Sample Category Title

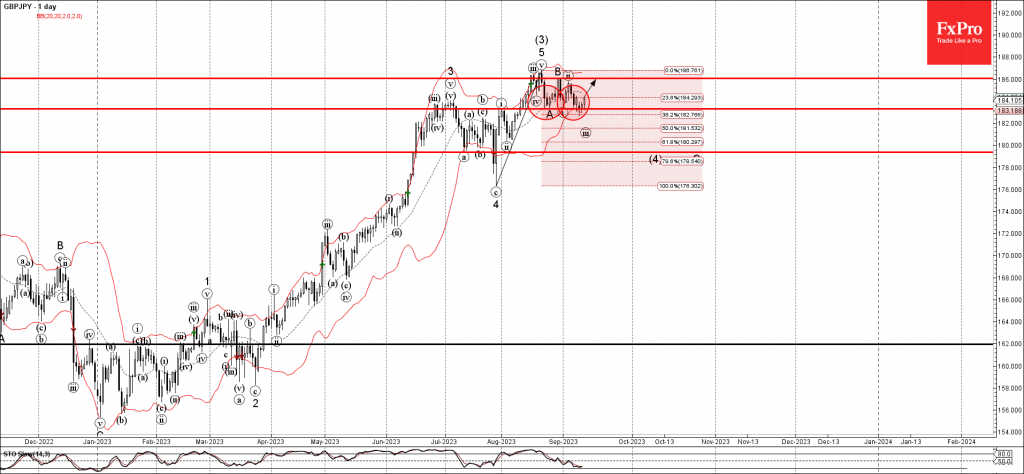

GBPJPY Wave Analysis

- GBPJPY reversed up from support level 183.30

- Likely to rise to resistance level 186.00

GBPJPY recently reversed up from the support level 183.30 (former top of wave i from the end of July) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 183.30 stopped the previous impulse wave ii of wave C from last month.

Given the overriding daily uptrend, GBPJPY currency pair can be expected to rise further toward the next resistance level 186.00 (top of the pervious waves 5 and B).

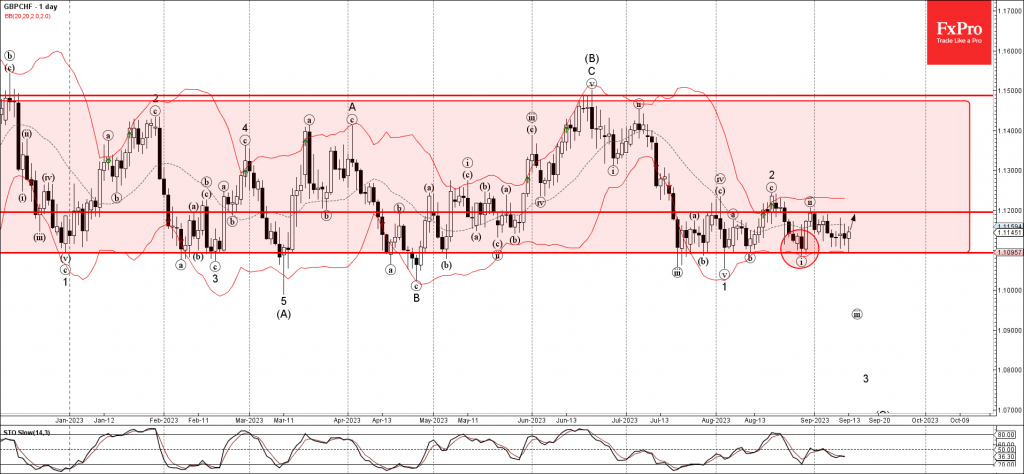

GBPCHF Wave Analysis

- GBPCHF currency pair reversed from support level 1.1095

- Likely to rise to resistance level 1.1200

GBPCHF currency pair recently reversed up from the key support level 1.1095 (lower boundary of the sideways price range inside which the pair has been trading from last December, as can be seen below).

The support level 1.1095 was strengthened by the lower daily Bollinger Band.

GBPCHF currency pair can be expected to rise further toward the next resistance level 1.1200 (top of the pervious minor correction ii).

Dollar Wavers after US Inflation Report

- September still a hold, while swap contracts suggest odds a 49.3% chance of a hike at the November 1st FOMC meeting

- Supercore inflation rate rises most since March

- Two-year Treasury drifts lower by 2.1 bps to 4.999%

Inflation is not easing enough for the Fed to abandon their hawkish stance. The upside surprises might be small, but that should keep the hawks in control. Core inflation heated up for the first time in six months and that should have markets leaning towards one more Fed rate hike in November. Inflation will likely still be running well above the Fed’s 2% target for the rest of the year, but a weaker consumer supports the case the disinflation process will remain intact.

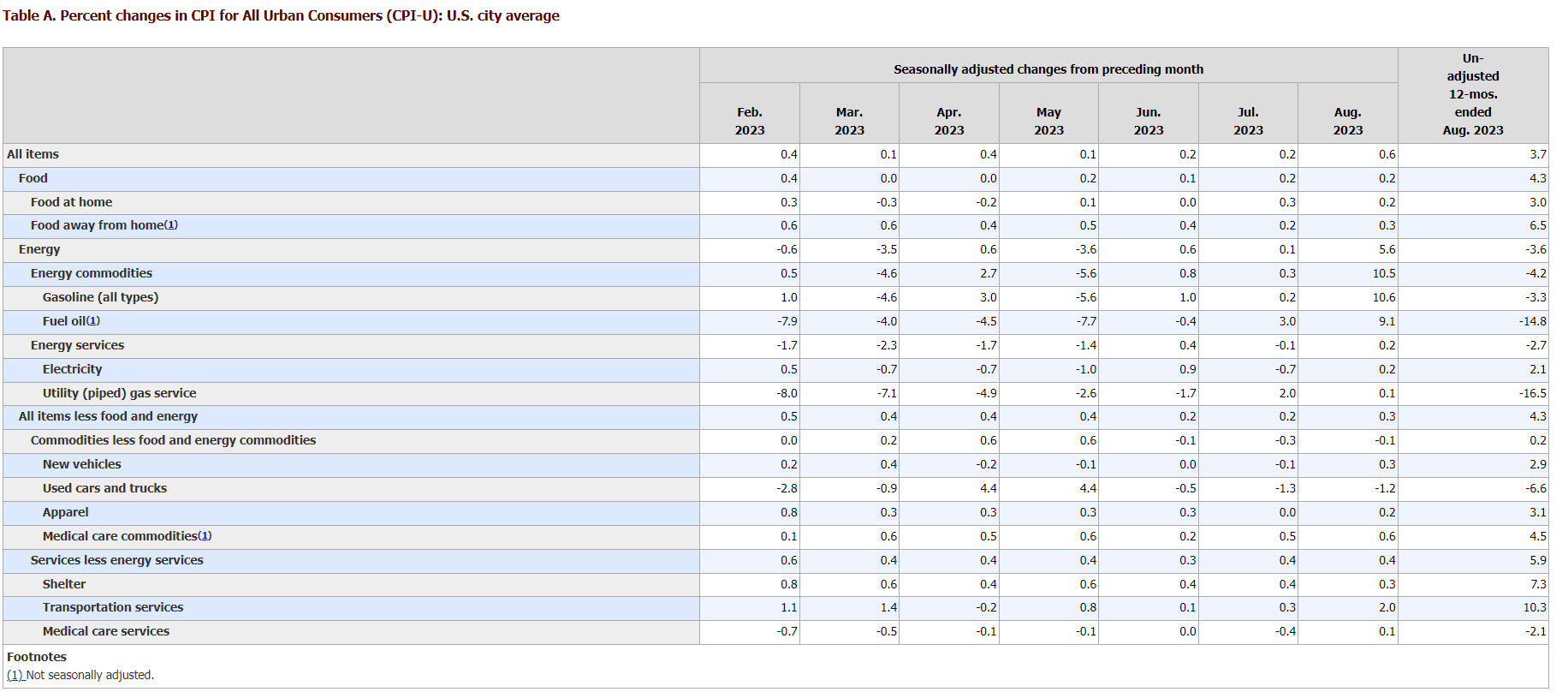

US CPI

Source: BLS

This was a complicated inflation report. Everyone knew that gas prices were sharply higher and that the housing market is still seeing elevated prices(house prices are now rising, while rents have eased). The headline inflation read showed CPI increased 0.6% in August from a month ago, which was the highest reading since June 2022. The annual inflation reading rose from 3.2% to 3.7%, a tick above expectations.

Market reaction

A weakening US consumer will continue as they battle surging gasoline prices, stubborn shelter prices, and increasing medical costs. US stocks are wavering as this inflation report will keep the Fed pushing the ‘higher for longer’ narrative. If Wall Street remains convinced that the labor market is cooling, that will do the trick for getting inflation closer to the Fed’s target.

The US dollar and Treasury yields were initially higher given the core CPI delivered an upside surprise, but once traders digested the entire report, the bond market reversed course. Core inflation rose 0.3%, which was due to the rounding of 0.278% which somehow makes it a lot less hot. Rent makes up 40% of Core PCE and prices posted the smallest gain since the end of 2021. Expectations are elevated for the consumer to be significantly weaker and that we could have a soft holiday spending season, which should support the disinflation process.

Dollar 5-minute Chart

The dollar is wavering as Wall Street wasn’t able to come up with any definitive stances on when the Fed will signal the all clear that policy is restrictive enough. The dollar’s strength is most notably against the Japanese yen, while the euro will likely react to Thursday’s ECB rate decision. Following yesterday’s Reuters report that the ECB will have inflation projections above 3%, markets appear to be leaning towards a rate hike.

Sunset Market Commentary

Markets

German Bunds underperformed from the start of trading on the back of a Reuters article which suggested that the ECB will tomorrow upwardly revise its 2024 CPI forecast from 3% currently. This bolsters the case for a rate hike even as GDP forecasts for 2023 (0.9%) and 2024 (1.5%) will face downward corrections. The market implied probability of a hike, our preferred scenario, rose from around 1/3 at the end of last week to 2/3 currently. German yields add up to 3.8 bps at the moment with the front end of the curve underperforming with part of the early gains erased after today’s main event, August US CPI inflation.

Headline US inflation rose by 0.6% M/M as expected (highest since June 2022) with the Y/Y-figure rising from 3.2% to 3.7% (vs 3.6% expected). The increase came on account of a 10.6% M/M increase in gasoline prices. We warned before that energy prices and energy commodity prices risk complicating the global disinflationary process in coming months. Core CPI rose by 0.3% M/M (vs 0.2% expected) with the Y/Y-number down to 4.3% from 4.7%. Core service prices excluding rents, the Fed’s so-called supercore inflation, accelerated to 0.38% M/M with the decline in the annual figure virtually stabilizing just above 4% for a third month running. Details showed the biggest upward surprise coming from transportation services. Used cars and trucks prices on the other hand decreased for a third time in a row (-1.2% M/M) Overall the CPI numbers won’t alter the outcome of next week’s FOMC meeting (skip) though they keep the debate on a Q4 move open. Markets traded volatile after the release not really knowing whether to cheer the ongoing disinflation process in categories like rents or fear the energy/transportation components and stubborn supercore. In a first move, US Treasuries sold off with the dollar profiting. Those didn’t went far, immediately triggering counter action. At the time of writing, US Treasuries are slightly stronger and the dollar marginally weaker. Changes on the US yield curve vary between -2.3 bps (2-yr) and flat (30-yr). EUR/USD changes hands near 1.0750 compared with 1.0730 ahead of the release.

News & Views

The Polish government is growing concerned on the pace of the decline of the zloty after last week’s unexpectedly aggressive 75 bps rate cut (6% from 6.75%) from the National Bank of Poland. Pawel Borys, an aide to Prime Minister Morawiecki, indicated that the recent sell-off of the zloty had brought the currency beyond a level the government sees as optimal. The government apparently prefers the zloty to stay in a range between EUR/PLN 4.40/4.60 as this isn’t too strong for exports while at same time not too weak to generate unwarranted inflationary pressures. Borys added that the government has tools to strengthen the zloty and reprimanded the central bank to take into account the potential consequences for the zloty when taking decisions on monetary policy. The comments are considered as opening the door to potential zloty interventions in case of a further disorderly decline of the Polish currency. In a different interview, MPC member Litwiniuk advocated the appropriateness of verbal interventions to clarify that the NBP sees the need for an appreciation of the zloty from current levels, illustrating differences of view within the MPC on last week’s NBP action. The zloty rebounded after the comments to currently trade near EUR/PLN 4.62 from 4.70 yesterday.

The Czech national bank recorded a current account deficit of CZK 30.4 bln in Q2 2023. The goods and services balance logged a surplus of CZK 105.2bn. The balance improved by CZK 112.1bn compared to the same quarter last year due to a decline in goods imports of almost 10% amid a slight increase in goods exports. The goods balance ended in a surplus of CZK 80.6bn, up by CZK 118.6bn. The surplus in the services balance at CZK 24.6bn was CZK 6.6bn lower Y/Y due mainly to a rise in imports of insurance and telecommunication services, as well as a deficit on foreign travel. The primary income deficit was CZK 131.1bn in Q2. Its YoY widening of CZK 58.7bn was due mainly to a rise in dividends paid to foreign owners. Secondary income ended Q2 in a deficit of CZK 4.5bn, down by CZK 1.5bn from a year earlier. The decline in the deficit was due to a decrease in social benefits paid to non-residents.

US: Despite Upside Surprise, Core Inflation Continues to Trend Favorably

The Consumer Price Index (CPI) rose 0.6% month-on-month (m/m) in August, in line with the consensus forecast. On a 12-month basis, CPI inched 0.4 percentage points (pp) higher to 3.7% .

- Energy prices (+5.6% m/m) were a big factor driving last month's acceleration, with prices rising at its fastest pace since June 2022. Meanwhile, food prices (0.2% m/m) matched last month's gain, as some deceleration in food at home (+0.2% from 0.3%) were offset my stronger gains in prices for food away from home (+0.3% from 0.2%).

Excluding the direct effects of food & energy, core inflation rose a 0.3% m/m – accelerating from June and July's monthly gains of 0.2% m/m and coming in a tenth of point above the consensus forecast. The 12-month change on core continued to edge lower, falling 0.3pp to 4.4%, while the three-month annualized change slipped to 2.4%.

Price growth across services rose 0.4% m/m, matching last month's gain, and remain at an elevated 5.9% year-over-year.

- Shelter costs remained a key source of inflationary pressure, with rent of primary residence (+0.5% m/m from 0.4% m/m) accelerating last month, while owners' equivalent rent (+0.4% m/m) matched July's gain.

- Price growth across non-housing services accelerated to 0.4% m/m in August – the strongest monthly gain in five months. Its twelve-month change remains at an elevated 4%.

Core goods prices declined by a very modest 0.1% m/m, with most of the pullback attributed to another sizeable decline in used vehicle prices (-1.2% m/m).

Key Implications

After two months of softer prints, core inflation surprised to the upside in August, highlighting what we have been saying for some time that progress is unlikely to come in a linear fashion. That said, even after accounting for the stronger monthly gain, the three-month annualized change on core still slipped to 2.4% – the slowest pace of growth since March 2021.

With core inflation continuing to move in the right direction, the labor market slowly coming back into better balance, and term yields having recently surpassed last year's highs, the FOMC can afford to skip the September meeting and continue to 'monitor the data'. However, it's still too soon to know whether the recent easing in inflationary pressures will be fleeting or more long lasting. This should keep the Fed guarded at its upcoming meeting, reinforcing the need for rates to remain 'higher for longer' and keeping the possibility of another rate hike in play, should progress on either the inflation or labor market stall in the months ahead.

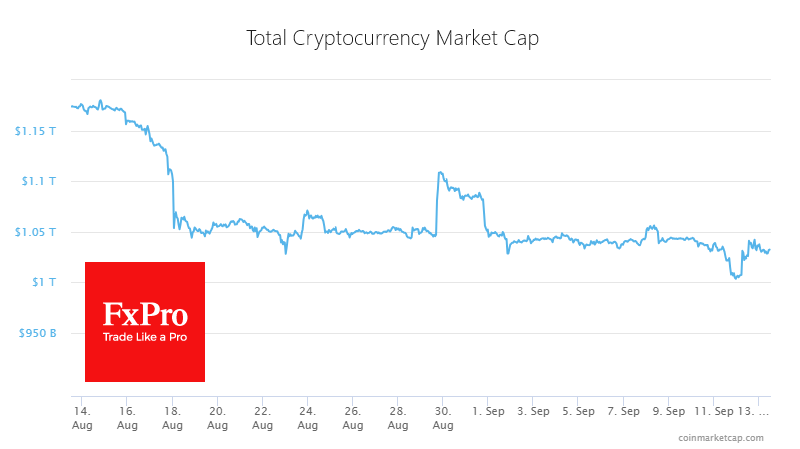

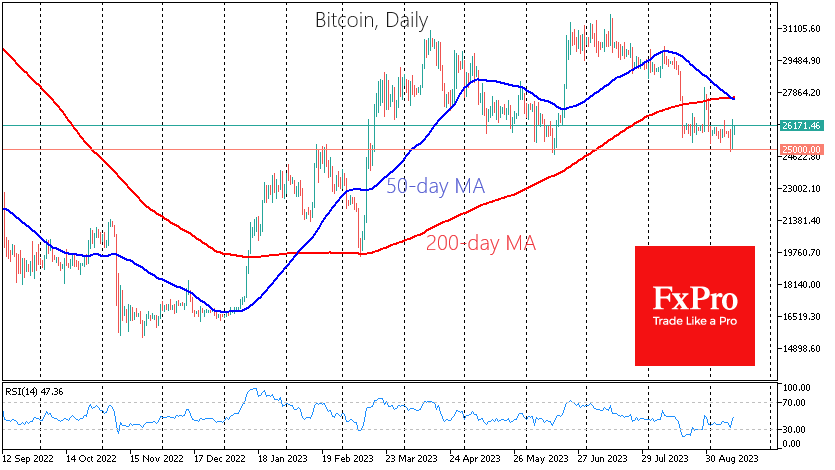

Crypto’s Landslide; Bitcoin’s Trying to Form a Trough

Market picture

We saw another attempt to shake up the crypto market on Monday and Tuesday. Still, the balance sheet quickly recovered with a total capitalisation of $1.033 trillion, just as before Monday’s $1 trillion failure. On a broader basis, the market is still sliding down bit by bit, as the equilibrium level was closer to 1.05 from the 18th to the 30th of August, dropping to 1.04 in early September, and is now hovering just above 1.033.

The technical picture of Bitcoin is beautiful in its ambiguity. BTCUSD failed spectacularly and bounced from 25k at the beginning of the week, reinforcing the belief that this price is an inflexion point. It also rallied from there in June and accelerated higher in March. From August last year to February this year, it repeatedly played the role of resistance.

On the other hand, a death cross has formed on the daily timeframe, which means that more traders focused on long-term technical analysis will be looking to sell on the upside.

On Wednesday and Thursday, Bitcoin may have no problem rising from the current $26.0K to $26.4K. The question is whether this will cause the sell-off to intensify.

News background

Volatility, liquidity, trading volume and the amount of bitcoin value transferred on the chain are at historic lows, according to Glassnode. This reinforces the likelihood that the market has entered a period of extreme apathy and exhaustion, suggesting significant price fluctuations soon.

Matrixport enabled the collapse of altcoins by selling FTX. Experts pointed to the court decision that allowed the bankrupt exchange’s creditors to sell $3.4 billion worth of cryptocurrencies as early as this week.

The Lightning Network (LN) could solve the resource-intensive process of sending money between countries and bring global payments out of the “fax era”, said Lightspark CEO and former head of Meta’s blockchain division David Marcus.

Payments giant PayPal has launched a service to convert cryptocurrencies into US dollars directly through wallets. The company previously integrated the ability to buy cryptocurrency with fiat.

GBP/USD Analysis: Price Sets a Minimum of 3 Months After GDP News

Disappointing UK economic data was released this morning. According to the Office for National Statistics, real gross domestic product fell by 0.5% in July 2023, with declines occurring across a range of sectors. The last time a decline of this magnitude occurred was in February of this year.

As a result of the publication, the GBP/USD rate dropped sharply. At the same time, it fell below the previous low set on September 7. Bears are putting pressure on the level of 1.245. Let us note that the last time one pound was given was 1.2443 dollars in June of this year.

Bearish arguments:

→ The UK has the highest inflation among Western countries. And the Bank of England is forced to keep rates high in order to lower them, thereby creating the preconditions for a further decline in GDP.

→ In case of a successful bearish breakdown of the level of 1.245, which provided support in September, this level may become resistance. As was the case with the level of 1.255.

→ The GBP/USD rate has been in a downward trend since mid-July, as shown by the red channel. And the median line may put pressure on the pound exchange rate in the near future.

Bullish arguments:

→ After the first reaction, the rate was restored. It is important. A bearish breakout pattern at the 1.245 level may form on the chart.

→ There is a chance that the RSI indicator will form a bullish divergence, indicating that the downtrend is exhausting.

→ The price of the pound may be supported by the lower border of the current downward channel.

Be sure to pay attention: today at 15:30 GMT+3 US inflation data will be published, which will certainly cause a surge in volatility in financial markets, including the GBP/USD pair.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Dollar Indecisive after CPI, Sterling Down But Not Out after Poor GDP

Dollar attempts to rally in early US session after modestly stronger than expected US consumer inflation data. But there is no clear follow through buying. Headline CPI's bounce back to a 14-month high was slightly above expectations. Meanwhile, core CPI's monthly reading also beat market forecasts. Yet, it appears that traders are not convinced that this set of data is strong enough to sway Fed much away from the policy path ahead. Whether there is another hike by the end of the year, after next week's expected pause, would remain largely a coin toss.

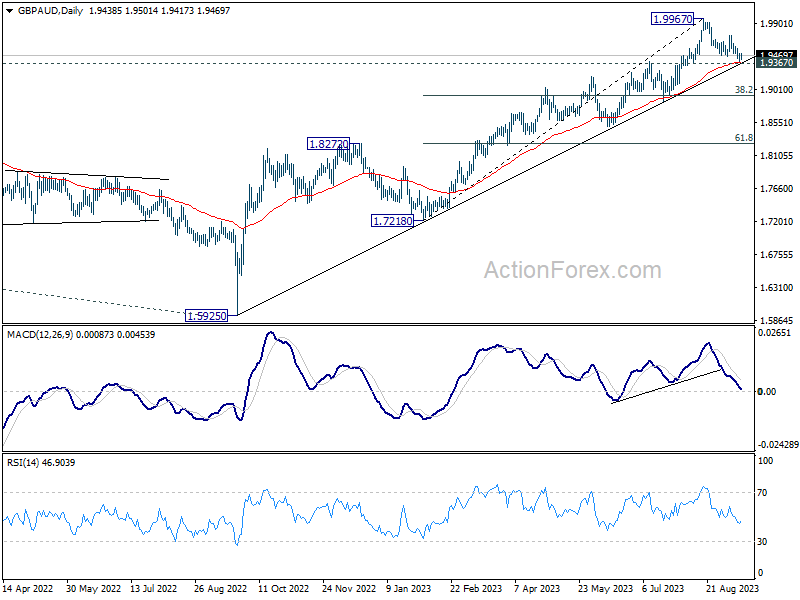

Sterling was under some selling pressure after deeper than expected UK GDP contraction but there was also no clear follow through momentum. Indeed for now, Aussie is the worst performer for the day, followed by Yen, and then Swiss Franc. Kiwi is the best performer, followed by Dollar and then Euro and Canadian. The Pound is just mixed in the middle.

Aussie will be a focus in the upcoming Asian session with Australian employment data featured. GBP/AUD is now pressing 1.9367 resistance turned support, 55 D EMA (now at 1.9377), as well as a medium term rising trend line. Strong bounce from current level will argue that pull back from 1.9967 has completed, and larger up trend from 1.5929 is ready to resume. On the downside, sustained break of 1.93 handle will indicate that it's at least in correction to the rise from 1.7218, and target 38.2% retracement of 1.7218 to 1.9967 at 1.8917. Let's see how it goes.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.55%. CAC is down -0.50%. Germany 10-year yield is up 0.0199 at 2.666. Earlier in Asia, Nikkei dropped -0.21%. Hong Kong HSI dropped -0.09%. China Shanghai SSE dropped -0.45%. Singapore Strait Times rose 0.14%. Japan 10-year JGB yield dropped -0.0001 to 0.710.

US CPI at 0.6% mom, 3.7% yoy; CPI core at 0.3% mom, 4.3% yoy

US CPI rose 0.6% mom in August, matched expectations. CPI core (ex food and energy) rose 0.3% mom, above expectation of 0.2% mom. Energy index was up 5.6% mom. Food index was up 0.2% mom. Gasoline was the largest contributor to monthly CPI rise, accounting for over half of the increase. Another contributor was shelter index, which rose for the 40th consecutive month.

For the 12 months period, headline CPI rose from 3.2% yoy to 3.6% yoy above expectation of 3.6% yoy. CPI core slowed from 4.7% yoy to 4.3% yoy, matched expectations. Energy index decreased -3.6% yoy. Food index rose 4.3% yoy.

Eurozone industrial production down -1.1% mom in Jul

Eurozone industrial production fell -1.1% mom in July, worse than expectation of -0.7% mom. Production of capital goods fell by -2.7% mom and durable consumer goods by -2.2% mom, while production of intermediate goods grew by 0.2% mom, non-durable consumer goods by 0.4% mom and energy by 1.6% mom.

EU industrial production was down -1.1% mom. Among Member States for which data are available, the largest monthly decreases were registered in Denmark (-9.1%), Ireland (-6.6%) and Lithuania (-4.4%). The highest increases were observed in Sweden (+5.1%), Malta (+3.4%) and Hungary (+2.9%).

UK GDP down -0.5% mom in Jul, dragged by services contraction

UK GDP contracted -0.5% mom in July, much worse than expectation of -0.2% mom. Services was down -0.5% mom, the main contributor to the fall in GDP. Production fell by -0.7% mom. Construction fell by -0.5% mom.

In the three months to July compared with the prior three-month period, GDP increased by 0.2%. Production rose 0.6%, and was the main contributing sector. Services and construction both rose by 0.1%.

Also released, industrial production came in at -0.7% mom, 0.4% yoy in July, versus expectation of -0.5% mom, 0.5% yoy. Manufacturing was at -0.8% mom, 3.0% yoy, versus expectation of -0.9% mom, 2.7% yoy. Goods trade deficit narrowed to GBP -14.1B, versus expectation of GBP -15.9B.

Japan's CGPI records eighth consecutive month of slowdown in August

Japan's annual wholesale inflation, as measured by Corporate Goods Price Index, registered a slowdown for the eighth consecutive month in August. CGPI eased to 3.2% yoy, aligning with market expectations and continuing its downward trend from the peak of 10.6% yoy recorded in December.

Export price index recorded a lesser contraction of -0.8% yoy compared to -2.6% yoy in July. Meanwhile, import price index also demonstrated a slight moderation in its decline, posting a -15.9% yoy compared to -16.0% yoy observed in the preceding month.

On a month-on-month basis, PPI saw an uptick of 0.3% mom. Delving into the specifics, export price index witnessed a recovery, improving by 0.5% mom. In contrast, the import price index reported a decline of 0.9% mom. within the same period.

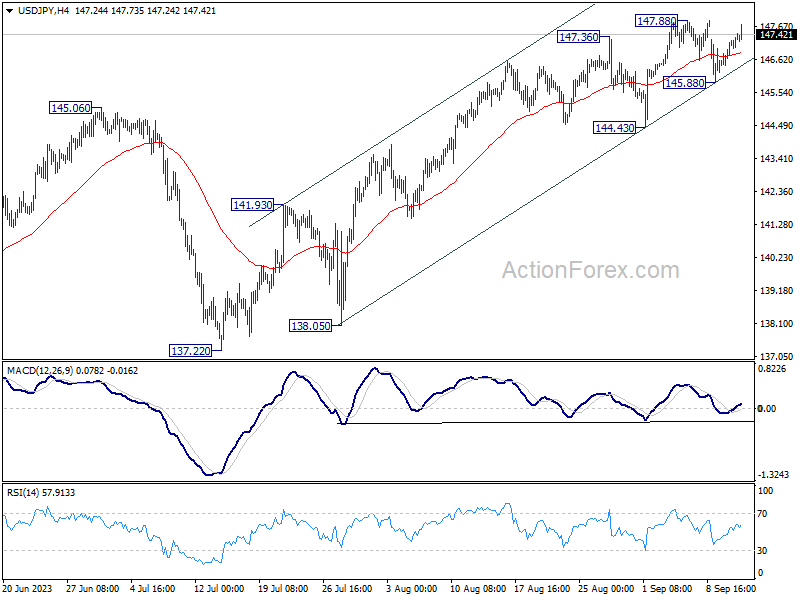

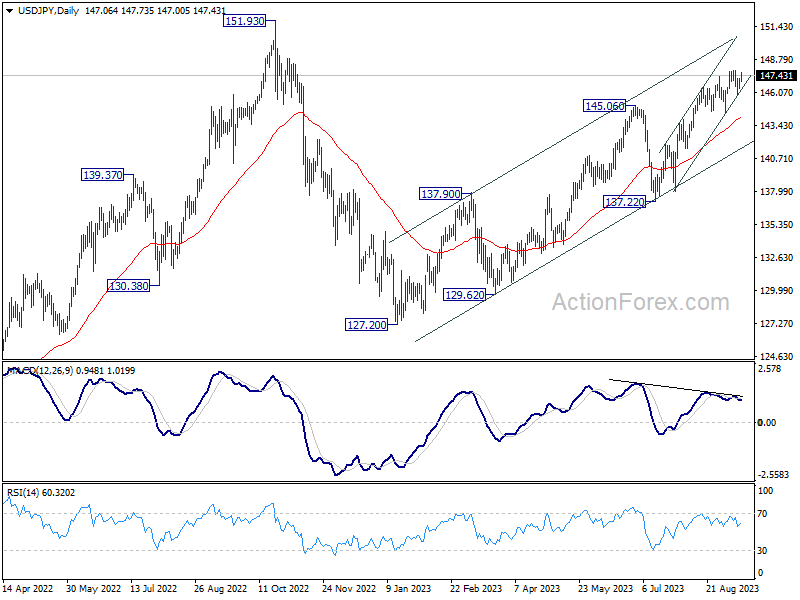

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.61; (P) 146.92; (R1) 147.40; More...

USD/JPY's rebound from 145.88 extends higher today, but upside is still capped by 147.88 resistance. Intraday bias remains neutral at this point and more consolidations could be seen. But even in case of another pull back, near term outlook will remain bullish as long as 144.43 support holds. On the upside, firm break of 147.88 will resume larger rise from 127.20, to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Aug | 3.20% | 3.20% | 3.60% | 3.40% |

| 23:50 | JPY | BSI Large Manufacturing Conditions Q3 | 5.4 | 0.2 | -0.4 | |

| 06:00 | GBP | GDP M/M Jul | -0.50% | -0.20% | 0.50% | |

| 06:00 | GBP | Industrial Production M/M Jul | -0.70% | -0.50% | 1.80% | |

| 06:00 | GBP | Industrial Production Y/Y Jul | 0.40% | 0.50% | 0.70% | |

| 06:00 | GBP | Manufacturing Production M/M Jul | -0.80% | -0.90% | 2.40% | |

| 06:00 | GBP | Manufacturing Production Y/Y Jul | 3.00% | 2.70% | 3.10% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | -14.1B | -15.9B | -15.5B | |

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | -1.10% | -0.70% | 0.50% | 0.40% |

| 11:00 | GBP | NIESR GDP Estimate Aug | 0.20% | 0.30% | ||

| 12:30 | USD | CPI M/M Aug | 0.60% | 0.60% | 0.20% | |

| 12:30 | USD | CPI Y/Y Aug | 3.70% | 3.60% | 3.20% | |

| 12:30 | USD | CPI Core M/M Aug | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Aug | 4.30% | 4.30% | 4.70% | |

| 14:30 | USD | Crude Oil Inventories | -2.2M | -6.3M |

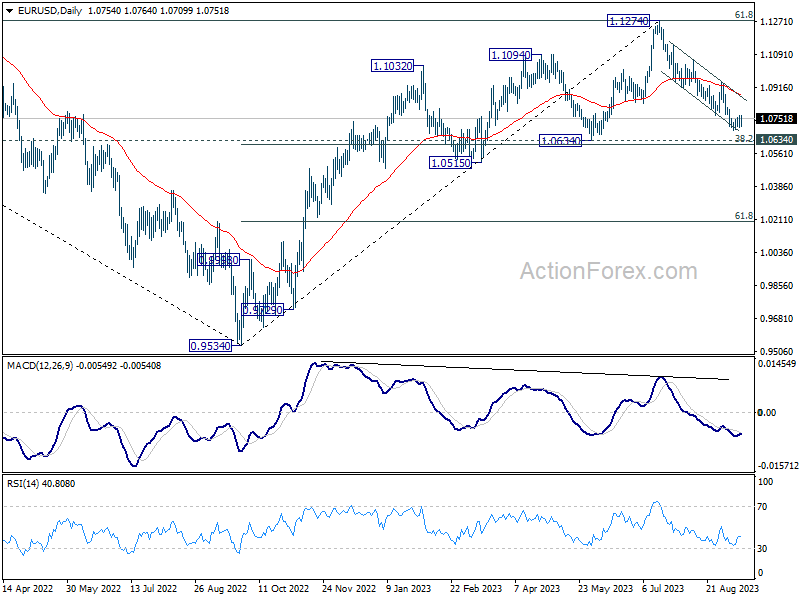

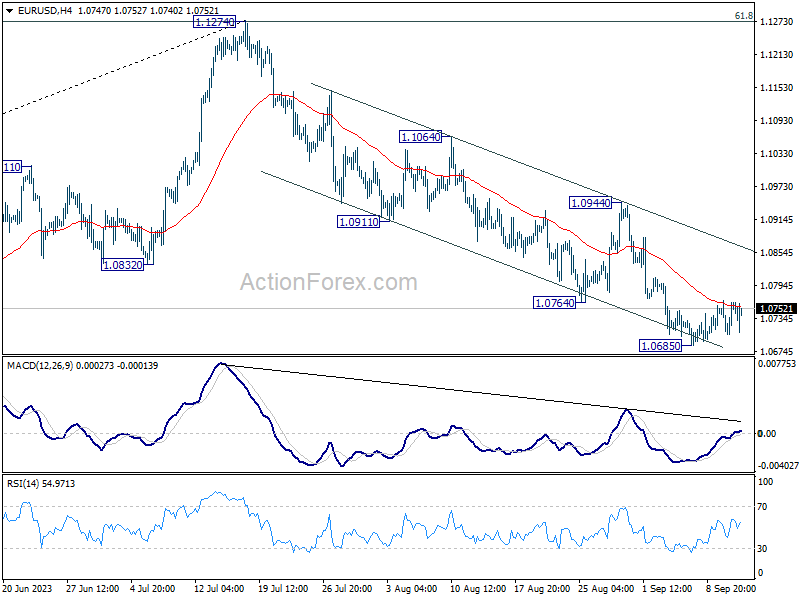

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0718; (P) 1.0743; (R1) 1.0781; More...

Intraday bias in EUR/USD stays neutral at this point, and consolidation from 1.0685 could extend. While stronger recovery might be seen, outlook will stay bearish as long as 1.0944 resistance holds. On the downside, below 1.0685 will resume the fall from 1.1274 to 1.0609/34 cluster support zone next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.