Sample Category Title

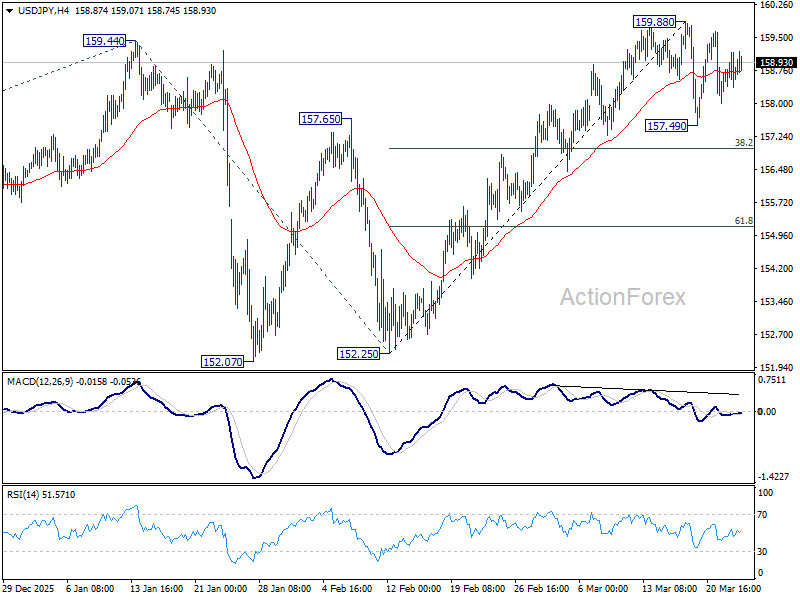

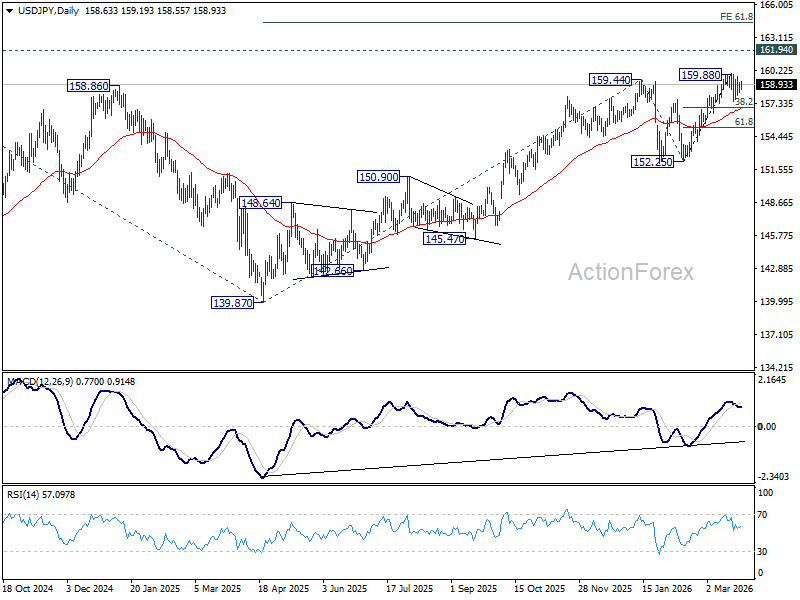

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.23; (P) 158.71; (R1) 159.19; More...

Intraday bias in USD/JPY stays neutral as consolidations continue below 159.88. In case of another dip, downside should be contained by 38.2% retracement of 152.25 to 159.88 at 156.96 to bring rebound. On the upside, break of 159.88 will target a test on 161.94 high.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

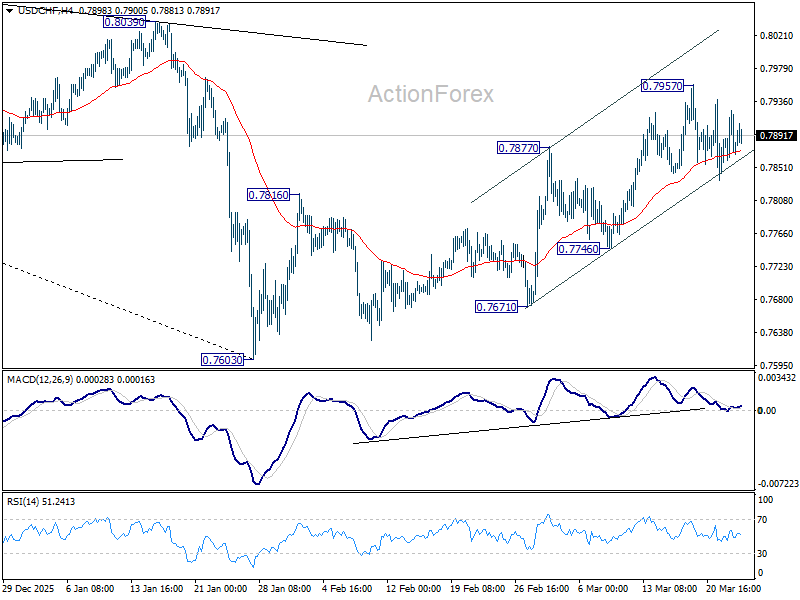

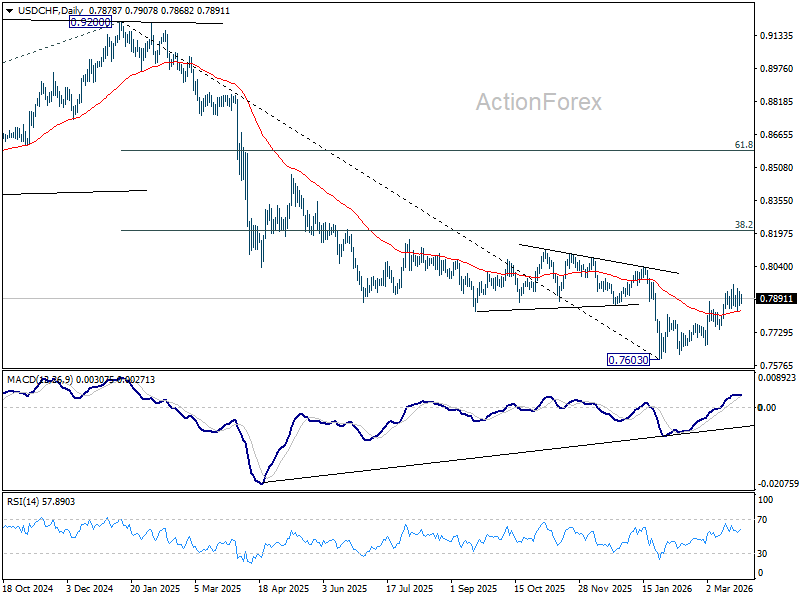

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7853; (P) 0.7889; (R1) 0.7919; More….

USD/CHF is still bounded in consolidations below 0.7957 and intraday bias stays neutral. As noted before, rise from 0.7603 should be correcting whole decline from 0.9200. Above 0.7957 will target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. This will remain the favored case as long as 0.7746 support holds.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

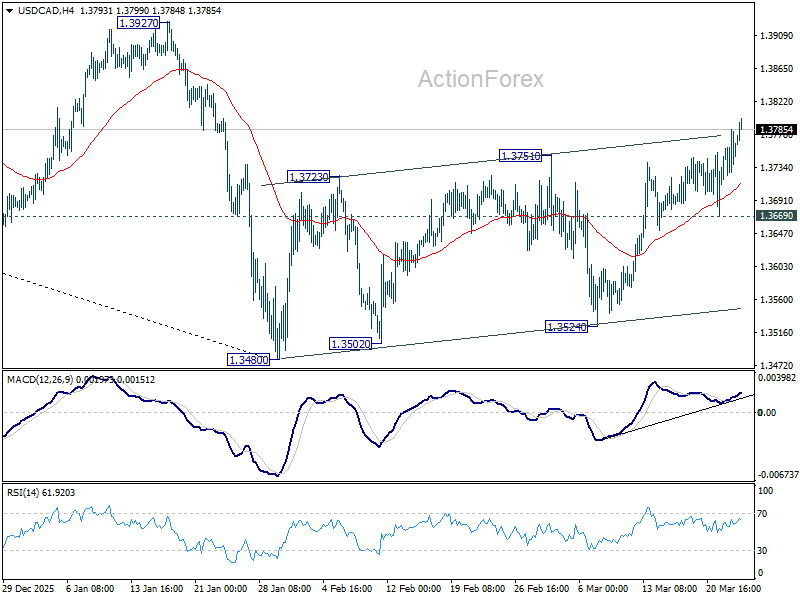

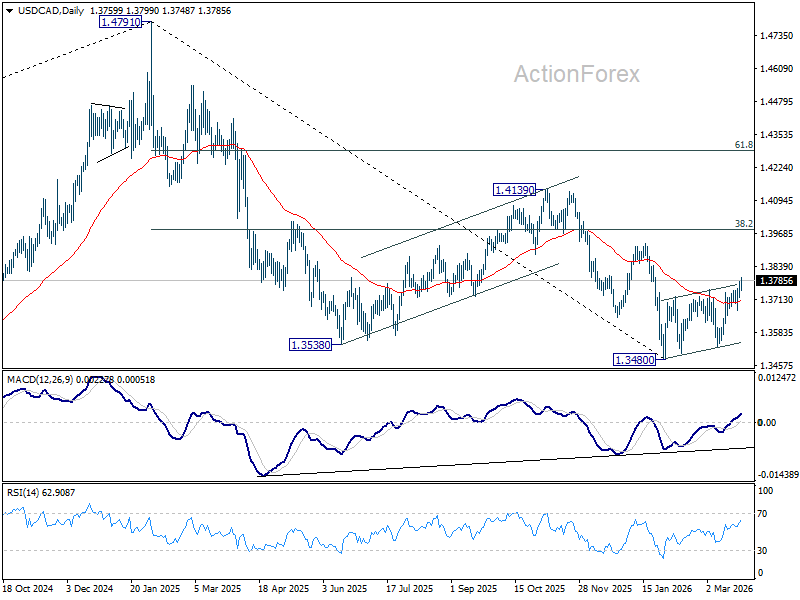

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3756; (R1) 1.3796; More...

Intraday bias in USD/CAD stays on the upside at this point. Rebound from 1.3480 is seen as correcting the whole down trend from 1.4791. Further rise should be seen to 1.3927 resistance, and probably further to 38.2% retracement of 1.4791 to 1.3480 at 3981. For now, risk will stay on the upside as long as 1.3669 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

Canadian Dollar Weakens on Oil Pullback as Markets Await Ceasefire Clarity

Loonie weakened as oil prices pulled back, with markets turning cautious while awaiting clarity on ceasefire negotiations between the US and Iran. Brent crude easing to the 100 level has triggered a de-risking move in energy-linked assets, removing a key pillar of support for the Canadian Dollar.

The move reflects more than just oil price dynamics. With Canada heavily reliant on energy exports, shifts in crude prices quickly feed into currency performance. At the same time, the domestic economy remains too fragile to absorb tighter policy, limiting the Bank of Canada’s ability to follow more hawkish peers.

Beyond oil, markets are broadly in a “wait-and-hope” mode. Negotiations around a US-led 15-point ceasefire plan appear to be ongoing, while Iran has signaled that non-hostile vessels may obtain safe passage through the Strait of Hormuz under coordination. These developments offer tentative signs of de-escalation, but fall short of a confirmed resolution.

That lack of clarity is keeping overall price action muted. While sentiment has improved marginally, it has not translated into decisive risk-on positioning. Instead, markets are holding steady, with investors reluctant to commit ahead of clearer geopolitical signals.

In currency markets, divergence is becoming more pronounced. Sterling firmed modestly following the UK’s February CPI release, while Aussie and Kiwi remain under pressure, reflecting their sensitivity to global growth risks.

The UK inflation data itself offered a slightly hawkish tilt beneath the surface. While headline CPI matched expectations, core inflation edged higher, driven by services and clothing prices. This suggests that underlying price pressures remain persistent.

More importantly, the data reflect pre-escalation conditions. Since then, energy prices have surged following disruptions linked to the Strait of Hormuz. Analysts are already projecting inflation to rise toward 3.5%–4.0% by autumn as higher fuel costs feed through.

This shift is reinforcing expectations that the Bank of England may be forced back into a tightening stance. Today’s CPI release adds weight to that view, suggesting that the disinflation path may be interrupted.

Comments from BoE Chief Economist Huw Pill yesterday further support this narrative. His remark that uncertainty “cannot be an excuse for inaction” signals that the hawkish camp within the MPC remains prepared to act if inflation risks become more persistent.

In contrast, Canada’s policy outlook appears constrained. With growth already soft and oil prices retreating, the Bank of Canada is unlikely to tighten, widening the divergence with central banks such as the BoE and ECB.

For the day so far, Dollar is the strongest performer, followed by Sterling and Euro. Aussie leads losses, followed by Kiwi and Loonie, while Yen and Swiss Franc are holding in the middle.

In Europe, at the time of writing, FTSE is up 0.92%. DAX is up 1.22%. CAC is up 1.10%. UK 10-year yield is down -0.153 at 4.799. Germany 10-year yield is down -0.007 at 2.967. Earlier in Asia, Nikkei rose 2.87%. Hong Kong HSI rose 1.09%. China Shanghai SSE rose 1.30%. Singapore Strait Times rose 0.87%. Japan 10-year JGB yield fell -0.016 to 2.255.

UK Inflation Unchanged at 3.0% as Services Keep Price Pressure Elevated

UK CPI held at 3.0% while core inflation rose to 3.2%, with rising energy prices now threatening to derail the disinflation trend. Read More.

German Business Sentiment Drops as Iran War Hits Confidence

Germany’s Ifo index weakened as firms turned more pessimistic, reflecting rising geopolitical uncertainty and fading recovery prospects. Read More.

Australia Inflation Eases Pre-War, RBA Still Faces Sticky Core Pressures

Pre-war data show modest easing in Australia inflation, though underlying pressures remain firm and could rise again as energy costs increase. Read more.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3756; (R1) 1.3796; More...

Intraday bias in USD/CAD stays on the upside at this point. Rebound from 1.3480 is seen as correcting the whole down trend from 1.4791. Further rise should be seen to 1.3927 resistance, and probably further to 38.2% retracement of 1.4791 to 1.3480 at 3981. For now, risk will stay on the upside as long as 1.3669 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

USD/CAD Rises to a Two-Month High

Today, the USD/CAD currency pair climbed above the 1.3787 level for the first time since late January.

- → Demand for the US dollar is being supported by concerns over escalating tensions in the Middle East. Market participants are favouring the USD as a safe-haven asset.

- → The Canadian dollar is under pressure due to domestic economic concerns. According to media reports, recent data point to weak GDP growth and a soft labour market. This increases the likelihood that the Bank of Canada will cut interest rates, while the Federal Reserve is expected to keep them unchanged.

Technical Analysis of USD/CAD

On 23 February, when the pair was trading around the 1.3700 level, we:

- → highlighted the ongoing long-term descending channel and the key support at 1.3500;

- → noted similarities with a rounding top pattern;

- → suggested a scenario in which bears might attempt to regain control and resume the longer-term downtrend.

Indeed, in the following sessions, USD/CAD showed signs of strong selling pressure, with the most pronounced move occurring on 9 March, when the pair dropped below 1.3530.

However, the onset of the Middle East conflict and other factors have significantly shifted market sentiment. The long-term descending channel has now been broken, suggesting that:

- → bulls have regained control of the market;

- → the pair may continue to develop within a newly formed ascending channel (shown in blue);

- → the 1.3700 level, which previously acted as resistance, may now serve as support going forward.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Currency Market Awaits Negotiations

- The global economy is heading towards 1970s-style stagflation.

- EURUSD depends on US-Iran talks.

The world is moving towards stagflation, and the currency market risks repeating the experience of the 1970s. Back then, the oil crisis led to soaring prices and a slowdown in economic growth. The Fed yielded to pressure from the White House and started cutting rates. The result was runaway inflation and a double-dip recession. With Kevin Warsh at the helm of the central bank, this remains a possibility. However, for now, the USD continues to respond to news from the Middle East.

The increase in prices tied to the armed conflict is slowing European and American business activity to its lowest levels since April–May 2025. Purchasing Managers’ Indexes, by contrast, are rising swiftly. These indicate a stagflationary scenario, which is purportedly supporting the US dollar. Goldman Sachs believes the greenback will weaken if investors fear not stagflation but recession, causing capital to flow into the Swiss franc and the Japanese yen.

New talks are fuelling rumours of US-Iran negotiations. Washington has provided Tehran with a list of 15 demands, and Tehran is preparing its own list in reply. Brent is falling, stripping the dollar of the advantage that has propelled its rise in recent weeks, driven by a flight to safe-haven assets and a reassessment of the trade balances of the world’s largest economies.

If the talks do indeed take place and are constructive, EURUSD will revert to its main drivers. Primarily, monetary policy. Divergence in this area favours the euro. The futures market anticipates the Fed will keep the federal funds rate on hold until the end of the year, with some chance of a hike. Meanwhile, the ECB can tighten monetary policy two or three times. However, this may not be necessary. If oil prices drop, the inflation spike will be brief.

It is by no means certain that progress will be made in the US-Iran talks, especially in the initial phase, given the parties’ significant differences. Bad news will put pressure on EURUSD, though a collapse is unlikely. Similarly, one should not harbour hopes that Brent prices will return to pre-war levels, regardless of how quickly the Strait of Hormuz is reopened.

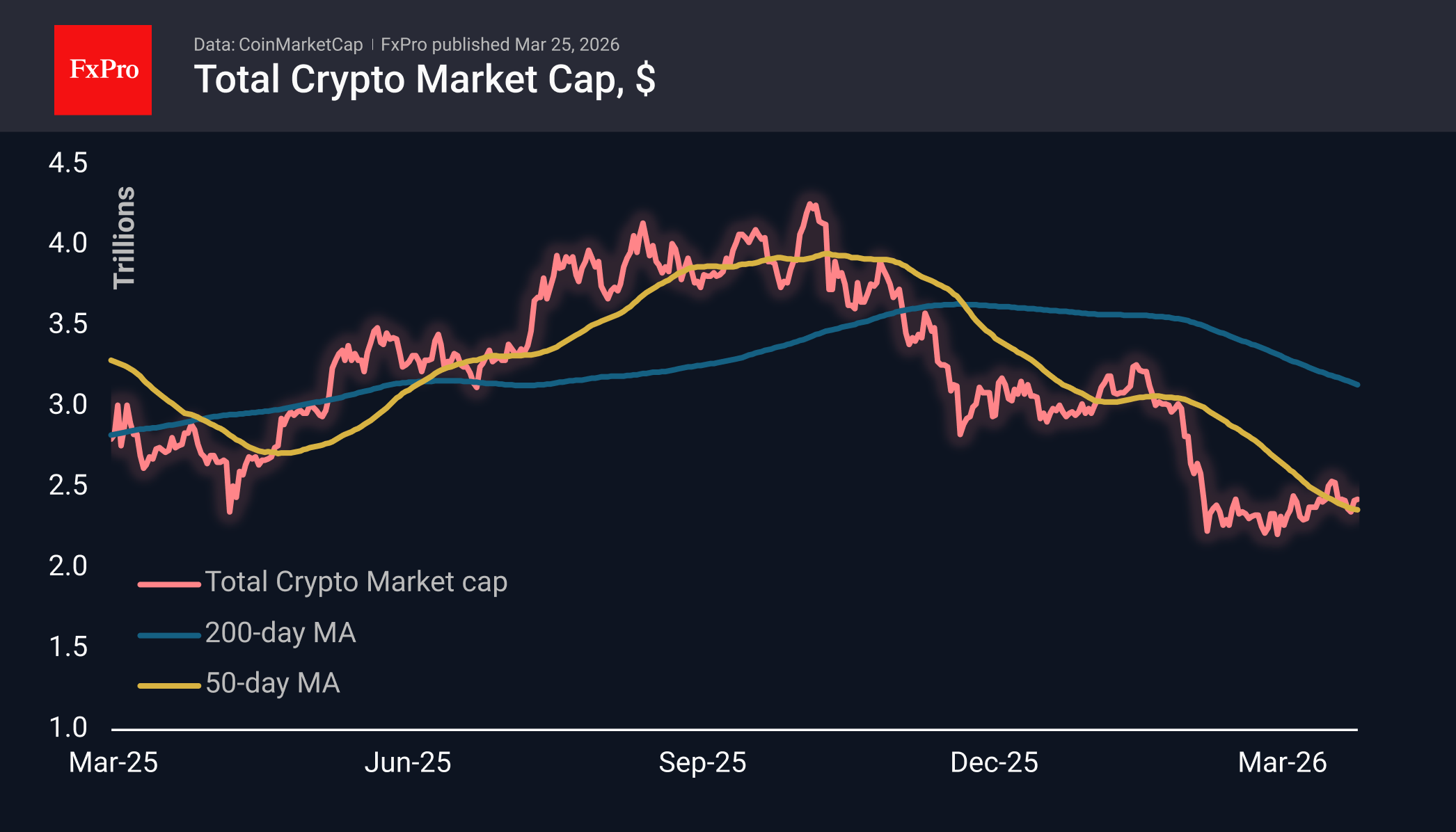

Crypto Market Laying the Ground for Growth

Market Overview

The crypto market cap has increased by 0.3% over the past 24 hours to $2.43 trillion. The market’s ability to hold at recent highs while maintaining low volatility is a sign of buyer confidence and readiness for a further rally. Conversely, bears may be merely allowing these fluctuations for now, as the market remains within a correctional rebound pattern following the collapse two months ago. A move above $2.5T will be necessary before we can consider a bullish breakthrough and evaluate the prospects of a recovery to $3–3.3T.

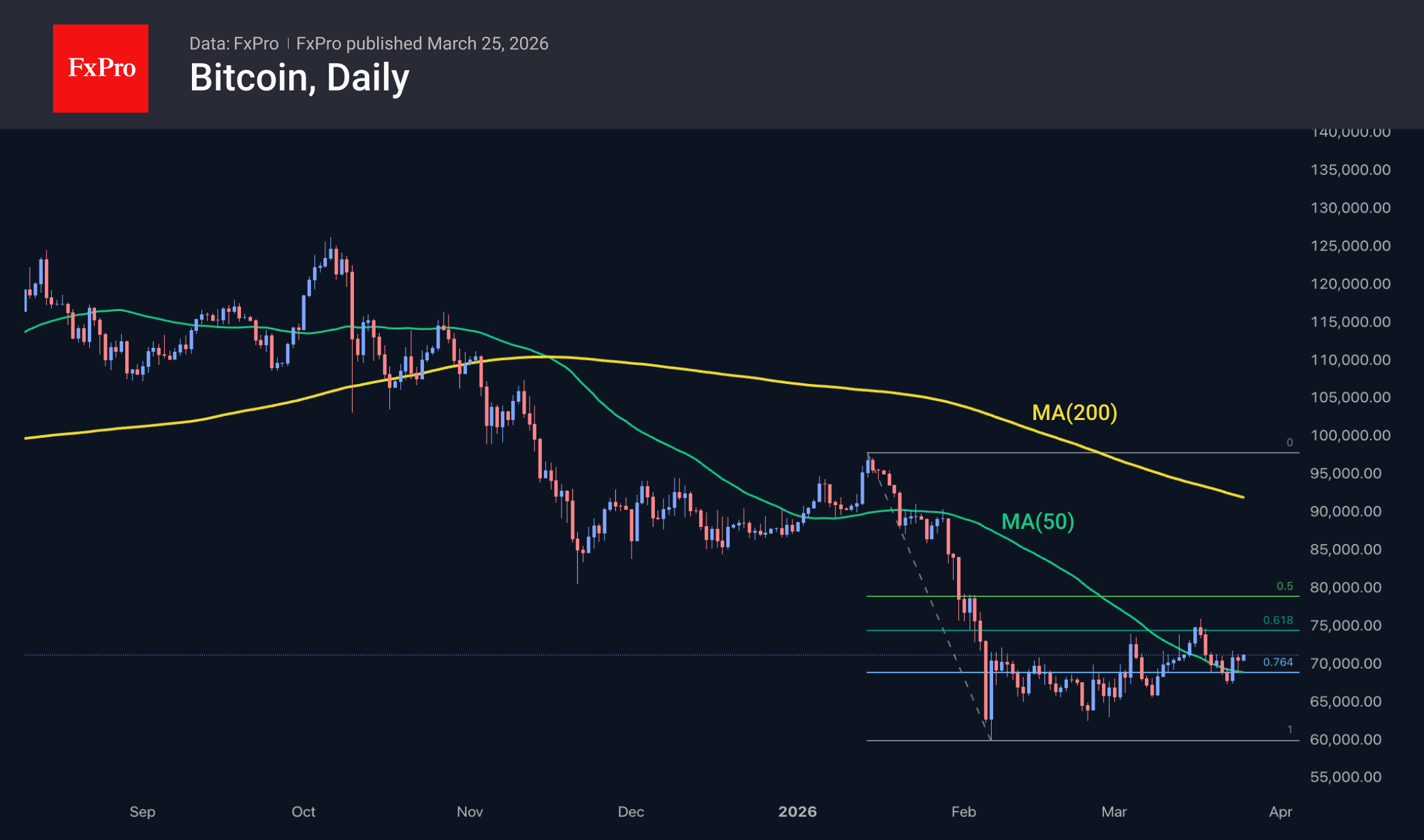

Bitcoin is trading near $71K, encountering resistance for the sixth consecutive day as it attempts to climb above $71.5K. However, this seems to be a short-term setback, considering the pattern of higher local lows since early February. Additionally, the 50-day moving average over the past two months has dropped from $90K to $70K, lowering the barrier that bulls need to overcome to signal a trend reversal.

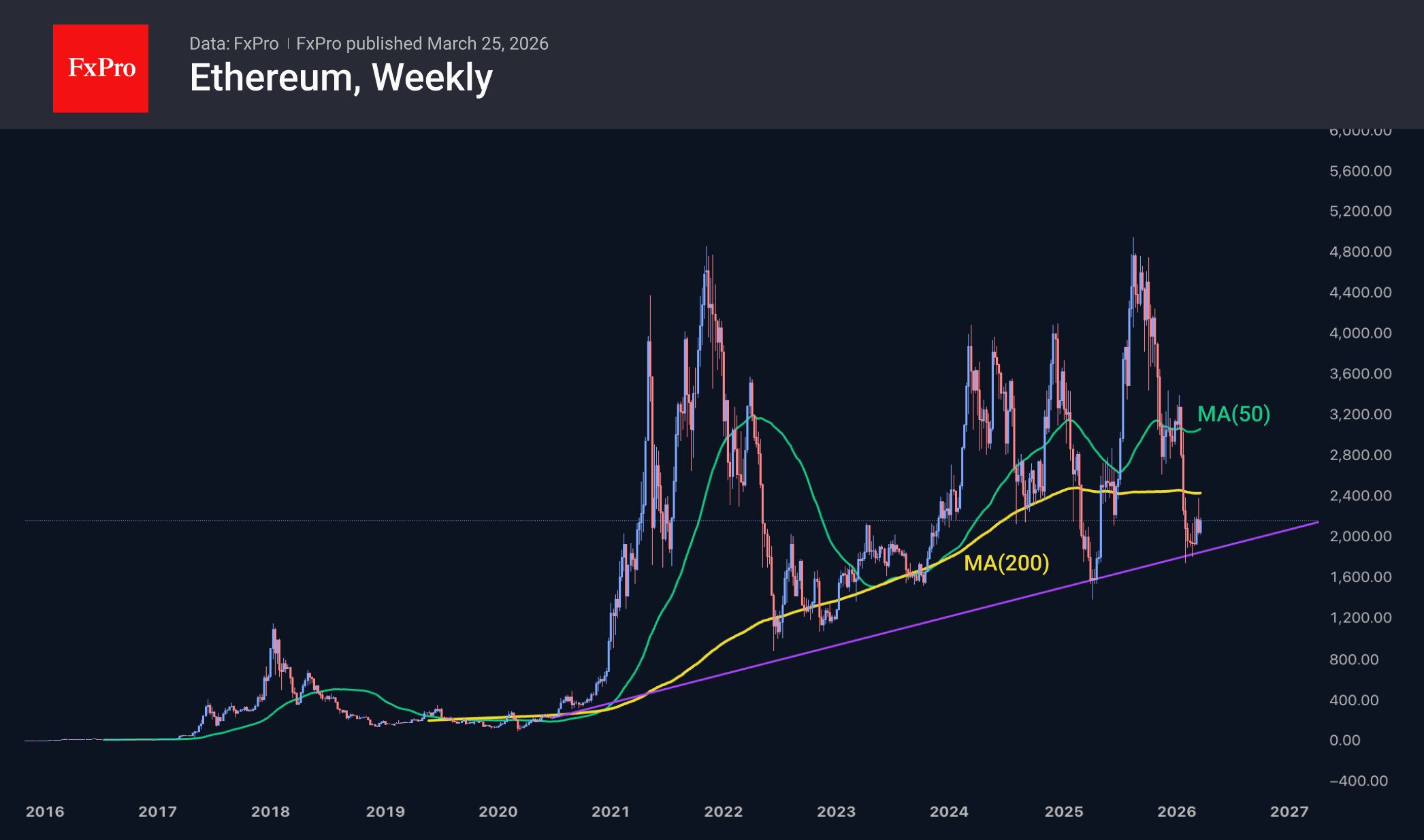

Ethereum, trading above $2,200, continues to rebound from a long-term support line near $1,800, up from $1,550 a year earlier. However, the second-largest cryptocurrency remains below its 50- and 200-week moving averages, indicating a bearish market sentiment. By all accounts, Ethereum is no longer a good choice for a ‘buy and hold’ strategy. However, right now is a relatively good time to buy for a holding period of up to a year, with the potential for a twofold increase.

News Background

Bitcoin could boost its growth if it surpasses $72K, as there is no major seller resistance in the $82K range, according to Bitfinex Research.

The Bitcoin miner activity index has fallen to its lowest point ever. CryptoQuant describes this as a potentially bullish signal.

According to Bloomberg, Hostplus, one of Australia’s largest pension funds with $105 billion in assets, is considering offering participants access to cryptocurrency investments.

The stablecoin market has gained a new long-term growth driver: autonomous programmes based on artificial intelligence (AI agents), notes Bernstein. Circle and Coinbase could be the key beneficiaries of AI-powered payments.

The Financial Stability Board (FSB), under the G20, has highlighted the growing risks associated with stablecoins, despite the crypto market’s limited influence on the financial system in 2025.

The Ethereum Foundation has unveiled a new strategic vision for the role of layer-2 (L2) networks. Ethereum will remain the most decentralised hub for settlement, liquidity, and decentralised finance.

The Solana Foundation has introduced a new approach to attract major institutional clients, based on adaptable privacy options.

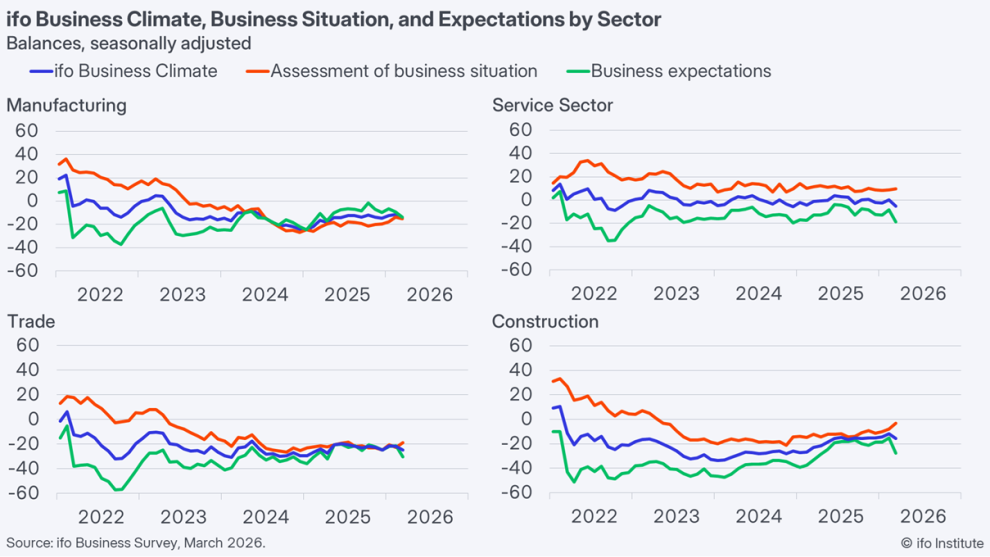

German Ifo Business Sentiment Drops as Iran War Hits Confidence

Germany’s Ifo Business Climate index deteriorated in March, falling from 88.4 to 86.4, as the escalation in the Middle East weighed heavily on corporate sentiment. The decline was driven by a notable drop in expectations, which fell from 90.2 to 86.0, while the current situation index remained unchanged at 86.7.

The weakness was broad-based across sectors. Manufacturing sentiment worsened from -11.5 to -14.3, while services saw a sharp shift from slightly positive territory at 0.1 to -5.1. Trade and construction also deteriorated further to -24.6 and -15.8 respectively, underscoring the widespread impact of rising uncertainty and weaker demand conditions.

Ifo President Clemens Fuest noted that sentiment has “dropped by a considerable degree,” adding that the war in Iran has effectively put any recovery hopes “on ice.” The data suggest that Germany’s fragile recovery has stalled, with geopolitical risks now compounding existing structural weaknesses in Europe’s largest economy.

UK February Inflation: Stable Headline Rate Masks Rising Retail and Housing Costs, GBP/USD Steady

- UK annual inflation held steady at 3% in February 2026, matching the previous month’s figure.

- The Bank of England (BoE) faces a policy dilemma as public inflation expectations soar amid war fears and manufacturing cost increases.

- The GBP/USD pair remained largely flat, trading in a "squeeze" between key moving averages, which suggests an imminent technical breakout is likely.

Data from the ONS showed the UK's annual inflation rate held firm at 3% in February 2026, matching the previous month's figure and meeting market expectations. This consistency marks a continued period of relative stability, with inflation remaining at its lowest point since March 2025. While the headline figure remained unchanged, the underlying data revealed shifting price pressures across various sectors.

Source: TradingEconomics

Primary Drivers of Price Growth

The most significant upward pressure came from the clothing and footwear sector, which saw prices climb by 0.9%. This represents the first increase in four months, largely driven by the seasonal arrival of new spring collections following the conclusion of January sales. Additionally, costs for housing and utilities experienced a slight acceleration, rising to 4.6% from 4.5% in January.

Sectors Seeing a Slowdown

Conversely, several categories helped keep the headline rate in check:

- Transport: Prices slowed to 2.4% (down from 2.7%), primarily due to a drop in motor fuel costs. Petrol prices fell by 1.6 pence per litre this month, a sharp contrast to the 2.0 pence per litre increase seen during the same period last year.

- Essential Goods and Leisure: Food inflation eased to 3.3%, while recreation and culture slowed slightly to 2.5%.

- Hospitality and Services: Costs for restaurants and hotels cooled to 4%, and the closely watched services inflation rate ticked down to 4.3%.

Overall, the data suggests a balancing act where rising retail and housing costs are being offset by cheaper fuel and a gradual cooling in service and food prices.

Inflation expectations soar on Iran war fears

The Bank of England (BoE) faces an increasingly complex policy environment as new data released on Tuesday revealed a surge in public inflation expectations. This shift in sentiment compounds an already difficult situation for policymakers, as manufacturers have reported their sharpest cost increases since 1992, pressures that are expected to be passed on to consumers in the near future.

Household energy tariffs are currently capped, a scheduled price adjustment in July looms as a significant upcoming catalyst for further inflation. These mounting pressures have created a notable divide between market participants and economic forecasters regarding the BoE's next move.

As of Tuesday per LSEG data, investors were pricing in nearly three quarter-point interest rate hikes before the end of the year to combat rising prices. This should keep GBP partially supported in the interim.

However, any significant escalation to tensions in the Middle East could see the US Dollar surge once more and this could drag on cable.

The initial market reaction

Markets seemed to shrug off today's data with GBP/USD remaining largely flat after the release.

Looking at the bigger picture technical outlook, GBP/USD is caught between long-term bearish momentum and a recent short-term recovery.

The pair is currently trading in a "squeeze" between two critical Simple Moving Averages (SMAs). While the price has recovered from its mid-March lows, it remains capped by the 200-period SMA (dark blue) at 1.34567, which is currently acting as dynamic resistance.

Conversely, the 100-period SMA (light blue) at 1.33560 has shifted from resistance to support, providing a floor for the recent price consolidation. The narrow range between these two averages suggests an imminent breakout is likely as the price searches for a definitive direction.

The path of least resistance appears slightly tilted to the downside unless the bulls can clear and close above the 1.34500 – 1.35000 resistance cluster. A rejection at the 200 SMA could lead to a retest of the 1.3333 support.

However, if the price holds above the 100 SMA, we may see further consolidation before a breakout attempt.

GBP/USD H4 Chart, March 25, 2026

Source: TradingView.com

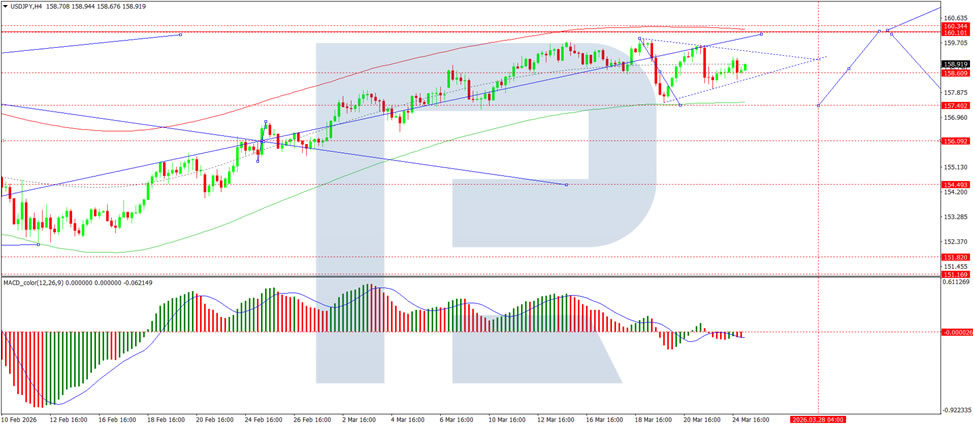

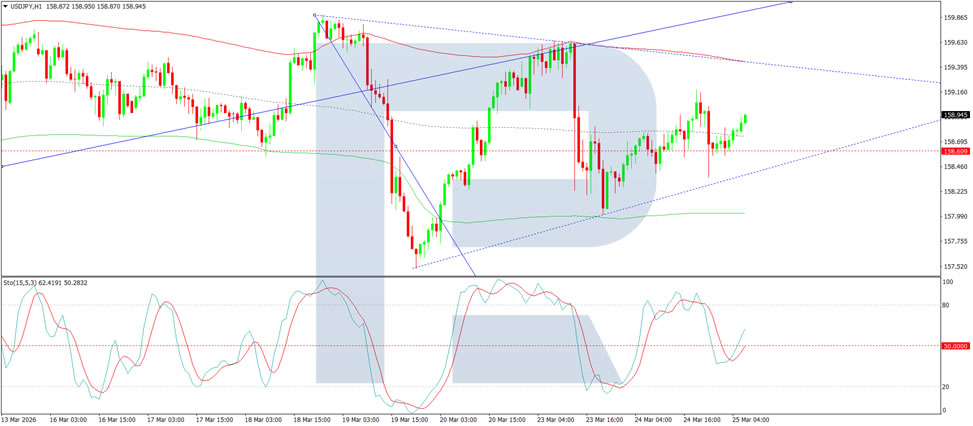

USD/JPY Maintains Growth Mood: Market Sympathies on the US Dollar Side

USD/JPY continues its upward trajectory on Wednesday, rising to 158.78 following a volatile start to the week. Pressure on the yen has eased amid a pullback in oil prices and expectations of a potential resolution to the Middle East conflict-a development of particular significance for Japan's energy-importing economy.

The move comes amid reports of US diplomatic efforts aimed at resolving the conflict with Iran. However, scepticism persists in the market, as Tehran had previously denied the existence of any negotiations with Washington.

Additional support for the yen stems from expectations of possible government intervention. Japanese officials have signalled their readiness to take necessary measures to stabilise the currency.

It has also been reported that Japan's Ministry of Finance is in contact with market participants regarding potential intervention in the oil futures market, given its impact on the yen.

Technical Analysis

On the H4 chart, USD/JPY is forming a consolidation range around the 158.60 level. A decline to 157.40 is expected today, followed by an increase to 158.50. Should the market break upwards from this range, a correction towards 160.10 would be relevant to consider. Subsequently, a new downward impulse to 157.40 is anticipated, with the potential for the correction to extend to 156.00.

Technically, this scenario is confirmed by the MACD indicator-its signal line is below zero and pointing strictly downwards, reflecting the potential for continued correction.

On the H1 chart, the market is shaping a downward wave pattern towards 157.40. Reaching this target level will be considered today. Following the completion of this wave, the development of the next growth wave to 160.10 (test from below) is expected.

The scenario is confirmed by the Stochastic oscillator-its signal line is below the 50 level and pointing strictly downwards towards 20, indicating that short-term downside potential remains.

Conclusion

USD/JPY remains in a growth-oriented mood as easing oil prices and tentative hopes for diplomatic progress in the Middle East offer some relief to the yen. While reports of US-led negotiations with Iran have contributed to a pullback in energy markets, market scepticism persists given Tehran's earlier denial of talks. Japanese authorities stand ready to intervene should volatility spike, adding an element of caution for traders. Technical indicators point to a short-term correction lower before the broader upward trend potentially resumes towards 160.10. The yen's trajectory remains closely tied to developments in both energy markets and geopolitical tensions, which continue to shape the Bank of Japan's policy landscape.