Sample Category Title

GBP/JPY Weekly Outlook

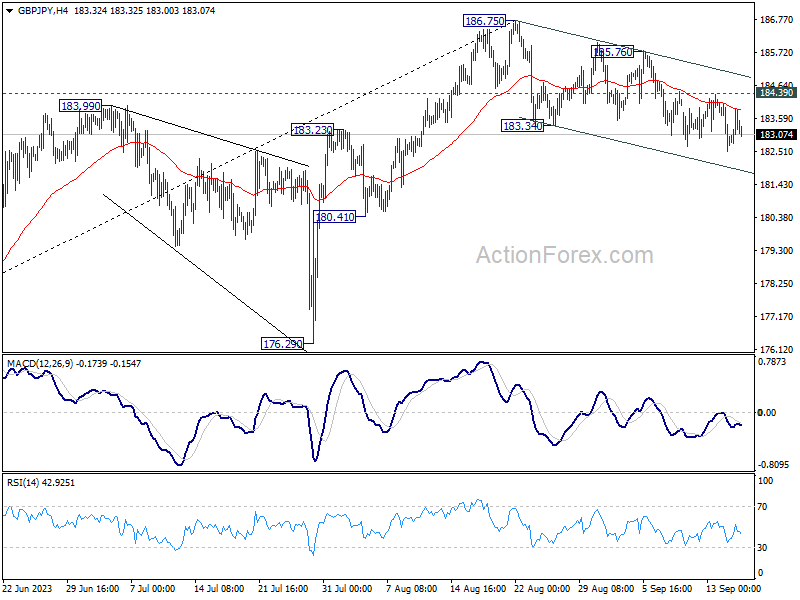

GBP/JPY's choppy decline from 186.75 extended lower last week even though downside momentum has been week. Further fall is expected this week as long as 184.39 resistance holds. Sustained trading below 55 D EMA (now at 182.44) will argue that it's already in a larger scale correction and target 176.29 support next. On the upside, break of 184.39 resistance will argue that the pull back from 186.75 has completed. Intraday bias will be turned back to the upside for 185.76 resistance next.

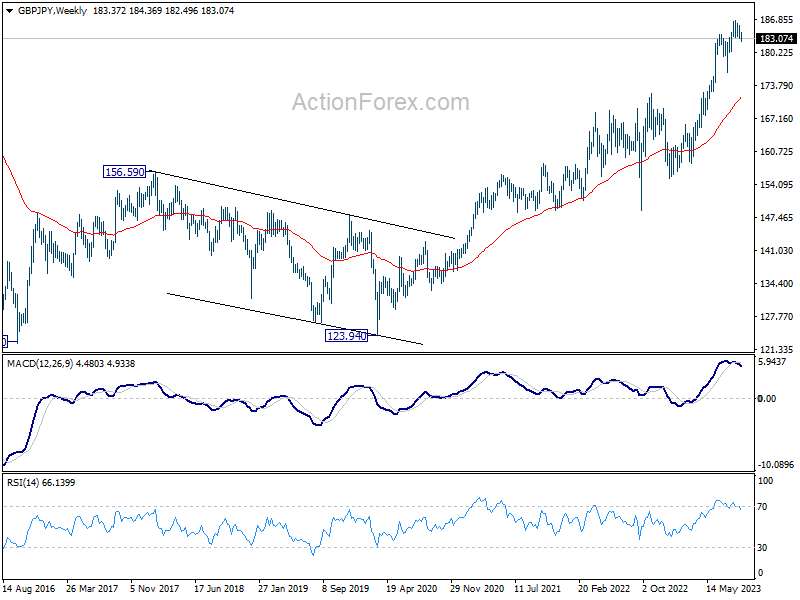

In the bigger picture, as long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and turn outlook neutral for lengthier and deeper consolidations.

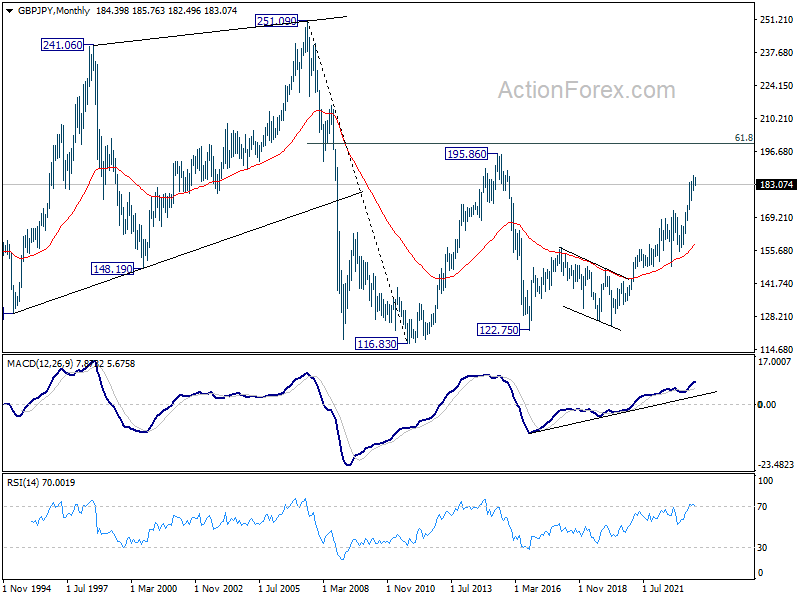

In the longer term picture, rise from 122.75 (2016 low) in still in progress but started lose upside momentum as seen in W MACD. Further rise will remain in favor, though, as long as 176.29 support holds, to retest 195.86 (2015 high).

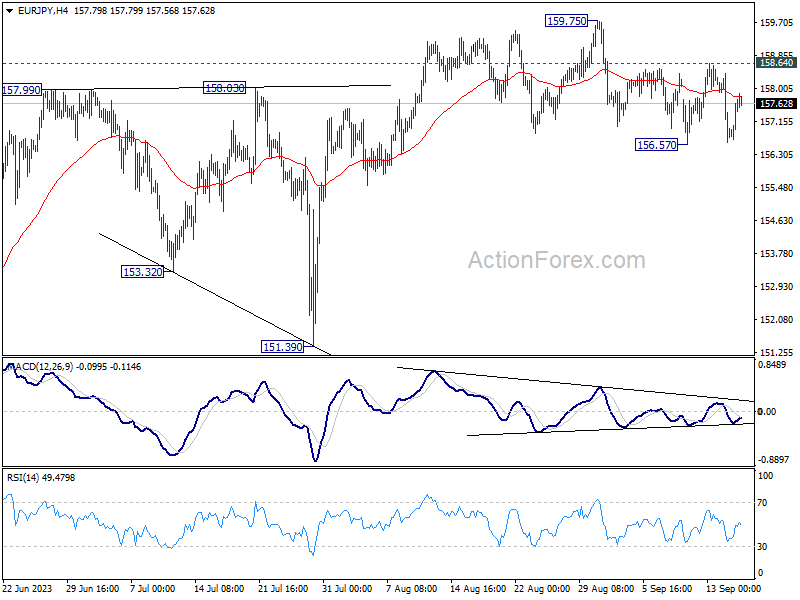

EUR/JPY Weekly Outlook

EUR/JPY engaged in sideway trading above 156.57 last week. Initial bias stays neutral this week first. Risk will be mildly on the downside as long as 158.64 resistance holds. Break of 156.57 support, and sustained trading below 55 D EMA (now at 156.73) will argue that fall from 159.75 is a larger scale correction. Deeper decline would be seen back towards 151.39 support. Nevertheless, above 158.64 would bring retest of 159.75 high instead.

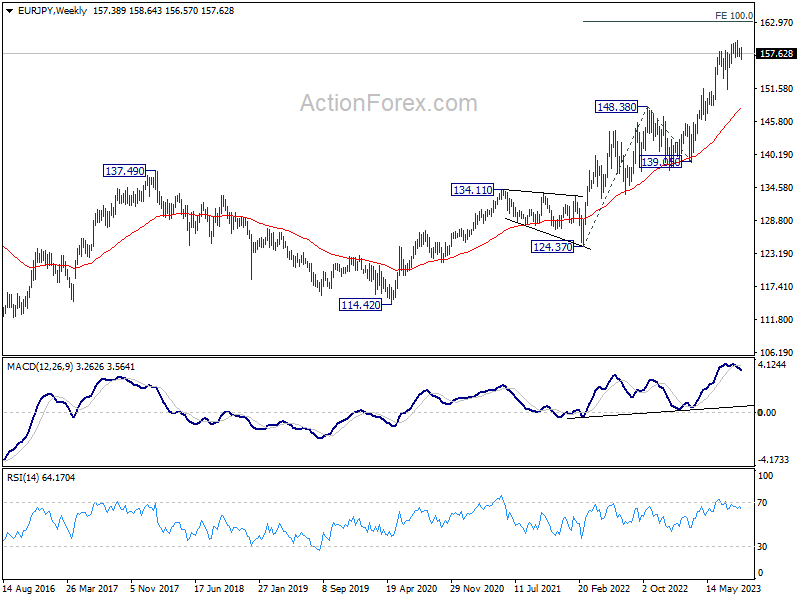

In the bigger picture, as long as 151.39 support holds, rise from 114.42 is still expected to continue. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96.

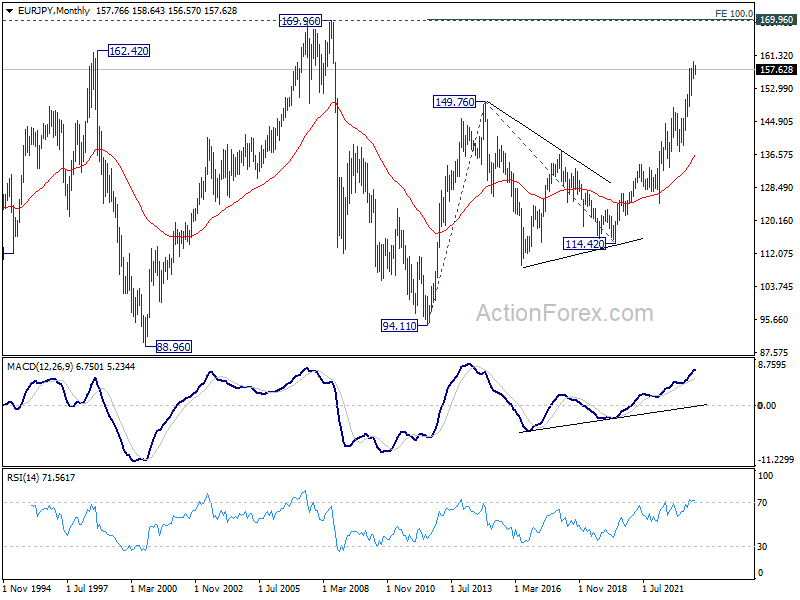

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high).

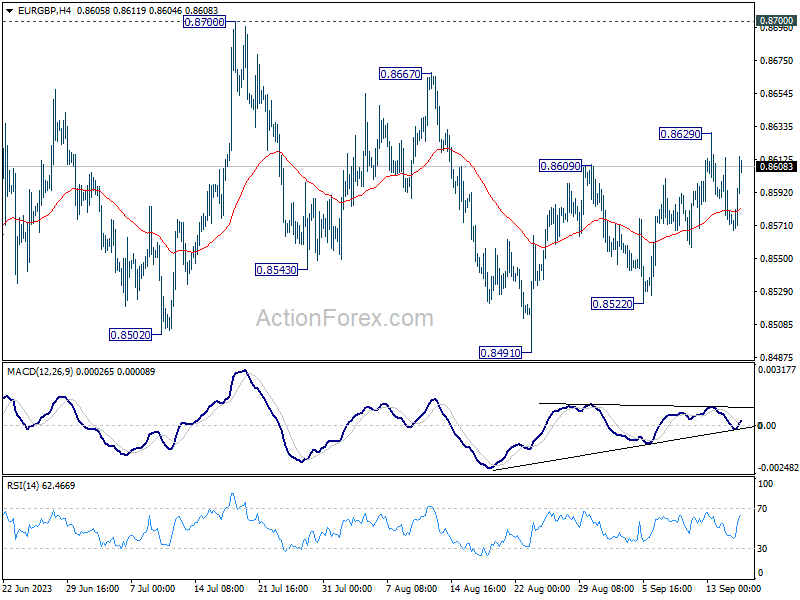

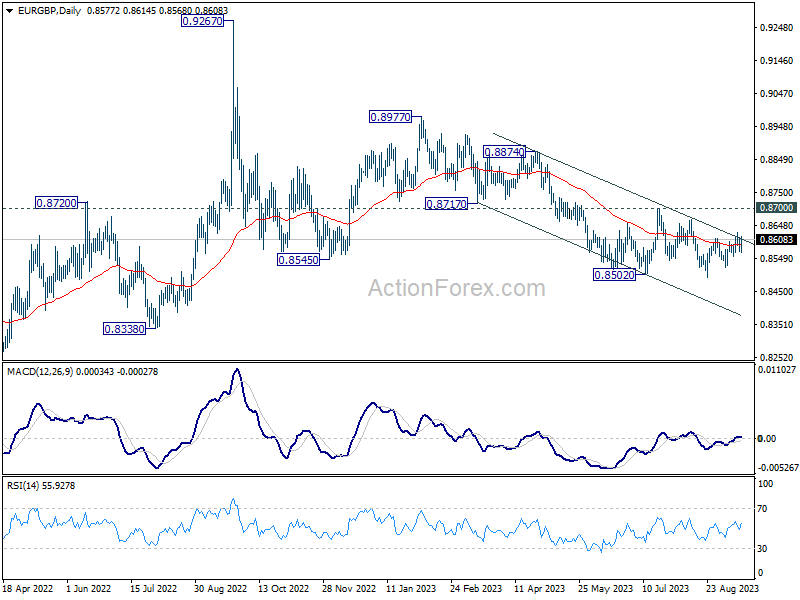

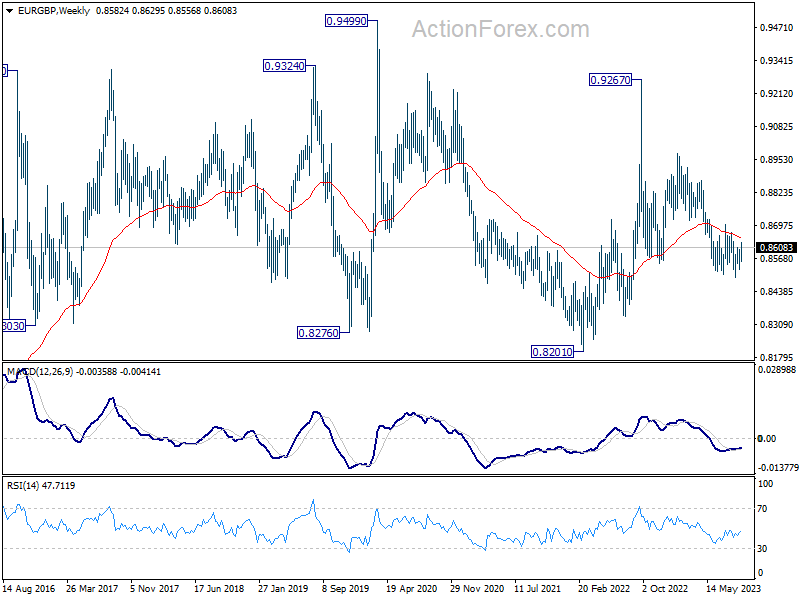

EUR/GBP Weekly Outlook

EUR/GBP edged higher to 0.8629 last week but retreated since then. Initial bias remains neutral this week first, and outlook is unchanged. Price actions from 0.8502 are seen as a corrective pattern, with rise from 0.8491 as the third level. Above 0.8609 will bring further rise to 0.8667/8700 resistance zone. On the downside, below 0.8522 will bring retest of 0.8491 support.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Fall from 0.8977 is seen as the third leg. As long as 0.8700 resistance holds, further decline is still expected. Break of 0.8491 will resume the fall towards 0.8201 (2022 low). Nevertheless, firm break of 0.8700 will now be a sign of bullish reversal.

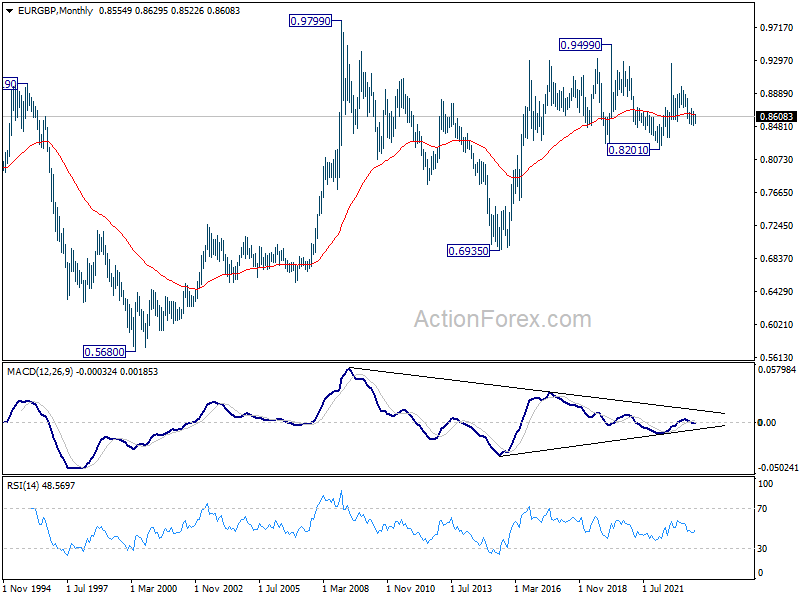

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

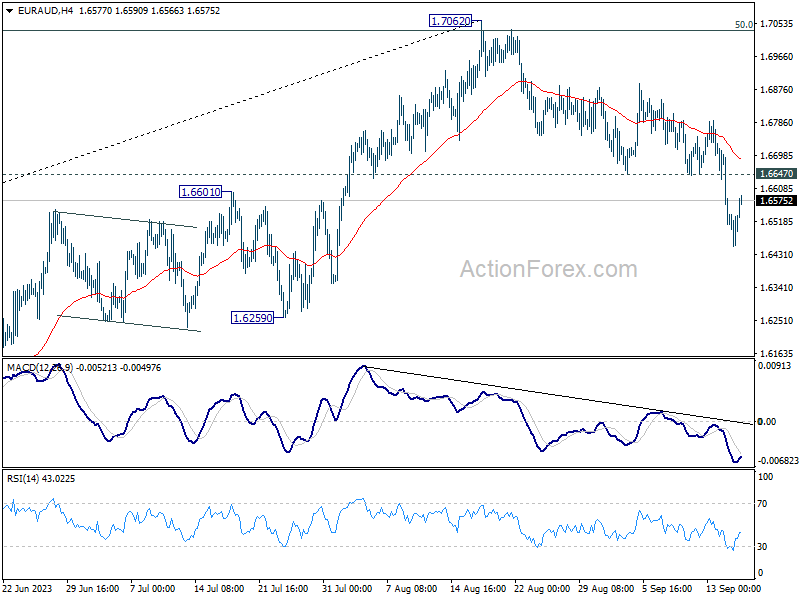

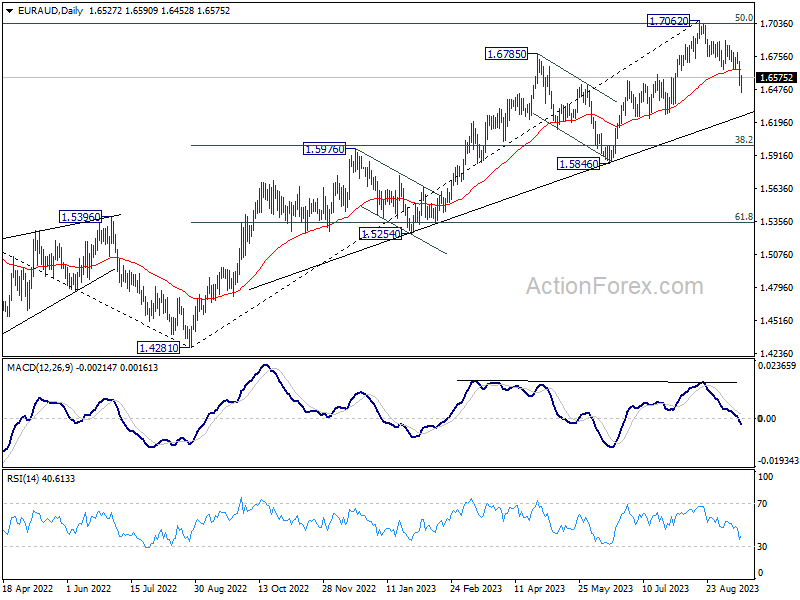

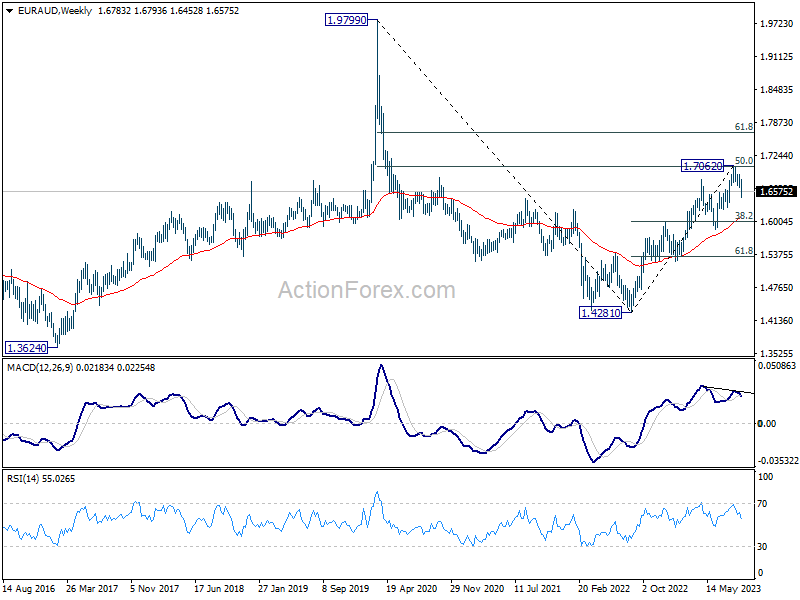

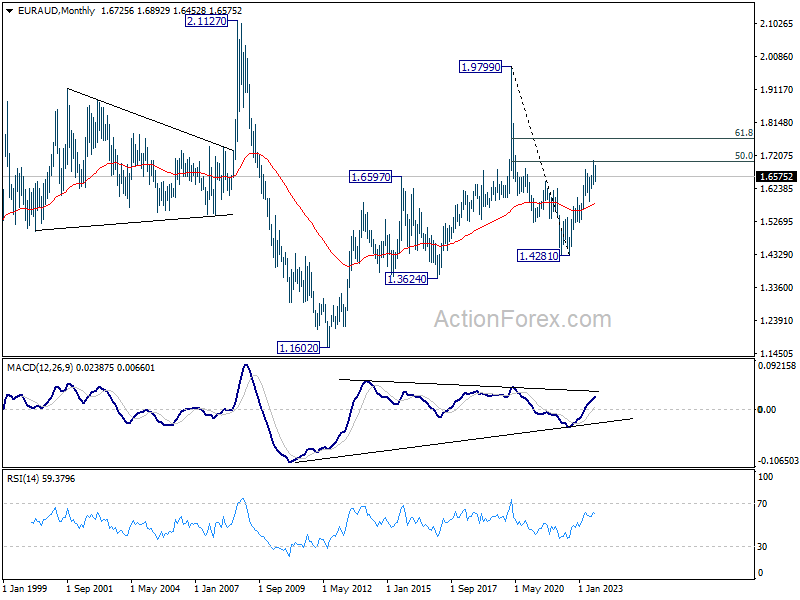

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.7062 extended lower last week and the development argues that it's already in a larger scale correction. Initial bias stays on the downside this week first. Deeper fall would be seen to 1.6000 fibonacci level. On the upside, above 1.6647 support turned resistance will turn intraday bias neutral. But risk will stay on the downside as long as 1.7062 resistance holds.

In the bigger picture, current development argues that fall from 1.7062 is probably correcting whole up trend from 1.4281. Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5846 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

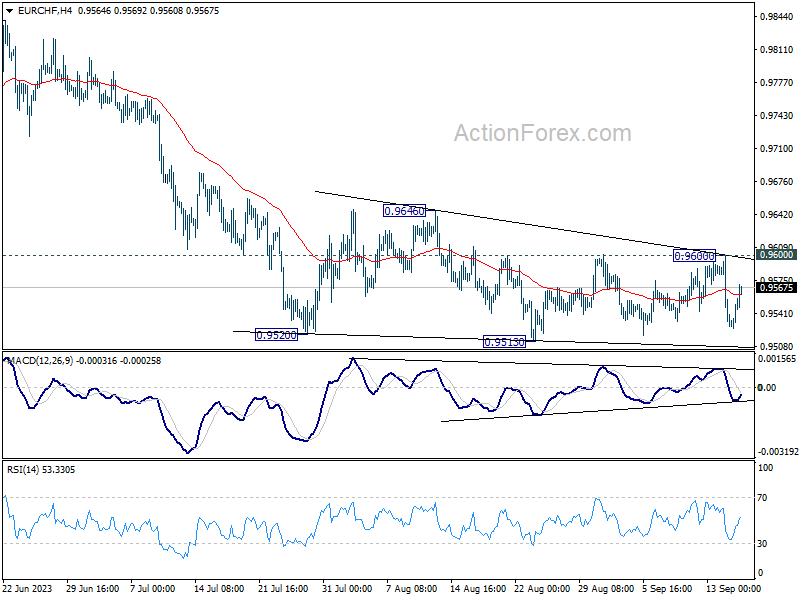

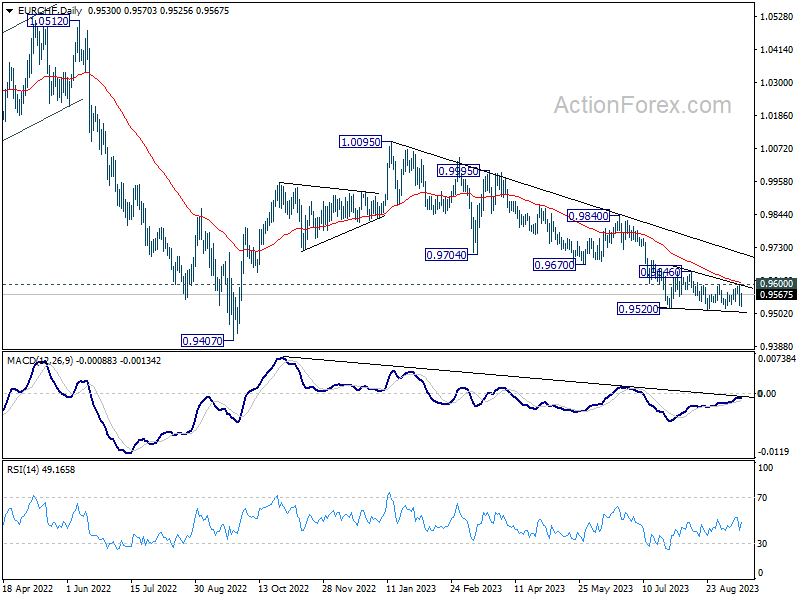

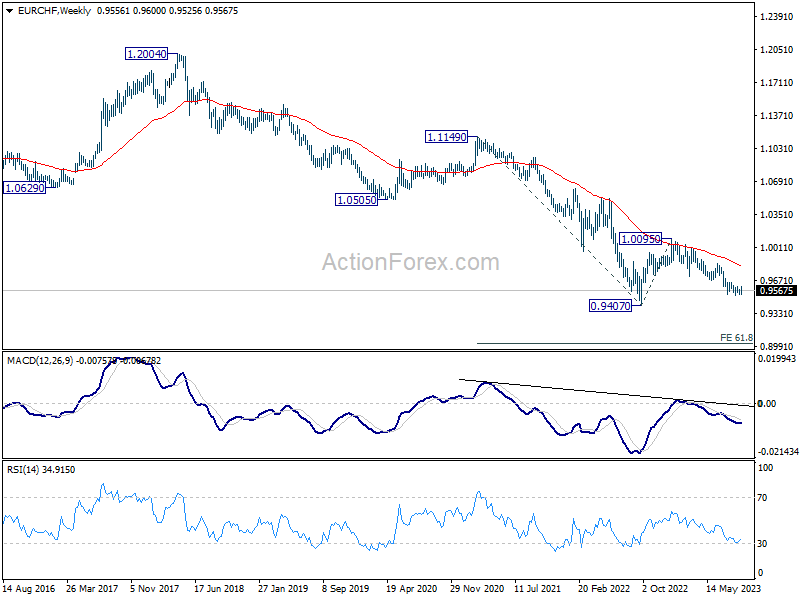

EUR/CHF Weekly Outlook

EUR/CHF's sideway trading continued last week and overall outlook is unchanged. Initial bias stays neutral this week first. As long as 0.9600 resistance holds, downside breakout is in favor. Firm break of 0.9513 will resume larger fall from 1.0095 to 0.9407 low. Nevertheless, on the upside, sustained break of 0.9066 resistance will indicate that strong rebound is underway, and turn bias back to the upside for 0.9840 resistance.

In the bigger picture, medium term outlook is staying bearish as the cross is capped well below falling 55 W EMA (now at 0.9818). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

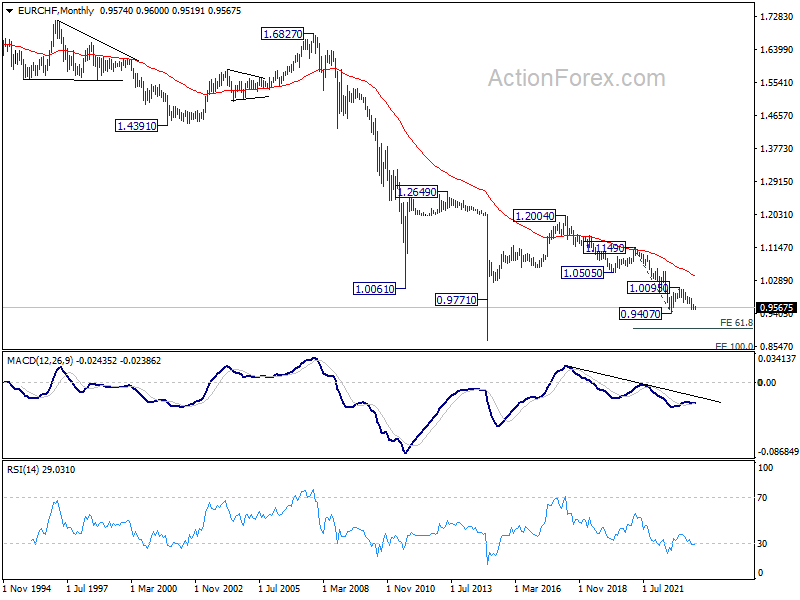

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0391). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: FOMC to Stand Pat, but Keep Door Open to Possibility of Further Hikes

Summary

United States: The Best of Summer Gone, and the New Fall Uncertain

- The Consumer Price Index picked up 0.6% in August—the largest monthly gain since June 2022. The outturn was broadly expected amid the surge in gasoline prices last month. Short-term and long-term consumer inflation expectations declined, suggesting consumers are more convinced that inflation is cooling.

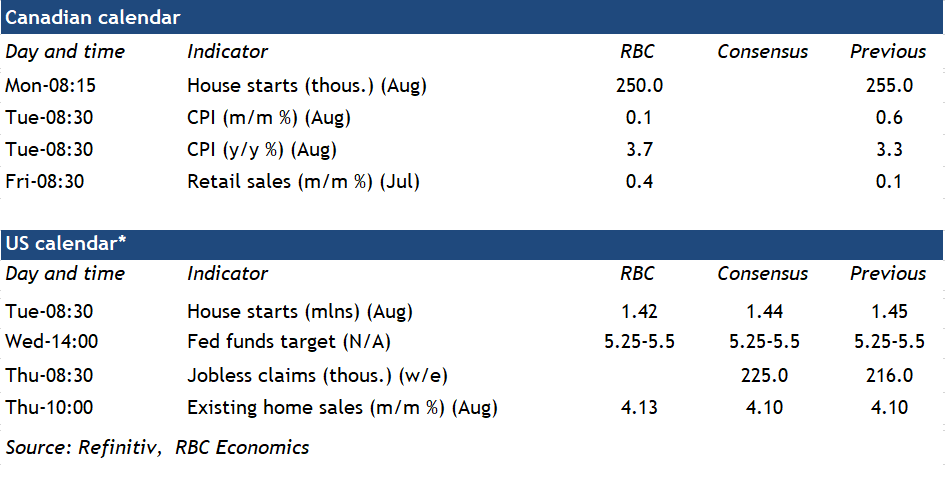

- Next week: Housing Starts (Tue), Existing Home Sales (Thu), Leading Economic Index (Thu)

International: The ECB's Dovish Hike

- Leading into the European Central Bank's (ECB) September assessment of monetary policy, we felt policymakers would opt to end their respective tightening cycle. Needless to say, ECB policymakers delivered another 25 bps of tightening; however, the forward guidance associated with the decision became the larger focus of the meeting.

- Next week: Brazilian Central Bank (Wed), Bank of England (Thu), Bank of Japan (Fri)

Interest Rate Watch: FOMC to Stand Pat, but Keep Door Open to Possibility of Further Hikes

- The FOMC is widely expected to keep the fed funds target rate unchanged at 5.25-5.50% at its upcoming meeting as inflation has more clearly started to slow. However, with price growth still running well-above target, we expect the hold to be delivered with the message that further policy tightening is possible if incoming data warrants it.

Credit Market Insights: How Tight Are Financial Conditions?

- Some recent data point to a tightening and costlier credit market, but how tight are financial conditions broadly? Timely evidence from the Federal Reserve Bank of Chicago suggests national financial conditions are still looser than average and have been easing in recent weeks.

Topic of the Week: Median Household Income Falls in 2022

- The U.S. Census Bureau released its annual Income & Poverty Report this week, which showed that U.S. incomes fell for the third straight year in 2022. Real median household income before taxes fell to $74,580 in 2022, down 2.3% from the 2021 estimate of $76,330.

The Weekly Bottom Line: Canada – Waiting in Inflation Limbo

U.S. Highlights

- The third quarter is shaping up to be the strongest of the year for the U.S. economy, with GDP tracking 3.7% q/q (annualized).

- The August reading of CPI showed inflationary pressures accelerated last month, though the trend remains favorable, with the three-month annualized change on core inflation slipping to 2.4%.

- A 1-2-3 punch of risks lies on the horizon for the U.S. economy. The end of the student debt moratorium, a potential government shutdown, and the UAW strike could all leave a mark on Q4 growth.

Canadian Highlights

- We can’t fault Canadian investors for peeking south of the border for signs on what the Bank of Canada (BoC) is going to do next. The stronger than expected U.S. Consumer Price Index (CPI) print may provide a good guide for Canada’s CPI release next week.

- The BoC has spoken about the stickiness of Canadian inflation as a rationale for its higher for longer interest rate strategy. The expectation for another increase in CPI next week has government yields and mortgage rates stabilizing at higher levels.

- While inflation has been slow to respond to the BoC’s hikes, there has been a clear deceleration in Canadian economic momentum over the last few months. Look no further than the August real estate data, which showed another drop in sales activity and prices.

U.S. – Flying High in Q3, But Headwinds on the Horizon

There were a lot of new data reads on the U.S. economy this week, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

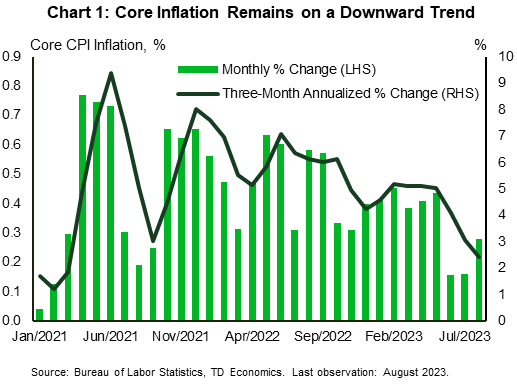

Over half of the gain in headline inflation was due to higher gasoline prices, which rose sharply alongside the recent uptick in oil prices. Meanwhile, the 0.3% m/m gain in core inflation came in a tick above expectations and bucked the trend from the ‘soft’ 0.2% gains seen in both June and July (Chart 1). However, putting these numbers in context, the monthly gain was still the third smallest in nearly two-years. Moreover, the trend on inflation remains favorable, with the three-month annualized pace cooling to 2.4% – the slowest pace of growth since March 2021.

Next week’s interest rate announcement hangs in the balance, where it is widely expected that the Federal Reserve will keep the policy rate unchanged. However, the devil will be in the details. The FOMC will also release revised economic projections, where at a minimum, they’re likely to lift the near-term growth forecast and lower the unemployment rate projection to account for the more persistent strength since the June update. The big question will be if policymakers see the near-term resilience as a source of more persistent inflationary pressures, and whether that alters the expected future path of the fed funds rate. While it is very unlikely that the FOMC would lift its terminal rate projection of 5.75% for 2023, a shallower rate cut trajectory could be signaled, reinforcing the need for rates to remain higher for longer.

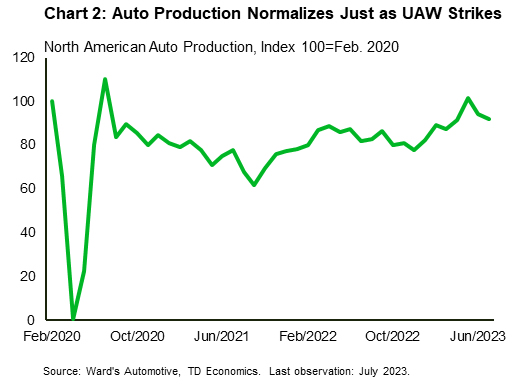

The Fed needs to thread a very small needle in its communication next week. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

Canada – Waiting in Inflation Limbo

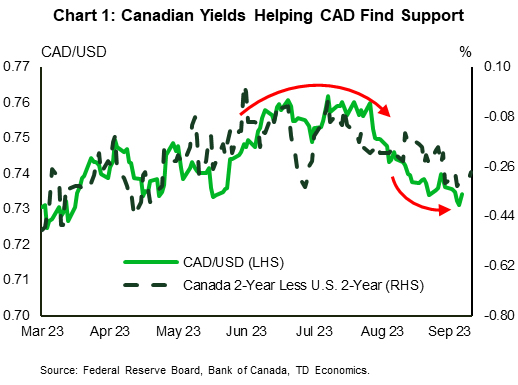

We can't fault Canadian investors for peeking south of the border for an indication of what the Bank of Canada (BoC) is going to do next. The stronger than expected U.S. CPI print may provide a good guide for Canada's CPI release next week. The expected rebound in Canadian inflation has raised bets of another BoC hike by year-end. Canadian yields have subsequently kept pace with their U.S. equivalents this week, putting a floor under the loonie at 73 U.S. cents (Chart 1).

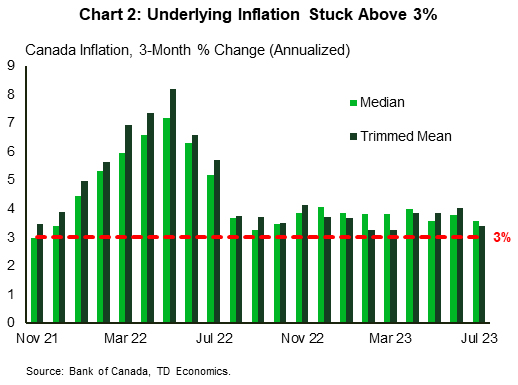

Our expectation is that Canadian consumer price inflation will show a hefty increase – hitting 3.8% year-on-year (y/y), from 3.3% y/y in July and 2.8% y/y in June. The 5% month-on-month pop in the price of gasoline will once again be the culprit for rising CPI in August. But given its volatility, the BoC would be right to look straight past that headline print and focus on the movement of core inflation. Unfortunately, we aren't expecting much progress here. There is no longer any downdraft coming from base effects and the three-month average of monthly price movements in the BoC's two core measures appears stuck at the mid-3% level (Chart 2). No wonder the BoC has been reinforcing that investors shouldn't rule out more rate hikes.

Part of the rationale for the BoC's hawkishness has been the resiliency of the Canadian consumer. Given an improved financial position, consumers have been able to withstand the impact of higher rates. Adding to this narrative was the release of Canadian household wealth data, which revealed an overall improvement in net worth. Canadian's wealth grew by a whopping $256 billion in 2023 Q2. This only adds to the financial cushion of Canadians, who already have approximately $140 billion in excess savings that have yet to be spent. This could pose a problem for the BoC if consumers decide to spend their newfound wealth.

The one area of the economy that has been most responsive to the BoC's policy actions has been the real estate market. When the BoC hit pause in January 2023, we saw a surge in real estate activity in the spring, sending the market decisively back into sellers' territory. But once the BoC started hiking again in June, mortgage rates started to rise, pushing would-be buyers to the sidelines. Today's data confirm a continuation of that trend, with sales down another 4.1% month-on-month in August. With the rise in listings bringing greater balance to the market, house prices dropped 2.3% on the month, and 5.2% in the last three months.

While there has been a clear slowing in spending, employment, and the real estate market, the better financial position of Canadians and stubbornness of inflation make the BoC's job more challenging. And although we don't think the BoC needs to raise rates again this year, the Bank will likely keep the door open in case economic data surprise again to the upside.

Week Ahead – Fed, BoE, BoJ, SNB, SARB, CBRT and More to Look Forward To

-

- Federal Reserve could be cautious as data continues to show economic resilience

- BoE may raise rates for the last time in this cycle

- BoJ eyed for more clues on interest rates after recent hints

US

The main event of the week will be the September FOMC meeting. Powell and Co. are expected to keep rates steady but may still signal one more rate increase is coming. Too many upside surprises with service/jobs/consumer readings will keep the Fed upbeat on the economy, forcing them to revise up their GDP forecasts and to price in one more rate hike.

Investors will also pay close attention to a steady dose of housing data. On Tuesday, the release of both building permits and housing starts should show the housing market is stabilizing. On Thursday, weekly jobless claims are expected to show the labor market slowdown is slowly happening and existing home sales are steadying. The key economic release of the weak is the flash PMIs, which are expected to show the economy is losing momentum.

Eurozone

The ECB probably brought an end to its tightening cycle at its September meeting but it doesn’t end there, with traders now switching their focus to when the easing cycle will begin. Lagarde was keen to stress that they could hike again if necessary but the likelihood is that they won’t.

Final HICP inflation data will be of interest on Tuesday, although revisions are not common and when they do happen, they’re usually small. Flash PMIs at the end of the week for the eurozone, Germany, and France will also be eyed.

UK

It feels like a pivotal week for the UK, with inflation figures for August being released on Wednesday, one day before the Bank of England rate decision. While the central bank is believed to be near the end of its tightening cycle – in part due to the comments from policymakers in front of the Treasury Select Committee recently – one more on Thursday looks highly likely.

And the inflation data a day earlier is not expected to complicate the discussion, with the headline CPI seen rising to 7.1% – driven by energy prices as we’ve seen elsewhere – and the core reading falling slightly to 6.8%. I can’t imagine that will inspire a majority to declare job done or even consider pausing just yet. Retail sales and flash PMIs will also be released on Friday.

Russia

A quiet week following the CBR meeting on Friday, at which the central bank raised the Key Rate by another 100 basis points to 13%. Resurgent inflation and a slumping rouble is driving the central bank’s tightening efforts and more may be needed. PPI data on Wednesday will be eyed for signs of price pressures cooling, something we haven’t seen much of yet. We’ll also hear from various CBR policymakers throughout the week which will be interesting under the circumstances.

South Africa

The SARB is one of the few central banks that is not expected to raise interest rates next week, with the Repo Rate seen staying at 8.25%. Inflation data released a day earlier could spark a more lively debate but with headline and core both at 4.7% – well within the 3-6% target range – it probably won’t change the outcome. Retail sales figures will also be released on Wednesday.

Turkey

The CBRT meeting on Thursday brings a wide array of possibilities. Markets are expecting another 5% rate hike, taking the Repo Rate to 30% but expectations will vary massively. With inflation at almost 59% and the lira near record lows, there’s clearly a lot more to do to clean up the mess left by the previous Governor.

Switzerland

Inflation is back below 2% – 1.6% in August – and yet the SNB is widely expected to raise interest rates by 25 basis points on Thursday. It’s expected to be the final hike in the cycle, leaving the Policy Rate at 2%, with the first cut not priced in until late next year.

China

The only data to focus on will be the PBoC decision on the 1-year and 5-year loan prime rates on Wednesday. After they left the 1-year medium-term lending rate unchanged at 2.50% on Friday following a reduction on the commercial banks’ reserve requirements ratio by 25 basis points, it is likely that the 1-year and 5-year loan prime rate rates will remain unchanged at 3.45% and 4.2% respectively.

Chinese economic data recently has started to improve. Retail sales in August rose 4.6% y/y, above the consensus of 3%, and surpassing July’s 2.5%; the strongest pace of growth since May. August’s industrial production also managed to beat expectations of 3.9% with a growth of 4.5% y/y; the highest reading since April.

All things considered, the latest set of economic data suggests that the risk of a deflationary spiral in China has abated by another notch.

India

No key data releases.

Australia

On Tuesday minutes of the recent RBA meeting will be released. At the last monetary policy meeting, the RBA extended its interest rate pause at 4.1% for the third consecutive meeting. Market participants will be looking for more clues on whether there will be further hikes after the latest jobs data rebounded following a surprise drop in July.

Next up, flash services and manufacturing PMIs for September will be released on Friday. A deeper contraction in the services PMI is expected, falling to 46.5 from 47.8 in August. That would be the third consecutive month of contraction in the services sector. Meanwhile, manufacturing is expected to remain almost unchanged at 49.5 versus 49.6 in August.

New Zealand

Two key data releases to take note of. Firstly, Q2 GDP on Thursday could see a dip to 1.2% y/y from 2.2% in Q1. That would be the weakest annualized quarterly growth since Q2 2022.

Balance of trade data for August is due on Friday with the trade deficit expected to narrow slightly to NZ$-0.9 billion from NZ$-1.11 billion in July. Imports are seen falling to NZ$6.1 billion from NZ$6.56 billion recorded in July.

Japan

A pivotal week with inflation data and the Bank of Japan’s monetary policy decision. After BoJ Governor Ueda’s recent “quiet exit” comment from the current ultra-easy monetary policy stance, expectations for an earlier exit have dialed up with the first interest rate hike seen as early as Q1 2024.

Therefore, the upcoming inflation numbers for August out on Friday will be scrutinized closely. The core inflation rate is expected to be almost unchanged at 3% y/y versus 3.1% in July. That would be the eighteenth consecutive month that it exceeds BoJ’s target of 2%. Interestingly, the core-core inflation rate (excluding fresh food & energy) is expected to accelerate further to 4.4% y/y in August from 4.3% in July.

The BoJ’s monetary policy decision will be on the same day. No change is expected after the “flexible” yield curve control policy on the 10-year JGB yield was enacted at the previous meeting. No release of the latest economic forecasts for Japan, hence all ears will be on Ueda’s press conference for hints on how confident he is on the inflation trajectory.

Singapore

Balance of trade data for August will be out on Monday with export growth expected to be still in contractionary mode albeit at a slower pace, -15.8% y/y from -20.2% in July. This would be the 11th straight month of contraction.

Economic Calendar

Saturday, Sept. 16

Economic Events

- Global Geothermal Conference in Beijing

- Informal meeting of EU finance ministers concludes in Spain

Sunday, Sept. 17

Economic Events

- No major events

Monday, Sept. 18

Economic Data/Events

- US cross-border investment, NY Fed services business activity, NAHB housing market index

- Canada housing starts

- Singapore trade

- Russian and Chinese foreign ministers to talk in Moscow

- RBA Deputy Governor Bullock becomes central bank chief

- German Finance Minister Lindner speaks at the Bloomberg Future of Finance Conference in Frankfurt

- Ukraine defense ministers meet in Germany

Tuesday, Sept. 19

Economic Data/Events

- US housing starts

- Canada CPI

- Eurozone CPI

- Mexico international reserves

- RBA releases minutes of this month’s policy meeting

- General debate starts at the United Nations’ 78th general assembly

- OECD releases interim economic outlook report on the global economy

- New Zealand PM Hipkins debates National Party leader Christopher Luxon

- ECB’s Elderson addresses conference at Goethe-Universität/Center for Financial Studies in Frankfurt

- BOC Deputy Governor Kozicki speaks at the University of Regina

- EU European affairs ministers to meet in Brussels

Wednesday, Sept. 20

Economic Data/Events

- FOMC Rate Decision: Expected to maintain benchmark lending rate target at 5.25% to 5.5%

- China loan prime rates

- Eurozone new car registrations

- Japan trade

- South Africa retail sales, CPI

- UK CPI

- Bank of Canada issues summary of this month’s policy meeting

- ECB’s Elderson speaks at Springtij Forum 2023 in Netherlands

- FedEx reports earnings

Thursday, Sept. 21

Economic Data/Events

- US leading index, initial jobless claims, existing home sales

- BOE Rate Decision: Expected to raise rates by 25bps to 5.50%

- Eurozone consumer confidence

- New Zealand GDP

- Norway rate decision: Expected to raise rates by 25bps to 4.25%

- South Africa rate decision: Expected to keep rates steady at 8.25%

- Spain trade

- Sweden rate decision: Expected to raise rates by 25bps to 4.00%

- Switzerland rate decision: Expected to raise rates by 25bps to 2.00%

- Turkey rate decision: Expected to raise rates by 500bps to 30.00%

- ECB’s Schnabel speaks at the ECB Annual Research Conference

- ECB chief economist Lane addresses Money Marketeers of New York University in New York

Friday, Sept. 22

Economic Data/Events

- US Sept flash manufacturing PMI: 47.9e v 47.9 prior; Services PMI: No est v 50.5 prior

- Australia manufacturing PMI, services PMI

- Canada retail sales

- European flash PMIs: Eurozone, Germany, France, and the UK

- Japan BOJ rate decision: No change expected with rates, to keep ultra-easy policy

- Japan CPI and preliminary PMIs

- New Zealand trade

- Spain GDP

- Taiwan jobless rate

- ECB VP de Guindos addresses online event

- China’s Bund Summit

- Atlantic Council’s “Transatlantic Forum on GeoEconomics” in Berlin, with German Economy Minister Habeck and others

- Riksbank Governor Thedeen speaks on “Why is the Swedish krona so weak” in separate events

Sovereign Rating Updates

- Germany (S&P)

- Poland (Moody’s)

- Finland (DBRS)

- France (DBRS)

Summary 9/18 – 9/22

Monday, Sep 18, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 47.8 | |

| 23:01 | GBP | Rightmove House Price Index M/M Sep | -1.90% | |

| 12:15 | CAD | Housing Starts Aug | 257K | 255K |

| 12:30 | CAD | Industrial Product Price M/M Aug | 0.50% | 0.40% |

| 12:30 | CAD | Raw Material Price Index Aug | 3.80% | 3.50% |

| 14:00 | USD | NAHB Housing Market Index Sep | 50 | 50 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | |

| Forecast: | Previous: 47.8 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Sep | |

| Forecast: | Previous: -1.90% | ||

| 12:15 | CAD | Housing Starts Aug | |

| Forecast: 257K | Previous: 255K | ||

| 12:30 | CAD | Industrial Product Price M/M Aug | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 12:30 | CAD | Raw Material Price Index Aug | |

| Forecast: 3.80% | Previous: 3.50% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | |

| Forecast: 50 | Previous: 50 | ||

Tuesday, Sep 19, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes | ||

| 06:00 | CHF | Trade Balance (CHF) Aug | 4.23B | 3.13B |

| 08:00 | EUR | Current Account (EUR) Jul | 30.2B | 35.8B |

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | 5.30% | 5.30% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | 5.30% | 5.30% |

| 12:30 | USD | Building Permits Aug | 1.45M | 1.44M |

| 12:30 | USD | Housing Starts Aug | 1.44M | 1.45M |

| 12:30 | CAD | CPI M/M Aug | 0.10% | 0.60% |

| 12:30 | CAD | CPI Y/Y Aug | 3.80% | 3.30% |

| 12:30 | CAD | CPI Median Y/Y Aug | 3.70% | 3.70% |

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 3.50% | 3.60% |

| 12:30 | CAD | CPI Common Y/Y Aug | 4.80% | 4.80% |

| 22:45 | NZD | Current Account (NZD) Q2 | -4.40B | -5.22B |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.44T | -0.56T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Minutes | |

| Forecast: | Previous: | ||

| 06:00 | CHF | Trade Balance (CHF) Aug | |

| Forecast: 4.23B | Previous: 3.13B | ||

| 08:00 | EUR | Current Account (EUR) Jul | |

| Forecast: 30.2B | Previous: 35.8B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | |

| Forecast: 5.30% | Previous: 5.30% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | |

| Forecast: 5.30% | Previous: 5.30% | ||

| 12:30 | USD | Building Permits Aug | |

| Forecast: 1.45M | Previous: 1.44M | ||

| 12:30 | USD | Housing Starts Aug | |

| Forecast: 1.44M | Previous: 1.45M | ||

| 12:30 | CAD | CPI M/M Aug | |

| Forecast: 0.10% | Previous: 0.60% | ||

| 12:30 | CAD | CPI Y/Y Aug | |

| Forecast: 3.80% | Previous: 3.30% | ||

| 12:30 | CAD | CPI Median Y/Y Aug | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Aug | |

| Forecast: 3.50% | Previous: 3.60% | ||

| 12:30 | CAD | CPI Common Y/Y Aug | |

| Forecast: 4.80% | Previous: 4.80% | ||

| 22:45 | NZD | Current Account (NZD) Q2 | |

| Forecast: -4.40B | Previous: -5.22B | ||

| 23:50 | JPY | Trade Balance (JPY) Aug | |

| Forecast: -0.44T | Previous: -0.56T | ||

Wednesday, Sep 20, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Aug | 0.00% | |

| 06:00 | EUR | Germany PPI M/M Aug | 0.20% | -1.10% |

| 06:00 | EUR | Germany PPI Y/Y Aug | -12.80% | -6.00% |

| 06:00 | GBP | CPI M/M Aug | 0.70% | -0.40% |

| 06:00 | GBP | CPI Y/Y Aug | 7.10% | 6.80% |

| 06:00 | GBP | Core CPI Y/Y Aug | 6.80% | 6.90% |

| 06:00 | GBP | RPI M/M Aug | 0.90% | -0.60% |

| 06:00 | GBP | RPI Y/Y Aug | 9.30% | 9.00% |

| 06:00 | GBP | PPI Input M/M Aug | 0.20% | -0.40% |

| 06:00 | GBP | PPI Input Y/Y Aug | -3.30% | |

| 06:00 | GBP | PPI Output M/M Aug | 0.20% | 0.10% |

| 06:00 | GBP | PPI Output Y/Y Aug | -0.80% | |

| 06:00 | GBP | PPI Core Output M/M Aug | 0.10% | |

| 06:00 | GBP | PPI Core Output Y/Y Aug | 2.30% | |

| 07:00 | CHF | SECO Economic Forecasts | ||

| 14:30 | USD | Crude Oil Inventories | 4.0M | |

| 18:00 | USD | Fed Rate Decision | 5.50% | 5.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 22:45 | NZD | GDP Q/Q Q2 | 0.40% | -0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Aug | |

| Forecast: | Previous: 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Aug | |

| Forecast: 0.20% | Previous: -1.10% | ||

| 06:00 | EUR | Germany PPI Y/Y Aug | |

| Forecast: -12.80% | Previous: -6.00% | ||

| 06:00 | GBP | CPI M/M Aug | |

| Forecast: 0.70% | Previous: -0.40% | ||

| 06:00 | GBP | CPI Y/Y Aug | |

| Forecast: 7.10% | Previous: 6.80% | ||

| 06:00 | GBP | Core CPI Y/Y Aug | |

| Forecast: 6.80% | Previous: 6.90% | ||

| 06:00 | GBP | RPI M/M Aug | |

| Forecast: 0.90% | Previous: -0.60% | ||

| 06:00 | GBP | RPI Y/Y Aug | |

| Forecast: 9.30% | Previous: 9.00% | ||

| 06:00 | GBP | PPI Input M/M Aug | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 06:00 | GBP | PPI Input Y/Y Aug | |

| Forecast: | Previous: -3.30% | ||

| 06:00 | GBP | PPI Output M/M Aug | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 06:00 | GBP | PPI Output Y/Y Aug | |

| Forecast: | Previous: -0.80% | ||

| 06:00 | GBP | PPI Core Output M/M Aug | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | |

| Forecast: | Previous: 2.30% | ||

| 07:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 4.0M | ||

| 18:00 | USD | Fed Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 22:45 | NZD | GDP Q/Q Q2 | |

| Forecast: 0.40% | Previous: -0.10% | ||

Thursday, Sep 21, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 9.8B | 3.5B |

| 07:30 | CHF | SNB Interest Rate Decision | 2.00% | 1.75% |

| 11:00 | GBP | BoE Interest Rate Decision | 5.50% | 5.25% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 8--0--1 | 8--0--1 |

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.00% | -0.10% |

| 12:30 | USD | Initial Jobless Claims (Sep 15) | 222K | 220K |

| 12:30 | USD | Philadelphia Fed Survey Sep | -0.7 | 12 |

| 12:30 | USD | Current Account (USD) Q2 | -220B | -219B |

| 14:00 | USD | Existing Home Sales Aug | 4.10M | 4.07M |

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -16.5 | -16 |

| 14:30 | USD | Natural Gas Storage | 57B | |

| 22:45 | NZD | Trade Balance (NZD) Aug | -1107M | |

| 23:00 | AUD | Manufacturing PMI Sep P | 49.6 | |

| 23:00 | AUD | Services PMI Sep P | 47.8 | |

| 23:01 | GBP | GfK Consumer Confidence Sep | -27 | -25 |

| 23:30 | JPY | National CPI Y/Y Aug | 3.30% | |

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Aug | 3.00% | 3.10% |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Aug | 4.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | |

| Forecast: 9.8B | Previous: 3.5B | ||

| 07:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 2.00% | Previous: 1.75% | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 8--0--1 | Previous: 8--0--1 | ||

| 12:30 | CAD | New Housing Price Index M/M Aug | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 15) | |

| Forecast: 222K | Previous: 220K | ||

| 12:30 | USD | Philadelphia Fed Survey Sep | |

| Forecast: -0.7 | Previous: 12 | ||

| 12:30 | USD | Current Account (USD) Q2 | |

| Forecast: -220B | Previous: -219B | ||

| 14:00 | USD | Existing Home Sales Aug | |

| Forecast: 4.10M | Previous: 4.07M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | |

| Forecast: -16.5 | Previous: -16 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 57B | ||

| 22:45 | NZD | Trade Balance (NZD) Aug | |

| Forecast: | Previous: -1107M | ||

| 23:00 | AUD | Manufacturing PMI Sep P | |

| Forecast: | Previous: 49.6 | ||

| 23:00 | AUD | Services PMI Sep P | |

| Forecast: | Previous: 47.8 | ||

| 23:01 | GBP | GfK Consumer Confidence Sep | |

| Forecast: -27 | Previous: -25 | ||

| 23:30 | JPY | National CPI Y/Y Aug | |

| Forecast: | Previous: 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Aug | |

| Forecast: 3.00% | Previous: 3.10% | ||

| 23:30 | JPY | National CPI ex Food Energy Y/Y Aug | |

| Forecast: | Previous: 4.30% | ||

Friday, Sep 22, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | |

| 00:30 | JPY | Manufacturing PMI Sep P | 49.9 | 49.6 |

| 06:00 | GBP | Retail Sales M/M Aug | 0.50% | -1.20% |

| 07:15 | EUR | France Manufacturing PMI Sep P | 46.00 | 46.00 |

| 07:15 | EUR | France Services PMI Sep P | 46.00 | 46.00 |

| 07:30 | EUR | Germany Manufacturing PMI Sep P | 39.5 | 39.1 |

| 07:30 | EUR | Germany Services PMI Sep P | 47.1 | 47.3 |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | 44.0 | 43.5 |

| 08:00 | EUR | Eurozone Services PMI Sep P | 47.5 | 47.9 |

| 08:30 | GBP | Manufacturing PMI Sep P | 43.0 | 43.0 |

| 08:30 | GBP | Services PMI Sep P | 49.0 | 49.5 |

| 12:30 | CAD | Retail Sales M/M Jul | 0.10% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | -0.80% | |

| 13:45 | USD | Manufacturing PMI Sep P | 47.8 | 47.9 |

| 13:45 | USD | Services PMI Sep P | 50.3 | 50.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: -0.10% | Previous: -0.10% | ||

| 00:30 | JPY | Manufacturing PMI Sep P | |

| Forecast: 49.9 | Previous: 49.6 | ||

| 06:00 | GBP | Retail Sales M/M Aug | |

| Forecast: 0.50% | Previous: -1.20% | ||

| 07:15 | EUR | France Manufacturing PMI Sep P | |

| Forecast: 46.00 | Previous: 46.00 | ||

| 07:15 | EUR | France Services PMI Sep P | |

| Forecast: 46.00 | Previous: 46.00 | ||

| 07:30 | EUR | Germany Manufacturing PMI Sep P | |

| Forecast: 39.5 | Previous: 39.1 | ||

| 07:30 | EUR | Germany Services PMI Sep P | |

| Forecast: 47.1 | Previous: 47.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | |

| Forecast: 44.0 | Previous: 43.5 | ||

| 08:00 | EUR | Eurozone Services PMI Sep P | |

| Forecast: 47.5 | Previous: 47.9 | ||

| 08:30 | GBP | Manufacturing PMI Sep P | |

| Forecast: 43.0 | Previous: 43.0 | ||

| 08:30 | GBP | Services PMI Sep P | |

| Forecast: 49.0 | Previous: 49.5 | ||

| 12:30 | CAD | Retail Sales M/M Jul | |

| Forecast: | Previous: 0.10% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | |

| Forecast: | Previous: -0.80% | ||

| 13:45 | USD | Manufacturing PMI Sep P | |

| Forecast: 47.8 | Previous: 47.9 | ||

| 13:45 | USD | Services PMI Sep P | |

| Forecast: 50.3 | Previous: 50.5 | ||

U.S. Fed to Hold the Line on Rates as BoC Awaits Inflation Data

The U.S. Federal Reserve is widely expected to hold the Fed funds rate at the 5.25-5.5% range next week. U.S. economic growth data remains exceptionally strong with GDP growth tracking a 3%+ rate in Q3 and employment is rising solidly. Still, job openings and quit rates have continued to trend lower, suggesting labour demand is continuing to soften under the surface. Indeed, the unemployment rate ticked up to 3.8% in August. More important, interest rates are now at levels ‘restrictive’ enough to cool the economy and inflation pressures have moderated significantly. The Fed remains firmly focused on the data and won’t hesitate to lift the interest rate again if necessary (particularly if inflation shows signs of reaccelerating). But not next week.

The Bank of Canada is also watching inflation closely with August CPI data to be released next week. As in the U.S., higher energy prices will push headline price growth higher. We expect a 3.7% year-over-year rate in August, up from 3.3% in July. Grocery prices will remain high, but the pace of growth has been edging lower. And mortgage interest costs will continue to drive a disproportionate share of overall price growth (this accounted for over a quarter of total year-over-year price growth in July by our count.)

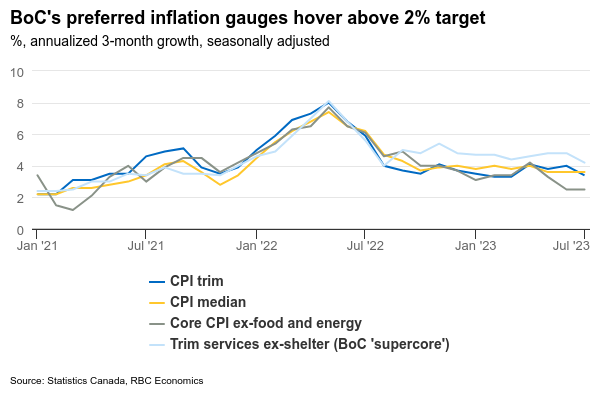

The BoC is more concerned about where price growth is going rather than where it’s been. And more recent broader measures of inflation pressure are a better indicator of that. The BoC’s preferred core measures may tick higher on a year-over-year basis due to soft year-ago ‘base-effects’ (the month-over-month increase in those measures a year ago was relatively small). But it’ll be more focused on the recent 3-month average growth rate for the ‘median’, ‘trim’, and trim services ex-shelter (sometimes called ‘super core’) measures. All of these are still ‘sticky’ at rates above the top-end of the BoC’s inflation target. But we continue to expect signs of softening in the economy to spill over into softer price growth over the remainder of the year—preventing additional BoC interest rate hikes.

Week ahead data watch

We expect July Canadian retail sales to show minimal change from the prior month, in line with Statistics Canada’s preliminary estimate of +0.4%. By our count, auto sales declined on a seasonally-adjusted basis in each of July and August, suggesting some downside risk to near-term retail sales.