Sample Category Title

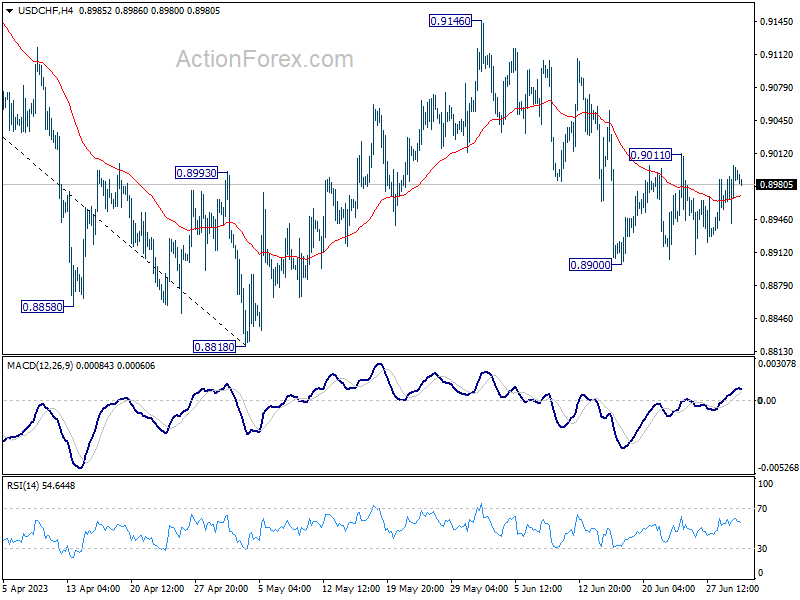

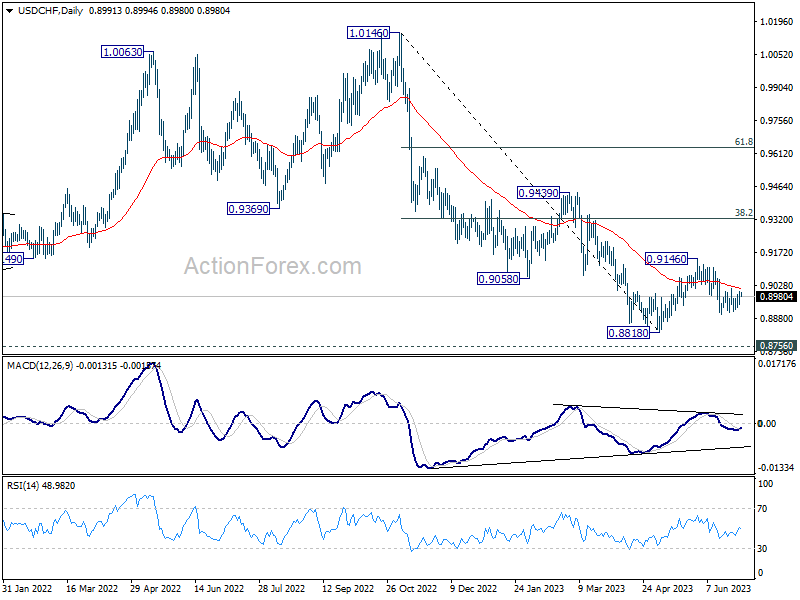

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8959; (P) 0.8980; (R1) 0.9018; More...

Intraday bias in USD/CHF stays neutral as range trading continues and outlook is unchanged. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. But for now, strong support is still expected from 0.8756 long term support to bring rebound. On the upside, above 0.9011 will bring stronger rise towards 0.9146 resistance.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

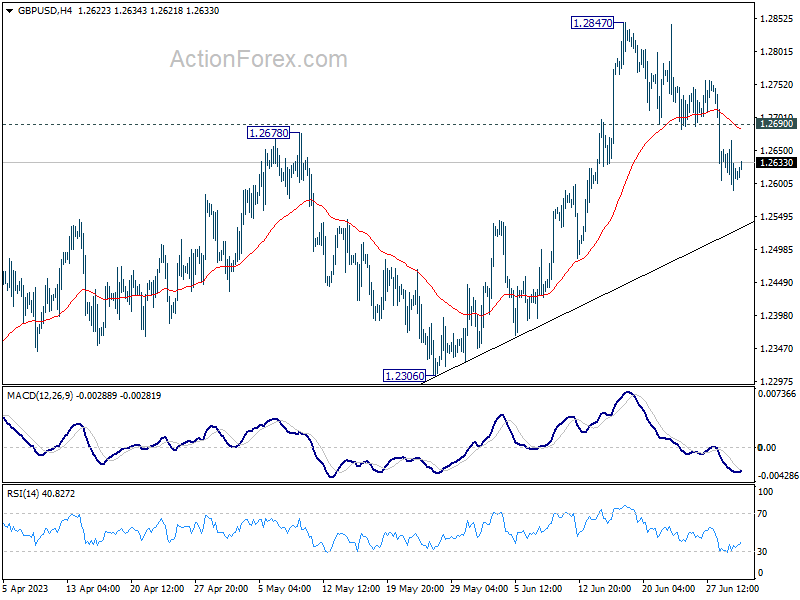

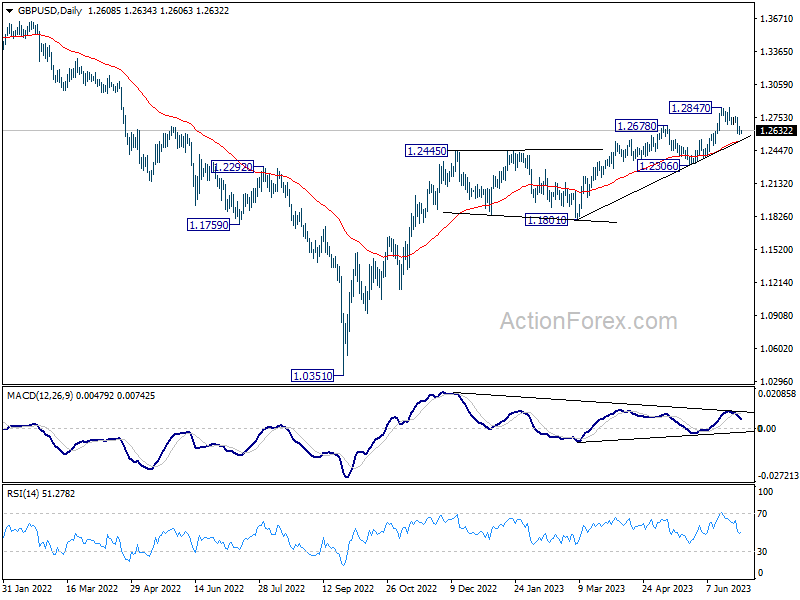

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2623; (R1) 1.2656; More...

Intraday bias in GBP/USD remains mildly on the downside as fall from 1.2847 short term top is in progress. Considering bearish divergence condition in D MACD, sustained break of 55 D EMA (now at 1.2529) will argue that it's already in correction to larger up trend and target 1.2306 support. On the upside, though, break of 1.2690 minor resistance will bring retest of 1.2847 instead.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

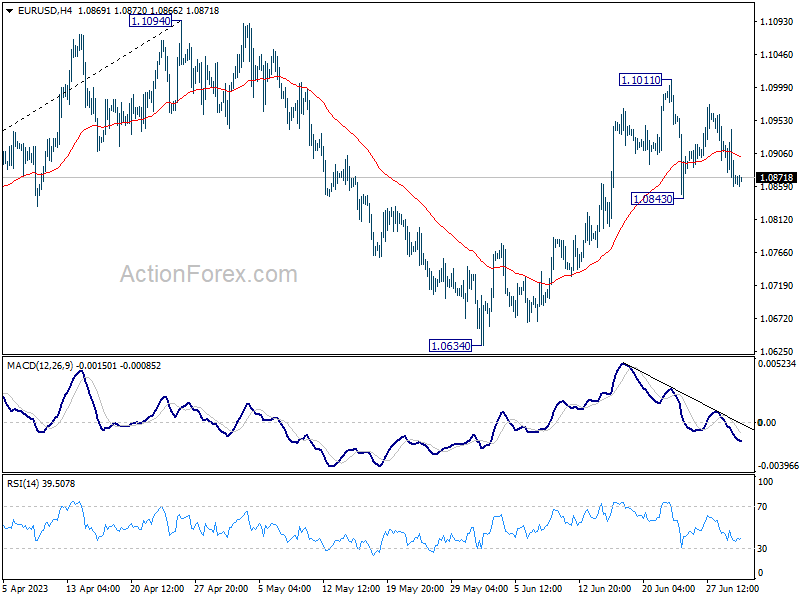

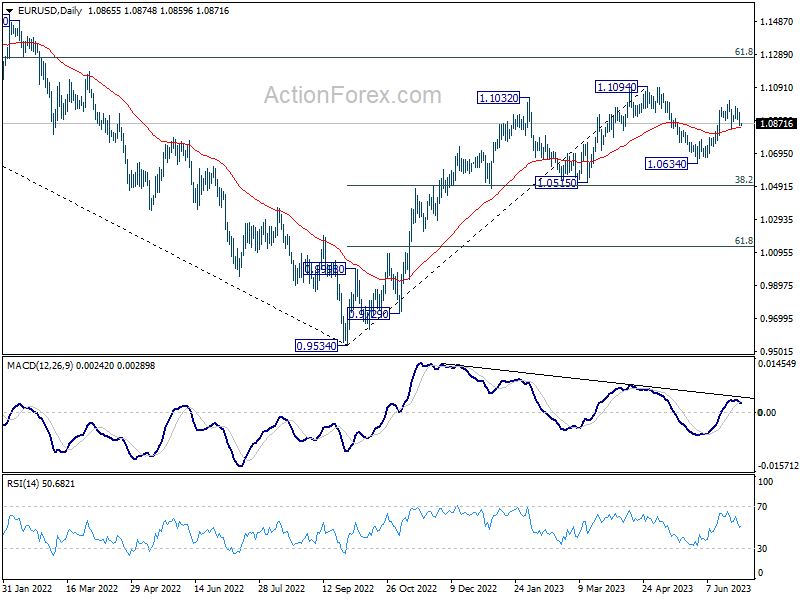

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

Intraday bias in EUR/USD remains neutral at this point as sideway trading continues. Further rally is mildly in favor with 1.0843 support intact. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, break of 1.0843 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Euro and Dollar Await Inflation Data as Markets Tread Water

In the run-up to the close of the first half, forex markets appear to be treading water in today's Asian session. Market responses to China's lackluster PMI data have been tepid, while Yen remains largely unfazed by Japan's industrial production figures and Tokyo's CPI. Asian indexes are mixed with mild selloff in Nikkei.

Dollar and Euro are neck-and-neck in the race for this week's top spot, with the final outcome possibly hinging on upcoming Eurozone CPI flash and US PCE inflation data. Commodity currencies, on the other hand, are languishing at the bottom of the chart, with Kiwi underperforming against its Australian and Canadian counterparts. Sterling, Swiss Franc, and Yen are stuck in a mixed performance amidst the fray.

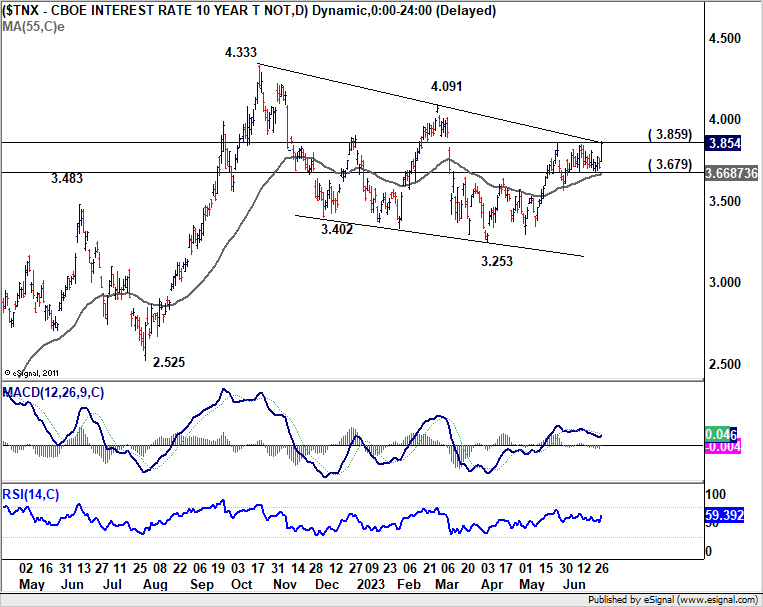

Technically, US 10-year yield's breach of 3.854 short term top overnight is worth a mention. Rise from 3.253 might be finally resuming. A strong close above the resistance today will solidify near term bullishness, and the case that whole correction from 4.333 has completed with three waves down to 3.253. This development could pave the way for further rally in the coming week, especially with a slew of high-impact US data on the horizon, and potentially providing a boost for USD/JPY. The lingering question for USD/JPY is when Japan might decide to step in with intervention again.

In Asia, at the time of writing, Nikkei is down -0.54%. Hong Kong HSI is up 0.02%. China Shanghai SSE is up 0.78%. Singapore Strait times is up 0.03%. Japan 10-year JGB yield is up 0.0131 at 0.397, getting close to 0.4 handle again. Overnight, DOW rose 0.80%. S&P 500 rose 0.45%. NASDAQ closed flat. 10-year yield rose 0.144 to 3.854.

Japan industrial production down -1.6% mom in May on vehicle sector

Japan's industrial production recorded a sharper decline than anticipated, dropping by 1.6% mom in May. This marked the first contraction in four months, surpassing expectations of -1.0% decrease. According to survey by Ministry of Economy, Trade and Industry, manufacturers forecast industrial output to recover by 5.6% in June, only to fall again by -0.6% in July.

Among the 15 industrial sectors, 12 reported falling output, with only three seeing rise in production. Notably, motor vehicle sector bore the brunt of the decline, experiencing substantial -8.9% slump from the previous month, with passenger cars and auto body parts being the significant contributors.

Also released, the country's unemployment rate remained unchanged at 2.6%, as expected. The number of jobless individuals decreased by -30k from the prior month, standing at 1.77 million. However, the Ministry of Health, Labor and Welfare revealed a slight downturn in the job market, with ratio of job openings to job seekers in May dropping to 1.31, down 0.01 point from April.

Meanwhile, Tokyo CPI edged down to 3.1% yoy in June, from 3.2% in May. Core CPI, which excludes fresh food, held steady at 3.2% yoy. Core-core CPI, excluding both food and energy, saw a mild decrease from 3.9% yoy to 3.8% yoy.

China PMI manufacturing ticked up to 49.0, still in contraction

June saw a modest uptick in China's NBS PMI Manufacturing from 48.8 to 49.0, missing expectation of 49.5. The manufacturing sector remains in contractionary state, albeit with a slight improvement from the previous month.

In some details of PMI Manufacturing, new orders improved slightly, climbing to 48.6 from May's 48.3. However, new export orders saw a five-month low at 46.4, suggesting weakening demand from overseas. Employment fell from 48.4 to 48.2.

In parallel, PMI Non-Manufacturing dropped from 54.5 in May to 53.2 in June, underperforming 53.7 forecast. This decline marks the weakest reading index since December. Employment sub-gauge for non-manufacturing sector fell noticeably, from 48.4 to 46.8.

Additionally, PMI Composite, which combines both manufacturing and service sector activity, declined from 52.9 to 52.3. This lower figure highlights a broader slowdown in China's economic activity beyond manufacturing alone.

Looking ahead

The economic calendar is rather busy today. Eurozone CPI flash is the main highlight in European session while unemployment rate will be released. Other features include UK GDP final, Swiss retail sales and KOF economic barometer, France consumer spending and Germany unemployment.

Later in the day, focuses will be on Canada GDP and US PCE inflation. Chicago PMI and U of Michigan consumer sentiment final will also be published.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0888; (R1) 1.0917; More...

Intraday bias in EUR/USD remains neutral at this point as sideway trading continues. Further rally is mildly in favor with 1.0843 support intact. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534. However, break of 1.0843 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 3.10% | 3.80% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | 3.20% | 3.30% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jun | 3.80% | 4.40% | 3.90% | |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M May P | -1.60% | -1.00% | 0.70% | |

| 01:30 | CNY | Manufacturing PMI Jun | 49.0 | 49.5 | 48.8 | |

| 01:30 | CNY | Non-Manufacturing PMI Jun | 53.2 | 53.7 | 54.5 | |

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.40% | 0.60% | |

| 05:00 | JPY | Housing Starts Y/Y May | -2.20% | -11.90% | ||

| 06:00 | EUR | Germany Import Price Index M/M May | -2.00% | -1.70% | ||

| 06:00 | EUR | Germany Retail Sales M/M May | 0.20% | 0.80% | ||

| 06:00 | GBP | GDP Q/Q Q1 F | 0.10% | 0.10% | ||

| 06:00 | GBP | Current Account (GBP) Q1 | -7.7B | -2.5B | ||

| 06:30 | CHF | Real Retail Sales Y/Y May | -2.50% | -3.70% | ||

| 06:45 | EUR | France Consumer Spending M/M May | 0.70% | -1.00% | ||

| 07:00 | CHF | KOF Economic Barometer Jun | 89.2 | 90.2 | ||

| 07:55 | EUR | Germany Unemployment Change May | 15K | 9K | ||

| 07:55 | EUR | Germany Unemployment Rate May | 5.60% | 5.60% | ||

| 08:00 | EUR | Italy Unemployment May | 7.90% | 7.80% | ||

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.50% | 6.50% | ||

| 09:00 | EUR | CPI Y/Y Jun P | 5.60% | 6.10% | ||

| 09:00 | EUR | CPI Core Y/Y Jun P | 5.40% | 5.30% | ||

| 12:30 | CAD | GDP M/M Apr | 0.20% | 0.00% | ||

| 12:30 | USD | Personal Income M/M May | 0.40% | 0.40% | ||

| 12:30 | USD | Personal Spending May | 0.20% | 0.80% | ||

| 12:30 | USD | PCE Price Index M/M May | 0.40% | |||

| 12:30 | USD | PCE Price Index Y/Y May | 4.40% | |||

| 12:30 | USD | Core PCE Price Index M/M May | 0.40% | 0.40% | ||

| 12:30 | USD | Core PCE Price Index Y/Y May | 4.70% | 4.70% | ||

| 13:45 | USD | Chicago PMI Jun | 44.5 | 40.4 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 63.9 | 63.9 |

China PMI manufacturing ticked up to 49.0, still in contraction

June saw a modest uptick in China's NBS PMI Manufacturing from 48.8 to 49.0, missing expectation of 49.5. The manufacturing sector remains in contractionary state, albeit with a slight improvement from the previous month.

In some details of PMI Manufacturing, new orders improved slightly, climbing to 48.6 from May's 48.3. However, new export orders saw a five-month low at 46.4, suggesting weakening demand from overseas. Employment fell from 48.4 to 48.2.

In parallel, PMI Non-Manufacturing dropped from 54.5 in May to 53.2 in June, underperforming 53.7 forecast. This decline marks the weakest reading index since December. Employment sub-gauge for non-manufacturing sector fell noticeably, from 48.4 to 46.8.

Additionally, PMI Composite, which combines both manufacturing and service sector activity, declined from 52.9 to 52.3. This lower figure highlights a broader slowdown in China's economic activity beyond manufacturing alone.

Japan industrial production down -1.6% mom in May on vehicle sector

Japan's industrial production recorded a sharper decline than anticipated, dropping by -1.6% mom in May. This marked the first contraction in four months, surpassing expectations of -1.0% decrease. According to survey by Ministry of Economy, Trade and Industry, manufacturers forecast industrial output to recover by 5.6% in June, only to fall again by -0.6% in July.

Among the 15 industrial sectors, 12 reported falling output, with only three seeing rise in production. Notably, motor vehicle sector bore the brunt of the decline, experiencing substantial -8.9% slump from the previous month, with passenger cars and auto body parts being the significant contributors.

Also released, the country's unemployment rate remained unchanged at 2.6%, as expected. The number of jobless individuals decreased by -30k from the prior month, standing at 1.77 million. However, the Ministry of Health, Labor and Welfare revealed a slight downturn in the job market, with ratio of job openings to job seekers in May dropping to 1.31, down 0.01 point from April.

Meanwhile, Tokyo CPI edged down to 3.1% yoy in June, from 3.2% in May. Core CPI, which excludes fresh food, held steady at 3.2% yoy. Core-core CPI, excluding both food and energy, saw a mild decrease from 3.9% yoy to 3.8% yoy.

We Confirm Our Call for 0.25% Increase in Cash Rate Next Week

The Reserve Bank Board meets next week on July 4. We confirm our view that the Board will decide to lift the cash rate by 0.25% to 4.35% at the July meeting with a further 0.25% increase to follow in August.

With core inflation holding above 6%; the unemployment rate holding nearly 1 ppt below the NAIRU (RBA's estimate) and the cash rate only around 1 ppt into contractionary territory (we see neutral around 3%) the cash rate will need to go higher. A second pause, to gather further information, seems unnecessary and only risks the need for the cycle to extend even further into 2023 when the prospects for damage to the economy increase substantially.

A terminal cash rate of 4.6% is likely to be sufficient to achieve the Bank's inflation objectives, although growth is forecast to slow to a crawl this year and next. Westpac's forecasts, which are based on a 4.6% terminal rate, point to very weak growth in both 2023 (0.6%) and 2024 (1.0%) and an earlier achievement of the inflation target than currently forecast by the RBA.

The case for a further rate increase has strengthened since the last Board meeting on June 6.

Of most importance are indications that the Board has, appropriately, adjusted its reaction function at the June meeting to prioritise containing inflationary expectations and addressing the risk (admittedly low) of a 1970s-style extended period of high inflation. Specifically, the minutes to the meeting noted that: "Members discussed the possibility of implicit indexation of wages to past high inflation and the potential for this to become widespread."

The objective of "preserving as many of the gains in employment as possible" is still noted by the Board in the minutes but other communication suggests it is taking a more cautious approach to safeguarding employment gains. Deputy Governor Bullock in a speech on June 20 indicated that the Board's inflation objective could not be achieved without the unemployment rate rising to 4.5%. Recall that the unemployment rate was around 5% before the pandemic, so an unemployment rate objective of 4.5% only represents a modest 0.5% net gain.

There have been some the key developments in the economy since that last Board meeting.

- The unemployment rate fell from 3.7% to 3.6% in May – remaining near recent lows despite the 4% tightening cycle.

- Jobs growth printed 76,000 in May – well above market consensus of 15,000 and Westpac's forecast of 40,000, meaning that the monthly pace of jobs growth has hardly slowed since the tightening cycle began.

- Business surveys continue to point to intense labour shortages. Official job vacancies fell a modest 2% between February and May – a slightly slower pace than the 2.2% fall we saw between November and February with the vacancy-to-unemployed ratio still 0.83 compared to 0.27 before the pandemic.

- The May CPI indicator showed a sharp fall in headline inflation to 5.6% in May from 6.8% in April but was largely due to volatile items (fruit, vegetables and fuel) and holiday travel. The Reserve Bank typically strips out these items when assessing inflation trends. Annual inflation in the CPI excluding volatile items and holiday travel fell from 6.5% to 6.4%, while the monthly increase in this measure lifted from 0.2% in April to 0.5% in May. Fuel provides a clear example of the risks involved with relying on monthly moves without adjusting for volatile items. Fuel prices fell 7.6% in May but are already up 6.4% over the June month to date.

- The measure for the trimmed mean inflation fell from 6.7% to 6.1%. Even if the fall is confirmed by the much more reliable June quarter CPI, annual underlying inflation at over 6% at a time when the unemployment rate is holding well below full employment is not consistent with pausing.

- The RBA should be unnerved by dwelling prices which have continued to post gains despite recent rate hikes – an unwelcome 1.4% rise in May has been followed by what looks to be a further 1.3% lift in June.

- A surprise 0.7% lift in nominal retail sales in May suggests consumer demand has retained some momentum in the second quarter, albeit with volumes still tracking a subdued pace.

- The March quarter national accounts reported a further lift in annual unit labour costs growth, surging to 7.9%yr, up from 7%yr in December and just 4%yr in June last year. Unit labour costs, which are closely linked to market services inflation, have become a particular source of concern for the Board.

- The surprise 50 basis point lift by the Bank of England, last week, highlights the general mood overseas that central banks expect that their tightening cycles have further to run.

What are the arguments against a move?

The July decision comes one month before the Board can assess the staff's revised inflation and growth forecasts, which are refreshed in February, May, August and November. This will include an extension of the forecasting horizon out to the end of 2025.

The minutes to the June meeting show there is already unease on the Board about the time being taken to reach the inflation target. Specifically: "… members noted that a more prolonged period of above-target inflation would increase the risk that firms' and households' expectations for inflation rise." Waiting for the refreshed forecasts is always a respectable reason not to move. It seems unlikely that they will entail any change in the 'timetable' and should include the expectation that inflation will be in the centre of the target band by end 2025.

The Board minutes describe the arguments for and against the June tightening as 'finely balanced'. My view is that arguments will always be 'finely balanced' near the peak of a tightening cycle.

But from the perspective of our forecast for July, a much more troubling aspect of the minutes is the absence of the comment that "some further tightening of monetary policy may be required". This was used by the Governor in his statement following the decision and repeated in his speech the following day, which the Board minutes noted "would provide an opportunity to explain the decision in more detail."

It would be extraordinary if the omission of this sentence was a basic oversight, especially when used twice by the Governor in other communication.

With the Governor nearing the end of his tenure, the spectre of the recommendations of the recent Review of the Reserve Bank, and some turnover at Board level the current task of forecasting monetary policy has become even more challenging.

We can only promote what we think is the appropriate decision given the issues outlined above.

Last month the Board had two high profile triggers to move – the award wage agreements and the increase in the monthly inflation gauge.

A more tentative Board than we think should be appropriate at this stage of the cycle which does not have the high profile "trigger" of the wage agreements and the temporary boost from the monthly Inflation Indicator could choose to pause pending more information.

Given the issues, which are clearly pointing to the need for higher rates, a second pause in this cycle seems inappropriate and unnecessarily complicates the central task of bringing inflation back into line.

Cliff Notes: Persistence of Underlying Inflation Continues to Trouble Policy Makers

Key insights from the week that was.

The main data release for Australia this week was the Monthly CPI Indicator which provided a mixed read on current inflation trends. The headline index surprised to the downside in May, the 0.4% monthly decline seeing the annual rate ease from 6.8%yr in April to 5.6%yr. The detail was broadly as anticipated, with prices for many services still rising on a monthly basis; however, a large decline in holiday travel and accommodation prices (–11.3%mth) more than offset this.

Measures of underlying inflation were more resilient however, the recently reinstated annual trimmed mean only falling from 6.7%yr to 6.1%yr, while the index that excludes volatile items (including holiday travel) was little changed. If anything, the May update reinforces the fact that the Monthly CPI Indicator is a volatile gauge, making it difficult to obtain a clear read through the quarter.

The decline in job vacancies was modest. From a high level, the 2.0% fall over the three months to May leaves vacancies just 10% below their May 2022 peak and still almost twice the level observed before the onset of the pandemic. This is consistent with other labour market indicators, including the Labour Force Survey and business surveys like the Westpac-ACCI Survey on Industrial Trends, which suggest the labour market remains historically tight with only tentative signs of easing evident.

It is also interesting to note that retail sales surprised to the upside in May, rising 0.7%mth after a poor run since December. Considering the context — high inflation and strong population growth — nominal spending in May is still best considered weak. We estimate that sales volumes were flat in Q2.

As outlined by Chief Economist Bill Evans, the persistence of service sector inflation and labour market strength warrant the RBA tightening further in July and August; and, as important, thereafter holding the resulting 4.60% cash rate peak into 2024. That said, from May 2024 to end-2025, there will be need for concerted policy easing as activity growth remains materially below trend and the unemployment rate rises above the RBA’s estimate of full employment.

Offshore, attention was focussed on the ECB Forum on Central Banking in Sintra, Portugal. Overall, the policy panel, which included the heads of the Bank of England, Bank of Japan, the European Central Bank and the US Federal Reserve, made clear that further tightening is likely to prove necessary in coming months.

The ECB’s Lagarde signalled a hike in July remains the Council’s expectation; however, she pushed back on the idea that a follow-up move in September was certain, citing the slew of data to be released between now and then. Sticky underlying inflation and labour market strength justify the ECB’s hawkish bias.

Looking back to the June decision, the BoE’s Bailey clarified that the step up to a 50bp hike occurred because the Bank believed data to hand warranted two further 25bp hikes. Bailey also pointed out that policy transmission was slower in this tightening cycle, with circa 85% of all mortgages being fixed rate loans. The UK’s tight labour market is expected to remain a concern for inflation, with many businesses expected to hold on to labour through the impending downturn.

Unsurprisingly, FOMC’s Chair Powell also highlighted strength in the labour market, although he pointed out that momentum was heading in the right direction and risks coming into balance. The Committee’s median expectation of two more hikes in 2023 was referenced, but Chair Powell also made clear the FOMC’s actions would remain data dependent. (Note, Chair Powell subsequently spoke at a Bank of Spain event, although the primary focus was financial stability.)

In stark contrast to the above speakers, BoJ’s Governor Ueda subsequently justified holding policy steady, referencing moderate ‘underlying inflation’ and a continued belief that headline and core inflation would return below target towards the end of 2025.

Coupled with the light but constructive data flow for the US and other markets, the above comments on policy led the market to price in a greater chance of ‘higher rates for longer’, the US 2 and 10-year yields, as examples, currently 12bps and 10bps higher than the end of last week, respectively 4.86% and 3.84%. With respect to the short-term risks for policy rates, the market’s concern is acute for the UK, with 5 more hikes priced by December/February versus the 1-2 moves for the FOMC and ECB.

Turning then to the international data received. While modest in scale, the market was most surprised by the revision in the third estimate of Q1 US GDP from 1.3% to 2.0% annualised. This update occurred because of a mix of modestly stronger consumption; slightly less inflation; and better exports. The market’s response also looked to be supported by initial jobless claims retreating near their historic lows.

Earlier in the week, the US saw a substantial 12% gain in new home sales in May as existing home supply remained constrained – pending home sales 21% lower than a year ago in May and S&P CoreLogic CS’ April house price gain of 0.9% attesting to the latter. Durable goods orders also gained 1.7% in May, though much of the orders uptick reportedly came from the transportation sector as easing supply chain pressures prompted car manufacturers to ramp up production.

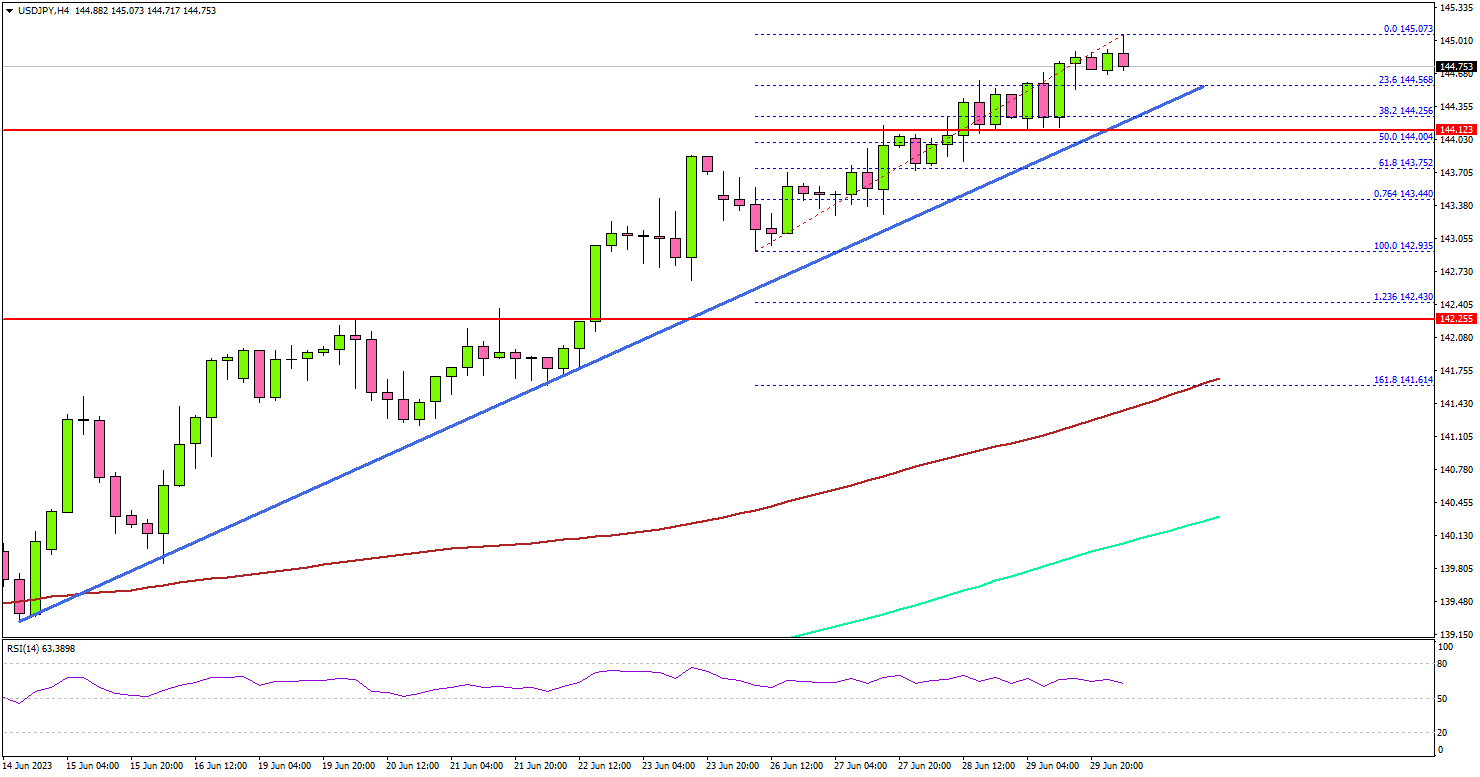

USD/JPY Accelerates Higher and Seems Unstoppable

Key Highlights

- USD/JPY extended gains above the 144.00 resistance zone.

- A key bullish trend line is forming with support near 144.15 on the 4-hour chart.

- EUR/USD is stuck in a range below the 1.1000 resistance.

- GBP/USD extended its decline below the 1.2680 support.

USD/JPY Technical Analysis

The US Dollar started a steady increase above the 142.50 resistance against the Japanese Yen. USD/JPY broke many hurdles near 143.50 to move further into a positive zone.

Looking at the 4-hour chart, the pair gained pace above 144.00. It also settled well above the 144.00 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

It seems like the bulls are aiming for more gains above the 145.00 resistance. On the upside, the first major resistance above 145.00 is near the 145.50 zone.

If there is a move above the 145.50 resistance, the pair could rise toward 146.20. Any more gains might send USD/JPY toward the 147.00 level.

Immediate support is near the 144.20 level. There is also a key bullish trend line forming with support near 144.15 on the same chart. The next major support is near the 143.65 level. If there is a downside break below the 143.65 support, the pair could decline toward the 143.00 support.

Looking at EUR/USD, the pair is struggling to clear the 1.1000 resistance zone and there are chances of a downside correction.

Economic Releases

- UK GDP for Q1 2023 (QoQ) - Forecast +0.1%, versus +0.1% previous.

- Euro Zone CPI for June 2023 (YoY) - Forecast +5.6%, versus +6.1% previous.

- Euro Zone CPI for June 2023 (MoM) - Forecast 0%, versus 0% previous.

EURJPY Bullish Impulse Elliott Wave Structure Calling Higher

Short term view in EURJPY suggests rally from 5.11.2023 low is unfolding as a 5 waves impulse. Up from 5.11.2023 low, wave ((i)) ended at 151.06 and pullback in wave ((ii)) ended at 148.596. The pair then rallies higher in wave ((iii)) in 5 waves of lesser degree. Up from wave ((ii)), wave (i) ended at 150.19 and pullback in wave (ii) ended at 148.61. Pair extended higher in wave (iii) towards 156.93 and pullback in wave (iv) ended at 155.04. Final leg wave (v) ended at 158 which completed wave ((iii)) in higher degree as the 45 minutes chart below shows.

Pullback in wave ((iv)) is currently in progress as a double three Elliott Wave structure. Down from wave ((iii)), wave a ended at 157.216 and wave b ended at 157.919. Wave c lower ended at 157.19 which completed wave (w). Expect pair to rally in wave (x) to correct cycle from 6.28.2023 high (158) before turning lower again in 3 waves to complete wave (y). This should complete wave ((iv)) in higher degree before pair resumes higher again. Near term, as far as pivot at 154 low stays intact, expect pullback to find support in 3, 7, or 11 swing for further upside.

EURJPY 45 Minutes Elliott Wave Chart

EURJPY Elliott Wave ChartEURJPY Elliott Wave Video

https://www.youtube.com/watch?v=zYV9E02jb8c