Sample Category Title

ADP Job Figures Weigh on Dollar, But Uptrend Still Intact

Dollar softens broadly today, as it seems traders are exercising caution, pivoting their focus towards forthcoming heavy-weight economic data releases from the US in the second half of the week. The greenback's pull back also extends following much weaker than expected ADP private job data. Interestingly, this "bad news is good news" effect is also reflected in the positive turn of DOW futures, suggesting a potential stabilization in the stock markets following yesterday's steep decline. Concurrently, 10-year yield is also witnessing a retracement from its peak.

Today, European majors are stealing the spotlight, leading the pack in the forex market. Sterling, in particular, is enjoying additional support following an upward revision in UK's PMI Services data. In contrast, Yen seems to be losing steam as the unconfirmed intervention by Japan appears to be losing its initial impact. Commodity-linked currencies, on the other hand, are languishing, hampered by a yet-to-recover risk sentiment.

On the technical front, Dollar is expected to undergo further consolidation in anticipation of Friday's NFP. However, key levels are holding firm, suggesting that the near-term outlook for the greenback remains bullish, priming it for another rally. These pivotal levels include 1.0616 resistance in EUR/USD, 1.2270 resistance in GBP/USD, and 0.9089 support in USD/CHF.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is up 0.35%. CAC is up 0.54%. Germany 10-year yield is down -0.0324 at 2.936. Earlier in Asia, Nikkei dropped -2.28%. Hong Kong HSI dropped -0.78%. Singapore Strait Times dropped -1.41%. Japan 10-year JGB yield rose 0.0442 to 0.808.

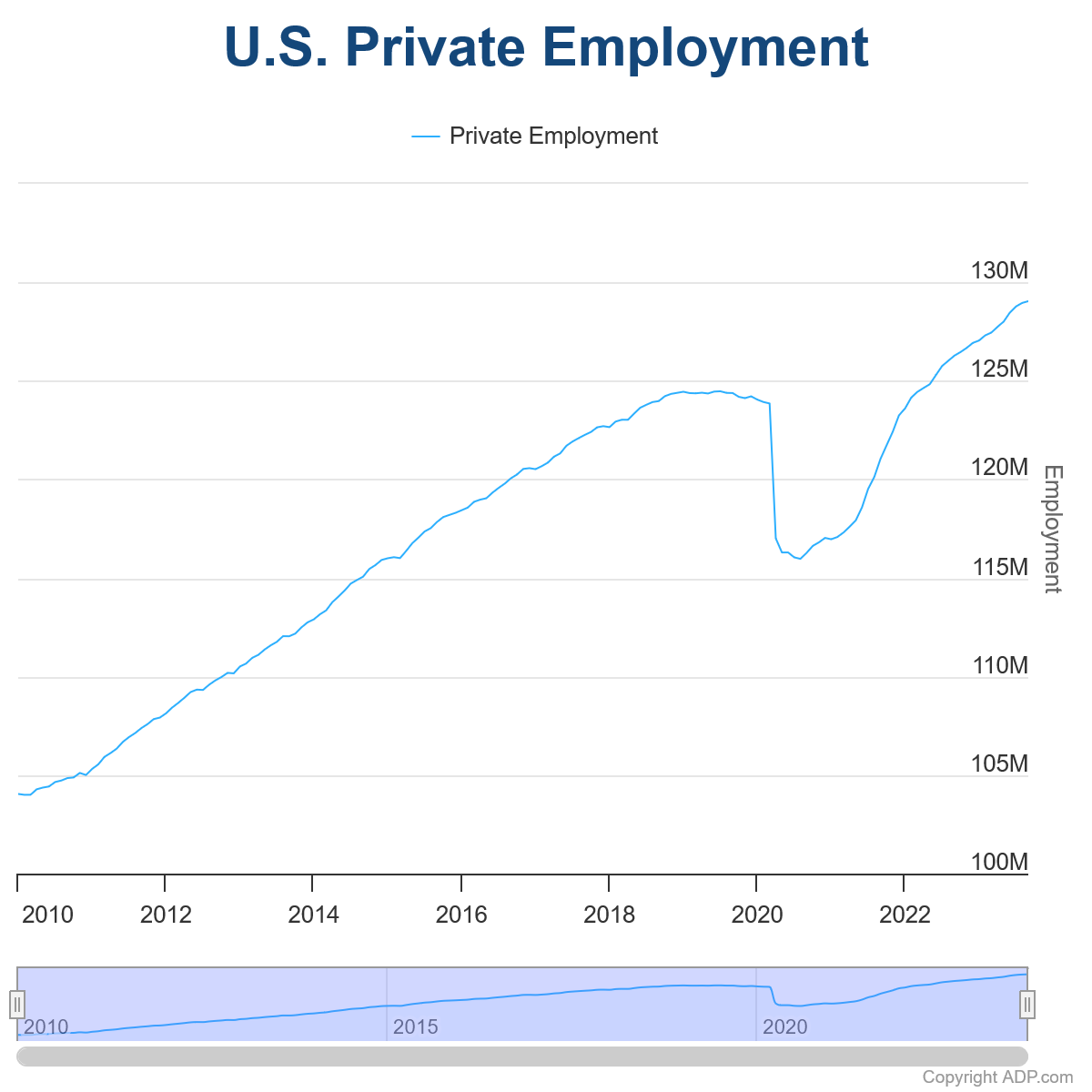

US ADP employment rises only 89k, wages growth slows

US private sector witnessed a notable slowdown in employment growth last month, as revealed by the ADP's latest report. A mere addition of 89k jobs in September fell significantly short of the anticipated 155k.

Dissecting these figures, goods-producing sector experienced a modest increase, adding 8k positions, while services sector contributed the lion's share with an 81k rise. By establishment size, small companies added 95k jobs, medium added 72k, large cut -83k.

In terms of wage dynamics,for those who remained in their current positions, the median change in annual pay persisted at 5.9% yoy. However, those switching roles saw a deceleration in wage growth, descending from 9.7% yoy to 9.0% yoy.

Nela Richardson, ADP's chief economist, expressed her concerns on the current employment scenario, stating, "We are seeing a steepening decline in jobs this month." Adding to the bleak outlook, she commented on the wage scenario, observing, "Additionally, we are seeing a steady decline in wages in the past 12 months."

ECB's Lagarde: Rates reached level for timely return of inflation to target

ECB President Christine Lagarde reiterated in a speech today that current interest rates are at the level to return inflation to target in a timely manner. She also laid out three criteria for future decisions.

"Based on our current assessment, we consider that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our medium-term target", Lagarde said.

Further shedding light on ECB's decision-making framework, Lagarde stated that their "future decisions will continue to be based on these three criteria." She detailed these criteria as: "the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission."

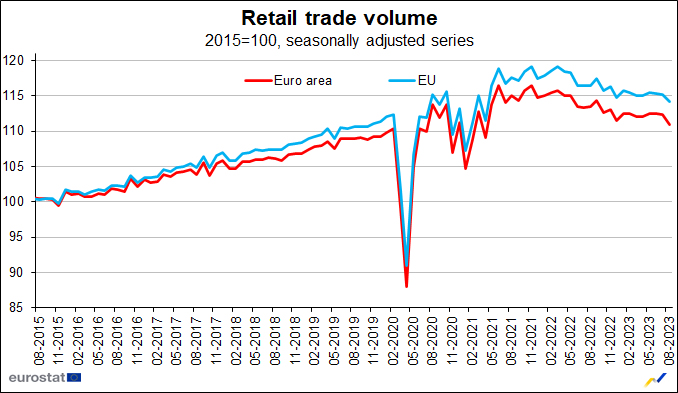

Eurozone retail sales falls -1.2% mom in Aug, EU down -0.9% mom

Eurozone retail sales fell -1.2% mom in August, well below expectation of -0.5% mom. Volume of retail trade decreased by -3.0% for automotive fuels, by -1.2% for food, drinks and tobacco and by -0.9% for non-food products.

EU retail sales was down -0.9% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in the Portugal (-3.0%), France (-2.8%) and Belgium (-1.5%). The highest increases were observed in Luxembourg (+1.9%), Poland (+1.7%) and Denmark (+1.6%).

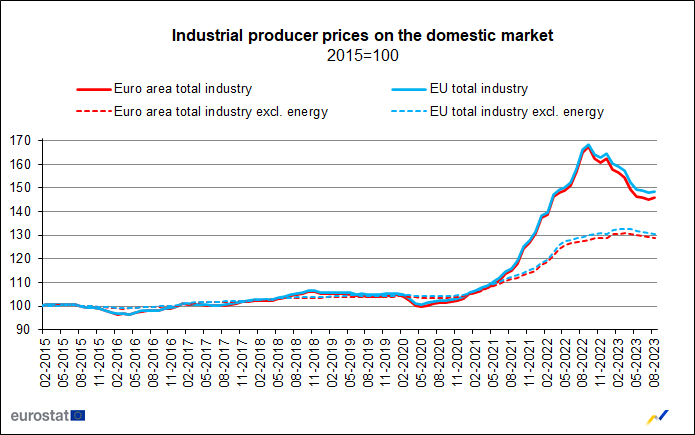

Eurozone PPI at 0.6% mom, -11.5% yoy in Aug

Eurozone PPI came in at 0.6% mom, -11.5% yoy in August, versus expectation of 0.6% mom, -11.6% yoy. For the month, industrial producer prices increased by 2.5% mom in the energy sector, while prices remained stable for capital goods and for non-durable consumer goods, and prices decreased by -0.1% mom for durable consumer goods and by 0.4% for intermediate goods. Prices in total industry excluding energy decreased by -0.2% mom.

EU PPI came in at 0.5% mom, -10.5% yoy. The biggest monthly increases in industrial producer prices were observed in Ireland (+3.7%), Finland (+2.4%) and Greece (+2.0%), while the largest decreases were recorded in Romania (-1.3%), Slovenia (-0.7%) and Belgium (-0.6%).

Eurozone PMI composite finalized at 47.2, can't jump on the hope train yet

The latest Eurozone PMI Services data brings both a glimmer of optimism and a note of caution to an economic region. The finalized PMI Services for September stood at 48.7, marking an increment from August's 47.9. Composite index also saw a marginal uplift to 47.2 from the previous month's 46.7. While the numbers reflect an uptick, the fragility of the recovery becomes apparent when examining the country-specific data and underlying factors.

A look at the composite PMI output index reveals a contrasting scenario among the countries. Ireland tops the chart with a two-month low of 52.1, while France lags at a 34-month low of 44.1. Germany (46.4) and Italy (49.2), despite being on a multi-month high, are still not out of the woods, pointing towards a segmented recovery pattern.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, offers a balanced perspective. "The HCOB Composite PMI for the Eurozone did rebound a bit. However, we can't jump on the hope train yet," he cautioned. The declining new business, especially in powerhouse economies like Germany and France, underscores this sentiment, indicating a continual decline in outstanding business and a drop in business expectations.

In the corridors of ECB, where deliberations over the next interest rate decision are underway, the latest PMI data could act as a double-edged sword. The hawks find solace in the Input Price Index, propelled by wages and energy costs, marking a four-month pinnacle. In contrast, the doves might highlight the moderated pace at which service prices are increasing – the slowest since the summer of 2021.

"Prices are nevertheless still climbing the ladder rather fast, a weird twist when the economy is singing the blues," de la Rubia noted.

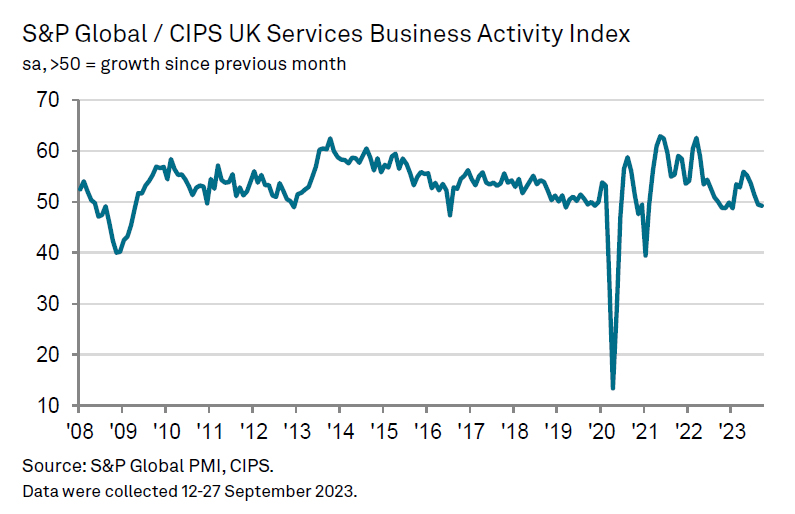

UK PMI services finalized at 49.3, silver lining in easing inflationary pressures

UK PMI Services was finalized at 49.3 in September, a marginal drop from the neutral 50.0 recorded in August. S&P Global's analysis points to persistent declines in both business activity and new ventures, and notably, the pace of job shedding is at its quickest since January 2021. However, the silver lining lies in easing inflationary pressures, marking their lowest in over two years.

Tim Moore, Economics Director at S&P Global Market Intelligence, cited reductions in non-essential business and consumer expenditure as significant dampeners on service sector activity. "A combination of elevated borrowing costs and subdued economic conditions had led to lower new business intake," he remarked.

Decline in export sales, particularly influenced by reduced European demand, further contributed to the sector's woes. Service providers' response has been cautionary, with hiring significantly scaled back given the current uncertainties.

On a positive note, Moore highlighted the diminishing inflationary pressures in the sector, observing, "headline rates of inflation will continue to moderate in the coming months, with service sector input costs rising at the slowest pace for nearly two-and-a-half years." This, coupled with the anticipation of consistent decreases in UK consumer price inflation, could potentially revive demand, instilling a sense of optimism for the future.

RBNZ holds rates, hints at longer duration of restrictive policy

RBNZ has opted to keep the Official Cash Rate stable at 5.50%, aligning with broad market anticipations. The minutes of the meeting revealed a consensus among committee members that restrictive interest rate environment might be needed "for a more sustained period of time".

In the short term, RBNZ is looking at a scenario where domestic demand could exhibit "greater resilience", spurred by migration. This situation could "slow the pace of expected disinflation". A related concern is wage inflation, which could take a longer time to ease than initially expected. Recent rise in oil prices could also risk "headline inflation being higher than expected".

Looking at the medium term, the minuted noted concerns about greater slowdown in global growth. Such a downturn could lead to further reductions in non-oil import prices. Moreover, weakened global demand, with a particular emphasis on China, could exert additional pressure on commodity prices, subsequently affecting New Zealand's export revenues.

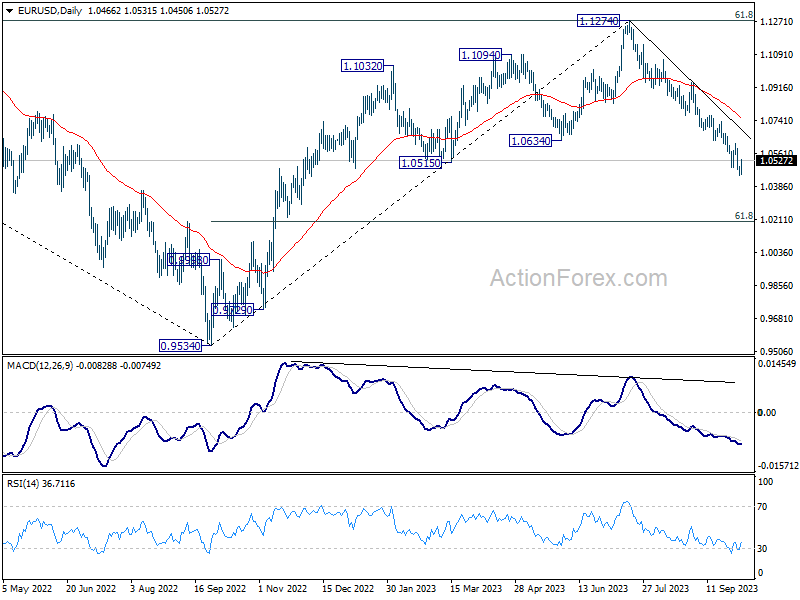

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0445; (P) 1.0469; (R1) 1.0491; More...

Intraday bias in EUR/USD is turned neutral first with today's recovery. Some consolidations could be seen. But outlook will remain bearish as long as 1.0616 resistance holds. Break of 1.0477 will resume the fall from 1.1274 to 1.0199 fibonacci level next. Nevertheless, firm break of 1.06161 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 07:45 | EUR | Italy Services PMI Sep | 49.9 | 50 | 49.8 | |

| 07:50 | EUR | France Services PMI Sep F | 44.4 | 43.9 | 43.9 | |

| 07:55 | EUR | Germany PMI Sep F | 50.3 | 49.8 | 49.8 | |

| 08:00 | EUR | Eurozone Services PMI Sep F | 48.7 | 48.4 | 48.4 | |

| 08:30 | GBP | Services PMI Sep F | 49.3 | 47.2 | 47.2 | |

| 09:00 | EUR | Eurozone PPI M/M Aug | 0.60% | 0.60% | -0.50% | |

| 09:00 | EUR | Eurozone PPI Y/Y Aug | -11.50% | -11.60% | -7.60% | |

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | -1.20% | -0.50% | -0.20% | -0.10% |

| 12:15 | USD | ADP Employment Change Sep | 89K | 155K | 177K | 180K |

| 13:45 | USD | Services PMI Sep F | 50.2 | 50.2 | ||

| 14:00 | USD | ISM Services PMI Sep | 53.6 | 54.5 | ||

| 14:00 | USD | Factory Orders M/M Aug | 0.20% | -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | -0.1M | -2.2M |

US ADP employment rises only 89k, wages growth slows

US private sector witnessed a notable slowdown in employment growth last month, as revealed by the ADP's latest report. A mere addition of 89k jobs in September fell significantly short of the anticipated 155k.

Dissecting these figures, goods-producing sector experienced a modest increase, adding 8k positions, while services sector contributed the lion's share with an 81k rise. By establishment size, small companies added 95k jobs, medium added 72k, large cut -83k.

In terms of wage dynamics,for those who remained in their current positions, the median change in annual pay persisted at 5.9% yoy. However, those switching roles saw a deceleration in wage growth, descending from 9.7% yoy to 9.0% yoy.

Nela Richardson, ADP's chief economist, expressed her concerns on the current employment scenario, stating, "We are seeing a steepening decline in jobs this month." Adding to the bleak outlook, she commented on the wage scenario, observing, "Additionally, we are seeing a steady decline in wages in the past 12 months."

Nikkei 225 May See a Silver Lining from Japanese Banks

- The current second-half performance of the Nikkei 225 is considered wobbly as it recorded a Q3 loss of -4% and underperformed slightly against the US S&P 500.

- The recent lacklustre performance of the Nikkei 225 has been impacted significantly by the performance of the S&P 500 rather than JPY movement.

- In the past three months, Japanese banks have offered a silver lining in a bearish Nikkei 225 environment as the TOPIX Banks sector outperformed with a positive return of +13.22%

- Watch the 200-day moving average of the Nikkei 225 now acting as key medium-term support at 29,880.

In the first half of 2023, the Japanese benchmark stock index, Nikkei 225 recorded a stellar performance of +27.19% that managed to surpass the US S&P 500 (+15.91%) and the MSCI All Country World Index exchange-traded fund (+13.03) over the same period.

In contrast, the second half of 2023 has painted a different tune, the Nikkei 225 ended Q3 with a loss of -4.01%, and it also kickstarted Q4 will a quarter-to-date loss of -4.18% as of 4 October 2023 at this time of the writing. Also, the Nikkei 225 underperformed slightly against the US S&P 500 (- 3.65%), and MSCI All Country World Index ETF (-3.72%) in Q3.

What is the main factor that is driving the current lacklustre performance of Nikkei 225?

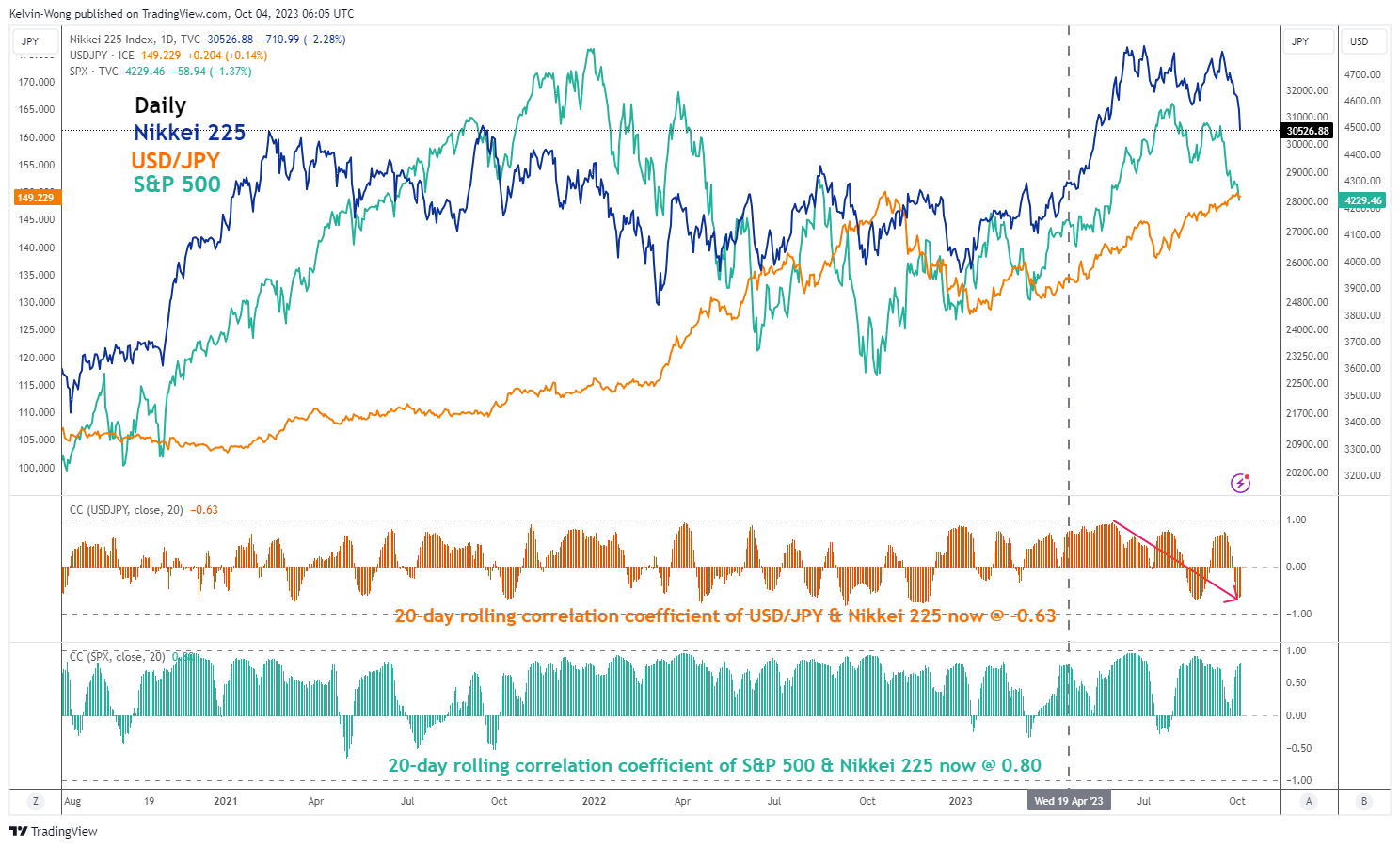

Fig 1: Nikkei 225’s 20-day rolling correlation with USD/JPY & S&P 500 as of 4 Oct 2023 (Source: TradingView, click to enlarge chart)

Based on a multi-factor model approach to determine the potential future returns of the Japanese stock market (Nikkei 225), the “traditional” positive beta factor of USD/JPY has diminished in recent months.

The prior USD/JPY’s high direct correlation with Nikkei 225 since June 2023 has broken down as the USD/JPY’s 20-day rolling correlation with Nikkei 225 has dipped into a negative significant reading of -0.64 as of 4 October 2023.

In contrast, the US S&P 500 ‘s 20-day rolling correlation with the Nikkei 225 has maintained a high positive reading of 0.80 over the same period.

Therefore, the current weak performance seen in the Nikkei 225 is likely to be more impacted by the US stock market (S&P 500) rather than the movement of the JPY as right now a weaker JPY against the USD has not triggered a positive feedback loop back into the Japanese stock market.

The TOPIX Banks sector has offered a silver lining

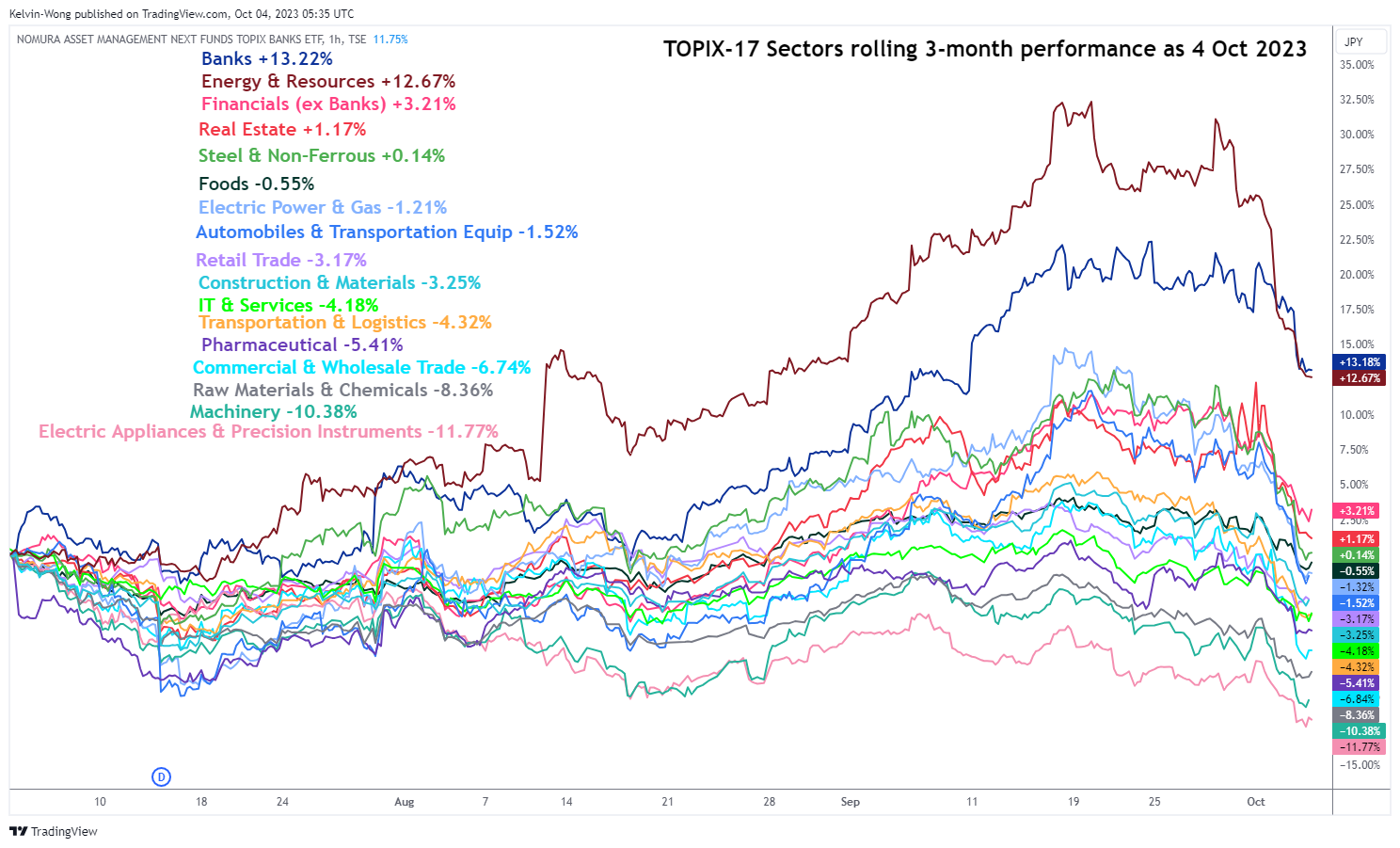

Fig 2: 3-month rolling performances of TOPIX sectors as of 4 Oct 2024 (Source: TradingView, click to enlarge chart)

Among the 17 TOPIX industry sectors in the Japanese stock market, the Banks sector was one of the worst performers in the first half of 2023, but its fortunes have started to reverse in Q3 where it is now the top performer with a +13.22% return based on a three-month rolling calculation as of 4 October 2023.

Fig 3: JGB yield curves as of 4 Oct 2024 (Source: TradingView, click to enlarge chart)

The primary driver that triggered the current resilient performance of the TOPIX Banks sector has been the steep rise in the Japanese government bonds (JGBs) yield curve after the Bank of Japan (BoJ) introduced a “flexible yield curve control” policy on the 10-year JGB yield during its July’s monetary policy meeting that in turn signalled a gradual step in exiting negative interest rates in Japan. A further steepening of the JGB yield curve is likely to give a significant positive boost to the net interest margins of Japanese banks.

The next line of defence will be the 200-day moving average

Fig 4: Nikkei 225 medium-term & major trends as of 4 Oct 2024 (Source: TradingView, click to enlarge chart)

The ongoing decline of -9.72% seen in the Nikkei 225 from its 19 June 2023 high of 33,773 is now fast approaching its key 200-day moving average now acting as key medium-term support at 29,880 that confluences with the swing high areas of 4/19 November 2022 and close to 38.2% Fibonacci retracement of the recent major uptrend phase from 9 March 2022 low to 19 June 2023 high.

In addition, the daily RSI oscillator has dipped into its oversold region which increases the odds of a potential multi-week rebound. Overall, the long-term secular uptrend of the Nikkei 225 remains intact as its price actions are still above the lower boundary of a major ascending channel in place since the March 2020 low.

In order to kickstart a potential new medium-term impulsive up move sequence, the bulls need to recapture the 32,390 resistance (congestion area of 11/25 September 2023, 50-day moving average & the 61.8% Fibonacci retracement of the entire decline from 19 June 2023 high to 4 October 2023 current intraday low).

On the other hand, failure to hold at the 200-day moving average support of 29,880 exposes the Index to an extended decline to challenge the long-term pivotal support zone of 28,500/28,100.

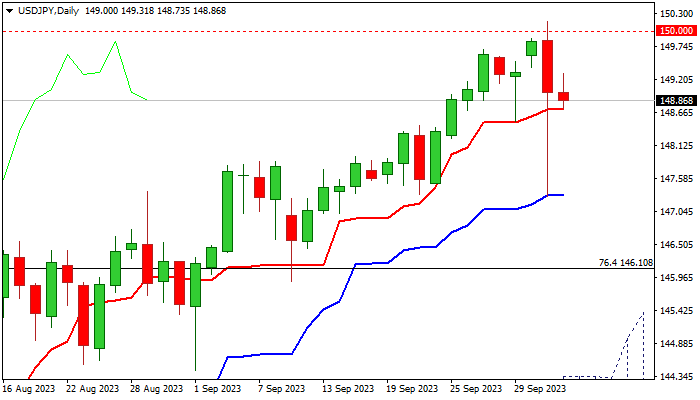

USD/JPY: Stabilizes after Wednesday’s Plunge, Risk of More Intervention Remains High

USDJPY regained traction in early Wednesday’s trading and held above 149 mark, following turbulent action in the US session on Tuesday.

The pair cracked psychological 150 barrier after upbeat US JOLTS job openings report and hit the highest in nearly one year, ahead of sharp dip, which markets suspect to be sparked by intervention, as Japan’s authorities signaled several times that they will intervene to support falling currency.

Quick bounce from the spike low (147.29) where the drop was contained by rising daily Kijun-sen, left long-tailed daily candle, suggesting that the dollar remains bid.

Daily studies remain bullish and supportive for another attack at 150 barrier, break of which would unmask 2022 peak (151.94).

However, risk of further action by Japanese authorities keeps the downside vulnerable, with initial negative signal expected on break below daily Tenkan-sen (148.72) and confirmation on drop and close below daily Kijun-sen (147.29)

Res: 149.31; 149.70; 150.00; 151.04.

Sup: 148.72; 148.29; 147.32; 146.10.

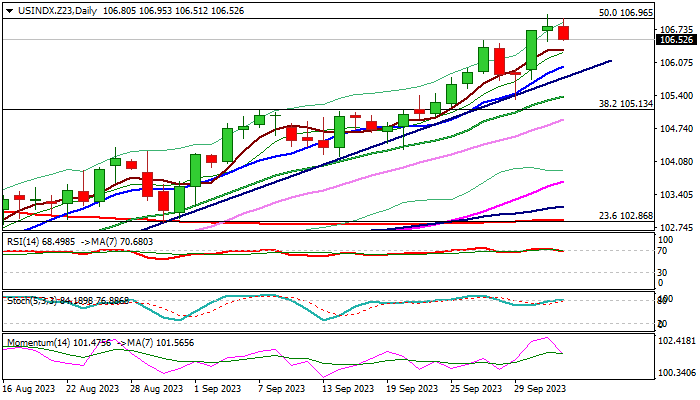

Dollar Index: Bulls Take a Breather Ahead of Key US Labor Reports

The dollar index edges lower from new 2023 high in European session on Wednesday, driven by a partial profit-taking, as the price faced headwinds at 107 zone (50% retracement of 114.72/99.20 downtrend/psychological/weekly Ichimoku cloud top).

The action could be seen as positioning for further advance, as the dollar remains supported by signals that the US Federal Reserve may keep high interest rates for some time to eventually push inflation towards 2% target.

Recent US economic data showed that the economy remains resilient despite negative impact from high borrowing cost that provides relief for the central bank.

Significantly better than expected US JOLTS report showed strong rise in job openings in August, adding to signals that the labor market remains tight and contributing to other positive signals however, ADP (due today) and NFP (Friday) reports are in focus and expected to provide more evidence about the situation in the sector.

Solid numbers from September’s labor report would add to positive signals and offer fresh support to the greenback.

Technical studies on daily chart are firmly bullish but overbought, which opens way for consolidation.

Dips should find firm ground above trendline support at 105.85 to keep larger uptrend intact for fresh push higher, with firm break through 107 resistance zone to signal bullish continuation and expose target at 108.79 (Fibo 61.8% of 114.72/99.20).

Caution on potential break below lower pivots at 105.85/35 (trendline / weekly cloud base) which would risk deeper pullback.

Res: 106.96; 107.13; 107.88; 108.79.

Sup: 106.33; 105.85; 105.38; 105.13.

Eurozone PPI at 0.6% mom, -11.5% yoy in Aug

Eurozone PPI came in at 0.6% mom, -11.5% yoy in August, versus expectation of 0.6% mom, -11.6% yoy. For the month, industrial producer prices increased by 2.5% mom in the energy sector, while prices remained stable for capital goods and for non-durable consumer goods, and prices decreased by -0.1% mom for durable consumer goods and by 0.4% for intermediate goods. Prices in total industry excluding energy decreased by -0.2% mom.

EU PPI came in at 0.5% mom, -10.5% yoy. The biggest monthly increases in industrial producer prices were observed in Ireland (+3.7%), Finland (+2.4%) and Greece (+2.0%), while the largest decreases were recorded in Romania (-1.3%), Slovenia (-0.7%) and Belgium (-0.6%).

Eurozone retail sales falls -1.2% mom in Aug, EU down -0.9% mom

Eurozone retail sales fell -1.2% mom in August, well below expectation of -0.5% mom. Volume of retail trade decreased by -3.0% for automotive fuels, by -1.2% for food, drinks and tobacco and by -0.9% for non-food products.

EU retail sales was down -0.9% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in the Portugal (-3.0%), France (-2.8%) and Belgium (-1.5%). The highest increases were observed in Luxembourg (+1.9%), Poland (+1.7%) and Denmark (+1.6%).

ECB’s Lagarde: Rates reached level for timely return of inflation to target

ECB President Christine Lagarde reiterated in a speech today that current interest rates are at the level to return inflation to target in a timely manner. She also laid out three criteria for future decisions.

"Based on our current assessment, we consider that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our medium-term target", Lagarde said.

Further shedding light on ECB's decision-making framework, Lagarde stated that their "future decisions will continue to be based on these three criteria." She detailed these criteria as: "the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission."

UK PMI services finalized at 49.3, silver lining in easing inflationary pressures

UK PMI Services was finalized at 49.3 in September, a marginal drop from the neutral 50.0 recorded in August. S&P Global's analysis points to persistent declines in both business activity and new ventures, and notably, the pace of job shedding is at its quickest since January 2021. However, the silver lining lies in easing inflationary pressures, marking their lowest in over two years.

Tim Moore, Economics Director at S&P Global Market Intelligence, cited reductions in non-essential business and consumer expenditure as significant dampeners on service sector activity. "A combination of elevated borrowing costs and subdued economic conditions had led to lower new business intake," he remarked.

Decline in export sales, particularly influenced by reduced European demand, further contributed to the sector's woes. Service providers' response has been cautionary, with hiring significantly scaled back given the current uncertainties.

On a positive note, Moore highlighted the diminishing inflationary pressures in the sector, observing, "headline rates of inflation will continue to moderate in the coming months, with service sector input costs rising at the slowest pace for nearly two-and-a-half years." This, coupled with the anticipation of consistent decreases in UK consumer price inflation, could potentially revive demand, instilling a sense of optimism for the future.

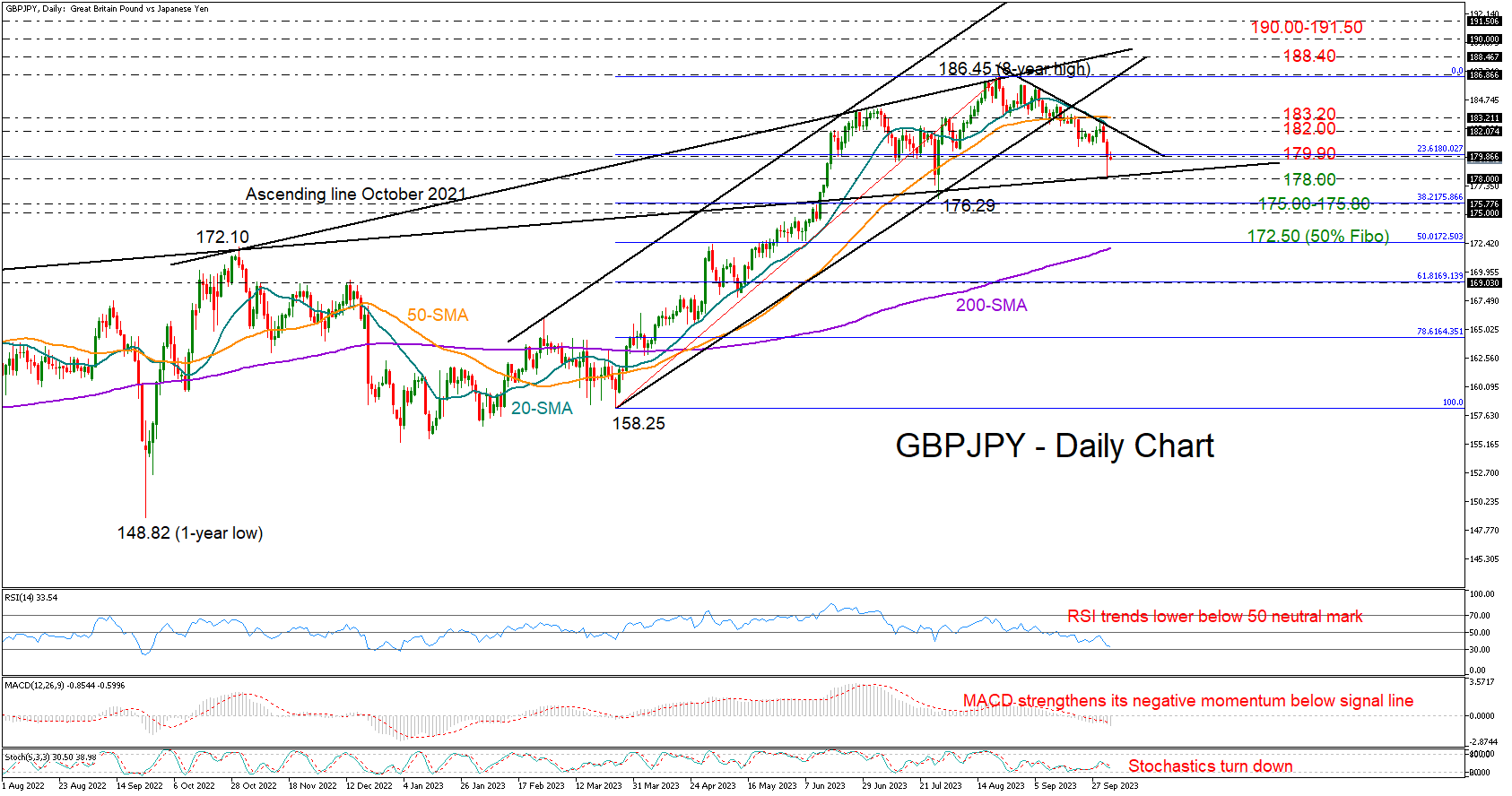

GBPJPY Stays in Bear Mode After Slump

- GBPJPY finds support after sudden fall, but risks remain

- Bearish wave could gain new legs below 178

GBPJPY slumped suddenly to 10-week low of 178.00 on Tuesday in what looked to be a currency intervention from the Bank of Japan.The resistance-turned-support trendline from April 2022 halted the bearish action and lifted the price back to the 179.90 constraining area, but downside risks have not evaporated yet.

The RSI remains negatively charged comfortably below its 50 neutral mark, while the stochastic oscillator has resumed its negative momentum. Meanwhile, the decline in the MACD has picked up pace below the red signal line, suggesting downside pressures may dominate in the short-term.

Should sellers drive below 178.00, the pair might seek shelter within the 175.00-175.80 area, where the 38.2% Fibonacci retracement level of the 158.25-186.45 uptrend is found. A step lower could stretch towards the 50% Fibonacci of 172.50 and the 200-day simple moving average (SMA). If buyers don’t show up there, the bearish wave could strengthen towards the 61.8% Fibonacci of 169.00.

On the upside, the 20-day SMA and the short-term resistance trendline drawn from recent highs could cancel any progress around 182.00. The 50-day SMA could cement that ceiling, preventing a quick rally towards the eight-year high of 186.45. Slightly higher, the bulls could face a noisy trading around the resistance line coming from October 2022 at 188.45. If this proves easy to overcome, the door will open for the 190.00 psychological mark and the 191.50 barrier from 2015.

In summary, GBPJPY bears might have some extra fuel in the tank, with traders expected to engage in new selling tendencies below 178.00.