Sample Category Title

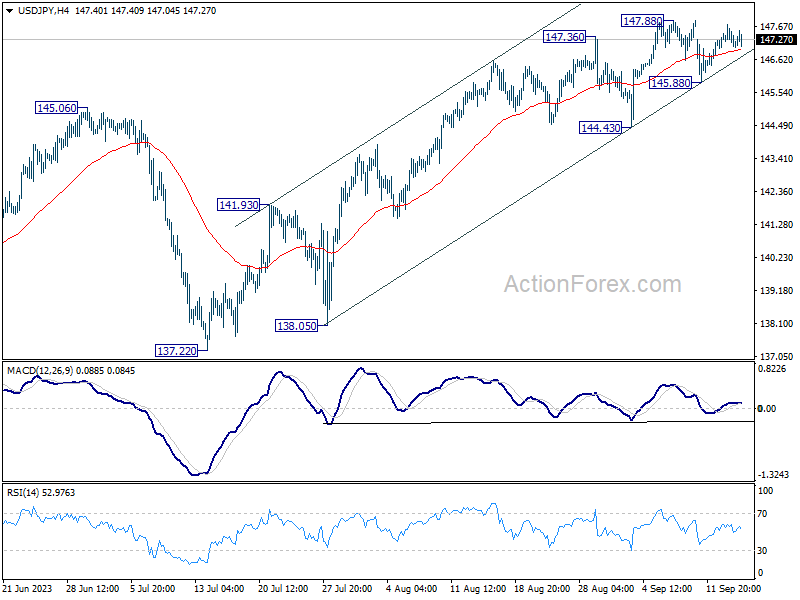

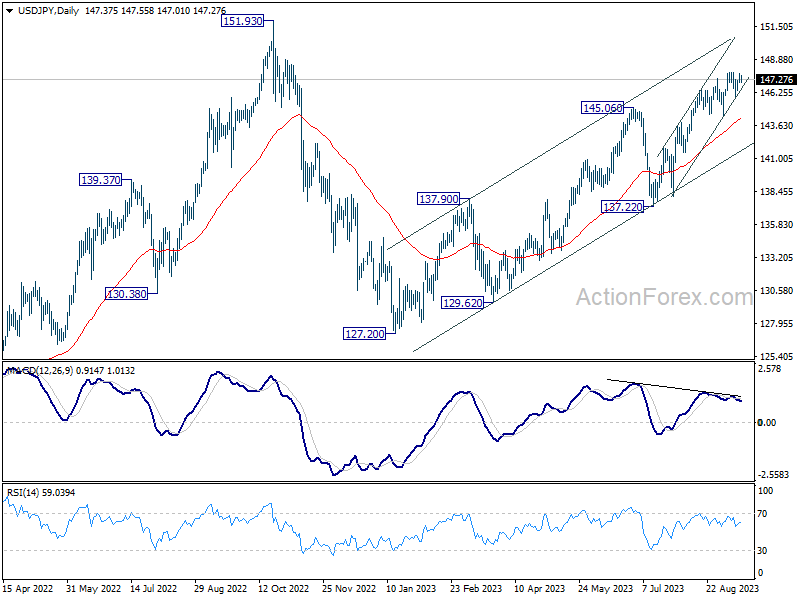

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.08; (P) 147.41; (R1) 147.80; More...

USD/JPY is still bounded in consolidation from 147.88 and intraday bias stays neutral. In case of another pull back, near term outlook will remain bullish as long as 144.43 support holds. On the upside, firm break of 147.88 will resume larger rise from 127.20, to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

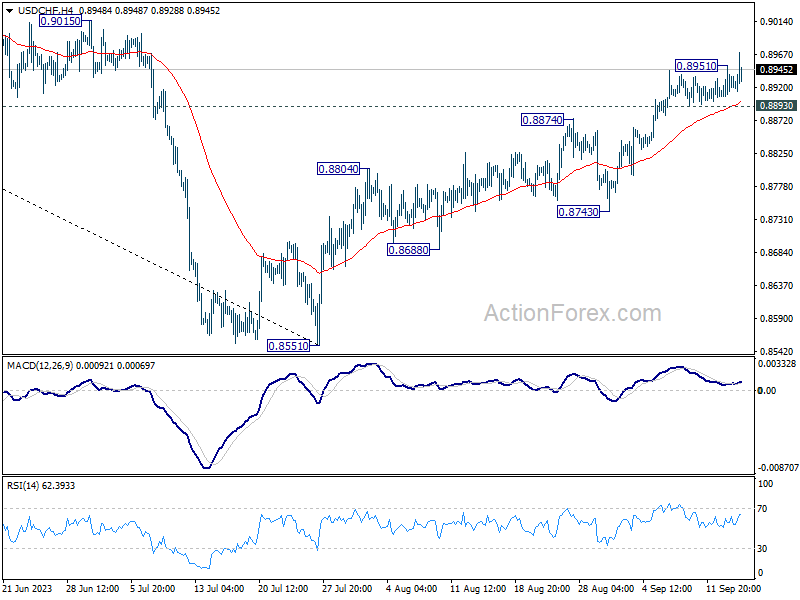

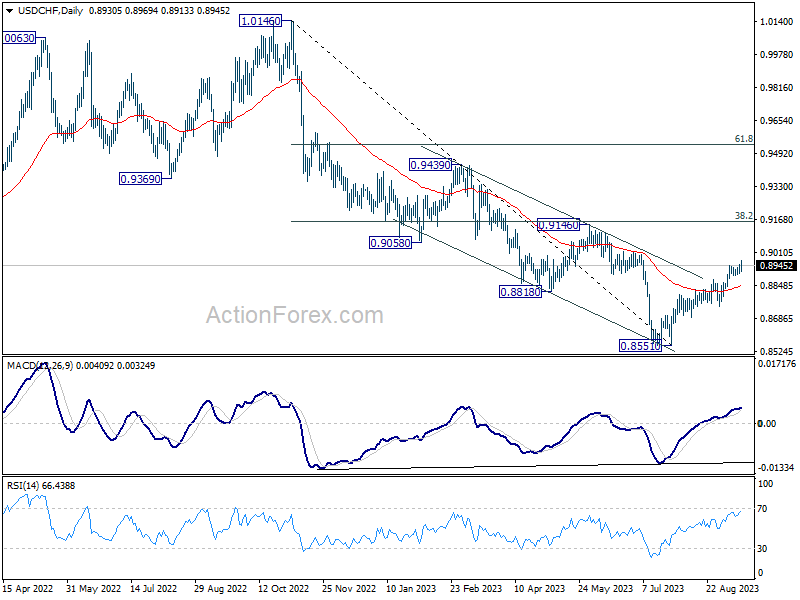

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8908; (P) 0.8930; (R1) 0.8959; More....

Intraday bias in USD/CHF is back on the upside with break of 0.8915 resistance. Rise from 0.8551 is resuming for 0.9146 cluster resistance. On the downside, though, break of 0.8893 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

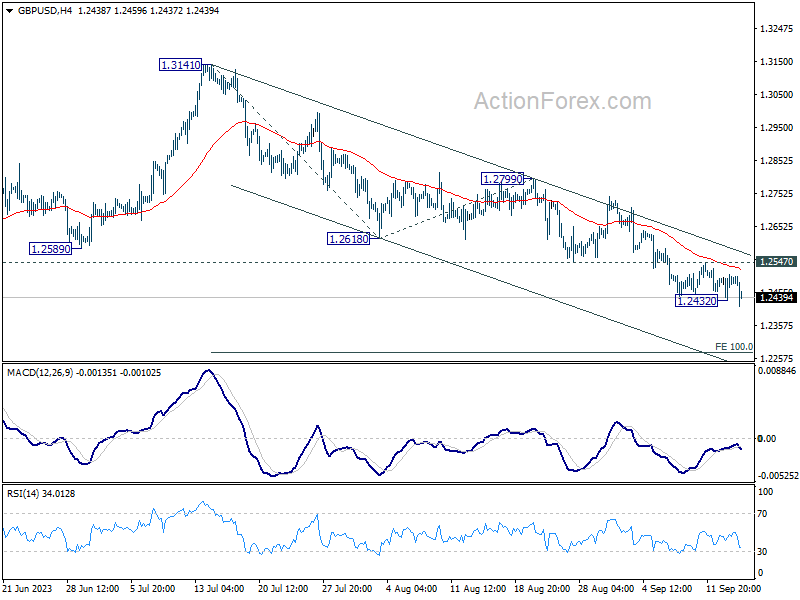

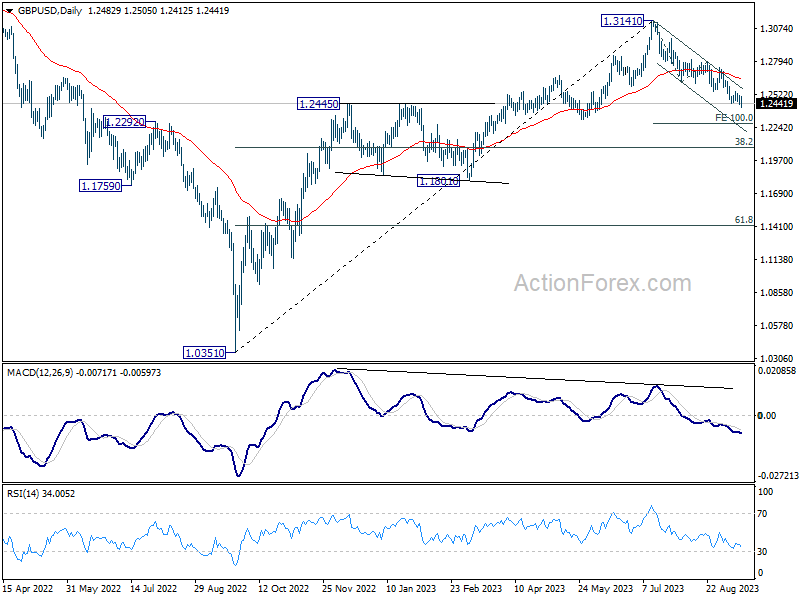

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2446; (P) 1.2479; (R1) 1.2523; More...

Intraday bias in GBP/USD is back on the downside with breach of 1.2432. Fall from 1.3141 is trying to resume, and further fall would be seen to 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, however, firm break of 1.2547 resistance will now indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

U.S. Retail Sales Rise in August, Beating Expectations

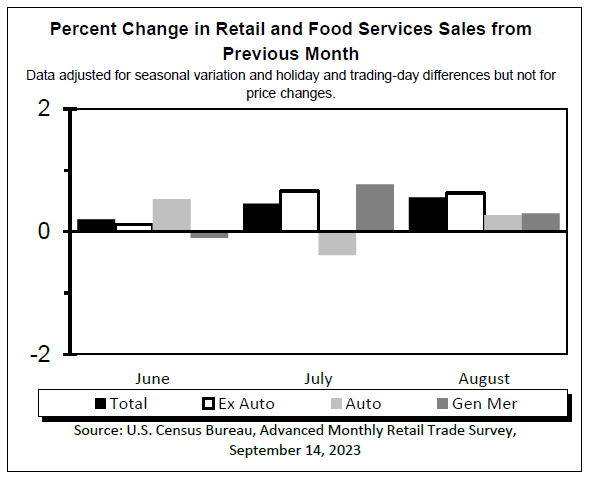

Retail sales rose by 0.6% month-on-month (m/m) in August, up from the downwardly revised 0.5% (previously 0.7%) reading in July. This was notably above the median consensus forecast calling for a more muted gain of 0.1%.

Trade in the auto sector strengthened on the month rising by 0.3% m/m, relative to a -0.4% m/m decline in July. This largely reflected sales at motor vehicle dealers, which rose 0.4% (erasing a similar decline last month). Meanwhile, sales at automotive parts and accessory stores declined by -0.9% m/m – its first decline since March of this year.

The large gain in headline retail sales was driven by sales at gasoline stations, which soared by 5.2% m/m (the largest increase since March 2022). The rebound at gas stations largely reflects recent upward movements in gas prices. The building materials and equipment category rose by 0.1% m/m, but is down by 4.9% versus a year ago.

Sales in the retail sales "control group", which excludes the above volatile components (autos, building materials and gas) and is used to estimate personal consumption expenditures (PCE) came in at 0.1% m/m – this was above consensus forecast which called for a -0.1% decline. However, July's figure was revised lower to show an increase of 0.7% instead of the previously reported 1.0%.

- Among the control group, the largest contribution came from sales at clothing and accessory stores (+0.9% m/m), health and personal care (+0.5% m/m), food and beverage stores (+0.4% m/m) and general merchandise store (+0.3% m/m).

- The main categories posting declines were sporting goods stores (-1.6% m/m) and miscellaneous stores retailers (-1.3% m/m).

Food services & drinking places – the only services category in the retail sales report – was up 0.3% m/m, the smallest increase since March.

Key Implications

Retail sales continued to pull ahead in August, although downward revisions to July's numbers tempered pervious gains. With two months of data in for the third quarter, sales are currently tracking 4.4% annualized for 2023 Q3, notably above the revised 0.4% annualized gain recorded in Q2 (previously 0.6%). This should give a decent boost to consumer spending which continues to defy expectations for a major slowdown.

Even as retail spending continues to post gains, the headwinds facing U.S. consumers continue to gain traction. Notably, the labor market is gradually cooling, taking some of the steam out of consumers' sails, credit markets remain tight and student loan payments are coming due. Additionally, while overall price gains are moderating, the recent uptick in gasoline prices evident in today's numbers is causing consumers pain at the pump. Given these confluence of factors, we still expect to see a deceleration in spending towards the end of the year as consumers' resilience gets tested even more.

EUR/USD: ECB Hikes and Euro Falls as Stagflation Risks Grow; Dollar Strength Extends after US Retail Sales Data

- Euro falls to the lowest levels in May after ECB hikes rates and delivers an abysmal growth forecasts, while upgrading 2023 and 2024 inflation outlooks

- Post ECB decision – October 26th ECB rate hike odds hover around 35.4%

- US retail sales remained strong on back-to-school spending and despite the extra energy costs at the pump

The euro initially spiked after the ECB raised rates, but quickly tumbled after traders digested the ECB forecasts that suggest stagflation might be here. Shortly after, the US posted robust retail sales and jobless claims data, which basically drove home the message that the US economy will easily outperform the eurozone economy throughout the rest of the year. Investors were thinking that the US might be poised to deliver more rate cuts than the eurozone, but that seems like that won’t be happening anytime soon.

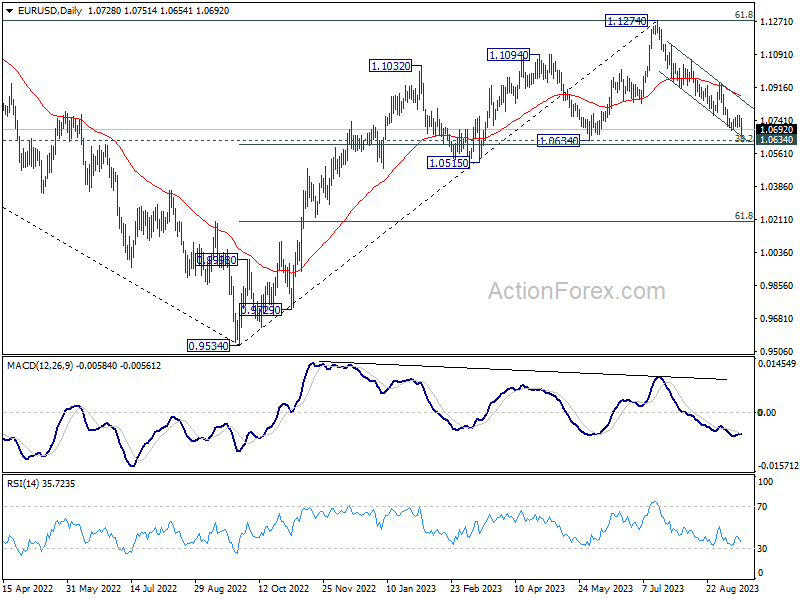

EUR/USD – 30 minute chart

ECB

The summer break is over for the ECB and they have a tough job ahead. Inflation remains too high and that is forcing the ECB to signal that they ” will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary.” The market was split on whether they would raise rates, but when processed the forecasts, they realized stagflation risks are here.

ECB Forecasts:

- 2023 GDP forecast cut from 0.9% to 0.7%

- 2024 GDP forecast cut from 1.5% to 1.0%

- 2023 GDP forecast cut from 1.6% to 1.5%

- 2023 Inflation forecast raised from 5.4% to 5.6% (core steady at 5.1%)

- 2024 Inflation forecast raised from 3.0% to 3.2%(a tick lower to 2.9%

ECB’S Lagarde Press Conference

When asked if she was done with rate hikes, Lagarde noted that some members preferred to pause, but that still a solid majority of members agreed with the decision. One of the key takeaways from Lagarde is that they won’t be cutting rates anytime soon as inflation is still far from target. Lagarde repeated this quote a few times, “based on current assessment…. the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target.”

EUR/USD – Daily Chart

The euro might not be ready to punch a one-way ticket to the 1.05 level, but it sure seems like it is heading there. Price action on the EUR/USD daily highlights the bearish trend has firmly been in place since mid-July. As the risks for growth continue to deteriorate even further, the euro could see short-term weakness before a bottom is put in place. Major long-term support could be provided by the 1.04 level, which is the 50% Fibonacci retracement of the September low to July high move.

On the other side of the Atlantic, another round of US data supported USD strength after it reminded investors how strong the US economy remains; retail sales ex-auto had a fifth straight increase, producer prices came in hotter-than-expected, and jobless claims remained low.

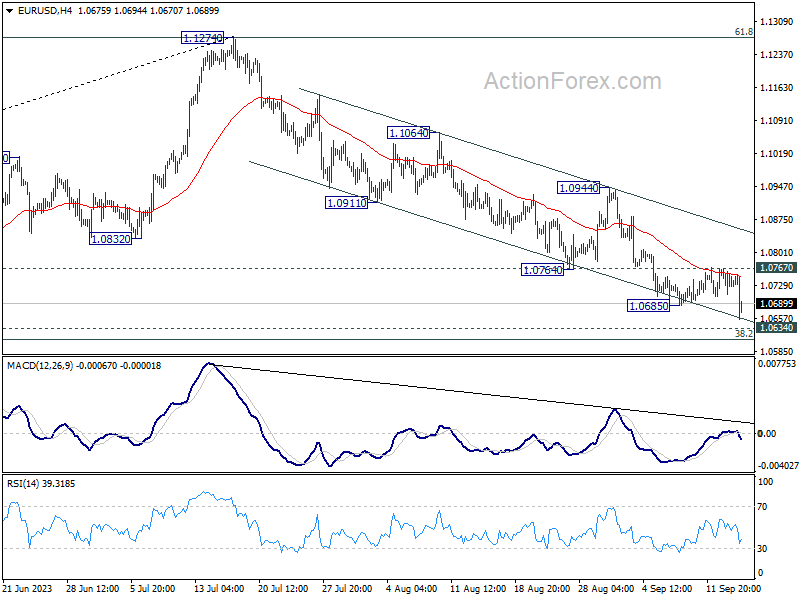

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0706; (P) 1.0735; (R1) 1.0760; More...

EUR/USD's fall from 1.1274 resumed by breaking through 1.0685 temporary low today. Intraday bias is back on the downside for 1.0609/34 cluster support zone next. On the upside, break of 1.0767 resistance will now indicate short term bottoming, and turn bias back to the upside for stronger rebound to 1.0944 resistance next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

Euro Stumbles on Dovish ECB Hike, Dollar Rides on Strong Data

In a twist of events today, Euro takes a considerable hit following ECB's dovish rate hike which communicated a possibly peak in the tightening cycle. The downgrading of core CPI and GDP growth forecasts for the coming years - 2024 and 2025 - further aggravates the descent. This bearish sentiment spills over to Sterling and Swiss Franc, painting a subdued picture for European majors across the board.

In a contrasting scenario, Dollar exhibits a spirited performance, leveraging off the back of a stream of encouraging economic data releases. US retail sales and PPI figures emerged strong, coupled with data pointing to a hearty employment market echoed by jobless claims report. Despite this upbeat tide, Dollar finds itself outshone slightly by Australian and Canadian dollars in the financial market space.

Aussie Dollar is seen deriving some backing from China's decision to cut RRR, a move aiming to inject liquidity and stimulate economic activity. On another front, Canadian dollar rise on the rally observed in WTI oil, which notably surges past 90 handle.

Technically, as the greenback is rallying against European majors, the focus is on whether buying momentum could continue. In particular, EUR/USD and GBP/USD will have to sustain below 1.0685 and 1.2432 temporary lows. USD/CHF will also have to sustain above 0.8951 temporary high. Otherwise, the greenback will be back to square one.

In Europe, at the time of writing, FTSE is up 1.04%. DAX is up 0.34%. CAC is up 0.49%. Germany 10-year yield is down -0.070 at 2.584. Earlier in Asia, Nikkei rose 1.41%. Hong Kong HSI rose 0.21%. China Shanghai SSE rose 0.11%. Singapore Strait Times rose 0.95%. Japan 10-year JGB yield dropped -0.0013 to 0.709.

Dovish ECB hike, peak reached already, 2024 & 2025 core inflation and growth downgraded

ECB delivers a dovish 25bps rate hike today. The accompany statement indicated that the current tightening cycle could have reached its peak already. Also, core inflation and growth forecasts for 2024 and 2025 were revised down.

The newly set rates are as follows: main refinancing operations rate at 4.50%, marginal lending facility rate at 4.75%, and deposit facility rate at 4.00%.

ECB President cited the persistent nature of inflation being "too high for too long" as the primary motivator behind this strategy to "reinforce progress" in ushering inflation back to the target in a "timely manner".

ECB added, "the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target". Future decisions will "ensure" that the interest ares are set at "sufficiently restrictive levels for as long as necessary.

In the new economic projections, inflation is forecast to be at 5.6% in 2023 (prior projection at 5.1%), 3.2% in 2024 (prior 3.0%) and 2.1% in 2025 (prior 2.3%). The upward revision for 2023 and 2024 mainly reflects a higher path for energy prices.

Core inflation is projected to average 5.1% in 2023 (unchanged), 2.9% in 2024 (prior 3.0%), and 2.2% in 2025 (prior 2.3%).

Growth is projected to be at 0.7% in 2023 (prior 0.9%), 1.0% in 2024 (prior 1.5%), and 1.5% in 2025 (prior 1.6%).

US retail sales up 0.6% mom, ex-auto sales up 0.6%, above expectations

US retail sales rose 0.6% mom to USD 697.6B in August, above expectation of 0.2% mom. Ex-auto sales rose 0.6% to USD 564.0B, above expectation of 0.4% mom. Ex-gasoline sales rose 0.2% mom to USD 642.3B. Ex-auto & gasoline sales rose 0.2% mom to USD 508.8B

In the three months through August, sales were up 2.2% yoy from the same period a year ago.

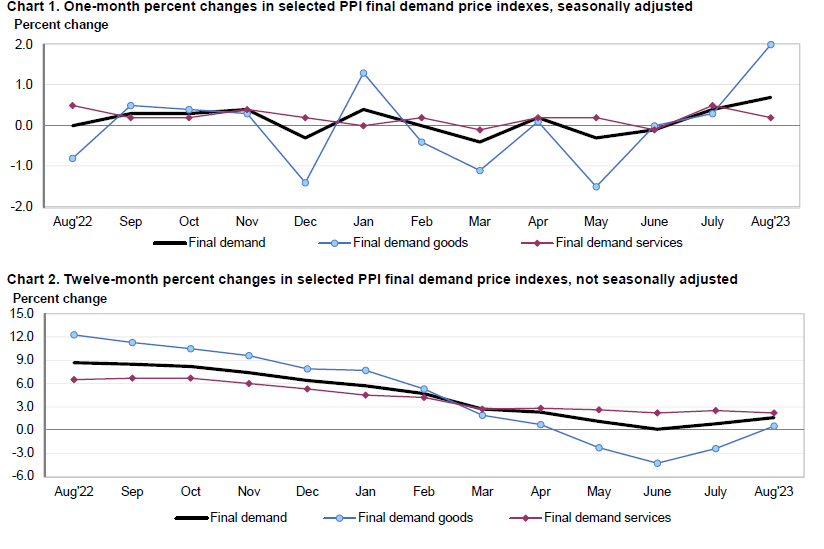

US PPI rose 0.7% mom in Aug, highest since Jun 2022

US PPI for final demand rose 0.7% mom in August, above expectation of 0.4% mom. That's also the largest monthly increase since June 2022.

80% of the rise in PPI is attributable to the 2% mom jump in PPI goods, highest since June 2022, mostly attributable to energy prices which was up 10.5% mom. Prices for services rose 0.2% mom.

For the 12 months ended in August, PPI rose 1.6% yoy, above expectation of 1.2% yoy.

PPI less foods, energy, and trade services rose 0.3% mom. For the 12 months period, PPI less foods, energy, and trade services was up 3.0% yoy, largest annual advance since April.

Also released, initial jobless claims rose slightly from 217k to 220k in the week ending September 8, below expectation of 229k.

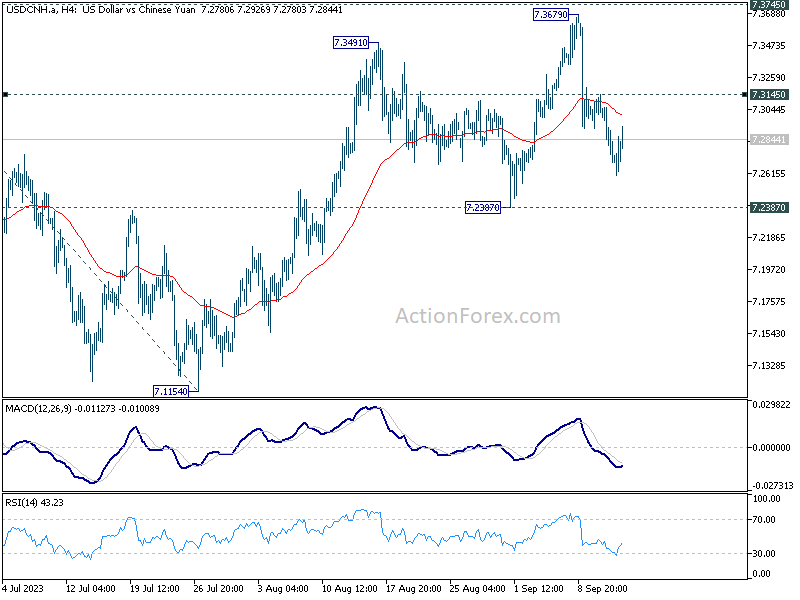

PBOC cuts reserve requirement ratio to release CNY 500B liquidity

People's Bank of China slashed the Reserve Requirement Ratio for a majority of banks by 25bps today. This marks the second such reduction in this calendar year, aiming to spur liquidity in the market and support the economy. Following this adjustment, the weighted average RRR for banks will stand at 7.4%. This strategic step is slated to unleash medium to long-term liquidity exceeding CNY 500B (approximately USD 68.7B) into the financial system.

In the aftermath of this announcement, the offshore Yuan experienced a mild depreciation, fueling a recovery in the USD/CNH from its day low at 7.2603. While fall from 7.3679 could extend lower, strong support is likely at around 7.2387 to contain downside to bring rebound. Break of 7.3145 resistance will bring stronger rise back to 7.3679. But for the near term, some more range trading is likely because USD/CNH would have enough momentum to take on 7.3745 high.

UK RICS house price balance fell to 14-year low, deepening slump

In the latest sign of mounting pressures in the UK property market, RICS house price balance deteriorated notably, plummeting to -68 in August, down from -55 in the previous month. This development has surpassed the grim expectation set at -56 and marks the most unfavorable reading since February 2009.

Dissecting the UK reveals that almost every region is grappling with "relatively steep fall in house prices," as noted by RICS.

Looking ahead, surveyors anticipate that the upcoming months will not bring any reprieve. Short-term projections illustrate a more pronounced dip, with net balance drifting deeper into negative terrain at -67%, a decline from prior figure of -60%.

Furthermore, long-term outlook remains relatively unchanged but still under a cloud, with expectations cementing around a net balance of -48%, mirroring the sentiment recorded in both June and July.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0706; (P) 1.0735; (R1) 1.0760; More...

EUR/USD's fall from 1.1274 resumed by breaking through 1.0685 temporary low today. Intraday bias is back on the downside for 1.0609/34 cluster support zone next. On the upside, break of 1.0767 resistance will now indicate short term bottoming, and turn bias back to the upside for stronger rebound to 1.0944 resistance next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Jul | -1.10% | -0.70% | 2.70% | |

| 01:00 | AUD | Consumer Inflation Expectations Sep | 4.60% | 4.90% | ||

| 01:30 | AUD | Employment Change Aug | 64.9K | 24.3K | -14.6K | |

| 01:30 | AUD | Unemployment Rate Aug | 3.70% | 3.70% | 3.70% | |

| 04:30 | JPY | Industrial Production M/M Jul F | -1.80% | -2.00% | -2.00% | |

| 06:30 | CHF | Producer and Import Prices M/M Aug | -0.20% | 0.10% | -0.10% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | -0.80% | -0.60% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.25% | 4.25% | |

| 12:30 | CAD | Wholesale Sales M/M Jul | 0.20% | -2.00% | -2.80% | -2.10% |

| 12:30 | USD | Retail Sales M/M Aug | 0.60% | 0.20% | 0.70% | 0.50% |

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.60% | 0.40% | 1.00% | 0.70% |

| 12:30 | USD | PPI M/M Aug | 0.70% | 0.40% | 0.30% | 0.40% |

| 12:30 | USD | PPI Y/Y Aug | 1.60% | 1.20% | 0.80% | |

| 12:30 | USD | PPI Core M/M Aug | 0.60% | 0.20% | 0.30% | 0.50% |

| 12:30 | USD | PPI Core Y/Y Aug | 2.20% | 2.20% | 2.40% | |

| 12:30 | USD | Initial Jobless Claims (Sep 8) | 220K | 229K | 216K | 217K |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:00 | USD | Business Inventories Jul | 0.10% | 0.00% | ||

| 14:30 | USD | Natural Gas Storage | 51B | 33B |

US PPI rose 0.7% mom in Aug, highest since Jun 2022

US PPI for final demand rose 0.7% mom in August, above expectation of 0.4% mom. That's also the largest monthly increase since June 2022.

80% of the rise in PPI is attributable to the 2% mom jump in PPI goods, highest since June 2022, mostly attributable to energy prices which was up 10.5% mom. Prices for services rose 0.2% mom.

For the 12 months ended in August, PPI rose 1.6% yoy, above expectation of 1.2% yoy.

PPI less foods, energy, and trade services rose 0.3% mom. For the 12 months period, PPI less foods, energy, and trade services was up 3.0% yoy, largest annual advance since April.

US retail sales up 0.6% mom, ex-auto sales up 0.6%, above expectations

US retail sales rose 0.6% mom to USD 697.6B in August, above expectation of 0.2% mom. Ex-auto sales rose 0.6% to USD 564.0B, above expectation of 0.4% mom. Ex-gasoline sales rose 0.2% mom to USD 642.3B. Ex-auto & gasoline sales rose 0.2% mom to USD 508.8B

In the three months through August, sales were up 2.2% yoy from the same period a year ago.

Dovish ECB hike, peak reached already, 2024 & 2025 core inflation and growth downgraded

ECB delivers a dovish 25bps rate hike today. The accompany statement indicated that the current tightening cycle could have reached its peak already. Also, core inflation and growth forecasts for 2024 and 2025 were revised down.

The newly set rates are as follows: main refinancing operations rate at 4.50%, marginal lending facility rate at 4.75%, and deposit facility rate at 4.00%.

ECB President cited the persistent nature of inflation being "too high for too long" as the primary motivator behind this strategy to "reinforce progress" in ushering inflation back to the target in a "timely manner".

ECB added, "the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target". Future decisions will "ensure" that the interest ares are set at "sufficiently restrictive levels for as long as necessary.

In the new economic projections, inflation is forecast to be at 5.6% in 2023 (prior projection at 5.1%), 3.2% in 2024 (prior 3.0%) and 2.1% in 2025 (prior 2.3%). The upward revision for 2023 and 2024 mainly reflects a higher path for energy prices.

Core inflation is projected to average 5.1% in 2023 (unchanged), 2.9% in 2024 (prior 3.0%), and 2.2% in 2025 (prior 2.3%).

Growth is projected to be at 0.7% in 2023 (prior 0.9%), 1.0% in 2024 (prior 1.5%), and 1.5% in 2025 (prior 1.6%).