Sample Category Title

RBA Warns of ‘Restrictive’ Shift: Why Rising Neutral Rates and Petrol Shocks Could Trigger More Hikes

RBA Assistant Governor Christopher Kent warned today that the prolonged Middle East conflict is pushing Australia’s "neutral" interest rate higher, signaling a potentially more aggressive path for the cash rate. Despite global uncertainty usually cooling markets, Kent noted that persistent supply shocks in energy are forcing a "tighter stance of monetary policy" to prevent long-term inflation expectations from spiraling.

The Middle East "Wealth Tax"

In a sobering assessment of the ongoing regional conflict, Kent highlighted that the surge in oil and natural gas prices is effectively making Australians "all poorer." He noted that while the RBA cannot change the supply of oil, it must react to the "material repricing of assets" caused by the war.

"A negative supply shock pushes up prices and leads to weaker economic activity, making us all poorer. Central banks cannot change that. But they can ensure that the initial rise in prices does not lead to a rise in longer term inflationary expectations," he said.

The Neutral Rate Reassessment

The core of Kent's message was a warning to those expecting rate cuts. He explained that the conflict in the Middle East creates two countervailing forces, but the risk to inflation expectations is currently winning the tug-of-war.

"This could both push short-run neutral rates higher and necessitate a more restrictive stance of policy. Indeed, financial market participants have revised up their expectations of monetary policy rates in Australia," he said.

Ensuring "Stable Inflation"

Kent concluded by reaffirming the Board's commitment to its medium-term targets, even if the "supply shock" makes the path more difficult. He emphasized that the RBA will not allow temporary price spikes to become a permanent fixture of the Australian economy.

Fragile Optimism Stands in Equities, What’s Next? – Dow Jones and US Stock Market Outlook

- US Stock Benchmarks attempt a continued rebound in the current session, with the narrative seemingly easing in recent days

- After the previous session's stalling progress, Equities pursue their cautious rebound

- Exploring Technical Levels for the Dow Jones, Nasdaq and S&P 500

US Stock benchmarks are still attempting to price a cautious but seemingly better narrative around the Middle East conflict into another rebound in today's session.

This continues the theme that had shaken Markets in Monday's chaotic, but more positive weekly open: The War doesn't seem to be taking a turn for the worse, hinting at what could really be a four to five-week-long conflict.

It would be almost too good to be true to see Donald Trump make good on his words, having announced such a deadline to the ceaseless strikes on Islamic regime targets in Iran.

The current War isn't faring well with the American public, and right ahead of the Midterms coming up in November, the President surely doesn't want to aggravate his case.

But during wartime, each headline has to be taken with a pinch of salt, particularly with Iran reportedly rejecting Trump's 15-point plan to add their own demands – They are particularly keen on conserving their long-range ballistic missile capabilities, but the world knows how dangerous they have been, so expect this to be a zone of contention.

We should learn more on these developments by Friday.

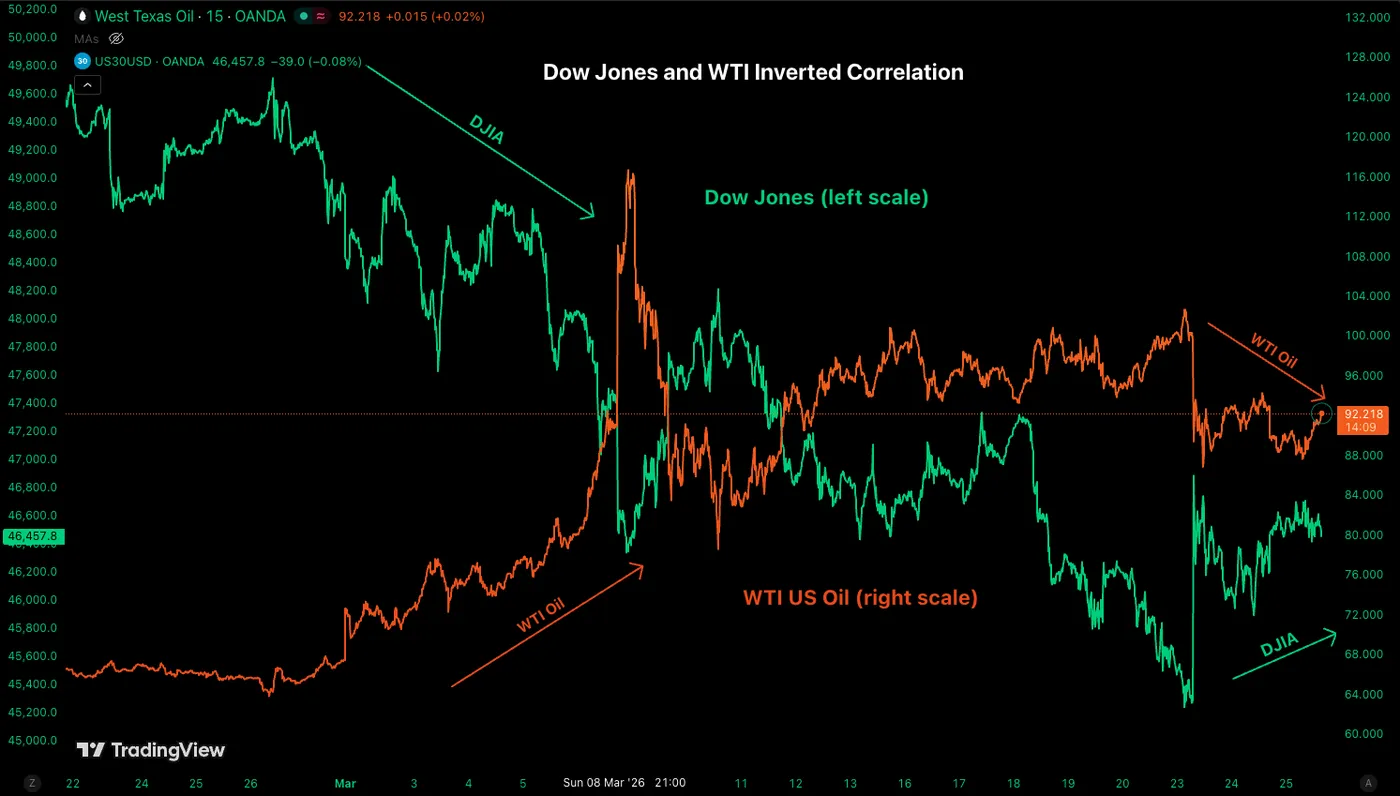

Dow Jones – WTI Inverted Correlation sustains – Source: TradingView

Despite all the uncertainty, traders should focus more on what is happening in front of them: The Oil-Stocks inverse correlation is the only clear Market development since the beginning of the month; Tracking the commodity will act as a guide to navigate this clouded environment (while headlines do the exact opposite).

WTI Oil had gapped lower in recent sessions and held a lower trajectory since, but has stalled its descent around the $88 Level, and this has weighed on Stock Markets since the mid-session.

(Don't forget to check out our recent WTI Analysis to have a better guess of where Support and resistance can occur, as long as no real solution is found.

In today's action, all Stock Indexes are moving together with no clear outperformer – See more just below.

Let's spot where today's cautiously optimistic price action is heading by looking at today’s intraday charts and trading levels for the major US indexes: the Dow Jones, Nasdaq, and S&P 500.

Current Session's Stock Heatmap

Current picture for the Stock Market (12:17 PM ET) – Source: TradingView – March 25, 2026

The rebound hasn't seen formed any consistent pattern since Monday, except for the previous session's Manufacturing outperformance – Process Industries and Pharmaceuticals are the only sectors flashing green in today's session.

The rest is broadly chaotic, so for individual Stock traders, the best is to look for local ranges to play.

Dow Jones 4H Chart and Trading Levels

Dow Jones (CFD) 4H Chart – March 25, 2026 – Source: TradingView

For the first time since February 26, the Dow Jones is trading above its 4H 50-period Moving Average, a striking progress particularly with the consistent downtrend that had developed since.

Combining with a weak, but persistent exit from the March bear channel, it seems that the DJIA is only a few positive headlines from a rebound – 48,000 would be a decent target in that event – Above 48,000, expect the rebound to hold towards 50,000.

The only issue is that optimism in such an environment could prove short-lasted, hence with bullish views in the Market, make sure that your size is under control to allow for more flexibility in case things turn sour again.

Any session close below 46,300 would continue the downtrend.

Dow Jones technical levels for trading:

Resistance Levels

- Resistance 47,000 +/- 100 Points (session highs and major resistance)

- Momentum Resistance 47,500 to 47,650

- Key Resistance at 48,000

- 48,400 to 48,500 mini-resistance

Support Levels

- 4H 50-period MA 46,437

- March 8 War lows Pivot 46,200 to 46,300.

- January 2025 Highs 45,000 to 45,280 (Monday lows)

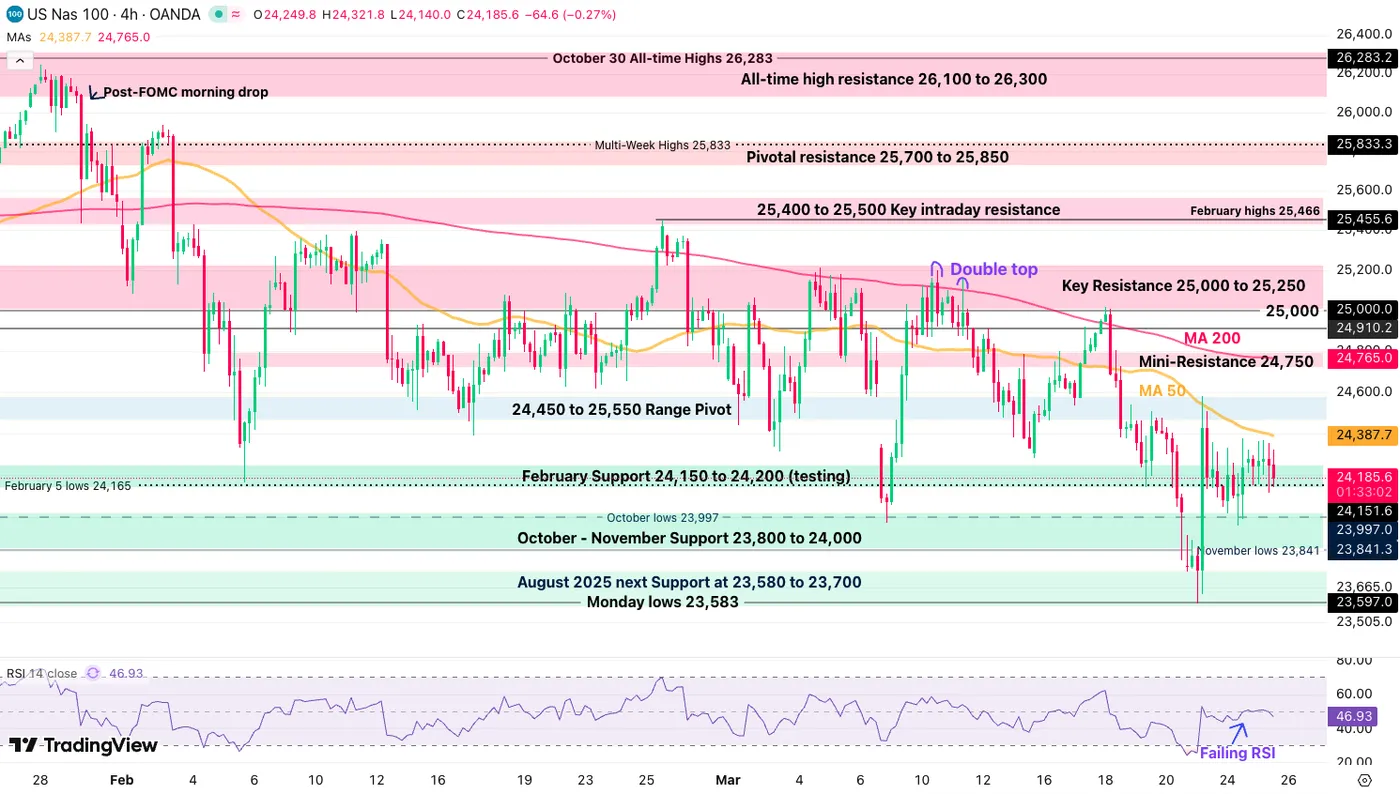

Nasdaq 4H Chart and Trading Levels

Nasdaq (CFD) 4H Chart – March 25, 2026 – Source: TradingView

Nasdaq is actually looking more pessimistic than its elder, failing to persistently hold above 24,200 with its RSI actually turning bearish.

Breaking 24,150 could see a quick test of the 23,800 support; Even in the event of the rebound, it looks like the tech Index has less inherent strength and could lag on a rally.

Nasdaq technical levels of interest:

Resistance Levels

- 24,387 4H 50-period

- 24,450 to 25,550 Range Pivot (short-term resistance)

- Mini-intraday Resistance 24,750

- Key Resistance 25,000 to 25,200 (Range highs – Long-term Bullish above)

Support Levels

- February Support 24,150

- October - November Support 23,800 to 24,000

- Morning lows: August 2025 next Support at 23,580 to 23,700

- Early 2025 ATH at 22,000 to 22,229 Support

S&P 500 4H Chart and Trading Levels

S&P 500 (CFD) 4H Chart – March 25, 2026 – Source: TradingView

The S&P 500 looks right in the middle between bullish and bearish; it remains the Index to trade if you prefer less brutal up-and-down swings.

As long as the price action remains above 6,580, the outlook isn't bearish, but not so bullish either:

Buyers will want a break above 6,650 to relaunch a bullish outlook.

S&P 500 technical levels of interest:

Resistance Levels

- Momentum Pivot 6,640 to 6,650

- 6,680 to 6,700 Mini-resistance

- 6,740 Key intraday resistance

- Pivotal Resistance 6,770 to 6,800

Support Levels

- 6,570 to 6,600 Monday Key Double Bottom support

- 6,490 to 6,512 October lows

- 6,442 Morning Lows

- 6,400 Major psychological support

Safe Trades and Keep track of WTI prices!

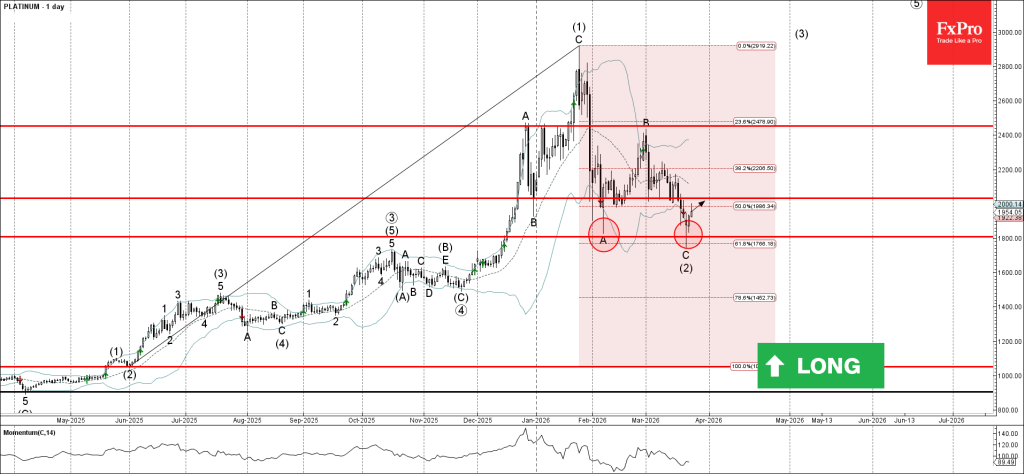

Platinum Wave Analysis

Platinum: ⬆️ Buy

- Platinum reversed from support zone

- Likely to rise to resistance level 2030.0

Platinum recently reversed up from the support zone between the round support level 1800.00 (low of wave A from February), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from May.

The upward reversal from this support zone created the daily hammer, which stopped the previous ABC correction (2) from the end of January.

Given the clear daily uptrend, Platinum can be expected to rise toward the next resistance level 2030.0 (former support from February and March).

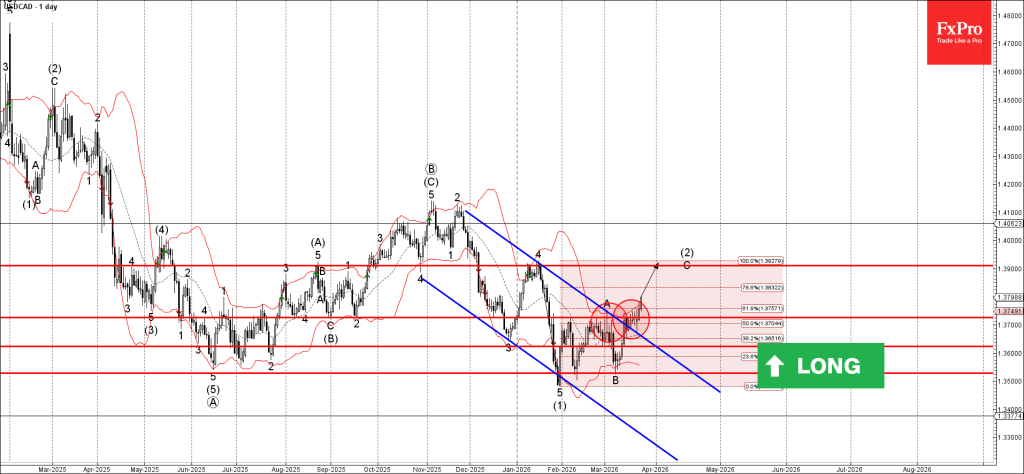

USDCAD Wave Analysis

USDCAD: ⬆️ Buy

- USDCAD broke resistance area

- Likely to rise to resistance level 1.3900

USDCAD currency pair recently broke the resistance area between the resistance level 1.3725 (top of the previous wave A from the end of February) and 50% Fibonacci correction of the downward impulse 5 from January.

The breakout of this resistance zone accelerated the C-wave of the active ABC correction (2).

USDCAD currency pair can be expected to rise toward the next resistance level 1.3900 (target price for the completion of the active C-wave).

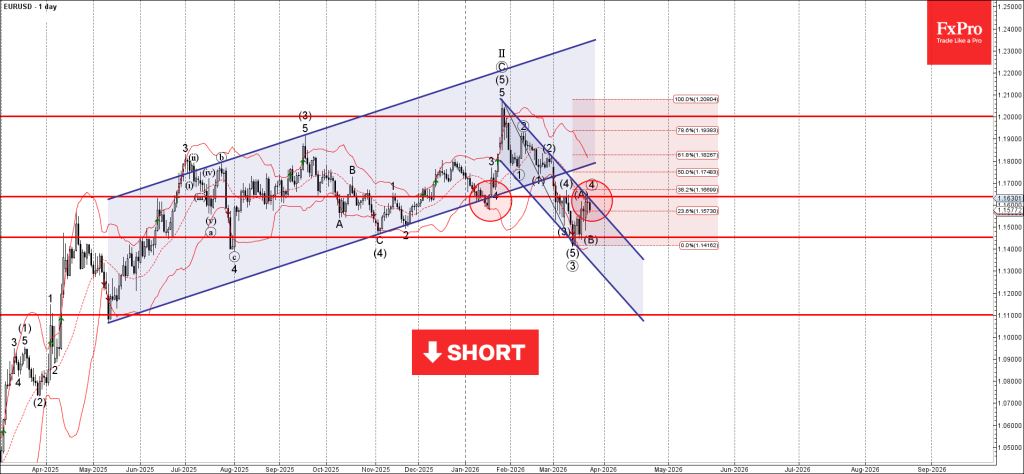

EURUSD Wave Analysis

EURUSD: ⬇️ Sell

- EURUSD reversed from resistance zone

- Likely to fall to support level 1.1450

EURUSD currency pair recently reversed from the resistance area between the resistance level 1.1635 (former support from January), resistance trendline of the daily down channel from January and 38.2% Fibonacci correction of the downward impulse from January.

The downward reversal from this resistance zone stopped the previous long-term ABC correction 4.

EURUSD currency pair can be expected to fall toward the next support level 1.1450 (which has been reversing the price from last year).

Eco Data 3/26/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Feb | 2.70% | 2.60% | 2.60% | |

| 07:00 | EUR | Germany GfK Consumer Confidence Apr | -28 | -28.6 | -24.7 | -24.8 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 3.00% | 3.20% | 3.30% | 3.20% |

| 12:30 | USD | Initial Jobless Claims (Mar 20) | 210K | 211K | 205K | |

| 14:30 | USD | Natural Gas Storage (Mar 20) | -54B | -49B | 35B |

| 23:50 | JPY |

| Corporate Service Price Index Y/Y Feb | |

| Actual | 2.70% |

| Consensus | 2.60% |

| Previous | 2.60% |

| 07:00 | EUR |

| Germany GfK Consumer Confidence Apr | |

| Actual | -28 |

| Consensus | -28.6 |

| Previous | -24.7 |

| Revised | -24.8 |

| 09:00 | EUR |

| Eurozone M3 Money Supply Y/Y Feb | |

| Actual | 3.00% |

| Consensus | 3.20% |

| Previous | 3.30% |

| Revised | 3.20% |

| 12:30 | USD |

| Initial Jobless Claims (Mar 20) | |

| Actual | 210K |

| Consensus | 211K |

| Previous | 205K |

| 14:30 | USD |

| Natural Gas Storage (Mar 20) | |

| Actual | -54B |

| Consensus | -49B |

| Previous | 35B |

Sunset Market Commentary

Markets

ECB president Lagarde at the ECB Watchers Conference went into more detail on the central bank’s potential response to the energy shock. The strategy is based on three key principles. The first is to assess the nature, size and persistence of the shock before taking decisions on policy. The ECB must identify when higher energy costs risk spilling over into broad-based inflation – be it through indirect effects or through second-round effects via wages and inflation expectations. Lagarde admitted 2026 isn’t 2022 but its legacy lingers in the minds of consumers and businesses and this may prompt quicker pass-through effects. Yesterday’s PMIs are case in point. Secondly, the ECB focuses on risks – which may get non-linear – and not only the baseline. That translates into the third principle: having a set of options for how to respond, which depend on the intensity and duration of the shock and how it propagates. Lagarde then went on to point to three broad cases which, reading between the lines, basically correspond with the ECB’s baseline (A), adverse (B) and severe (C) scenario published last week. An energy shock limited in size and short-lived (A) would be looked through. In case of a shock leading to a large though not too-persistent overshoot of the 2% inflation target (B), some measured adjustment of policy could be warranted, also from a communication & signaling point of view. If inflation is expected to deviate significantly and persistently from target (C), the response must be appropriately forceful or persistent to prevent self-reinforcing mechanisms to kick in and risk a de-anchoring of inflation expectations. It is too soon to determine which scenario is prevailing, Lagarde noted. But in an echo to BoE’s Pill “fog of uncertainty cannot be an excuse for inaction” yesterday, the ECB president sounded resolute: “But we will not be paralyzed by hesitation: our commitment to delivering 2% inflation over the medium term is unconditional.”

Lagarde’s speech came against the backdrop of the US having ramped up diplomatic efforts to end the war with a 15-point proposal and a one-month ceasefire. Iran, however, already rejected the proposal. It has 5 conditions to begin talking about the end of the war, with “international recognition and guarantees of Iran’s sovereign authority over the Strait of Hormuz” probably not landing well in the US. Markets nevertheless take the optimistic view with stocks rebounding around 1.3% in Europe and 0.7-1.3% in the US. Brent oil fell towards the $100 barrier, down from $104.5 yesterday but up from intraday lows. European yields fell 6 bps across the curve at the open before entering a sideways trading range afterwards. Gilts hugely outperform with net daily changes varying between 8-12 bps despite above-consensus and -target February inflation numbers even before the Iran war erupted early March. The US curve bull flattens, showing declines up to 2.4 bps. Currency markets trade calm with a small US dollar bias. EUR/USD eases to sub 1.16, DXY moves higher towards 99.34. USD/JPY hovers around the recent highs just south of 160 (158.9 currently). Sterling treads water around EUR/GBP 0.865.

News & Views

In speech on purchasing power and the real cost of living in New Zealand, Reserve Bank of New Zealand Paul Conway observes that New Zealand is an expensive country, with prices for many products well above the OECD average. Since the pandemic, prices overall have risen by 26%, with prices for some essentials increasing by much more. Income per person has increased by slightly more, suggesting little change in purchasing power. Before 2020, purchasing power of wages grew faster than the OECD average, supported by strong employment growth and favourable terms of trade. Currently wage purchasing power is around the OECD average, but about 20% below the average of the more advanced economies. Monetary policy can anchor prices but can’t make New Zealand more affordable on its own. Sustained gains in purchasing power require higher productivity. Indicators suggest that the quality of structural policies in parts of New Zealand’s framework lag behind OECD best practice. On the current monetary policy stance, Conway indicated that he still sees excess capacity in the economy. At the April 8 meeting, the RBNZ will assess how much it has to lean against the wind in terms of potential rate hikes going forward. Markets see the RBNZ starting rate hikes in summer (May only 30% discounted), which might accelerate later with OCR near 3% discounted around year end. The Kiwi dollar underperformed the Aussie dollar already before and after the conflict in the Middle East started. NZD/USD eased from a peak just below 0.61 end January to currently 0.582.

BoE’s Greene Signals Inflation Concerns Without Immediate Hike Bias

BoE policymaker Megan Greene signaled that while inflation risks are rising, there is no immediate case for further tightening. At an even today, she said she “wasn’t tempted to hike” at the latest meeting, noting that higher inflation expectations increase risks but do not necessarily imply a sustained inflation cycle.

Greene emphasized that second-round effects remain uncertain. With the labor market weaker than during the 2022 inflation surge, the likelihood of strong wage-driven inflation appears lower. She also pointed to recent PMI data showing rising input costs, but cautioned that these indicators signal risk rather than a guaranteed outcome.

Despite this, Greene underscored that her primary concern is inflation rather than growth. She warned that energy prices are unlikely to fall back quickly due to damage to Gulf infrastructure, while food prices are expected to stay elevated.

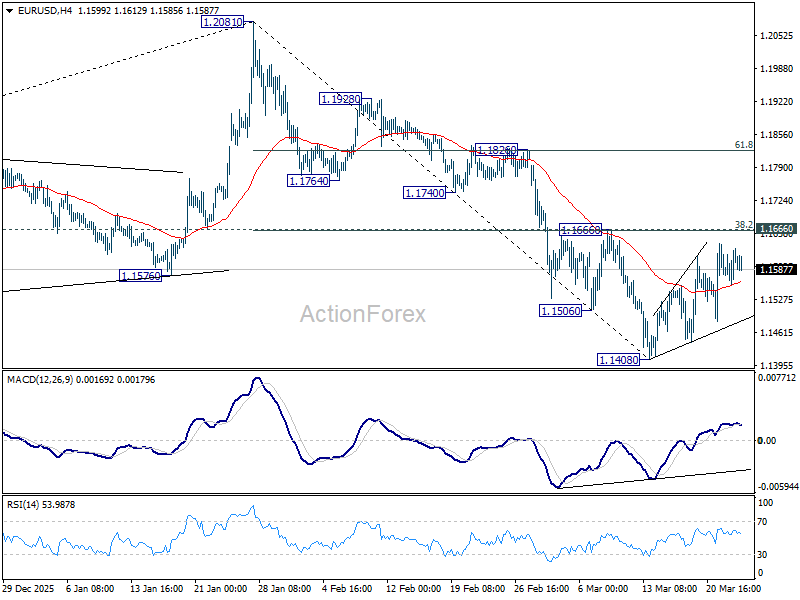

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1567; (P) 1.1597; (R1) 1.1638; More….

Intraday bias in EUR/USD remains neutral as consolidations continue above 1.1408. With 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665) intact, further decline is in favor. On the downside, below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

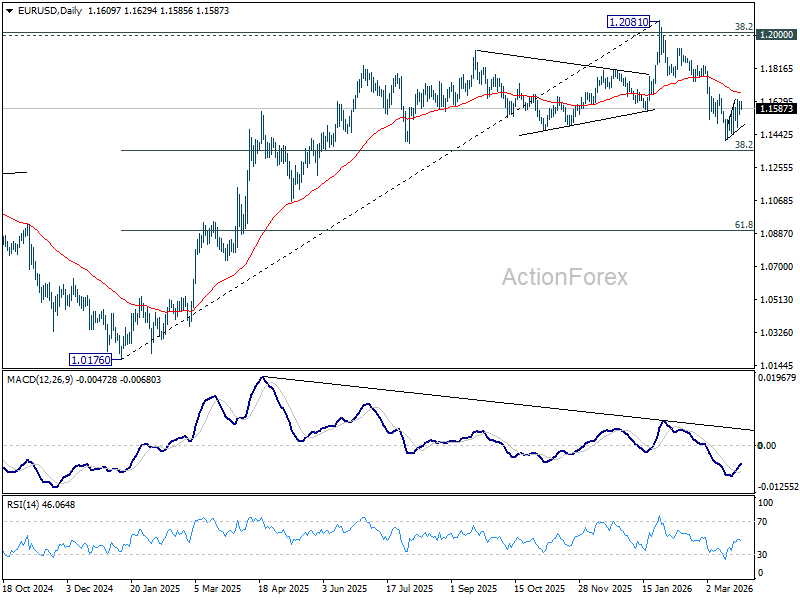

In the bigger picture, prior break of 55 W EMA (now at 1.1501) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0528). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

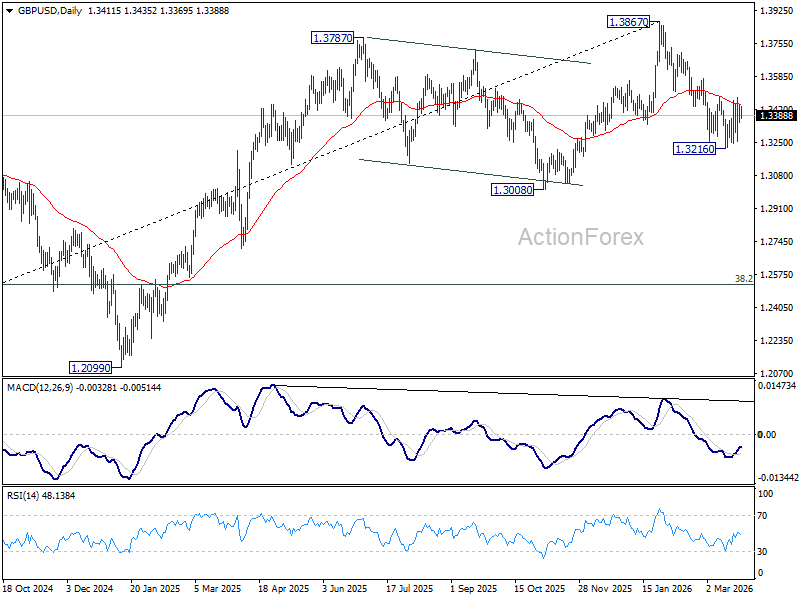

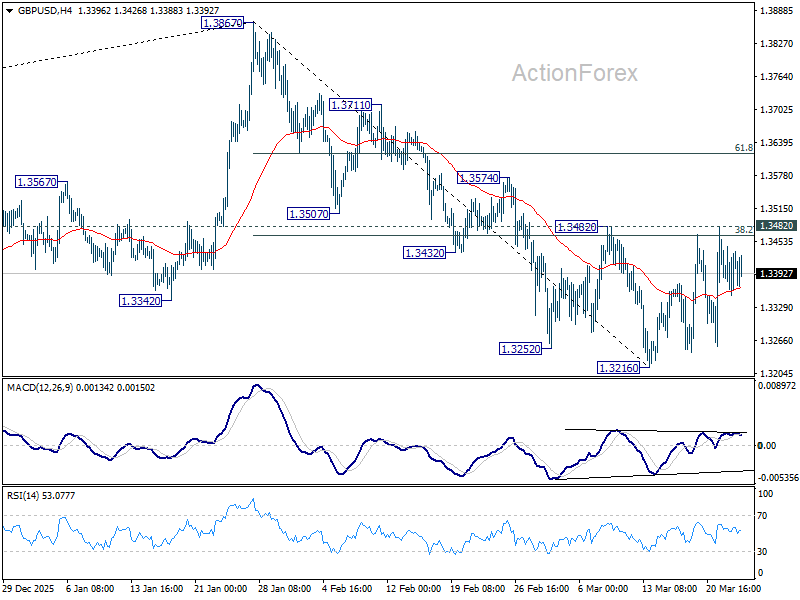

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3300; (P) 1.3389; (R1) 1.3522; More...

Intraday bias in GBP/USD remains neutral as range trading continues. With 1.3482 resistance intact, further decline is in favor. On the downside, below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.