Sample Category Title

Sunset Market Commentary

Markets

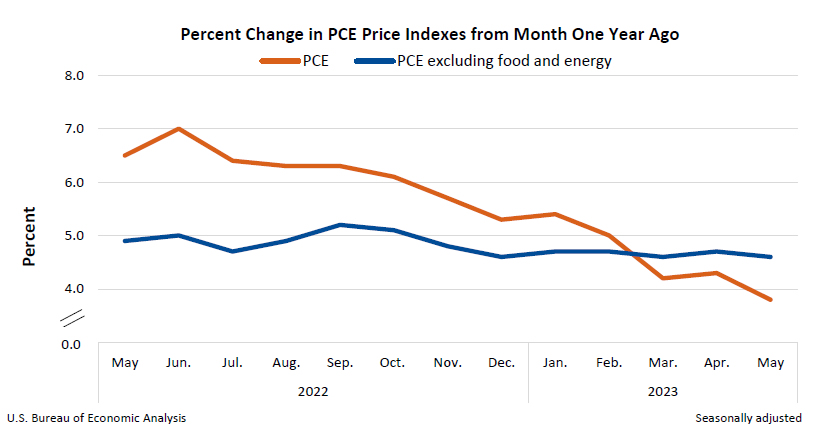

EMU June inflation data brought no big surprise anymore in the wake the of the releases from Germany and other EMU member states earlier this week/today. The story in the meantime is well-known. Headline inflation declined further from 6.1% to 5.5% mainly driven by lower energy prices. At the same time, the core measure (excluding energy, food alcohol and tobacco) reaccelerated from 5.3% to 5.4%. Food price inflation remains elevated (11.7% from 12.5%). Services prices continue trending ever higher (5.4% from 5.0%). The CPI release had little direct impact on European bond markets. In a technical reaction, yields even temporarily declined a few basis points. In a broader perspective, persistent core/services inflation leaves the ECB no choice but to hike rates further in July with September also a live meeting. Similar story from the US May PCE deflators. The headline slowed to 0.1% M/M and 3.8% Y/Y (0.4% M/M, 4.3% Y/Y in April). The core deflator printed at 0.3% M/M and 4.6% Y/Y (from 4.7%). The indicators were close to expectations. May Personal income at 0.4% was marginally stronger than expected but spending disappointed slightly at 0.1% M/M. After yesterday’s strong post-claims jump in yields, today’s data provided no strong enough driver to really extend the uptrend. US yields currently change less than 2 bps (2-y + 1 bp/30-y -1.5 bp) ceding less than 2 bps across the curve. The 10-y yield (3.83%) attacked the 3.86% resistance (top end May) but at last for now fails to clear this hurdle. German yields are rising 3-2 bps. The German 2-y is testing recent top near 3.22%. The decline in the headline inflation for now apparently is enough to give comfort to equity investors. The Euro Stoxx 50 adds 1.0%+, again nearing the Mid May top (4413). US indices also open higher (S&P + 0.9%, Nasdaq +1.25%) Oil ($74.75 p/b) is returning higher in the $70 -79 consolidation pattern.

On FX markets, yesterday’s post-jobless claims USD rally is largely undone. DXY drops back below the 103 area from an open near 103.33. The euro also restores the balance. EUR/USD tested the 1.0945 support but the test was rejected with the pair returning to the 1.09+ area. USD/JPY eases slightly to 144.45 after testing the 145 barrier in Asia this morning as traders ponder the changes for interventions from the Japanese Ministry of finance. EUR/GBP is drifting back below the 0.86 handle as UK short-term yields (2-y +7.5 bps testing the 5.32% top) continue pushing higher. The risk-on sentiment hardly supports the likes of the Norwegian (EUR/NOK 11.70) or the Swedish krone (EUR/SEK 11.79).

News & Views

Polish inflation flatlined for a second month straight in June, data from Statistics Poland showed. The 0% m/m reading brought the yearly figure from 13% to a lower-than-expected 11.5%. Food (-0.3%), energy (-0.3%) and fuel (-0.9%) all fell on a monthly basis. Additional details aren’t available before the publication of the final figure July 14. Core inflation numbers are due for release July 17 but early analyst estimates range between 10.7-11.1%, down from 11.5% in May. KBC Economics expects an outcome of 10.5%. The Polish zloty barely budged on today’s data. EUR/PLN did hit an intraday high around 4.46 before paring gains and even trading lower for the day at 4.438 currently.

The Chinese currency is on track for its third monthly decline straight, making the current quarter the second worst since the country dropped the dollar peg in 2005. USD/CNY (7.26) today again gains with the pair closing in on the November 2022 highs – in turn the strongest level since 2007. At the heart of the matter lie investor concerns over the Chinese economy. Performance has underwhelmed in recent months following a boost early this year after China ditched its strict zero-Covid policy. Domestic spending has faded with debt-laden and wary consumers trying to keep their finances in check. Foreign demand, meanwhile, has also eased due to the ongoing global monetary tightening effort. The opposite is happening in China with the central bank in a gradual easing mode to support the economy. This growing monetary divergence is weighing heavily on the yuan. In growing evidence of the PBOC becoming uncomfortable with the weak currency, it fixed the exchange rate several times stronger than expected in recent days. Regulators also surveyed exporters, importers and banks about money flows and hedging demand and collected views on the yuan and trading sentiment, Bloomberg reported citing people familiar. The PBOC today also released an announcement, vowing to keep the yuan basically stable at a reasonable and balanced level.

US: Income Higher, Spending Flat, Prices Slowing but Still Elevated in May

Personal income grew 0.4% month-on-month (m/m) in May, just above market expectations (0.3%). This marked a slight acceleration from the prior month's downwardly revised gain of 0.3% (previously 0.4%). Gains were led by compensation to employees, which rose 0.5% in May – up from 0.4% in April.

Accounting for inflation and taxes, real personal disposable income rose 0.3% m/m, accelerating from a -0.1% decline the previous month.

Personal consumption expenditures rose 0.1% m/m, a marked deceleration from the 0.6% gain in April (revised lower from 0.8%). May's reading came in just below market expectations for 0.2% growth.

- Expenditures on services decelerated to 0.4% m/m (from a downwardly revised 0.5% in April). Spending on healthcare was the primary contributor to movements in the services category.

- There was a marked decline in goods spending. Goods spending fell by 0.5% m/m, a big step down from the 0.9% growth posted in April. There was a decline in spending on both durables (-0.9%) and non-durables (-0.3%).

Adjusting for inflation, real spending was flat on the month, coming in just below the consensus estimate for a 0.1% gain. In real terms, goods spending was down -0.4% m/m, while services were up 0.2%.

The personal consumption expenditure (PCE) price deflator rose 0.1% m/m, and 3.8% on a year-on-year (y/y) basis – right in line with market consensus forecast and below April's reading (4.3% y/y).

The core PCE price deflator (which excludes food and energy and is the Fed's preferred measure of inflation) rose 0.3% m/m, again in line with the consensus forecast and below April's reading (0.4%). On an annual basis, core PCE inflation decelerated to 4.6% y/y from 4.7% y/y the month prior. The measure has not gone below 4.6% over the last six months.

The personal saving rate was 4.6% in May, which was 0.3%-pts above the upwardly revised 4.3% reading in April.

Key Implications

Consumers continue to be a pillar of support for the US economy. Nevertheless, they are coming under increasing pressures, with high prices, tightening credit and other indicators pointing to a slowdown on the way. With data in for the first two months of the quarter, growth of real consumption expenditure is expected to decelerate from an upwardly revised 4.2% (annualized) in 2023 Q1 to about 1.3% in Q2.

The stickiness of core PCE inflation continues to be the proverbial bee in the bonnet of policymakers at the Fed. Given that lingering worries around the recent regional banking crisis have largely abated, and the debt ceiling question has been settled for now, the Fed has a clearer path for setting policy at their July meeting. Despite keeping rates steady at the June meeting, it has clearly signaled its willingness to increase rates further, should inflation remain persistently above target. Today's print has done very little to weaken that resolve. In fact, the market continues to expect that the Fed will raise rates by 25bps at their next meeting. If they do, it would take the policy rate to a 22-year high – the last time the rate was at 5.5% was in January 2001.

Canada’s Economy Stalls in April, But Swift Rebound Likely in May

The Canadian economy flatlined in April, coming in below Statistics Canada and consensus estimates of 0.2% month-on-month (m/m). However, the disappointment is somewhat offset by a one tick upgrade to March, and a flash estimate pointing to a healthy rebound of +0.4% m/m in May.

April's reading was mixed, with output expanding in 11 of 20 industries. Services-producing industries remained effectively flat for a third straight month, while goods-producing industries rebounded to 0.1% m/m, after a slight contraction in March.

The gain on the goods side was led by oil and gas extraction (+2.1% m/m), helping the broader mining, quarrying, and oil & gas sector rise for a fourth straight month. Partially offsetting growth in goods sectors was a 0.6% m/m contraction in manufacturing, driven by chemical manufacturing (-2.6%).

As anticipated, cumulative services activity was dragged down by the public administration sector (-1.0% m/m) on the back of April's federal public sector worker strike. The real estate and rental and leasing sector provided a partial offset, expanding 0.5% m/m driven by strength in the housing resale market. Transportation and warehousing was up 0.4% m/m.

Estimated growth of 0.4% m/m for May would mark the largest gain since January 2023. The gain is likely to be derived from a rebound in federal government public administration, as well as activity in manufacturing and wholesale sectors.

Key Implications

Canadian GDP surprised to the downside, but details didn't flash any major warning signs. With today's print and the flash estimate for May, second quarter GDP growth is tracking around a trend pace. This would once again overshoot the Bank of Canada's (BoC) most recent 1.0% annualized estimate for Q2 growth.

The BoC is waiting for a few more key markers before making their policy decision on July 12, notably June jobs data next week. In our view, today's GDP print doesn't change the balance of risks towards another quarter-point hike of the policy rate at next meeting–markets are split down the middle on the odds of a hike. We think that ongoing strength in economic activity, a still-tight labour market, and inflation above target tips the likelihood towards a 25 bps hike to 5.00% in July.

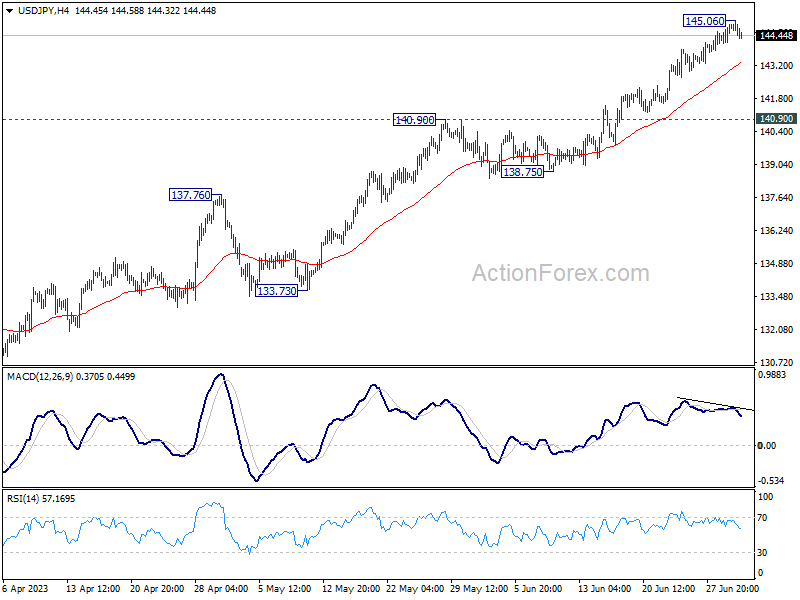

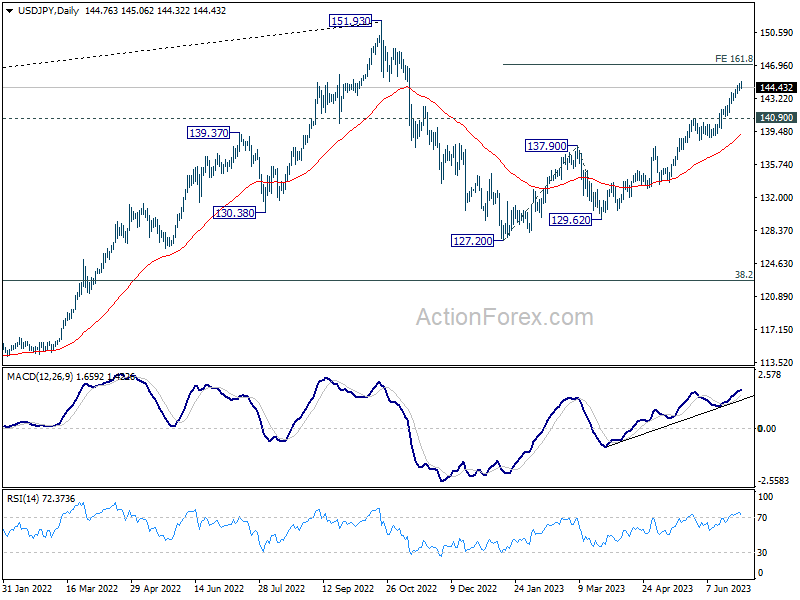

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.31; (P) 144.61; (R1) 145.08; More...

Intraday bias in USD/JPY is turned neutral with current retreat. Some consolidations would be seen first, but further rally will remain in favor as long as 140.90 resistance turned support holds. On the upside, break of 145.06 will resume larger rise to 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 137.90 resistance turned support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 137.90 will indicate the the third leg has started back towards 127.20.

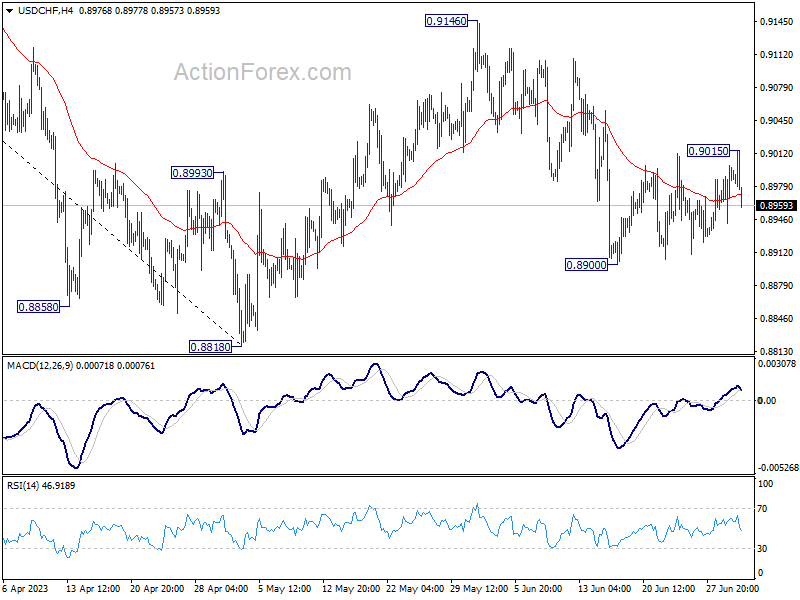

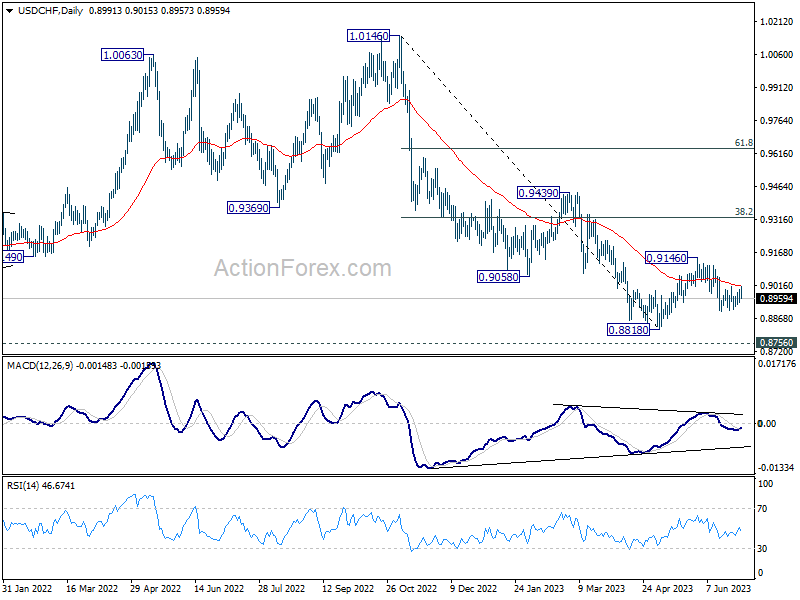

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8959; (P) 0.8980; (R1) 0.9018; More...

USD/CHF reverses quickly after edging higher to 0.9015 and intraday bias remains neutral first. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. But for now, strong support is still expected from 0.8756 long term support to bring rebound. On the upside, above 0.9015 will bring stronger rise towards 0.9146 resistance.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

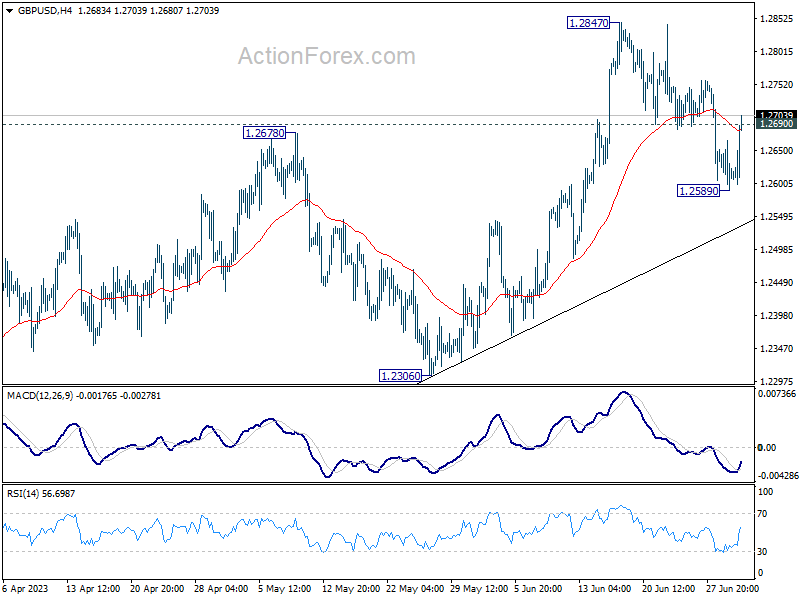

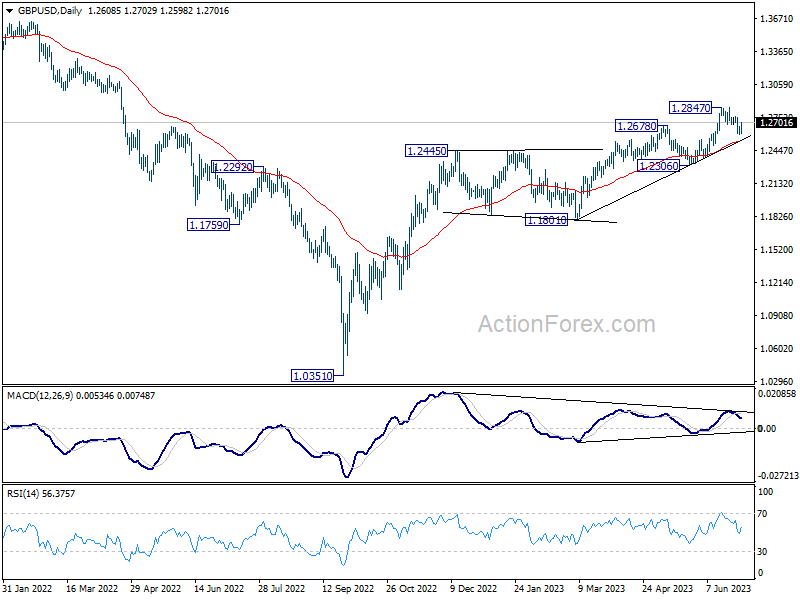

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2623; (R1) 1.2656; More...

Break of 1.2690 minor support suggests that GBP/USD's pull back from 1.2847 has completed. Intraday bias is back on the upside for retesting 1.2847 first. Firm break there will resume larger up trend from 1.0351. On the downside, though, break of 1.2589 will extend the fall to 55 D EMA (now at 1.2529).

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

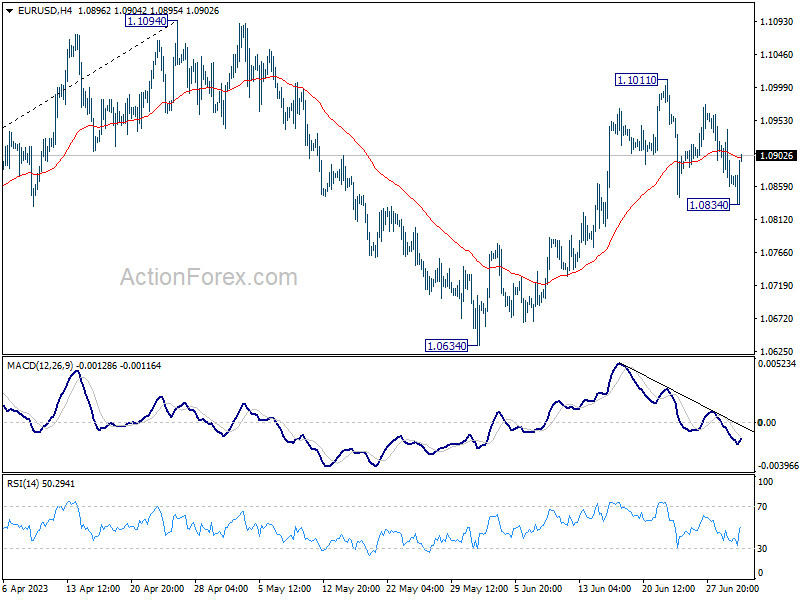

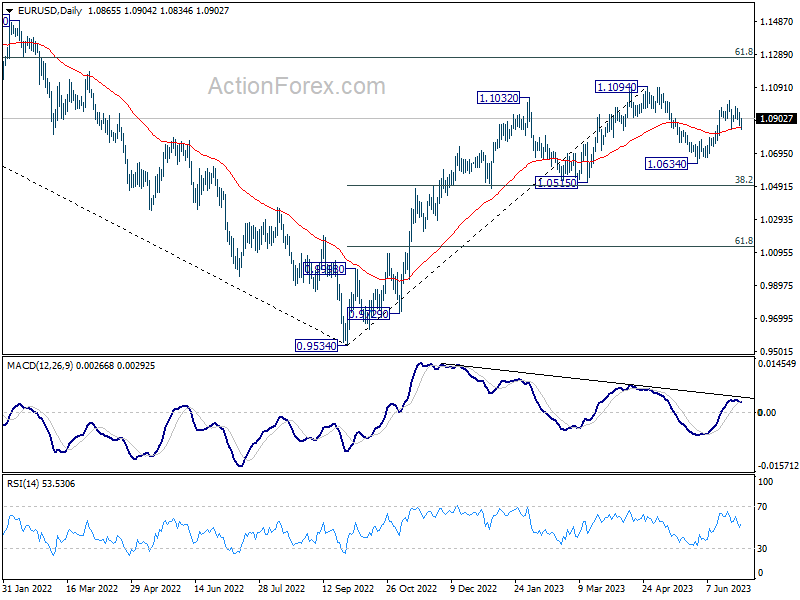

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

EUR/USD dipped to 1.0834 earlier today but quickly recovered. It's still trying to defend 55 D EMA. Intraday bias stays neutral first. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Dollar Dips as Headline and Core PCE Inflation Slowed

Dollar sees a significant dip in early US session after release of economic data showed a slower than expected headline PCE inflation and a slight decline in core PCE inflation. In contrast, Eurozone reported a tick up in core inflation for the same period. Stock futures rally on this news, while benchmark treasury yields dip Overall, the data, at least, doesn't lend support to more aggressive tightening by Fed.

As the month draws to a close, both Yen and Greenback are poised to end as the worst performers. Despite a slight hiccup in response to today's disappointing data, Canadian Dollar takes the crown as the strongest performer for the month, with Aussie Dollar taking the runner-up position, despite widespread selloffs this week. European majors are showing a mixed performance, with no clear winner among them.

In Europe, at the time of writing, FTSE is up 0.89%. DAX is up 1.25%. CAC is up 1.28%. Germany 10-year yield is down -0.014 at 2.408. Earlier in Asia, Nikkei dropped -0.14%. Hong Kong HSI dropped -0.09%. China Shanghai SSE rose 0.62%. Singapore Strait Times dropped -0.04%. Japan 10-year JGB yield rose 0.0161 to 0.400.

US PCE price index slowed to 3.8% yoy, core PCE down to 4.6% yoy

US personal income rose 0.4% mom, or USD 91.2B, matched expectations. Personal spending rose 0.1% mom, or USD 18.9B, below expectation of 0.2% mom.

Headline PCE price index rose 0.1% mom, below expectation of 0.5% mom. PCE core (excluding food and energy) rose 0.3% mom, below expectation of 0.4% mom. Goods prices fell -0.4% mom while services price rose 0.2% mom. Food prices rose 0.1% mom. Energy prices fell -3.9% mom.

From the same month one year ago, headline PCE price index slowed from 4.3% yoy to 3.8% yoy, below expectation of 4.6% yoy. PCE core (excluding food and energy) ticked down from 4.7% yoy to 4.6% yoy, matched expectations. Goods prices rose 1.1% yoy while services prices jumped 5.3% yoy. Food prices rose 5.8% yoy and energy prices decreased -13.4% yoy.

Also released, Canada GDP was unchanged for the month in April, below expectation of 0.2% mom growth. Goods-producing industries rose 0.1% mom while services-producing industries were flat. Overall, 11 of 20 industrial sectors posted increases.

Eurozone CPI slowed to 5.5% yoy in Jun, CPI core rose to 5.4% yoy

Eurozone CPI slowed from 6.1% yoy to 5.5% yoy in June, below expectation of 5.6% yoy. CPI core rose from 5.3% yoy to 5.4% yoy, matched expectations.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate(11.7%, compared with 12.5% in May), followed by non-energy industrial goods (5.5%, compared with 5.8% in May), services (5.4%, compared with 5.0% in May) and energy (-5.6%, compared with -1.8% in May).

Eurozone unemployment rate unchanged at 6.5%, EU down to 5.9%

Eurozone unemployment rate was unchanged at 6.5% in May, matched expectations. EU unemployment rate ticked down from 6.0% to 5.9%.

Eurostat estimates that 12.937m persons in the EU, of whom 11.014, in Eurozone, were unemployed in May 2023. Compared with April 2023, unemployment decreased by -75k in the EU and by -57k in Eurozone.

Swiss KOF fell to 90.8, third decline in a row

Swiss KOF Economic Barometer dropped slightly from 91.4 to 90.8 in June, above expectation of 89.2. That's the third consecutive monthly decline.

KOF said: " The downward movement in the Barometer is primarily caused by bundles of indicators that capture foreign demand. Here, the outlook continues to deteriorate.

"The indicators covering private consumption and the economic sector of other services also give a slightly negative signal. The indicators for manufacturing and construction, on the other hand, point slightly in a positive direction."

Japan industrial production down -1.6% mom in May on vehicle sector

Japan's industrial production recorded a sharper decline than anticipated, dropping by 1.6% mom in May. This marked the first contraction in four months, surpassing expectations of -1.0% decrease. According to survey by Ministry of Economy, Trade and Industry, manufacturers forecast industrial output to recover by 5.6% in June, only to fall again by -0.6% in July.

Among the 15 industrial sectors, 12 reported falling output, with only three seeing rise in production. Notably, motor vehicle sector bore the brunt of the decline, experiencing substantial -8.9% slump from the previous month, with passenger cars and auto body parts being the significant contributors.

Also released, the country's unemployment rate remained unchanged at 2.6%, as expected. The number of jobless individuals decreased by -30k from the prior month, standing at 1.77 million. However, the Ministry of Health, Labor and Welfare revealed a slight downturn in the job market, with ratio of job openings to job seekers in May dropping to 1.31, down 0.01 point from April.

Meanwhile, Tokyo CPI edged down to 3.1% yoy in June, from 3.2% in May. Core CPI, which excludes fresh food, held steady at 3.2% yoy. Core-core CPI, excluding both food and energy, saw a mild decrease from 3.9% yoy to 3.8% yoy.

China PMI manufacturing ticked up to 49.0, still in contraction

June saw a modest uptick in China's NBS PMI Manufacturing from 48.8 to 49.0, missing expectation of 49.5. The manufacturing sector remains in contractionary state, albeit with a slight improvement from the previous month.

In some details of PMI Manufacturing, new orders improved slightly, climbing to 48.6 from May's 48.3. However, new export orders saw a five-month low at 46.4, suggesting weakening demand from overseas. Employment fell from 48.4 to 48.2.

In parallel, PMI Non-Manufacturing dropped from 54.5 in May to 53.2 in June, underperforming 53.7 forecast. This decline marks the weakest reading index since December. Employment sub-gauge for non-manufacturing sector fell noticeably, from 48.4 to 46.8.

Additionally, PMI Composite, which combines both manufacturing and service sector activity, declined from 52.9 to 52.3. This lower figure highlights a broader slowdown in China's economic activity beyond manufacturing alone.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

EUR/USD dipped to 1.0834 earlier today but quickly recovered. It's still trying to defend 55 D EMA. Intraday bias stays neutral first. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 3.10% | 3.80% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | 3.20% | 3.30% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jun | 3.80% | 4.40% | 3.90% | |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M May P | -1.60% | -1.00% | 0.70% | |

| 01:30 | CNY | Manufacturing PMI Jun | 49 | 49.5 | 48.8 | |

| 01:30 | CNY | Non-Manufacturing PMI Jun | 53.2 | 53.7 | 54.5 | |

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.40% | 0.60% | |

| 05:00 | JPY | Housing Starts Y/Y May | 3.50% | -2.20% | -11.90% | |

| 06:00 | EUR | Germany Import Price Index M/M May | -1.40% | -2.00% | -1.70% | |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.40% | 0.20% | 0.80% | |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.10% | 0.10% | 0.10% | |

| 06:00 | GBP | Current Account (GBP) Q1 | -10.8B | -7.7B | -2.5B | |

| 06:30 | CHF | Real Retail Sales Y/Y May | -1.10% | -2.50% | -3.70% | -4.00% |

| 06:45 | EUR | France Consumer Spending M/M May | 0.50% | 0.70% | -1.00% | -0.80% |

| 07:00 | CHF | KOF Economic Barometer Jun | 90.8 | 89.2 | 90.2 | 91.4 |

| 07:55 | EUR | Germany Unemployment Change May | 28K | 15K | 9K | 13K |

| 07:55 | EUR | Germany Unemployment Rate May | 5.70% | 5.60% | 5.60% | |

| 08:00 | EUR | Italy Unemployment May | 7.60% | 7.90% | 7.80% | |

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.50% | 6.50% | 6.50% | |

| 09:00 | EUR | CPI Y/Y Jun P | 5.50% | 5.60% | 6.10% | |

| 09:00 | EUR | CPI Core Y/Y Jun P | 5.40% | 5.40% | 5.30% | |

| 12:30 | CAD | GDP M/M Apr | 0.00% | 0.20% | 0.00% | 0.10% |

| 12:30 | USD | Personal Income M/M May | 0.40% | 0.40% | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending May | 0.10% | 0.20% | 0.80% | |

| 12:30 | USD | PCE Price Index M/M May | 0.10% | 0.50% | 0.40% | |

| 12:30 | USD | PCE Price Index Y/Y May | 3.80% | 4.60% | 4.40% | 4.30% |

| 12:30 | USD | Core PCE Price Index M/M May | 0.30% | 0.40% | 0.40% | |

| 12:30 | USD | Core PCE Price Index Y/Y May | 4.60% | 4.70% | 4.70% | |

| 13:45 | USD | Chicago PMI Jun | 44.5 | 40.4 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 63.9 | 63.9 |

US PCE price index slowed to 3.8% yoy, core PCE down to 4.6% yoy

US personal income rose 0.4% mom, or USD 91.2B, matched expectations. Personal spending rose 0.1% mom, or USD 18.9B, below expectation of 0.2% mom.

Headline PCE price index rose 0.1% mom, below expectation of 0.5% mom. PCE core (excluding food and energy) rose 0.3% mom, below expectation of 0.4% mom. Goods prices fell -0.4% mom while services price rose 0.2% mom. Food prices rose 0.1% mom. Energy prices fell -3.9% mom.

From the same month one year ago, headline PCE price index slowed from 4.3% yoy to 3.8% yoy, below expectation of 4.6% yoy. PCE core (excluding food and energy) ticked down from 4.7% yoy to 4.6% yoy, matched expectations. Goods prices rose 1.1% yoy while services prices jumped 5.3% yoy. Food prices rose 5.8% yoy and energy prices decreased -13.4% yoy.

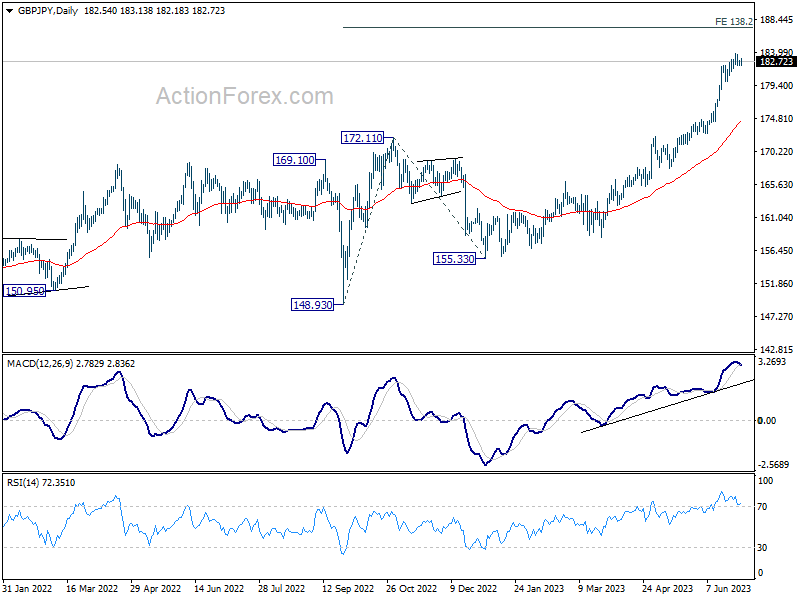

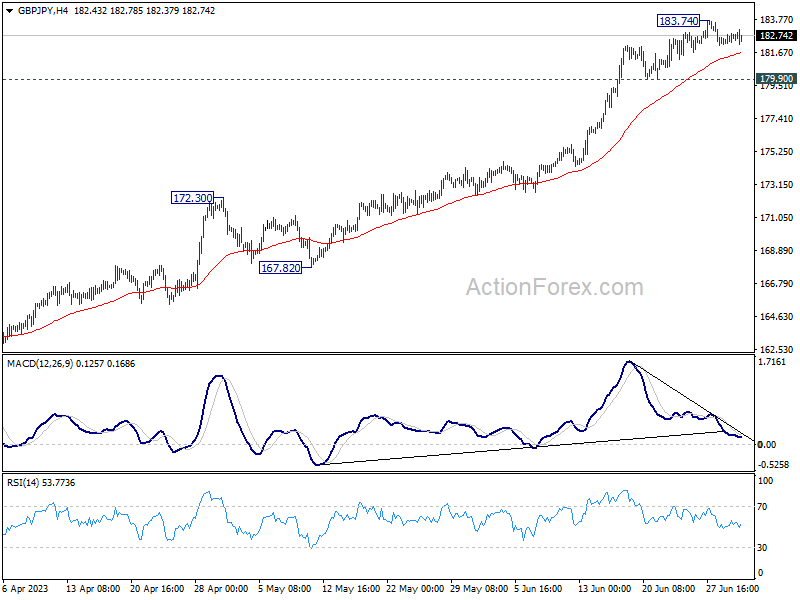

GBP/JPY Daily Outlook

Daily Pivots: (S1) 182.26; (P) 182.57; (R1) 182.92; More...

Intraday bias in GBP/JPY stays neutral for the moment, and further rise is expected as long as 179.90 support holds. Above 183.74 will resume larger up trend to 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36 next. On the downside, however, break of 179.90 support will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.