we still see reasons to expect slower growth in the Australian economy during the second half of this year. Household incomes have not kept up with the pace of inflation, meaning that the trend in real household disposable incomes has turned negative, a factor that should continue to weigh on consumer spending. In addition, China's ongoing economic challenges could be a headwind for Australia's economy.

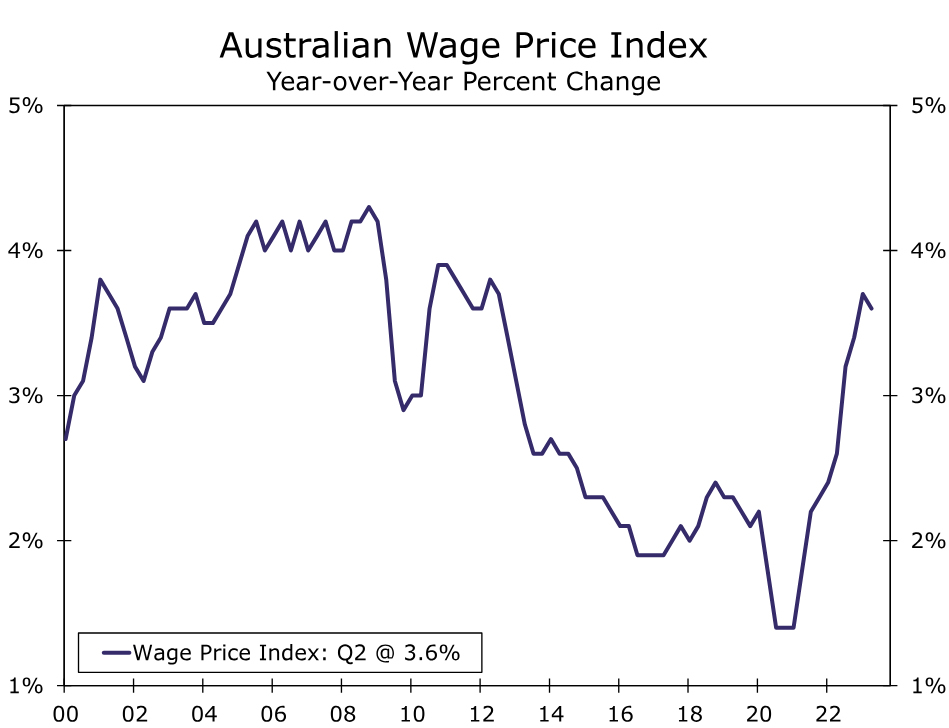

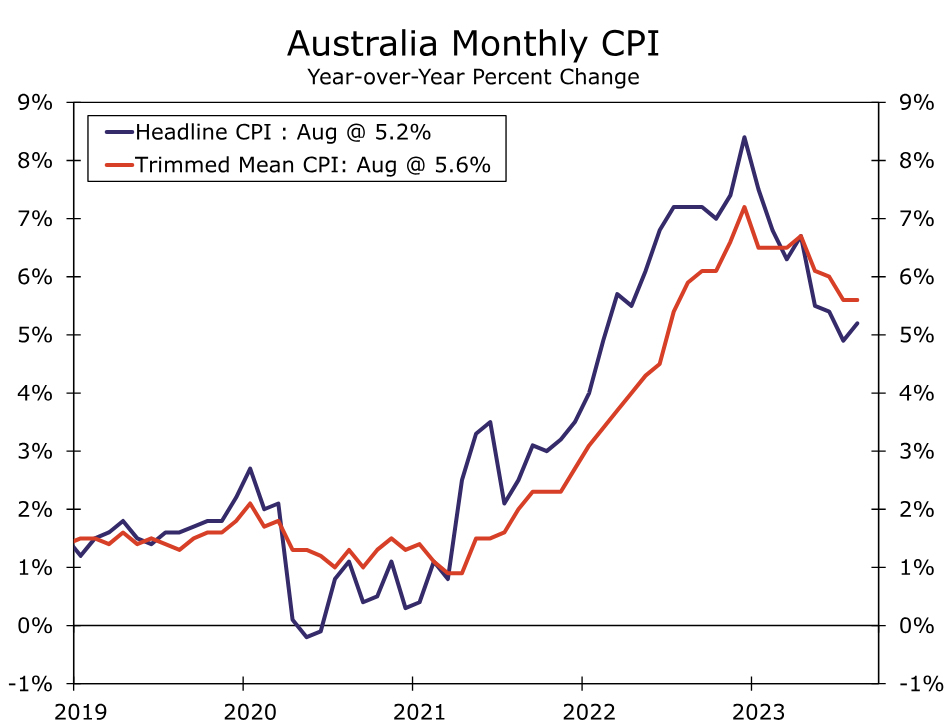

In addition to subdued economic growth, Australian wage and price inflation has started trending in a more favorable direction, albeit gradually. Even with a still relatively tight labor market, there are very early hints of an easing in wage pressures, and the Wage Price Index slowed slightly to 3.6% year-over-year in Q2. The more timely data available on price trends shows a more perceptible slowing of inflation. The August headline CPI rose 5.2% year-over-year, down from a peak of 8.4% last December. Underlying measures of inflation have also slowed, including the trimmed mean CPI, which rose 5.6% in August. So long as Australia economic growth remains subpar and inflation continues to trend in a more favorable direction, we believe the Reserve Bank of Australia will be comfortable remaining on hold. In contrast, there appears to be more debate and discussion about the possibility of a further Federal Reserve rate increase, as well as how long the Fed's policy rate will remain at elevated levels, a factor that has contributed to rising U.S. bond yields. Considering the resilience of the U.S. economy to date, we believe this backdrop remains consistent with further U.S. dollar strength, including versus the Australian currency. For the months ahead we remain biased toward Australian dollar downside, and forecast a low for the Australian currency around $0.6100 by end Q1-2024.

Reserve Bank of New Zealand Joins The Higher For Longer Club

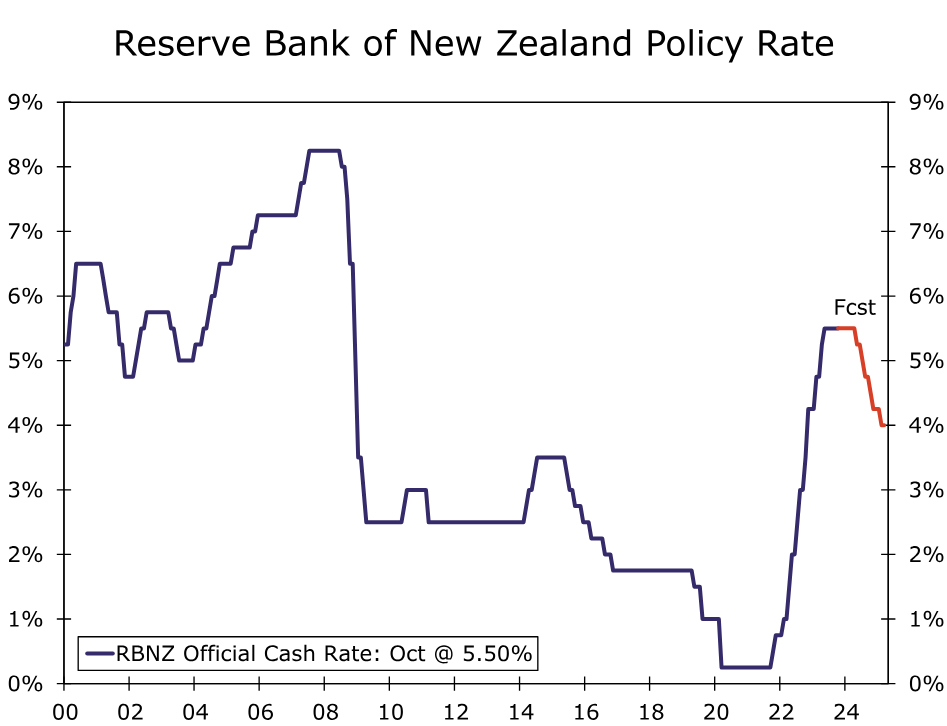

The Reserve Bank of New Zealand (RBNZ) held its Official Cash Rate at 5.50% at this week's announcement, an outcome that was also widely expected. While the central bank reiterated its determination to return inflation towards target, its accompanying comments were not as hawkish as might have been anticipated, especially in the context of rising expectation for further interest rate hikes at upcoming meetings that had emerged in recent weeks. Among the RBNZ's main points:

- Higher interest rates are constraining economic activity and reducing inflationary pressure as required.

- While Q2 GDP growth was stronger than expected, demand growth continues to ease overall.

- A prolonged period of subdued activity is required to reduce inflation pressure.

- The Official Cash Rate needs to stay at a restrictive level to ensure that inflation returns to target.

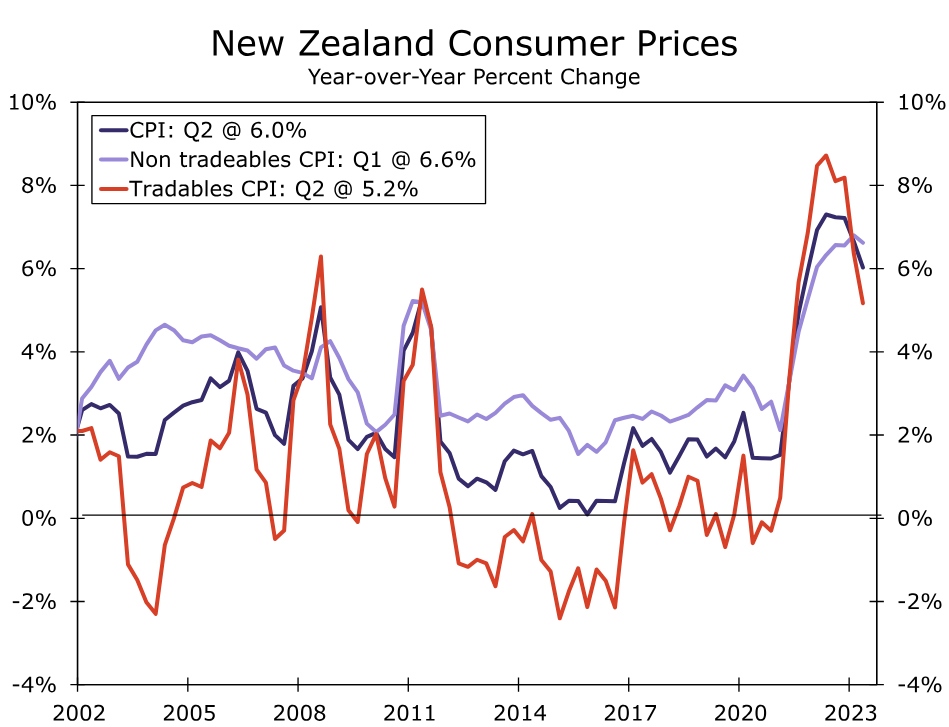

Of particular note, the summary record of the meeting noted that policymakers "agreed that interest rates may need to remain at a restrictive level for a more sustained period of time, to ensure annual consumer price inflation returns to the 1 to 3% target range and to support maximum sustainable employment." The desire to keep interest rates at current levels for an extended period is perhaps not surprising given that domestically-oriented non-tradeables inflation is still running at an elevated pace for the time being.

Overall, there was no clear indication of further tightening from the RBNZ, and our view remains that the policy rate peak for the current cycle has already been reached at 5.50%. However, it also appears that interest rates could remain at an elevated level for a longer period of time, suggesting the risk is that RBNZ rate cuts could begin later than the Q2-2024 easing we currently forecast. Against a backdrop of overall resilient U.S. activity trends and higher U.S. yields, that suggests some further downside for the NZ dollar, although the RBNZ's "higher for longer" mantra might limit the extent of the NZ currency's decline. We target a low for the New Zealand dollar around $0.5700 by end Q1-2024.

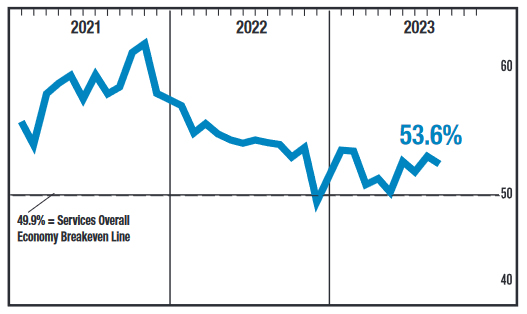

ISM Index Shows Services Sector Expanded in September

The ISM Services PMI fell to 53.6 in September from 54.5 in August, roughly in line with the 53.5 print consensus was expecting. This is the ninth consecutive month of expansion for the services sector.

The business activity sub-index rose 1.5 percentage points (pp) to 58.8 in September.

The new orders index sank 5.7 pp to 51.8, the softest print since December 2022.

The prices paid component was unchanged at 58.9. This ends two consecutive months of increases and keeps the index below the values it reached between July 2020 and April 2023.

Supplier delivery times registered 50.4, up from 48.5 in August, while the backlog of orders index retraced some of last month's losses, gaining 6.8 points to 48.6.

The employment sub-component fell 1.3 pp to 53.4.

Thirteen out of 18 industries expanded in September, the same number as in August.

Key Implications

The ISM services index gave back some of its August gains, but still remains above the soft patch from this past spring. However, signs are pointing to increasing headwinds for the sector. New orders growth continues to trend lower, while order backlogs have contracted in six of the past seven months.

For policymakers concerned about inflationary pass through, the silver lining in the report is although prices paid growth is still running above the pre-pandemic pace, it is significantly slower than during the inflationary burst over the past two years. The developments in this report support the notion that growth is set to slow through the rest of the year and should take some pressure off prices.

EUR/USD: Dollar Follows Bond Market and Hits Ludicrous Speed

- ADP report shows job weakness occurred in September

- ISM Services report shows largest part of economy remains resilient

- Yields remain near session lows

Wall Street is waking up to more FX and bond market chaos. Overnight, the 30-year Treasury yield surged to 5%, the highest level since 2007. With hedge funds aggressively riding this bond market selloff, Treasury yields blew right by ‘ridiculous’ speed and entered ‘ludicrous speed’.

Heading into the NY open, the 30-year Treasury yield has reversed course and is now trading around 4.879%. The resilience of the US economy and lack of buyers in the bond market means market swings will remain violent, especially once the DC drama intensifies. The dollar remains overbought and the bullish trend could remain intact as the current swings continue to mirror what is happening in the Treasury markets.

US stocks are higher after the bond market selloff cooled off and following softer private payrolls data. Wall Street is looking for any signs that the labor market is cooling and a big miss with the ADP report was somewhat embraced. Most however are ignoring the private payrolls release since ADP has yet to prove to be a reliable indicator as to what will happen with NFP.

The dollar pared losses and stocks held onto gains after the ISM services index showed the service sector remains strong. Service employment still looks good and service inflation could be sticky.

Ousted

The removal of US House speaker McCarthy surprised many DC insiders. Far-right Republicans voted alongside Democrats delivering a historic ouster of a speaker. The republican party is in disorder as they just tentatively lost control of the one chamber of one branch of government. The House can’t pass anything until they can agree upon a new speaker. Government shutdown odds are going up as the speaker is one of the most important roles for the upcoming debt ceiling and spending cap negotiations. In addition to being third in line to the presidency, the speaker decides which bills are brought to the floor and sets the legislative agenda.

Possible successors include:

Republican Patrick McHenry was named temporary speaker under House rules. The other Republican favorites include Steve Scalise, Tom Emmer, and Tom Cole.

Given the House speaker uncertainty will stretch out over the next couple of weeks, this is going to be a major obstacle that will make it harder in avoiding a government shutdown come mid-November.

ADP

The private sector added only 89,000 jobs in September, much lower than the 150,000 consensus estimate. The ADP report also noted that pay growth slowed for a 12th straight month as job stayers saw a 5.9% y/y pay increase. Pay gains for job changers softened from 9.7% to 9.0%. ADP’s chief economist said, “We are seeing a steepening decline in jobs this month.” Small and medium size businesses posted job gains while large establishments lost 83,000 jobs.

The US labor market is slowing, but this will need to be confirmed with Friday’s NFP report.

Sunset Market Commentary

Markets:

Yesterday’s sudden drop in USD/JPY remained talk of town. The pair breached last year’s intervention-threshold (150) following stronger US JOLTS job openings before suddenly sinking to 147.50. While top officials declined to say if they had intervened, Finance Minister Suzuki did tell media that they are watching FX with a high sense of urgency, that excessive FX moves are undesirable and that it is important that currencies move stably. In our humble opinion, we find that yesterday’s move had intervention written all over it. If it weren’t for the bond correction we are seeing today, USD/JPY (148.85 currently) would already be again in the dire position it was in yesterday. Without real policy shift by the BoJ, JPY won’t find a proper support despite trading at multidecade lows.

Core bond yields hitting some high profile levels (eg Germany 10-yr 3%, US 30-yr 5%) took the sting out of the post-FOMC core bond sell-off today. There were no specific drivers that caused the turnaround just as the past couple of sessions lacked strong evidence to the significant weakness. It did say a lot about underlying bearish core bond momentum though inspired by higher real rates. US yields today lose around 6 bps across the curve. The eco calendar contained September ADP employment change which gave evidence that the labour market is turning more into balance from extreme scarcity. The net job creation of 89k disappointed compared to consensus (150k). It was the lowest monthly figure since the positive streak of job gains started back in February 2021. Leisure and hospitality (+92k) drove the September gain, offsetting job losses at professional and business services (-32k), manufacturing (-13k) and trade and transportation (-12k). The bulk of the job losses (-85k) came at large enterprises. ADP added that workers who stayed in their job saw a 5.9% Y/Y median pay increase which was the smallest in two years. It coincides with a pick-up in the labour force participation rate (62.8% last month; highest since March 2020 and near pre-pandemic (2014-2019) levels). The US September services ISM was bang in line with consensus (53.6).

German yields today lose up to 4.2 bps at the very long end of the curve with the front end trading flat. ECB president Lagarde stuck with the view that the ECB will ensure that interest rates will be set at sufficiently restrictive levels for as long as necessary. The dollar ceded some ground with EUR/USD changing hands at 1.0516 from an open at 1.0467. European stock markets rebound 0.50% with key US indices opening with modest gains (S&P 500+0.35%)

News & Views:

The Italian Statistical of Office (Istat) published the Q2 non-financial general government account. The net government deficit for H1 2023 was 8.3% of GDP, only marginally lower from 2022 (8.4%). The primary balance was also little changed at -4.4% from -4.3%. Both YTD revenues and expenses as a percentage of GDP eased to respectively 44.2% and 52.5% (from 45% and 53.4% last year). Interest rate expenses at €38.23bn even were slightly lower than in H1 2022 (€38.91bn). The Italian government last week raised its 2023 deficit target to 5.3% of GDP from 4.5%. The 2024 expected deficit was increased from 3.7% to 4.3%. The 2022 deficit was 8%. Other data showed that gross disposable income of households fell by 0.1% over the previous quarter, while their final consumption expenditure grew by 0.2%. Households’ saving rate was 6.3%, 0.4 percentage points lower than in the first quarter of 2023. A combination of the deterioration in the Italian budget and higher global (real) yields pushed the 10-yr yield spread between Italy and Germany close to 200 bps compared to a YTD low of 156 bps mid-June.

Hungarian retails sales were 7.1% Y/Y lower in August (from -7.6% in July and vs -5.7% Y/Y consensus). Sales decreased by 0.5% M/M. Sales volumes for the January–August 2023 period were 9.6% lower than in the corresponding period of the previous year. Domestic demand is an important parameter both for monetary and fiscal policy. Next to lower commodity prices and government measures to strengthen market competition, the MNB sees subdued domestic demand as an important factor contributing the expected further decline in inflation that should allow the bank to ease monetary policy further. For the government, tax on consumption (VAT) is an important source of revenues. The government yesterday raised its 2023 budget deficit target to 5.2% of GDP from 3.9% which was said to be due to increased spending on pensions, energy subsidies and family subsidies, but lower than expected revenues due to poor domestic demand probably were also in play.

US ISM services falls to 53.6, corresponds to 1.3% annualized GDP growth

US ISM Services PMI fell from 54.5 to 53.6 in September, matched expectations. Looking at some details, business activity/production rose from 57.3 to 58.8. New orders dropped sharply from 57.5 to 51.8. Employment dropped from 54.7 to 53.4. Prices was unchanged at 58.9.

ISM said: "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for September (53.6 percent) corresponds to a 1.3-percent increase in real gross domestic product (GDP) on an annualized basis."

Platinum (PL) Correction Remains In Progress

Platinum (PL) is still correcting cycle from 9.1.2022 low before the rally resumes. We also present an alternate view if the pivot at September 2022 low (796.8) fails. If it breaks below 796.8, it suggests a bigger correction against March 2020 low. In the higher time frame, the metal is in a bullish grand super cycle move higher against March 2020 low.

Platinum (PL) Monthly Elliott Wave Chart

Monthly Elliott Wave Chart of Platinum above shows that the metal has ended wave ((II)) at 562 on January 2020 low in 3 swing. Up from there, it ended wave (I) at 1348.2 and wave (II) pullback is proposed complete at 796.8. While above 796.8, the metal can see further upside. If it breaks below 796.8, then the metal is doing a double correction in wave (II) and opens further downside to reach 610 area before support is seen.

Platinum (PL) Daily Elliott Wave Chart

Daily Elliott Wave Chart on Platinum above shows that the metal is pulling back in wave ((2)) to correct rally from 9.1.2022 low (796.8). Pullback is unfolding in the form of a double three structure. As far as pivot at 801.9 stays intact, expect the metal to extend higher.

Platinum (PL) Elliott Wave Video

https://www.youtube.com/watch?v=ESoxwv54jf4

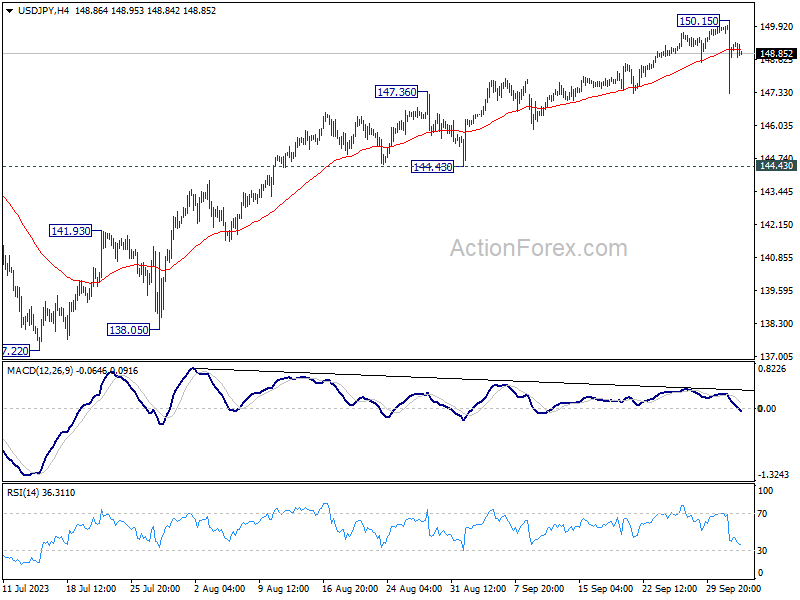

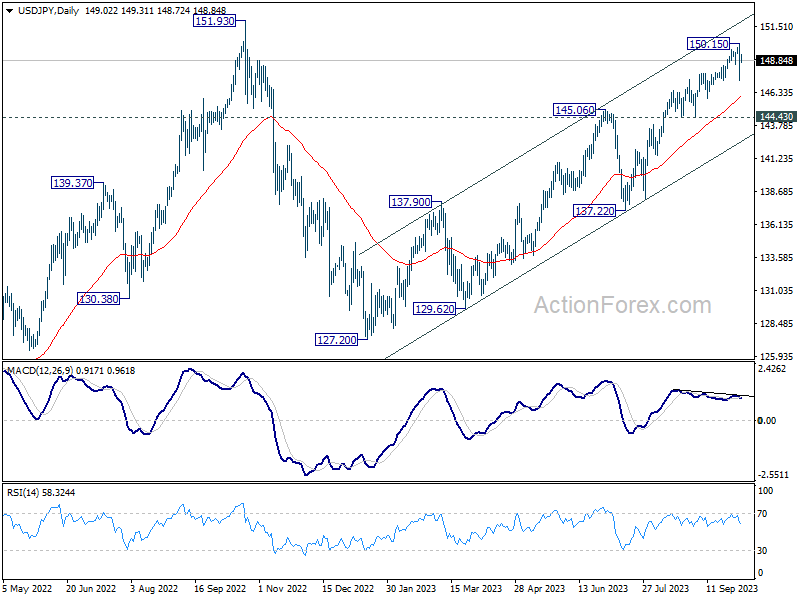

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.21; (P) 149.18; (R1) 150.03; More...

Intraday bias in USD/JPY stays neutral first, and more consolidations could be seen below 150.15. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

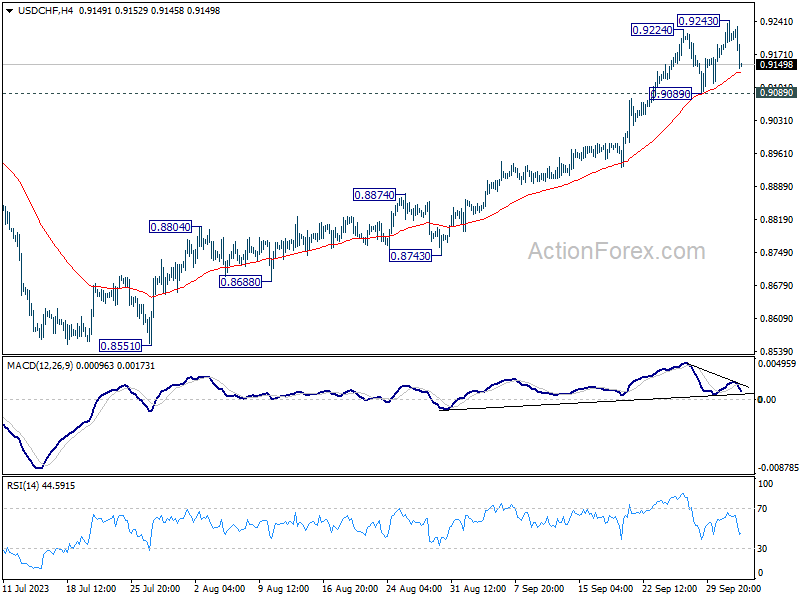

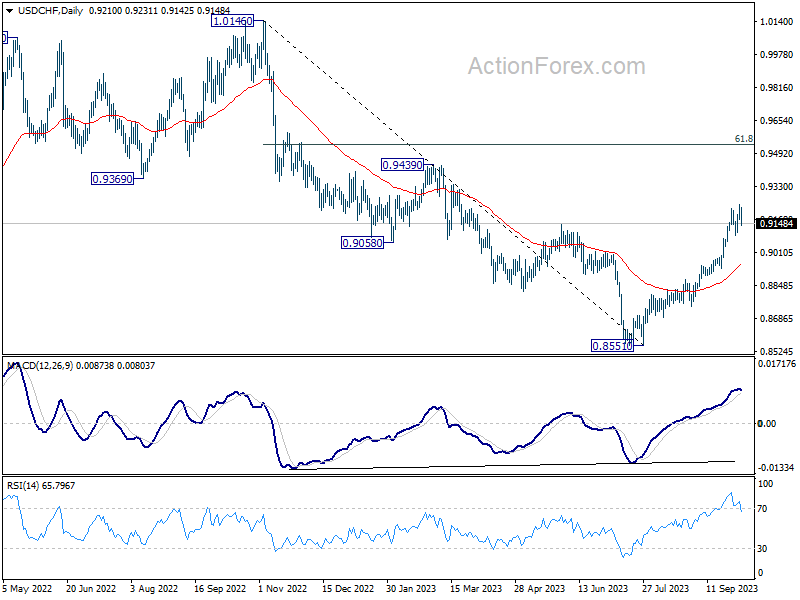

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9175; (P) 0.9209; (R1) 0.9246; More....

Intraday bias in USD/CHF is turned neutral with current retreat, and some consolidations could be seen first. But further rally is expected as long as 0.9089 support holds. Break of 0.9243 will resume the rally from 0.8551 and target 0.9439 resistance next. However, firm break of 0.9089 will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8942) holds, even in case of deep pullback.

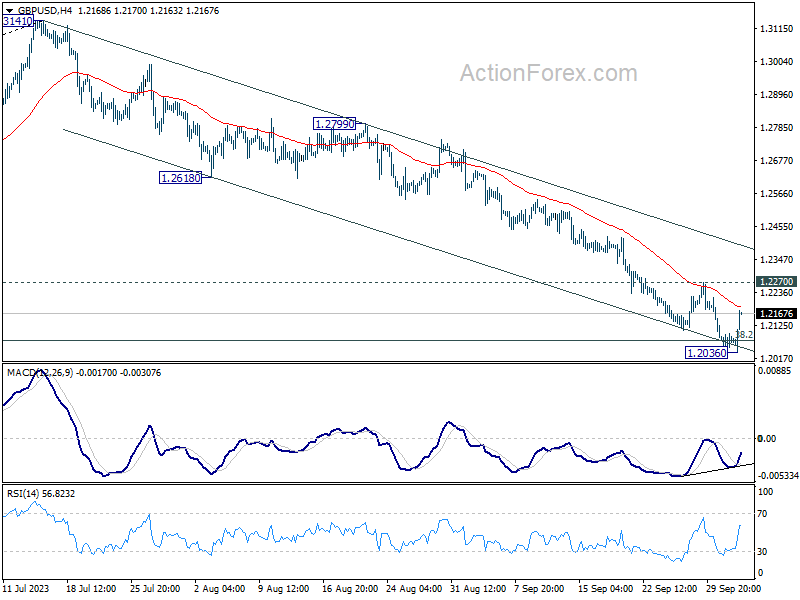

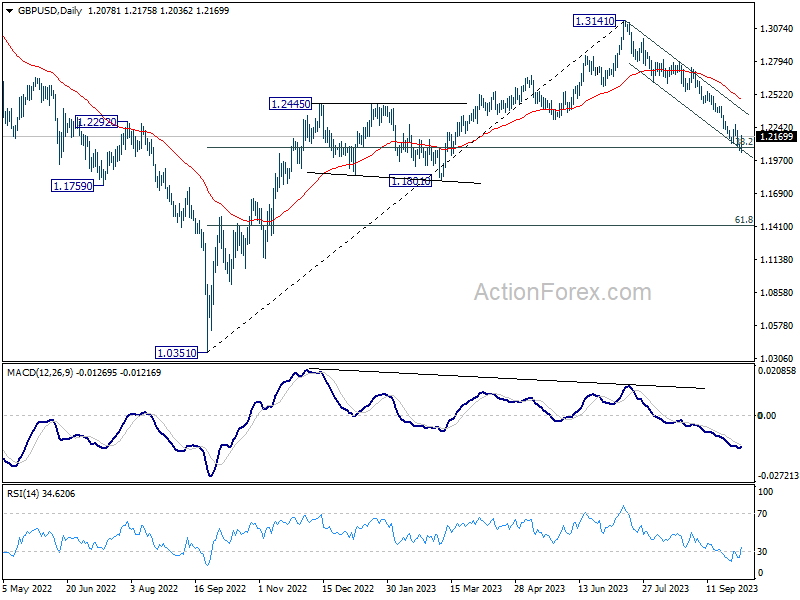

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2052; (P) 1.2077; (R1) 1.2102; More...

Intraday bias in GBP/USD is turned neutral with current recovery and some more consolidations could be seen. But outlook will stay bearish as long as 1.2270 resistance holds. Break of 1.2026 will resume the fall from 1.3141. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication, and target 1.1801 support next. On the upside, firm break of 1.2270 resistance will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

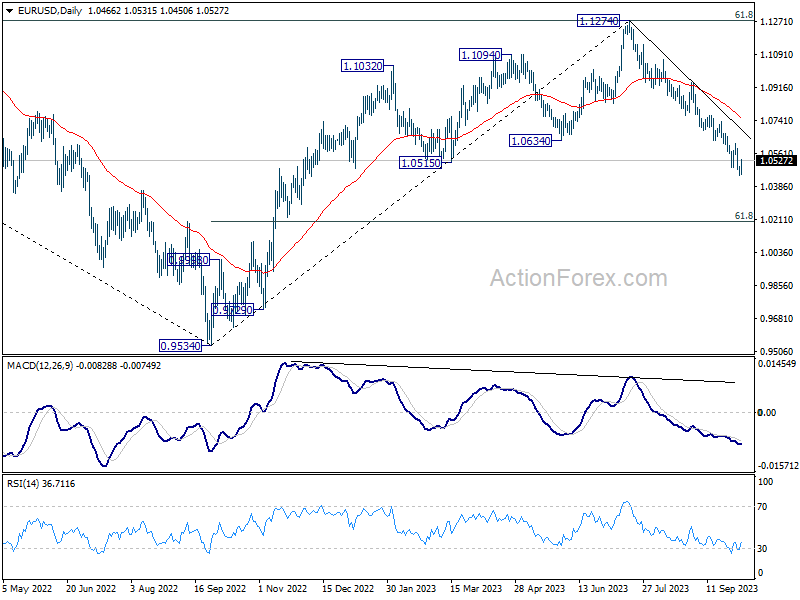

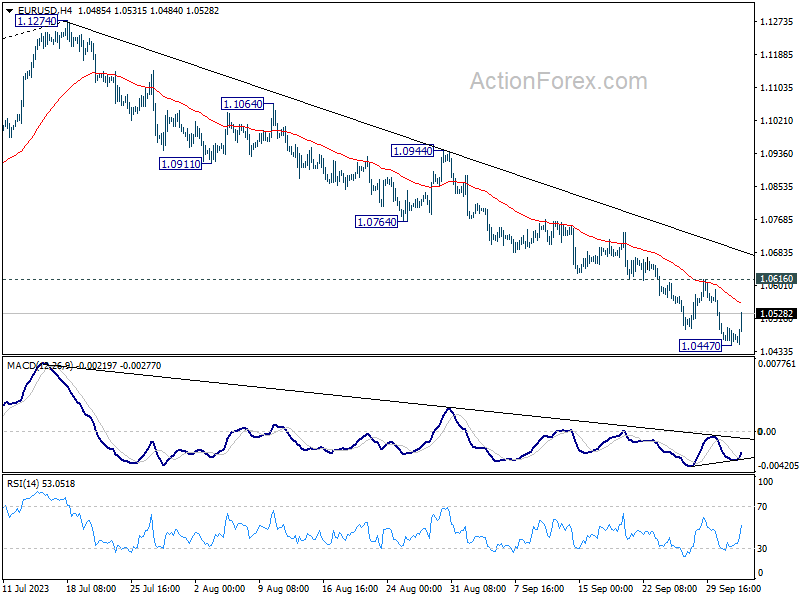

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0445; (P) 1.0469; (R1) 1.0491; More...

Intraday bias in EUR/USD is turned neutral first with today's recovery. Some consolidations could be seen. But outlook will remain bearish as long as 1.0616 resistance holds. Break of 1.0477 will resume the fall from 1.1274 to 1.0199 fibonacci level next. Nevertheless, firm break of 1.06161 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.