Sample Category Title

Research US – Rising Real Rates Cast a Shadow Over Upbeat Macro Data

Research US - Rising Real Rates Cast a Shadow Over Upbeat Macro Data

- The persistent strength of the US economy's service sector combined with steady labour market and too fast wage inflation call for one more Fed hike in July.

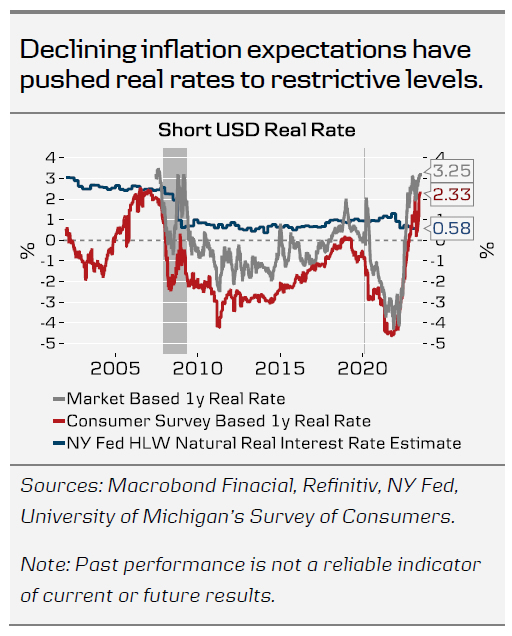

- As inflation expectations decline, real rates have risen above levels prevailing before SVB's collapse - increasing the risk of a hard landing down the line.

While the June macro data has been mixed, the overall tone has been more positive than anticipated. ISM Services showed a clear pick-up in both business activity and new orders, and even on the manufacturing side, order-inventory balance is gradually recovering. While PMIs sent somewhat contrasting signals, both surveys signalled that price pressures have continued to ease across different sectors.

Growth has relied heavily on the consumer, and so far, strong labour market has been a key factor supporting both real income growth and consumer confidence. Even though job openings declined modestly in the May JOLTs report, both voluntary quits and hiring picked up, suggesting that confidence in finding new jobs remains high.

While NFP growth slowed down in June, wage and wage sum growth remained too fast to be consistent with 2% inflation. Hence, we revise our Fed call, and now expect the Fed to hike by 25bp to 5.25-5.50% at the July meeting. We do not expect hikes beyond July.

Since November, we have been calling for the Fed to end the hiking cycle at the current level of 5.00-5.25%. We expected the Fed to hike the nominal policy rate until real interest rates are at a positive and modestly restrictive level, where we are today based on most estimates. This cools the excessively high aggregate demand over time, bringing inflation down slowly but sustainably. Given the recessionary signals from longer-lead monetary indicators and the first 'cracks' in the economy emerging last March, we think this approach strikes the best balance for cooling inflation while minimizing the risk of a hard landing.

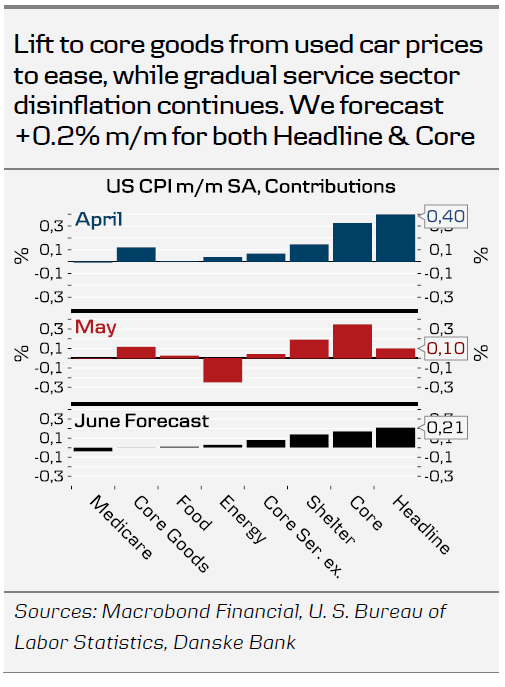

Next week, we forecast a downside surprise to the Core CPI (+0.2% m/m), as temporary lift from used car prices eases, and services disinflation continues. For now, yields have headed steadily higher ignoring the disinflationary signals, but over the past year, the market has not been able to sustain 10y UST yields above 4% for long before recession fears from tightening financial conditions have settled in. Today, real yields are at the highest levels since the GFC. The decline in inflation expectations has been evident not just in markets, but lately especially on the consumer surveys.

Continuing to hike nominal rates further from here will ultimately increase the risk of a hard landing down the line, but with few data releases remaining before the meeting, and following hawkish comments from the Fed, we see the chance of another pause low.

A pause would likely require 1) a low CPI print, 2) further decline in University of Michigan's short-term inflation expectations (due 14 July) and 3) deterioration in market risk sentiment, reflecting growing recession fears. If the Fed chooses to signal another hike beyond July in line with the June SEP, we think a risk of a deeper downturn increases, despite the recent upbeat macro data. This would also imply faster turn towards cutting rates in the future.

Will Upcoming UK Data Allow the Pound to Keep its Crown?

Following the 50bps hike by the Bank of England in June, many market participants are now convinced that another increase of that size will be delivered in August, while they are anticipating several more hikes before the Bank calls the end of this tightening crusade. So, as they try to better assess how the Bank will move forward, next week, investors are likely to pay attention to Tuesday’s jobs data for May (06:00 GMT) and Thursday’s monthly GDP for that same month (06:00 GMT).

Investors anticipate another 50bps hike in August

With UK inflation staying stubbornly high and political pressure mounting, the BoE decided to proceed with a 50bps rate increment at its June gathering, reiterating the guidance that if there were evidence of more price pressures, further tightening in monetary policy would be required.

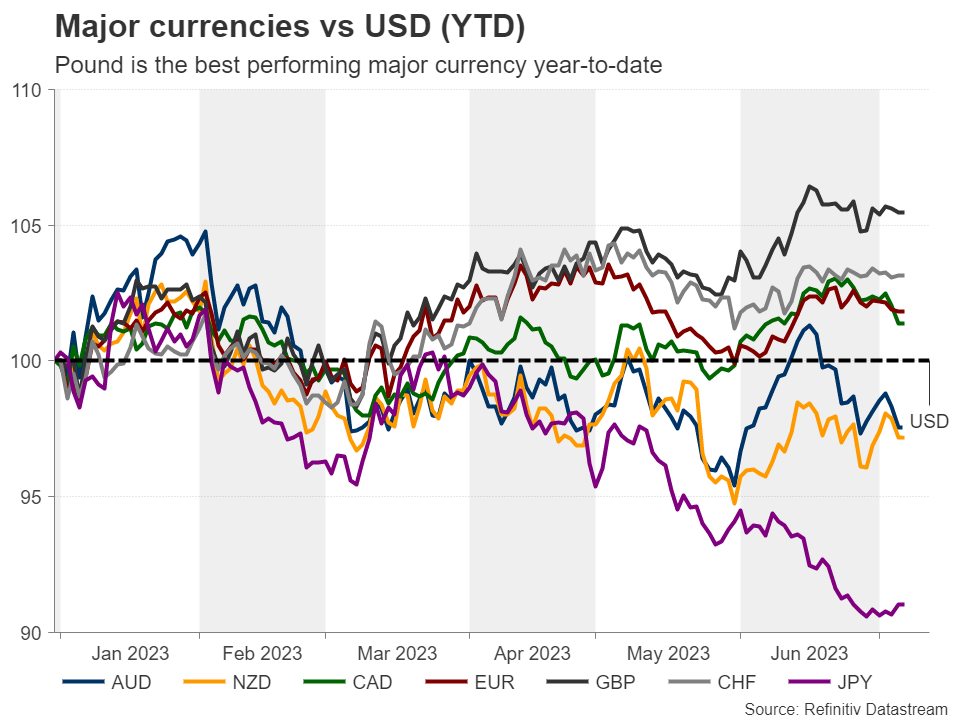

This, combined with yesterday’s comments from Governor Bailey that they must act now to bring inflation to heel, allowed market participants to maintain bets of several more hikes before the Bank decides the end credits of this tightening season roll. Investors are now pricing a 70% probability of another double hike at the upcoming gathering, with the remaining 30% pointing to a quarter-point increase, while they are penciling in slightly more than 100bps worth of additional rate increases thereafter. This puts the BoE at the top spot in terms of hike expectations among other major central banks, a view that allowed the pound to perform better against every other major currency year-to-date.

Will upcoming data add to the need for more hikes?

Since the last Bank decision, the only top-tier data that was released were the retail sales for May, which slowed instead of contracting as the forecasts suggested, and the PMIs for June. Both the manufacturing and services indices fell by more than expected, driving the composite PMI down to 52.8 from 54.0. On top of that, the surveys revealed that prices charged by private sector firms slowed to the lowest pace in 26 months, which is somewhat encouraging inflation-wise.

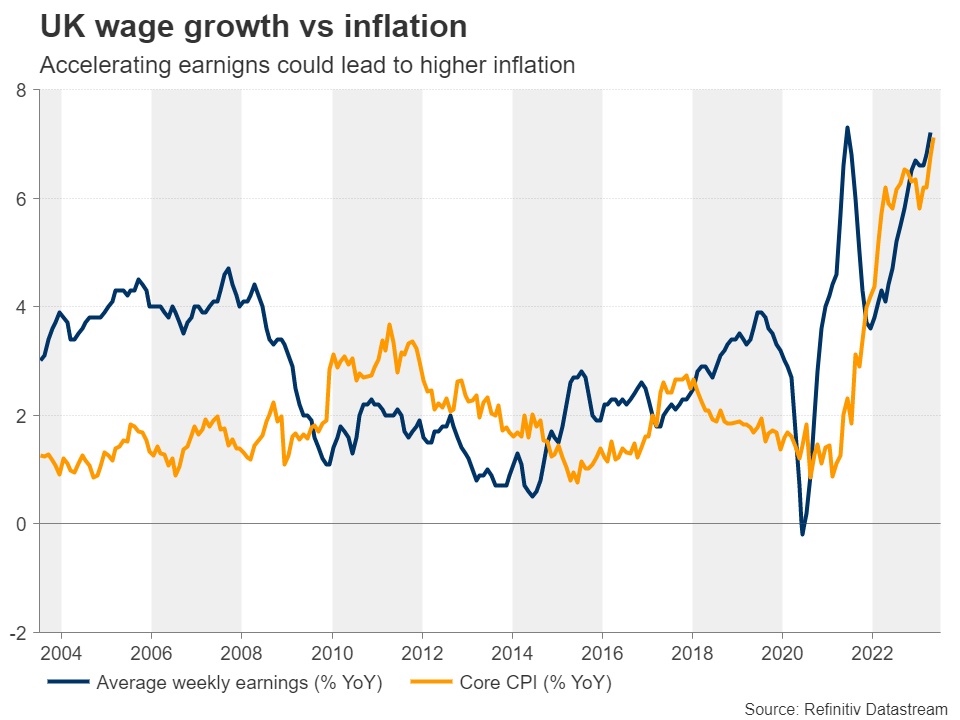

That said, with the headline CPI rate staying at 8.7% in May, more than double the US rate, and underlying price pressures accelerating to 7.1% from 6.8%, the June PMIs are far from alleviating any pressure from the BoE to continue raising rates aggressively. Next week brings more UK data to the table, with the employment report for May coming out on Tuesday and the monthly GDP for the same month on Thursday. Industrial and manufacturing production data will also be released that day.

There are no forecasts currently available for the jobs report, but GBP-traders are likely to pay extra attention to wage growth. In April, average weekly earnings, both including and excluding bonuses, accelerated and thus, another acceleration in May could revive fears that inflation is unlikely to cool anytime soon.

Pound’s uptrend likely destined to continue for a while more

This could prompt investors to add to their already brave rate-hike bets, thereby supporting the pound. The currency could extend its gains if Thursday’s data confirmed that the economy is able to bear a series of additional rate hikes.

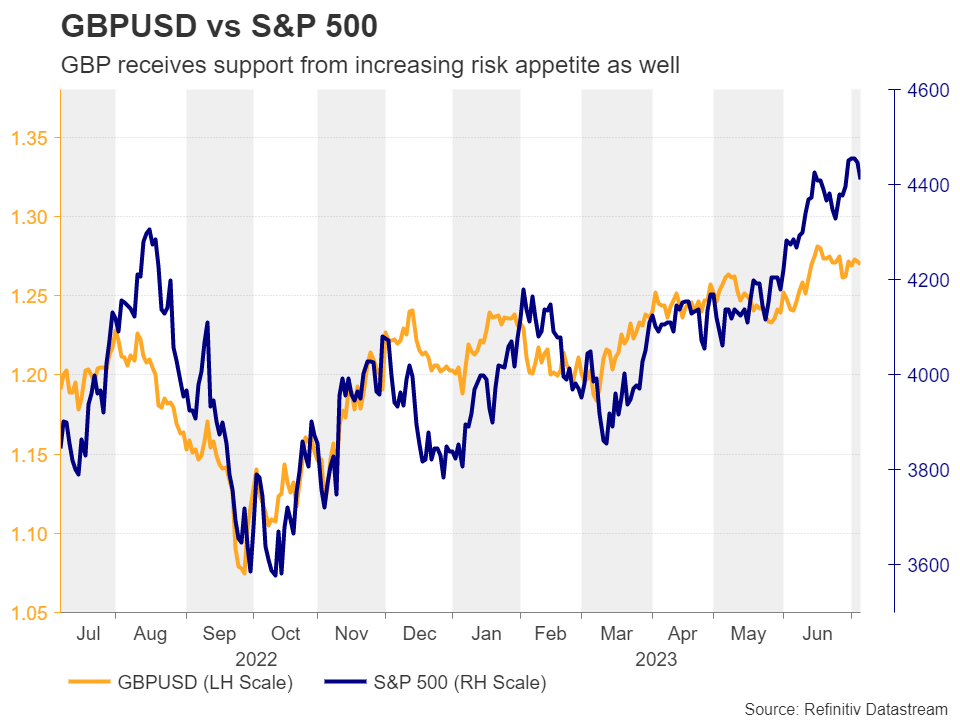

Having said that though, monetary policy expectations are not the only catalyst behind the pound’s rally. Due to the UK’s twin deficit, the British currency has developed risk-linked characteristics in the last few years, with the correlation coefficient between pound/dollar and the S&P 500 since the October lows, being at an impressive 0.85. Therefore, an uptrend continuation in global equity markets could keep giving that extra boost to the pound.

From a technical standpoint, pound/dollar has recently rebounded from near the 1.2590 zone, staying above the uptrend line drawn from the low of October 12. This suggests that the upward trajectory remains intact, but its continuation is likely to be signaled upon a break above 1.2845, a move that will confirm a higher high on the daily chart.

If indeed this is the case, the bulls may quickly test the 1.2975 zone, which acted as strong support during March and April last year, and should they manage to overcome it, they may start marching towards the peak of March 23, 2022, at around 1.3305.

For the outlook to turn bearish, the pair may need to fall below the key zone of 1.2340, which offered both strong support and resistance during the last year or so. Such a break may encourage the bears to dive towards the 1.2025 zone, the break of which could carry extensions towards the low of March 8 at 1.1795.

Week Ahead – US Inflation Report, BoC and RBNZ Meetings Eyed

Another exciting week lies ahead for FX markets, before trading conditions start to wind down for the summer. The spotlight will fall on the latest US inflation report, which could help the dollar break out of its recent stalemate. Central bank meetings in New Zealand and Canada will also be closely watched, especially the Bank of Canada rate decision, which is currently priced as a coin toss.

Dollar in limbo, awaits inflation test

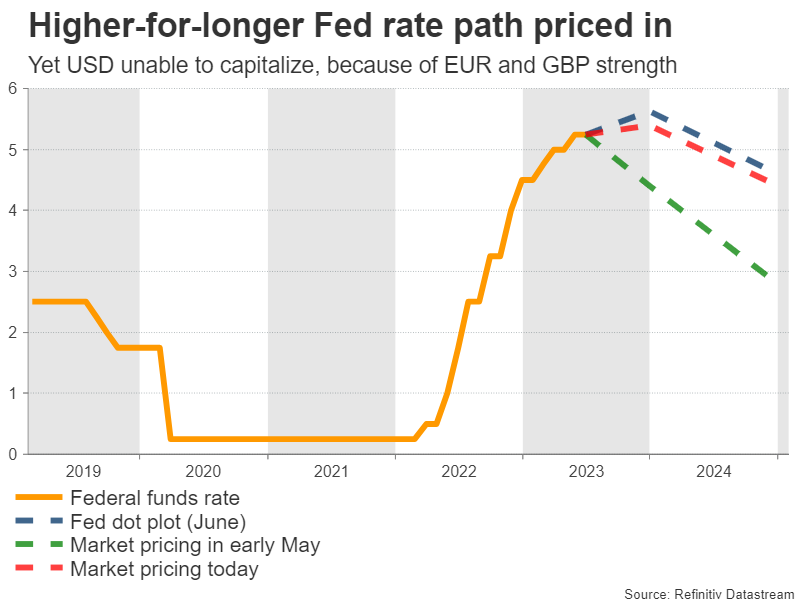

The second quarter of this year was tough for the dollar, even though the US economy seems to be humming along. Economic growth is running near 2%, the housing market has enjoyed a sensational comeback, and the labor market seems to be in good shape.

Investors responded by pricing in a higher-for-longer path for interest rates, pushing out the projected timing of any rate cuts into the second half of 2024. In turn, that sparked some pretty impressive moves in the bond market, with the 2-year yield in particular racing higher.

Yet the dollar was unable to capitalize, drifting sideways instead. This stagnation probably reflects the strength in other major currencies, specifically the euro and sterling, as their central banks telegraphed a series of rate increases ahead.

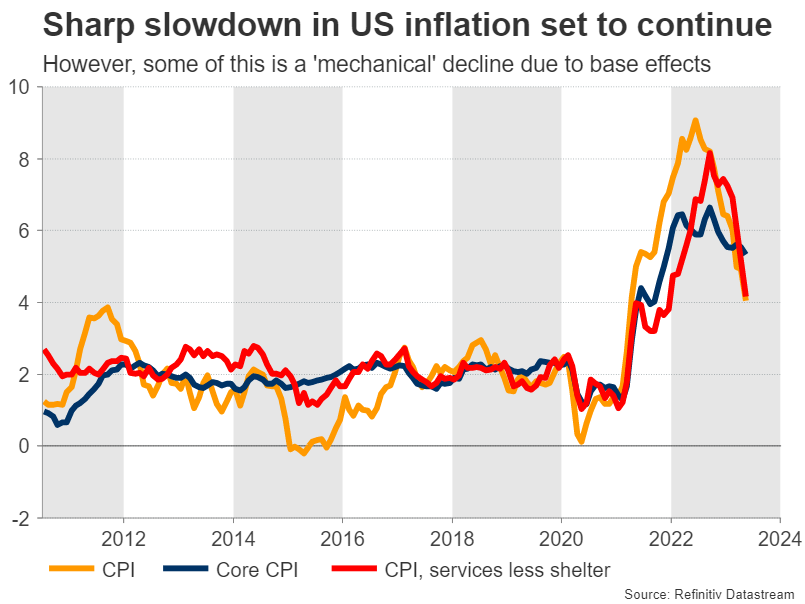

The upcoming US inflation report on Wednesday can help break this FX stalemate. In yearly terms, forecasts point to a sharp slowdown in inflation. The headline CPI rate is set to decline to 3.6% from 4% previously, while the core rate is seen dropping to 5% from 5.3% in May.

Much of this improvement is due to base effects, as some extremely hot CPI prints from June 2022 will now be dropping out of the 12-month calculation. Inflation is definitely coming down, something also confirmed by business surveys, but not at such an astonishing pace. Data on producer prices will also be released on Thursday.

As for the dollar, the outlook for the second half of the year seems brighter. It’s a story of relative economic performance, as the US economy is far superior to the Eurozone’s or China’s at this stage. And this gap could widen further as the year unfolds, amid warnings from business surveys that both Europe and China are losing steam, in contrast to resilient US surveys.

Currency markets have been trading almost entirely on rate differentials lately, helping to explain the strength in the euro as the ECB maintained a hawkish stance. However, with central banks approaching the end of their tightening cycles, the next trading theme might be growth differentials, which clearly favor the US.

A potential shift in global risk appetite could also help the dollar to recover. If the euphoria in stock markets calms down and there’s a correction in risk assets later this year, the world’s reserve currency could finally attract some safe haven flows.

Traders divided on Canadian rate hike

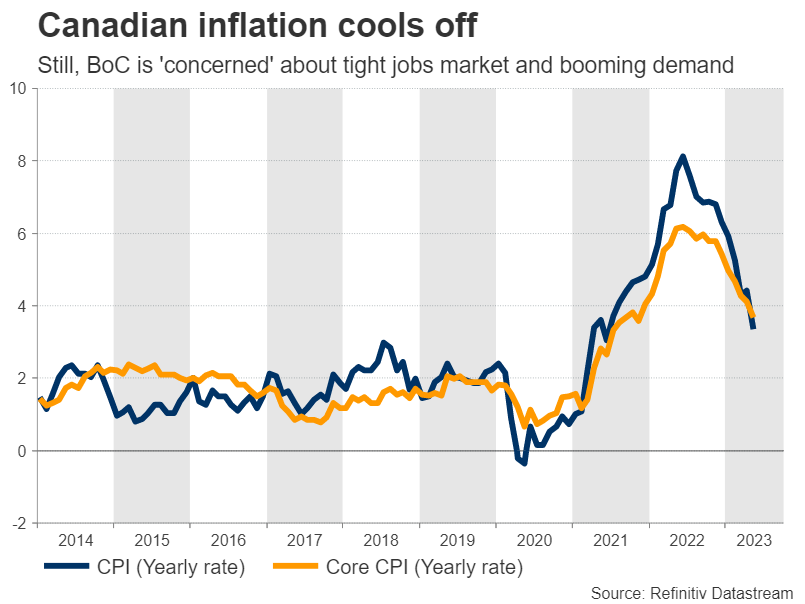

Crossing into neighboring Canada, the central bank will wrap up its meeting on Wednesday, with market participants assigning almost equal chances for a 25bps rate increase or no action at all.

Arguing for the Bank of Canada to do nothing is the steady decline in inflation this year, which is the most important element for any central bank. Additionally, the nation’s manufacturing sector is struggling amid a global downturn and oil prices have declined substantially.

However, the labor market is still very tight, consumer spending has been resilient, and housing costs have not really cooled despite the sharp increase in interest rates, as net population growth has been exceptionally strong.

Hence, it’s a true dilemma for the central bank - inflation is cooling but several factors suggest it could heat up again moving forward.

In the FX market, the risks seem tilted towards a negative reaction in the Canadian dollar. With inflation coming down, it would make more sense for the BoC to take the sidelines for now. Even if the BoC raises rates and the loonie spikes higher, there’s still a risk the initial excitement fades quickly if policymakers signal this is probably their final move.

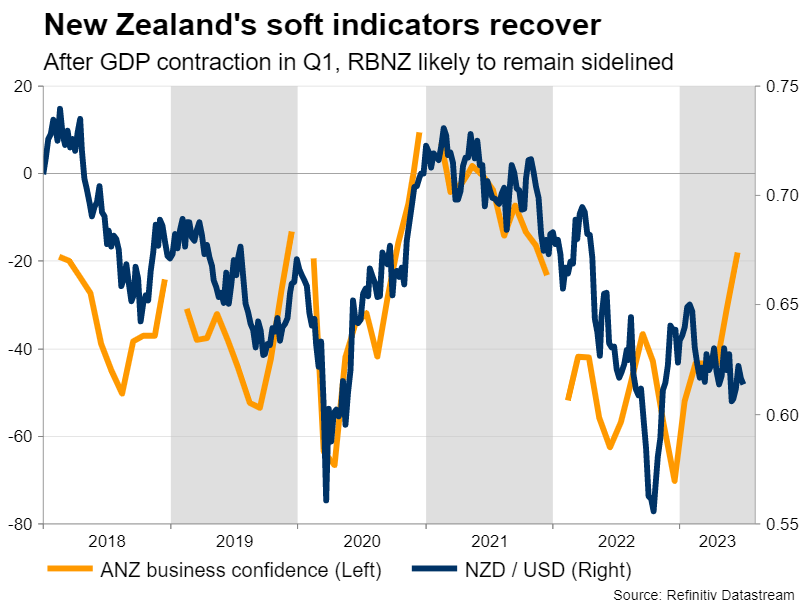

RBNZ - A quiet meeting

It’s going to be a more straight-forward affair when the Reserve Bank of New Zealand decides early on Wednesday. The RBNZ made it clear at its latest meeting that it will adopt a wait-and-see stance and examine incoming data for some time, before making its next move.

Economic data since then has been mixed, with GDP growth turning slightly negative in Q1 but survey-based indicators pointing to a recovery in the second quarter. Overall though, nothing shocking enough to nudge the RBNZ out of its neutral stance.

Therefore, the reaction in the New Zealand dollar might be relatively minimal, leaving the currency mostly in the hands of global risk sentiment and any news out of China. Specifically, any stimulus announcements by Chinese authorities could be crucial, considering the close trading links between the two economies.

Speaking of China, the nation’s inflation stats for June will be released early on Monday. Producer prices - a proxy for factory demand - have been falling steadily in recent months as the manufacturing sector lost power and it will be interesting to see if this trend persists. The latest trade data will also be released on Thursday.

Last but not least, the UK will see the release of its employment numbers for May on Tuesday, ahead of monthly GDP data for the same month on Thursday.

Week Ahead – US Inflation Data the Headline, BoC Ponders Another Hike, Possible RBNZ Pause

US

This week is all about inflation. Annual inflation will tumble as energy prices drop and due to base effects, but many traders will pay close attention to the core readings. CPI on a monthly basis is expected to increase by 0.3%, higher than May’s pace of 0.1%. The headline annual reading is expected to fall from 4.0% to 3.0%. The monthly core reading is expected to rise 0.3%, while the year-over-year reading softens to 5.0%. Expectations are for pricing pressures to edge higher going forward.

The upcoming week is filled with Fed speakers and the Wednesday release of the Beige Book. On Monday, we hear from Barr on bank supervision, Daly talks about inflation and banking, and Mester discusses the economic and policy outlook. Wednesday contains appearances by Barkin, who talks about inflation, Kashkari discusses monetary policy, Bostic attends the Atlanta Fed payments event, and Mester speaks on FedNow. The recent flow of economic data may warrant steady hawkish Fed speak.

Eurozone

Not the most thrilling of weeks, dominated by tier two and three economic data. The standout is probably the ECB accounts, although I’m not sure there’ll be anything overly surprising in them. ZEW surveys, final inflation readings, and new EU economic forecasts are also notable but may not move the needle when it comes to economic or interest rate expectations.

UK

Next week offers a selection of economic data, the most notable being the labor market report on Tuesday. Better data seems to be appearing everywhere but the UK at the moment and BoE policymakers will be hoping the jobs data brings some overdue good news, being more modest wage growth and signs of an overheated labor market cooling. No doubt BoE Governor Andrew Bailey will comment on this is his numerous appearances throughout the week. We’ll also get an update on the resilience of the economy with GDP data on Tuesday and Thursday, the latter being the official release.

Russia

Inflation data on Wednesday is expected to show pressures heating up which may explain why the CBR has been hinting that the next interest rate move may be higher rather than lower. The extent to which the CPI number rises will likely determine the urgency with which the central bank will respond. The rouble remains under pressure and rate hikes may help to address both problems.

South Africa

No major economic data or events next week. Manufacturing production and the business confidence survey are the only notable releases.

Turkey

The lira remains under immense pressure after the government abandoned its unsustainable and unconventional policy of monetary easing and market interventions, which triggered an enormous spike in inflation. Inflation eased slightly last month but that won’t likely last as the currency has fallen to new record lows. Data next week include unemployment, industrial production, and current account.

Switzerland

No major releases or events next week, with PPI on Friday as the only thing on the calendar.

China

Several key data and events to watch for this week. On the geopolitical front, US Treasury Yellen has kick-started her official visit to China and will be meeting top Chinese officials over the weekend, 8 July to 9 July. Market participants will be watching for signs of whether there will be progress made between the US and China in finding areas of common economic ground and opening communication channels for further dialogue amid a still frosty relationship between them over the current “tech war”.

On Monday, inflation and producers’ prices data for June will be out and the consensus is set for a continuation of lackluster readings. Consumer inflation is expected to come in at 0.2% year-on-year, unchanged from 0.2% in April, a 26-month low. On the other hand, producers’ prices are expected to slip further to -5% year-on-year from -4.6% in May. If it turns out as expected, it will be the ninth consecutive month of contraction which increases the risk of a deflationary spiral in China.

On Tuesday, outstanding loan growth together with M2 money supply data will be released. Loan growth is expected to inch slightly lower to 11.2% year-on-year in June from 11.4% in May; its weakest pace of increase since January 2023.

On Thursday, the balance of trade for June will be out to gauge the latest conditions in external and internal demand. Exports growth is forecasted to shrink at a lesser magnitude of -3.1% year-on-year from -7.5% in May, a three-month low. Imports growth is forecasted to decline at a lesser rate of -2 % year-on-year from -4.5% in May. If it turns out as forecasted, it will be the fourth consecutive month of falling purchases, signaling the continuation of a weak domestic demand environment.

India

Out on Wednesday, consumer inflation for June is forecasted to dip slightly to 4.1% year-on-year from 4.25% in May, the lowest level of growth since April 2021. On a month-on-month basis, consumer inflation is forecasted to inch lower to 0.3% from 0.51% in May.

Wholesale inflation for June will be released on the following day and are forecast to drop further to -3.7% year-on-year from -3.48% in May. If it turns out as expected, it will be the third consecutive month of contraction.

To wrap up the week, the balance of trade for June will be out on Friday.

Australia

Two key soft data will be out on Tuesday; Westpac consumer confidence is expected to rise further to 3.2% month-on-month for July from 0.2% recorded in June. In contrast, the NAB Business Confidence for June is forecasted to deteriorate further to -6 from -4 in May.

Consumer inflation expectations for Jul will be released on Thursday, it is expected to dip slightly to 4.9% from 5.2% in June.

New Zealand

The RBNZ monetary policy decision is on Wednesday, with no change expected after the central bank hiked its official cash rate for the 12th consecutive time in May. This took it to 5.5%, its highest level since December 2008.

Japan

Out on Monday, the current account surplus for May is expected to shrink slightly to JPY1,884.5 billion from JPY1,895.1 billion in April. Bank lending for June is forecasted to drop to 1.6% year-on-year from 3.4% in May.

Eco Watchers Survey, a gauge for Japan’s service sector sentiment is forecasted to improve further to 56 in June from 55 recorded in May, its highest reading since December 2021. If it turns out as expected, it will be the fifth consecutive month of increases for service sector sentiment.

Machinery orders for May will be released on Wednesday. The consensus is expecting a reduction in growth decline to -0.2% year-on-year from -5.9% in April.

Singapore

Flash Q2 GDP will be out on Friday; some forecasters are calling for a technical recession where -0.2% is being forecasted on a quarter-on-quarter basis for Q2. If it turns out as expected, it will be the second consecutive quarter of negative growth after Q1’s reading of -0.7% q/q.

On a year-on-year basis, Q2 GDP is forecast to come in lower at 0.1% from 0.4% recorded in Q1.

Economic Calendar

Saturday, July 8

Economic Events

- US Treasury Secretary Yellen is in China through Sunday for meetings with senior government officials

- Monetary Authority of Singapore to name Deputy Prime Minister Wong as central bank chair

- ASEAN foreign ministers and their counterparts from the US, China, Russia, and other key partners

Sunday, July 9

Economic Data/Events

- China aggregate financing, money supply, new yuan loans

- US President Joe Biden attends 74th NATO summit

- ECB policymakers Villeroy, Centeno, and de Cos, plus Bank of England Governor Bailey speak at Les Rencontres Economiques d’Aix-en-Provence 2023 conference

- Australian Conference of Economists in Brisbane through Wednesday

Monday, July 10

Economic Data/Events

- China CPI, PPI

- Japan balance of payments

- New Zealand home sales

- Singapore GDP

- US wholesale inventories

- Fed’s Daly to discuss inflation and bank supervision at Brookings Institution event

- Fed’s Mester speaks on the economic and policy outlook at a virtual event hosted by the University of California at San Diego

- Fed’s Bostic speaks at the Cobb Chamber of Commerce

- Fed’s Barr in a discussion at Bipartisan Policy Center about bank supervision, regulation, and new capital requirements

- BOE Governor Bailey delivers speech at Financial and Professional Services Dinner

- Riksbank releases minutes from June 28 meeting

- German Chancellor Scholz, Australia’s Prime Minister Albanese joint news conference

Tuesday, July 11

Economic Data/Events

- Australia consumer confidence

- Germany CPI, ZEW survey expectations

- Italy industrial production

- Japan money stock, machine tool orders

- Mexico international reserves

- South Africa manufacturing production

- Turkey current account

- UK jobless claims, unemployment

- Fed’s Bullard speaks at National Association for Business Economics meeting

- NATO holds its annual summit

Wednesday, July 12

Economic Data/Events

- US CPI

- Canada rate decision: Expected to raise rates by 25bps to 5.00%

- India CPI, industrial production

- Japan PPI, machinery orders

- Mexico industrial production

- New Zealand rate decision

- Russia CPI

- Spain CPI

- Turkey industrial production

- US President Biden visits Helsinki for a US-Nordic summit

- US Federal Reserve issues Beige Book regional economic survey

- ECB’s Vujcic speaks on monetary policy and euro-area outlook

- ECB chief economist Lane and Fed’s Kashkari speak on a panel about banking solvency and monetary policy at the National Bureau of Economic Research Summer Institute 2023 event

- Fed’s Mester speaks about FedNow at the NBER event

- Fed’s Bostic speaks at the bank’s 2023 Payments Inclusion Forum

- White House economic adviser Brainard to address the Economic Club of New York

- BOE Governor Bailey at a news conference on results of financial stability report and stress tests of UK banking system

- BOE’s Breeden and Foulger brief on the stability report

- RBA Gov Lowe to speak at an event in conjunction with the Australian Conference of Economists in Brisbane

- Far East Grain Forum 2023 in Vladivostok, Russia

Thursday, July 13

Economic Data/Events

- US initial jobless claims, PPI

- China trade

- Eurozone industrial production

- France CPI

- Israel trade

- New Zealand food prices, manufacturing PMI

- UK industrial production

- French President Emmanuel Macron hosts Indian PM Narendra Modi

- EU-Japan Summit in Brussels with an appearance from Japanese PM Kishida

- French President Macron hosts Indian PM Modi at dinner in Paris

Friday, July 14

Economic Data/Events

- US University of Michigan consumer sentiment

- Bank Earnings from JPMorgan, Citigroup, and Wells Fargo

- Canada existing home sales

- India trade, wholesale prices

- Italy trade

- Japan industrial production

- Poland CPI

- Thailand foreign reserves

- G20 finance ministers and central bank governors meet in India

Sovereign Rating Updates

- EFSF (Fitch)

- ESM (Fitch)

- Ireland (Fitch)

- Spain (Moody’s)

- Iceland (Moody’s)

- Austria (DBRS)

Sunset Market Commentary

Markets:

After yesterday’s US-data inspired bond market sell-off, (bond) markets temporary shifted into a lower gear, awaiting confirmation from the US payrolls report. Still, in the this ‘wait-and-see pause’, the natural drift in yields remained north. ECB speakers in the meantime held to their recent mantra. ECB de Guindos repeated that underlying price pressures remain strong even as most core indicators show some softening. The perfect narrative for keep all options open for September. Chair Lagarde in an interview stressed the need for fiscal authorities to withdraw pandemic support programs. US payrolls were close to expectations. A 209k June job growth combined with a net 110k downward revision for the previous two months was slightl disappointed especially after recent strong data beats. Even so, the unemployment rate again easing from 3.7% to 3.6 only confirmed ongoing labour market tightness. AHE (wage growth) at 0.4% M/M and 4.4% Y/Y even printed on the higher side of expectations. To summarize: the payrolls missed expectations after a strong report last month. The consumer survey printed OK after a soft report last month. In a brief Pavlov reaction, US yields dropped 5 bps +, but markets soon realized that the report in no way pointed to the easing of labour market conditions needed to sustainably slow inflation. The Fed probably remains behind the curve. US yields currently trade mixed with the 2-y easing 4 bps but the 30-y adding 4 bps. Recent peak levels for the 2-y and the 10-y yield touched yesterday, near 5.11% and 4.10% respectively, are still under attack. The German yield curve also re-steepens with the 2-y ceding 4 bps and the 30-y adding 5 bps. On other markets, equities mostly maintained yesterday’s loss. An attempt of the Eurostoxx 50 to reverse some is far from convincing (+0.2 currently). The S&P opens almost unchanged. Oil ($76.5/b) continues fighting the $77/78 resistance, but no break occurred. A (supply-driven) break higher wouldn’t be comforting for the overall inflation narrative.

In FX, the recent relative standstill among the major cross rates continues, with the dollar slightly underperforming. DXY declines to 102.75 (open near 103.05) amongst other driven by a further correction in USD/JPY (142.55 from an open near 144). EUR/USD also gains marginally (1.0915). EUR/GBP (0.8535) is holding within reach of recent lows (0.8518) but no real test occurred yet. CE currencies enter calmer waters after yesterday’s sell-off.

News & Views:

Canadian payrolls beat forecasts in June. Employment increases by 60k, driven by gains in full-time work (+110k). Employment rose in wholesale and retail trade (+33k), manufacturing (+27k), health care and social assistance (+21k) and transportation and warehousing (+10k). Meanwhile, declines were recorded in construction (-14k), educational services (-14k) and agriculture (-6k). The unemployment rate rose to 5.4% as more people searched for work. The participation rate ticked up from 65.5% to 65.7%, matching the highest level since February 2022. Average hourly wages rose 4.2% Y/Y in June, following an increase of 5.1% in May. The loonie rallied after the release with USD/CAD down to 1.332 from 1.338. Canadian swap rates rise by 5.8 bps to 7.5 bps with the belly of the curve underperforming the wings. Canadian money markets almost discount an additional 50 bps of rate hikes by the end of the year (to 5.25%), likely starting with 25 bps next week.

The FAO Food Price Index continued its downtrend in June, averaging 122.3 in June, down from 124 in May. The index is down 23.4% from its peak in March 2022 (159.7). The month-on-month decline in the index in June reflected drops in the indices for sugar, vegetable oils, cereals and dairy products, while the meat price index remained virtually unchanged. For sugar, it’s the first decline following four consecutive monthly increases, mainly triggered by the good progress of the 2023/24 sugarcane harvest in Brazil and a sluggish global import demand, particularly from China, the world’s second largest importer of sugar. The vegetable oil index dropped to the lowest level since November 2020 driven by lower world prices of palm and sunflower oils, more than offsetting higher soy and rapeseed oil quotations..

Gold Struggles to Gain Momentum: Challenges Persist in Precious Metals Sector

The precious metals sector continues to face challenges, as gold has experienced a meager 5.1% increase from January to June 2023. This growth pales in comparison to the indicators seen in the US stock markets. Currently, the price of one troy ounce of gold stands at $1917 as we enter the second half of the year.

One of the key factors weighing on XAUUSD is the upward trend in interest rates, particularly in the US. This trend leads to higher yields in US government bonds and a stronger USD exchange rate. Historically, gold prices have exhibited an inverse correlation with these indicators.

Technical Analysis of XAU/USD:

On the H4 XAU/USD chart, the price has once again rebounded from the moving averages, indicating the development of a bearish trend since May 22, 2023. This price behavior reinforces the strength of the current trend and the ongoing pressure from sellers. The closest support area lies at the level of 1895, and a breakout below this level would pave the way for a decline towards 1860. Technically, this scenario is supported by the MACD, as its signal line has moved out of the histogram area, signaling a decline and the continuation of the bearish trend. It is worth noting the formation of a bullish divergence signal on the MACD indicator on June 30, 2023, when the quotes reached 1935, and the signal was successfully executed.

On the H1 XAU/USD chart, the quotes have broken out of the boundaries of the bullish correction channel. The price is currently below the 200-day moving average, indicating increasing pressure from sellers and a lack of upward movement in the market. There is still potential for a minor bullish correction, with a possible test of the 1915 level before a decline towards 1895 is expected. Technically, this scenario is confirmed by the MACD, as histogram bars have dropped below the July 5, 2023 minimum, nullifying the attempt to form a bullish divergence. A favorable scenario for sellers would be a breakout of the resistance area with the price consolidating above the 1920 level.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0851; (P) 1.0875; (R1) 1.0917; More...

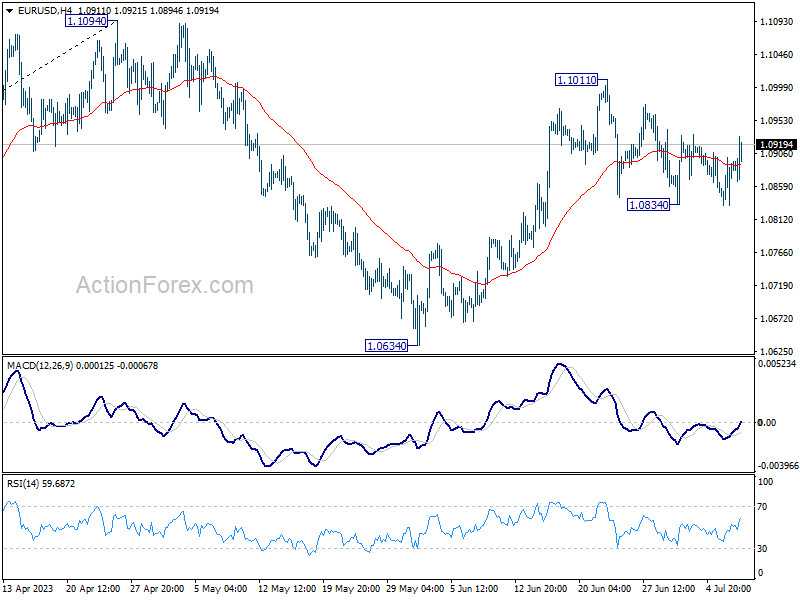

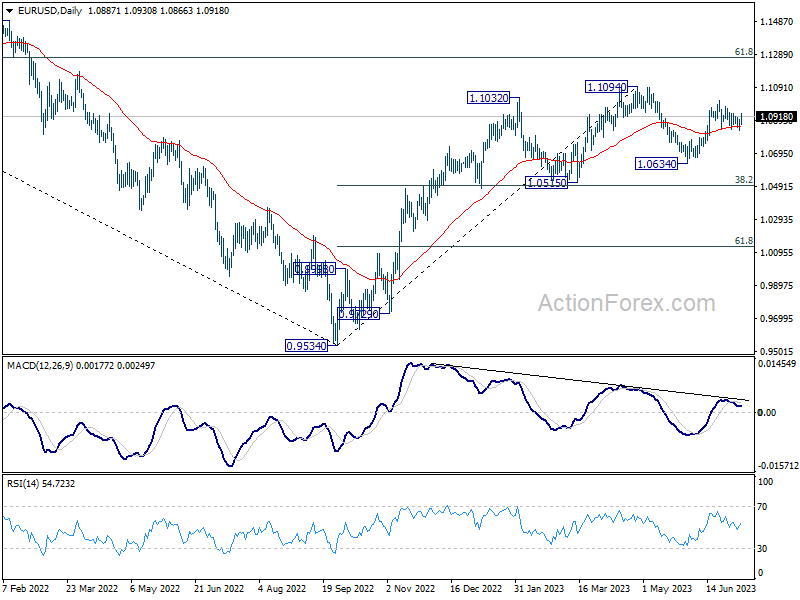

EUR/USD is still bounded in range of 1.0834/1011 despite today's rally attempt. Intraday bias stays neutral, but further rise is in favor. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

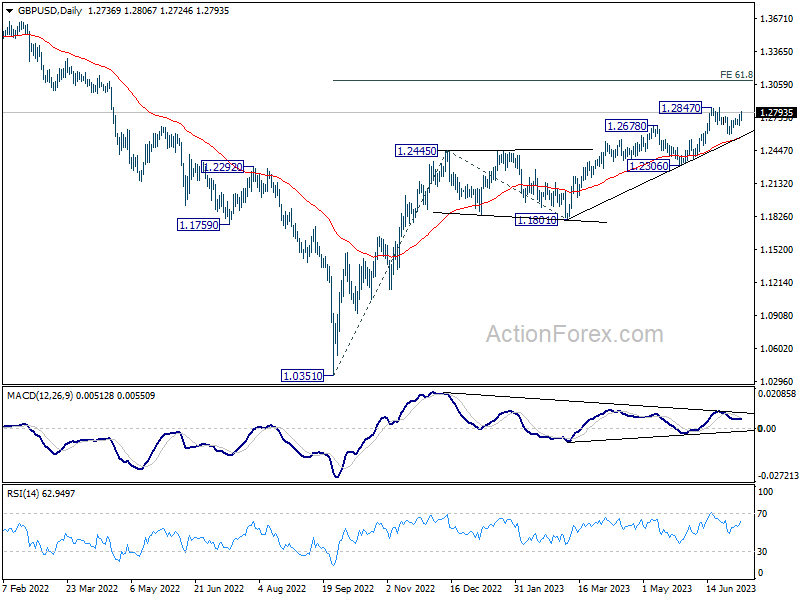

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2682; (P) 1.2731; (R1) 1.2789; More...

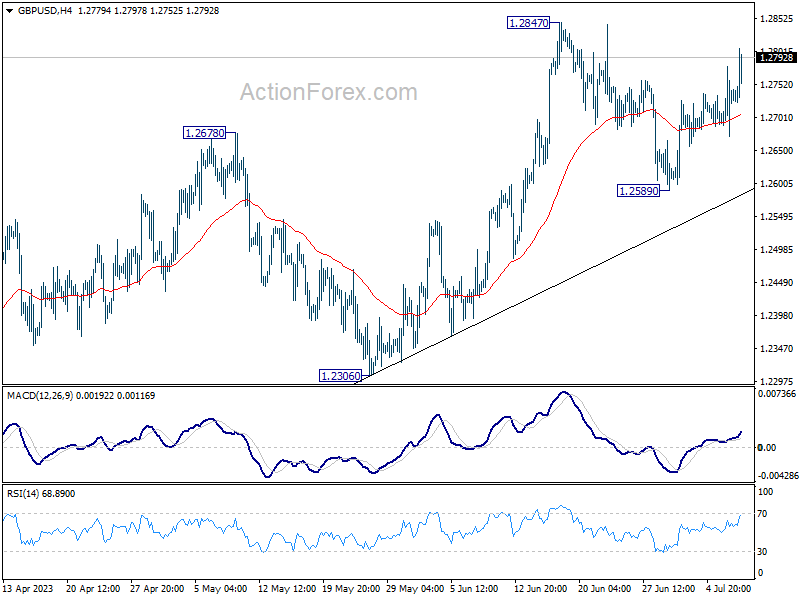

GBP/USD is staying below 1.2847 despite today's rally. Intraday bias remains neutral first. On the upside, firm break of 1.2847 will resume larger up trend from 1.0351 to 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, though, break of 1.2589 will extend the fall from 1.2847 to 55 D EMA (now at 1.2558).

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

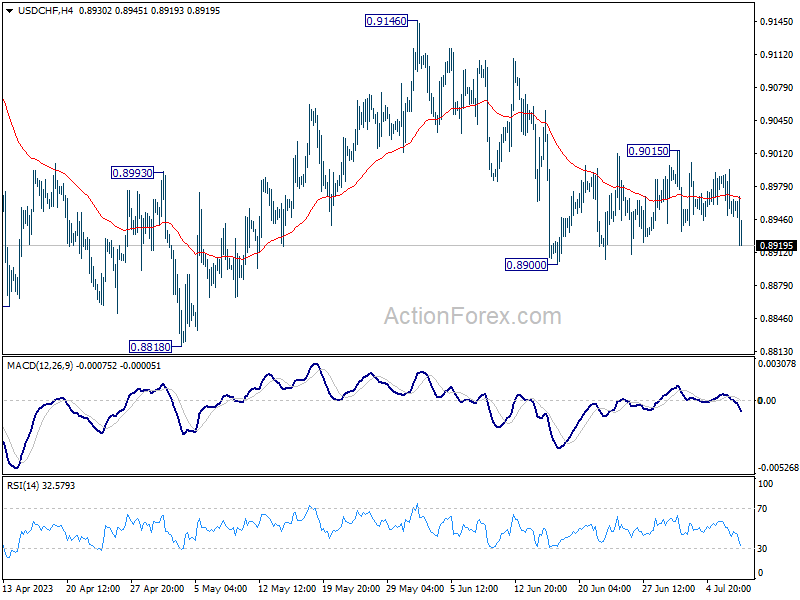

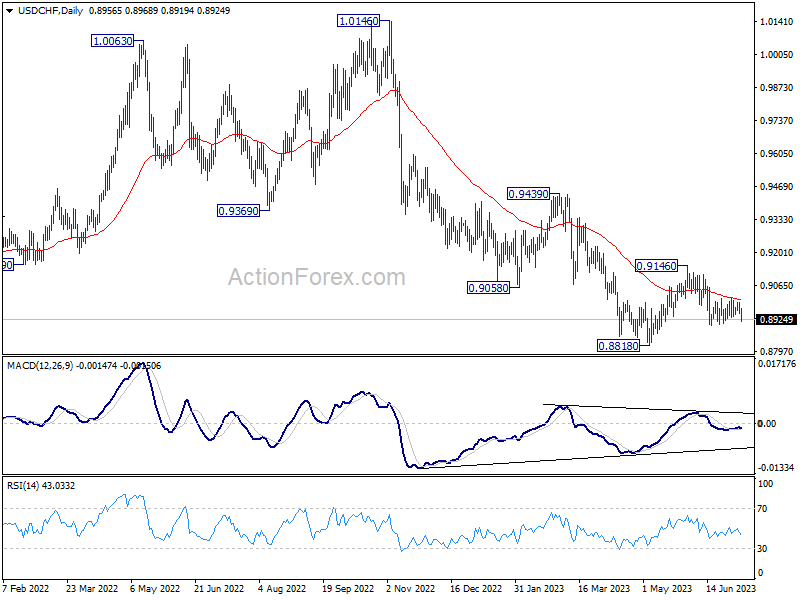

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8936; (P) 0.8968; (R1) 0.8984; More...

USD/CHF dips notably but stays above 0.8900 support for now. Intraday bias stays neutral first while further decline is expected. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. On the upside, above 0.9015 will bring stronger rise towards 0.9146 resistance instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). While further decline cannot be ruled out, strong support is expected from 0.8756 long term support to bring reversal. Firm break of 0.9146 resistance should confirm medium term bottoming.

US: Job Growth Slows in June, Remains Elevated on a Trend Basis

The U.S. economy added 209k jobs in June, slightly below the consensus forecast of 225k. Revisions to the two prior months were negative, subtracting 110k jobs from the previously reported figures.

- Hiring over the last three-months averaged 244k jobs per-month, a step down from the 312k measured over the three-months prior (March-January).

Hiring across the service sector (+120k) in June was the weakest it has been since December 2020 when it shed 339k jobs. Gains were narrowly concentrated in education & healthcare (+73k), leisure & hospitality (+21k), professional & business services (+21k) and 'other' services (+17k). Goods-producing industries (29k) notched a decent gain, with job growth concentrated in construction (+23k) and manufacturing (+7k). Government added 60k jobs last month.

- The breath of hiring – as captured by the diffusion index – narrowed to 58.0, its lowest level in three-months and second lowest of this expansionary cycle.

In the household survey, civilian employment rose by 273k, while the labor force grew by a smaller 133k. As a result, the unemployment rate ticked down 0.1 percentage points to 3.6%. Meanwhile, the participation rate held steady at its cyclical high of 62.6% for the fourth consecutive month.

Average hourly earnings rose 0.4% month-on-month (m/m) – matching May's upwardly revised gain – and are up 4.4% over the past year and an even stronger 4.7% on a three-month annualized basis.

Key Implications

There was plenty of evidence in this morning's report that the labor market is starting to cool. Not only did hiring come in below expectations – a first in fifteen months (!) – but revisions to prior months were also meaningfully lower. The breadth of hiring also narrowed considerably. It's important to note, however, that we are still very early stages. Hiring over the past three-months is still running at a pace that's nearly three times what's required to meet trend growth in the labor force.

Beyond the hiring numbers, signals on the inflation front remain somewhat mixed. While the optimist may point to average hourly earnings having slowed on a trend basis over the past year, the pessimist could counter with progress having stalled more recently. Moreover, other more comprehensive measures of wage growth including the Atlanta Fed's wage tracker and the Employment Cost Index (ECI) both continue to run well above average hourly earnings. We'll get the Q2 ECI reading on July 28th, and it will be interesting to see if it shows any recent signs of wage pressures easing.

Despite the early signs of cooling, the labor market remains far too tight. Taken alongside the recent strength across other key economic indicators (i.e., housing starts, home sales, new orders of capital goods) all point to an economy that's still running far too hot to cool inflation. With nearly all Fed officials supporting a more restrictive policy rate, another 25-basis point rate hike later this month seems inevitable.