Sample Category Title

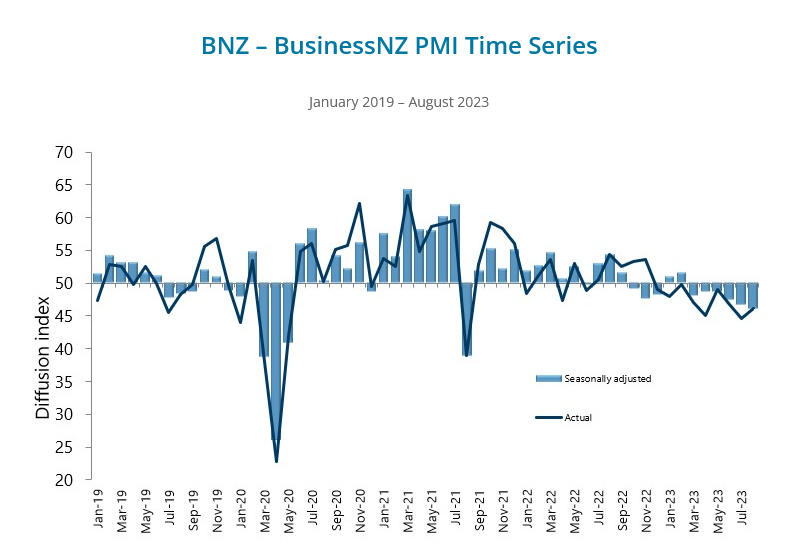

NZ BNZ PMI falls to 46.1, manufacturing activity slumps to multi-year low

New Zealand's manufacturing sector experienced a further slowdown in August, with BusinessNZ Performance of Manufacturing Index falling slightly from 46.6 in July to 46.1. This marks the lowest rate of activity for a non-pandemic affected month since June 2009. Furthermore, the latest PMI data sits significantly below its long-term average of 52.9.

A closer look at the August data reveals: Production observed a modest increase, moving from 43.1 to 43.9. Employment metrics improved, rising from 44.8 to 47.7. New orders experienced a minor uptick, growing from 45.5 to 46.6. Finished stock levels retreated slightly from 52.7 to 52.1. Deliveries, however, showed more promise, escalating from 42.9 to 47.7.

Despite the grim headline figure, it is noteworthy that there was a slight decrease in the proportion of negative comments, standing at 66.7%, a marginal relief compared to July's 72%. However, the level of pessimism mirrored that of May, maintaining the same rate of 66.7%. The pervasive market uncertainty stemming both from domestic and offshore influences, coupled with rising costs and weather-impacted demand, continued to be highlighted as primary drivers for the negative sentiment pervading the industry.

BNZ Senior Economist Craig Ebert expressed concern over the PMI's latest results, noting that while the headline figure had seen much lower points during previous recessions, the composition of August figures brought little consolation. Ebert pinpointed new orders and production as substantial drags on the performance, trailing behind the standard levels by 8.0 and 9.5 points respectively.

Fed Preview: Plotting the Way Forward

- We expect the Fed to maintain rates unchanged in the next week's meeting, as widely anticipated in the markets.

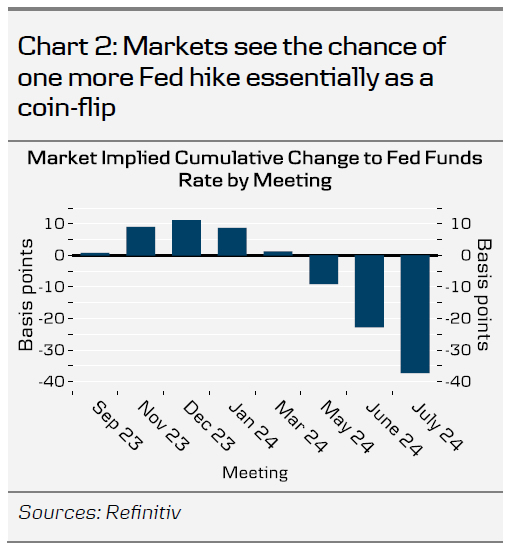

- Markets will focus on how FOMC participants assess the need for later hikes. In June, 12 out of 18 'dots' looked for one more hike, but we doubt it will materialize.

- Markets have bought into the 'higher for longer' narrative, and the consequent tightening in financial conditions limits the need for further hikes.

The Fed has made it clear it has the room to remain on hold for September, while keeping the door open for later hikes if needed. But the outlook beyond next week's Wednesday is everything but clear, as Q3 GDP Nowcast estimates range from St. Louis Fed's -0.3% all the way to Atlanta Fed's +4.9%, with only two weeks left of the quarter. In any case, markets have bought into the Fed's view of maintaining rates higher for longer, which is in stark contrast to the speculation seen 6M ago, when first cuts were being priced already for the next week's meeting.

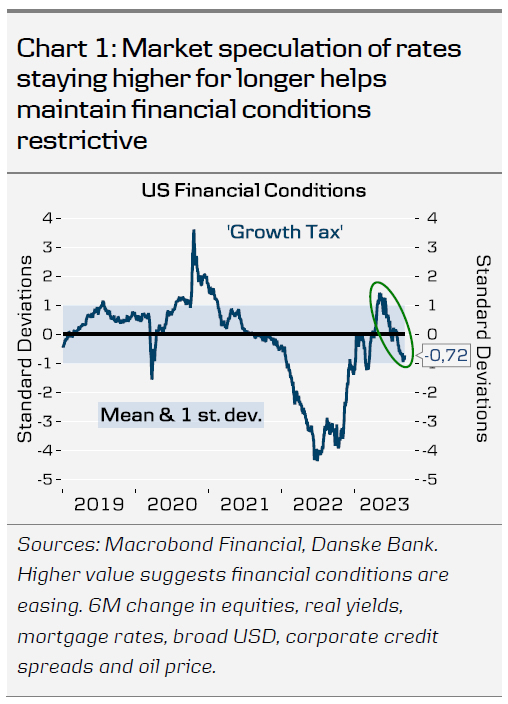

Counter-intuitively, this reduces the need for hikes going forward, as financial conditions have tightened over the summer. Our in-house 'growth tax' measure (Chart 1, 6M change in financial conditions), is at the most restrictive level since the collapse of SVB, not least reflecting higher mortgage rates and stronger USD, but also higher oil prices. With real yields at the highest levels since the GFC, it only makes sense that the Fed is turning more cautious on growth, even if we see no imminent signs of rapid weakening.

Market prices in around four 25bp rate cuts for 2024, which would still leave monetary policy stance fairly restrictive in real terms. And as QT continues to provide passive tightening in 2024 as well, we think the nominal policy rate has already reached a sufficiently restrictive level. Further hikes could be justified, if the underlying growth backdrop is significantly stronger than we have anticipated, for example reflecting the past fiscal support to investments (see Research US, 22 August). But for now, our baseline GDP forecasts remain on the bearish side of the spectrum, +1.9% for 2023 and +0.6% for 2024.

With little need to pre-commit to any policy action, we expect Powell to deliver a balanced message, highlighting positive development in cooling labour demand and recovering supply, but underscoring that there is still ways to go before declaring victory over inflation.

Strong realized data likely warrants an upward revision to the GDP projections, but the main focus will be on the 'dots', and if some of the 12 participants calling for 5.50-5.75% terminal rate have reverted their call for another hike. Leading up to the blackout, only two out of 12 voters were in favour of holding rates steady from here, while three favoured hikes at a later stage, leaving majority of the voter views still unclear.

This leaves the door open for market volatility during the meeting. We expect long treasury yields to decline gradually over the coming months as the probability of further rate hikes is being priced out, cuts (expected to start in Q1 2024) are drawing closer and weaker US inflation/growth data is dampening long term market inflation expectations. We expect the 10Y UST yield to end the year at around 4%, and see EUR/USD at 1.06/1.03 in 6/12M.

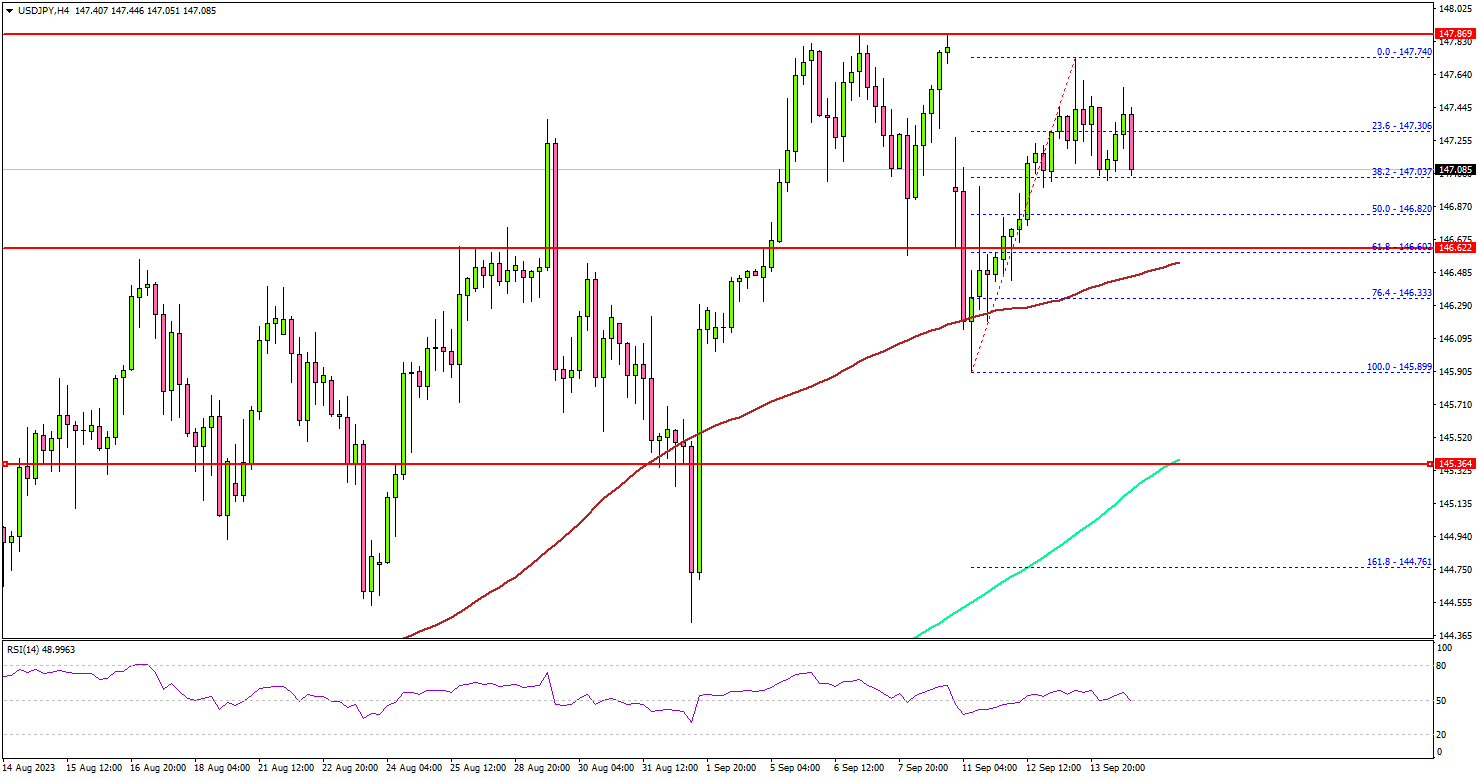

USD/JPY At Risk of Bearish Reaction, Oil Price Extends Rally

Key Highlights

- USD/JPY is struggling to clear the 147.80 resistance zone.

- A major support is forming near 146.60 on the 4-hour chart.

- EUR/USD took a hit and traded below the 1.0700 support.

- Crude oil prices rallied further and climbed above the $90.00 level.

USD/JPY Technical Analysis

The US Dollar made a couple of attempts to clear 147.80 against the Japanese Yen but failed to gain traction. USD/JPY is now showing a few bearish signs below 147.50.

Looking at the 4-hour chart, the pair climbed higher nicely above the 147.00 level. However, the bears seem to be active near the 147.80 resistance zone. The pair failed on more than two occasions to settle above 147.80.

It is now correcting gains below 147.50. On the downside, immediate support is near 146.80, and the 50% Fib retracement level of the upward move from the 145.89 swing low to the 147.74 high.

The next key support is seen near the 146.60 level or the 100 simple moving average (red, 4 hours). If there is a move below 146.60, the pair could dive toward 146.00. Any more losses might send the pair toward the 145.35 level or the 200 simple moving average (green, 4 hours).

If there is another increase, the pair might face resistance near 147.50. The next major resistance is near the 147.80 zone. A close above 147.80 could start another decent increase.

In the stated case, the pair could rise toward the 148.40 level. Any more gains might send USD/JPY toward the 150.00 handle.

Looking at EUR/USD, the pair failed to start a recovery wave and extended its drop below the 1.0700 level.

Economic Releases

- US Industrial Production for August 2023 (MoM) – Forecast 0.1%, versus 1% previous.

- Michigan Consumer Sentiment Index for Sep 2023 (Prelim) – Forecast 69.1, versus 69.5 previous.

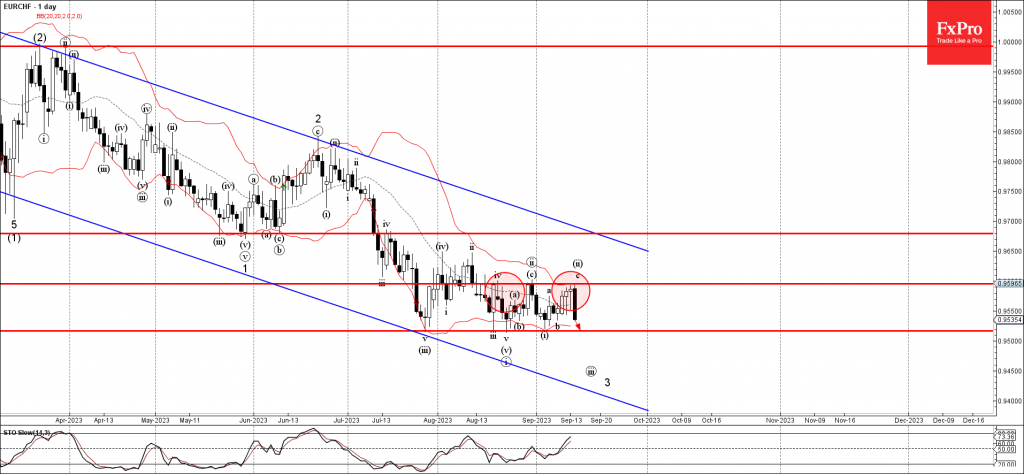

EURCHF Wave Analysis

- EURCHF reversed from resistance level 0.9595

- Likely to fall to support level 0.9515

EURCHF currency pair recently reversed down from the resistance level 0.9595 (which has been reversing the pair from last month) intersecting with the upper daily Bollinger Band.

The downward reversal from the resistance level 0.9595 stopped the minor ABC correction ii.

Given the clear daily downtrend, EURCHF currency pair can be expected to fall further toward the next support level 0.9515 (low of the previous waves v, ii, v, and (i)).

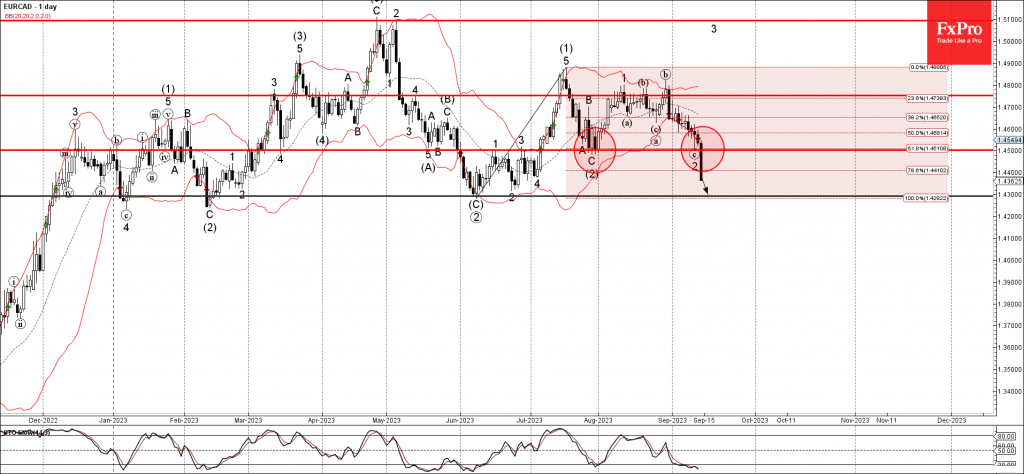

EURCAD Wave Analysis

- EURCAD broke the support level 1.4500

- Likely to fall to support level 1.4300

EURCAD currency pair recently broke the support level 1.4500 (low of the previous ABC correction (2)) intersecting with the 61.8% Fibonacci correction of the upward impulse (1) from June.

The breakout of the support level 1.4500 accelerated the active ABC correction 2.

Given the strong CAD purchases, EURCAD currency pair can be expected to fall further toward the next support level 1.4300 (former multi-month low from June).

ECB Review: Confirmed – A Final Rate Hike, But Restrictive Policies Not Over

- Today, the ECB delivered a 25bp rate hike and indicated that it is now on pause, which is fully in line with our expectation.

- ECB still expects inflation will 'remain too high for too long', but it now wants to work with the 'patience' argument more than the 'level' argument for additional hikes, i.e. see the lagged effect of the monetary policy tightening already implemented impact the inflation outlook.

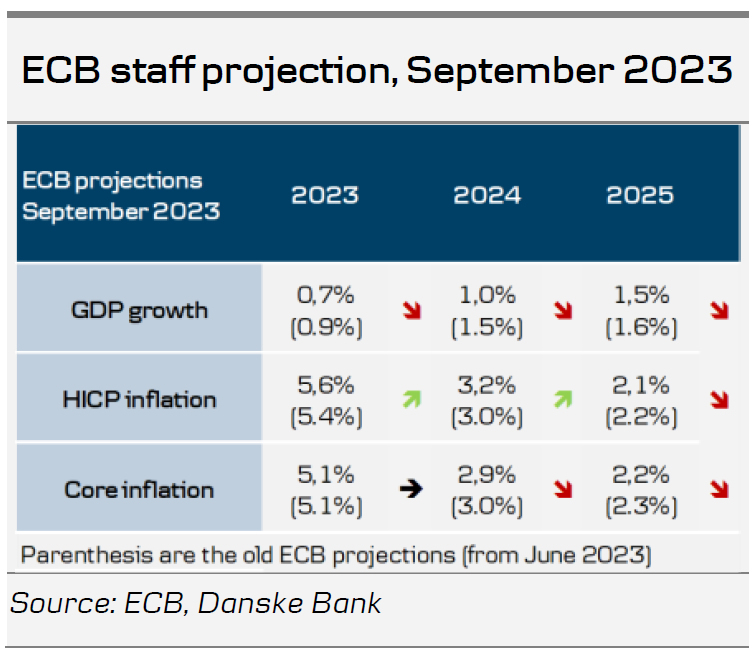

- The ECB's staff inflation projection was revised higher for 2023 and 2024 but lower for 2025. For core inflation, the projection is now slightly lower across the board.

- We recommend to pay the December 2023 ECB meeting.

No additional ECB hikes

Today, the ECB announced that all three policy rates will be hiked by 25bp (effective from 20 September) and guided that it will not make any more hikes for now. In our view, the monetary policy statement can best be described as a balancing act in a stagflationary-ish environment. The ECB's clear message to markets is that inflation is still too strong, but economic activity and the outlook are weaker. As a result, today's decision should be seen as a compromise in the governing council. During the Q&A session, president Lagarde also said that today's hike was taken on the back of a 'solid majority' as 'some' members favoured a pause to see how the monetary policy decisions already taken so far are working through the economy.

It was somewhat surprising to us that the ECB didn't include much optionality for additional rate hikes, should the incoming data warrant it. The guidance provided was clear the ECB is on pause for now as it weighs the weakening economic outlook and its impact on inflation. As usual, Lagarde also highlighted that the three key elements still prevail in their reaction function: monetary policy transmission, inflation outlook and the economic and financial data. As such, given the current information, the ECB is done with further hikes, but should economic acitivity hold up better than anticipated or inflation see another rise near term, the ECB is ready to adjust its policy rate. Overall, we see the ECB's monetary policy-setting approach focusing on the 'patience' argument and not the 'level' one.

During the Q&A session, Lagarde also said that the transmission channel is working faster in the current hiking cycle than in previous hiking cycles.

The ECB didn't discuss advancing PEPP reinvestments or potential APP sales today. The Italian-German bond spread tightened marginally on the ECB not having discussed further balance sheet normalisation.

Cooling economy lowers staff projection of growth and core inflation

Lagarde characterised the current economic environment as a period with sluggish growth. The service sector now looks weak too, but real incomes will underpin consumer spending. The labour market is still strong amid signals that employment demand is fading. Lagarde stressed that the ECB expects inflation to decline significantly in the coming months due to base effects from energy prices last year. However, inflation is expected to remain too high for too long.

The new staff projections revised the inflation forecast higher for 2023 and 2024 but lower for 2025. Headline inflation is now expected at 5.6% in 2024 (vs 5.4% in June), 3.2% in 2024 (vs 3.0% in June) and 2.1% in 2025 (vs 2.2% in June). The upward revisions mainly reflect a higher path for energy prices since the forecast in June. The ECB revised down projections for core inflation by 0.1pp for both 2023 and 2024, while 2025 was left unchanged. The ECB acknowledged that underlying inflationary pressure remains high, even though most indicators have started to ease. The lower estimate for core inflation reflects that the previous policy tightening is working its way through financial conditions into the real economy. Hence, the wage forecast for 2024 was revised down to 4.3% from 4.5% in June. The ECB lowered the forecast for growth to 0.7% in 2023 (vs 0.9% in June), 1.0% in 2024 (vs. 1.5% in June) and 1.5% in 2025 (vs. 1.6% in June). Most of the downward revision for 2024 is due to carry over from sluggish growth in second-half 2023.

Risks to the economic outlook are tilted to the downside due to stronger monetary policy transmission and weak external demand. These two factors pose downward risks to the inflation outlook while upside risks to inflation include higher than expected energy prices, wage increases and profits.

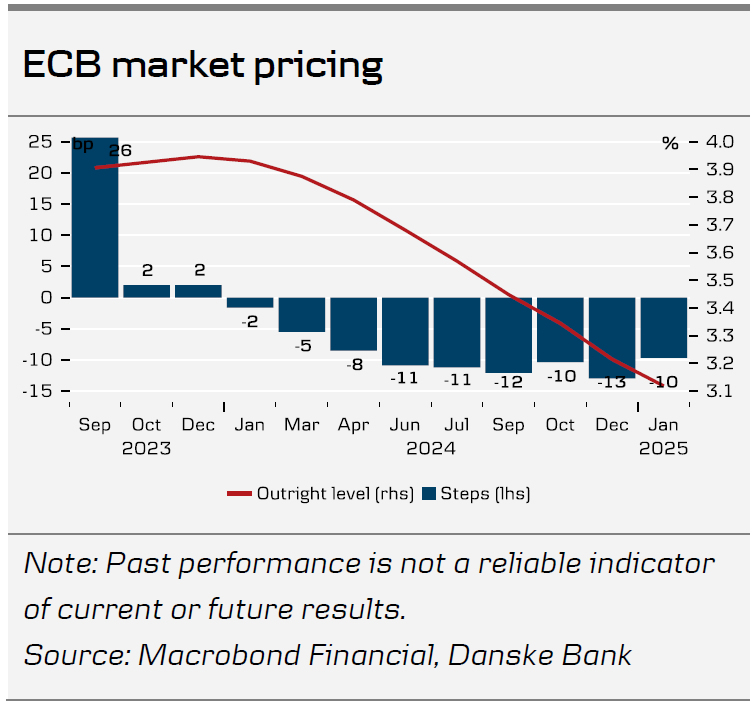

ECB has finished hiking, but paying the Dec ECB meeting is attractive from a risk-reward perspective

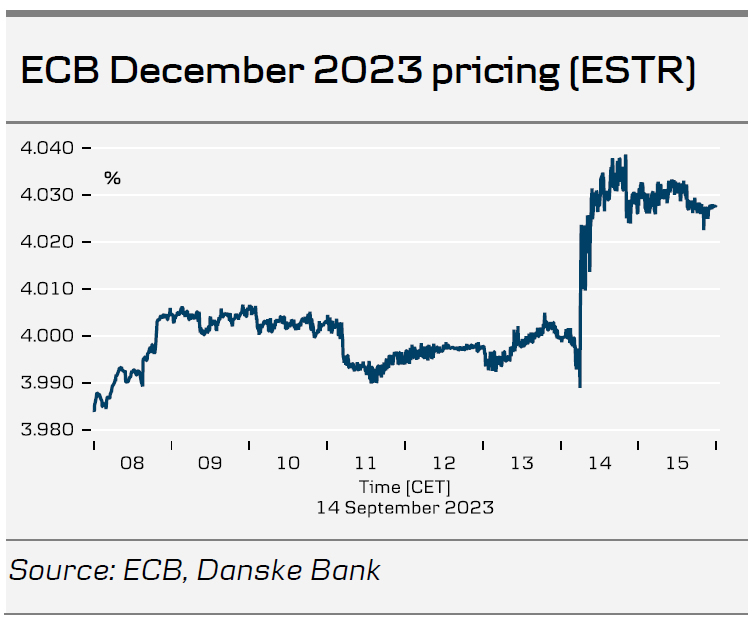

With the ECB guiding that its policy rate has 'reached levels that have been maintained for a sufficiently long duration', we observe that markets are pricing 4bp of additional hikes this year. And while our baseline is for the ECB not to make further rate hikes, we still recommend to pay the Dec23 ECB meeting with an entry level of 4bp and a target of 12bp, which we perceive as an attractive risk-reward. With the ECB's hike today, we book a 19.5bp profit on our paid September ECB meeting, which we initiated on 1 September. Markets are pricing 73bp of rate cuts in 2024, which is 7bp more than before the meeting.

EUR weakness and USD strength

EUR/USD first declined towards 1.07 on the dovish 25bp rate hike from the ECB, and shortly after further declined well below the 1.07 mark on stronger-than-expected US retail sales. The USD broadly strengthened in the G10 space, while the EUR fell to its weakest level since May this year. Altogether, the dovish hike from the ECB and ongoing US outperformance are weighing on the cross. The next big event for the cross should be the Fed meeting on 20 September. We expect a relatively muted market reaction on that meeting, as it is highly expected that the Fed will be on hold.

Overall, we make no changes to our EUR/USD forecast, and hence we maintain our strategic case for a lower EUR/USD based on relative terms of trade, real rates and relative unit labour costs. As we deem that peak rates have now been reached – we do not expect further rate hikes from the Fed or the ECB – we expect the relative strength of the US economy to continue weighing on the EUR/USD in the coming months as growth differentials take the driver's seat, and we continue to forecast the cross at 1.06/1.03 in 6/12M. As it is hard to imagine a sudden change of the current USD momentum, and with commodity prices currently rising, we may reach our 6M forecast for the cross earlier than expected.

ECB Delivers Dovish Final Rate Hike of the Tightening Cycle

The ECB raised interest rates again today, probably for the last time in the tightening cycle although it did leave itself some flexibility on that front.

This certainly falls into the dovish hike category, with the ECB acknowledging inflation remains too high but also that growth is suffering. What's more, it clearly indicated that it believes the current stance should be tight enough to return inflation to target, given time.

It would appear the decision wasn't unanimous though, with only a solid majority backing the decision. Again, we shouldn't be surprised at this stage of the cycle that, considering the uncertain outlook, not everyone is in agreement on their assessment of the situation.

The euro slipped after the decision and following comments from President Christine Lagarde, as did euro area yields. Further progress on inflation over the coming months, as the ECB anticipates, should enable pauses over the coming meetings, at which point the focus will gradually shift to the timing of the first rate cut.

Sunset Market Commentary

Markets

The ECB today hiked rates by 25 bps in a decision supported by a “solid majority”. The deposit rate now stands at a record 4%. As per bond portfolios, Lagarde explained there was no discussion about a potential quicker rundown of APP (through active sales) or PEPP (through a sooner than currently communicated ending of reinvestments). Frankfurt’s statement opens with “Inflation continues to decline but is still expected to remain too high for too long.” Indeed, projections were lifted upwards for this year and the next by 0.2 ppts to 5.6% and 3.2% respectively, mainly on the account of higher energy prices. The 2025 forecast was lowered marginally to 2.1% (-0.1 ppt). Core inflation is seen at 5.1% this year, 2.9% in 2024 and 2.2% in 2025 with minor downward revisions for the latter two. In any case, all gauges remain above the 2% target over the policy horizon, warranting another hike “to reinforce progress towards its target”. Related to this, ECB president Lagarde said that some indicators of inflation expectations must be monitored carefully. We assume the 5y5y forward inflation swap (rising to 2.6%) is one of those. GDP forecasts were cut (sharply) in every year through 2025 amid further tightening of financing conditions and weakening domestic & external demand. Growth is expected at 0.7% this year (-0.2 ppts vs June), 1% in 2024 (-0.5 ppts) and 1.5% in 2025 (-0.1 ppt). Risks remain tilted to the downside. The ECB retains policy rate optionality through its data-dependent approach and Lagarde later refused to say rates indeed hit their peak. However, the statement this time also added that “Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target.” It’s a dovish twist that does suggest the tightening cycle has ended. Despite that it clearly states rates are needed at a high enough level for a long enough period, it immediately sparked market speculation about the timing of a first rate cut. German Bunds strengthen following today’s decision as a result, even as it wasn’t fully priced in. Yields lose between 1.6-6.7 bps with the belly of the curve outperforming. The euro slips. EUR/USD specifically was additionally hit by a dollar-supporting triple whammy of strong US retail sales, higher than expected PPI numbers and another consensus-beating reading of US jobless claims. The pair trades at the lowest level since early June around 1.067.

News & Views

Inflation in Sweden for the second consecutive month declined faster than expected. August headline inflation printed at 0.1% M/M and 7.5% Y/Y (0.0% M/M and 9.3% in July). The Riksbank’s reference, CPIF inflation (using a fixed interest rate), eased -0.1% M/M to 4.7% Y/Y (was -0.2% M/M and 6.4% Y/Y in July). Core CPIF (ex. energy), was reported at -0.3 M/M and 7.2% Y/Y (from 8.0%). Despite the easing, 0.5%+ M/M rises were still registered for several sub-categories, suggesting still broad-based underlying inflationary tendencies. The August inflation data probably won’t change the scenario for the Riksbank to raise its policy rate by 25 bpn to 4.0% next week. In the June policy statement, the RB indicated it intended to raise the policy rate at least one more time this year. However, this ‘commitment’ didn’t help the Swedish currency, with the krone setting a new all-time low against the euro in august and holding near that level. Weakness of the currency became an important topic for RB policy. Giving higher rates outside Sweden, further interest rate support beyond next week is probably needed to change SEK fortunes. EUR/SEK hovered near 11.94 post the inflation data, with the all-time top (low for the krone) at EUR/SEK 11.963.

A quarterly survey of the Norges bank questioning regional contacts in the country shows participants expect output growth at 0.3% in Q3 2023 Q3 followed by a slowdown to 0.1% in Q4. Reduced construction activity and weaker household demand are dampening activity growth, while investment related to energy production, and commercial services continues to rise. A number of contacts also point out that the krone depreciation over the past year has helped improve Norwegian firms’ competitiveness. Contacts expect annual wage growth of 5.4% in 2023 and 4.6% in 2024. At the same time, contacts report reduced profitability in Q3 compared with the same time in 2022. The Norges Bank holds a policy meeting Thursday next week where it is expected to raise the policy rate by 25 bps to 4.25%, potentially marking the end of the rate hike cycle. The krone (EUR/NOK 11.5) currently hovers in a short-term consolidation pattern between EUR/NOK 11.40/60.

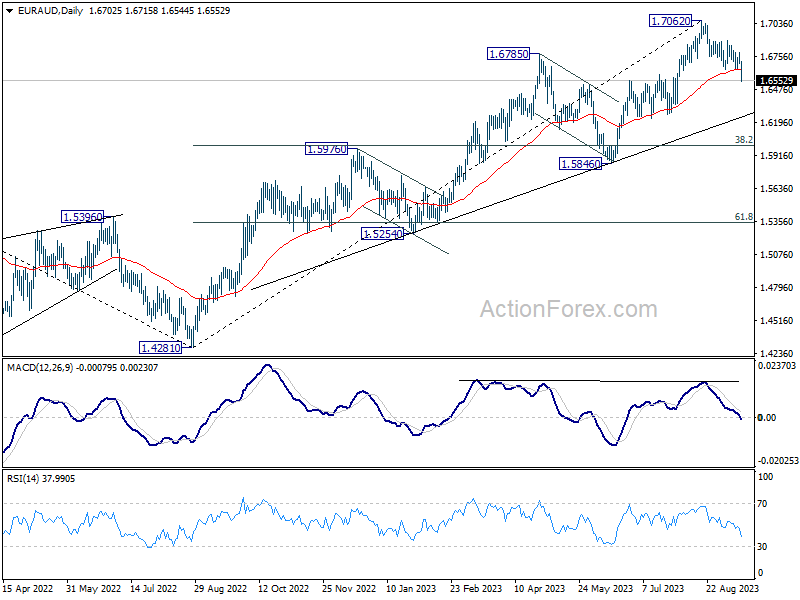

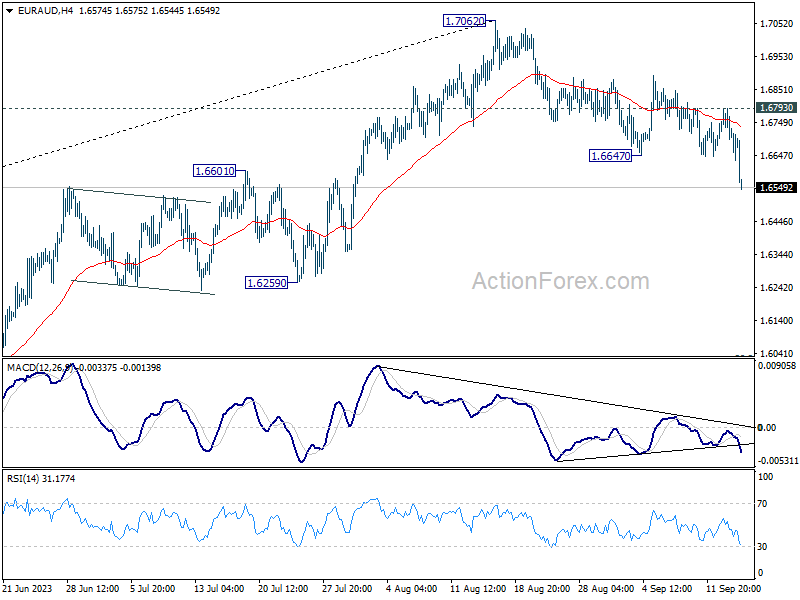

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6675; (P) 1.6735; (R1) 1.6770; More...

EUR/AUD's decline from 1.7062 resumes by breaking through 1.6647 support. Intraday bias is back on the downside for 1.6601 support next. On the downside, break of 1.6793 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, Fall from 1.7062 could be seen as correction to whole up trend from 1.4281 (2022 low). Sustained trading below 55 EMA (now at 1.6644) would affirm this case and target 38.2 retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt.