Sample Category Title

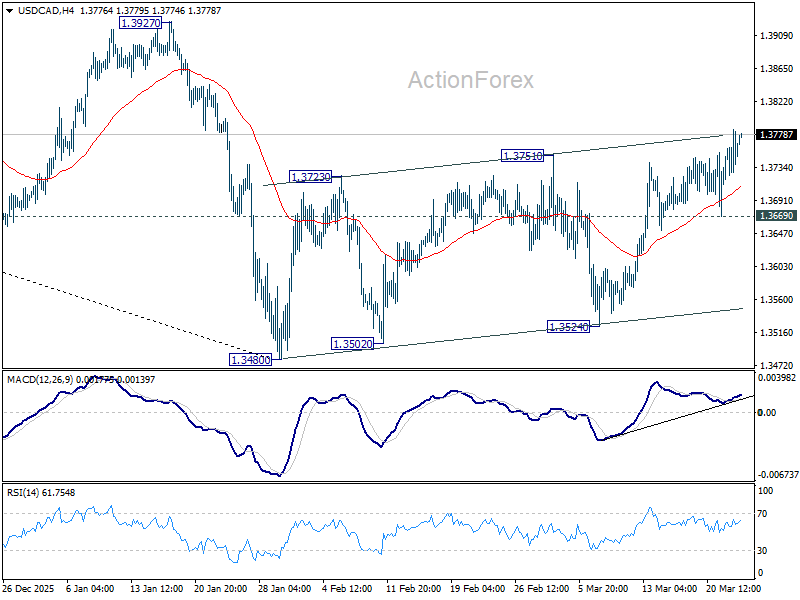

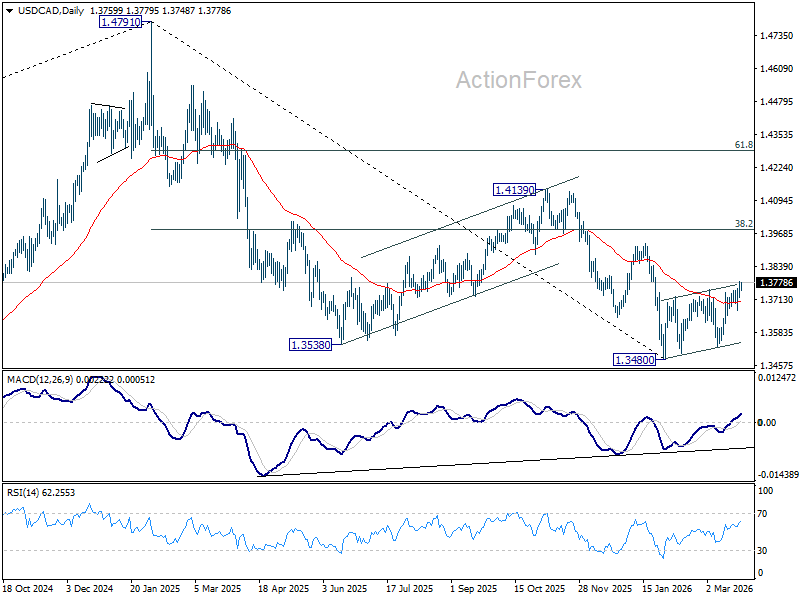

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3756; (R1) 1.3796; More...

Intraday bias in USD/CAD is back on the upside with break of 1.3751 resistance. Rebound from 1.3480 is seen as correcting the whole down trend from 1.4791. Further rise should be seen to 1.3927 resistance, and probably further to 38.2% retracement of 1.4791 to 1.3480 at 3981. For now, risk will stay on the upside as long as 1.3669 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

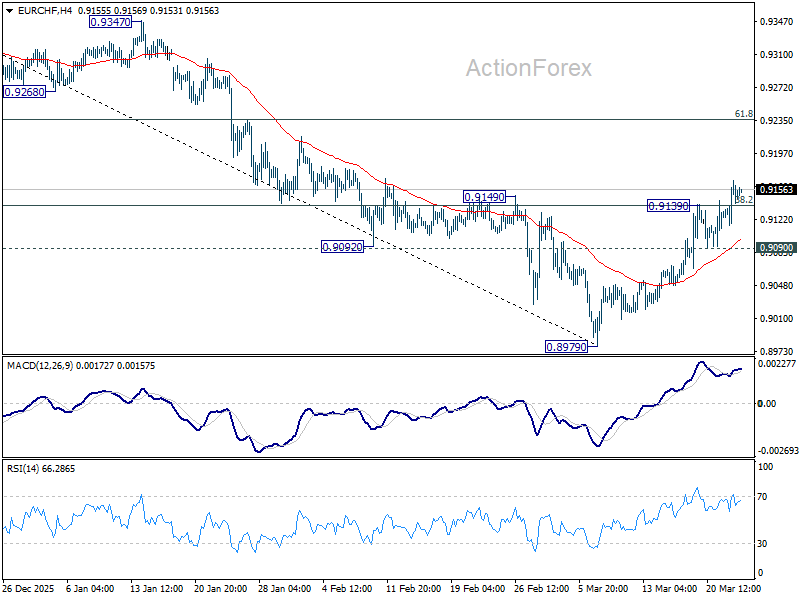

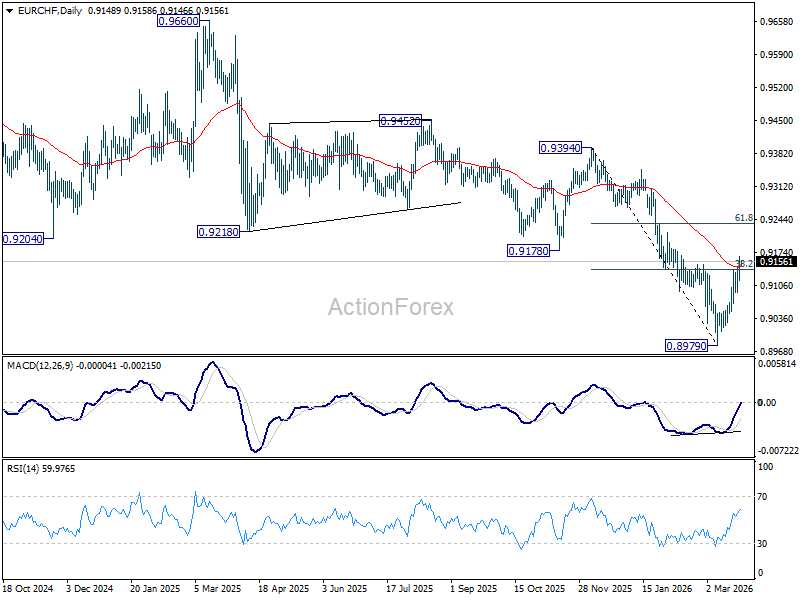

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9122; (P) 0.9145; (R1) 0.9174; More....

EUR/CHF's rebound from 0.8979 resumed by breaking through 0.9139 resistance and intraday bias is back on the upside. Further rally should be seen to 61.8% retracement of 0.9394 to 0.8979 at 0.9235 next. On the downside, below 0.9090 minor support will turn intraday bias neutral again first.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

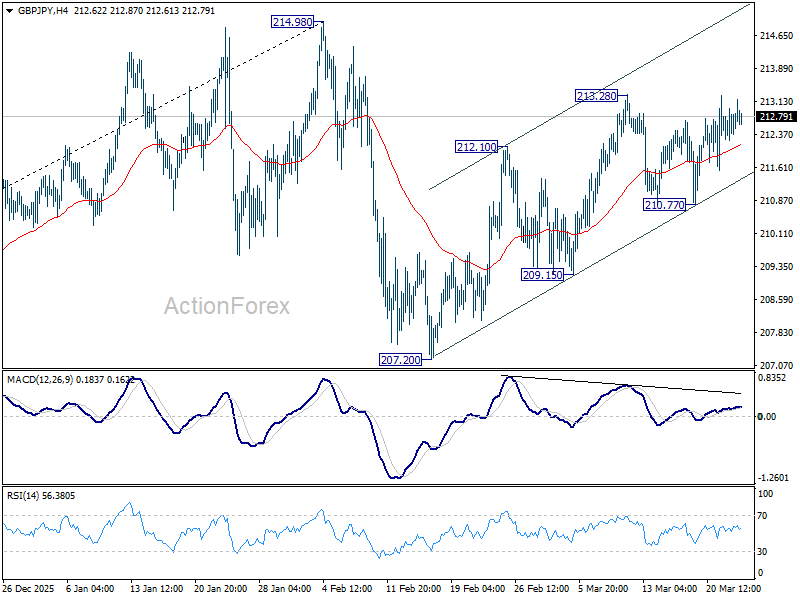

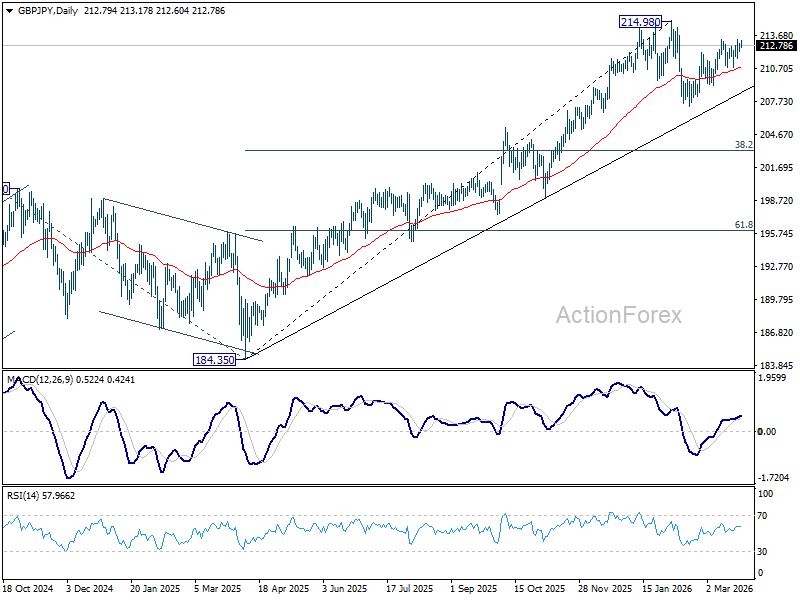

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.40; (P) 212.70; (R1) 213.12; More...

Intraday bias in GBP/JPY remains mildly on the upside at this point. Firm break of 213.28 resistance will resume the rally from 207.20 and target a retest on 214.98 high. For now, risk will stay mildly on the upside as long as 210.77 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

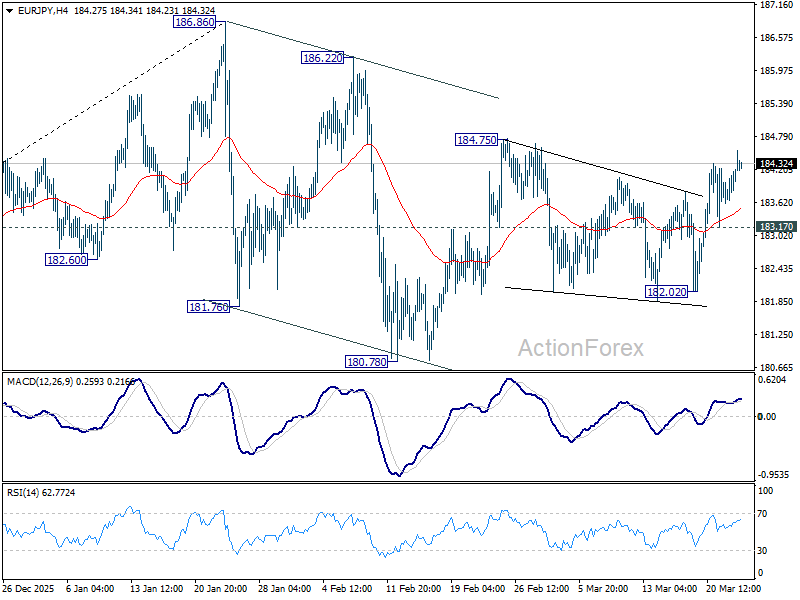

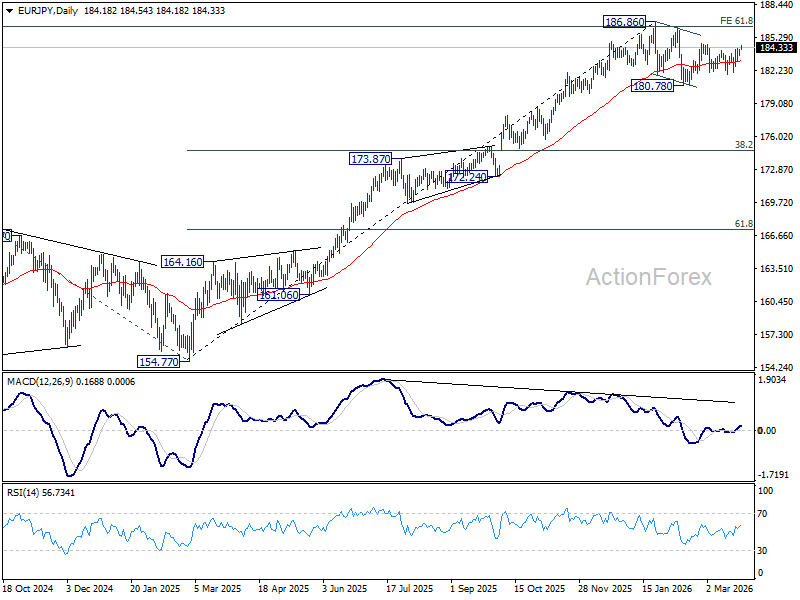

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.80; (P) 184.04; (R1) 184.45; More...

EUR/JPY's rebound is in progress and intraday bias stays on the upside. Firm break of 184.75 resistance will resume the whole rise from 180.78 and target a retest on 186.86 high. On the downside, below 183.17 minor support will turn intraday bias neutral first. Further break of 182.02 will bring deeper fall back to 180.78 support.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.61) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

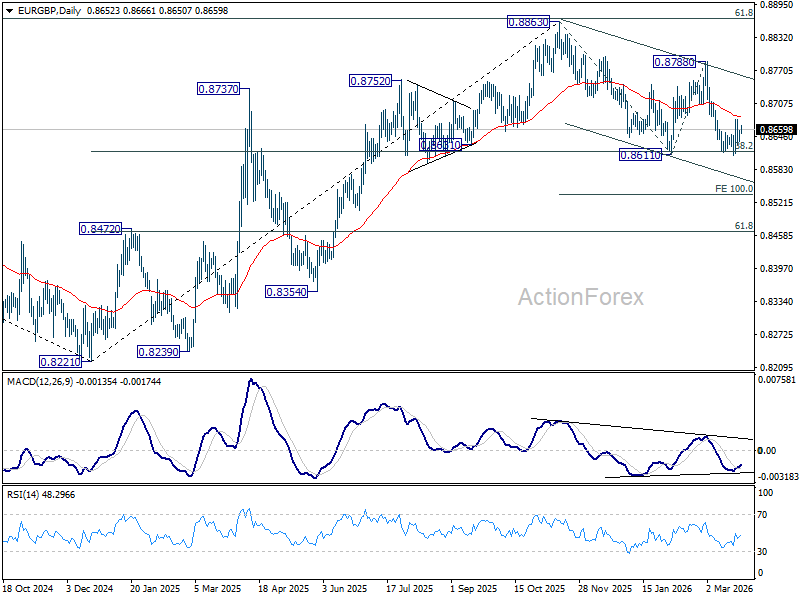

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8642; (P) 0.8652; (R1) 0.8665; More…

Range trading continues in EUR/GBP and intraday bias stays neutral. With 55 D EMA (now at 0.8682) intact, further decline is in favor. On the downside, firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536. However, sustained break above 55 D EMA will turn bias back to the upside for 0.8788 resistance instead.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

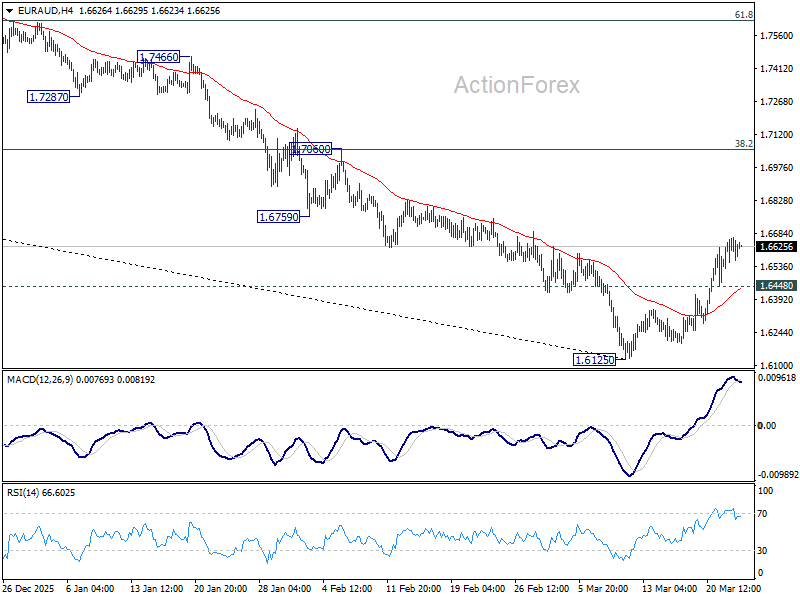

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6528; (P) 1.6600; (R1) 1.6664; More...

Intraday bias in EUR/AUD stays mildly on the upside at this point. Rebound from 1.6125 short term bottom should extend to 55 D EMA (now at 1.6757). Sustained break there will pave the way to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. Nevertheless, below 1.6448 minor support will suggest that the recovery has completed, and bring retest of 1.6125 low.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7245) holds, even in case of strong rebound.

Ceasefire Hopes Lift Markets, FX Signals Skepticism Over Strait of Hormuz Reopening

Markets are turning cautiously positive as hopes build around a potential ceasefire that could reopen the Strait of Hormuz, easing the current supply-side shock. The tone has shifted from outright panic earlier in the week to a more measured phase of “probing for a bottom,” though conviction remains limited.

Oil remains the key anchor. Brent crude has eased back to around 100 level, suggesting that some war premium is being priced out. However, the move is tentative, reflecting that markets are not yet convinced a lasting resolution is imminent. Equities are responding more positively. Asian stock markets are rebounding as investors begin to price in the possibility of an “off-ramp” scenario, where tensions de-escalate and supply disruptions are reversed.

In contrast, currency markets are signaling greater skepticism. The performance profile still leans risk-off, with Aussie sitting at the bottom of the weekly ladder, followed by Kiwi and Loonie. On the other hand, Sterling is leading gains, with Euro and Yen also outperforming, while Dollar and Swiss Franc are holding in the middle.

This divergence highlights a key dynamic: while equities are pricing hope, FX markets remain focused on uncertainty and policy implications. The lack of alignment suggests that current optimism is still fragile and highly conditional.

At the center of the narrative is a reported 15-point ceasefire proposal from the US, delivered via Pakistani intermediaries. The plan outlines a one-month ceasefire designed to create a window for broader negotiations. For markets, the most critical element is the immediate reopening of the Strait of Hormuz. Such a move would quickly alleviate supply constraints, reduce energy prices, and ease global inflation pressures. In exchange, the US is reportedly offering full relief from economic sanctions, signaling a willingness to pursue a diplomatic off-ramp even as military pressure remains in place.

However, the response from Iran has been dismissive. Officials have described the proposal as “negotiating with themselves,” maintaining a defiant stance and reiterating demands for reparations and guarantees against future strikes. At the same time, the military backdrop remains tense. The Pentagon continues to deploy additional forces to the region, including elements of the 82nd Airborne, underscoring that escalation risks have not been removed.

This dual-track dynamic—diplomacy alongside military buildup—keeps markets in a state of cautious balance. Until there is concrete progress, such as a confirmed reopening of Hormuz, the current optimism is likely to remain constrained.

In Asia, at the time of writing, Nikkei is up 3.00%. Hong Kong HSI is up 0.81%. China Shanghai SSE is up 1.17%. Singapore Strait Times is up 0.76%. Japan 10-year JGB yield is down -0.014 at 2.257. Overnight, DOW fell -0.18%. S&P 500 fell -0.37%. NASDAQ fell -0.84%. 10-year yield rose 0.058 to 4.392.

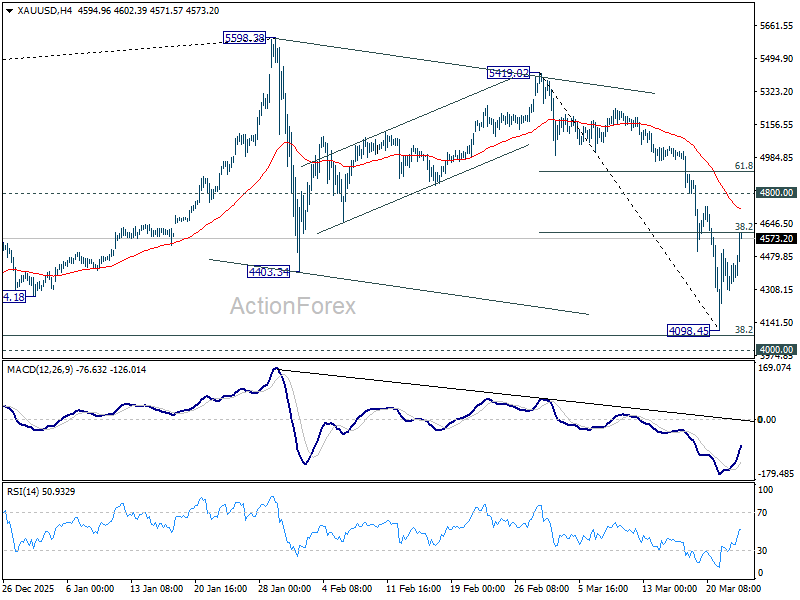

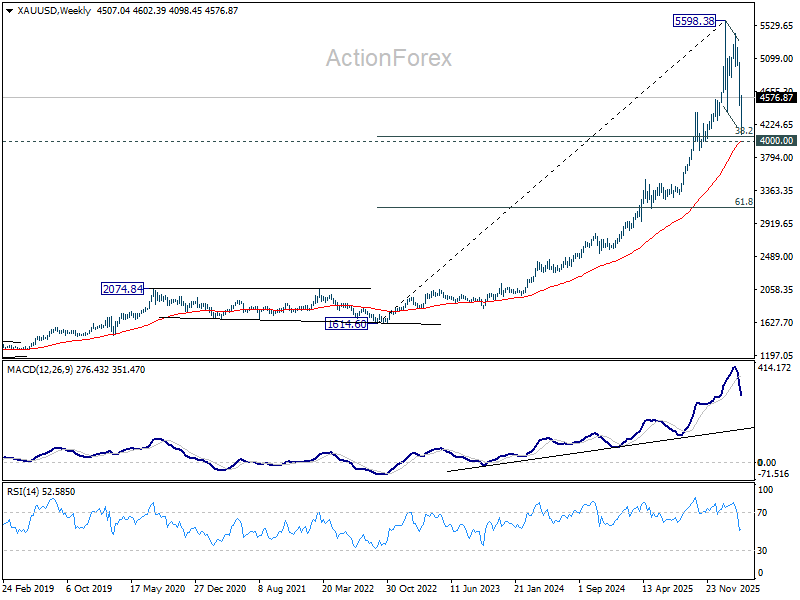

Gold Price Today: Bounce Faces ‘Sell-the-Rally’ Test at 4,600–4,800 Resistance Cluster

Gold price today rebounds on short covering but faces a key 4600–4800 resistance cluster, with the move seen as corrective in a sell-the-rally environment. Read More.

Australia Inflation Eases Pre-War, RBA Still Faces Sticky Core Pressures

Pre-war data show modest easing in Australia inflation, though underlying pressures remain firm and could rise again as energy costs increase. Read more.

Fed Rate Cuts on Hold as Barr Seeks Clear Inflation Progress

Fed Governor Michael Barr signaled that rate cuts remain on hold, stressing the need for clear evidence that inflation is sustainably declining, with rising oil prices posing fresh risks. Read more.

Interest Rate Path May Shift as Fed's Goolsbee Warns of New Inflation Shock

Fed’s Austan Goolsbee warned that a new energy-driven inflation shock could alter the interest rate path, stressing that rate cuts depend on clear progress toward 2% inflation. Read more.

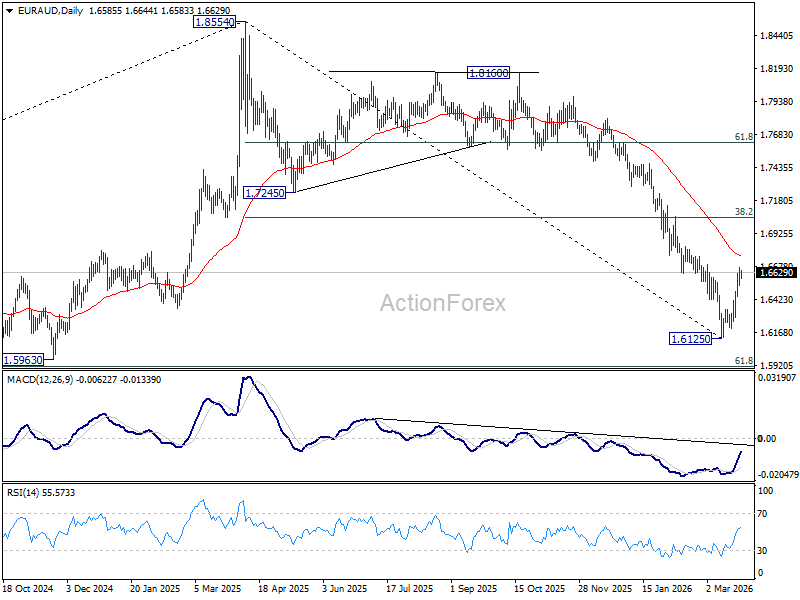

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6528; (P) 1.6600; (R1) 1.6664; More...

Intraday bias in EUR/AUD stays mildly on the upside at this point. Rebound from 1.6125 short term bottom should extend to 55 D EMA (now at 1.6757). Sustained break there will pave the way to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. Nevertheless, below 1.6448 minor support will suggest that the recovery has completed, and bring retest of 1.6125 low.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7245) holds, even in case of strong rebound.

Gold Price Today: Bounce Faces ‘Sell-the-Rally’ Test at 4600–4800 Resistance Cluster

Gold’s rebound is gaining some traction today as broader financial markets stabilize, but the move is still seen as corrective rather than the start of a sustained bullish reversal. The recovery follows a sharp and stretched selloff earlier this week, with price action below 4,100 triggering what appears to have been a near-term exhaustion point.

The initial lift has been driven largely by positioning. Profit-taking on short positions has provided the base for the rebound, rather than fresh bullish demand. Some support has also come from cautious optimism around de-escalation in the Middle East after the US announced a five-day postponement of strikes on Iranian energy infrastructure.

Technical factors have also played a role. The 4,000 level has emerged as a strong support zone, combining psychological significance with a key technical cluster. Bargain hunting interest around this level helped stabilize the market and reinforced the near-term floor.

However, the upside is now approaching a critical resistance “traffic jam” between 4,600 and 4,800. This zone includes 38.2% retracement of 5,419.02 to 4,098.45 at 4,602.90, as well as 55 4H EMA near 4,725. Together, these levels create a dense resistance band that is likely to cap further gains.

Importantly, this is also where short-term traders who bought into the rebound are likely to take profits. If selling pressure emerges in this zone, it would confirm that the market remains in a “sell-the-rally” regime rather than shifting to a “buy-the-dip” environment.

As long as this resistance holds, the broader outlook remains cautious. Another leg lower cannot be ruled out, but the 4,000 level, with 38.2% retracement of 1,614.60 (2022 low) to 5,598.38 (Jan high) at 4,076.57, should continue to act as a strong floor barring a major escalation in geopolitical tensions.

Only a firm break above 4,800 would signal that a more meaningful bullish reversal is underway. Such a move would likely indicate that macro risks—particularly related to energy and geopolitics—are easing.

Elliott Wave Perspective: Silver (XAGUSD) Nearing Support Floor

Silver (XAGUSD) reached an all-time high of $121.64 on January 29, 2026, before entering a larger corrective phase. The decline has unfolded as a zigzag Elliott Wave structure, a common corrective pattern in technical analysis. Wave a concluded at $71.31, while wave b terminated at $96.39. The market is now progressing through wave c, which is developing as an impulse Elliott Wave.

From the end of wave b, wave ((1)) finished at $77.92, followed by a rally in wave ((2)) that reached $90.09. The metal then extended lower in wave ((3)), which subdivided into five distinct waves. Within this sequence, wave (1) ended at $77.03, wave (2) at $82.53, wave (3) at $65.47, and wave (4) at $74.54. The final leg, wave (5), concluded at $60.95, thereby completing wave ((3)) at a higher degree.

At present, wave ((4)) is unfolding as a corrective rally. This move retraces the cycle that began from the March 10, 2026 high, before the market resumes its downward trajectory. In the near term, as long as the pivot at $90.09 remains intact, rallies are expected to fail in either three or seven swings. Such failure would confirm renewed downside pressure. The broader implication is that Silver remains vulnerable to further weakness once the current corrective rally exhausts itself.

Silver (XAGUSD) 60-Minute Elliott Wave Chart

XAGUSD Elliott Wave Video:

https://www.youtube.com/watch?v=xHQyvSYmKt8

AUD/USD: The Technical Squeeze Between 0.6980 and 0.7070

- Australia's annual CPI cooled slightly to 3.7% in February 2026, yet it remains above the RBA's target range.

- The AUD/USD pair is technically "coiled" within a tight trading range of 0.6980 and 0.7070.

- Near-term price direction will be dictated by US Dollar strength and geopolitical developments.

- Key levels to watch are a sustained bearish candle close below 0.6980 or a bullish breakout above 0.7070.

AUD/USD continues to struggle below the psychological 0.7000 handle following softer than expected CPI data. Market participants still seem to be erring on the side of caution with more rate hikes still expected from the RBA moving forward.

Soft CPI print fails to move the needle

Australia’s annual inflation rate showed signs of cooling in February 2026, dipping to 3.7%. This result was slightly lower than the 3.8% market forecast and the figures seen in the previous two months, though it remains stubbornly above the central bank’s 2–3% target range.

Source: TradingEconomics

A significant driver of this slowdown was the easing of goods inflation, which dropped to 3.5% from 3.8% in January. This was largely fueled by a sharp decline in transport costs, particularly automotive fuel, which fell by 7.2%, a much steeper drop than the 2.7% decline recorded before the recent Middle East conflict. Other sectors contributing to the downward trend included:

- Alcohol and tobacco: Eased to 4.3%

- Education: Slowed to 4.8%

- Clothing: Eased to 4.9%

- Communication: Dropped to 0.8%

While several categories cooled, price growth remained persistent in other areas. Inflation for food and non-alcoholic beverages held steady at 3.1%, and financial services remained at 2.4%. Conversely, costs accelerated for recreation (4.0%) and housing, with the latter jumping to 7.3% from 6.8%. Services inflation remained unchanged at 3.9%.

On a monthly basis, the Consumer Price Index (CPI) remained flat, a notable shift from the 0.4% increase seen in January. Additionally, the trimmed mean CPI, a key measure of underlying inflation edged down to 3.3%, coming in below both the previous figure and market expectations of 3.4%.

These latest numbers arrive at a time when the Reserve Bank of Australia (RBA) has already pushed interest rates up to 4.10% to fight stubborn inflation.

The RBA is worried that current price hikes might lead to "second-round effects," such as a cycle where wages and prices keep pushing each other higher. Because inflation isn't dropping as fast as hoped, many experts now expect the bank to raise interest rates again in the near future.

This in part explains the lack of conviction by AUD/USD bears with the pair failing to find any sustainable downside push since breaching the 0.7000 handle.

The path forward for AUD/USD

Given the lack of high impact Australian data in the coming days, the US dollar and geopolitical developments will be the driving force behind any immediate moves.

The US Dollar has been supported by risk off sentiment since the start of the US-Iran war. News that diplomatic efforts are underway has boosted sentiment with rumors of talks between the two countries as early as Thursday.

If sentiment continues to improve and hopes of a ceasefire grows, the US Dollar could continue to lose steam and this in turn could send AUD/USD back above the 0.7000 level.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis - AUD/USD

Based on the four-hour (4H) AUD/USD chart, the pair is currently caught between fundamental inflation concerns and a clear technical squeeze.

Current Price Action: The "Squeeze"

The chart shows AUD/USD trading within a descending triangle or a narrowing wedge pattern. After a sharp rejection from the 0.7130 area mid-month, the pair has been making lower highs, constrained by a descending trendline.

- Key Resistance Zone: There is a heavy "death cross" forming with the 50-period SMA (0.7038), 100-period SMA (0.7052), and 200-period SMA (0.7063) all hovering just above the current price. This creates a dense ceiling of resistance between 0.7040 and 0.7070.

- Psychological Support: The price is currently dancing around the 0.70000 psychological level. While it dipped toward 0.6940 recently, it has clawed back to the parity line, suggesting some dip-buying is occurring.

- RSI Neutrality: The RSI is sitting at approximately 45.50, which is neutral. It isn't oversold yet, meaning there is room for a move in either direction once the pattern breaks.

AUD/USD Four-Hour Chart, March 25, 2026

Source:TradingView.com

1. The Bearish Case (Breakdown)

If the RBA's 4.10% rate and the persistent 3.7% inflation data cause markets to fear a "hard landing" (economic slowdown), we could see a break below the recent support.

- Trigger: A sustained candle close below 0.6980.

- Targets: The first major target would be the recent swing low near 0.6940, followed by the long-term horizontal support at 0.6913.

2. The Bullish Case (Breakout)

If the market interprets the slight dip in inflation (3.7% vs 3.8%) as a sign that the RBA's hikes are finally working or if the RBA signals an aggressive hike to 4.35%, the Aussie could catch a bid.

- Trigger: A break and hold above the descending trendline and the cluster of SMAs (specifically above 0.7070).

- Targets: A successful breakout would likely see a quick move toward 0.7080, with a medium-term goal of retesting the March high at 0.7130.

Bottom Line: AUD/USD is coiled tightly. Until it breaks out of the 0.6980 – 0.7070 range, expect "choppy" sideways movement as the market digests the latest inflation data.