Sample Category Title

Japanese Officials Won’t be Able to Fight Strong USD Without Backing by BoJ U-Turn

Markets

The US manufacturing ISM on Monday and US JOLTS job openings (9.61mn from 8.8mn vs stabilization expected) yesterday. Eco data provided the bearish bond trend with some additional ammo, delaying in time any US recession bets and keeping the Fed’s preferred soft landing scenario alive. US money markets for the first time attach a 50/50 probability that the US central bank will effectively deliver on its “promised” (via dot plot) final rate hike this year. The sell-off nevertheless centered again at the longer end of the curve. US yields added 4.7 bps (2-yr) to 13.5 bps (30-yr) in a daily perspective. Since the Fed delivered the 5%+ message until end 2024 at the September 20 policy meeting, the US 10-yr yield and 30-yr yield increased by 44 bps and 50 bps respectively driven by higher real rates. Both are obviously at cycle and multiyear highs respectively at 4.85% and 4.97%. The US 10-yr real rate (2.43%) overtook inflation expectations (2.40%) for the first time since 2009. Other (global) core bonds followed US Treasuries south with the Fed’s course serving as a template for the rest. German yield changes varied between -1.7 bps (2-yr) and +7.6 bps (30-yr). The German 10-yr yield closed at a cycle high 2.97% and is about to pass beyond 3% for the first time since June 2011. The German 30-yr yield closed at 3.21%. The trade-weighted dollar closed off the intraday highs yesterday following a suspicious move in USD/JPY. The pair was fighting the psychologic 150 threshold which is seen as line in the sand for Japanese officials. As the pair tried to make its way beyond 150 following JOLTS data, it was countered by strong JPY inflows, pulling the FX rate temporary to USD/JPY 147.50. Currently, we’re back around 149.25, adding strength to our case that Japanese officials won’t be able to fight a strong USD without backing by a BoJ policy U-turn. Stock markets were wacked again with key European indices losing over 1% and Wall Street losses ranging between -1.3% (Dow) and -1.9% (Nasdaq). Technical pictures become more and more dire, with the trading pattern shifting to sell-on-upticks. We don’t fight ruling trends today even though the eco calendar might cause some additional 2-way volatility with ADP employment change and the services ISM scheduled in the US. The key European focus is on ECB President Lagarde’s speech at a monetary policy conference in Frankfurt with often overlooked Q2 Italian deficit data serving as a wildcard. As the Italian spread over Germany (10y) is on the verge of passing 200 bps for the first time since end of last year.

News & Views

The Reserve Bank of New Zealand this morning kept its policy rate unchanged at 5.50%. The Monetary Policy Committee assessed that interest rates are constraining economic activity and reducing inflationary pressure as required. Even as GDP growth in the June quarter was stronger than expected (0.9% Q/Q 1.8% Y/Y), the RBNZ expects demand in the economy to continue to slow. Weakening global demand is putting downward pressure on New Zealand export volumes and prices. Global import prices (ex oil) are seen easing. While the imbalance between supply and demand is moderating, the RBNZ indicates that a prolonged period of subdued activity remains required to reduce inflation, supporting the case to keep policy restrictive. At the same time, the RBNZ in the press release didn’t given a clear hint on further tightening. The central bank sees a near-term risk that activity and inflation do not slow as much as needed. Over the medium term, a greater slowdown in global demand, particularly in China, could weigh more on commodity prices and New Zealand exports. Markets expected a more hawkish tone. The 2-y government bond yields eased 3 bps after the decision (5.79%). The kiwi dollar dropped to NZD/USD 0.59.

Kevin McCarthy, the Republican Speaker of the US House of Representatives, was removed from his function as the House in a 216-210 vote approved a ‘motion to vacate’. Eight Republicans joined the 208 democrats in the vote. The vote came after opposition within the Republican party led by Matt Geatz, after McCarthy last week needed the support from democratic representatives to approve a bill avoiding a partial government shutdown. The House now needs to look for a new speaker, but there remains a high degree of dissent within the Republican party. The current situation de facto brings legislative action to a halt. A new agreement to fund the US government is needed by mid-November to again prevent a government shut-down. Also other key topics including US aid to Ukraine might be blocked in the process.

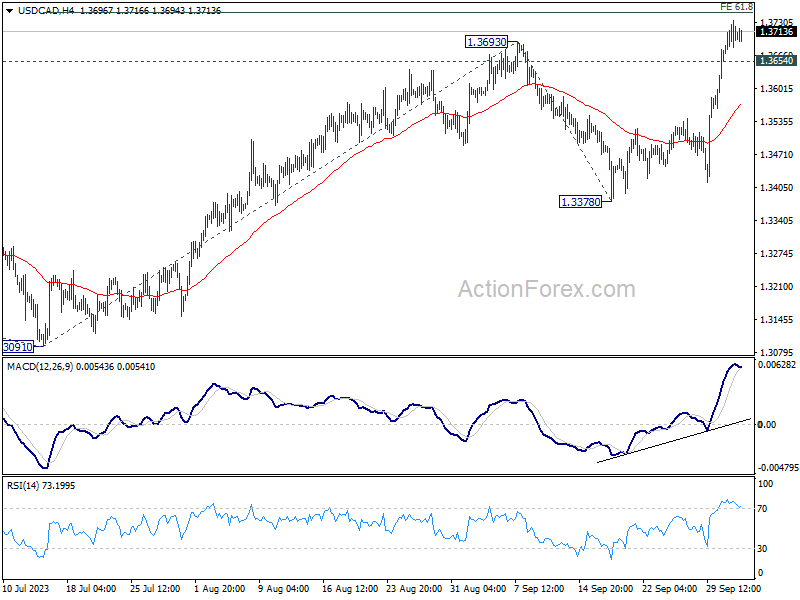

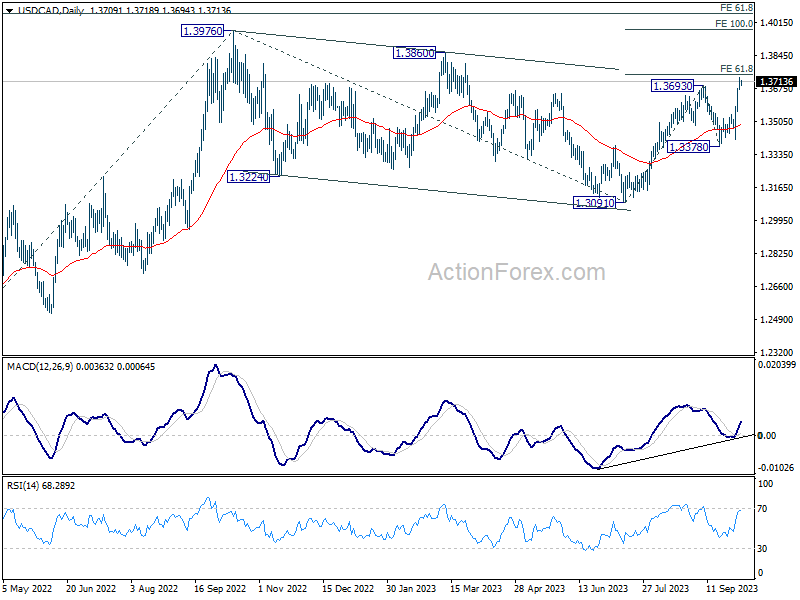

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3668; (P) 1.3702; (R1) 1.3743; More....

Intraday bias in USD/CAD remains on the upside at this point. Current rise from 1.3091 should target 61.8% projection of 1.3091 to 1.3693 from 1.3378 at 1.3750. Firm break there will target 100% projection at 1.3980. On the downside, below 1.3654 minor support will turn intraday bias neutral first.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

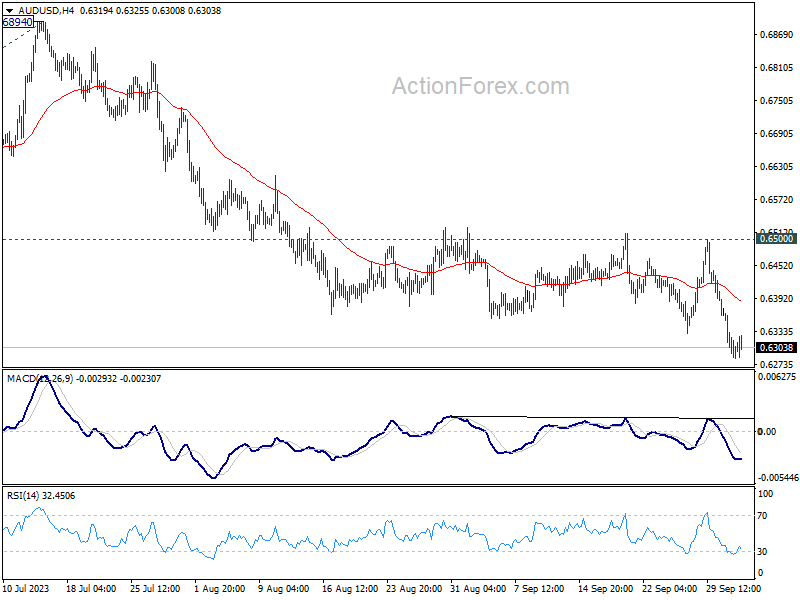

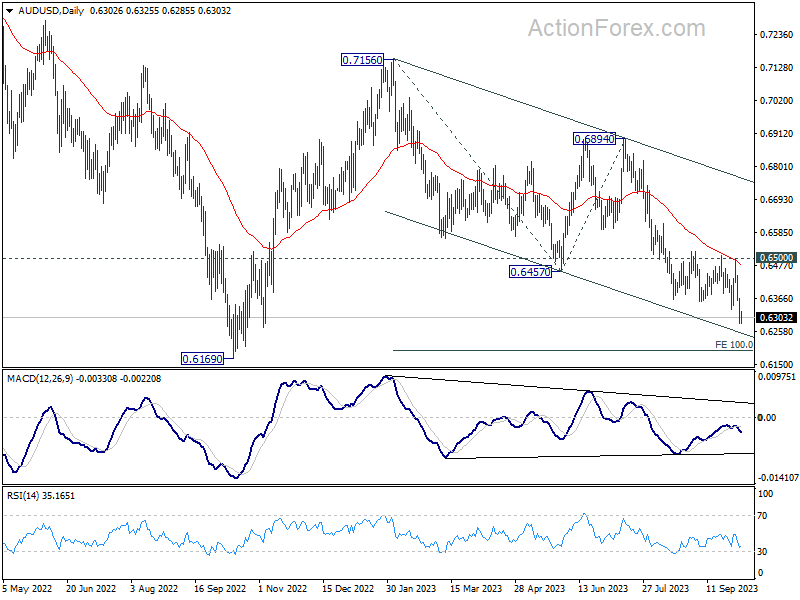

AUD/USD Daily Report

Daily Pivots: (S1) 0.6268; (P) 0.6320; (R1) 0.6353; More...

Intraday bias in AUD/USD remains on the downside for the moment. Current fall from 0.7156 is in progress and should target 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, break of 0.6500 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

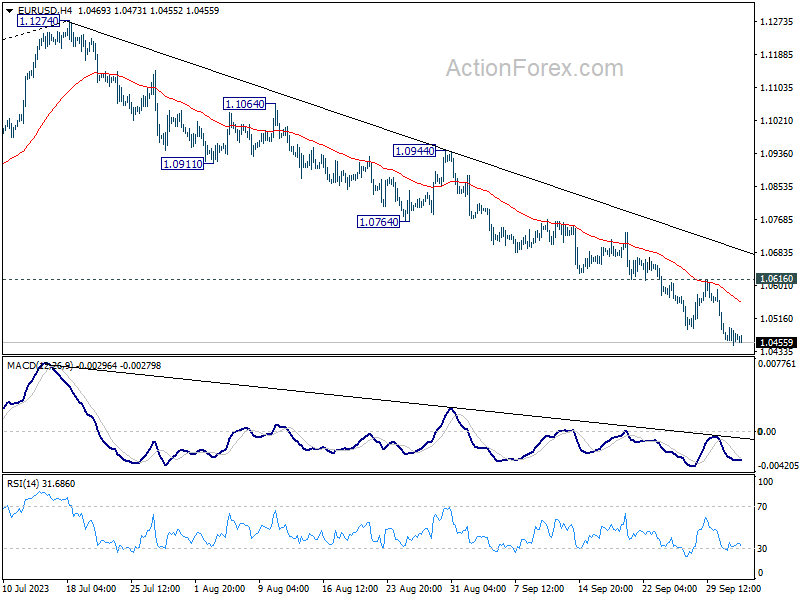

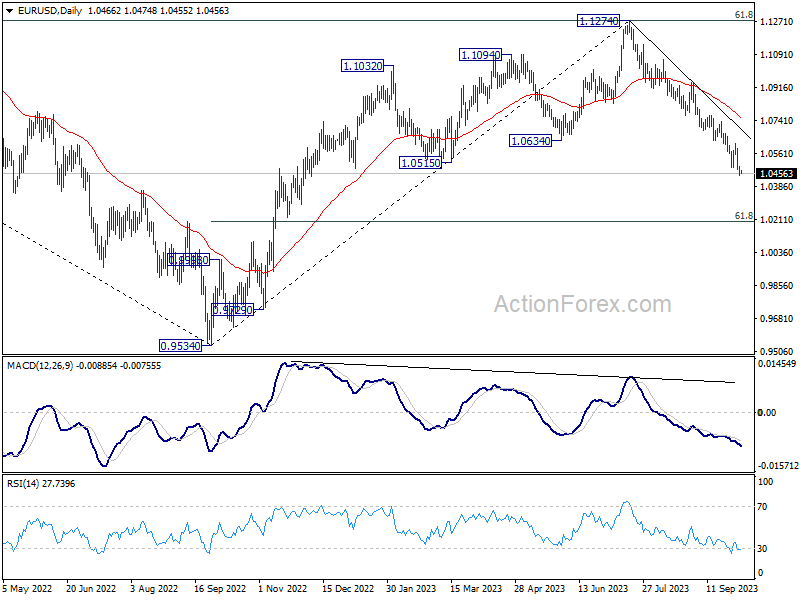

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0445; (P) 1.0469; (R1) 1.0491; More...

Intraday bias in EUR/USD stays on the downside for the moment. Fall from 1.1274 is in progress and should target 1.0199 fibonacci level next. On the upside, break of 1.0616 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

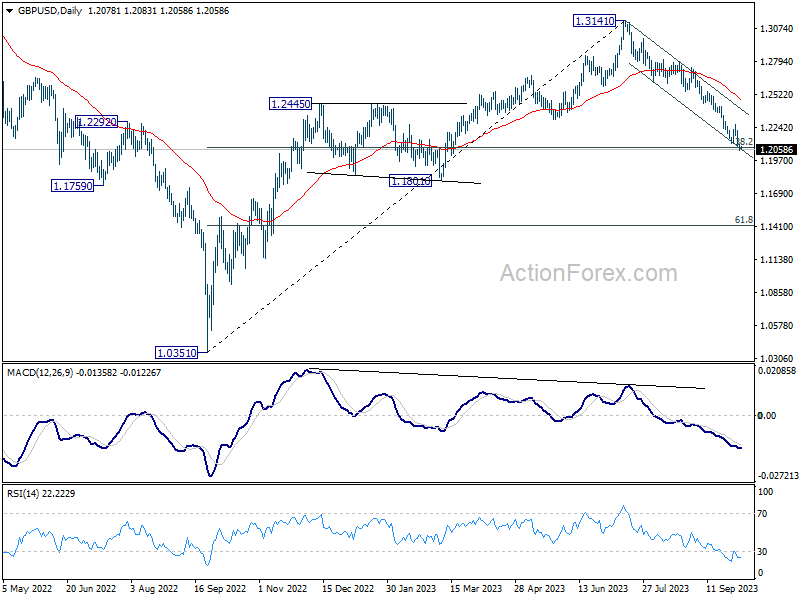

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2052; (P) 1.2077; (R1) 1.2102; More...

Outlook in GBP/USD is unchanged and intraday bias stays on the downside. Sustained trading below 1.2075 fibonacci level would carry larger bearish implication. Fall from 1.3141 should then target 1.1801 support next. On the upside, break of 1.2270 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2486) holds, in case of rebound.

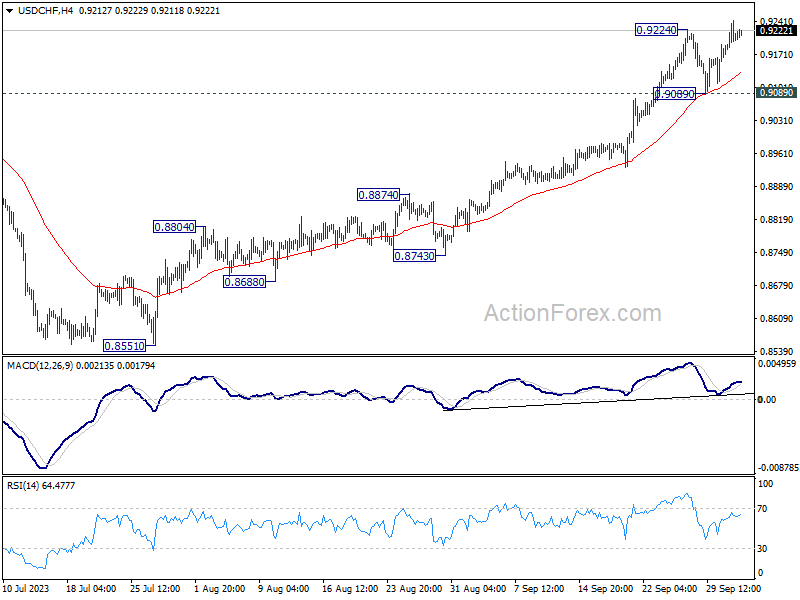

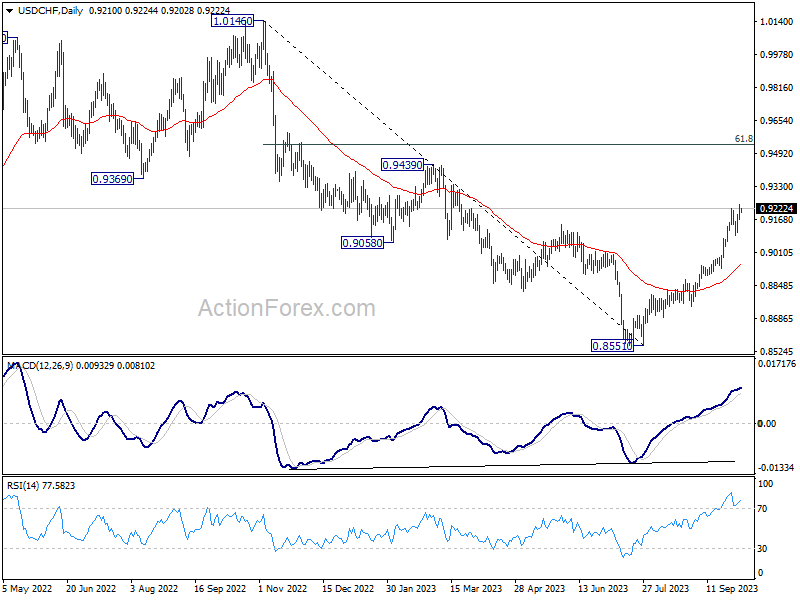

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9175; (P) 0.9209; (R1) 0.9246; More....

Intraday bias in USD/CHF remains on the upside for the moment. Current rise from 0.8551 should 0.9439 resistance next. On the downside, break of 0.9089 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8942) holds, even in case of deep pullback.

The Fear of Strong Jobs

Even a hint of an improving US jobs market sends shivers down investors' spines.

This is why the stronger than expected job openings data from the US spurred panic across the global financial markets yesterday. Although hirings and firings remained stable, the financial world was unhappy to see so many job opportunities offered to Americans as the data hinted that the US jobs market could be going back toward tightening, and not toward loosening. And that means that Americans will keep their jobs, find new ones, asked better pays, and keep spending. That spending will keep US growth above average and continue pushing inflation higher, and the Federal Reserve (Fed) will not only keep interest rates higher for longer but eventually be obliged to hike them more. Alas, a catastrophic scenario for the global financial markets where the rising US yields threaten to destroy value everywhere. PS. JOLTS data is volatile, and one data point is insufficient to point at changing trend. We still believe that the US jobs market will continue to loosen.

But the market reaction to yesterday’s JOLTS data was sharp and clear. The US 2-year yield spiked above 5.15% after the stronger than expected JOLTS data, the 10-year yield went through the roof and hit the 4.85% mark. News that the US House Speaker McCarthy lost his position after last week’s deal to keep the US government open certainly didn’t help attract investors into the US sovereign space. The US blue-chip bond yields on the other hand have advanced to the highest levels since 2009, and the spike in real yields hardly justify buying stocks if earnings expectations remain weak. The S&P500 is now headed towards its 200-DMA, which stands near the 4200 level. The more rate sensitive Nasdaq still has ways to go before reaching its own 200-DMA and critical Fibonacci levels, but the selloff could become harder in technology stocks if things got uglier.

In the FX, the US dollar extended gains across the board. The Reserve Bank of New Zealand (RBNZ) kept the interest rate steady at 5.5% as expected. Due today, the ADP report is expected to show a significant slowdown in US private job additions last month; the expectation is a meagre 153’000 new private job additions in September. Any weakness would be extremely welcome for the rest of the world, while a strong looking data, an - God forbid – a figure above 200K could boost the Federal Reserve (Fed) hawks and bring the discussion of a potential rate hike in November seriously on the table.

The EURUSD consolidates below the 1.05 level, the USDJPY spiked shortly above the 150 mark, and suddenly fell 2% in a matter of minutes, in a move that was thought to be an unconfirmed FX intervention. Gold extended losses to $1815 per ounce as the rising US yields increase the opportunity cost of holding the non-interest-bearing gold.

The barrel of American crude remains under pressure below the $90pb level. US shale producers say that they will keep drilling under wraps even if oil prices surge to $100pb, pointing at Joe Biden’s war against fossil fuel. A tighter oil supply is the main market driver for now, but recession fears will likely keep the upside limited, and September high could be a peak.

Strong JOLTS Data Supports Even Higher Yields

Market movers today

ECB president Christine Lagarde delivers pre-recorded welcome address to a monetary policy conference, and ECB board member Luis de Guindos is among the speakers at a conference organised by the Central Bank of Cyprus.

We receive euro area PPI figures for august. Producer prices have dropped like a stick this year after the sharp increases last year. In July, the index fell -7.6% and will likely drop even more in August as the price increases peaked in August last year at 43.4% y/y. The decline in producer prices will continue to weigh on goods prices, which have declined over the last months. This is welcoming news for the ECB but also as expected after the sharp rise in producer prices last year. However, the price pressure in the service sector continues due to a tight labour market and rising wages. Service PMI output prices are still at 55.

We also get data for the August retail sales in the euro area. Retail sales in real terms has been weak this year but surprised marginally on the upside in both June and July. Rising consumer confidence and real wages should support the figure going forward, but for now, consumers still seem chary with spending.

ISM non-manufacturing and the final version of the S&P service PMI are released in the US. The flash service PMI surprised to the upside both on activity and prices paid.

The ADP employment report is released in the US, but note that it is not always a good predictor for the official jobs report due Friday.

Fed governor Michelle Bowman speaks on banking reform.

The 60 second overview

US Data & Fed: The US August JOLTs report added support for the rates higher for longer narrative, as job openings unexpectedly rose to 9.61 million (July revised higher to 8.92 million; from 8.83). The ratio of job openings to unemployed still declined to 1.51 (from 1.53) reflecting the sharp recovery in labour force participation, but in any case labour market conditions remain tight. Hiring showed no signs of cooling, involuntary layoffs remained stable below pre-pandemic levels and the uptick in voluntary quits suggests that workers' confidence in finding new job opportunities has remained high. UST yields continued to edge higher following the release, and while both the Fed's Mester and Bostic acknowledged that the recent tightening in financial conditions would likely weigh on growth, neither appeared overly concerned, with Bostic noting that businesses would not be affected 'beyond what would happen in a normal tightening cycle'.

US politics: Last night republican Kevin McCarthy was ousted from his position as Speaker of the House. The motion-to-vacate came after the last weekends' continuing resolution (CR) funding bill required House democrats' support to pass. Vast majority of House republicans supported McCarthy in a tight vote, but as all of the House democrats joined only eight hardliner republicans in voting against the speaker, McCarthy lost the vote 216-210. As the CR bill covers government funding until mid-November, the result will not have immediate effect on the economy or the markets. But even so, as this was the first time in history when House speaker has been ousted by a vote, and as McCarthy's successor remains unclear, the path towards agreeing on the remaining funding bills by mid-November likely turned even more uncertain.

RBNZ: The Reserve Bank of New Zealand maintained the Official Cash Rate unchanged at 5.50% this morning as widely anticipated by both markets and analyst consensus. While risks to the growth outlook were seen as balanced, the overall tone in the press release was to the dovish side. RBNZ maintained its forward guidance unchanged, signalling that rate hikes are most likely already over, but that rates would remain at restrictive levels for 'a more sustained period of time'. Markets have speculated with a modest chance of RBNZ returning to hiking going forward, and hence the guidance was a slight dovish surprise, causing NZD/USD to decline following the meeting. We maintain a modestly downward-sloping forecast profile, with 12m forecast at 0.57.

Japan: Service PMI declined to 53.8 (revised up from 53.3) in September from 54.3 in August. It marks the lowest level since January and thus the service sector continues to decelerate. Even so, it remains strong not least supported by a booming tourism sector, which makes up for less impressive domestic demand. In the longer run, wage data will be key for more demand and a normalisation of monetary policies. We will know more on Friday.

Equities: Equities were sharply lower as yields broke a new record. The sell-off intensified in the US session amid the hot job print. Unlike last week, this resulted in a more classic value and defensive rotation. FANMAG, tech and yield sensitive real estate underperformed while defensives and value sectors (industrials, staples, materials) held up better. However, one sector stuck out: Banks. Banks underperformed yesterday which would normally not be the case in a rising yield environment. Fear of renewed bond losses in regional banks is probably one explanation behind this quite unusual mix. However, Nordic banks sold off massively too, and even underperformed the debt sensitive real estate sector. We have a hard time understanding the logic behind this and recommend buying banks on weakness.

Small caps underperform quite remarkably in this environment. This continued yesterday with Russell 2000 -1.7% (vs S&P 500 -1.1%) and OMX Nordic small cap -2% (vs Stoxx 600 -1.1%). This makes sense to us given the higher financing risk in small caps on top of weak liquidity. There will be a strong buy case in small caps later on, but probably not until after the recession, which is also when we expect QT to be done and liquidity to improve.

FI: Global bonds continue to rise despite inflation expectations such as 5y5y EUR and US inflation expectations either decline or have stabilised as spot inflation continues to decline. However, long-dated real rates and nominal rates have risen significantly during September and are slowly approaching 5% in 10Y Treasuries and 3% in 10Y Bunds. Furthermore, the bearish steepening of the curves continues. Yesterday's US labour market data from JOLT's report supported the higher for longer theme.

FX: The primary event in FX markets yesterday was the JPY volatility that followed USD/JPY hitting the 150 mark, which triggered a knee-jerk reaction drop in the cross. While not confirmed it has left markets speculating in the Japanese authorities intervening in the FX market. While the USD also had a strong session the Scandies came under heavy selling pressure with both EUR/NOK and EUR/SEK extending the rebounds following the last weeks' decline.

Credit: Muted activity in credit markets continued Tuesday with main 1bp wider and X-Over 4bp tighter. In Scandi space Carlsberg announced the termination of all licence agreements in Russia which means that the Russian Baltica business will be prevented from producing, marketing and selling Carlsberg group products. Furthermore, Carlsberg will take full impairment on the related assets. Overall this was not a surprise and we see no spread impact from the news.

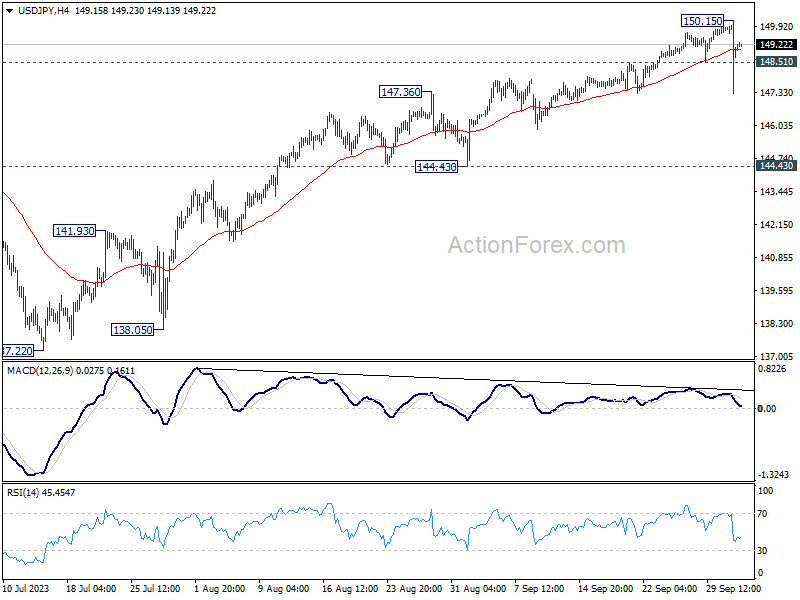

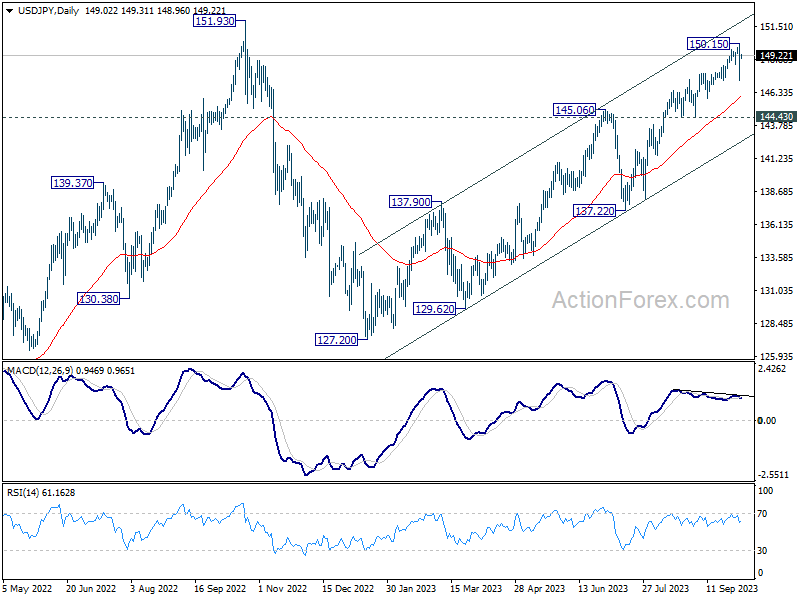

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.21; (P) 149.18; (R1) 150.03; More...

USD/JPY spiked lower to 147.28 overnight, on alleged intervention by Japan, but recovered quickly since then. As short term top should be in place at 150.15, on bearish divergence condition in 4H MACD. Intraday bias is turned neutral first and more corrective could be seen. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Market Mayhem: Escalating Risk Aversion Meets Yen Intervention

Dollar is finding strength amidst an atmosphere of palpable anxiety in the financial markets, stemming from a continuation of the risk-off mood from US into Asian session. This prevailing anxiety in the markets has been heightened by the pronounced drop in US stocks overnight, coupled with a surge in long-end treasury yields. Adding to the complexity, there's been a quick normalization in the yield curve accompanied by a notable spike in the VIX fear index. As investors brace themselves, the focus now pivots towards the forthcoming US ADP employment and ISM Services data. However, the market is caught in a conundrum, trying to decipher if positive data will quell or exacerbate the prevailing anxiety.

At the same time, Yen has made significant strides, an strong bounce that could be attributed to Japan's unconfirmed intervention in the currency markets. However, this edge was short-lived, with USD/JPY experiencing a swift rebound. Current behavior suggests that speculators might have been gearing up to capitalize on Yen sales, rather than aligning with Japan's presumed objective of buying the currency. With the financial climate teetering on unease and impending significant data releases like Friday's US NFP, we can expect substantial fluctuations in USD/JPY in the immediate future.

Following RBNZ's decision to keep interest rates steady, New Zealand Dollar is currently languishing near the bottom of the currency chart. Aussie, too, is underperforming, particularly after RBA's parallel decision yesterday. For the time being, European majors display a mixed performance, though the Swiss Franc is exhibiting a slight advantage. Yet, when considering their performances against each other, Euro, Sterling, and Swiss Franc are trading within their usual bounds.

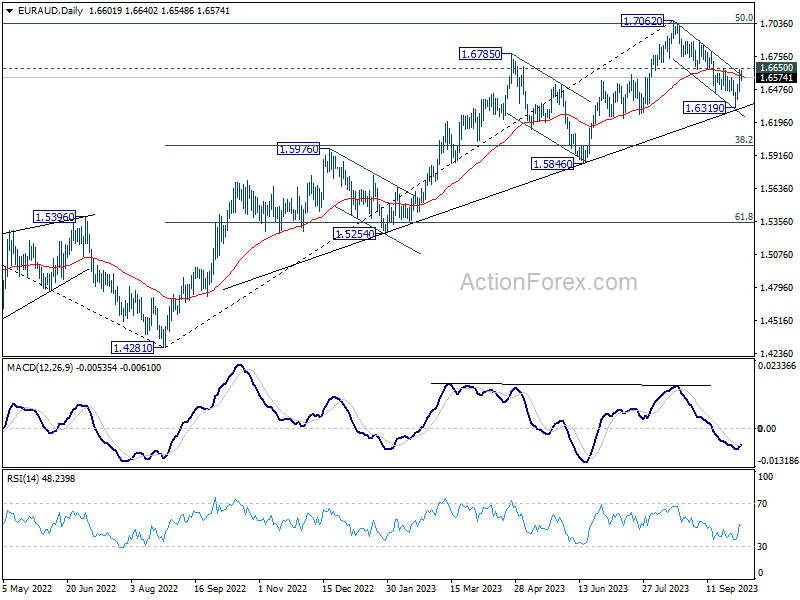

Technically, EUR/AUD is now pressing 1.6650 resistance after this week's bounce. Firm break there will argue that correction from 1.7062 has completed after drawing support from medium term rising trend line. Stronger rally would be seen back to retest 1.7062 high next. If realized, that would be a signal of more broad based selloff in Aussie, as probably intensification of risk aversion too.

In Asia, at the time of writing, Nikkei is down -1.87%. Hong Kong HSI is down -0.99%. Singapore Strait Times is down -1.50%. Japan 10-year JGB yield is up 0.033 at 0.797, just shy of 0.8 handle. Overnight, DOW dropped -1.29%. S&P 500 dropped -1.37%. NASDAQ dropped -1.87%. 10-year yield rose 0.119 to 4.802.

Japan's top brass remains mum on intervention claims

Market watchers were in a frenzy after Japanese Yen surged from 150 to the 147 zone against Dollar overnight , fuelling speculation that Japan's government may have stealthily intervened to push up the struggling currency. While evidence of a Yen-buying, Dollar-selling maneuver abounds, top officials in Japan remained tight-lipped today.

Finance Minister Shunichi Suzuki, when confronted by reporters, chose the path of silence over confirmation. He held back from validating the swirl of speculations about intervention. Suzuki reiterated a standard narrative, emphasizing the desirability of market-driven, stable currency movements that mirror economic fundamentals.

"Currency rates ought to move stably driven by markets, reflecting fundamentals. Sharp moves are undesirable," Suzuki noted. "The government is monitoring market developments very carefully with a sense of urgency. We will take appropriate steps against excessive volatility without excluding any options."

Masato Kanda, the top currency diplomat, provided insights into the government's assessment mechanism for currency movements. "If currencies move too much on a single day or, say, a week, that's judged as excess volatility," Kanda explained.

The implied volatility stands as a critical metric, among others, shaping the official perspective on whether Yen's moves are reaching alarming amplitudes.

Kanda further outlined that even in the absence of abrupt shifts, a gradual yet one-sided build-up of significant currency movements over time is also classified as excessive volatility. However, he too refrained from offering a direct commentary on the overnight upswing of Yen.

RBNZ holds rates, hints at longer duration of restrictive policy

RBNZ has opted to keep the Official Cash Rate stable at 5.50%, aligning with broad market anticipations. The minutes of the meeting revealed a consensus among committee members that restrictive interest rate environment might be needed "for a more sustained period of time".

In the short term, RBNZ is looking at a scenario where domestic demand could exhibit "greater resilience", spurred by migration. This situation could "slow the pace of expected disinflation". A related concern is wage inflation, which could take a longer time to ease than initially expected. Recent rise in oil prices could also risk "headline inflation being higher than expected".

Looking at the medium term, the minuted noted concerns about greater slowdown in global growth. Such a downturn could lead to further reductions in non-oil import prices. Moreover, weakened global demand, with a particular emphasis on China, could exert additional pressure on commodity prices, subsequently affecting New Zealand's export revenues.

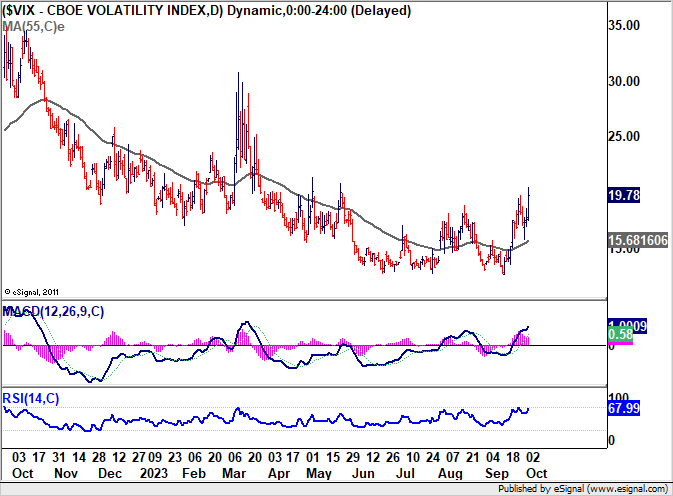

Anxiety grips Wall Street: DOW plummets, VIX jumps, Yields soar

Economic storm clouds appear to be gathering on the horizon. With DOW experiencing its most significant drop since March and key Treasury yields touching multi-year highs, whispers of a potential recession are becoming more audible. This is further exacerbated by the behavior of VIX, often dubbed the "fear index", which indicates heightened market apprehensions.

DOW plummeted by -430.97 points, or -1.29%, nudging it into negative territory for the year, now lagging by -0.4%. This downturn wasn't isolated to stocks. The 10-year yield reached a staggering 4.8%, a pinnacle not seen in 16 years. Similarly, 30-year yield hit a peak of 4.925%, levels of which we haven't seen since 2007.

The narrowing gap between the 2-year and 10-year Treasury yields, contracting to a mere 35 basis points from over 100 basis points a few months earlier, is especially concerning. This normalization, or "de-inverting", of a vital part of the yield curve is often viewed as a precursor to economic downturns, igniting debates on the imminence of a recession.

Adding to the market's jitters, VIX has climbed for three consecutive sessions, momentarily crossing the critical 20 level and finishing at a six-month high. Values below 20 on the VIX generally signify market stability, but as it surpasses this threshold, it denotes an environment fraught with investor unease and skittishness.

Back to DOW, it's now pressing and important near fibonacci support at 38.2% retracement of 28660.94 to 35679.13 at 32998.17. Sustained break of this level will strengthen the case that fall from 35679.13 is reversing whole rise from 28660.94. This decline could be viewed as the third leg of the long term pattern from 36952.65 high. Deeper fall would be seen to 31.429.82 support, which is close to 61.8% retracement at 31341.88.

In any case, near term outlook will stay bearish as long as 34029.22 support turned resistance holds. The rest of the week, with ISM services today and non-farm payrolls release on Friday, will be crucial.

Looking ahead

Eurozone PMI services final, PPI and retail sales will be released in European session. UK will also release PMI services final. Later in the day, US ADP employment ISM services and factory orderes will take center stage.

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.21; (P) 149.18; (R1) 150.03; More...

USD/JPY spiked lower to 147.28 overnight, on alleged intervention by Japan, but recovered quickly since then. As short term top should be in place at 150.15, on bearish divergence condition in 4H MACD. Intraday bias is turned neutral first and more corrective could be seen. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 07:45 | EUR | Italy Services PMI Sep | 50 | 49.8 | ||

| 07:50 | EUR | France Services PMI Sep F | 43.9 | 43.9 | ||

| 07:55 | EUR | Germany PMI Sep F | 49.8 | 49.8 | ||

| 08:00 | EUR | Eurozone Services PMI Sep F | 48.4 | 48.4 | ||

| 08:30 | GBP | Services PMI Sep F | 47.2 | 47.2 | ||

| 09:00 | EUR | Eurozone PPI M/M Aug | 0.60% | -0.50% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Aug | -11.60% | -7.60% | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | -0.50% | -0.20% | ||

| 12:15 | USD | ADP Employment Change Sep | 155K | 177K | ||

| 13:45 | USD | Services PMI Sep F | 50.2 | 50.2 | ||

| 14:00 | USD | ISM Services PMI Sep | 53.6 | 54.5 | ||

| 14:00 | USD | Factory Orders M/M Aug | 0.20% | -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | -0.1M | -2.2M |