Sample Category Title

Silver Price Falls Back Below $70

As can be observed on the XAG/USD chart, the price of silver has once again dropped below the psychological $70 level. At the same time, this week has been marked by sharp fluctuations: on Monday, prices traded below $65, while as recently as yesterday, silver reached $74 per ounce.

Market volatility is being driven by ongoing geopolitical uncertainty. Conflicting statements from the United States and Iran regarding potential peace negotiations continue to unsettle financial markets. According to media reports:

- → Washington maintains that negotiations are ongoing, with the Trump administration reportedly delivering a 15-point proposal to Iran via intermediaries, aimed at resolving the conflict and reopening the Strait of Hormuz.

- → Iran, in turn, has stated that it does not intend to negotiate with the US, rejecting the proposed ceasefire and instead putting forward its own conditions.

On the morning of 19 March, analysing the XAG/USD chart, we:

- → concluded that the market was under significant pressure;

- → identified and plotted a descending channel (marked in red) on the silver price chart;

- → suggested that the channel’s median line could act as near-term resistance, thereby validating the structure.

Indeed, subsequent price action confirmed this framework, as indicated by the arrows:

- → the lower boundary acted as support on the same day;

- → yesterday, price reversed lower from the median line (which shifted from support to resistance), reinforcing the prevailing bearish sentiment observed throughout March.

From a bullish perspective:

- → the break below the 6 February low around the $64 level highlights aggressive demand — so-called “smart money” may have absorbed liquidity in this zone, positioning for higher prices;

- → silver may be in the process of forming an inverse head and shoulders pattern.

However, as long as price continues to trade below the red median line of the active channel, it would be premature to speak of any meaningful bullish conviction.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

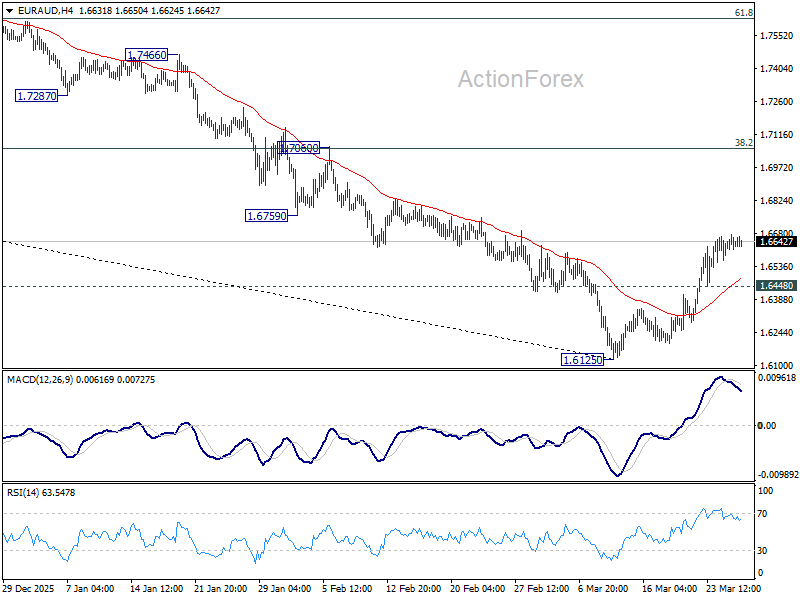

EUR/AUD Pair Rose by More Than 2% Over the Week

If last Thursday trading was taking place below the 1.6300 level, today one euro is worth more than 1.6660 Australian dollars. The upward trend seen in recent days has been driven by a combination of factors, including:

- → Bullish factor for the euro: The European Central Bank (ECB) has revised its 2026 inflation forecast upwards (to 2.6%). The reason lies in the Middle East conflict and rising energy prices. This signals to the market that the ECB may not only refrain from cutting rates but could also begin discussing potential rate hikes this year.

- → Bearish factor for the Australian dollar: The Middle East conflict is placing significant pressure on China’s economy (which is already dealing with a property market crisis). A slowdown in trade with China is weakening the Australian currency. For more details, see the article: What Are Commodity Currencies?

However, the chart indicates that the bullish momentum is fading — this is reflected in a series of bearish divergences, with the RSI moving down from overbought territory.

Continuing the technical analysis of the EUR/AUD chart, it can be observed that price fluctuations have formed a long-term descending channel. In this context:

- → Bulls have shown initiative: after touching the lower boundary of the channel, they (as marked by arrows) gradually took control over intermediate channel levels.

- → The current situation can be interpreted as a period of short-term consolidation (with the formation of a narrowing triangle pattern). The triangle may have been broken this morning, but Australia’s inflation report came in line with expectations — and the market continues to consolidate.

If we assume that bulls manage to gather enough strength for another upward push, they may face a significant test in the form of a resistance zone:

- → the March high around the 1.6730 level;

- → the upper boundary of the descending channel.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB’s ‘Option April’: Nagel Warns Against Shying Away from Pre-emptive Hikes

Bundesbank President Joachim Nagel signaled today that an April ECB rate hike is a live option, driven by rising inflationary risks following the conflict-induced energy spike in Iran. Nagel emphasized that the Governing Council will have sufficient data by April to determine if action is required, warning that the ECB should not "shy away" from early tightening if wage growth and medium-term inflation expectations continue to climb.

Speaking with Reuters, the Bundesbank chief cited the sharp increase in energy costs stemming from the Middle East conflict. He argued that "every passing day contributes to an increase in inflationary risks". His rhetoric suggests a shift toward pre-emptive action to protect medium-term inflation expectations.

While describing April as one of several possible options, Nagel pointed to mounting market speculation that the ECB could move sooner rather than later. "It is certainly an option, but just one option... We shouldn’t shy away from it now just because we think it’s still too early."

Nagel’s primary concern is "secondary" inflation. While energy prices provided the initial shock, the Bundesbank is now hunting for signs of price hikes spreading into the broader services sector and wage negotiations. If wage growth suggests that higher inflation is taking root, the ECB may be forced to move in April to prevent a wage-price spiral that would be far harder to break later in the year.

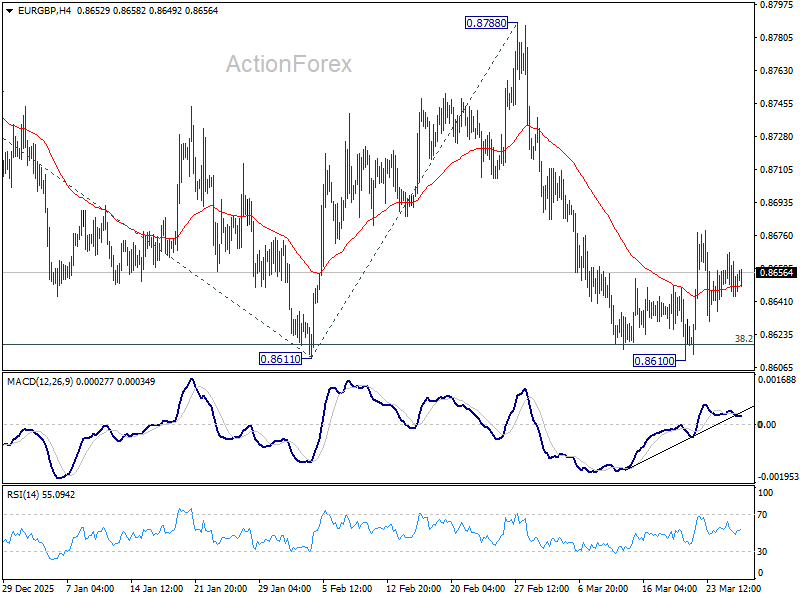

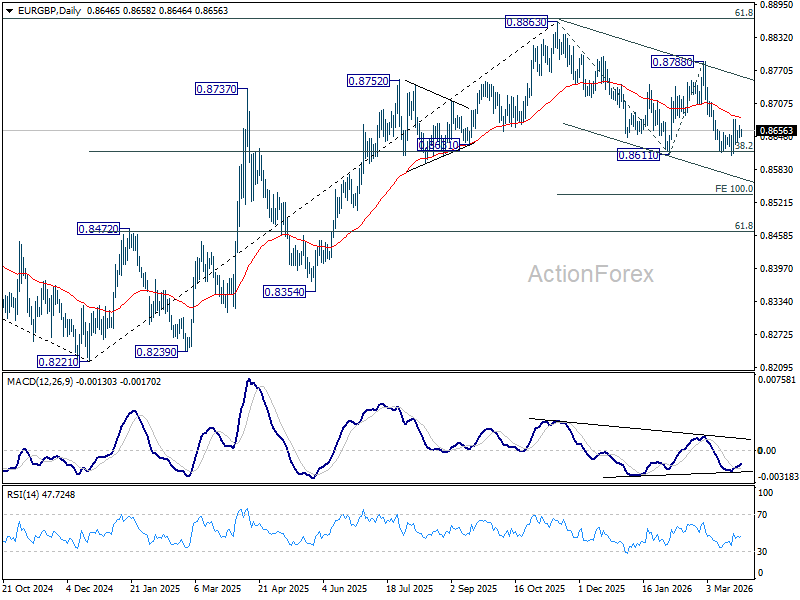

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8640; (P) 0.8655; (R1) 0.8664; More…

Intraday bias in EUR/GBP remains neutral at this point. With 55 D EMA (now at 0.8681) intact, further decline is in favor. On the downside, firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536. However, sustained break above 55 D EMA will turn bias back to the upside for 0.8788 resistance instead.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

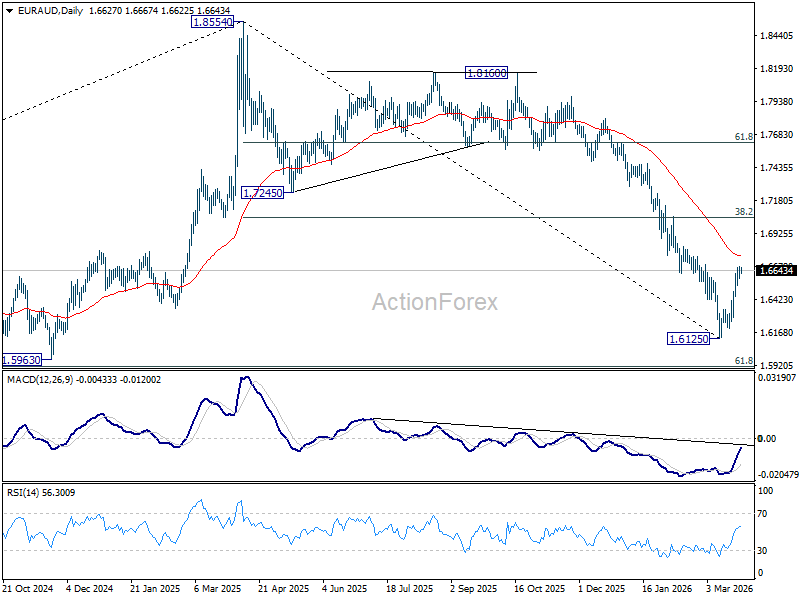

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6585; (P) 1.6632; (R1) 1.6683; More...

Intraday bias in EUR/AUD stays mildly on the upside despite loss of momentum. Rebound from 1.6125 short term bottom should extend to 55 D EMA (now at 1.6753). Sustained break there will pave the way to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. Nevertheless, below 1.6448 minor support will suggest that the recovery has completed, and bring retest of 1.6125 low.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7245) holds, even in case of strong rebound.

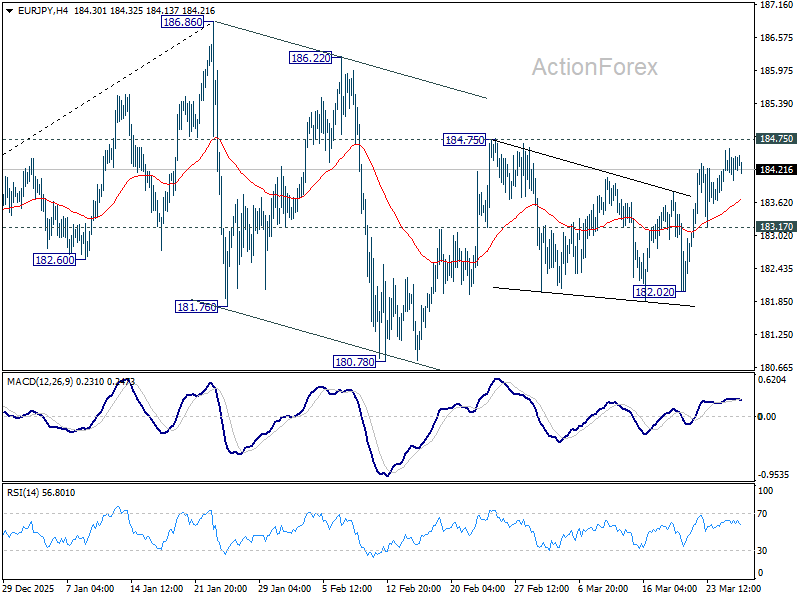

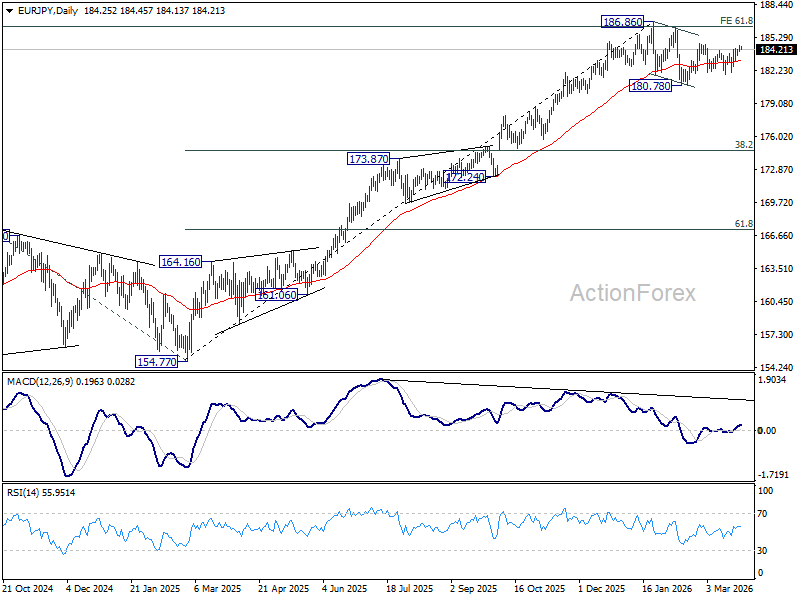

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.02; (P) 184.32; (R1) 184.61; More...

Intraday bias in EUR/JPY remains mildly on the upside. Firm break of 184.75 resistance will resume the whole rise from 180.78 and target a retest on 186.86 high. On the downside, below 183.17 minor support will turn intraday bias neutral first. Further break of 182.02 will bring deeper fall back to 180.78 support.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.61) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

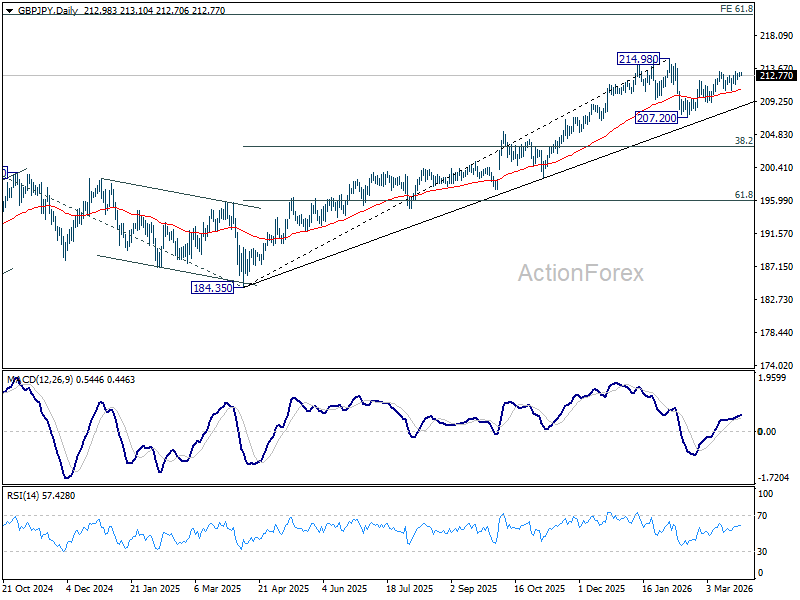

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.71; (P) 212.97; (R1) 213.37; More...

Intraday bias in GBP/JPY stays mildly on the upside for the moment. Firm break of 213.28 resistance will resume the rally from 207.20 and target a retest on 214.98 high. For now, risk will stay mildly on the upside as long as 210.77 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

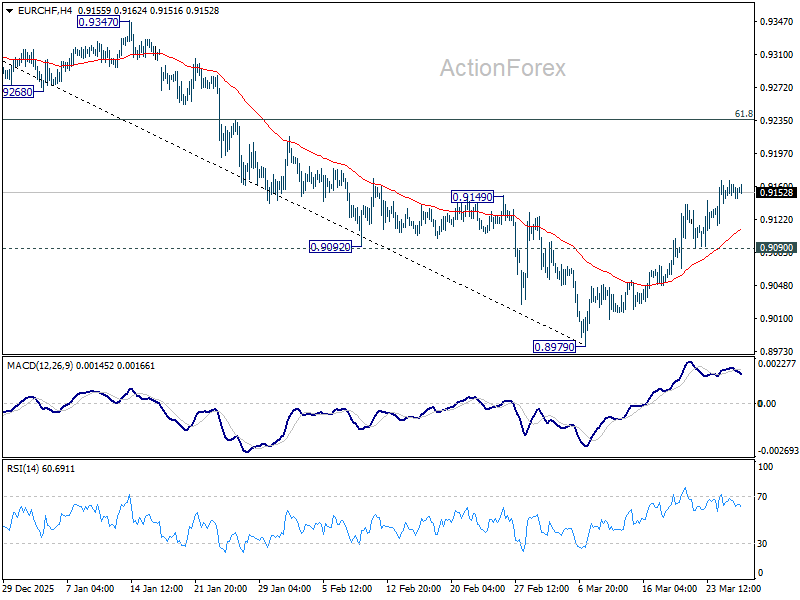

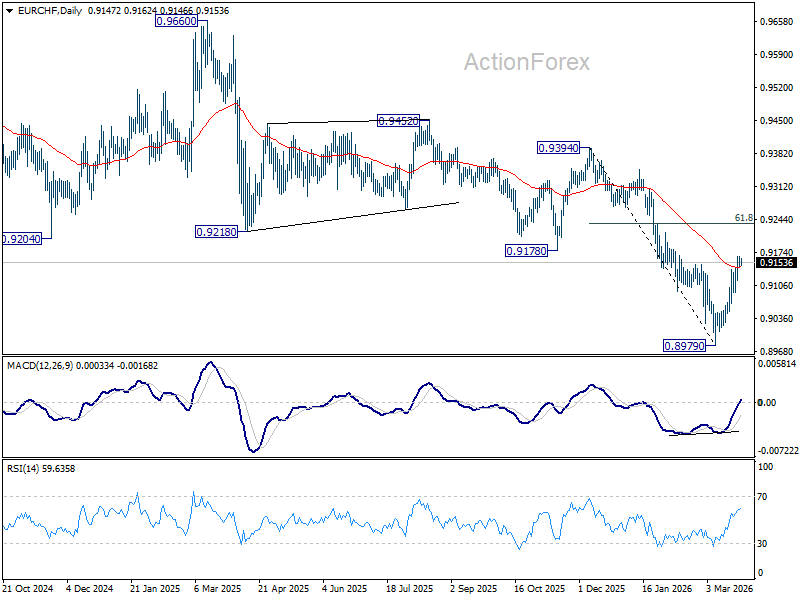

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9141; (P) 0.9155; (R1) 0.9165; More....

Intraday bias in EURCHF stays on the upside at this point. Rebound from 0.8979 short term bottom should target 61.8% retracement of 0.9394 to 0.8979 at 0.9235 next. On the downside, below 0.9090 minor support will turn intraday bias neutral again first.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

Consumer Confidence in the UK Collapsed

Markets

The ECB Watchers Conference distracted from the ongoing war in the Middle East yesterday. Key takeaways include that, while the 2026 macroeconomic backdrop is different from 2022, the ECB is on high alert for energy inflation to spill over and affect inflation expectations through wage price setting. The latter is likely to adjust much quicker because of the 2022 legacy. Any shock that is not short-lived and limited in size would require a monetary policy response, if only for the sake of communication and to underscore the central bank’s resolve to keep inflation at 2%. The market impact was limited and in any case distorted by reports of a 15-point US plan offered to Iran to end the war. A one-month ceasefire was included to allow for negotiations. After weeks of bombardments and aggressive rhetoric, the diplomatic outreach prompted some risk on in markets. Stocks rose, Brent oil lost the triple digit mark at some point and core bonds sighed of relief. European and UK bonds outperformed Treasuries. German rates eased between 6 and 7.1 bps in bull steepening. Gilt yields tanked 5.6 (2-yr) -13.3 (30-yr) bps. US net daily changes went from -0.4 to -3 bps. That slight yield advantage kept the USD favored over peers, be it in technical irrelevant trading. EUR/USD dropped below 1.16. DXY rose from the low 99s towards 99.6. USD/JPY is closing in on the loaded, FX-intervention prone 160 barrier.

Yesterday’s optimistic market view was striking given that it completely looked through Iranian rejection of the proposal. The Middle East country replied with five conditions that need fulfilment before agreeing to any end of the war. International recognition of Iran’s sovereignty over the Strait of Hormuz is a particular thorny one. Meanwhile the US is building up presence in the region, fanning speculation for boots on the ground and a possibly protracted war that spans far beyond the 4-6 week timeframe currently put forward by the US. The conflicting signals inject renewed doubt in the market today, dragging Asian bourses and Treasuries again lower. Brent oil rises 3% to $104/b. The dollar steadies around yesterday’s closing levels. A relatively empty eco calendar keeps the spotlights on the war. That means trading continues to be headline-based and inherently unpredictable. Several Bank of England policymakers hit the wires today. Two of them are among those having dropped their previous call for rate cuts earlier this month.

News & Views

A survey by the British Retail Consortium shows that consumer confidence in the UK collapsed as the Middle East conflict raised the prospect of higher inflation in the months ahead. As stock markets tumbled, both the index of confidence in the economy over the next three months (-56 from -30) as well as consumers’ expectations on their own personal finances (-17 from -6) dropped to their lowest levels on record. BRC analyses that the drop in confidence was most pronounced among the boomer generation who are most reliant on investment and pension funds. Spending expectations rose but BRC analyses, but this was due to the fact that consumers expect to see rising energy costs being reflected across the economy. Data supporting the survey were collected between March 10-13.

RBA assistant governor Kent offered an in depth view on Australian financial conditions and the meaning/reference of the neutral policy rate when setting monetary policy. On the current developments, Kent assessed that heightened geopolitical and economic uncertainty globally have led to some tightening in financial conditions which all else equal implies a decline in short-term neutral rates. However, the supply shock also poses a risk to inflation and longer term inflation expectations at a time when there are ongoing capacity pressures in Australia and several other advanced economies. This could both push short-run neutral rates higher and necessitate a more restrictive stance of policy. ‘A negative supply shock pushes up prices and leads to weaker economic activity, making us all poorer. Central banks cannot change that. But they can ensure that the initial rise in prices does not lead to a rise in longer term inflationary expectations and extended inflationary pressures’ Kent analyses. At the same time, he indicated that it is not the RBA’s intention to force the economy in a recession. It wants to shield the labour market as long as inflation is on a credible path down. The Austrian 3-y yield nevertheless rose 10 bps this morning (4.72%). Markets raised the prospect of a 25 bps next hike at the May meeting from about 65% to 82%. After a correction this week, AUD/USD holds near 0.695.

Too Early to Price Out the War

The US sent a 15-point plan to Iran to end the war, which Iran publicly refused. They proposed alternative conditions instead and continued attacks in the region.

Interestingly, equity investors bought into the US 15-point peace plan and hardly reacted to Iran’s rejection. The S&P 500 rose 0.54% yesterday. Despite trade and geopolitical uncertainties, analyst estimates for S&P500 earnings may have improved since the start of the war, according to Bloomberg Intelligence. Expectations for profit growth rose from 10.9% to 11.9% since the beginning of Middle East hostilities, narrowing the margin for disappointment and increasing the risk of a sharper correction.

The index met resistance at the 200-DMA, while US crude jumped 4%.

Oil is higher again this morning, with Brent crude preparing to regain the $100pb handle. Asian equities are down, while US and European futures point to a lower open. Investors are trying to price out the war and price in a peace rally ahead of time. But risks remain elevated and downside risks prevail.

Donald Trump insists that peace negotiations are ongoing, describing developments in the Middle East as “big”, but he is no longer controlling the narrative. One of Iran’s senior military figures mocked the US, saying: “Has the level of your inner struggle reached the stage of you negotiating with yourself?” This reflects where we stand in negotiations.

That said, Trump appears eager to end the war as political and geopolitical pressure builds into the midterm elections. Deutsche Bank has even created a “pressure index” incorporating factors such as the one-month change in Trump’s approval ratings, stock market performance, and inflation expectations derived from bond markets. That index is now at its highest level since his election.

And the economic pressure is spreading beyond oil prices. US mortgage rates, for example, have returned to their highest levels since October, weighing on new purchase applications. These rates are driven by the US 10-year yield and a risk premium—both of which have risen since the start of hostilities, alongside oil prices, inflation expectations and US debt concerns. The US 10-year yield has risen by as much as 50bp from its early-month lows, as investors shifted from pricing in summer rate cuts to considering the possibility of rate hikes later this year and more military spending in the coming years. Fed funds futures currently imply around a 30% chance of at least a 25bp hike by year-end. But note that this could change rapidly as stagflation risks also rise.

In FX, the US dollar appreciated yesterday and remains slightly bid in Asia. The EURUSD and Cable are both under pressure despite increasingly hawkish expectations for the European Central Bank (ECB) and the Bank of England (BoE). In Europe, ECB President Christine Lagarde said the bank “will not be paralysed by hesitation” in responding to the energy shock from the Middle East war. In the UK, hotter-than-expected inflation data—partly reflecting earlier declines in energy prices—suggest that the energy shock could materially shift the inflation trajectory and force a policy response.

In Westminster, Rachel Reeves indicated plans to accelerate power plant construction, aiming for projects to come online by the end of 2027... a bit ambitious!

Global X Uranium ETF rose 1.58% yesterday but has declined since the start of the war, despite European pledges to return to nuclear energy. The medium- to long-term outlook remains positive, and current levels could attract buyers back into the market.

Elsewhere, gold reversed the past two sessions’ gains in Asia this morning, falling more than 1.5% as optimism around a Middle East peace fades. Other metals, including silver and copper, are also under pressure from a stronger US dollar, higher yields and deteriorating global growth expectations, as the war risks extending beyond a month.

Commodities and TIPS remain effective hedges in an inflationary environment, but uncertainty is currently so high that cash is king—and in practice, that often means the US dollar.

Once the dust settles, however, the hawkish divergence between European and other major central banks relative to the Fed could cap further dollar appreciation. The US dollar and Treasuries have been losing their international appeal due to erratic trade policies, rising US debt and US’ deteriorating international relations, which are pushing central banks to diversify reserves away from US assets. That longer-term trend is likely to reassert itself. For now, however, the dollar benefits from a lack of credible alternatives. Today’s US 30-year bond auction will be worth watching.

In tech, news flow was mixed. Meta and Google were found liable for harming young users of their platforms and will face fines. However, their share prices were largely unchanged, as the penalties are marginal relative to revenues and investors remain focused on AI, growth opportunities rather than regulatory risks. The primary valuation risk remains delayed returns on heavy AI investment.

That said, AI demand remains strong. Arm Holdings jumped more than 16% after announcing plans to start building its own chips, with potential annual revenue of up to $15bn by 2031. The company has historically focused on chip design for third parties. That said, Arm remains expensive, trading at around 190 times earnings. While new revenue streams may compress that multiple, the stock is unlikely to become cheap anytime soon.