Sample Category Title

Data Supports BoJ Tweak, Not Bold Moves

The inflation target has been met for 16 consecutive months but the reflation narrative has lost some steam recently.

We think the data supports another tweak of the yield curve control (YCC) this year, most likely in October, as one last step ahead of completely dismantling YCC.

We expect enough reflation traction for the BoJ to hike its policy rate to zero in Q2 2024. However, we think there is a long way to a situation where the BoJ can tighten much further than that.

We forecast USD/JPY towards 130 on 6/12M horizon, primarily as we deem long US yields are at (or around) peak and that the global environment favours the JPY.

Week Ahead – Fed, BoE, and BoJ Meetings to Fuel FX Volatility

- Central bank decisions in United States, United Kingdom, Japan, and Switzerland

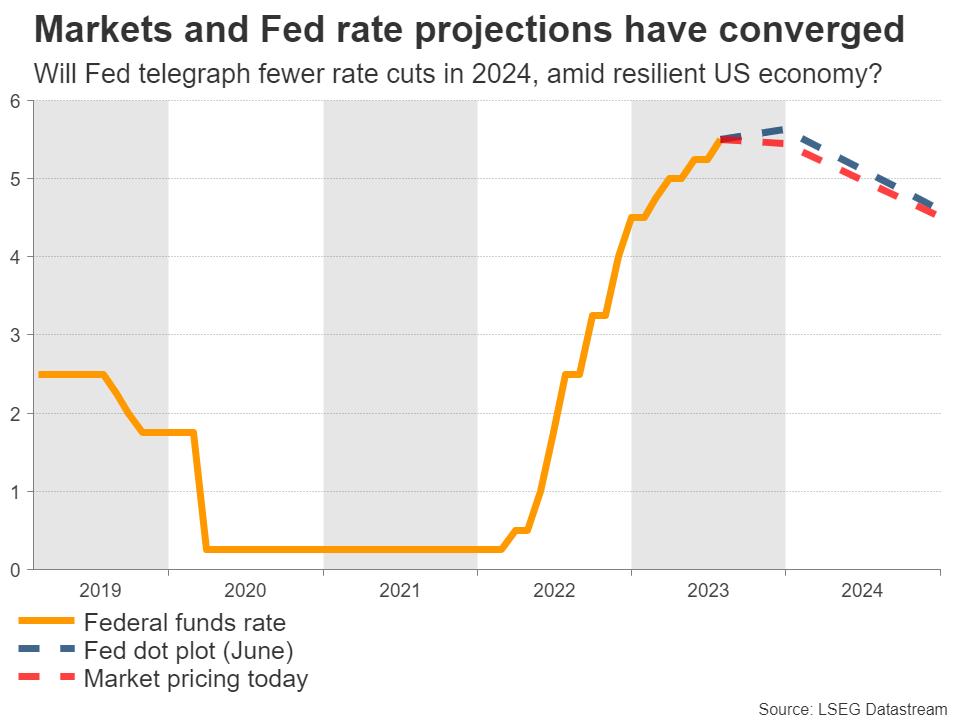

- Fed almost certain to hit pause, markets will focus on updated rate projections

- More scope for surprises from Bank of England and Swiss National Bank instead

Fed - mind the dots

The central bank bonanza will kick off with the Fed on Wednesday. Markets are pricing in almost no chance of a rate increase, following several remarks from FOCM officials calling for patience and more time to examine incoming data before making their next move.

As such, the market action will most likely come from the updated economic forecasts and the interest rate projections in the new ‘dot plot’. Specifically, will the Fed continue to signal another rate increase this year and how many rate cuts will it telegraph for next year?

The latest projections showed interest rates closing next year at 4.6%, projecting roughly 100bps worth of rate cuts from the anticipated peak. But given the streak of robust economic data lately and signs the US economy is not cooling off, the risk is that policymakers signal fewer rate cuts this time.

Economic growth seems to have reaccelerated over the summer, with some help from resilient consumer spending and a labor market that’s beyond most estimates of full employment. With energy prices soaring as well, inflationary pressures are unlikely to die out. Therefore, this might be a meeting where the Fed cements the notion that rates will remain higher for a longer period of time, adding fuel to the rally in US yields and the dollar.

Overall, the outlook for the dollar seems bright as the reserve currency offers a unique combination of solid economic fundamentals, attractive interest rates, and safe haven qualities. That stands in contrast to the rest of the FX arena. Europe and China are plagued by a severe economic slowdown, the yen has been demolished by the Bank of Japan’s refusal to exit negative rates, and sterling is vulnerable to shifts in global risk sentiment.

BoE decision could be a close call

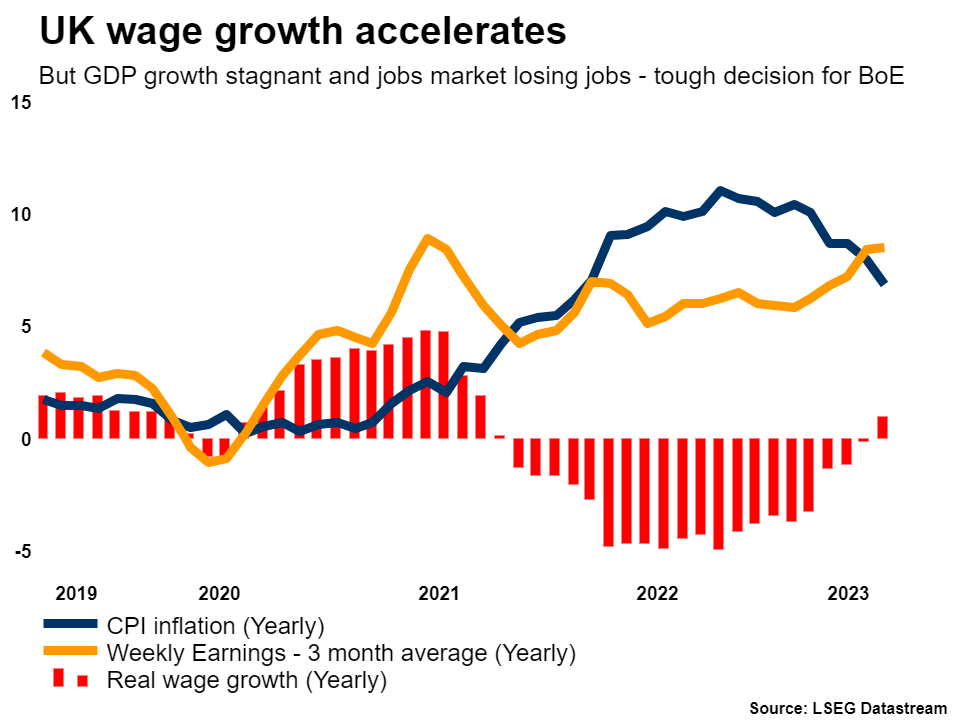

Over in the UK, the Bank of England will unveil its own decision on Thursday and traders assign a 70% probability to a rate increase. Recent data releases have been mixed, showcasing a sharp slowdown in growth and a weakening labor market. However, inflationary pressures remain hot, creating a dilemma for BoE officials.

Economic growth was stagnant in July from a year earlier, and business surveys point to a contraction ahead. Similarly, employment trends are moving in a negative direction. The labor market lost jobs in July, a phenomenon that will likely persist according to leading indicators.

And yet, wage growth accelerated in July, reaching 8.5% in annual terms. That’s a sign that inflation is unlikely to cool anytime soon, hence the dilemma for policymakers. Raising rates further would help bring inflation down, but it might also choke growth completely and push the economy into recession.

Therefore, the vote count for this decision will likely be split. Recent remarks from BoE officials suggest a rate increase is the more likely outcome, but it might be a closer call than markets expect.

As for sterling, the risks seem tilted to the downside. If the BoE raises rates the currency could initially spike higher, although any upside reaction might be minor as this is the market’s baseline scenario already, and reverse quickly if the vote is split and there’s no clear commitment to further hikes. And if the BoE doesn’t hike, that would be a huge surprise, pushing the pound lower instantly.

On the data front, the inflation stats for August will be released ahead of the BoE meeting on Wednesday, while the latest batch of business surveys is scheduled for Friday.

SNB and BoJ meetings

The Swiss franc is the best performing currency of 2023, with the British pound close behind. Driving this stellar performance was the Swiss National Bank’s exit from negative interest rates and FX interventions to strengthen the franc, alongside some quiet safety flows, courtesy of the darker growth outlook in the Eurozone.

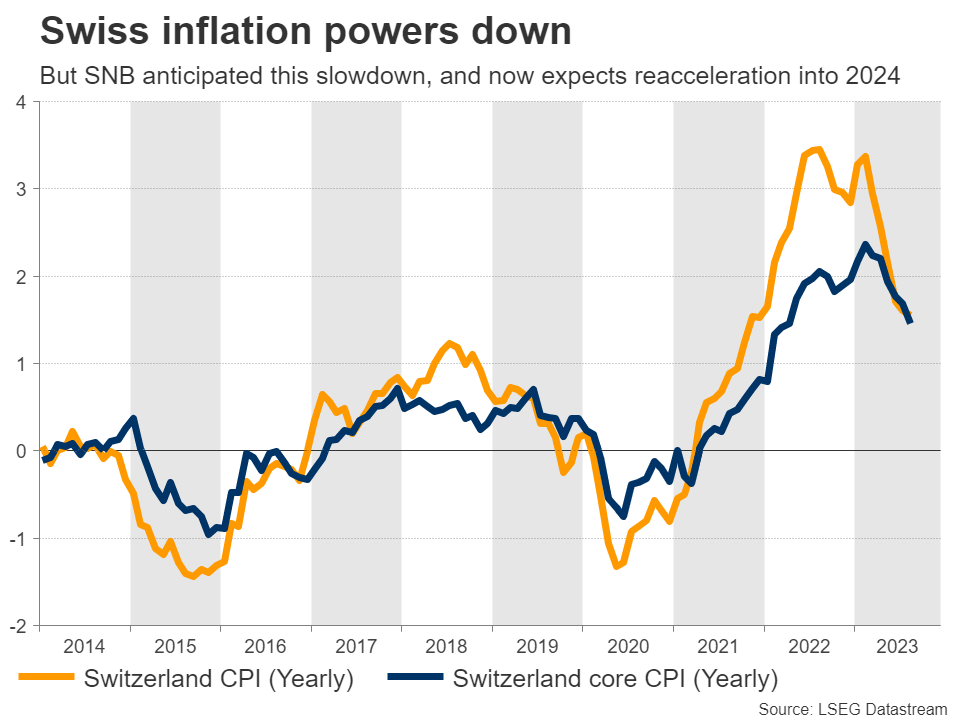

SNB officials meet on Thursday and there’s a 60% probability they raise rates. Hence, there’s uncertainty on whether they will pull the trigger, as the Swiss economy has started to lose momentum and inflation was running at only 1.6% in August. Still, the central bank expects inflation to reaccelerate amid rising electricity and rent prices, and the recent spike in energy costs will likely reinforce their view.

Because of this inflation assessment, the SNB seems more likely to raise rates, potentially boosting the franc on the decision. That said, it might be the final rate increase of this cycle, as inflation is mostly under control.

Crossing into Japan, there isn’t much scope for any shifts when the central bank meets on Friday. The Bank of Japan already recalibrated policy back in July and will most likely take the sidelines this time while it monitors the effects of its previous actions.

But despite the BoJ’s tightening move, the yen has continued to lose ground, suffering at the hands of rising US yields and soaring energy prices. Dollar/yen is currently testing its highest levels of the year, and a combination of a slightly hawkish Fed alongside a BoJ that maintains its loose stance next week may be the catalyst for a break.

Finally, it’s a busy week in terms of data releases. The highlights will be the S&P Global PMIs for September, due on Friday. Markets will pay special attention to the Eurozone prints, amid signs the economy is slipping into recession. The latest batch of Canadian inflation stats on Tuesday and New Zealand’s GDP on Thursday will also be in focus.

Weekly Focus – Central Banks Remain in Focus as Rates Peak

This week, the ECB delivered a 25bp hike which, combined with a dovish message, we see as a compromise in a stagflationary-ish environment. We were quite surprised by the limited optionality for further hikes in the statement, although Lagarde naturally refused to write off the possibility. We see the ECB's approach now focusing much more on the time horizon for rates being in restrictive territory. As the new staff projections kept the forecast for headline and core inflation in 2025 above 2%, the road to neutral rates could end up being a long one. Our baseline is for the ECB to abstain from further hikes, and we see the next move being gradual cuts starting in the summer 2024 (see Flash ECB Review Confirmed: A final rate hike, but restrictive policies are not over, September 14).

Next week, focus turns to Federal Reserve which we expect to keep rates unchanged despite an upside surprise in August core CPI this week. The uptick in core was driven by faster services inflation, particularly airfares, but overall, underlying price pressures seem to have remained slightly higher than anticipated in early Q3. In this context, we think markets will keep a close eye on how FOMC participants assess the need for later hikes. In June, 12 out of 18 dots looked for one more hike, but we doubt it will materialise. Markets have bought into the 'higher for longer' narrative, and in our view, the consequent tightening in financial conditions limits the need for further hikes (see Research US: Fed preview - Plotting the way forward, 15 September).

We believe the Riksbank will deliver one final rate hike next week, as core inflation is still too high, and they want to be sure they are not relaxing monetary policy too early. Weaker SEK fuels inflation for imported products, and hence, Riksbank cannot deviate too much from ECB's policy. Luckily for Riksbank, this time, ECB's dovish hike weakened the euro versus the hard-hit Swedish krona. Also in Sweden, rates will remain high for some time, and we do not expect rate cuts until Q2 next year. Starting in Apr-2024, we expect 25bp cut at each meeting, taking the policy rate to 3.0% by year-end.

We also expect both Norges Bank and the SNB to deliver their final 25bp hikes next week accompanied, and we expect this to mark the peak for both central banks. For Bank of England, we also expect a 25bp hike to 5.50% but the August CPI print ahead of the meeting could prove decisive.

We expect no changes in monetary policy by Bank of Japan next Friday. We do however expect another tweak to YCC later this year. On Thursday, the People's Bank of China (PBoC) announced a 25bp cut to the reserve requirement ratio for most banks. They also injected a net CNY191bn into the financial system through 1-year policy loans while keeping the lending rate unchanged. We see room for further policy support, if needed, to counter problems in the country's real estate sector.

In terms of data releases, next week's focus will be on September preliminary PMIs from euro area and the US on Friday. While global manufacturing has been in a contractionary territory for 12 consecutive months, service sector has kept the engine running, but in August, euro area service PMI fell below 50. We also expect modest weakening in the US driven by service sector.

GBP/USD: Cable Stands at the Back Foot ahead of UK CPI Report and BOE Rate Decision

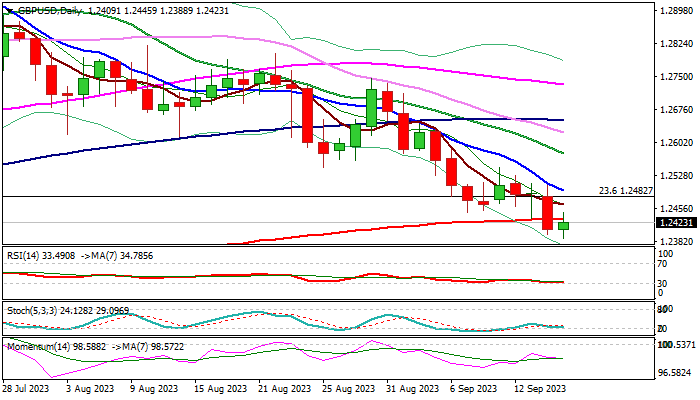

GBPUSD bears slowed on Friday but hold grip and point to further weakness, following a 0.6% drop on Thursday.

Adding to negative signals was break below 200 DMA (1.2431) for the first time since early March, with Friday’s close below it, to reinforce bearish structure.

Fresh extension lower probed below 1.2400 handle after 3 ½ months, eyeing target at 1.2310/04 (May 26/25 higher base) test of which to mark full retracement of 1.2307/1.3141 rally.

South-heading 14-d momentum is deeply in negative territory and MA’s in full bearish setup, contributing to negative outlook.

Traders turn focus on UK inflation report (Aug CPI m/m 0.7% f/c vs -0.4% in July; core m/m Aug 0.7% f/c vs July 0.3%) due on Wednesday and BOE policy meeting on Thursday.

Markets widely expect the central bank to deliver another 25 basis points hike (15th consecutive rate increase) and push the interest rate to 5.5% but expect that this would be the last in the hiking cycle and anticipate a dovish shift in BOE’s expectations.

The pound would be further deflated in such scenario, with initial risk of violating 1.2200 level and possible deeper drop on firmly dovish MPC.

However, this should not be seen as done jobs, as inflation in UK remains elevated (still the highest among the G7 group) and forecasts point to fresh rise in August, which would influence central bank’s plans for coming months.

Res: 1.2431; 1.2482; 1.2504; 1.2547.

Sup: 1.2388; 1.2368; 1.2307; 1.2269.

Sunset Market Commentary

Markets

Yesterday’s ECB assessment that rates being kept at current level ‘for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target’, understandably caused markets to conclude that the hiking cycle might be over. With markets looking forward by nature, the question on the timing of the first rate cut is looming on the horizon. This yesterday resulted in a mild decline in yields. However, even in a forward looking attitude, it is simply too early to play the U-turn in the euro interest rate cycle. Lagarde already said she couldn’t confirm that ECB rates had reached their peak. An FT article also suggested that ECB hawks still see the December meeting/projections as a new point of evaluation. If inflation or wage pressures stay too high a rate hike might still be discussed. ECB’s Vasle today indicated that the current rate level also opens more space to debate to discuss QT/an acceleration the reduction of the APP portfolio. This idea in theory supports the case for some curve steepening. This is what happened today. German yields rose between 4.5 bps (2-y) and 7.6 bps (30-y). This doesn’t look like a market that is already focused on the timing of a rate cut. After yesterday’s rise, US yield gains are lagging the rise in EMU. Still, US data confirmed the economic resilience. The Empire Manufacturing survey of the New York Fed unexpectedly returned into positive territory (1.9 from -19), with a sharp rebound in shipments and orders. Price indices also remained at elevated levels. Another report showed US import prices rising 0.5% M/M due to higher petroleum prices. Admittedly, these are not the most important data and they won’t change the Fed’s assessment at next week’s meeting. Even so, they are strong enough to keep bonds in the defensive with US yields rising between 1-3 bps across the curve. The US 10-y yield (4.32%) is only a whisker away from the cycle top at 4.34/4.36%. After finishing this report Consumer confidence of the University of Michigan (especially the inflation expectation measures) still has market moving potential. The EuroStoxx50 initially gained up to 1.0% building on WS gains and a positive sentiment in Asian after some hopeful figures out of China. However, momentum dwindled as US traders joined (EuroStoxx50 currently +0.6%; S&P 500 even opened with a loss of 0.35%).

In FX, the dollar rally shifted into a lower gear, but there is no sign at all that any meaningful correction might be on the cards. EUR/USD stabilized in the 1.0635/1.067 area. The 1.0635 support is far from save. The DXY is holding well north of 105. (105.37). USD/JPY set a minor YTD top just below 148. Markets are looking out for a potential policy reaction (or the absence of it) as the BOJ meets next Friday.

News & Views

The Turkish central bank (CBRT) is making it more expensive for local banks to offer short-term deposit schemes to clients under the KKM program. KKM is an initiative introduced in late 2021 via which Turks can deposit their liras (TRY) on accounts that offer a certain interest rate. If TRY losses would surpass the interest received on the deposit, the government compensates for the difference. It dampened the incentive to swap ever depreciating liras for FX, including the dollar, and turned out to be instrumental in containing further losses for the currency. The downside, however, is that it is draining state finances. The CBRT now decided to lift the amount of money that banks must hold as reserve by raising the reserve requirement ratio from 15% to 25%. This will drain TRY liquidity from the market (as banks hold more reserves) but the move risks losing efficacy if consumers start swapping the liras that no longer can be deposited under KKM again. USD/TRY today marginally gains to 26.98, further erasing losses after the shocker interest rate hike by the CBRT end of August. USD/TRY back then briefly traded below 26.

In its quarterly survey, the Bank of England finds that public trust in the institution has fallen to the lowest level since conducting the questionnaire in 1999. 40% of the respondents think the central bank is doing a bad job, up from 24% in May. This compares to less than one in five being satisfied with the BoE. The survey also gauges consumers for their inflation expectations. Those for the year ahead rose from 3.5% to 3.6%, well above the 2% BoE target. Consumers see inflation two years ahead at 2.8%, up from 2.6% in the May survey. It’s bad news for the central bank. Threadneedle Street meets next week Thursday. Markets have rapidly pared tightening bets over the past few weeks amid weakening economic data. They do expect at least one (but less than two) more rate hike(s), but not necessarily at the September meeting (70% chance discounted).

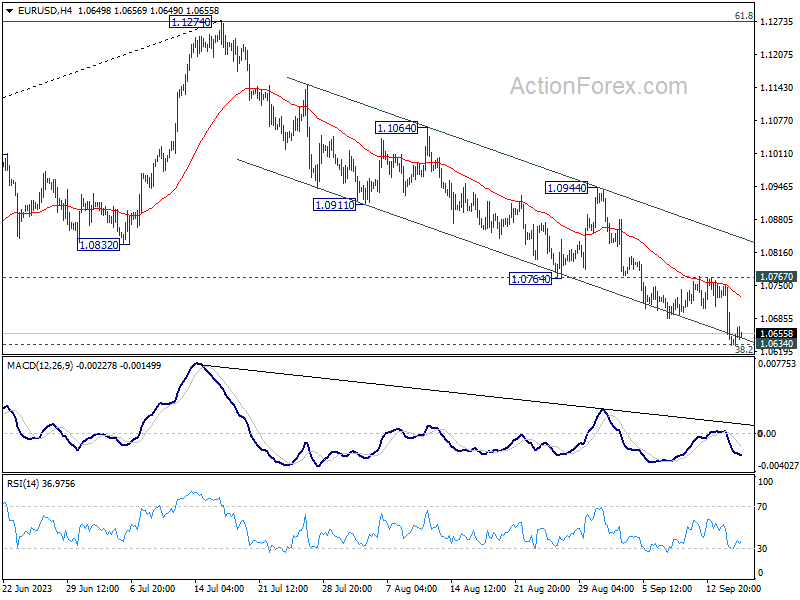

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0600; (P) 1.0676; (R1) 1.0720; More...

Intraday bias in EUR/USD is staying on the downside for the moment. Strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance. However, sustained break of 1.0609/34 support zone will carry larger bearish implication, and target 1.0515 support next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

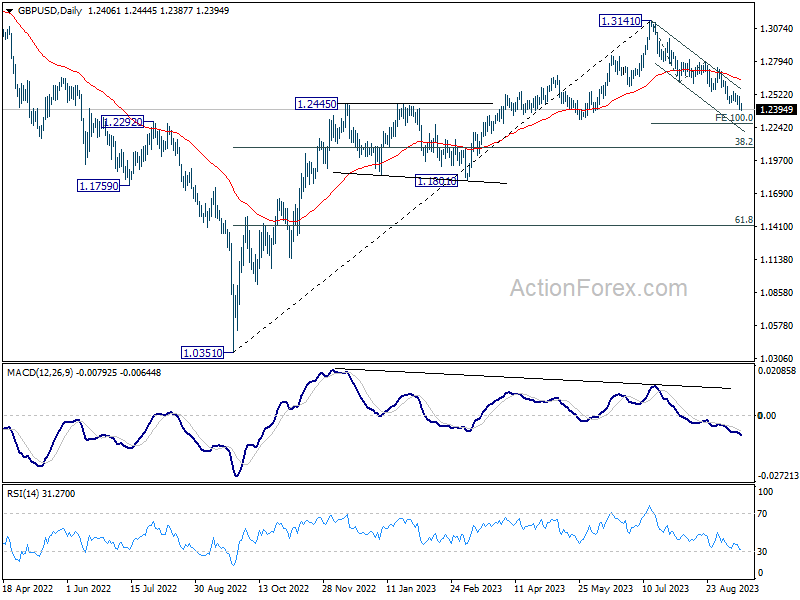

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2369; (P) 1.2438; (R1) 1.2478; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, however, firm break of 1.2547 resistance will now indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

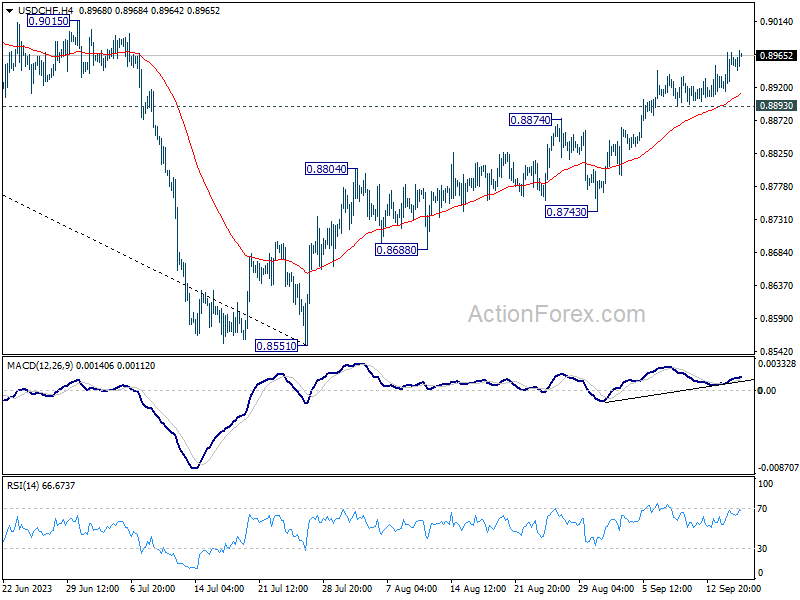

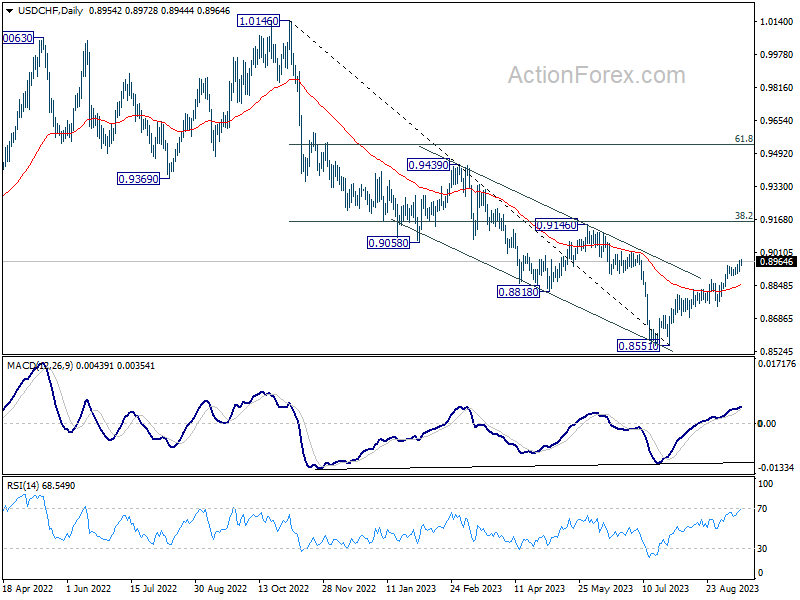

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8924; (P) 0.8948; (R1) 0.8980; More....

USD/CHF's rally from 0.8551 continues today and intraday bias stays on the upside. Further rise should be seen to 0.9146 cluster resistance. On the downside, though, break of 0.8893 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

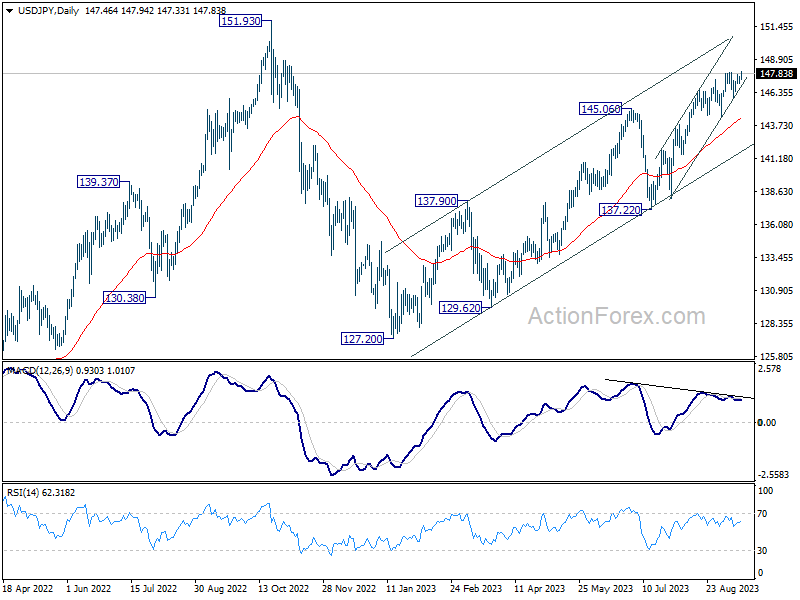

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.14; (P) 147.35; (R1) 147.69; More...

USD/JPY's breach of 147.88 resistance argues that rise from 127.20 is resuming. Intraday bias is back on the upside. Sustained trading above 147.88 will pave the way to retest 151.93 high. On the downside, below 147.00 minor support will turn intraday bias neutral again first. But outlook will remain bullish as long as 145.88 support holds.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Yen Hits Year Low on Yields, Euro Shows Signs of Stabilization

Japanese Yen registered notable slump today, recording a new low for the year against Dollar, a move driven largely by ascending benchmark yields in the US and European markets. Meanwhile, sentiment in risk markets appears to be on the upswing, partly propelled by encouraging economic data emerging from China, fostering an environment where commodity currencies are experiencing a lift, with Australian Dollar taking the forefront.

Euro, on the other hand, managed to slow its descent, buoyed by remarks from ECB officials who sought to downplay the prospects of rate cuts in the coming year. The comments stimulated a recovery in Euro, particularly against Sterling and Swiss franc. While Dollar is making efforts to strengthen up, traders remain cautious, seemingly unwilling to stake large bets ahead of Fed's rate decisions slated for next week.

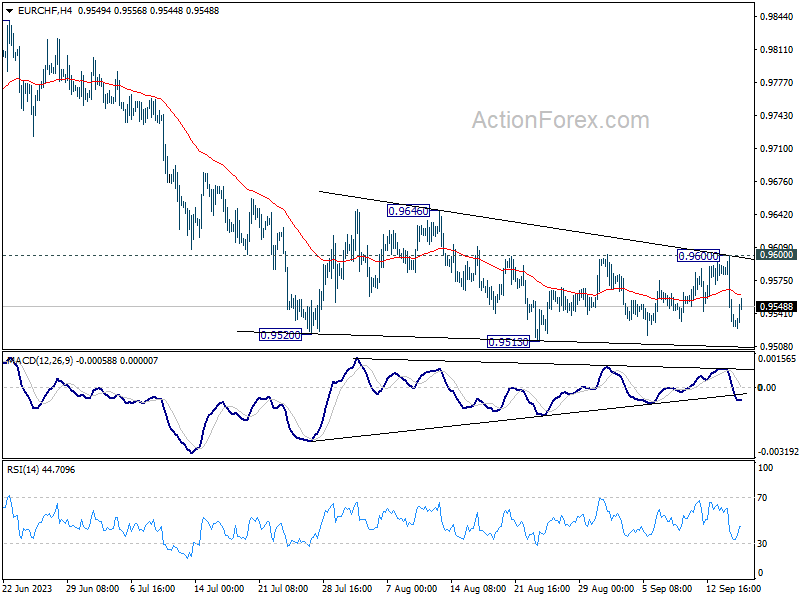

Technically, EUR/CHF recovered well ahead of 0.9513 low, and the developments argues that post-ECB selling might have past its climax. Nevertheless, outlook will stay bearish as long as 0.9600 resistance holds. Break of 0.9513 is in favor sooner or later to resume larger decline from 1.0095.

In Europe, at the time of writing, FTSE is up 0.68%. DAX is up 0.91%. CAC is up 1.43%. Germany 10-year yield is up 0.0649 at 2.661. Earlier in Asia, Nikkei rose 1.10%. Hong Kong HSI rose 0.75%. China Shanghai SSE dropped -0.28%. Singapore Strait Times rose 0.96%. Japan 10-year JGB yield rose 0.0013 to 0.710.

ECB officials dismiss predictions of early rate cuts

In a chorus of comments, ECB officias pushed back on market expectations on a rate cut next year.

During a press conference today, ECB President Christine Lagarde emphasized, "We have not decided, discussed or even pronounced cuts." She underlined that the institution's strategy will pivot according to incoming economic data and highlighted that the levels and duration of the existing high rates are designed to foster a return to the inflation target of 2%. The focus is on evolving economic indicators, reviewed in a meeting-by-meeting approach, hinting at the bank's readiness to adapt in the face of changing economic contexts.

Supporting Lagarde's stance, ECB Vice President Luis de Guindos conveyed skepticism regarding market pricing that forecast a rate cut in June 2024. Speaking to Spanish radio station Cadena Cope, de Guindos mentioned that the markets often rely on speculative "hypotheses that sometimes do not come true." He viewed such forecasts as gambles, affirming that they might not materialize. "It is a bet, it may be right and it may not be right," De Guindos added, underlining the uncertain nature of market forecasts.

Martins Kazaks, a member of ECB's Governing Council, expressed comfort with the current rate levels, showing optimism regarding achieving the 2% inflation goal by the second half of 2025. He maintained that the bank remains open to the possibility of another rate increase if substantiated by forthcoming data.

Kazaks was assertive in dismissing speculations about a rate cut in April, stating such conjectures are "inconsistent with our macro scenario." He reiterated the bank's firm stance to "stay in restrictive territory for as long as necessary to get inflation to 2%."

UK public anticipates elevated inflation and ascending interest rates, BoE Survey Reveals

Bank of England/Ipsos Inflation Attitudes Survey for August has shed light on how the public perceives inflation trends and the likely moves by the central bank.

Interestingly, public's perception of current inflation rate seems to have moderated, with a median estimate of 8.6%. This is a full percentage point decline from 9.6% recorded in May. This suggests that the public may feel the worst of inflationary surge has passed.

However, expectations for inflation over the short to medium term are slightly more elevated. The median expectation for inflation over the next year stood at 3.6%, a modest uptick from 3.5% three months ago. Looking a bit further out, the 12-month period after next, expectations rose to 2.8% from 2.6% in the prior survey.

Regarding BoE's policy path, a significant 63% anticipate interest rate hike over the next year, marking an increase from 57% in May. Meanwhile, those expecting rates to remain stable accounted for 19%, a slight decrease from prior reading of 20%.

Eurozone goods expects down -2.7 yoy, imports fell -18.2% yoy

Eurozone exports of goods to the rest of the world dropped -2.7% yoy to EUR 227.8B in Jul. Imports fell -18.2% yoy to EUR 221.3B. Eurozone recorded EUR 6.5B trade surplus. Intra-Eurozone trade fell -7.9% yoy to EUR 211.8B.

In seasonally adjusted term, exports fell -1.7% mom to EUR 232.6B. Imports rose 0.7% mom to EUR 229.7B. Trade surplus narrowed from EUR 8.6B to EUR 2.9B, smaller than expectation of EUR 13.5B. Intra-Eurozone trade fell slightly from EUR 219.3B to EUR 218.7B.

NZ BNZ PMI falls to 46.1, manufacturing activity slumps to multi-year low

New Zealand's manufacturing sector experienced a further slowdown in August, with BusinessNZ Performance of Manufacturing Index falling slightly from 46.6 in July to 46.1. This marks the lowest rate of activity for a non-pandemic affected month since June 2009. Furthermore, the latest PMI data sits significantly below its long-term average of 52.9.

A closer look at the August data reveals: Production observed a modest increase, moving from 43.1 to 43.9. Employment metrics improved, rising from 44.8 to 47.7. New orders experienced a minor uptick, growing from 45.5 to 46.6. Finished stock levels retreated slightly from 52.7 to 52.1. Deliveries, however, showed more promise, escalating from 42.9 to 47.7.

Despite the grim headline figure, it is noteworthy that there was a slight decrease in the proportion of negative comments, standing at 66.7%, a marginal relief compared to July's 72%. However, the level of pessimism mirrored that of May, maintaining the same rate of 66.7%. The pervasive market uncertainty stemming both from domestic and offshore influences, coupled with rising costs and weather-impacted demand, continued to be highlighted as primary drivers for the negative sentiment pervading the industry.

BNZ Senior Economist Craig Ebert expressed concern over the PMI's latest results, noting that while the headline figure had seen much lower points during previous recessions, the composition of August figures brought little consolation. Ebert pinpointed new orders and production as substantial drags on the performance, trailing behind the standard levels by 8.0 and 9.5 points respectively.

China's Economic Data Surpasses Forecasts, but Challenges Persist

China's economic indicators for August showcased a mixed picture but, on the whole, exceeded analyst expectations in key areas. Industrial production exhibited growth of 4.5% yoy, edging out forecast of 4.0% yoy. Retail sales also outperformed predictions, registering 4.6% yoy increase compared to anticipated 3.0% yoy. However, fixed asset investment lagged slightly, presenting a 3.2% rise year-to-date year-on-year, just shy of the 3.3% expected.

The official communique from the NBS acknowledged the data as revealing a "marginal improvement." Emphasizing the resilience and progress of the national economy, the statement underscored that "high-quality development" was on track and the accumulation of positive factors was evident. However, it also stressed caution. While the recovery is in motion, the bureau pointed out that there are still several "unstable and uncertain factors in the external environment" that China has to contend with.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.14; (P) 147.35; (R1) 147.69; More...

USD/JPY's breach of 147.88 resistance argues that rise from 127.20 is resuming. Intraday bias is back on the upside. Sustained trading above 147.88 will pave the way to retest 151.93 high. On the downside, below 147.00 minor support will turn intraday bias neutral again first. But outlook will remain bullish as long as 145.88 support holds.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Aug | 46.1 | 46.3 | 46.6 | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 4.50% | 4.00% | 3.70% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Aug | 3.20% | 3.30% | 3.40% | |

| 02:00 | CNY | Retail Sales Y/Y Aug | 4.60% | 3.00% | 2.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 0.90% | 0.20% | -0.40% | -0.70% |

| 08:30 | GBP | Consumer Inflation Expectations | 3.60% | 3.50% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 2.9B | 13.5B | 12.5B | 8.6B |

| 12:30 | CAD | Manufacturing Sales M/M Jul | 1.60% | 0.70% | -1.70% | |

| 12:30 | USD | Empire State Manufacturing Sep | 1.9 | -10 | -19 | |

| 12:30 | USD | Import Price Index M/M Aug | 0.50% | 0.30% | 0.40% | |

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | 1.00% | ||

| 13:15 | USD | Capacity Utilization Aug | 79.30% | 79.30% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | 69.5 | 69.5 |