Sample Category Title

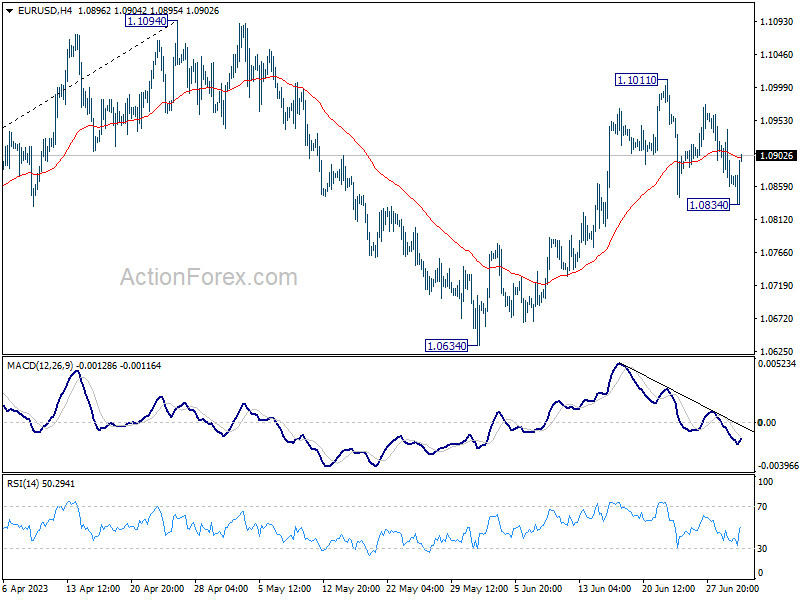

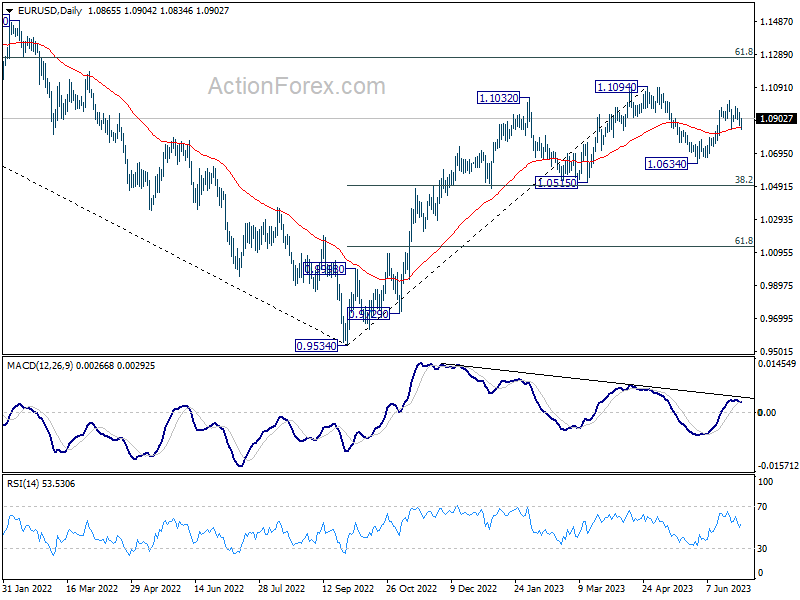

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

EUR/USD dipped to 1.0834 earlier today but quickly recovered. It's still trying to defend 55 D EMA. Intraday bias stays neutral first. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Dollar Dips as Headline and Core PCE Inflation Slowed

Dollar sees a significant dip in early US session after release of economic data showed a slower than expected headline PCE inflation and a slight decline in core PCE inflation. In contrast, Eurozone reported a tick up in core inflation for the same period. Stock futures rally on this news, while benchmark treasury yields dip Overall, the data, at least, doesn't lend support to more aggressive tightening by Fed.

As the month draws to a close, both Yen and Greenback are poised to end as the worst performers. Despite a slight hiccup in response to today's disappointing data, Canadian Dollar takes the crown as the strongest performer for the month, with Aussie Dollar taking the runner-up position, despite widespread selloffs this week. European majors are showing a mixed performance, with no clear winner among them.

In Europe, at the time of writing, FTSE is up 0.89%. DAX is up 1.25%. CAC is up 1.28%. Germany 10-year yield is down -0.014 at 2.408. Earlier in Asia, Nikkei dropped -0.14%. Hong Kong HSI dropped -0.09%. China Shanghai SSE rose 0.62%. Singapore Strait Times dropped -0.04%. Japan 10-year JGB yield rose 0.0161 to 0.400.

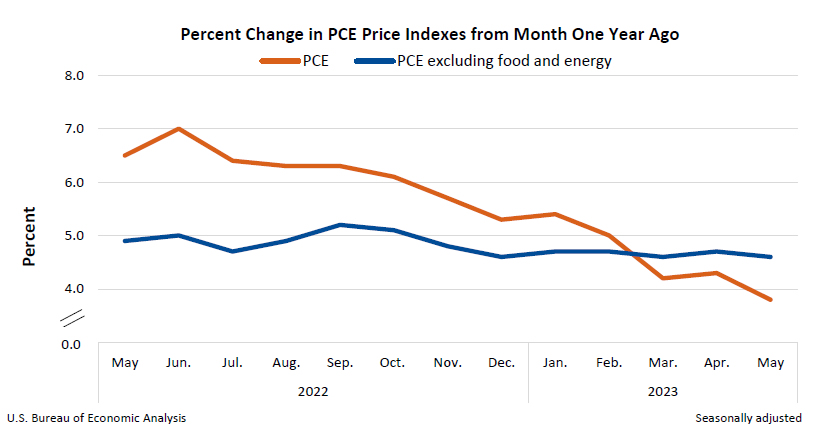

US PCE price index slowed to 3.8% yoy, core PCE down to 4.6% yoy

US personal income rose 0.4% mom, or USD 91.2B, matched expectations. Personal spending rose 0.1% mom, or USD 18.9B, below expectation of 0.2% mom.

Headline PCE price index rose 0.1% mom, below expectation of 0.5% mom. PCE core (excluding food and energy) rose 0.3% mom, below expectation of 0.4% mom. Goods prices fell -0.4% mom while services price rose 0.2% mom. Food prices rose 0.1% mom. Energy prices fell -3.9% mom.

From the same month one year ago, headline PCE price index slowed from 4.3% yoy to 3.8% yoy, below expectation of 4.6% yoy. PCE core (excluding food and energy) ticked down from 4.7% yoy to 4.6% yoy, matched expectations. Goods prices rose 1.1% yoy while services prices jumped 5.3% yoy. Food prices rose 5.8% yoy and energy prices decreased -13.4% yoy.

Also released, Canada GDP was unchanged for the month in April, below expectation of 0.2% mom growth. Goods-producing industries rose 0.1% mom while services-producing industries were flat. Overall, 11 of 20 industrial sectors posted increases.

Eurozone CPI slowed to 5.5% yoy in Jun, CPI core rose to 5.4% yoy

Eurozone CPI slowed from 6.1% yoy to 5.5% yoy in June, below expectation of 5.6% yoy. CPI core rose from 5.3% yoy to 5.4% yoy, matched expectations.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate(11.7%, compared with 12.5% in May), followed by non-energy industrial goods (5.5%, compared with 5.8% in May), services (5.4%, compared with 5.0% in May) and energy (-5.6%, compared with -1.8% in May).

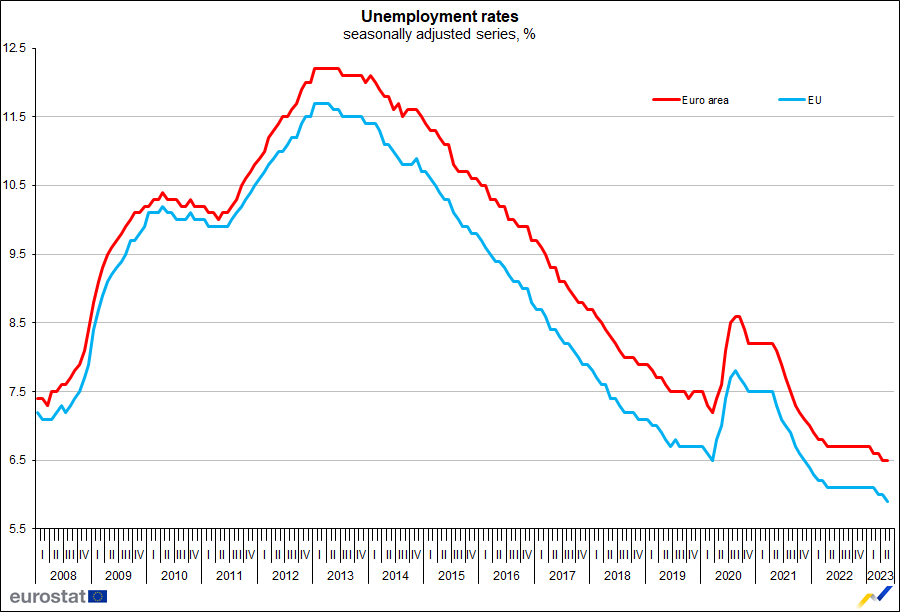

Eurozone unemployment rate unchanged at 6.5%, EU down to 5.9%

Eurozone unemployment rate was unchanged at 6.5% in May, matched expectations. EU unemployment rate ticked down from 6.0% to 5.9%.

Eurostat estimates that 12.937m persons in the EU, of whom 11.014, in Eurozone, were unemployed in May 2023. Compared with April 2023, unemployment decreased by -75k in the EU and by -57k in Eurozone.

Swiss KOF fell to 90.8, third decline in a row

Swiss KOF Economic Barometer dropped slightly from 91.4 to 90.8 in June, above expectation of 89.2. That's the third consecutive monthly decline.

KOF said: " The downward movement in the Barometer is primarily caused by bundles of indicators that capture foreign demand. Here, the outlook continues to deteriorate.

"The indicators covering private consumption and the economic sector of other services also give a slightly negative signal. The indicators for manufacturing and construction, on the other hand, point slightly in a positive direction."

Japan industrial production down -1.6% mom in May on vehicle sector

Japan's industrial production recorded a sharper decline than anticipated, dropping by 1.6% mom in May. This marked the first contraction in four months, surpassing expectations of -1.0% decrease. According to survey by Ministry of Economy, Trade and Industry, manufacturers forecast industrial output to recover by 5.6% in June, only to fall again by -0.6% in July.

Among the 15 industrial sectors, 12 reported falling output, with only three seeing rise in production. Notably, motor vehicle sector bore the brunt of the decline, experiencing substantial -8.9% slump from the previous month, with passenger cars and auto body parts being the significant contributors.

Also released, the country's unemployment rate remained unchanged at 2.6%, as expected. The number of jobless individuals decreased by -30k from the prior month, standing at 1.77 million. However, the Ministry of Health, Labor and Welfare revealed a slight downturn in the job market, with ratio of job openings to job seekers in May dropping to 1.31, down 0.01 point from April.

Meanwhile, Tokyo CPI edged down to 3.1% yoy in June, from 3.2% in May. Core CPI, which excludes fresh food, held steady at 3.2% yoy. Core-core CPI, excluding both food and energy, saw a mild decrease from 3.9% yoy to 3.8% yoy.

China PMI manufacturing ticked up to 49.0, still in contraction

June saw a modest uptick in China's NBS PMI Manufacturing from 48.8 to 49.0, missing expectation of 49.5. The manufacturing sector remains in contractionary state, albeit with a slight improvement from the previous month.

In some details of PMI Manufacturing, new orders improved slightly, climbing to 48.6 from May's 48.3. However, new export orders saw a five-month low at 46.4, suggesting weakening demand from overseas. Employment fell from 48.4 to 48.2.

In parallel, PMI Non-Manufacturing dropped from 54.5 in May to 53.2 in June, underperforming 53.7 forecast. This decline marks the weakest reading index since December. Employment sub-gauge for non-manufacturing sector fell noticeably, from 48.4 to 46.8.

Additionally, PMI Composite, which combines both manufacturing and service sector activity, declined from 52.9 to 52.3. This lower figure highlights a broader slowdown in China's economic activity beyond manufacturing alone.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

EUR/USD dipped to 1.0834 earlier today but quickly recovered. It's still trying to defend 55 D EMA. Intraday bias stays neutral first. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 3.10% | 3.80% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | 3.20% | 3.30% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jun | 3.80% | 4.40% | 3.90% | |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M May P | -1.60% | -1.00% | 0.70% | |

| 01:30 | CNY | Manufacturing PMI Jun | 49 | 49.5 | 48.8 | |

| 01:30 | CNY | Non-Manufacturing PMI Jun | 53.2 | 53.7 | 54.5 | |

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.40% | 0.60% | |

| 05:00 | JPY | Housing Starts Y/Y May | 3.50% | -2.20% | -11.90% | |

| 06:00 | EUR | Germany Import Price Index M/M May | -1.40% | -2.00% | -1.70% | |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.40% | 0.20% | 0.80% | |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.10% | 0.10% | 0.10% | |

| 06:00 | GBP | Current Account (GBP) Q1 | -10.8B | -7.7B | -2.5B | |

| 06:30 | CHF | Real Retail Sales Y/Y May | -1.10% | -2.50% | -3.70% | -4.00% |

| 06:45 | EUR | France Consumer Spending M/M May | 0.50% | 0.70% | -1.00% | -0.80% |

| 07:00 | CHF | KOF Economic Barometer Jun | 90.8 | 89.2 | 90.2 | 91.4 |

| 07:55 | EUR | Germany Unemployment Change May | 28K | 15K | 9K | 13K |

| 07:55 | EUR | Germany Unemployment Rate May | 5.70% | 5.60% | 5.60% | |

| 08:00 | EUR | Italy Unemployment May | 7.60% | 7.90% | 7.80% | |

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.50% | 6.50% | 6.50% | |

| 09:00 | EUR | CPI Y/Y Jun P | 5.50% | 5.60% | 6.10% | |

| 09:00 | EUR | CPI Core Y/Y Jun P | 5.40% | 5.40% | 5.30% | |

| 12:30 | CAD | GDP M/M Apr | 0.00% | 0.20% | 0.00% | 0.10% |

| 12:30 | USD | Personal Income M/M May | 0.40% | 0.40% | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending May | 0.10% | 0.20% | 0.80% | |

| 12:30 | USD | PCE Price Index M/M May | 0.10% | 0.50% | 0.40% | |

| 12:30 | USD | PCE Price Index Y/Y May | 3.80% | 4.60% | 4.40% | 4.30% |

| 12:30 | USD | Core PCE Price Index M/M May | 0.30% | 0.40% | 0.40% | |

| 12:30 | USD | Core PCE Price Index Y/Y May | 4.60% | 4.70% | 4.70% | |

| 13:45 | USD | Chicago PMI Jun | 44.5 | 40.4 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 63.9 | 63.9 |

US PCE price index slowed to 3.8% yoy, core PCE down to 4.6% yoy

US personal income rose 0.4% mom, or USD 91.2B, matched expectations. Personal spending rose 0.1% mom, or USD 18.9B, below expectation of 0.2% mom.

Headline PCE price index rose 0.1% mom, below expectation of 0.5% mom. PCE core (excluding food and energy) rose 0.3% mom, below expectation of 0.4% mom. Goods prices fell -0.4% mom while services price rose 0.2% mom. Food prices rose 0.1% mom. Energy prices fell -3.9% mom.

From the same month one year ago, headline PCE price index slowed from 4.3% yoy to 3.8% yoy, below expectation of 4.6% yoy. PCE core (excluding food and energy) ticked down from 4.7% yoy to 4.6% yoy, matched expectations. Goods prices rose 1.1% yoy while services prices jumped 5.3% yoy. Food prices rose 5.8% yoy and energy prices decreased -13.4% yoy.

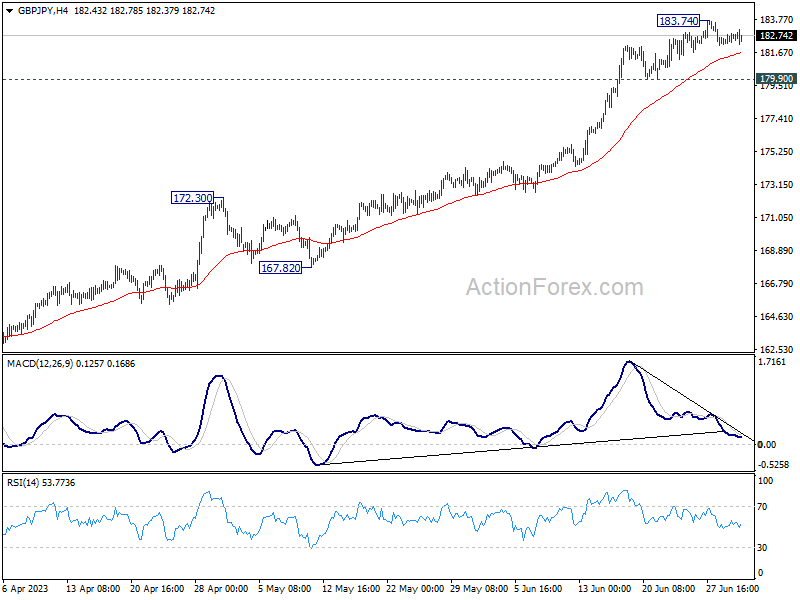

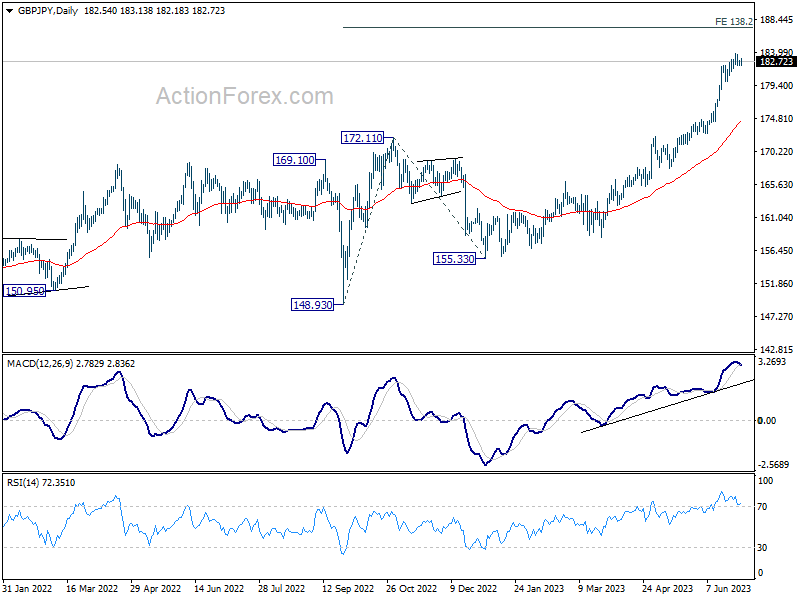

GBP/JPY Daily Outlook

Daily Pivots: (S1) 182.26; (P) 182.57; (R1) 182.92; More...

Intraday bias in GBP/JPY stays neutral for the moment, and further rise is expected as long as 179.90 support holds. Above 183.74 will resume larger up trend to 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36 next. On the downside, however, break of 179.90 support will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

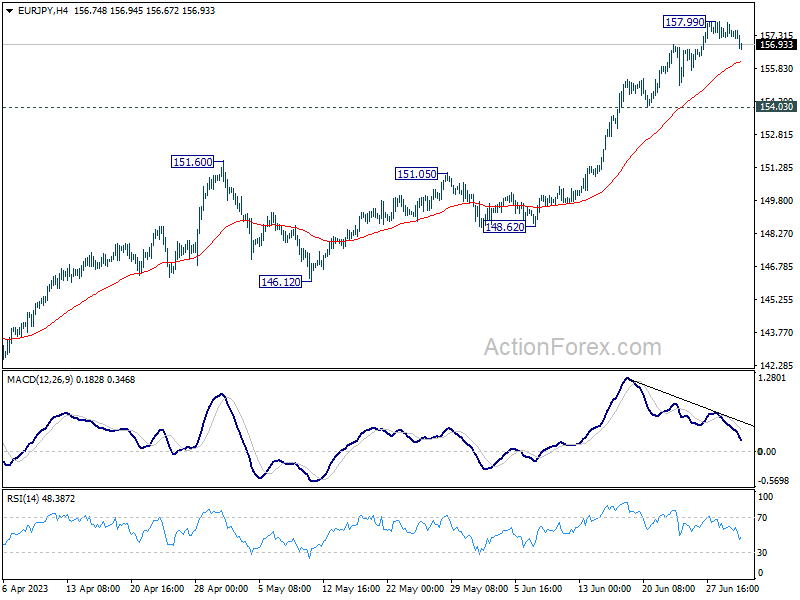

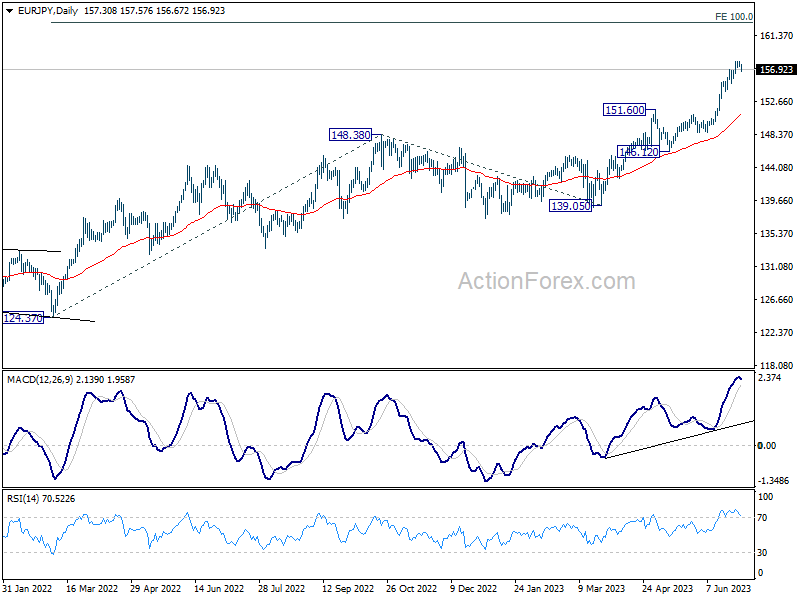

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.06; (P) 157.49; (R1) 157.73; More....

Intraday bias in EUR/JPY is turned neutral with current retreat. Some consolidations would be seen first. But further rally is expected as long as 154.03 support holds. Break of 157.99 will resume larger up trend to 162.82 projection level. However, break of 154.03 will argue that larger correction is under way back to 151.60 resistance turned support.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 151.60 resistance turned support holds, even in case of deep pull back.

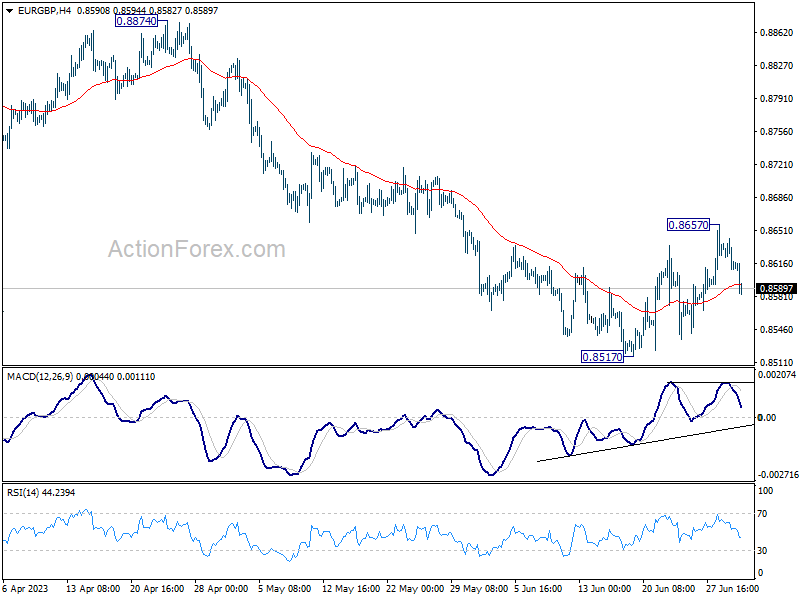

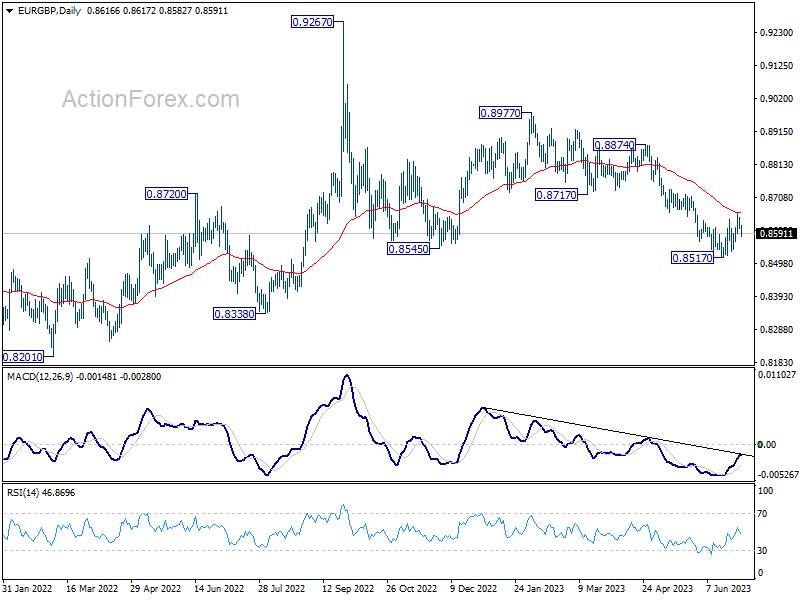

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8602; (P) 0.8623; (R1) 0.8634; More...

Intraday bias in EUR/GBP is turned neutral with current retreat. Rejection by 55 D EMA retains near term bearishness. Break of 0.8517 will resume the decline from 0.8977. On the upside, above 0.8657 resistance will resume the rebound from 0.8517.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

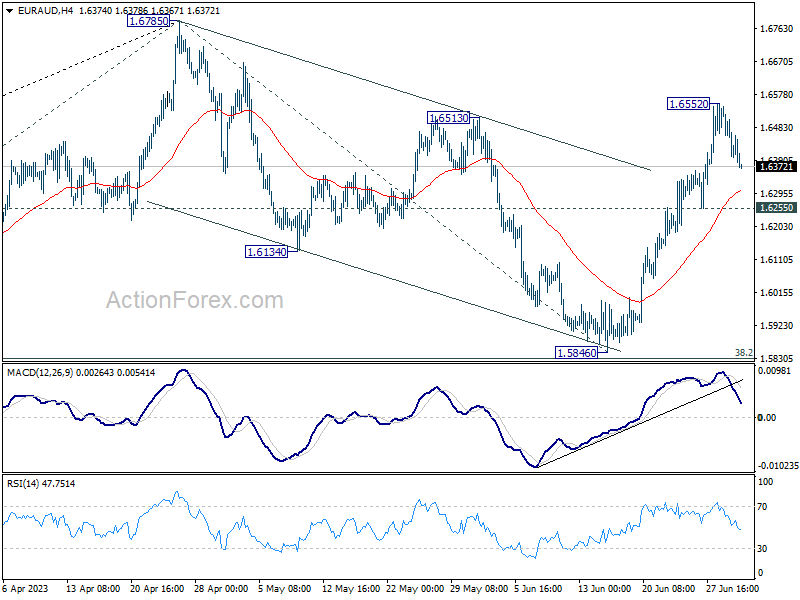

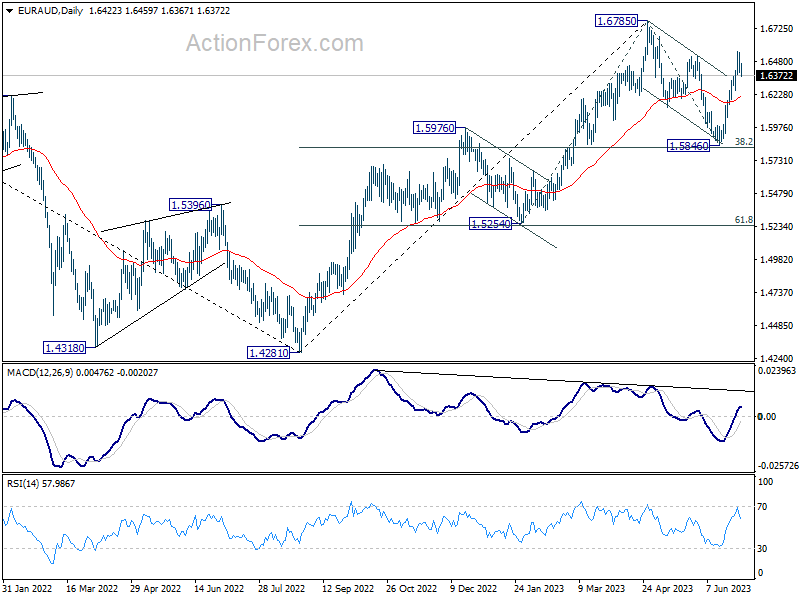

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6365; (P) 1.6454; (R1) 1.6509; More...

Intraday bias in EUR/AUD is turned neutral with current retreat. Further rally is expected as long as 1.6255 support holds. Correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, break of 1.6255 will dampen this view and turn bias to the downside for 1.5846 support.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rally resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9757; (P) 0.9782; (R1) 0.9797; More...

Range trading continues in EUR/CHF and intraday bias stays neutral for the moment. Another fall cannot be ruled out, to retest 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound from 0.9670 to 0.9878 resistance.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9918). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

Japanese Yen Flirts with 145, Core CPI Ticks Upwards

- Japanese yen briefly falls below 145 line

- Tokyo Core CPI rises to 3.2%

- US GDP revised higher, unemployment claims slide

USD/JPY is showing limited movement, trading at 144.62 in the European session. The yen briefly fell below the symbolic 145 line earlier today.

Tokyo Core CPI inches higher

Tokyo Core CPI, a key inflation gauge, moved slightly higher in June. The index came in at 3.2% y/y, up from 3.1% in May but below the consensus of 3.3%. This marks the 13th straight month that Tokyo Core CPI has remained above the Bank of Japan’s 2% target.

The Tokyo inflation release, considered a leading indicator of inflation trends nationwide, points to inflation remaining high across the economy and puts into question the central bank’s stance that high inflation levels are temporary. BoJ Governor Ueda has stated often that he will maintain the Bank’s ultra-loose policy until stronger wage growth keeps inflation sustainably around the 2% target. I’m not sure how Ueda defines “sustainable”, but it’s clear that the BoJ has no intention of tightening rates anytime soon.

The BoJ’s ultra-loose policy has sent the yen on another sharp decline – USD/JPY is up a massive 9% since April 1st. The yen breached 145 on Friday, and Finance Minister Suzuki responded with a warning that Tokyo “would respond appropriately if the moves become excessive.” The Finance Ministry intervened in the currency markets late last year when the yen fell below 150, and intervention will become more likely if the yen continues to lose ground.

US GPD revised upwards, jobless claims sink

The US economy remains in solid shape. Final GDP for the first quarter rose 2.0%, a major revision from the 1.3% gain in the second estimate. Still, the Fed’s aggressive tightening is dampening economic activity. GDP growth in the third and fourth quarters of 2022 was 3.2% and 2.6%, respectively, and has declined to 2.0% in Q1. The US labor market continues to thrive despite the Fed’s rate hikes. Initial jobless claims plunged to 235,000, down from 239,000 prior and below the consensus of 264,000.

The GDP revision and the strong unemployment claims report have caused the markets to reprice upwards the probability of a rate hike in July. The CME FedWatch tool has priced in a 25-bp hike at 89%, up from 72% just one week ago.

USD/JPY Technical

- There is resistance at 144.65 and 145.36

- 143.94 and 142.94 are providing support

Eurozone unemployment rate unchanged at 6.5%, EU down to 5.9%

Eurozone unemployment rate was unchanged at 6.5% in May, matched expectations. EU unemployment rate ticked down from 6.0% to 5.9%.

Eurostat estimates that 12.937m persons in the EU, of whom 11.014, in Eurozone, were unemployed in May 2023. Compared with April 2023, unemployment decreased by -75k in the EU and by -57k in Eurozone.