Sample Category Title

Gold Out of Favour: All Eyes on Inflation Risks

Gold prices fell to 4,300 USD per ounce on Tuesday, with quotes remaining under pressure amid the escalating Middle East conflict. Iran has denied reports of any talks with the US, stating that no such contacts have occurred.

Tehran dismissed Donald Trump's statements as an attempt to influence financial markets and has continued its attacks on American targets. Israel, meanwhile, continues to strike Iranian territory.

Gold saw a brief recovery earlier after Trump postponed potential strikes on Iran's energy infrastructure and announced that negotiations had allegedly begun. However, the prospects for resolving the conflict and reopening the Strait of Hormuz remain uncertain, keeping inflation risks elevated.

Since its March peak, gold has lost up to 25% amid rising energy prices. The rally in commodity prices has reinforced expectations of tighter monetary policy, weighing on the non-yielding asset.

Technical Analysis

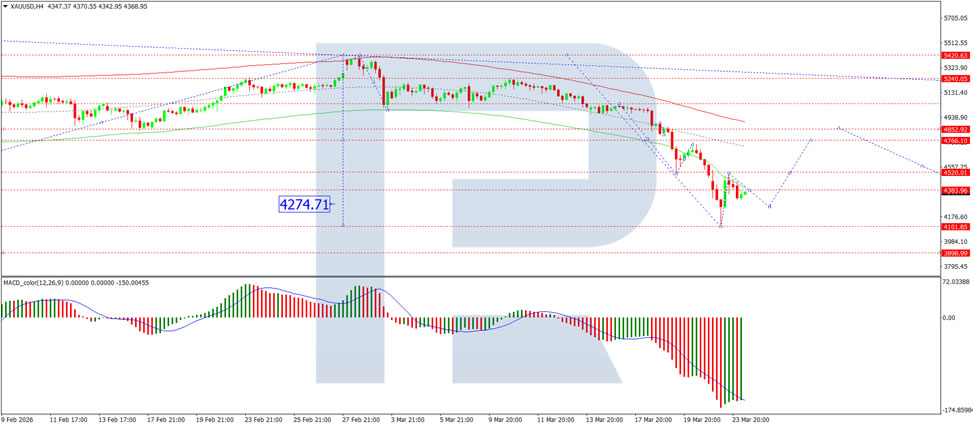

On the H4 XAU/USD chart, the market is forming a consolidation range around the 4,383 USD level. An upside breakout would open the path for a correction towards 4,850 USD, while a downside breakout could see the downward wave extend to 4,272 USD. The MACD indicator confirms the current momentum, with its signal line below the centre line but pointing sharply upwards.

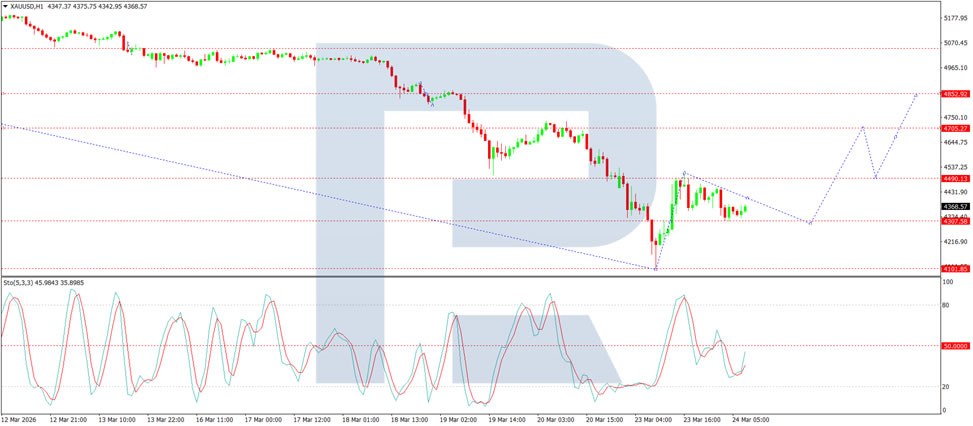

On the H1 chart, the market broke above the 4,300 USD level and completed a wave to 4,414 USD. Looking ahead, a corrective move back to 4,308 USD is likely, followed by an anticipated rise to 4,505 USD. The Stochastic oscillator supports this scenario, with its signal line remaining above the 20 level and showing potential to rise towards 80.

Conclusion

Gold continues to fall out of favour as the market prioritises inflation risks driven by the protracted Middle East conflict. Despite brief moments of relief following headlines about potential negotiations, the underlying reality of sustained hostilities and uncertainty over the Strait of Hormuz keeps energy prices elevated, and monetary policy expectations tilted towards tighter conditions. Having lost a quarter of its value from its March highs, gold now faces a challenging environment in which concerns about rising rates repeatedly overshadow safe-haven demand. While technical indicators suggest a short-term bounce is likely, the broader trend remains firmly bearish.

Dow Futures (YM): Tracking a Double Three Elliott Wave Pattern

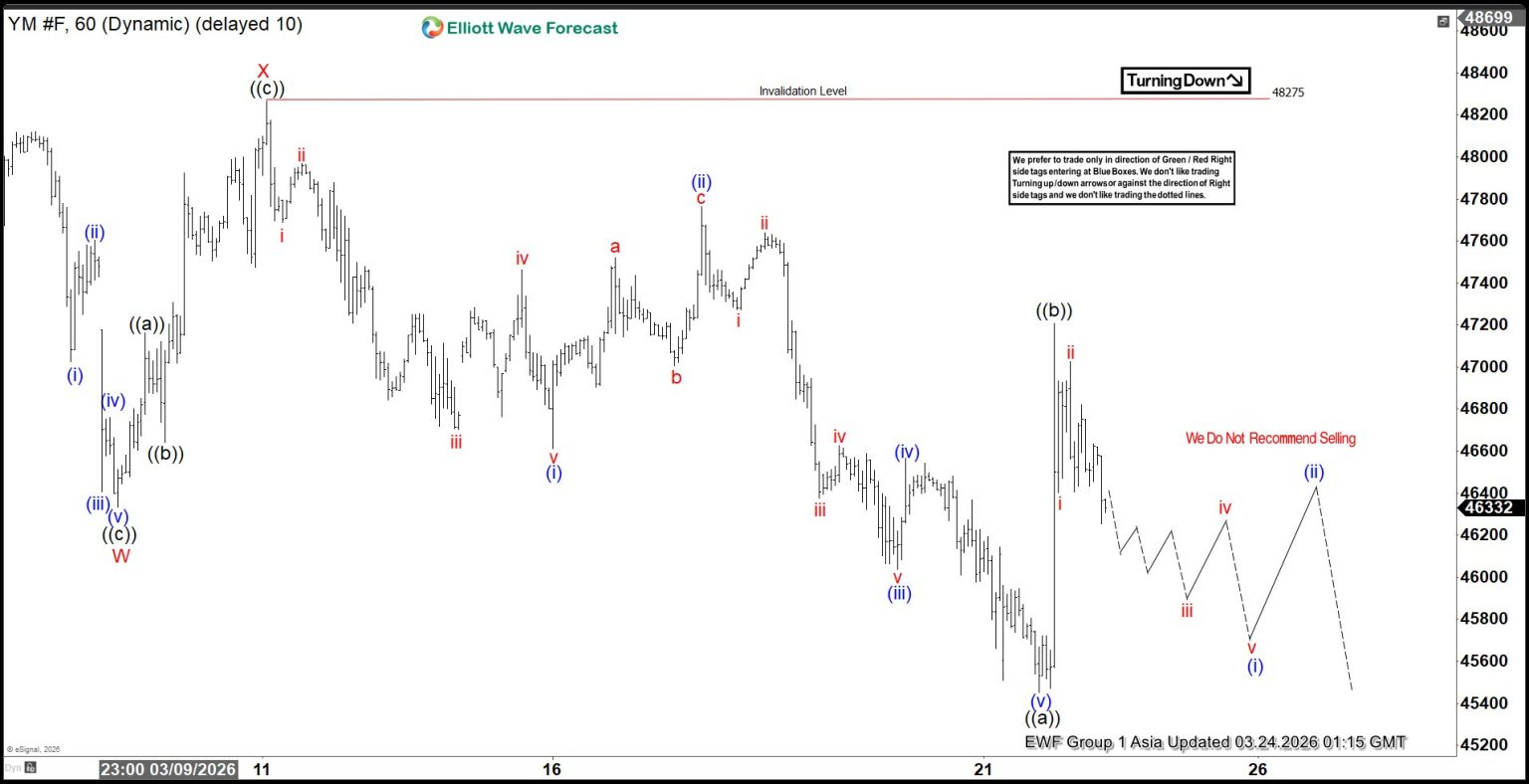

Dow Futures (YM) is correcting the larger degree cycle that began from the April 2025 low. The current decline is unfolding as a double three Elliott Wave structure, which highlights a complex corrective phase rather than a simple retracement. From the all-time high on February 10, 2026 at 50,611, wave W finished at 46,333, while the subsequent rally in wave X reached 48,275, as shown in the one-hour chart. The ongoing wave Y is progressing with internal subdivision that takes the form of a zigzag, consistent with the broader corrective framework.

From the peak of wave X, wave ((a)) dropped to 45,453, followed by wave ((b)) which appears complete at 47,210. In the near term, as long as rallies remain capped below 47,210 and more importantly below 48,275, the expectation is for the Index to continue extending lower. This outlook aligns with Fibonacci extension measurements taken from the February 10, 2026 high. The projected downside target falls within the 100% to 161.8% extension range, corresponding to 41,268 – 43,925. This zone is significant because it represents an area where buyers may emerge, potentially supporting renewed upside momentum once the corrective sequence has matured. The structure therefore suggests that while short-term weakness dominates, the broader cycle retains the potential for recovery once the corrective objectives are satisfied

Dow Futures (YM) 60-Minute Elliott Wave Chart

YM Elliott Wave Video:

https://www.youtube.com/watch?v=54zEkss3ksY

Chart Alert: Dow Jones (DJIA), TACO Trade May Not Work, Watch 46,710 Resistance

Key takeaways

- Downtrend confirmed, TACO rally likely a trap: Dow Jones Industrial Average has broken below its 200-day moving average and fallen ~10% from its peak, with the recent “TACO” (Trump Always Chickens Out) rebound likely a dead cat bounce rather than a sustainable reversal.

- Macro risks not fully priced by equities: The VIX/MOVE ratio signals that bond volatility is dominating, implying interest rate and stagflation risks remain underpriced in equities, leaving room for further downside.

- Key levels define next move: Immediate resistance sits at 46,710, while a break below 45,190 exposes further downside toward 44,975 and 44,505; failure to reclaim resistance keeps the bearish bias intact.

The price actions of the US Wall Street 30 CFD index (a proxy of the Dow Jones Industrial Average (DJIA) have tumbled as expected and broken below the key 200-day moving average on Wednesday, 18 March 2026.

On Monday, 23 March 2026, the US Wall Street 30 CFD index extended its bearish move to print an intraday low of 45,213 seen during the London session. All in all, it has plummeted by 10% from its current all-time high printed on 10 February 2026 to Monday’s 23 March 2026 low, reinforced by a flattening of the US Treasury yield curve triggered by rising stagflation risk due to global oil supply shock arising from the US-Iran war.

Risk-on behaviour roared back on Monday, 23 March 2026, after US President Trump sent a social media message that planned strikes against Iran’s energy infrastructure will be paused for five days as both sides are engaged in a renewed negotiation process, despite Iran's repeated assertion that no direct negotiations have been held with the US.

The TACO regime, the popular acronym, “Trump Always Chickens Out,” has its footprints in the global financial markets yesterday, where market participants remembered the ex-post “Liberation Day” events in late April 2025, where Trump walked back on his aggressive tariffs and paused the US’s trade war 2.0 with China, inducing a V-shaped recovery in global stock markets.

Last year’s April “Liberation Day” TACO regime was a reaction to a sell-off in risk assets caused by “words” rather than actions, which are military strikes on stakeholders’ physical infrastructure in the current context, in turn, are likely to have lasting economic damages that cannot be easily reversed by a change of rhetoric from Trump.

Hence, Monday’s TACO-induced rally in risk assets is likely a fake head, also known as a dead cat bounce.

Intermarket analysis and technical analysis suggest that the medium-term V-shaped rally for the US stock market and global equities in general remains elusive now.

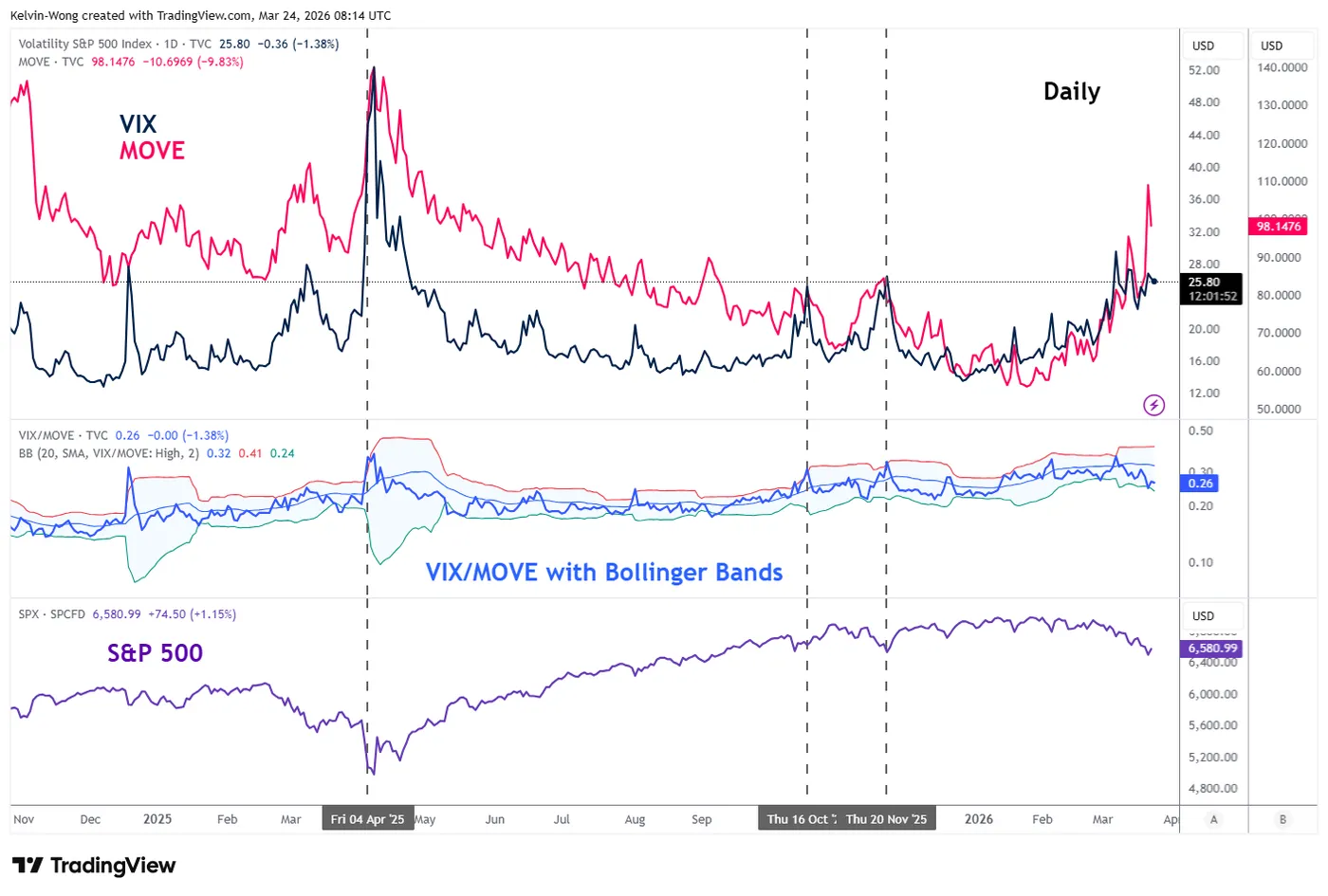

The VIX/MOVE ratio has not reached an extreme level on the upside

Fig. 1: VIX/MOVE ratio with S&P 500 medium-term trend as of 24 Mar 2026 (Source: TradingView)

The CBOE Volatility Index (VIX) is the implied volatility of the S&P 500, a gauge for US equities. On the other hand, the ICE BofA MOVE Index (MOVE) measures the implied volatility of US Treasuries.

Based on the latest price action of the VIX/MOVE ratio as of Tuesday, 24 March 2026, at the time of writing, it is trading below its 20-day moving average with a series of “lower highs and lower lows,” which suggests bond (US Treasuries) volatility is dominating, which implies interest rates uncertainty is the core driver at this juncture, and equity volatility is likely not fully pricing in such macro risk yet (may lead to more potential downside for US stock indices) (see Fig. 1).

Also, the VIX/MOVE ratio has not crossed above its daily Bollinger Bands’ upper limit, where such movements in the past led to or coincided with significant bullish reversals in the S&P 500 on 20 November 2025, 16 October 2025, and 8 April 2025 (see Fig. 1).

Let's now decipher the short-term trajectory (1 to 3 days) of the US Wall Street 30 CFD index and its supporting elements from a technical analysis perspective

Dow Jones (DJIA) – Bearish reaction at 200-day moving average

Fig. 2: US Wall Street 30 CFD index minor trend as of 24 Mar 2026 (Source: TradingView)

Watch the 46,710 key short-term pivotal resistance, and a break below 45,237/190 may expose the next intermediate supports at 44,975/810 and 44,505 (see Fig. 2).

On the other hand, a clearance above 46,710 invalidates the bearish reversal scenario for an extension of the mean reversion rebound towards the next intermediate resistances at 47,338 and 47,923.

Key elements to support the bearish bias on Dow Jones (DJIA)

- Yesterday’s rally stalled at the 200-day moving average and the upper boundary of the descending channel from the 26 February 2026 high.

- The hourly MACD trend indicator staged a bearish reaction at its horizontal resistance level.

XTI/USD Analysis: WTI Oil Prices Under Pressure from Trump’s Statements

Yesterday, following a false bullish breakout above the psychological $100 level, WTI crude prices fell sharply towards the $85 area. The primary driver of this rapid decline was comments made by the US President.

According to Donald Trump:

- → the United States has postponed planned strikes on Iranian energy infrastructure for five days;

- → productive negotiations are ongoing.

However, Iran later denied these claims, stating that no negotiations to end the conflict were taking place. Moreover, Israel continued its strikes on Iran, while Tehran launched fresh attacks on US assets in the Middle East.

Against this backdrop, the US President’s remarks appear to be a form of verbal intervention aimed at pushing oil prices lower — and, as the XTI/USD chart shows, it is having an effect. Today, WTI crude is trading below last week’s lows.

Technical Analysis of XTI/USD

When analysing WTI price movements on 16 March, we highlighted:

- → strong selling pressure near the psychological $100 level;

- → a support zone that formed after the breakout from a local descending channel.

This support area significantly slowed yesterday’s decline in oil prices. At the same time, recent price action allows for the construction of a broad ascending channel, with its lower boundary acting as an important support level.

From a bearish perspective:

- → the $91.50 level, which acted as support last week, has now turned into resistance;

- → if bulls attempt to develop a rebound from the lower boundary, a key test of their strength will be the $95 level, where bears previously pushed prices below the channel median.

In the near term, a period of consolidation between the lower boundary of the channel and the $91.50 level cannot be ruled out, at least until stronger news catalysts emerge, particularly those related to developments around the Strait of Hormuz.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

BoJ’s Ueda: Inflation to rise moderately, food tax cut impact limited

BoJ Governor Kazuo Ueda said underlying inflation in Japan is expected to "accelerate moderately", supported by a tight labor market and evolving corporate pricing behavior. He emphasized that firms are becoming more active in wage and price setting, sustaining a cycle in which wages and prices rise in tandem despite near-term distortions.

Ueda acknowledged that government measures to curb energy costs are currently weighing on headline inflation. However, he stressed that the underlying dynamics remain intact, with labor shortages and stronger wage growth continuing to support inflation over the medium term.

On fiscal policy, Ueda downplayed the long-term impact of a proposed suspension of Japan’s food consumption tax. While the plan could temporarily lower prices, he argued that "rational consumers" would look beyond short-term measures, meaning the effect on medium- and long-term inflation expectations would be limited.

What a Difference One Tweet Makes

Markets

What a difference one tweet makes. US President Trump claimed he had very good and productive talks with Iran and ordered a five-day pause in military strikes. Iranian officials shortly afterwards denied any such talks having happened but did confirm mediation efforts were under way by other countries including Pakistan and Turkey. It’s impossible for an outsider to know how much is true, especially considering Trump’s war tactics from the recent past. The news hitting the wires contains mixed signals as well, to say the least. Thousands of US Marines are to arrive in the Middle East on Friday, which is now considered the new deadline for the Strait of Hormuz to reopen. Meanwhile Saudi Arabia and the UAE reportedly are inching towards joining the US in the fight against Iran. It could be leverage to push Iran quicker into a deal or the prelude of another escalation in the war. Either way, we’re not seeing the likes of Brent crashing further today. Oil prices, which curiously saw major volumes shortly before Trump’s announcement, dropped yesterday from as high as $114 to an intraday low of $96 before closing around the triple digit mark. It is recovering somewhat currently towards $103. Trump’s tweet also triggered a relief rally in core bonds, with both rate hike bets and inflation concerns easing somewhat. Net daily changes amounted to up to 10 bps at the front in Germany and half that in the US. UK gilts outperformed by tanking 15 bps. We remains cautious about the extent of the recovery. Regardless of any potential short-term truce/peace deal, there are still longer-term consequences tied to the weeks long closure of the Strait, in fertilizers and as a result in food to name just one. Rising food prices have an outsized influence on inflation expectations and may still warrant rate hikes even as the geopolitical situation has improved (which is still highly uncertain, to be sure). ECB vice-president to be Vujcic said they are vigilant for second-round effects (governing council member Radev already sees some indications of that) and warned that the economy and inflation is already departing from the baseline scenario towards worst-case scenarios. Gold prices, enjoying the yield détente, rebounded exactly on the 200dMA around $4100, paring an intraday drop of 10% to just 3%. Stocks shot up sharply with the EuroStoxx50 closing 1.3% higher and similar gains for the main WS indices. The US dollar retreated in the same risk on vein. EUR/USD crawled back north of 1.16. DXY and USD/JPY fell back below 99 and to 158.4 respectively. None of yesterday’s moves are extended in Asian dealings though, (rightly, in our view) highlighting a sense of market hesitancy to go all-in on Trump’s comments. March PMI’s today lose their usual significance for trading because of the developing geopolitical situation. That’s going to be the case for most economic releases for some time to come unfortunately.

News & Views

Japanese headline inflation in Japan declined more than expected in February to 1.3% Y/Y from 1.5%. The closely watched series ex fresh food eased from 2% to 1.6% Y/Y, the lowest level March 2022 and also the first time since that reference than it fell below 2%. The underlying measure ex food and energy price still held well above the 2% reference easing only slightly from 2.6% to 2.5%. However, the decline in headline inflation was mainly due to a lower prices for regulated energy prices with utility prices easing 8.1% M/M and 5.5% Y/Y. Food price inflation printed at -0.4% M/M and 4.0% Y/Y (from 3.9%). With both the underlying inflation holding above expectations and higher energy prices at risk of pushing prices higher (including the measure ex-fresh food) coming months, the case for further BOJ policy normalization/rate hikes remains in place. Markets currently see a change of about 60% of a BoJ rate hike at the next policy meeting on April 28.

Australia and the European this morning signed a trade deal that has been negotiated for about 10 years. In essence the deal removes most tariffs for European goods as is the case for nearly all exports of Austrian critical minerals. However, the agreement still sets quotas on some Australian food products, which is drawing criticism from the local agricultural sector. The agreement comes as both parties accelerated negotiations as they were confronted with the US raising tariffs on imports while China was seen as taking a too dominant position in the supply of critical minerals. At the same time, the two parties also singed a Security and Defense partnership to address global security challenges.

Theatre of the Absurd

I don’t have time to finish a sentence before new headlines send markets upside down.

When I returned to my desk on Monday, Trump had given Iran a 48-hour ultimatum — with only a few hours left before it expired. After that, he said he would “obliterate” the nation’s power plants. Oil was up and the market selloff was deep.

By the time I posted my morning note and grabbed a coffee, Trump had made a major U-turn, saying he would give Iran five days of ceasefire following “very good and productive conversations regarding a complete and total resolution of our hostilities in the Middle East” — his words on Truth Social.

US crude tanked 10%, Brent fell nearly 9%, yields dropped, and equity markets rebounded sharply — as if the war were over and we could return to peace. Remember peace? It’s been a while.

Fun fact: Iranian officials said there had been no direct or indirect contact with Trump. (sad trombone).

So yes, Donald Trump ‘Chickens Out’—because the Iranian bite was probably too big to be swallowed, but him ‘chickening out’ won’t calm the game if Iranians don’t comply.

Therefore TACO optimism could hardly last. The idea that Trump can act alone and shape outcomes doesn’t hold if the counterparty refuses to engage. Any resolution in the Middle East is also contingent on Iran’s willingness to de-escalate.

The Strait of Hormuz remains effectively constrained, with only a limited number of tankers crossing the critical waterway, and oil is rebounding this morning — both Brent and WTI are up more than 3% at the time of writing. Equities are under pressure again, with Asian indices giving back earlier gains.

Trump’s five-day ceasefire is set to end toward the end of the trading week — no surprise. What happens next is anyone’s guess.

But yesterday’s price action suggests that investors are more afraid of missing a post-war rally — similar to the post-“Liberation Day” rebound — than of getting a few entries wrong. They continue to look for any hint of optimism.

Meanwhile, policymakers are watching through a more critical lens. European Central Bank (ECB) officials warn that the current energy shock could turn into stagflation if prices remain high and volatile.

In Japan, recent data showed inflation easing to near a four-year low, but the country’s largest labour group secured average pay rises above 5% for a third consecutive year — well above inflation — complicating efforts to stabilise price dynamics, especially alongside rising energy costs. The USD/JPY eased to 158 yesterday amid a broadly stronger US dollar following Trump’s unverified Iran announcement. The pair is rising again this morning, as the dollar rebounds more broadly on the realisation that Trump cannot unilaterally ease geopolitical tensions.

Market sentiment is fully dependent on war headlines and energy prices. Reactions are highly emotional: investors want the war to end, the latest selloff to be “the dip,” and to catch that dip. But uncertainty remains, and the TACO trade is only sustainable if Iran plays along.

So we wait — watching both headlines and data.

Today, we will get a first glimpse of how global economic sectors are reacting to rising energy prices and escalating tensions in the Middle East. Preliminary March PMI expectations mostly point lower, reflecting weaker demand and rising anxiety over a potential new energy shock and tighter monetary conditions.

- In Australia, both manufacturing and services PMI declined, with services slipping into contraction below 50 and manufacturing hovering near the threshold. Recall that the Reserve Bank of Australia (RBA) raised rates for the second time in a row at last week’s meeting.

- Japanese PMI figures also weakened, pointing to slower expansion in both services and manufacturing. The Bank of Japan (BoJ) remains on a gradual normalization path to keep inflation pressures in check.

- European PMI figures are expected to tell a similar story: softer activity amid higher energy costs and tighter financial conditions.

But softer-than-expected PMI data is unlikely to reverse the recent hawkish shift in central bank expectations. On the contrary, slowing growth combined with rising inflation pressures will fuel stagflation concerns and could weigh further on sentiment. In this environment, good news will be good news — and bad news will be bad news.

Looking ahead, even if the war were to stop today, repairing damage to Middle Eastern energy infrastructure would take time. Estimates suggest it could take months — even years — to fully restore output to pre-war levels.

As such, an energy-driven market shock would be harder to dismiss than a Trump-driven trade crisis — the backdrop against which the TACO acronym emerged. In that episode, Trump acted unilaterally, counterparts had limited leverage beyond negotiation, and eventual tariff rollbacks provided relief. The situation with Iran is fundamentally different.

That said, this remains a cautious view. Nothing prevents investors from buying like there is no tomorrow on any sign of optimism, overlooking risks, stretched valuations and margin pressures from rising energy costs.

TACO Questioned Amid Middle East De-escalation Efforts

In focus today

In the euro area, the March flash PMIs are released, which is the first growth indicator following the war in Iran. The manufacturing sector is expected to record a large decline to 49.6 from 50.8 as higher energy costs have likely lowered some production in March. The services sector is less directly affected by the energy increases in the short term, so we expect a smaller decline here to 51.1 from 51.9, thereby keeping the sector in growth territory.

From the US and UK, we also get flash March PMIs, which will shed further light on how rising oil prices are affecting global economic activity. Both countries are expected to report declines but remain in growth territory. Recent PMI data from the UK pointed to stronger economic momentum in Q1, while US data showed manufacturing slowing amid weaker output, prices and new orders.

In Hungary, the central bank is set to announce its Base Rate decision. We expect the rate to hold steady at 6.25%, aligning with consensus expectations.

Economic and market news

What happened overnight

In Japan, data has come in on the soft side, with composite PMI at 52.5 down from 53.9, driven by both manufacturing and service. CPI inflation, excluding fresh food, declined to 1.6% in February from 2.0%, marking the first time below the inflation target in four years. Fuel subsidies is a key driver, and the reality has changed a lot since February as PMIs reveal a marked increase in firms' input prices and the yen remains under pressure. We expect the next BoJ hike in April. Markets are pricing close to 50-50 for that.

In EU-Australia relations, a significant trade agreement has been finalised. The deal eliminates tariffs on nearly all European goods and Australian critical minerals, while introducing quotas for certain Australian agricultural exports such as beef and sheep meat. The removal of import tariffs on Australian critical minerals into the EU is expected to support the stabilisation of global supply chains.

What happened yesterday

The Middle East conflict triggered a shift in markets yesterday as the US announced a five-day pause in attacks on Iranian energy infrastructure amid reports of ongoing talks to end the conflict. Iran dismissed the claims as "fake news" but confirmed efforts to de-escalate tensions, while reports suggest direct negotiations may occur in Islamabad this week. Israel confirmed discussions to secure a deal addressing the war's objectives and "protecting vital interests," while a European official noted Egypt, Pakistan, and Gulf states are relaying messages between the US and Iran.

Markets saw relief from Trump's announcement, briefly sending Brent crude below USD 100/bbl, though prices remain elevated compared to pre-war levels. While easing tensions could drive prices lower, risks of a rebound persist as WSJ reports Saudi Arabia and the UAE are pushing US to continue to fight and are mulling joining the war.

In the US, Fed Governor Miran (voter) emphasised the need to wait for more data before adjusting the policy outlook. He maintained his stance on gradual interest rate cuts, revising his forecast from six to four cuts this year while raising his inflation outlook. This morning, we adjusted our Fed call slightly and now call for the final two rate cuts only in September and December this year (prev. June and September). Read more in Reading the Markets USD - War delays rate cuts, 24 March.

In the euro area, consumer confidence fell more than expected to -16.3 in March (cons: -14.2, prior: -12.2). Consumer confidence thus reached the lowest level since October 2023. Consumers are likely to be more cautious with spending due to the decline in confidence, which highlights the negative growth consequences of the war in Iran. The survey period is "generally the first two to three weeks of the month" according to Eurostat, so the effect of the war is captured, but as energy prices have continued to rise during the month the full effect is likely not captured yet.

Equities: Equities rebounded in a rare manner following a post from the US president that negotiations have been initiated and a five-day long halt to attacks will follow. European equities that were down south of -2.5% on Monday, rebounded 4.5% from low to high. The gains later faded, as Iranian officials denied that negotiations have been held. Nonetheless, equities closed higher with S&P 500 up 1.2%, small cap Russell 2000 up 2.3% and Stoxx 600 0.6%. Futures have however dipped back into negative this morning.

The sector preference was mostly reversal of geopolitical trades. Cyclicals led the gains, and primarily growth cyclicals as yields dropped, including tech and consumer discretionary in the lead. What is just as interesting is to see which sectors that did not rebound on the news. The real estate sector, one of the worst performers the last week, did not benefit from the drop in yields, but continued to underperform. Similarily, consumer staples that, believe it or now, have sold off more than industrials over the last month did not rebound either. To us, this is a sign that investors priced out some of the recession risk yesterday through the cyclicals, but that inflation and rate hike expectations are little changed. This can serve as a guide on what a TACO trade would like ahead.

FI and FX: It was quite the rollercoaster ride for market yesterday. From a tense opening, where oil prices were on the rise pushing the USD and yields higher to a sudden relief rally after US postponed attacks on Iranian energy installations citing productive talks to renewed rise in tensions as WSJ reports Saudi Arabia and UAE are pushing for the fight to continue. What was most striking yesterday was the development in EUR/NOK. The pair moved sharply higher in the morning - a move that did not reverse in the relief rally. The correlation to moves in energy prices has turned as risk assets have started to price a growing risk of recession should central banks tighten monetary policy on top of the energy supply shock.

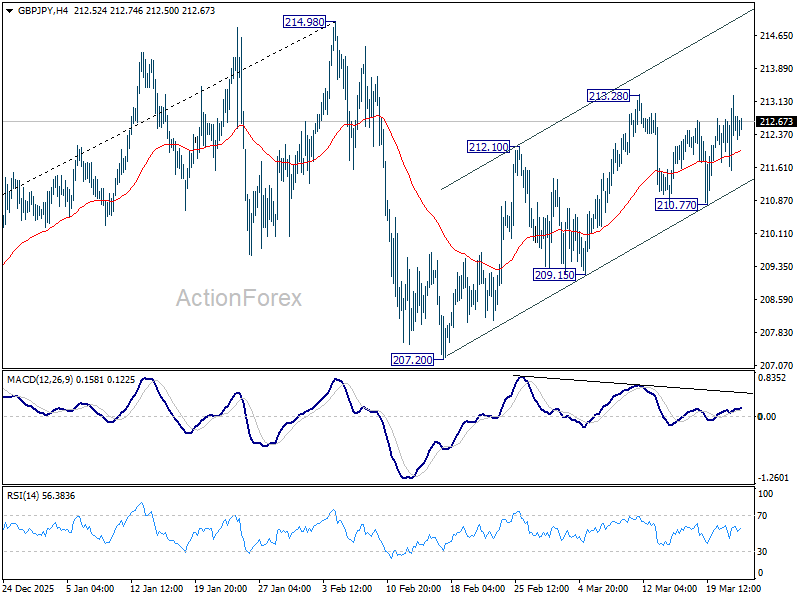

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.78; (P) 212.55; (R1) 213.50; More...

Intraday bias in GBP/JPY stays mildly on the upside. On the upside, Firm break of 213.28 resistance will resume the rally from 207.20 and target a retest on 214.98 high. For now, risk will stay mildly on the upside as long as 210.77 support holds, in case of retreat.

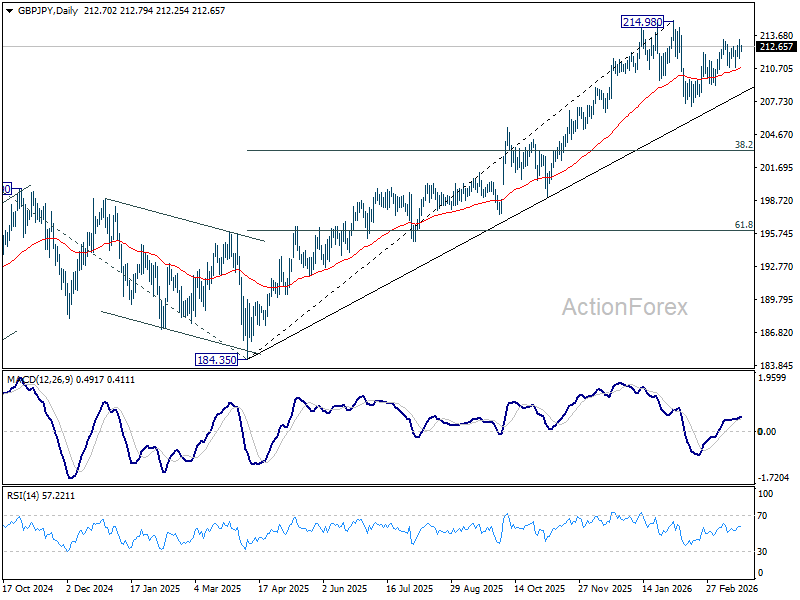

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

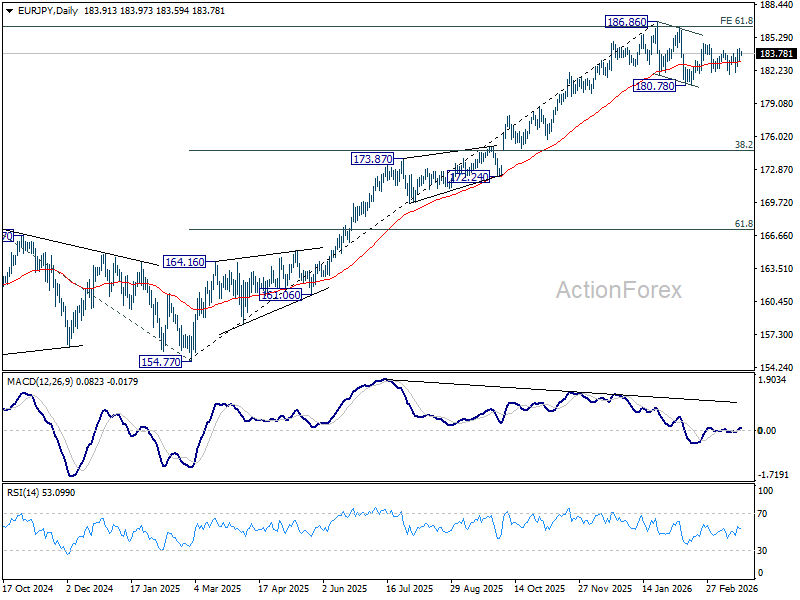

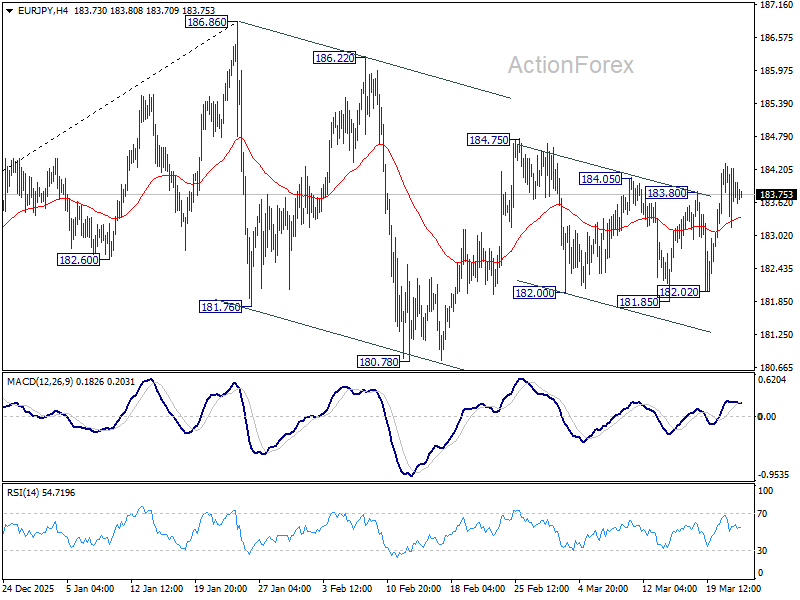

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.35; (P) 183.85; (R1) 184.51; More...

Intraday bias in EUR/JPY remains mildly on the upside for 184.75 resistance. Firm break there will resume the whole rise from 180.78 and target a retest on 186.86 high. For now, risk will stay mildly on the upside a long as 182.02 support holds, in case of retreat.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.61) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.