Sample Category Title

USD Struggles to Recover

USD/CHF attempts to bounce

The US dollar slipped after soft ISM manufacturing data in June. Following a pop above the psychological level of 0.9000, a brief pullback was contained at 0.8940, a key demand zone near a series of recent lows. A break above 0.9015 on the 30-day SMA would signal that the bulls have regained control of the price action and open the door to 0.9110 right under the May peak (0.9140), a last step before a broader recovery in the medium-term. On the downside, 0.8900 is critical in keeping the rebound mode intact.

GBP/USD tests resistance

Cable finds some support as expectations for UK peak rates exceed 6%. The latest retracement has met bids in the congestion area formed by the daily resistance–turned-support of 1.2600 and the 30-day SMA. A bullish RSI divergence indicates a slowdown in the sell-off momentum and may attract more long interests in this key demand zone. 1.2760 is the first hurdle and its breach would make the pair retest the recent high of 1.2850. Otherwise, a fall below 1.2600 would trigger a new round of sell-off towards 1.2500.

GER 40 probes support

The Dax 40 softened over a contraction in the region’s manufacturing activity last month. The price action continues to capitalise on its break above the psychological level of 16000. The support-turned-resistance of 16290 at the start of the mid-June correction could be sellers’ last stronghold as its breach would signal a bullish continuation towards a new all-time high. As the RSI drops back into the neutral area, 16000 near the base of the bullish breakout is the first level to expect follow-through bids while 15770 is a critical floor.

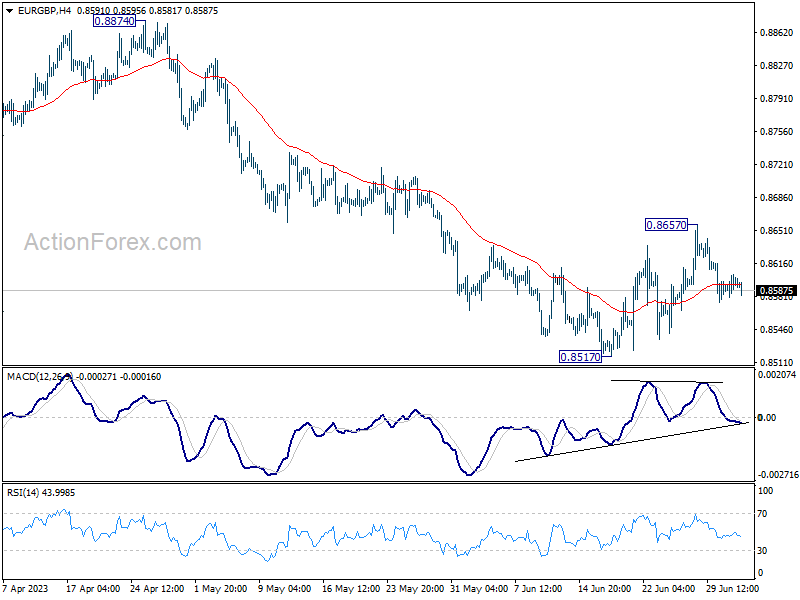

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.85868573; (P) 0.8595; (R1) 0.8610; More...

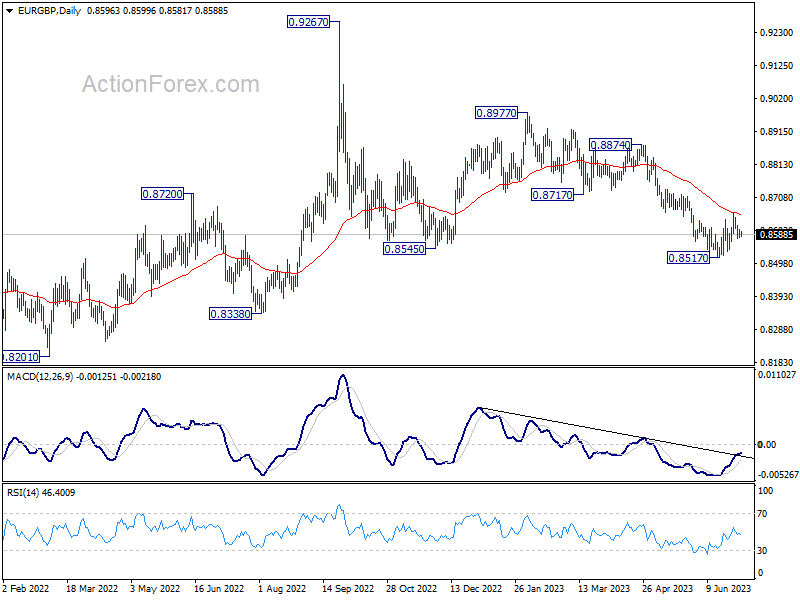

EUR/GBP is staying in consolidation from 0.8517 and intraday bias stays neutral. On the downside, break of 0.8517 will resume the whole fall from 0.8977. On the upside, above 0.8657 resistance will resume the rebound from 0.8517 towards 0.8717 support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

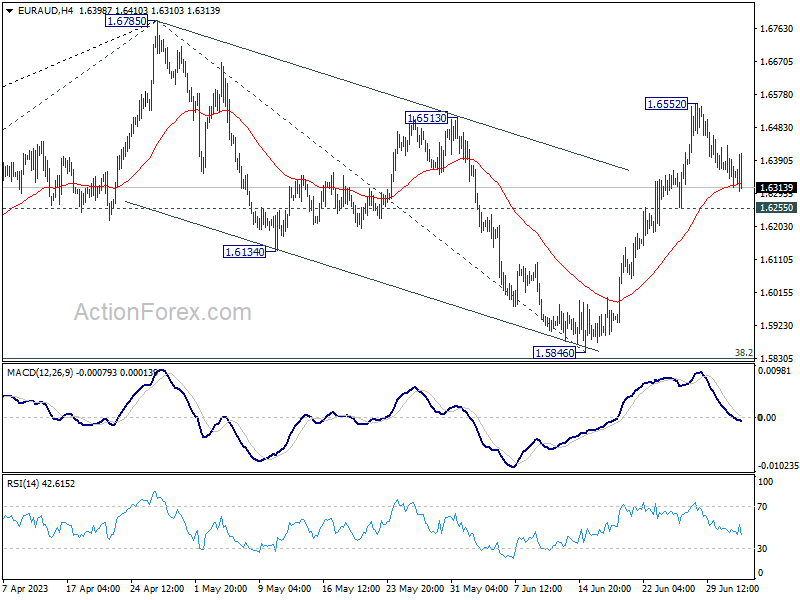

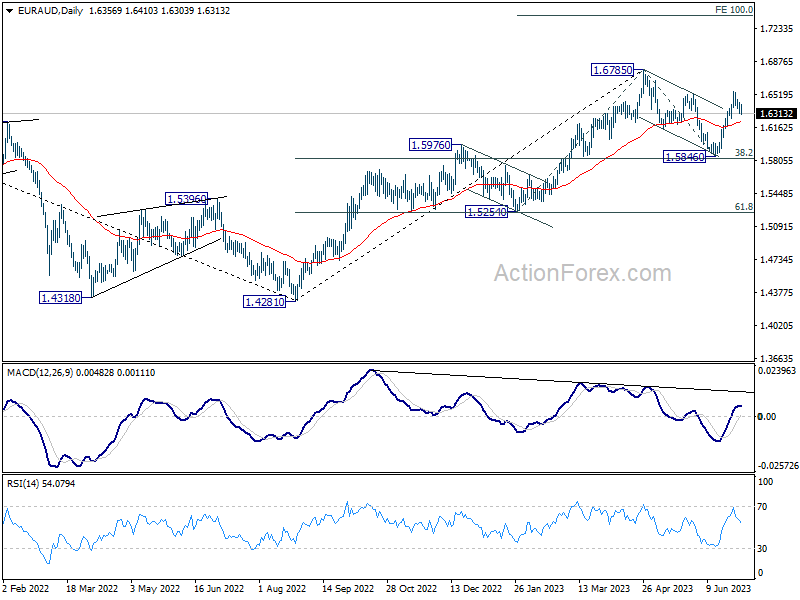

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6303; (P) 1.6369; (R1) 1.6421; More...

Intraday bias in EUR/AUD remains neutral as retreat from 1.6552 is extending. But further rally is expected with 1.6255 support intact. As noted before, correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, break of 1.6255 will dampen this view and turn bias to the downside for 1.5846 support.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.46; (P) 157.71; (R1) 158.16; More....

Intraday bias in EUR/JPY remains neutral for consolidation below 157.99. In case of another dip, further rally is still expected as long as 154.03 support holds. On the upside, break of 157.99 will resume larger up trend to 162.82 projection level. However, break of 154.03 will argue that larger correction is under way back to 151.60 resistance turned support.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 151.60 resistance turned support holds, even in case of deep pull back.

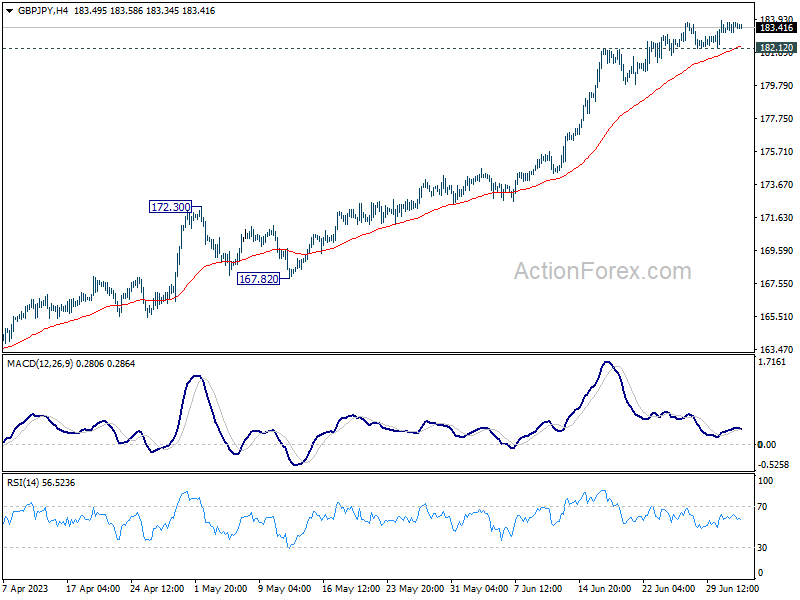

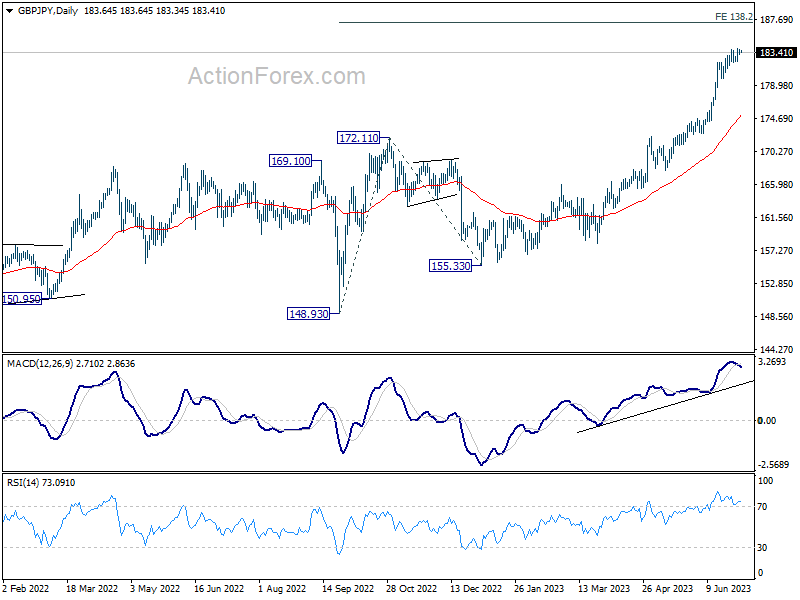

GBP/JPY Daily Outlook

Daily Pivots: (S1) 182.36; (P) 183.12; (R1) 184.03; More...

No change in GBP/JPY's outlook and intraday bias remains mildly on the upside for the moment. Current up trend should target 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36. On the downside, break of 182.12 minor support will turn bias back to the downside for deeper pull back first.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

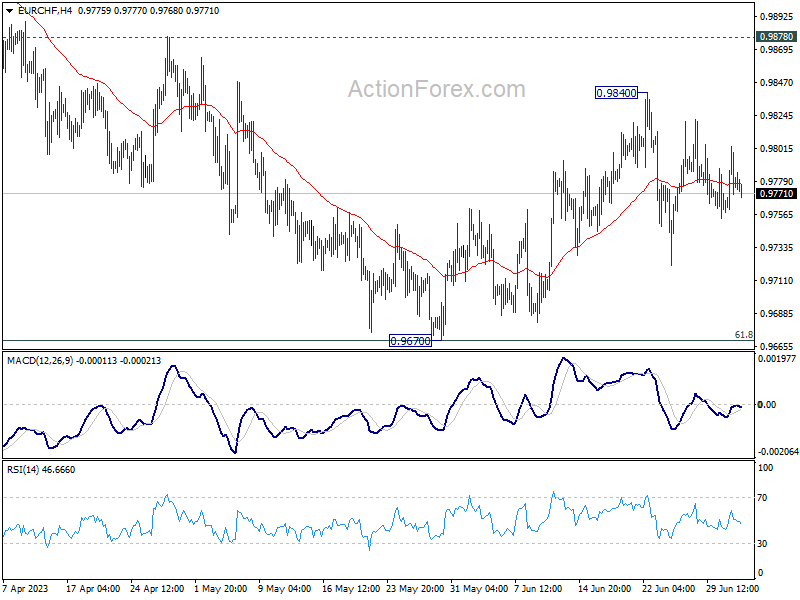

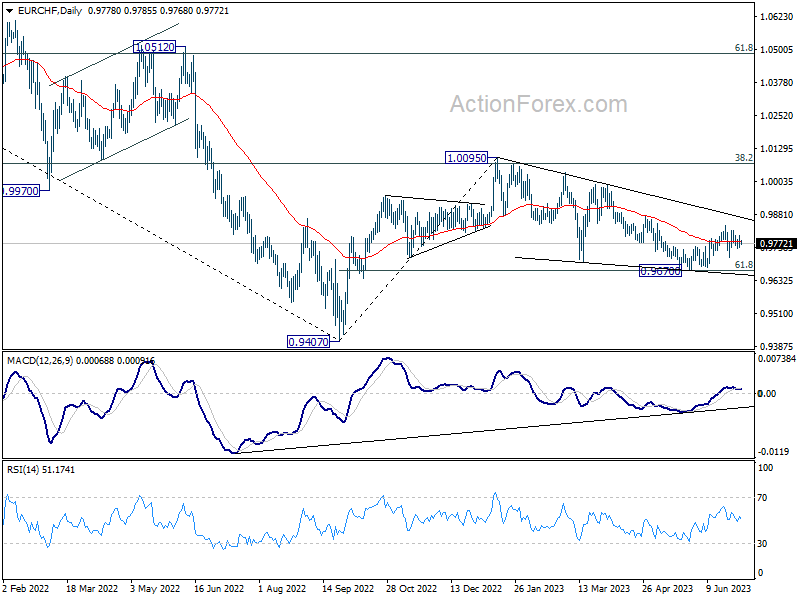

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9759; (P) 0.9782; (R1) 0.9804; More...

Intraday bias in EUR/CHF remains neutral as range trading continues. On the upside break of 0.9840 will resume the choppy rebound from 0.9670. That will also revive the case that whole corrective decline form 1.0095 has completed at 0.9670. Further rally should be seen to 0.9878 resistance next. However, sustained trading below 0.9670 will resume the whole fall from 1.0095.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

RBA Board Pauses in July, to Take More Time to Assess the Outlook

The Board has paused but the reasons we have given to support our call for a hike in July remain. Target terminal rate still 4.6% with 25bp hikes expected in both August and September.

The Reserve Bank Board held the cash rate steady at 4.1% at its July meeting.

The reason was: “to provide some time to assess the impact of the increase in interest rates to date and the economic outlook”.

This is the same wording used following the decision to pause in April.

Reference to the outlook seems related to the Board awaiting the staff’s revised forecasts that will be available for the meeting in August.

Note the recent pattern: a pause in January (when there was no meeting); increases in the next two months – February and March; a pause in April – increases in the next two months – May and June; and a pause again in July.

April and July are the months immediately preceding the quarterly inflation report and the Statement on Monetary Policy, which sees the staff update its forecasts for the Board.

Westpac lifted its forecast for the terminal rate to 4.6% following what appeared to be a clear rebalancing of the Board’s reaction function at the June Board meeting – placing central emphasis on containing inflation pressures and wage/price expectations and less on protecting the employment gains since the pandemic.

This point continues to be emphasised in the Governor’s decision statement, which abandoned the concept that had been used in previous statements – “The Board is seeking to keep the economy on an even keel …” – in favour of a more cautious: “The Board is still expecting the economy to grow …”.

Westpac had expected the Board to raise rates again in July, reflecting this assessed change in its reaction function and the data flow, which has included evidence of an ongoing tight labour market; emerging wage pressures; sticky underlying inflation; and a sustained upswing in the housing market.

Of most significance was the Deputy Governor defining the Bank’s measure of full employment as 4.5% – the rate required to achieve the inflation target – which is a long way from the 3.55% that printed in May.

The decision by the Board to pause pending further data does not change the assessment that further tightening is required, including our expectation that the terminal rate will need to reach 4.6%. Notably, the line that “Some further tightening of monetary policy may be required …” was repeated in the July Governor’s statement, having been omitted in the minutes to the June meeting but included in the June decision statement.

The language remains consistent with rate increases of 0.25% in both August and September, which is now our call.

But unlike the pattern we have seen so far this year we do not expect a follow-up hike in November after the next pause in October.

Our forecasts suggest progress on bringing down inflation, and evidence of some easing in labour market conditions and of very weak demand will allow the Board to remain on hold after September. The opportunity to ease policy will eventually come once the Board is confident that a sustained return to low inflation has been achieved.

We confirm our call that, following the hikes in August and September, rates will remain on hold until May next year when conditions will allow the Board to begin easing.

Conclusion

The clear signal from the June Board meeting that motivated our call for a follow-up move in July has been tempered by today’s decision to pause. Despite this, there remains a strong case for rates to go higher, a message that is still apparent in the Governor’s decision statement.

Following the June meeting we raised our forecast for the terminal rate to 4.6%. That still holds, with hikes now coming in August and September, but thereafter we expect that the evidence will be clear enough that the Board can be patient as inflation pressures ease and the economy stagnates.

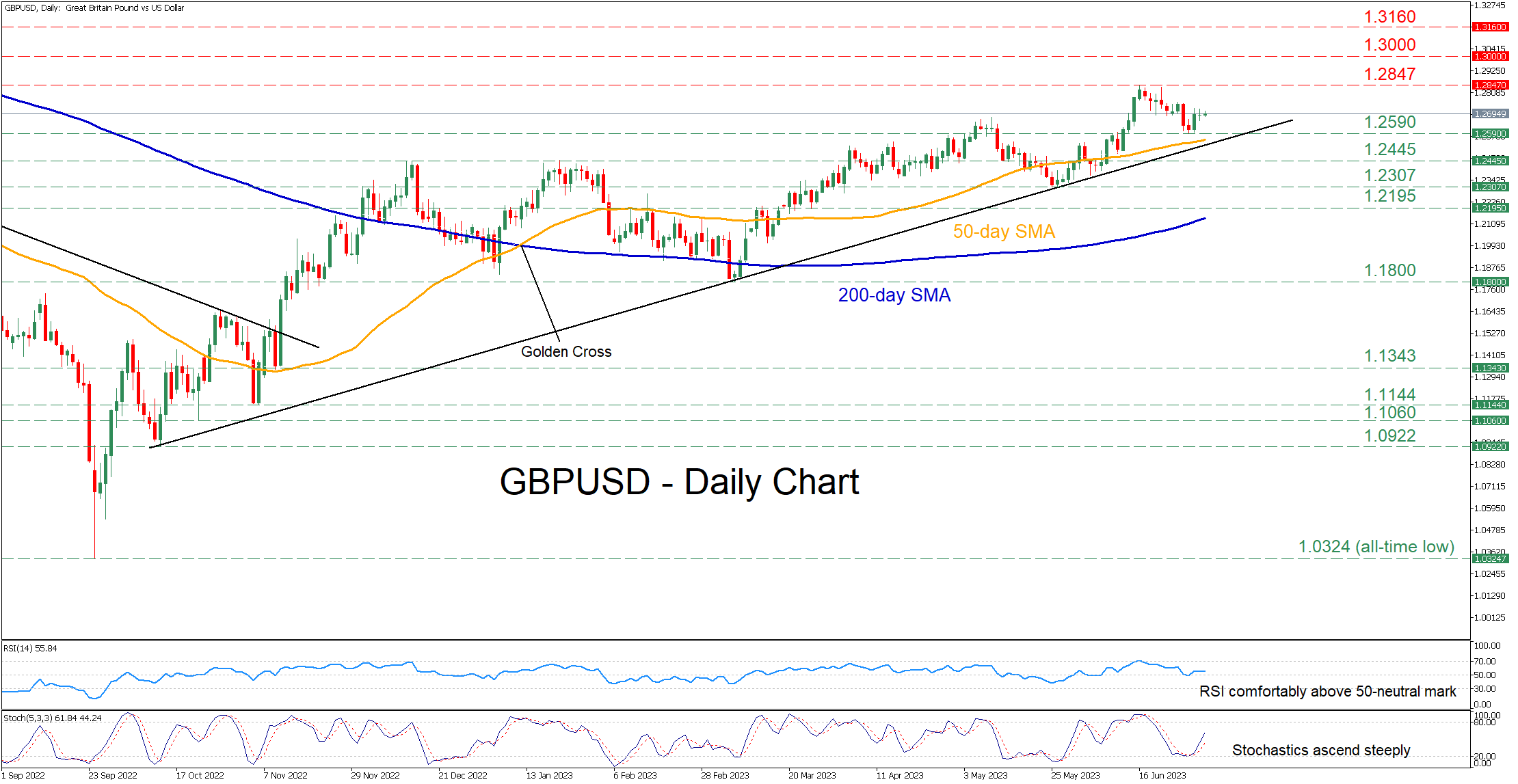

GBPUSD Regains Traction after Correction Pauses

GBPUSD has been in a prolonged uptrend since October 2022 supported by its long-term ascending trendline. In the near term, the pair experienced a pullback from its 14-month high of 1.2847, but it quickly found its feet and reversed back higher.

Despite the recent downside correction, the momentum indicators are tilted to the bullish side. Specifically, the RSI is flat after bouncing off its 50-neutral mark, while the stochastics are edging higher following their bullish cross near the oversold territory.

If the latest rebound extends, the focus could turn to the recent 14-month peak of 1.2847. Jumping to a fresh multi-month high, the price might encounter resistance at the crucial 1.3000 psychological mark. Surpassing that zone, the pair might ascend towards the March 2022 low of 1.3160, which could serve as resistance in the future.

Alternatively, if the price reverses lower, the recent support of 1.2590 could act as the first line of defense. Should that floor collapse, the pair may face the ascending trendline that connects its lows since October 2022 and the 50-day simple moving average before the 1.2445 resistance gets tested. A violation of that region could set the stage for the May bottom of 1.2307.

Overall, GBPUSD appears to have undergone a healthy correction due to reaching overbought conditions, with its positively charged SMAs painting a bullish technical picture. Therefore, it is likely that the pair extends its structure of higher highs as long as it holds above the ascending trendline.

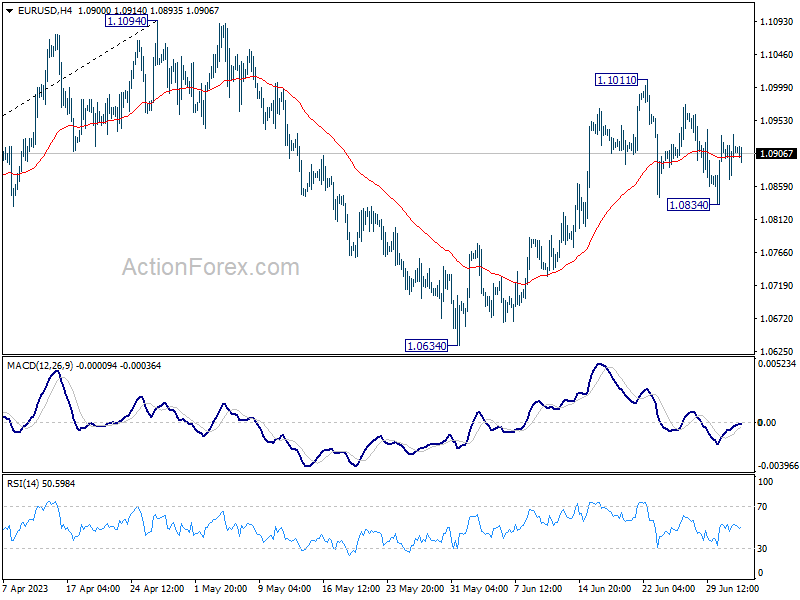

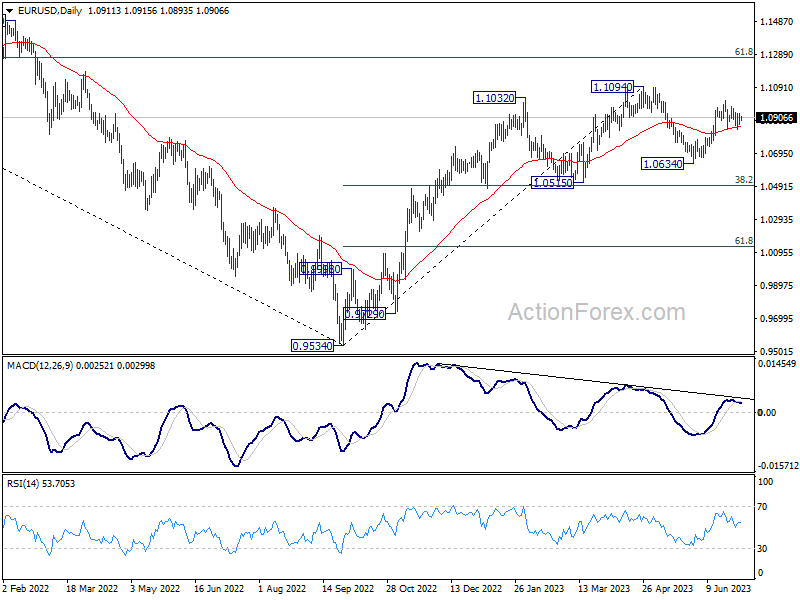

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0878; (P) 1.0906; (R1) 1.0942; More...

EUR/USD is staying in range below 1.1011 and intraday bus stays neutral. Further rally is mildly in favor with 55 D EMA (now at 1.0852) intact. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

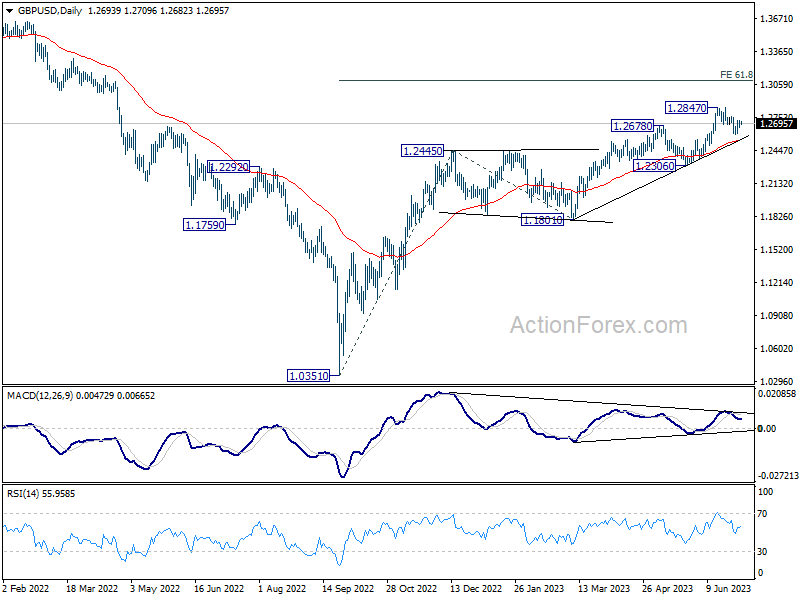

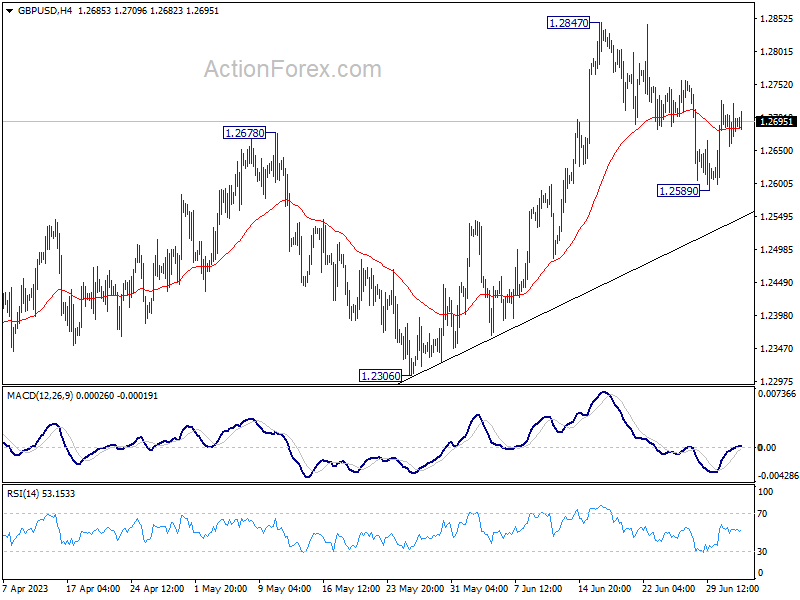

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2659; (P) 1.2691; (R1) 1.2723; More...

Intraday bias in GBP/USD remains mildly on the upside and rebound from 1.2589 would target retesting 1.2847 high first. Firm break there will resume larger up trend from 1.0351, to 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, though, break of 1.2589 will extend the fall to 55 D EMA (now at 1.2541).

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).