Sample Category Title

GBP/JPY Weekly Outlook

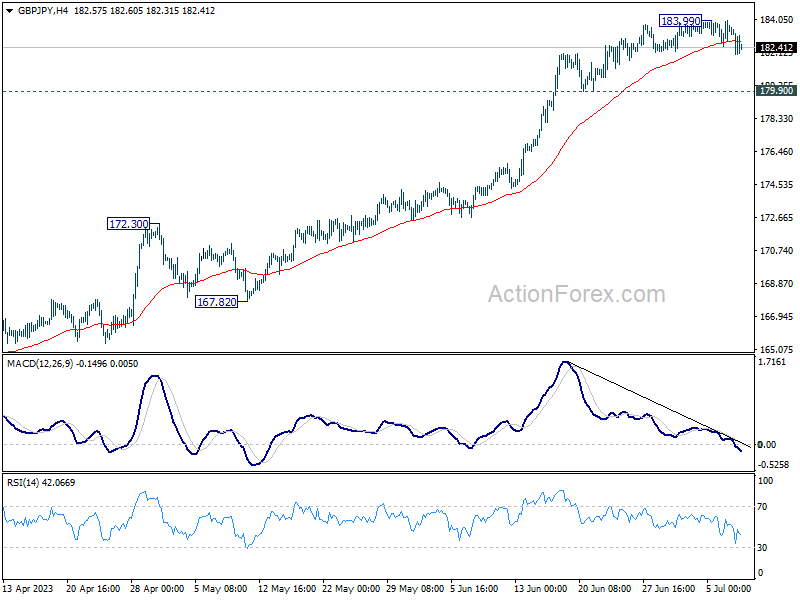

A short term top is likely in place at 183.99 in GBP/JPY, on bearish divergence condition in 4H MACD. Initial bias is mildly on the downside this week for 179.90 support. Firm break there will target 55 D EMA (now at 175.99 ). On the upside, break of 183.99 will resume larger up trend.

In the bigger picture, as long as 172.11 resistance turned support holds, uptrend from 123.94 (2020 low) is expected to continue. On resumption, next target is 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

In the longer term picture, rise from 122.75 (2016 low) in still in progress to retest 195.86 (2015 high). Based on current momentum, break of 195.86 is in favor. But strong resistance could still be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 (2011 low) at 199.80 to limit upside on first attempt.

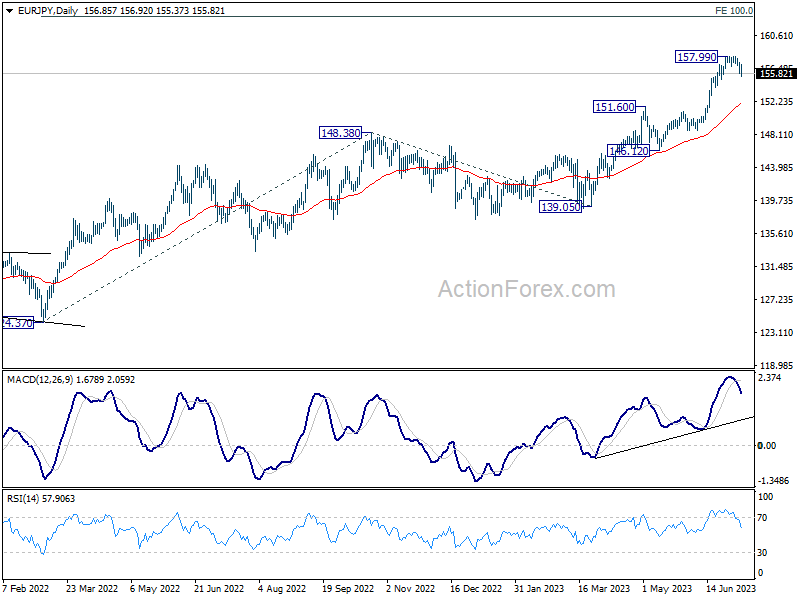

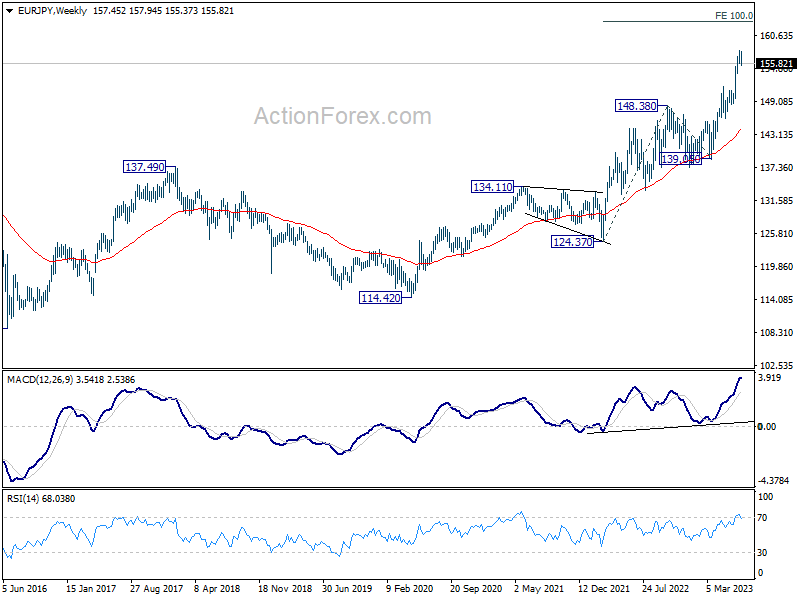

EUR/JPY Weekly Outlook

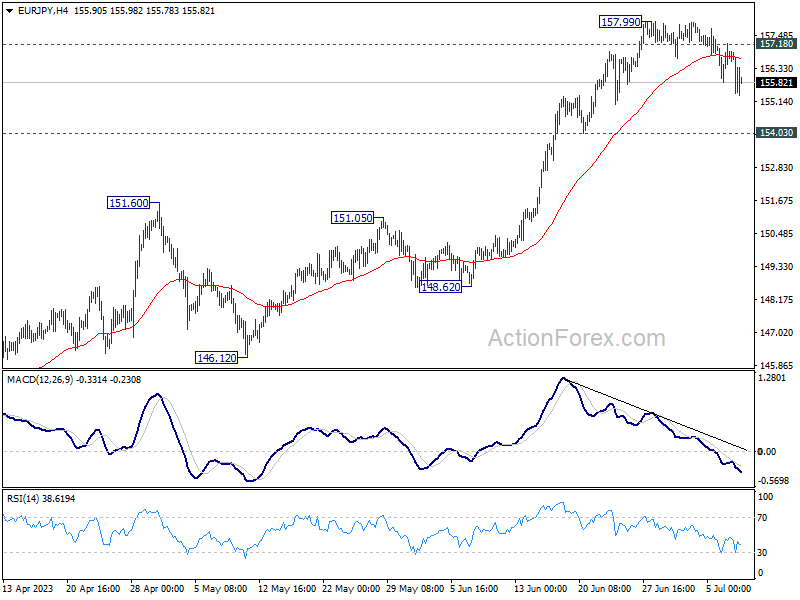

EUR/JPY's decline last week should confirm short term topping at 157.99, on bearish divergence condition in 4H MACD. Initial bias remains on the downside for deeper correction to 154.03 support or below. But overall outlook will stay bullish as long as 151.60 resistance turned support holds. Larger rally is still expected to resume through 157.99 after the correction completes. On the upside, above 157.18 minor resistance will bring retest of 157.99 high first.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway.

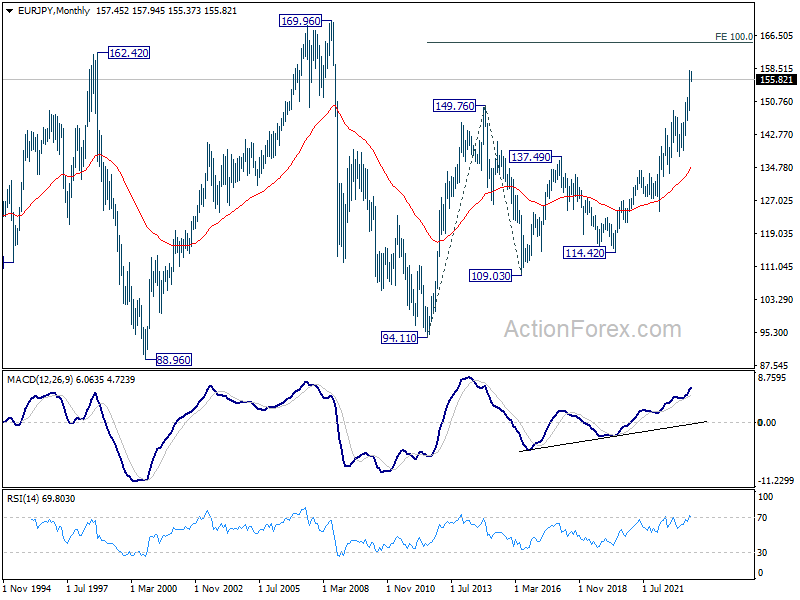

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

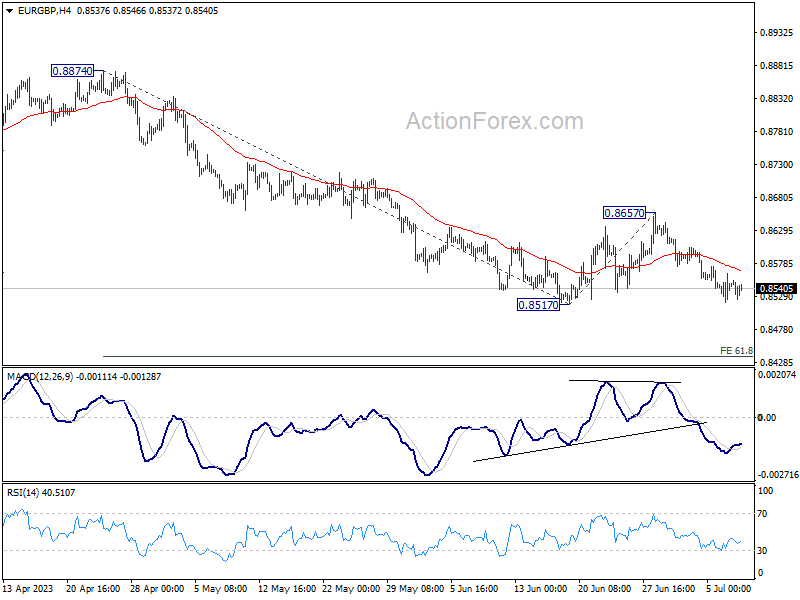

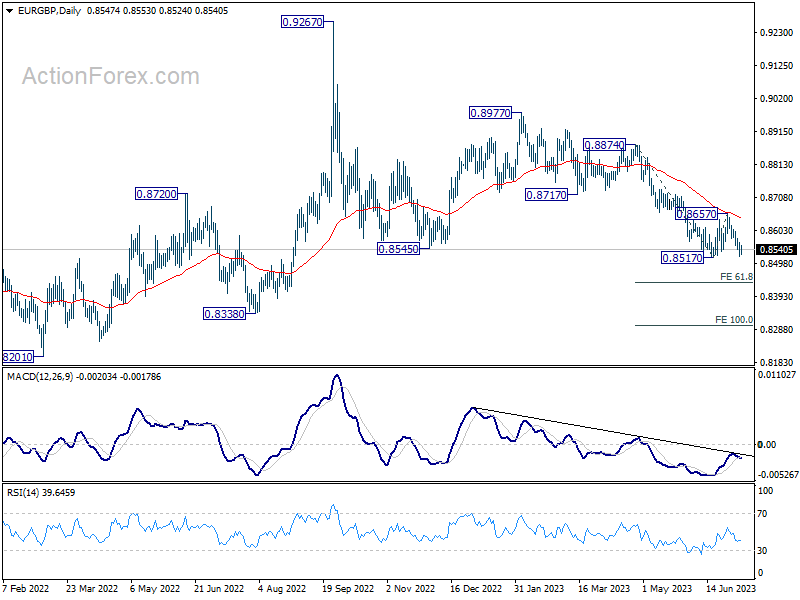

EUR/GBP Weekly Outlook

EUR/GBP's decline from 0.8657 extended lower last week but failed to break through 0.8517 low. Initial bias remains neutral this week first, and outlook stays bearish too. On the downside, firm break of 0.8517 will resume the whole decline from 0.8977. Next target will be 61.8% projection of 0.8874 to 0.8517 from 0.8650 at 0.8436. On the upside, above 0.8657 resistance will turn bias to the upside for stronger rebound instead.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

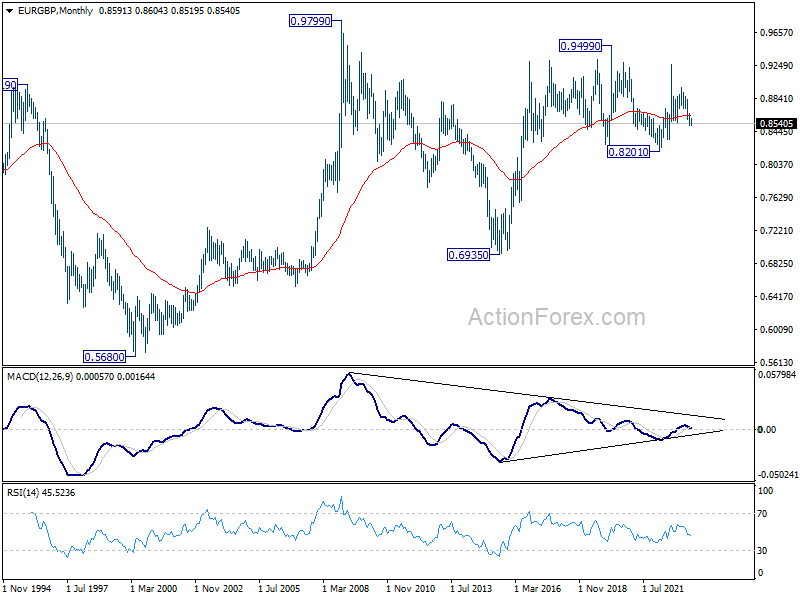

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

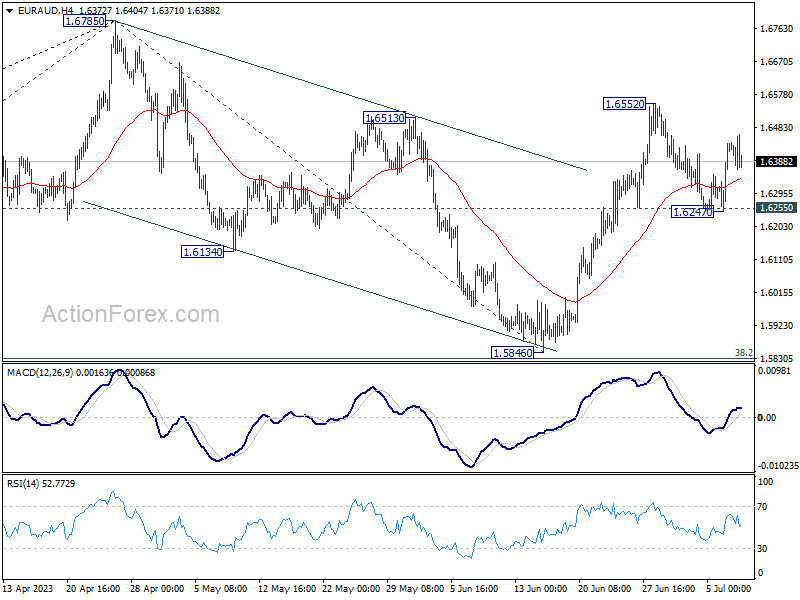

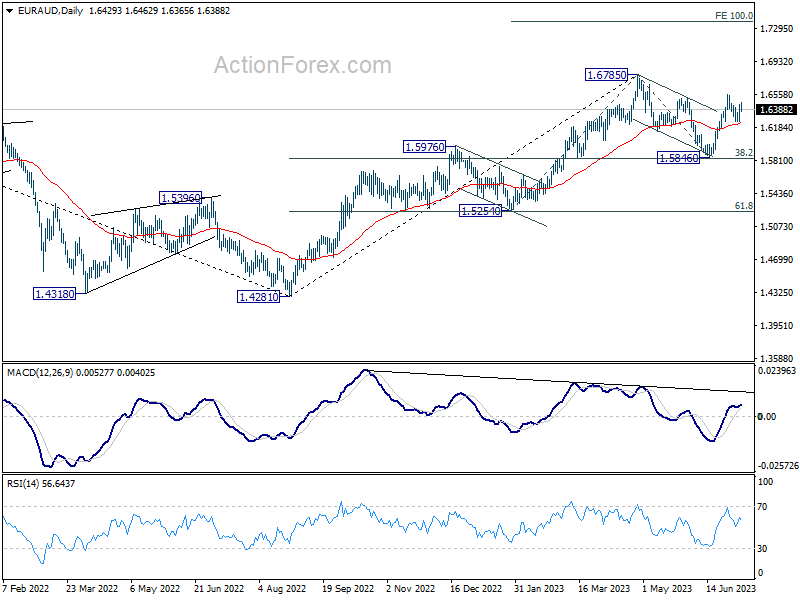

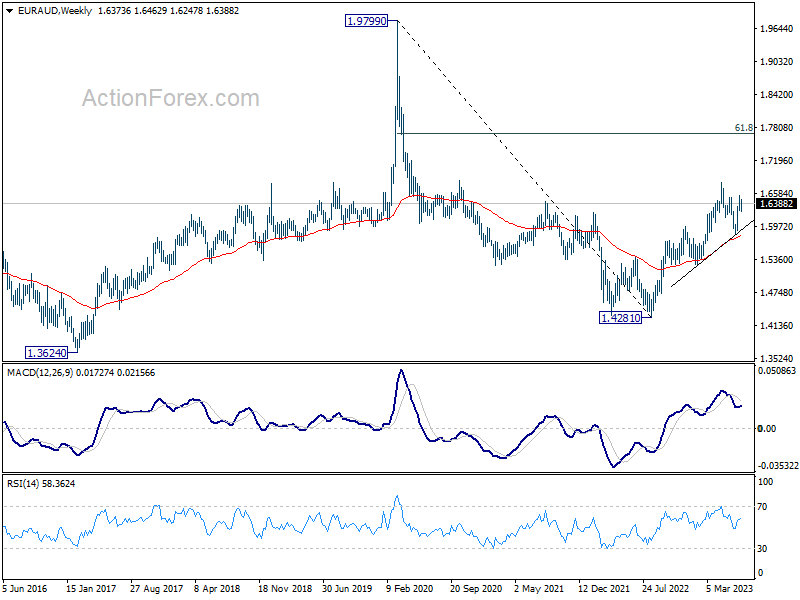

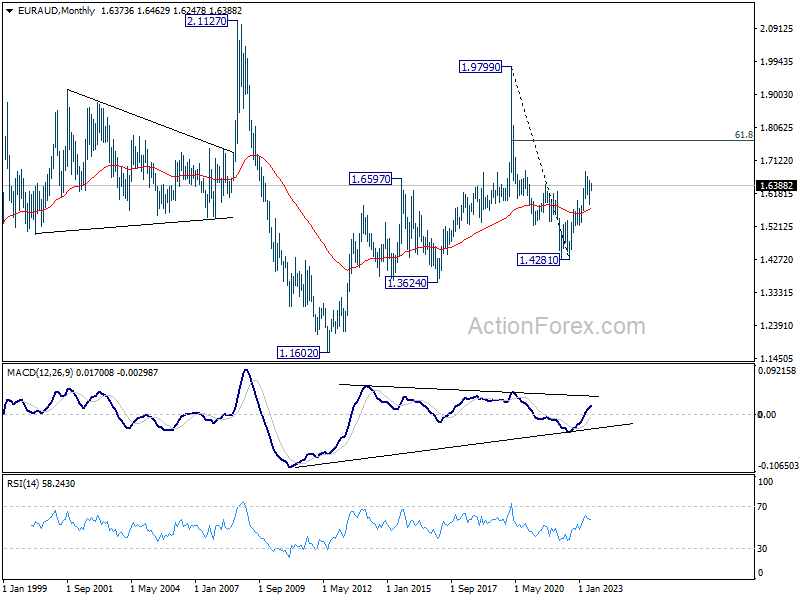

EUR/AUD Weekly Outlook

EUR/AUD dipped to 1.6247 last week but quickly rebounded after drawing support from 1.6255. Outlook is unchanged and initial bias stays neutral this week first. Further rally remains in favor. As noted before, correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, firm break of 1.6255 will dampen this view and turn bias to the downside for 1.5846 support.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

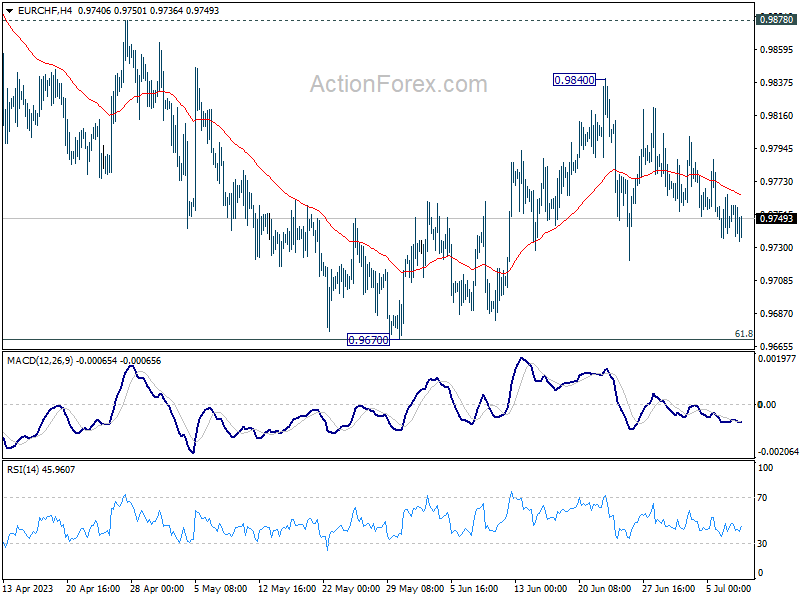

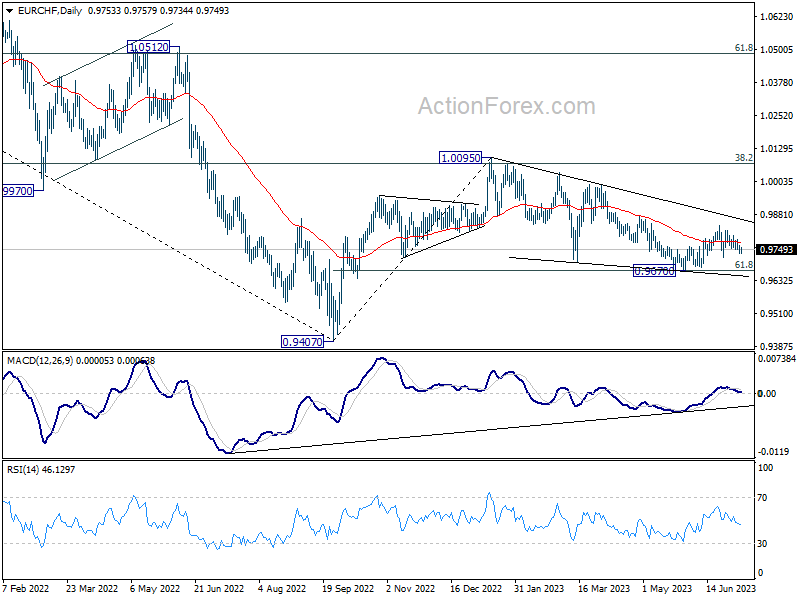

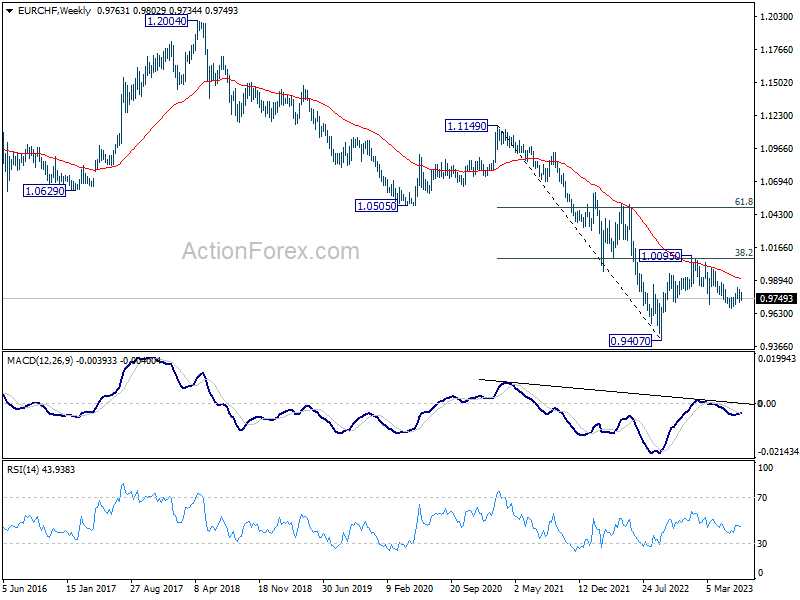

EUR/CHF Weekly Outlook

EUR/CHF continued to gyrate in established range last and outlook is unchanged. Initial bias stays neutral this week first. On the upside break of 0.9840 will resume the rebound from 0.9670. That will also revive the case that whole corrective decline from 1.0095 has completed at 0.9670. Further rally should be seen to 0.9878 resistance next. However, sustained trading below 0.9670 will resume the whole fall from 1.0095.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0459) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Weekly Economic & Financial Commentary: Light Still Green for the Fed to Hike Despite Soft Jobs Report

Summary

United States: Light Still Green for the Fed to Hike Despite Soft Jobs Report

- June hiring data came in short of expectations and signal the recent trend in hiring is clearly lower. But continued economic resilience and generally robust incoming data still give the Fed the green light to resume monetary policy tightening on July 26.

- Next week: CPI (Wed.), Consumer Sentiment (Fri.)

International: Encouraging Economic Signals from Japan

- The Bank of Japan's Tankan Survey offered an early indication that Japan's recovery continued, and perhaps even gathered momentum, during the second quarter. The results suggest some upside risk to our 2023 GDP growth forecast of 1.2% and are also a factor that could eventually see a hawkish Bank of Japan policy shift later this year.

- Next week: Reserve Bank of New Zealand Policy Rate (Wed.), Bank of Canada Policy Rate (Wed.), U.K. Monthly GDP (Thu.)

Interest Rate Watch: Is It a Dud? Better Be Sure Before You Walk Up to It

- Happy 247th anniversary to the United States and happy one-year anniversary to the inverted yield curve. In this week's Interest Rate Watch, we mark the occasion and note that the spread between 10-year and 2-year Treasuries reached its largest gap in 40+ years. How long is it safe to turn a blind eye on the inverted curve?

Credit Market Insights: Main Street Lending Conditions Tighten in First Quarter

- Last Friday, the Federal Reserve Bank of Kansas City released its Q1 Small Business Lending Survey (SBLS). The survey provides the first snapshot of lending activity and terms for small businesses, a critical component of the nation’s economy, since the banking turmoil in Q1.

Topic of the Week: Digging Deeper into the Surge in Manufacturing Construction Spending

- Manufacturing construction continues to boom, per the latest construction spending data covering the month of May reported this week. The upsurge in new manufacturing projects has been a boon for several regions and largely reflects the build-out of electric vehicle supply chains and semiconductor manufacturing facilities.

The Weekly Bottom Line: Job Market Cooling, But Not Enough

U.S. Highlights

- The week’s economic data was consistent with an economy that remains resilient, if no longer as robust as it was.

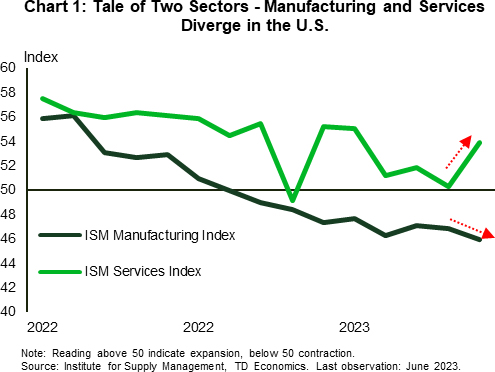

- Performance in the manufacturing and services sectors continued to diverge. The June ISM index showed manufacturing contracted for the eighth consecutive month, while services continued to expand six months in a row.

- The overall resilience will likely keep the Fed in hiking mode later this month, as the job market remains tight and wage growth stronger than the Fed would like. The FOMC minutes revealed that a few members favored a hiked at the June meeting, even if they did not formally dissent on the decision.

Canadian Highlights

- Canada’s job market sizzled in June, with job gains beating expectations by a factor of three. Odds are the Bank of Canada raises rates a quarter point next week to further slow demand in an overheated economy.

- A more positive development for inflation is that average hourly earnings increased at the slowest pace since May 2022. Wage growth remains a major issue at the port strike in B.C., which could affect the economy through merchandise trade.

- Statistics Canada’s report on distributions of household economic accounts suggests that the least wealthy are being affected more by the high interest rates and pressures coming from rising prices.

U.S. – Job Market Cooling, But Not Enough

The week that was showcased a U.S. economy that while cooling, is still too resilient to achieve the Fed’s aim. First up, the ISM Manufacturing and Services Indexes showed that the goods sector continued to slow, while the service sector continued to expand, albeit at a modest pace. The manufacturing index declined again in June, falling 0.9 points to a 3-year low of 46.0. This marks its eighth consecutive month in contraction territory and points to deteriorating conditions in the manufacturing sector. The index suggests that demand remains weak in the sector, with new orders still below the 50 mark. Manufacturers have responded by cutting both production and employment (with both sub-indexes coming in below 50). The survey result is consistent with data on consumption expenditure, which showed real spending flat in May and expenditure on goods pulling back by 0.4% on the month.

While a cool down on the goods side will be welcomed by the Fed, the real sticking point is still strong demand on the services side of the economy. The ISM services index remained in expansion territory for the sixth consecutive month in June, highlighting the divergence between the two indexes (Chart 1). While expanding, the services index is still off recent highs, and is consistent with a modest pace of growth in the broader economy. One factor likely to impede growth however is the looming resumption of student loan debt repayments, which combined with a softening labour market and rising interest rates, could reduce consumer spending and growth even further.

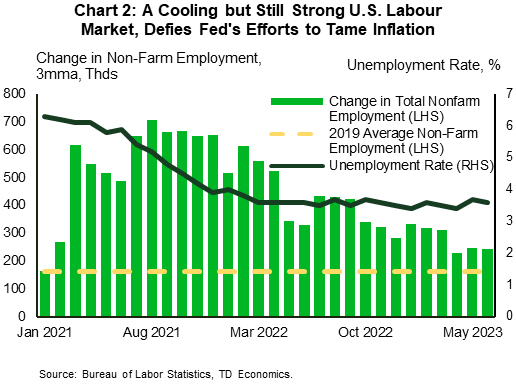

Fears about a softening labor market, however, may be more accurately characterized as normalization after the white-hot levels attained during the pandemic. The job opening and labor turnover survey for May showed that over 4 million American workers quit their jobs (250k more than the previous month) and that there were over 9.8 million job openings available. This morning’s jobs data reinforced the picture of a normalizing, but still strong labor market. The report showed firms added 209k jobs, easing from May’s 306k. The unemployment rate also pulled back 0.1 ppts to 3.6% (Chart 2). Taken together, the employment reports are indicative of a relatively resilient labor market despite a more than year-long campaign of rate hikes by the Fed to quell inflation.

In that regard, minutes of the June FOMC meeting revealed that the decision behind the Fed’s first pause may have been unanimous, but some committee members would have supported raising rates. Concerns about the effects of past rate increases though tempered desires for a hike, with the resultant “hawkish pause” in June.

With the services sector and labor market still showing resilience, the Fed is justified in signaling more hikes to come. This will have to be balanced against the hit to consumer spending from the resumption of student loan payments and a possible trade squabble with China over high tech as the two countries impose tit-for-tat measures. The balancing act the Fed is currently undertaking is a delicate one, and they will have to tread cautiously as they walk the tightrope to engineer that elusive soft landing.

Canada – Job Market Sizzles

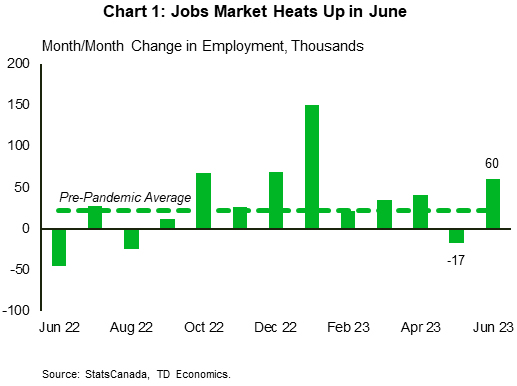

If you were looking to escape the scorching heat this week, the job market wasn't the right place. Less than a week before the Bank of Canada's rate decision on July 12th, the key June jobs report proved to be hotter than expected. The economy added 60k jobs – three times what was expected by the consensus, and more than enough to offset losses reported last month (Chart 1). The S&P TSX moved lower, and the 5-year Government of Canada yield briefly touched 4.0% on a conviction that policy rates are heading higher, and will remain elevated for longer than previously thought.

Meanwhile, the unemployment rate ticked up as more people entered the labour force thanks to a record pace of population growth. The increase in the unemployment rate offers a cautionary note, even as the level of the unemployment rate remains low at 5.4%. With luck, demand for labour will continue to cool in line with a slowdown in broader economic activity, which will help bring wage inflation down.

There was a bit of good news for the Bank of Canada's inflation battle in the jobs report. Average hourly earnings increased 4.2% over the past year - the slowest year-over-year rate since May 2022. This suggests wage growth is stepping down to trend and gradually getting closer to the pace more consistent with the BoC's 2% inflation target, but is still higher than the bank would like to see.

Wage growth is a major issue at the negotiating table between the International Longshore and Warehouse Union, representing around 7,400 port workers, and the B.C. Maritime Employers Association during a strike in B.C. that started July 1st. Should the strike continue for another week, the effects on the economy would come through merchandise trade, which in May registered the largest deficit since the fall of 2020. We estimate an impact to July's GDP would not exceed two tenth of a percentage point and will be offset in August.

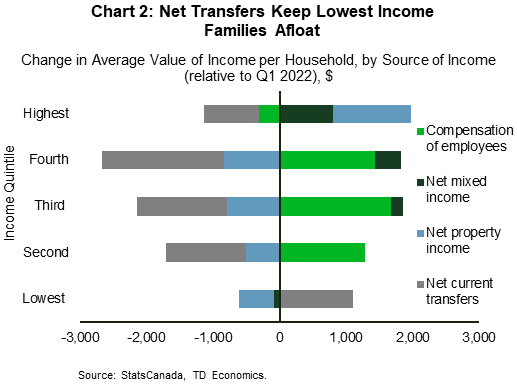

A high cost of living and rising debt service cost were also on full display in this week's Statistics Canada's report on distributions of household economic accounts in Q1 2023. According to the report, since the start of the Bank of Canada's hiking cycle last year, lowest income families' average wages were little changed, self-employment earnings declined, and investment returns failed to dilute the spike in the cost of borrowing. In addition, more of the lowest income households relied on government benefits and paid less taxes – a trend that would become more prevalent as an increasing share of baby boomers retire (Chart 2). In contrast, interest charges for the highest income earners were more than offset by gains in investment earnings, which helped boost overall average disposable income for this segment.

All in all, the report suggests that the least wealthy are being affected more by higher interest rates and inflation. Since fighting the latter is unattainable without keeping a hard line on the former, the Bank of Canada's task of keeping inflation in check is becoming more complicated by the day. Nevertheless, with the employment market offering little sunshade buffer, the Bank is likely to raise rates next week.

Summary 7/10 – 7/14

Monday, Jul 10, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jun | 3.50% | 3.40% |

| 23:50 | JPY | Current Account (JPY) May | 1.87T | 1.90T |

| 01:30 | CNY | CPI Y/Y Jun | 0.20% | 0.20% |

| 01:30 | CNY | PPI Y/Y Jun | -5.00% | -4.60% |

| 05:00 | JPY | Eco Watchers Survey: Outlook Jun | 54.8 | 55 |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -18.9 | -17.0 |

| 12:30 | CAD | Building Permits M/M May | -18.80% | |

| 14:00 | USD | Wholesale Inventories May F | -0.10% | |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jun | 3.70% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | 2.70% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jun | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 23:50 | JPY | Current Account (JPY) May | |

| Forecast: 1.87T | Previous: 1.90T | ||

| 01:30 | CNY | CPI Y/Y Jun | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 01:30 | CNY | PPI Y/Y Jun | |

| Forecast: -5.00% | Previous: -4.60% | ||

| 05:00 | JPY | Eco Watchers Survey: Outlook Jun | |

| Forecast: 54.8 | Previous: 55 | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | |

| Forecast: -18.9 | Previous: -17.0 | ||

| 12:30 | CAD | Building Permits M/M May | |

| Forecast: | Previous: -18.80% | ||

| 14:00 | USD | Wholesale Inventories May F | |

| Forecast: | Previous: -0.10% | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jun | |

| Forecast: | Previous: 3.70% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | |

| Forecast: 2.70% | Previous: 2.70% | ||

Tuesday, Jul 11, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jul | 0.20% | |

| 01:30 | AUD | NAB Business Conditions Jun | 8 | |

| 01:30 | AUD | NAB Business Confidence Jun | -4 | |

| 06:00 | GBP | Claimant Count Change Jun | -13.6K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 3.80% | 3.80% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | 6.80% | 6.50% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 7.20% | |

| 06:00 | EUR | Germany CPI M/M Jun F | 0.30% | 0.30% |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 6.40% | 6.40% |

| 08:00 | EUR | Italy Industrial Output M/M May | 0.90% | -1.90% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | -9.5 | -8.5 |

| 09:00 | EUR | Germany ZEW Current Situation Jul | -56.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | -9 | -10 |

| 10:00 | USD | NFIB Business Optimism Index Jun | 89.9 | 89.4 |

| 23:50 | JPY | PPI Y/Y Jun | 4.50% | 5.10% |

| 23:50 | JPY | Machinery Orders M/M May | 1.20% | 5.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jul | |

| Forecast: | Previous: 0.20% | ||

| 01:30 | AUD | NAB Business Conditions Jun | |

| Forecast: | Previous: 8 | ||

| 01:30 | AUD | NAB Business Confidence Jun | |

| Forecast: | Previous: -4 | ||

| 06:00 | GBP | Claimant Count Change Jun | |

| Forecast: | Previous: -13.6K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) May | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | |

| Forecast: 6.80% | Previous: 6.50% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | |

| Forecast: | Previous: 7.20% | ||

| 06:00 | EUR | Germany CPI M/M Jun F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Jun F | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 08:00 | EUR | Italy Industrial Output M/M May | |

| Forecast: 0.90% | Previous: -1.90% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | |

| Forecast: -9.5 | Previous: -8.5 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jul | |

| Forecast: | Previous: -56.5 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | |

| Forecast: -9 | Previous: -10 | ||

| 10:00 | USD | NFIB Business Optimism Index Jun | |

| Forecast: 89.9 | Previous: 89.4 | ||

| 23:50 | JPY | PPI Y/Y Jun | |

| Forecast: 4.50% | Previous: 5.10% | ||

| 23:50 | JPY | Machinery Orders M/M May | |

| Forecast: 1.20% | Previous: 5.50% | ||

Wednesday, Jul 12, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% |

| 12:30 | USD | CPI M/M Jun | 0.30% | 0.10% |

| 12:30 | USD | CPI Core Y/Y Jun | 5.30% | |

| 12:30 | USD | CPI Core M/M Jun | 0.30% | 0.40% |

| 12:30 | USD | CPI Y/Y Jun | 4.00% | |

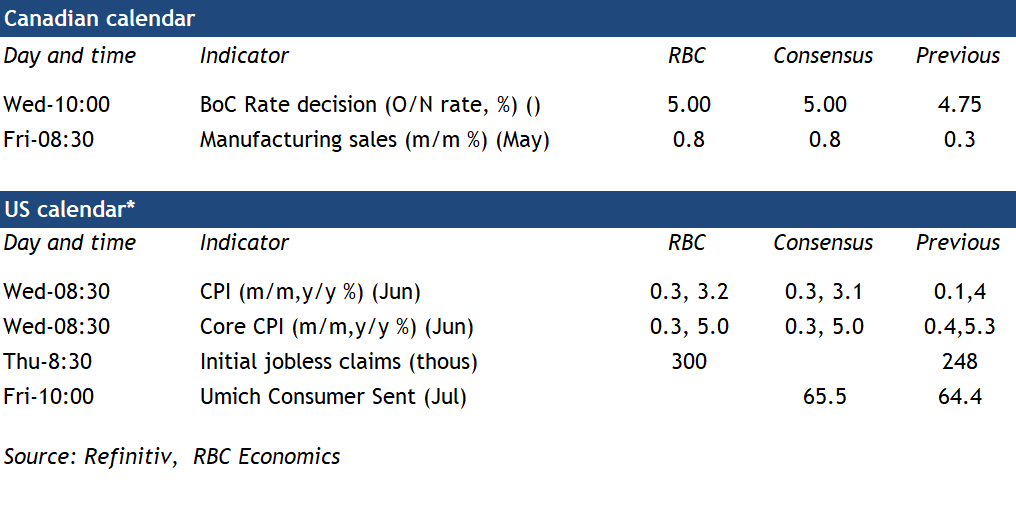

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 4.75% |

| 14:30 | USD | Crude Oil Inventories | -1.5M | |

| 15:00 | CAD | BoC Press Conference | ||

| 18:00 | USD | Fed's Beige Book | ||

| 22:30 | NZD | Business NZ PMI Jun | 48.9 | |

| 23:01 | GBP | RICS Housing Price Balance Jun | -30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 12:30 | USD | CPI M/M Jun | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Jun | |

| Forecast: | Previous: 5.30% | ||

| 12:30 | USD | CPI Core M/M Jun | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Y/Y Jun | |

| Forecast: | Previous: 4.00% | ||

| 14:00 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 4.75% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -1.5M | ||

| 15:00 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 22:30 | NZD | Business NZ PMI Jun | |

| Forecast: | Previous: 48.9 | ||

| 23:01 | GBP | RICS Housing Price Balance Jun | |

| Forecast: | Previous: -30% | ||

Thursday, Jul 13, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Jul | 5.20% | |

| 03:00 | CNY | Trade Balance (USD) Jun | 74.0B | 65.8B |

| 06:00 | GBP | GDP M/M May | -0.40% | 0.20% |

| 06:00 | GBP | Industrial Production M/M May | -0.40% | -0.30% |

| 06:00 | GBP | Industrial Production Y/Y May | -1.90% | |

| 06:00 | GBP | Manufacturing Production M/M May | -0.50% | -0.30% |

| 06:00 | GBP | Manufacturing Production Y/Y May | -0.90% | |

| 06:00 | GBP | Goods Trade Balance (GBP) May | -14.6B | -15.0B |

| 09:00 | EUR | Eurozone Industrial Production M/M May | 0.30% | 1.00% |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 12:30 | USD | PPI M/M Jun | 0.20% | -0.30% |

| 12:30 | USD | PPI Y/Y Jun | 1.10% | |

| 12:30 | USD | PPI Core M/M Jun | 0.20% | 0.20% |

| 12:30 | USD | PPI Core Y/Y Jun | 2.80% | |

| 12:30 | USD | Initial Jobless Claims (Jul 7) | 250K | 248K |

| 14:30 | USD | Natural Gas Storage | 72B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Jul | |

| Forecast: | Previous: 5.20% | ||

| 03:00 | CNY | Trade Balance (USD) Jun | |

| Forecast: 74.0B | Previous: 65.8B | ||

| 06:00 | GBP | GDP M/M May | |

| Forecast: -0.40% | Previous: 0.20% | ||

| 06:00 | GBP | Industrial Production M/M May | |

| Forecast: -0.40% | Previous: -0.30% | ||

| 06:00 | GBP | Industrial Production Y/Y May | |

| Forecast: | Previous: -1.90% | ||

| 06:00 | GBP | Manufacturing Production M/M May | |

| Forecast: -0.50% | Previous: -0.30% | ||

| 06:00 | GBP | Manufacturing Production Y/Y May | |

| Forecast: | Previous: -0.90% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) May | |

| Forecast: -14.6B | Previous: -15.0B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M May | |

| Forecast: 0.30% | Previous: 1.00% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | |

| Forecast: | Previous: | ||

| 12:30 | USD | PPI M/M Jun | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 12:30 | USD | PPI Y/Y Jun | |

| Forecast: | Previous: 1.10% | ||

| 12:30 | USD | PPI Core M/M Jun | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | PPI Core Y/Y Jun | |

| Forecast: | Previous: 2.80% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 7) | |

| Forecast: 250K | Previous: 248K | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 72B | ||

Friday, Jul 14, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M May F | -1.60% | -1.60% |

| 06:30 | CHF | Producer and Import Prices M/M Jun | 0.20% | -0.30% |

| 06:30 | CHF | Producer and Import Prices Y/Y Jun | -0.30% | |

| 08:00 | EUR | Italy Trade Balance (EUR) May | 1.45B | 0.32B |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | -10.3B | -7.1B |

| 12:30 | CAD | Manufacturing Sales M/M May | 0.80% | 0.30% |

| 12:30 | USD | Import Price Index M/M Jun | -0.60% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Jul P | 65.5 | 64.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M May F | |

| Forecast: -1.60% | Previous: -1.60% | ||

| 06:30 | CHF | Producer and Import Prices M/M Jun | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Jun | |

| Forecast: | Previous: -0.30% | ||

| 08:00 | EUR | Italy Trade Balance (EUR) May | |

| Forecast: 1.45B | Previous: 0.32B | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | |

| Forecast: -10.3B | Previous: -7.1B | ||

| 12:30 | CAD | Manufacturing Sales M/M May | |

| Forecast: 0.80% | Previous: 0.30% | ||

| 12:30 | USD | Import Price Index M/M Jun | |

| Forecast: | Previous: -0.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jul P | |

| Forecast: 65.5 | Previous: 64.4 | ||

BoC to Hike Again Amid “Persistent Excess Demand”

The latest round of Canadian economic data is in—and it’s unlikely to deter the Bank of Canada from hiking rates again next week. Nothing in the data on employment, inflation, GDP or the second quarter release of the Bank of Canada’s own Business Outlook Survey (BOS) showed sufficient evidence of slowing consumer demand to convince the Bank of Canada another hike isn’t needed. Headline inflation dropped lower in May and could hit the top end of the BoC’s 1% to 3% inflation target range in June on lower energy prices. But the BoC’s preferred CPI trim and median inflation measures (designed to measure underlying broader inflation pressures) were still growing at an elevated 3.5% to 4% on an annualized 3-month average basis. And growth in the so-called ‘supercore’ (services ex-shelter) has been running stronger at 4.7%. GDP growth slowed in April but the preliminary estimate for May was substantially stronger. The Q2 BOS pointed to a still slowing growth backdrop and further easing in the intensity of labour shortages. But the commentary attached by the BoC flagged still higher-than-normal expectations for wage and price increases among Canadian businesses.

The path for the overnight rate–beyond the expected 25 basis point increase in July—remains very uncertain. We expect next week’s increase to be the last of this cycle. But the BoC has maintained its “proactive” approach when it comes to battling sticky inflation. And it wouldn’t hesitate to hike rates again in September if the economy doesn’t show more signs of cooling off. Still, aggressive rate hikes over the last year are continuing to pass through to household debt payments. Given that, the question that remains is when, not if, economic activity will slow. Consumer insolvencies rose sharply in May, getting closer to pre-pandemic levels. The rate of unemployment remains very low but increased in May and June. And easing labour demand–job openings fell to the lowest level in two years in April—continue to flag more weakness under the surface. It is still our view that further deterioration in economic activity is in the pipeline, as households are increasingly challenged by rising costs of living. That should be enough to keep the Bank of Canada on the sidelines for the remainder of this year.

Week ahead data watch

Statistics Canada’s advance estimate indicates manufacturing sales ticked up 0.8% in May, despite a sharp pullback in petroleum prices. The volume of manufacturing sales (excluding price impacts) likely rose more significantly, with increases in both the motor vehicle sector and machinery sales.

U.S. headline inflation in June likely slowed to 3.2% on a year-over-year basis, with widespread moderation among food, energy, and other components. Core inflation (ex-food and energy) is expected to decelerate too as some of the key drivers of recent monthly readings, including rents and used cars, start to turn around following easing in market-posted rent indices and declines in the Manheim used car index.

Research US – Rising Real Rates Cast a Shadow Over Upbeat Macro Data

Research US - Rising Real Rates Cast a Shadow Over Upbeat Macro Data

- The persistent strength of the US economy's service sector combined with steady labour market and too fast wage inflation call for one more Fed hike in July.

- As inflation expectations decline, real rates have risen above levels prevailing before SVB's collapse - increasing the risk of a hard landing down the line.

While the June macro data has been mixed, the overall tone has been more positive than anticipated. ISM Services showed a clear pick-up in both business activity and new orders, and even on the manufacturing side, order-inventory balance is gradually recovering. While PMIs sent somewhat contrasting signals, both surveys signalled that price pressures have continued to ease across different sectors.

Growth has relied heavily on the consumer, and so far, strong labour market has been a key factor supporting both real income growth and consumer confidence. Even though job openings declined modestly in the May JOLTs report, both voluntary quits and hiring picked up, suggesting that confidence in finding new jobs remains high.

While NFP growth slowed down in June, wage and wage sum growth remained too fast to be consistent with 2% inflation. Hence, we revise our Fed call, and now expect the Fed to hike by 25bp to 5.25-5.50% at the July meeting. We do not expect hikes beyond July.

Since November, we have been calling for the Fed to end the hiking cycle at the current level of 5.00-5.25%. We expected the Fed to hike the nominal policy rate until real interest rates are at a positive and modestly restrictive level, where we are today based on most estimates. This cools the excessively high aggregate demand over time, bringing inflation down slowly but sustainably. Given the recessionary signals from longer-lead monetary indicators and the first 'cracks' in the economy emerging last March, we think this approach strikes the best balance for cooling inflation while minimizing the risk of a hard landing.

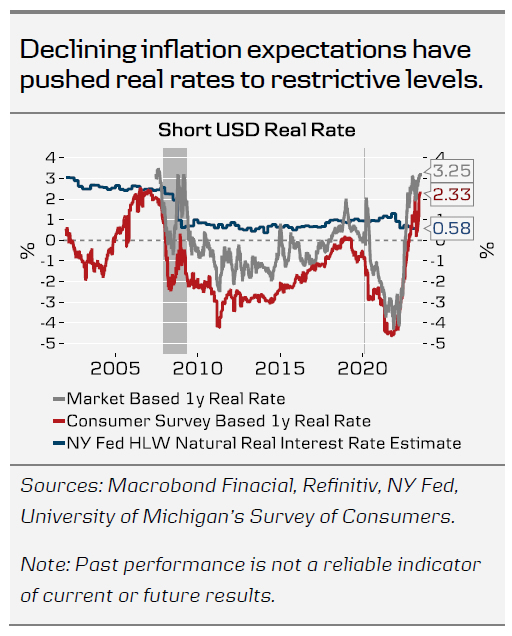

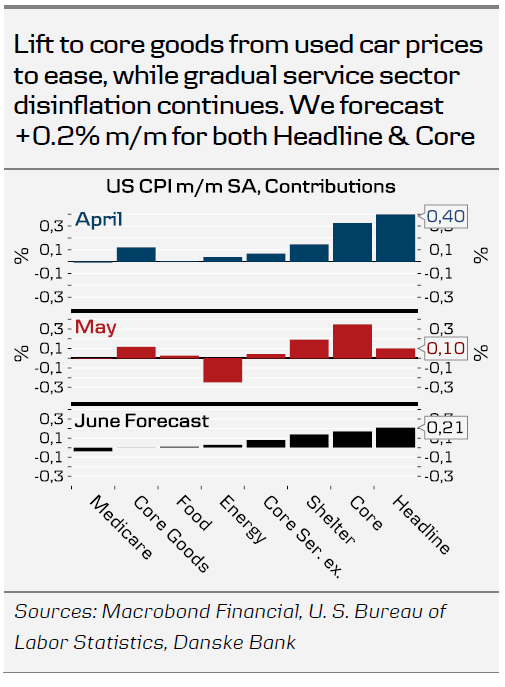

Next week, we forecast a downside surprise to the Core CPI (+0.2% m/m), as temporary lift from used car prices eases, and services disinflation continues. For now, yields have headed steadily higher ignoring the disinflationary signals, but over the past year, the market has not been able to sustain 10y UST yields above 4% for long before recession fears from tightening financial conditions have settled in. Today, real yields are at the highest levels since the GFC. The decline in inflation expectations has been evident not just in markets, but lately especially on the consumer surveys.

Continuing to hike nominal rates further from here will ultimately increase the risk of a hard landing down the line, but with few data releases remaining before the meeting, and following hawkish comments from the Fed, we see the chance of another pause low.

A pause would likely require 1) a low CPI print, 2) further decline in University of Michigan's short-term inflation expectations (due 14 July) and 3) deterioration in market risk sentiment, reflecting growing recession fears. If the Fed chooses to signal another hike beyond July in line with the June SEP, we think a risk of a deeper downturn increases, despite the recent upbeat macro data. This would also imply faster turn towards cutting rates in the future.