Sample Category Title

(ECB) Monetary policy decisions

Inflation continues to decline but is still expected to remain too high for too long. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. In order to reinforce progress towards its target, the Governing Council today decided to raise the three key ECB interest rates by 25 basis points.

The rate increase today reflects the Governing Council's assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission. The September ECB staff macroeconomic projections for the euro area see average inflation at 5.6% in 2023, 3.2% in 2024 and 2.1% in 2025. This is an upward revision for 2023 and 2024 and a downward revision for 2025. The upward revision for 2023 and 2024 mainly reflects a higher path for energy prices. Underlying price pressures remain high, even though most indicators have started to ease. ECB staff have slightly revised down the projected path for inflation excluding energy and food, to an average of 5.1% in 2023, 2.9% in 2024 and 2.2% in 2025. The Governing Council's past interest rate increases continue to be transmitted forcefully. Financing conditions have tightened further and are increasingly dampening demand, which is an important factor in bringing inflation back to target. With the increasing impact of this tightening on domestic demand and the weakening international trade environment, ECB staff have lowered their economic growth projections significantly. They now expect the euro area economy to expand by 0.7% in 2023, 1.0% in 2024 and 1.5% in 2025.

Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target. The Governing Council's future decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary. The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, the Governing Council's interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.

Key ECB interest rates

The Governing Council decided to raise the three key ECB interest rates by 25 basis points. Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be increased to 4.50%, 4.75% and 4.00% respectively, with effect from 20 September 2023.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

As concerns the PEPP, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

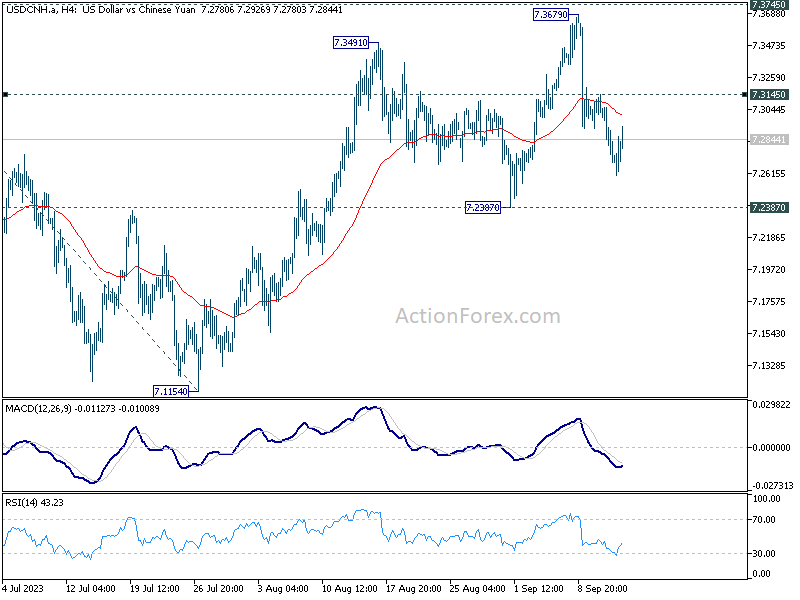

PBOC cuts reserve requirement ratio to release CNY 500B liquidity

People's Bank of China slashed the Reserve Requirement Ratio for a majority of banks by 25bps today. This marks the second such reduction in this calendar year, aiming to spur liquidity in the market and support the economy. Following this adjustment, the weighted average RRR for banks will stand at 7.4%. This strategic step is slated to unleash medium to long-term liquidity exceeding CNY 500B (approximately USD 68.7B) into the financial system.

In the aftermath of this announcement, the offshore Yuan experienced a mild depreciation, fueling a recovery in the USD/CNH from its day low at 7.2603. While fall from 7.3679 could extend lower, strong support is likely at around 7.2387 to contain downside to bring rebound. Break of 7.3145 resistance will bring stronger rise back to 7.3679. But for the near term, some more range trading is likely because USD/CNH would have enough momentum to take on 7.3745 high.

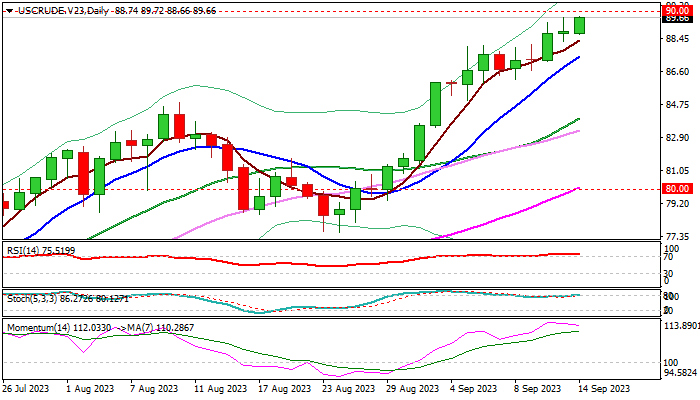

WTI Oil: Bulls Eye $90 Barrier, Underpinned by Tight Supply Outlook

WTI oil keeps firm tone and hit new multi-month high on Thursday, approaching psychological $90 barrier.

Tighter global supply outlook on the recent decision of Saudi Arabia and Russia to extend production cut until the end of the year, keeps the price supported and offsetting concerns over weakening economic growth and rise in US crude inventories.

Bulls pressure $90 pivot, break of which would generate fresh bullish signal, in addition to violation of pivotal Fibo resistance at $89.06 (38.2% of $130.48/$63.45) and open way for extension towards $93.30/70 (Oct/Nov 2022 lower platform) and $96.07 (50% retracement).

Bullish daily studies underpin, however overbought conditions may produce headwinds at $90 barrier.

Dips should ideally find footstep above rising daily Tenkan-sen ($87.35) and extensions lower not to exceed $84.87 (former top of Aug) to keep larger bulls in play and offer better buying opportunities.

Res: 90.00; 92.64; 93.30; 93.72.

Sup: 88.27; 87.35; 85.92; 84.87.

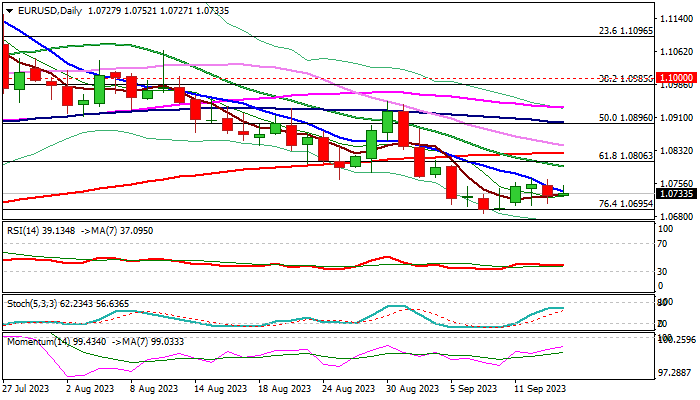

EUR/USD: ECB’s Verdict Expected to Define Near-term Direction

EURUSD is in a quiet mode in European session on Thursday, awaiting fresh direction signals from the ECB’s decisions on today’s policy meeting.

Near-term action remains at familiar levels, near the mid-point of a narrow range which extends into sixth consecutive day.

Larger bears from new 2023 high (1.1275) are pausing above Fibo support at 1.0695 (76.4% retracement of 1.0516/1.1275) which so far contained several attacks, but the upside remains protected by falling 10DMA (currently at 1.0738), keeping the pair in extended consolidation.

Technical studies on daily chart are bearish, with 14-d momentum holding in negative territory and Tenkan-sen / Kijun-sen in increasingly bearish configuration, adding to downside risk.

Bears need firm break of 1.0695 Fibo support to signal continuation of larger downtrend and expose next pivotal levels at 1.0635/11 (2023 low / Fibo 38.2% of 0.9535/1.1275 rally).

Conversely, lift above 10DMA would ease immediate downside risk, however sustained break above 200DMA (1.0827) is needed to sideline bears and open way for stronger recovery.

The European Central Bank is holding its policy meeting today and facing a difficult task in decision whether to raise its key interest to new record high in continuous fight with inflation, or to stay on hold as bloc’s economic conditions are deteriorating.

Eurozone inflation is still 2 ½ times above 2% target, with darkened outlook for 2024 adding to argument for a rate hike, as policymakers fear that inflation may get stuck at higher levels for a longer period.

On the other hand, weak economic indicators send strong warning that negative impact from high interest rates could push the economy into recession.

Res: 1.0768; 1.0796; 1.0827; 1.0896.

Sup: 1.0695; 1.0667; 1.0635; 1.0611.

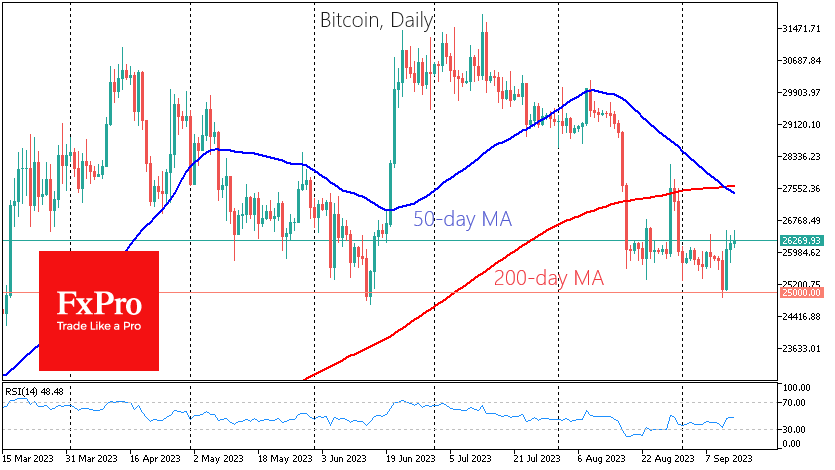

Temporary Relief for Bears in Crypto

Market picture

The crypto market capitalisation rose 1.2% in 24 hours to $1,043. The market’s fall to almost $1 trillion at the beginning of the week satisfied the sellers. The question is whether the recent dip will be the starting point for the next rally. Keep an eye on the activity near the recent highs; for now, the market is not allowed to go higher.

For bitcoin, the death cross has not yet led to an intensified sell-off. The accumulated oversold condition that has exhausted the sellers is having an impact. Despite the potential for a rebound, BTCUSD remains within the bearish momentum that has been in place since July, with lower and lower highs and lows.

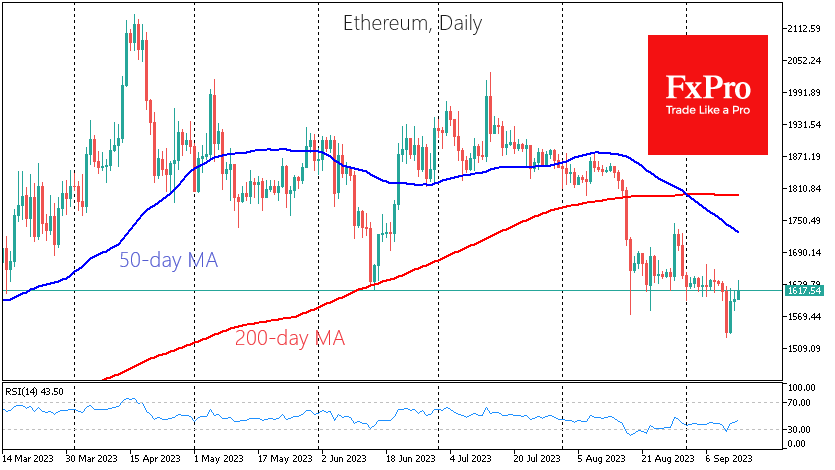

Ethereum, which formed a death cross at the beginning of September, remains in a downtrend, although its intensity is decreasing.

News background

The SEC continues to review the court’s decision in the Grayscale case, as well as numerous applications for spot bitcoin ETFs, the regulator’s head, Gary Gensler, said during a congressional hearing.

Ripple CEO Brad Garlinghouse called the US one of the “worst places” to launch crypto projects, blaming the SEC for the situation.

The bankrupt FTX has changed its cryptocurrency offering and will no longer give the markets advance notice of its upcoming sale. The court allowed FTX’s creditors to sell $3.4 billion worth of cryptocurrency to pay off their debts earlier. This amount includes $560 million in Bitcoin (BTC), $192 million in Ethereum (ETH) and $1.16 billion in SOL.

The Telegram messenger has integrated a cryptocurrency wallet based on The Open Network (TON) into the app for its more than 800 million users.

EUR/AUD Approaches Important Support Zone

Euro currency traders are focused on the ECB meeting, the decision of which will be published today at 15:15 GMT+3. There will be a press conference at 3:45 p.m.

According to Reuters, the probability of a rate hike is about 60%. The figure stood at 50% at the start of the week as the ECB's updated forecasts expect inflation to remain above 3% next year, well above its 2% target.

At the same time, Australian dollar traders experienced a spike in volatility this morning following the release of strong labor market data in Australia. Last month, the number of employed people increased by almost 65,000 people — the second highest figure in 2023.

Today, the EUR/AUD chart forms an interesting picture from the point of view of technical analysis — the price has approached an important support zone formed by the levels 1.658-1.665:

→ The level of 1.665 has already shown its impact on the rate in September. Moreover, the long lower shadow on the last bearish candle with a false breakout indicates demand in this zone.

→ The 1.658 level is a former resistance that worked effectively in June-July, and after the breakout in August, the EUR/AUD price has not yet tested it.

→ The psychological level of 1.66 can provide support.

→ The lower boundary of the ascending channel (shown in blue) may also provide support.

And it is possible that if the price falls inside the zone, the bulls will try to take advantage of the chances and resume the upward trend.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUD/USD – Buoyed by Australian Jobs Data as Markets Consider One More RBA Hike

- Australian employment increased by 64,900 in August (2,800 full-time, 62,100 part-time)

- Participation hits 67%, a new high

- Is a double bottom forming in AUDUSD?

The Australian jobs data on Thursday was surprisingly good, with the number of new jobs created vastly exceeding expectations, although the bulk were in part-time roles.

Participation also unexpectedly improved, hitting 67% for the first time which will be very welcomed by the central bank as it, and every other one around the world, seeks to defeat inflation while achieving a soft landing. That job will be much easier if the tightness in the labour market is eased through more people joining it, rather than people losing their jobs at higher interest rates bite.

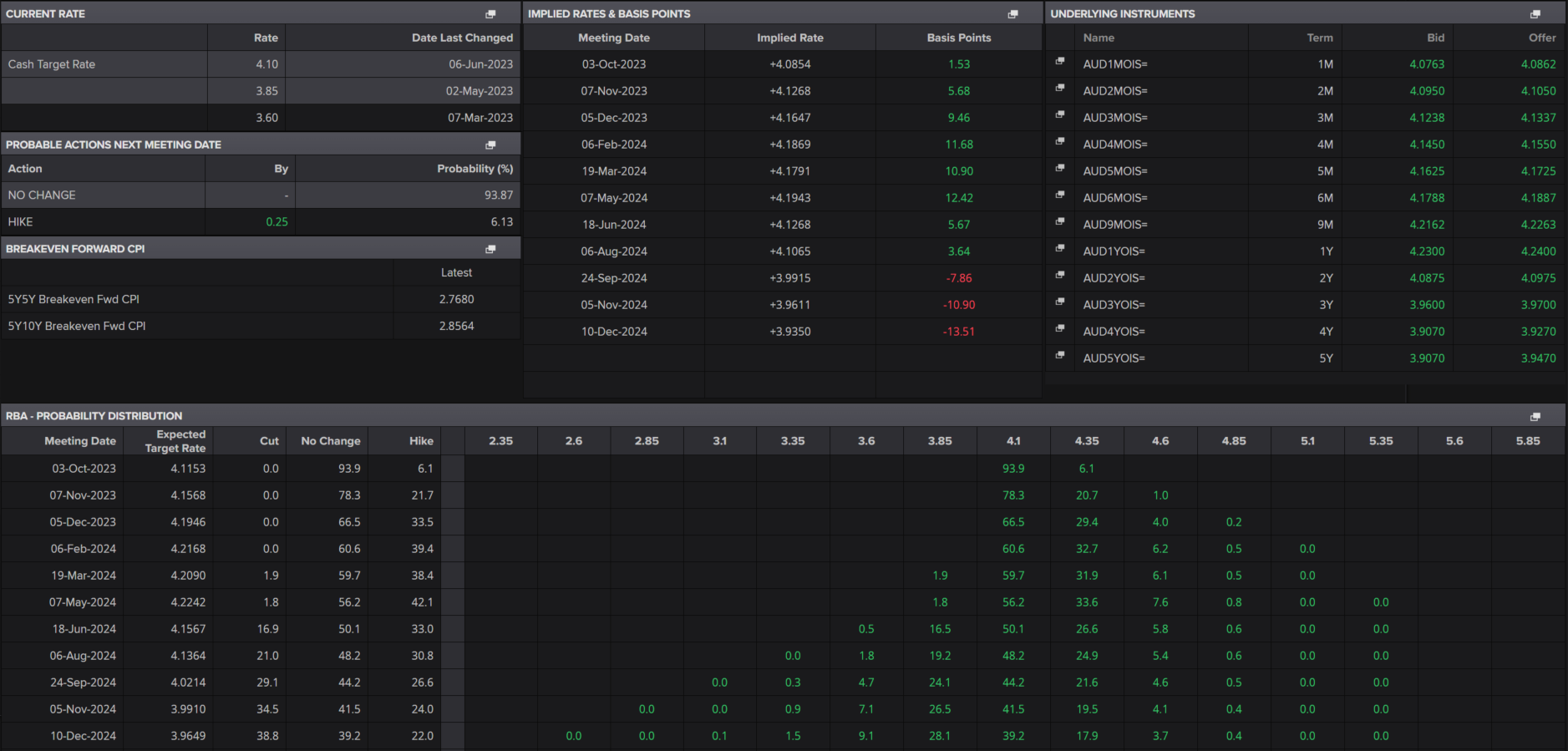

Despite these promising figures, markets are still positioning for another possible rate hike from the RBA over the coming meetings under the new leadership of Governor Michele Bullock. One more hike between now and the middle of next year is around 40% priced in which is arguably quite high under the circumstances.

RBA Interest Rate Probability

Source – Refinitiv Eikon

Aussie buoyed by jobs figures

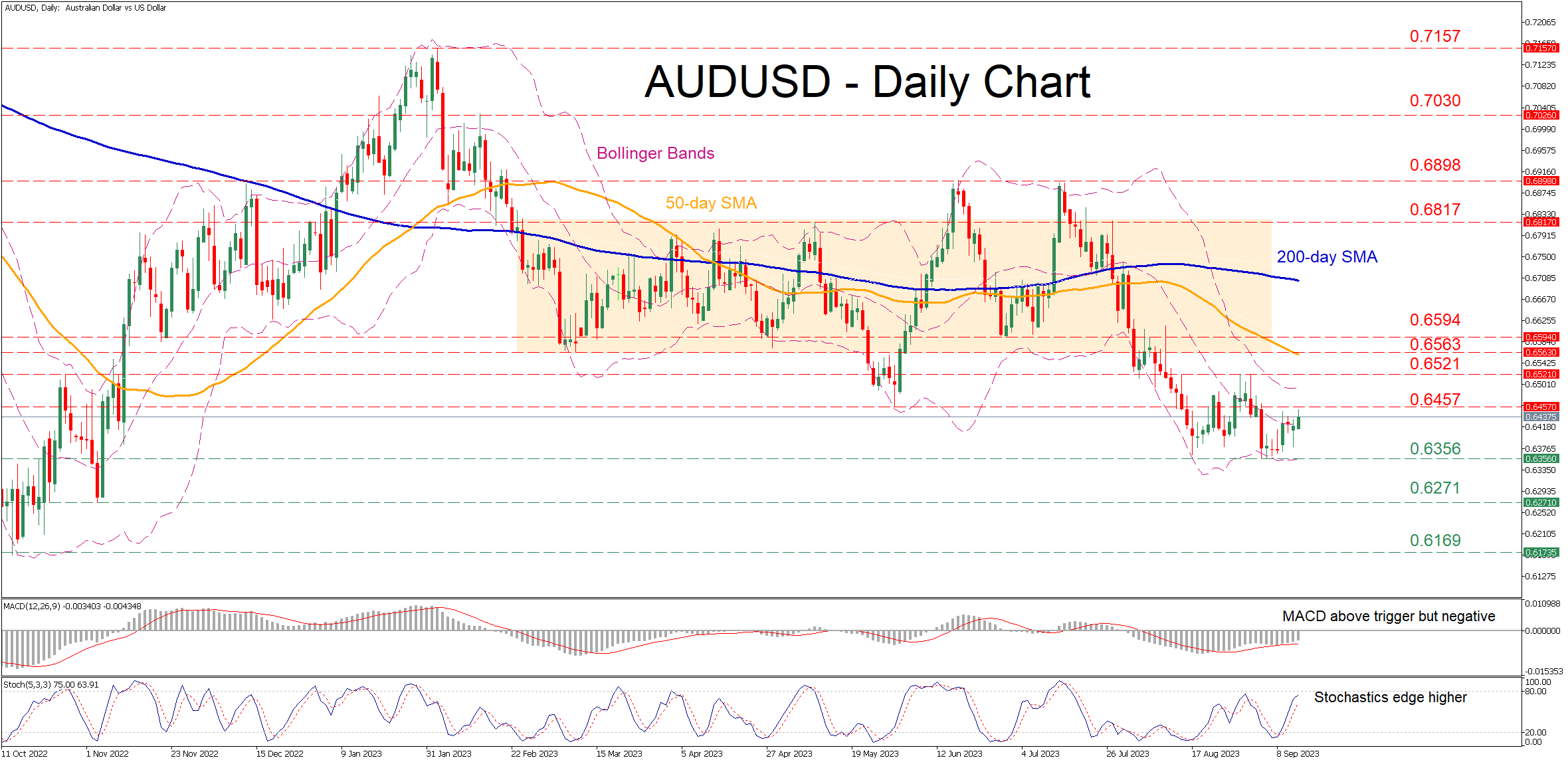

The technical picture in AUDUSD is really quite interesting. On the face of it, it’s been range-bound for the last month and therefore doesn’t look particularly exciting.

But two things stand out. One is the double top that formed between early June and August. The sell-off that followed was quite swift, falling around 230 pips over the following couple of weeks before the consolidation started. But with the double top itself being around 300 pips from the peak to the neckline, is there theoretically more to come? I’m sceptical considering how long it’s been trending sideways but it’s possible.

AUDUSD Daily

Source – OANDA on Trading View

The second is the potential double bottom that’s now formed during that consolidation period. With the neckline around 0.6520, a break above here could be quite a bullish move and, in theory, offer a possible price projection based on the size of the pattern. Obviously, there are no guarantees but a break of the neckline would make things interesting.

AUDUSD attempts recovery from 10-month low

- AUDUSD hit a fresh 10-month bottom of 0.6356 last week

- Regained some ground but clearly not out of the woods yet

- Momentum indicators suggest that the rebound could strengthen

AUDUSD had been in an aggressive decline following a double top pattern in mid-July, with the pair posting consecutive multi-month lows. Even though the price managed to find its feet at a fresh 10-month bottom and recoup some losses, the road to recovery seems rather long.

Should the negative pressures wane, the price could ascend to face the May support of 0.6457, which could now serve as resistance. Conquering this barricade, the bulls might attack the recent resistance zone of 0.6521. Further upside attempts could then stall at a couple of previous support regions such as 0.6563 and 0.6594.

Alternatively, bearish actions could send the price to re-test the 10-month low of 0.6356. A break beneath that zone could trigger a decline towards the November 2022 bottom of 0.6271. If that hurdle also fails, the spotlight may turn to the October 2022 low of 0.6169.

In brief, AUDUSD appears to have found its footing, but it has not yet recovered significant ground. For the bulls to regain confidence, the pair must at least reclaim the 50-day simple moving average (SMA).

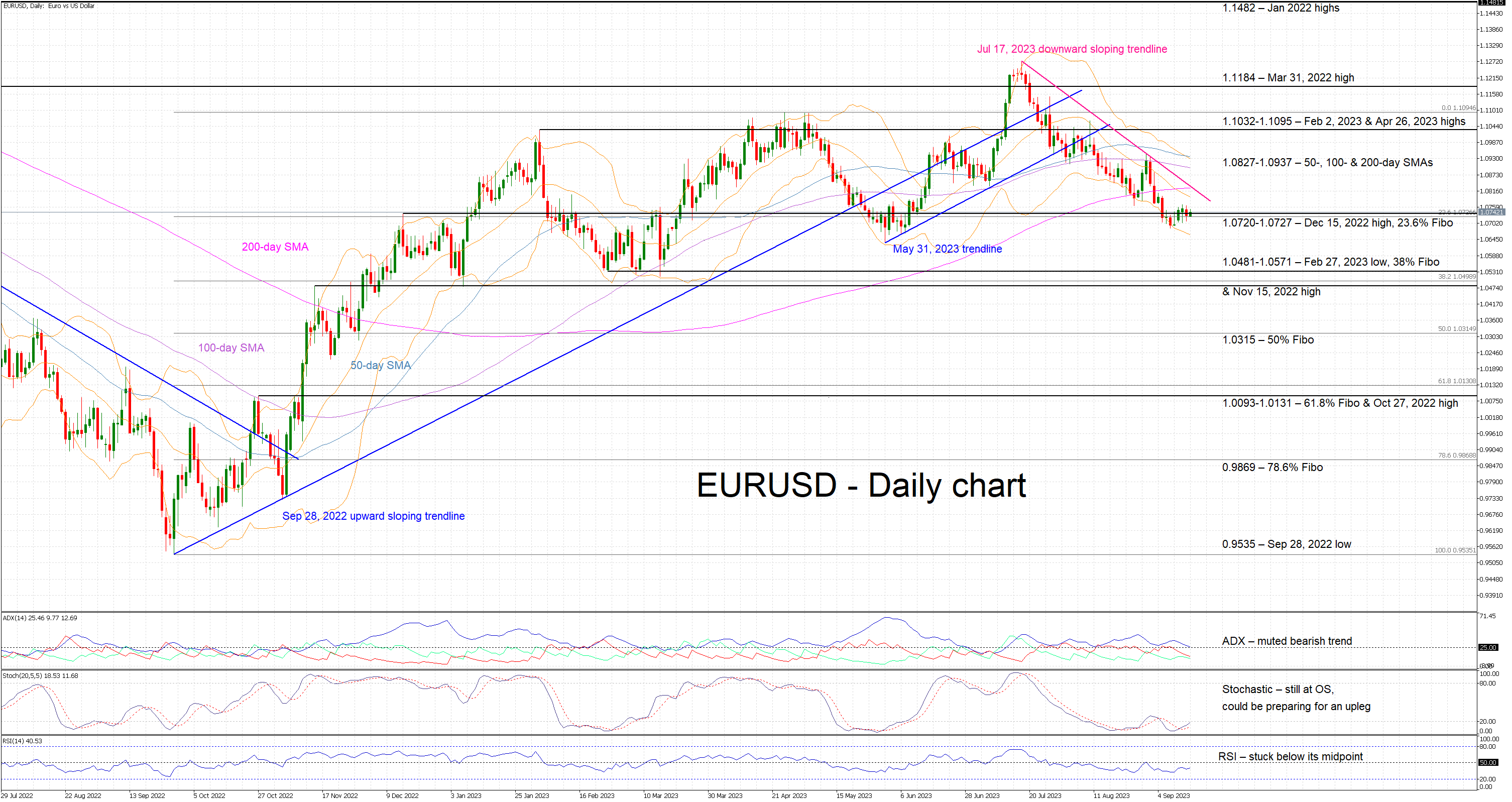

EURUSD in Waiting Mode; Bulls Desperate for a Move Higher

- EURUSD continues to hover around the 1.0720-1.0727 area

- Short-term bearish trend remains firmly in place

- But the stochastic oscillator could open the door to a bullish move

EURUSD continues to hover around the 1.0720-1.0727 area as market participants are preparing for the next key events. All eyes are on the stochastic oscillator at this juncture. It is hovering in its oversold territory, but it has surpassed its moving average and looks ready to climb above the 20 threshold and the August 31 local peak. This could be the signal the bulls have been waiting for to stage a proper rebound and test the July 17, 2023 trendline.

The remaining momentum indicators are still on the bears’ side. More specifically, the Average Directional Movement Index (ADX) is edging lower and towards its 25-threshold, thus pointing to a weakening bearish trend in EURUSD. More significantly, the RSI confirms the bearish tendency present in this market as it has been trading below its 50-midpoint since late-July.

Should the bulls decide to stage a rebound, they could try to overcome the July 17, 2023 downward sloping trendline and then test the resistance set by the 50-, 100- & 200-day simple moving averages (SMAs) in the 1.0827-1.0937 area. Even higher, they could come up against the more important 1.1032-1.1095 range, which is defined by the February 2, 2023 and April 26, 2023 highs respectively.

On the flip side, the bears could take advantage of any short-term upleg and then try to break the busy 1.0720-1.0727 area, which is populated by the December 15, 2022 high and the 23.6% Fibonacci retracement of the September 28, 2022 – April 26, 2023 uptrend respectively. Lower, they could have a look at making a new 2023 low, provided they cross the important 1.0481-1.0571 region.

To conclude, market participants remain on the sidelines ahead of the next key events with the bulls anxiously trying to stage a small rally if the stochastic oscillator provides the appropriate signal.

A 25 bps ECB Rate Hike Today is Our Preferred Scenario

Markets

August US CPI inflation data didn’t alter flagged Fed plans to keep policy rates stable at next week’s FOMC meeting. They nevertheless suggest a hawkish bias for November/December meetings as headline inflation rose at the fastest pace since June of last year (0.6% M/M). Rising energy (commodity) prices risk complicating the global disinflationary process in coming months. Core CPI rose by 0.3% M/M with the Y/Y-number down to 4.3% from 4.7%. Higher transportation (services) costs are something to look out for. US Treasuries sold off in a first instinctive move, but CPI numbers were too close to consensus to trigger a new downleg. Immediately, some return action followed with Treasuries in the end recording gains. The US $20bn 30-yr Bond auction was awarded at the highest yields since 2011 (4.345%) which was a full bp above the 1:00 PM bid yield. The bid cover ratio was slightly better than recent average (2.46). Daily changes on the US yield curve eventually ranged between -5.1 bps (2-yr) and -0.8 bps (30-yr). The US dollar whipsawed around the time of the CPI release, but eventually didn’t bother the loss of interest rate support, closing at EUR/USD 1.0730. US stock markets closed mixed (Dow -0.2%; Nasdaq +0.2%).

German Bunds underperformed following some final hawkish repositioning ahead of today’s ECB gathering. A Reuters article suggested an increase of June’s 3% inflation forecast for 2024 this afternoon, bolstering the case for a rate hike even if flanked by weaker growth prospects for this year and next. A 25 bps rate hike today is our preferred scenario as well. Apart from the pivotal inflation argument, we think that from a communication perspective the ECB will prefer a dovish/neutral hike over a hawkish skip. It allows time to extend the data-dependent approach until the December policy meeting with new quarterly updates and to pause in October. From a short-term perspective, it offers the benefit of clarity, reducing market volatility. Additionally, it buys the ECB time to review the run-off of its balance sheet with some hawkish governors suggesting to speed up the process through active sales from the APP bond portfolio or to end PEPP-reinvestments sooner than currently flagged (2025 at the earliest). We believe that today’s finetuning rate hike could push (ST) EUR rates and the euro in a first reaction higher, but like US CPI data yesterday we fear that especially on FX markets this could be short-lived as it will be perceived as the ECB’s final hike. Moves on FI markets could last more with the ECB stressing the need to keep policy restrictive for a long time.

News and views

Australian employment grew by 64.9k in August, crushing a 25k estimate. It followed a downwardly revised drop in July of -1.4k. The number of unemployed dropped slightly by around 3k, keeping the unemployment rate unchanged at 3.7% and close to the record low of 3.4% seen in October last year. The participation rate meanwhile rose to a record high of 67%. The head of the Australian Bureau of Statistics Jarvis said this continues to reflect a tight labour market. The strong labour market report loses some shine when noting the bulk of the employment increase came on the account of part-time jobs (62.1k). Hours worked also fell 0.5% in August. On a yearly basis, hours worked still grow faster (3.7%) than the annual increase in employment (3%) though. The Australian dollar whipsawed after the publication. AUD/USD is currently trading just shy of the intraday highs above 0.644. Swap yields temporarily rose before the fine print of the report kicked in. Current changes vary between 2.3-4.3 bps with the belly outperforming. Today’s numbers do little to alter the expected outcome for the Reserve Bank of Australia’s October 3 meeting (or any other meeting later this year). The RBA held rates steady for a third time straight this month at 4.1% and is seen to keep them at that level at least through 2024H1.

The IMF said that global debt as a percentage of GDP fell sharply in 2022 for a second year straight, from 248% to 238% in 2021. This compares to the 258% seen in 2020 after governments worldwide rolled out massive stimulus programs to cushion the impact of Covid. The decline in 2022 (and 2021) followed strong, post-pandemic growth as well as sharper-than-expected inflation. That said, the 2022 ratio is still above the pre-pandemic level of 238% in 2019. In addition, the IMF foresees global debt resuming its rise again going forward as inflation should stabilize at a low level over the medium term while the rebound of real GDP growth is fading.