Sample Category Title

EUR/GBP Weekly Outlook

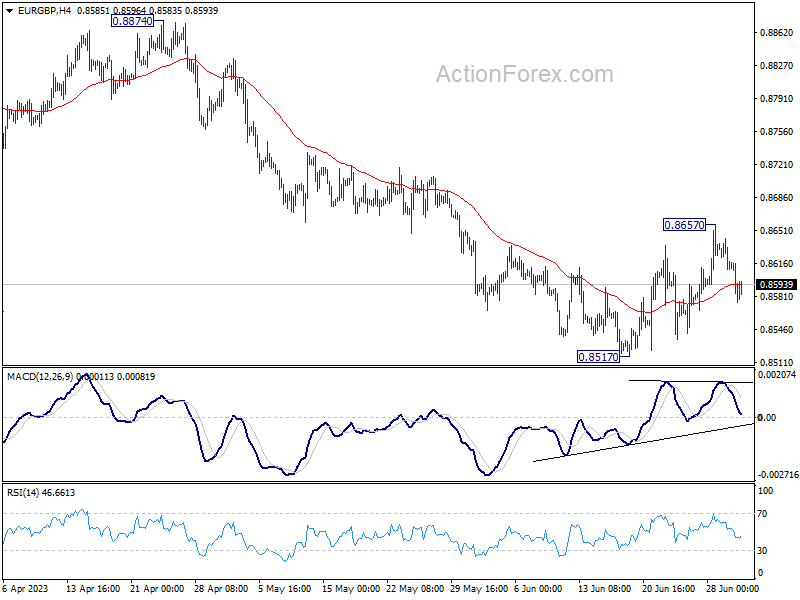

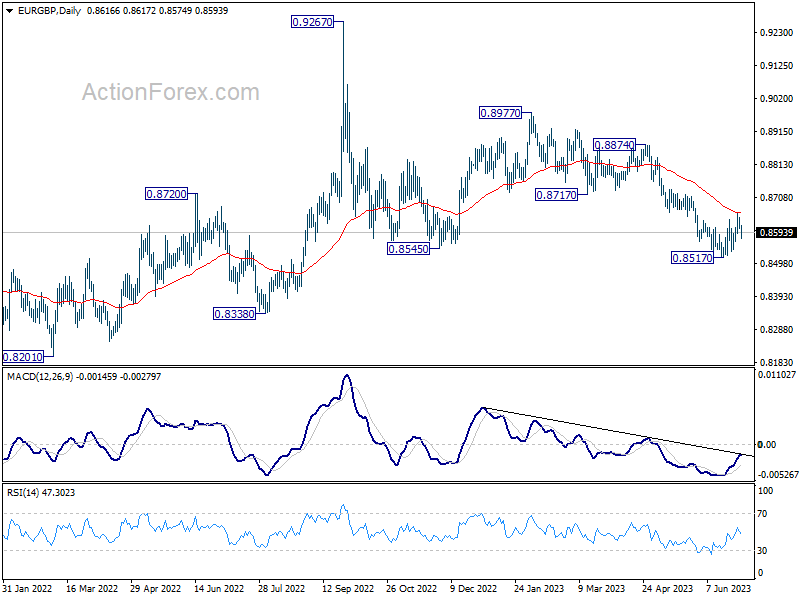

EUR/GBP edged higher to 0.8657 last week but reversed again. Initial bias remains neutral this week first. The rejection by 55 D EMA (now at 0.8655) maintains near term bearishness. Break of 0.8517 will resume the whole decline from 0.8977. On the upside, above 0.8657 resistance will resume the rebound from 0.8517 towards 0.8717 support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

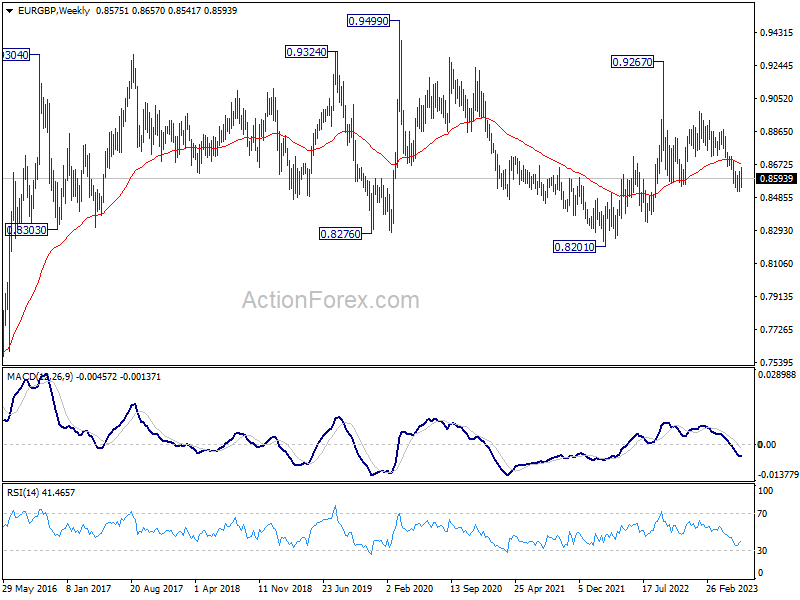

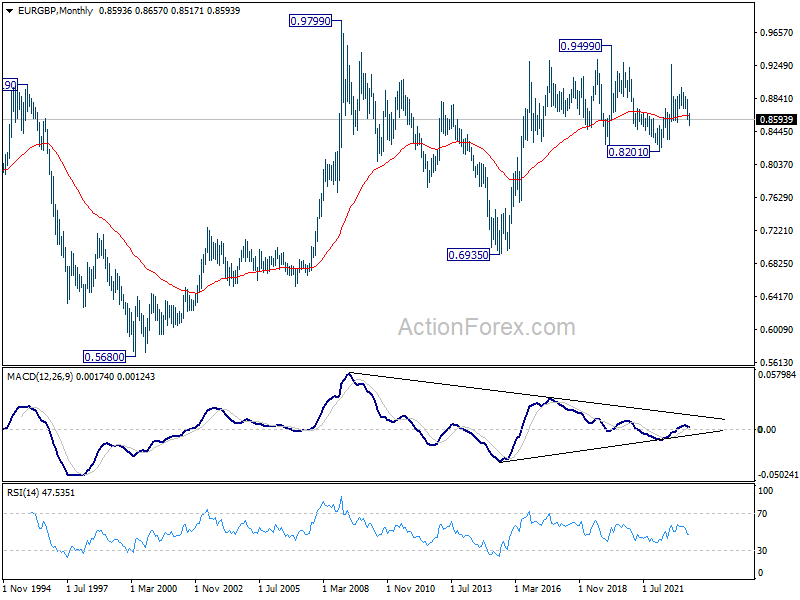

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

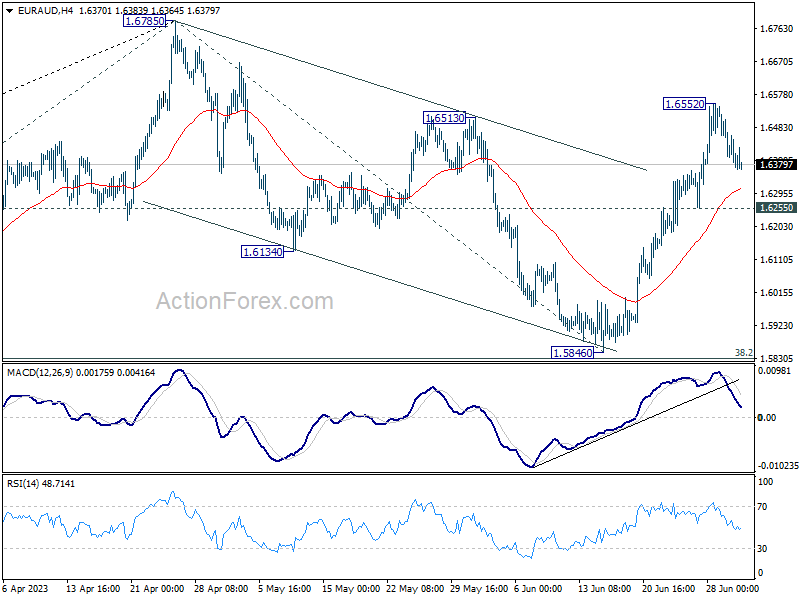

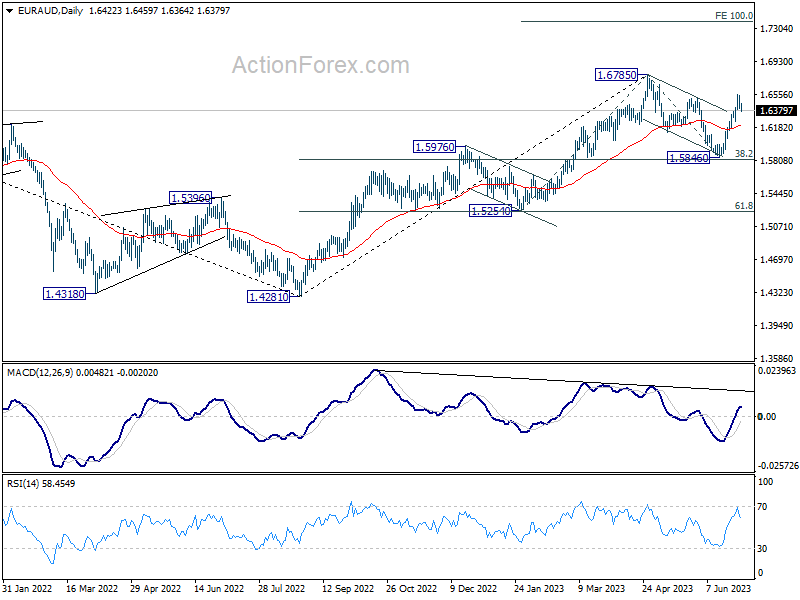

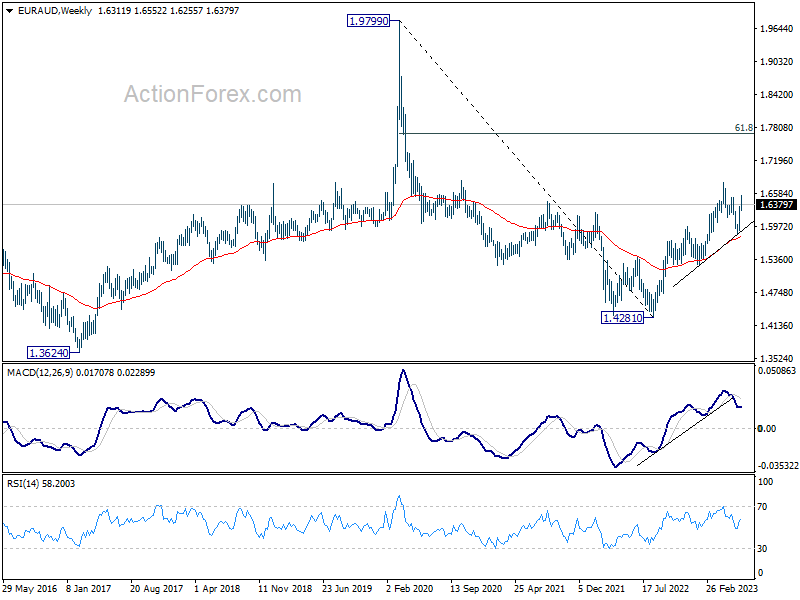

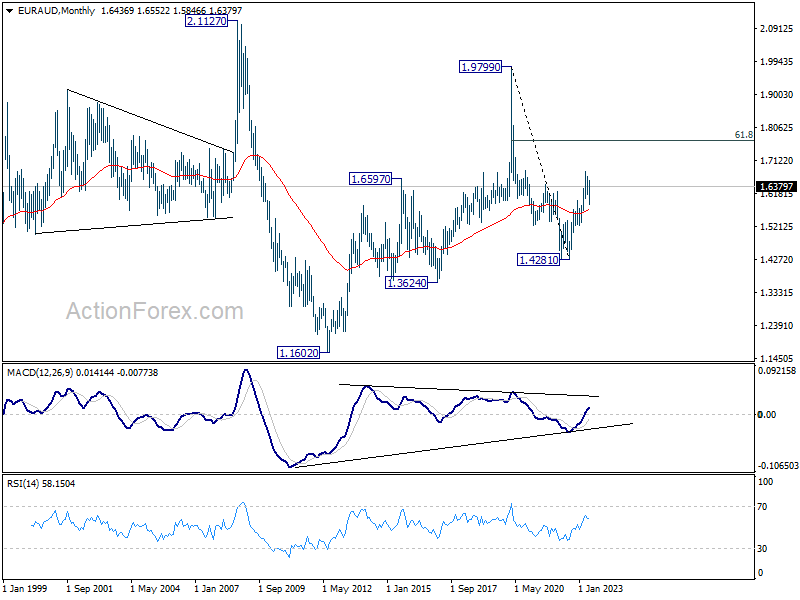

EUR/AUD Weekly Outlook

EUR/AUD rose further to 1.6552 last week, but failed to sustain above 1.6513 resistance and treated. Initial bias remains neutral this week for some consolidations first. But further rally is expected as long as 1.6255 support holds. As noted before, correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, break of 1.6255 will dampen this view and turn bias to the downside for 1.5846 support.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

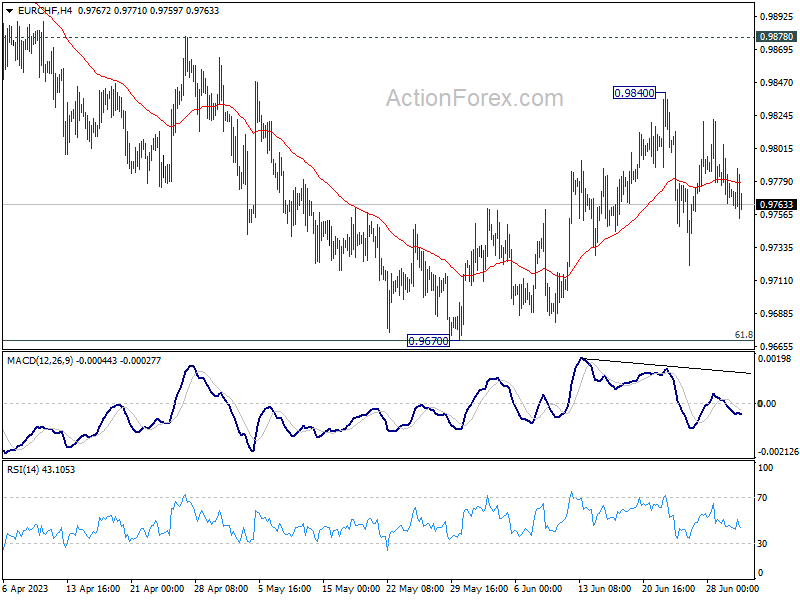

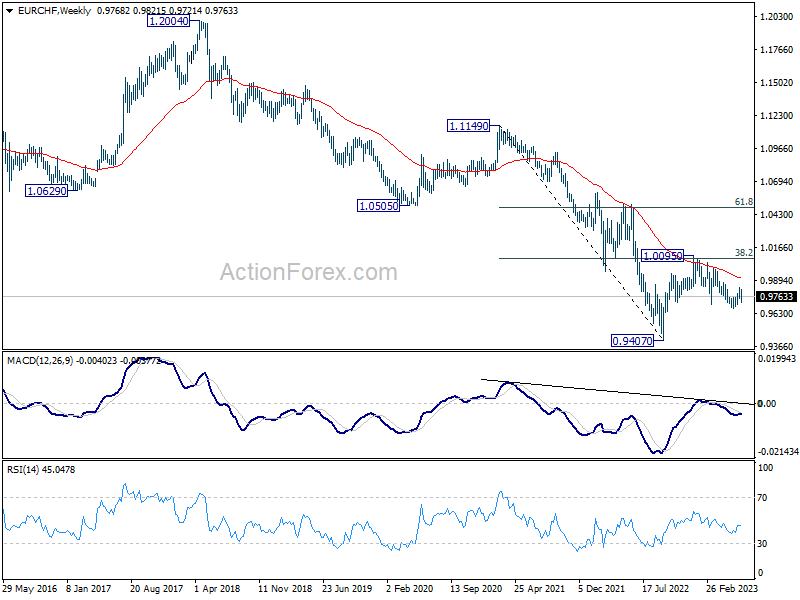

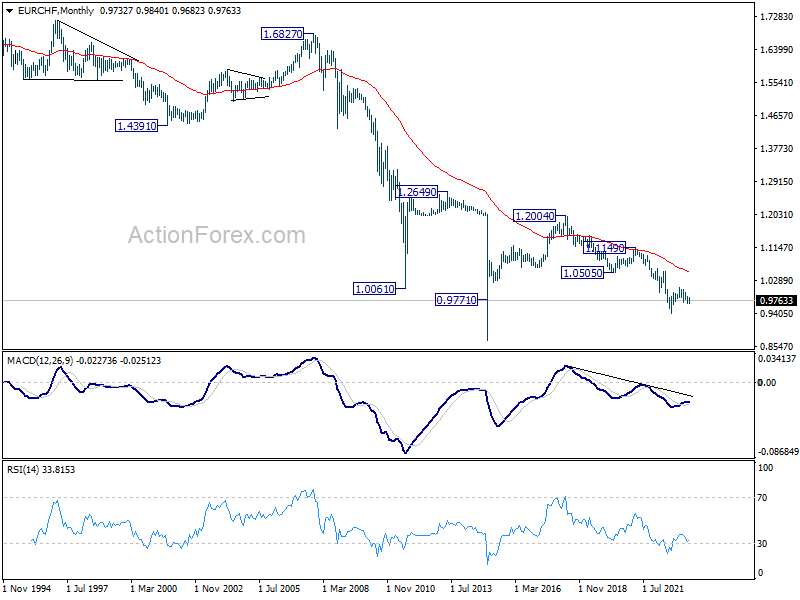

EUR/CHF Weekly Outlook

EUR/CHF stayed in range below 0.9840 last week despite some volatility. Intraday bias remains neutral this week first and outlook is mixed. On the upside break of 0.9840 will resume the choppy rebound from 0.9670. That will also revive the case that whole corrective decline form 1.0095 has completed at 0.9670. Further rally should be seen to 0.9878 resistance next. However, sustained trading below 0.9670 will resume the whole fall from 1.0095.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0484) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Week Ahead – FOMC Minutes and US Jobs Report Eyed, RBA May Hike Again

US

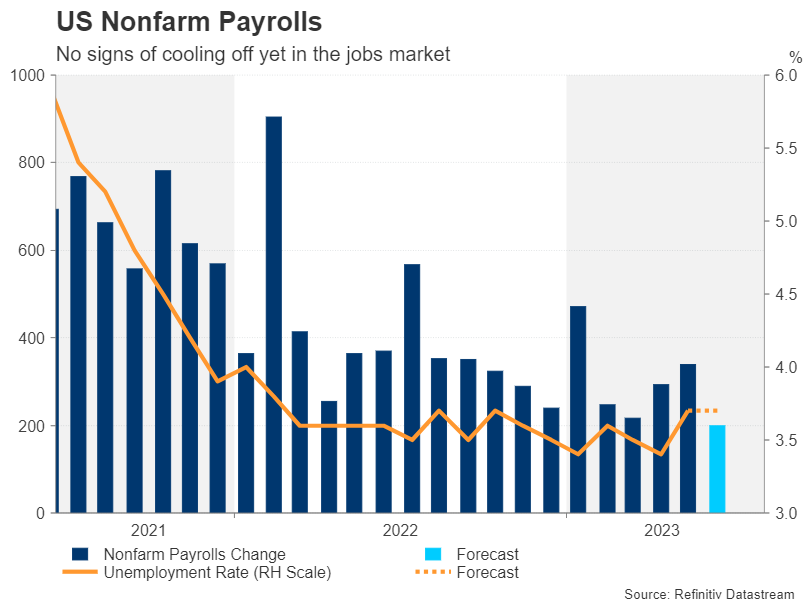

It will be an eventful week, the ISM manufacturing report, the fourth of July Holiday, the Fed Minutes, and the nonfarm payroll report. Wall Street is starting to believe in those Fed dot plots and this week’s economic data points may provide more evidence for the hawks. The ISM manufacturing report is expected to show activity is stabilizing. The Fed minutes will emphasize the fear that core inflation is proving to be stickier. The June US jobs report is expected to show hiring cooled from the 339,000 pace to 200,000 jobs. The unemployment rate however is expected to improve from 3.7% to 3.6%. Wage pressure is also expected to remain steady with a 0.3% increase from a month ago.

We will hear from a couple of Fed speakers this week. Williams participates in a moderated discussion at the 2023 annual meeting of the Central Bank Research Association at the New York Fed. Logan speaks on a panel about the policy challenges for central banks at the Central Bank Research Association annual meeting at Columbia University.

Eurozone

Eurozone inflation data on Friday was very promising and while it likely won’t influence whether the ECB hikes or not in July – Lagarde previously strongly hinted they will – if followed by further signs of disinflation over the summer, it could see the central bank consider a pause in September.

Next week is a little short of tier-one releases but final PMIs on Monday and Wednesday will be of interest, as will another appearance by ECB President Christine Lagarde on Friday.

UK

Very little data of note next week with final PMIs the only highlight. That aside, central bank speak will be followed closely although in the absence of better inflation data, their hands are seemingly tied. The real question ahead of the next meeting is whether they’ll hike by 25 basis points or 50 again.

Russia

A relatively quiet week with PMIs on Monday and Wednesday as the only notable releases. That aside there’s the Russian central bank financial congress on Thursday and Friday so we may hear from Governor Elvira Nabiullina.

South Africa

The whole economy PMI is the only notable economic release or event next week.

Turkey

With the CBRT pivoting toward more conventional monetary policy in the aftermath of the election, the economic data becomes increasingly relevant and next week we’ll get June inflation numbers on Wednesday. The CPI is expected to remain close to 40% but with the currency in freefall, the inflation outlook is likely to get worse before it gets sustainably better. The central bank has stepped back from burning through reserves to support the lira and effectively pay for bad policy choices and that has sent the lira to record lows, falling more than 20% in the last month, alone.

Switzerland

CPI inflation data on Monday is expected to show the headline rate falling back below 2% to 1.8% in June. Markets are still pricing in a 25 basis point hike in September at the moment but that may change if the data matches expectations and, importantly, remains below 2%. Unemployment is also released on Friday.

China

Another set of lackluster data seen on the official NBS manufacturing and non-manufacturing PMIs for June released on Friday. Manufacturing activities continued to contract for the third consecutive month at 49 and growth in the services sector decelerated to a 5-month low at 53.2 from 54.5 in May.

The focus will now turn to the Caixin manufacturing PMI which consists of small and medium enterprises out on Monday. Markets are expecting almost an unchanged condition of 50.2 for June versus 50.9 recorded in May.

The Caixin services PMI will be released on Wednesday with a forecasted slowdown in growth to 56.5 for June from 57.1 in May. Time is running out for the implementation of fresh fiscal stimulus measures.

India

The manufacturing PMI is released on Monday, where the consensus is expecting a slight growth slowdown to 58 for June from 58.7 in May, its strongest reading since October 2020.

A similar trajectory is anticipated for the services PMI on Wednesday where growth is expected to dip to 60.2 in June from 61.2 recorded in May, a continuation of consolidation from April’s near 13-year high of 62.

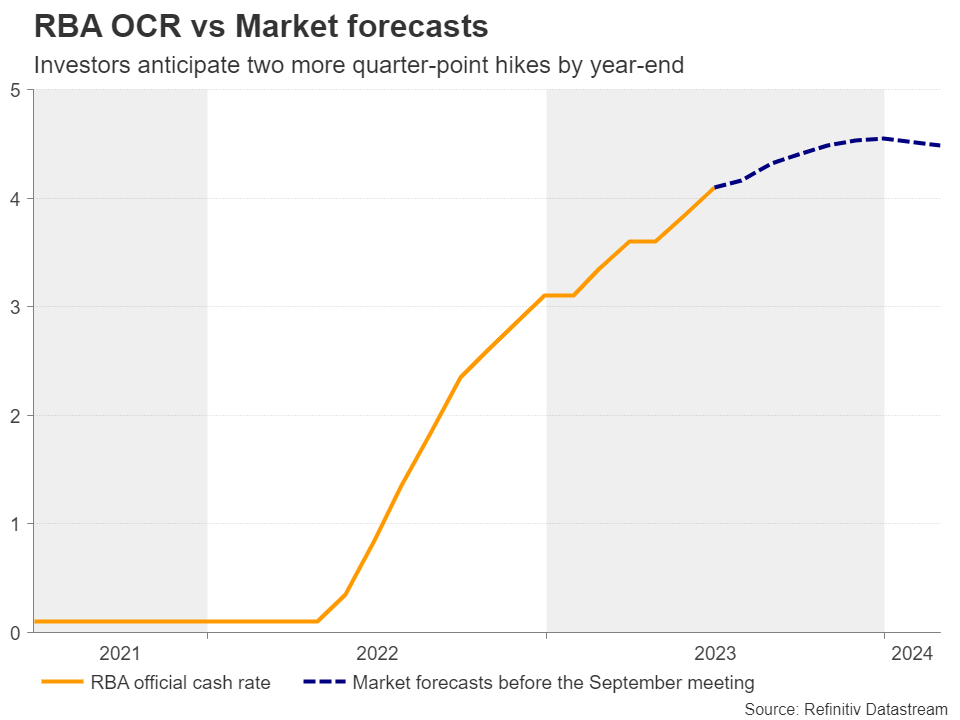

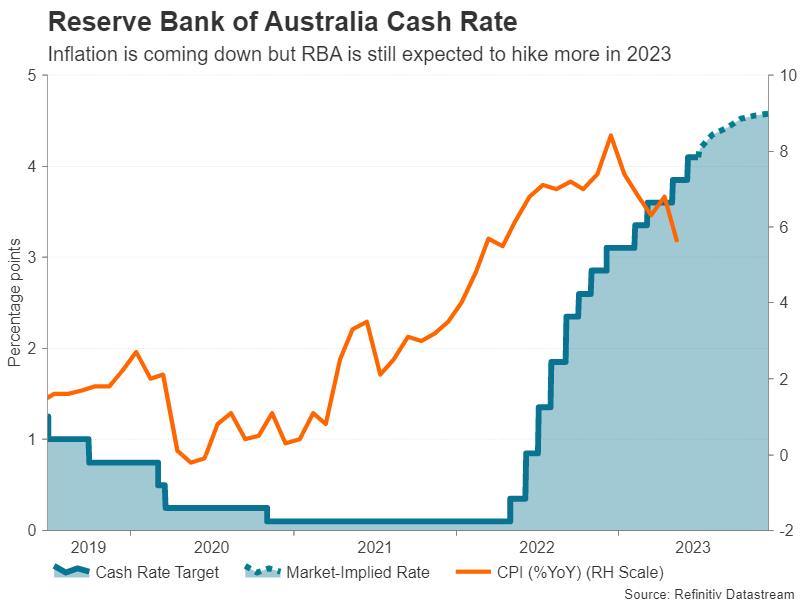

Australia

The key highlight for this week will be RBA’s monetary policy decision on Tuesday. The consensus is calling for another 25 basis points hike on the cash rate, bringing it to 4.35% after recent hawkish guidance inferred from the minutes of the prior meeting.

However, the interest rates futures market has implied a reduction in the odds of a 25 bps hike due to the recent softer-than-expected annualized monthly CPI data for May; 5.6% from 6.8% in April and below expectations of 6.1%. As of 29 June, the ASX 30-day interbank cash rate futures has priced in a 28% chance of 25 basis points (bps) hike on the cash rate, down from a 53% chance priced two weeks ago on 16 June.

On Thursday, we will have the balance of trade for May where April’s surplus of A$11.16 billion is expected to narrow to A$10.5 billion. If it turns out as expected, it will be the narrowest trade surplus since August 2022.

New Zealand

No key data.

Japan

A slew of key sentiment data to keep a lookout for this week. On Monday, big manufacturers, and non-manufacturers sentiment gauges for Q2; the Tankan Large Manufacturers Index is expected to improve to 3 from 1 recorded in Q1. Likewise, a similar improvement is expected on the Tankan Large Non-Manufacturing Index to 22 from 20 in Q1.

On Friday, the attention turns to consumers; household spending for May is expected to see an improvement, a jump to a growth of 0.5% month-on-month from -1.3% recorded in April. On a year-on-year basis, a narrower contraction is expected at -2.4% for May from -4.4% in April, its steepest decrease since June 2021.

Singapore

Several key data to focus on. On Monday, the preliminary URA property index for Q2 where its red-hot growth is expected to dip slightly to 2.9% quarter-on-quarter from 3.3% in Q1. The manufacturing PMI for June is released on Monday as well and is forecasted to improve slightly to 50 from 49.5 in May. If it turns out as expected it put a halt to its prior three months of contraction.

Lastly, growth in retail sales for May is expected to slow to 2.8% year-on-year from 3.6% recorded in April; a potential three consecutive months of growth slowdown.

Economic Calendar

Saturday, July 1

Economic Data/Events

- Deadline for Wagner Group fighters to sign contracts with Russian Defense Ministry

Sunday, July 2

Economic Events

- Pakistan Foreign Minister Zardari meets Japanese counterpart Hayashi in Japan

Monday, July 3

Economic Data/Events

- US construction spending, ISM Manufacturing, light vehicle sales

- Australia building approvals, Melbourne Institute inflation gauge

- China Caixin manufacturing PMI

- Eurozone final manufacturing PMI

- France manufacturing PMI

- Germany manufacturing PMI

- India manufacturing PMI

- Japan Tankan economic survey

- New Zealand building permits

- Singapore home prices, official PMI

- UK Manufacturing PMI

- Canada Day national holiday.

- Thailand’s newly elected parliament to convene

- ECB’s Nagel to speak in Frankfurt

Tuesday, July 4

Economic Data/Events

- US Independence Day national holiday. Financial markets closed

- RBA interest rate decision: Expected to raise rates by 25bps to 4.35%

- Mexico international reserves

- Spain unemployment

Wednesday, July 5

Economic Data/Events

- FOMC issues minutes on June policy meeting

- US factory orders

- China Caixin services and composite PMI

- Eurozone services PMI, PPI

- France industrial production

- Russia GDP

- Singapore retail sales

- Spain industrial production

- Thailand CPI

- The 8th OPEC International Seminar

- Bundesbank symposium

- ECB’s Villeroy speaks at the Paris Europlace forum

- Fed‘s Williams is part of “fireside chat” at the annual meeting of the Central Bank Research Association (CEBRA) at the New York Fed

Thursday, July 6

Economic Data/Events

- US initial jobless claims, trade, June ISM services index: 51.2e v 50.3 prior, job openings

- Australia trade

- Eurozone retail sales

- Germany factory orders

- Poland rate decision: Expected to keep rates steady at 6.75%

- Taiwan CPI

- Bloomberg Conference on “Foreign Direct Investment: Scaling New Heights” in London

- Bank of Russia Governor Nabiullina takes part in the bank’s financial congress in St. Petersburg

- Fed’s Logan speaks on a panel about the policy challenges for central banks at CEBRA meeting

Friday, July 7

Economic Data/Events

- US June Change in nonfarm payrolls: 200Ke v 339K prior, unemployment rate: 3.6%e v 3.7% prior, Average Hourly Earnings M/M: 0.3%e v 0.3% prior

- Canada unemployment

- Chile copper exports, CPI, trade

- China forex reserves

- France trade

- Germany industrial production

- Japan household spending

- Mexico CPI

- ECB’s Christine addresses the REAIX 2023 “Renewing Hope” event in Aix-en-Provence, France

- ECB’s de Guindos speaks at a workshop on “Examining the inflationary surge affecting economies around the world,” organized by King’s College in London

- BOE’s Mann on a panel at the CEBRA meeting in New York

Sovereign Rating Updates

- Hungary (S&P)

Summary 7/3 – 7/7

Monday, Jul 3, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | -2.60% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 3 | 1 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q2 | 22 | 20 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 5 | 3 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q2 | 21 | 15 |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 3.20% | |

| 00:30 | JPY | Manufacturing PMI Jun F | 49.8 | 49.8 |

| 01:00 | AUD | TD Securities Inflation M/M Jun | 0.90% | |

| 01:30 | AUD | Building Permits M/M May | 4.90% | -8.10% |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 50.2 | 50.9 |

| 06:30 | CHF | CPI M/M Jun | 0.20% | 0.30% |

| 06:30 | CHF | CPI Y/Y Jun | 1.80% | 2.20% |

| 07:30 | CHF | Manufacturing PMI Jun | 42.8 | 43.2 |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 45.4 | 45.9 |

| 07:50 | EUR | France Manufacturing PMI Jun F | 45.5 | 45.5 |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 41 | 41 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 43.6 | 43.6 |

| 08:30 | GBP | Manufacturing PMI Jun F | 46.2 | 46.2 |

| 13:45 | USD | Manufacturing PMI Jun F | 46.3 | 46.3 |

| 14:00 | USD | ISM Manufacturing PMI Jun | 47.2 | 46.9 |

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 44.2 | |

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 51.4 | |

| 14:00 | USD | Construction Spending M/M May | 0.50% | 1.20% |

| 22:00 | NZD | NZIER Business Confidence Q2 | -66 | |

| 23:50 | JPY | Monetary Base Y/Y Jun | -0.70% | -1.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | |

| Forecast: | Previous: -2.60% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | |

| Forecast: 3 | Previous: 1 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q2 | |

| Forecast: 22 | Previous: 20 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | |

| Forecast: 5 | Previous: 3 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q2 | |

| Forecast: 21 | Previous: 15 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | |

| Forecast: | Previous: 3.20% | ||

| 00:30 | JPY | Manufacturing PMI Jun F | |

| Forecast: 49.8 | Previous: 49.8 | ||

| 01:00 | AUD | TD Securities Inflation M/M Jun | |

| Forecast: | Previous: 0.90% | ||

| 01:30 | AUD | Building Permits M/M May | |

| Forecast: 4.90% | Previous: -8.10% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jun | |

| Forecast: 50.2 | Previous: 50.9 | ||

| 06:30 | CHF | CPI M/M Jun | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 06:30 | CHF | CPI Y/Y Jun | |

| Forecast: 1.80% | Previous: 2.20% | ||

| 07:30 | CHF | Manufacturing PMI Jun | |

| Forecast: 42.8 | Previous: 43.2 | ||

| 07:45 | EUR | Italy Manufacturing PMI Jun | |

| Forecast: 45.4 | Previous: 45.9 | ||

| 07:50 | EUR | France Manufacturing PMI Jun F | |

| Forecast: 45.5 | Previous: 45.5 | ||

| 07:55 | EUR | Germany Manufacturing PMI Jun F | |

| Forecast: 41 | Previous: 41 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | |

| Forecast: 43.6 | Previous: 43.6 | ||

| 08:30 | GBP | Manufacturing PMI Jun F | |

| Forecast: 46.2 | Previous: 46.2 | ||

| 13:45 | USD | Manufacturing PMI Jun F | |

| Forecast: 46.3 | Previous: 46.3 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | |

| Forecast: 47.2 | Previous: 46.9 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | |

| Forecast: | Previous: 44.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | |

| Forecast: | Previous: 51.4 | ||

| 14:00 | USD | Construction Spending M/M May | |

| Forecast: 0.50% | Previous: 1.20% | ||

| 22:00 | NZD | NZIER Business Confidence Q2 | |

| Forecast: | Previous: -66 | ||

| 23:50 | JPY | Monetary Base Y/Y Jun | |

| Forecast: -0.70% | Previous: -1.10% | ||

Tuesday, Jul 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.10% |

| 06:00 | EUR | Germany Trade Balance (EUR) May | 17.0B | 18.4B |

| 13:30 | CAD | Manufacturing PMI Jun | 49 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.10% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) May | |

| Forecast: 17.0B | Previous: 18.4B | ||

| 13:30 | CAD | Manufacturing PMI Jun | |

| Forecast: | Previous: 49 | ||

Wednesday, Jul 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Jun | 56.2 | 57.1 |

| 06:45 | EUR | France Industrial Output M/M May | -0.20% | 0.80% |

| 07:45 | EUR | Italy Services PMI Jun | 54 | |

| 07:50 | EUR | France Services PMI Jun F | 48 | 48 |

| 07:55 | EUR | Germany Services PMI Jun F | 54.1 | 54.1 |

| 08:00 | EUR | Eurozone Services PMI Jun F | 52.4 | 52.4 |

| 08:30 | GBP | Services PMI Jun F | 53.7 | 53.7 |

| 09:00 | EUR | Eurozone PPI M/M May | -3.90% | -3.20% |

| 09:00 | EUR | Eurozone PPI Y/Y May | 6.10% | 1.00% |

| 14:00 | USD | Factory Orders M/M May | 0.60% | 0.40% |

| 18:00 | USD | FOMC Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Jun | |

| Forecast: 56.2 | Previous: 57.1 | ||

| 06:45 | EUR | France Industrial Output M/M May | |

| Forecast: -0.20% | Previous: 0.80% | ||

| 07:45 | EUR | Italy Services PMI Jun | |

| Forecast: | Previous: 54 | ||

| 07:50 | EUR | France Services PMI Jun F | |

| Forecast: 48 | Previous: 48 | ||

| 07:55 | EUR | Germany Services PMI Jun F | |

| Forecast: 54.1 | Previous: 54.1 | ||

| 08:00 | EUR | Eurozone Services PMI Jun F | |

| Forecast: 52.4 | Previous: 52.4 | ||

| 08:30 | GBP | Services PMI Jun F | |

| Forecast: 53.7 | Previous: 53.7 | ||

| 09:00 | EUR | Eurozone PPI M/M May | |

| Forecast: -3.90% | Previous: -3.20% | ||

| 09:00 | EUR | Eurozone PPI Y/Y May | |

| Forecast: 6.10% | Previous: 1.00% | ||

| 14:00 | USD | Factory Orders M/M May | |

| Forecast: 0.60% | Previous: 0.40% | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

Thursday, Jul 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 10.70B | 11.16B |

| 06:00 | EUR | Germany Factory Orders M/M May | 1.50% | -0.40% |

| 08:30 | GBP | Construction PMI Jun | 50.9 | 51.6 |

| 09:00 | EUR | Eurozone Retail Sales M/M May | 0.20% | 0.00% |

| 11:30 | USD | Challenger Job Cuts Jun | 80.089K | |

| 12:15 | USD | ADP Employment Change Jun | 250K | 278K |

| 12:30 | USD | Initial Jobless Claims (Jun 30) | 249K | 239K |

| 12:30 | USD | Trade Balance (USD) May | -68.2B | -74.6B |

| 12:30 | CAD | Trade Balance (CAD) May | 1.5B | 1.9B |

| 13:45 | USD | Services PMI Jun F | 54.1 | 54.1 |

| 14:00 | USD | ISM Services PMI Jun | 51.3 | 50.3 |

| 14:30 | USD | Crude Oil Inventories | -9.6M | |

| 23:30 | JPY | Labor Cash Earnings Y/Y May | 1.20% | 1.00% |

| 23:30 | JPY | Overall Household Spending Y/Y May | -2.40% | -4.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | |

| Forecast: 10.70B | Previous: 11.16B | ||

| 06:00 | EUR | Germany Factory Orders M/M May | |

| Forecast: 1.50% | Previous: -0.40% | ||

| 08:30 | GBP | Construction PMI Jun | |

| Forecast: 50.9 | Previous: 51.6 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M May | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 11:30 | USD | Challenger Job Cuts Jun | |

| Forecast: | Previous: 80.089K | ||

| 12:15 | USD | ADP Employment Change Jun | |

| Forecast: 250K | Previous: 278K | ||

| 12:30 | USD | Initial Jobless Claims (Jun 30) | |

| Forecast: 249K | Previous: 239K | ||

| 12:30 | USD | Trade Balance (USD) May | |

| Forecast: -68.2B | Previous: -74.6B | ||

| 12:30 | CAD | Trade Balance (CAD) May | |

| Forecast: 1.5B | Previous: 1.9B | ||

| 13:45 | USD | Services PMI Jun F | |

| Forecast: 54.1 | Previous: 54.1 | ||

| 14:00 | USD | ISM Services PMI Jun | |

| Forecast: 51.3 | Previous: 50.3 | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -9.6M | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y May | |

| Forecast: 1.20% | Previous: 1.00% | ||

| 23:30 | JPY | Overall Household Spending Y/Y May | |

| Forecast: -2.40% | Previous: -4.40% | ||

Friday, Jul 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index May P | 97.50% | 96.80% |

| 05:45 | CHF | Unemployment Rate Jun | 2.00% | 2.00% |

| 06:00 | EUR | Germany Industrial Production M/M May | 0.10% | 0.30% |

| 06:45 | EUR | France Trade Balance (EUR) May | -9.5B | -9.7B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 734B | |

| 08:00 | EUR | Italy Retail Sales M/M May | 0.10% | 0.20% |

| 12:30 | USD | Nonfarm Payrolls Jun | 220K | 339K |

| 12:30 | USD | Unemployment Rate Jun | 3.70% | 3.70% |

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.30% | 0.30% |

| 12:30 | CAD | Net Change in Employment Jun | -17.3K | |

| 12:30 | CAD | Unemployment Rate Jun | 5.20% | |

| 14:00 | CAD | Ivey PMI Jun | 50.9 | 53.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index May P | |

| Forecast: 97.50% | Previous: 96.80% | ||

| 05:45 | CHF | Unemployment Rate Jun | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 06:00 | EUR | Germany Industrial Production M/M May | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 06:45 | EUR | France Trade Balance (EUR) May | |

| Forecast: -9.5B | Previous: -9.7B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | |

| Forecast: | Previous: 734B | ||

| 08:00 | EUR | Italy Retail Sales M/M May | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 12:30 | USD | Nonfarm Payrolls Jun | |

| Forecast: 220K | Previous: 339K | ||

| 12:30 | USD | Unemployment Rate Jun | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jun | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | CAD | Net Change in Employment Jun | |

| Forecast: | Previous: -17.3K | ||

| 12:30 | CAD | Unemployment Rate Jun | |

| Forecast: | Previous: 5.20% | ||

| 14:00 | CAD | Ivey PMI Jun | |

| Forecast: 50.9 | Previous: 53.5 | ||

The Weekly Bottom Line: Healthy Data Keep Pressure on Fed

U.S. Highlights

- A week’s worth of solid data did little to contradict Fed Chair Powell’s comments suggesting more monetary tightening is on the way.

- However, May’s personal consumption expenditure (PCE) report did provide a bit of reassurance for the Fed that demand is slowing down as real expenditure growth has been flat in three of the past four months.

- The problem remains that inflation is showing little sign of relenting and Fed officials are going to stay focused on tightening policy to cool the price pressure.

Canadian Highlights

- With less than two weeks to go until the next Bank of Canada (BoC) rate decision, economic data this week prompted financial markets to cement expectations for another rate hike this summer.

- Headline inflation did cool to the lowest pace in two years in May. But, progress on the BoC’s core measures is much slower. This raises concerns that inflation will remain stuck above the Bank’s 2% target.

- On the growth side, industry-level GDP signaled that the population driven boost to GDP growth during the winter continued into the spring. Growth appears to be running ahead of the BoC’s expectations yet again.

U.S. – Healthy Data Keep Pressure on Fed

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

First up, activity in the housing market has ticked up. New home sales rose to their highest level since February 2022 in May. The market for new single-family homes troughed in July 2022 and has been trending upwards since, as inventories in the existing home market remain tight (see commentary). Sales in the existing market did move up in May as well, as a solid labor market helps drive demand.

Consumers’ moods have also been improving lately as the Conference Board consumer confidence index for June jumped up to its highest reading since January 2022. With both consumers’ assessment of the present situation and future expectations moved up on the month. Overall, consumers are not as confident as they were prior to the pandemic, likely as they contend with high inflation, but their higher spirits defy the recession warnings.

The good news didn’t just stop there. The industrial side of the economy saw manufacturers’ new orders of durable goods blow out expectations for a contraction, with a healthy advance. Taking a closer look at a key indicator of business investment, new orders excluding defense and aircraft advanced a solid 0.7% in the month, and 0.3% month-on-month when stripping out the effects of inflation.

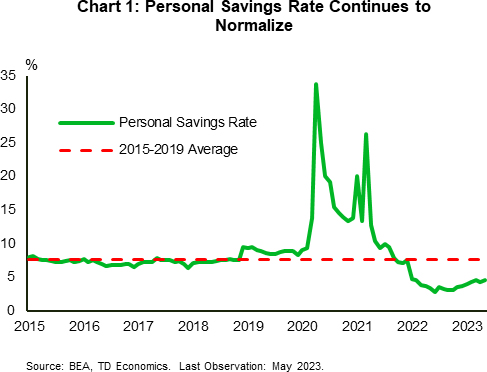

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

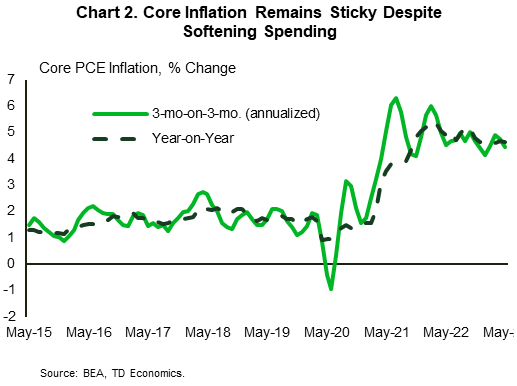

However, inflation continues to be problematic. Core PCE inflation (Chart 2) is showing little sign of relenting, up 4.6% y/y, with the near-term trend cruising along at 4.4% (annualized). Inflation has been stuck well above the two percent target, which is likely to keep officials focused on tightening policy to cool it down. Markets are looking for the Fed to hike rates again this year by another 25 basis points – taking the policy rate to a 22-year high of 5.5%. The FOMC’s next decision is at the end of July, giving it some time to see a few more readings on economic momentum before making its decision. Next week’s June jobs data is likely to be a key piece of it’s calculus.

Canada – Inflation Eases While Population Pops

The countdown is on to the next Bank of Canada rate decision on July 12th, and there was plenty economic data this week for them to factor into their thinking. All told, the data suggest that monetary policy has yet to exert enough of a braking force on the economy and inflation. Financial markets have further cemented expectations for a BoC interest rate hike this summer, leading the Canada 2-year yield to establish a new cycle high.

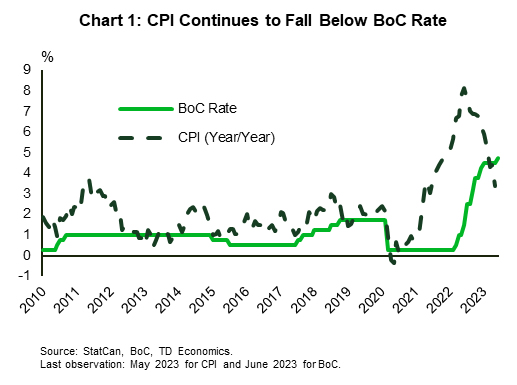

Headline inflation cooled notably in May, but core price pressures are coming down at a glacial pace. The Consumer Price Index was up 3.4% year-on-year (y/y) in May, down from 4.4% y/y in April, more than a percent below the BoC's policy rate (Chart 1). Gasoline was the main contributor, with prices at the pump now far below year ago levels . Unfortunately, food inflation remained a problem, with prices up 8.3% y/y, having barely budged from their peak in January 2023.

The Bank of Canada's core inflation metrics (trimmed mean and median) decelerated, but to a lesser degree than the headline figure, averaging 3.9% y/y in May, versus 4.3% y/y in April. More concerning was our measure of 'supercore' inflation that reflects cyclically driven services inflation, which at 5.5% y/y is little changed from April's reading of 5.7% y/y. Travel was the main driver here as Canadians prepare for summer vacations.

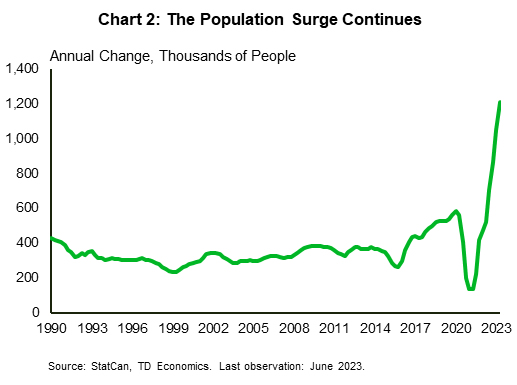

The surge in Canada's population over the past year has been a big swing factor in the economy. Canada welcomed 292k more people in the first three months of the year, bringing the 12-month total to above 1.2 million (Chart 2). With more people living and working in the country, consumer spending surged by nearly 6% quarter-on-quarter annualized (q/q) in the first quarter. Firms have struggled to keep up with rising demand, so they have been hiring more workers, boosting wages, and raising prices.

We received some insight this week into how much of this momentum has carried over into the second with the release of industry GDP. While the print for April was unchanged, the flash estimate for May showed a big increase. This sets up second quarter GDP to come in above the BoC's forecast. At the same time, the BoC released its Business Outlook Survey and its companion Canadian Survey of Consumer Expectations. While both have signaled caution going forward, there is growing belief that the worst is over "as uncertainty about the path of future interest rates and concerns of a recession fade".

The Bank of Canada has less than two weeks before its next interest rate decision. Although there has been a notable improvement in overall Canadian inflation, underlying core measures reveal a big challenge going forward. The economy has continued to grow at a very healthy clip, supported by a surging population. This has kept up pressure on wages and domestic prices. The BoC will have a few more data points next week, including the key June employment data, to help it decide what to do next. But thus far, the data have been leaning towards another hike in July.

Weekly Economic & Financial Commentary: Higher for Longer

Summary

United States: Hot Economic Data Accompanies the Heart of Summer

- The U.S. economic data released this week were almost universally strong. Jobless claims dipped lower, the housing market data continued to surprise to the upside and there were signs of life in business equipment spending.

- Next week: Construction Spending (Mon.), ISM Indices (Mon. & Thur.), Employment (Fri.)

International: Global Inflation Continues to Decelerate

- This week's data point to an ongoing improvement in global inflation trends, though perhaps not quite as quickly as might ideally be hoped. The Eurozone CPI slowed to 5.5% year-over-year, but core inflation actually ticked higher to 5.4%. Canada's May headline CPI slowed to 3.4% and Australia's May headline CPI slowed to 5.6%, though in both of those countries the slowing in core inflation was less pronounced.

- Next week: Japan Tankan Survey (Mon.), RBA Policy Rate (Tue.), Mexico CPI (Fri.)

Interest Rate Watch: Higher for Longer

- Recent policy actions and comments by central bank officials have convinced market participants that rates are heading higher and that they will remain elevated for longer than previously thought.

Topic of the Week: Immigration Flows Have Fully Rebounded After the Pandemic

- After essentially halting during the pandemic, U.S. immigration levels have rebounded. Immigration flows as a percentage of annual population growth rose above its pre-pandemic 10-year average in 2022, providing a boost to the population and labor force.

Will RBA Surprise the Market for a Third Time?

On Tuesday, at 04:30 GMT, the Reserve Bank of Australia (RBA) will announce its July monetary policy decision. After two consecutive surprise hikes, most market participants believe that policymakers will step to the sidelines this time, but economists foresee a 25bps hike by a very slim majority. Will the RBA go against market bets for the third time in a row?

The RBA confounded market bets in May and June

At its June meeting, the RBA caught the market off guard for a second straight time, raising the cash rate target by 25bps to 4.10% and noting that some further tightening may be required to ensure that inflation returns to target in a reasonable timeframe, but also that this will depend upon how the economy and inflation evolve.

Although there had been some expectations that the RBA could hit the hike button due to the rebound in the monthly year-on-year inflation print for April and the increase in the country’s minimum wage by 5.75%, most market participants were expecting officials to stay sidelined just after the May hike.

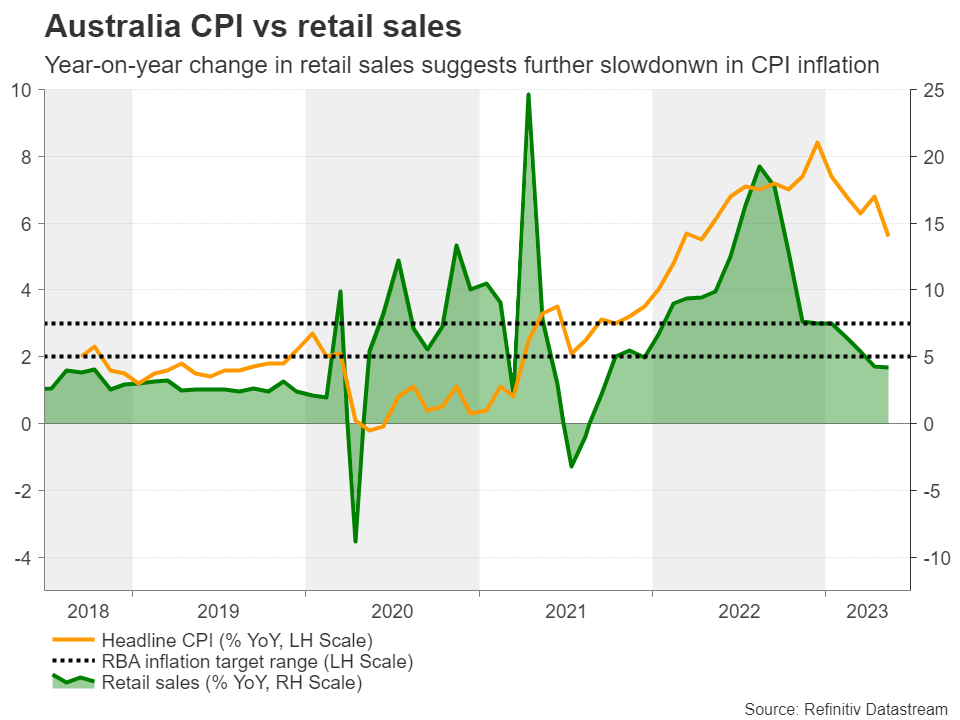

Inflation slows abruptly in May

Since then, GDP data showed that the economy slowed by more than expected in Q1, but also that the labor market gained more jobs than forecast in May, which pushed the unemployment rate down to 3.6% from 3.7%. Both the preliminary manufacturing and services PMIs came in better than expected, but the manufacturing index stayed in contractionary territory and the services one slid to just seven tenths of a point above the 50-stagnation mark.

Most importantly, the monthly y/y CPI rate for May dropped to 5.6% from 6.8%, extending the downtrend that started after the rate peaked at 8.4% in January. Yes, retail sales for the same month grew 0.7%, but the y/y rate slightly dropped to 4.22% from 4.25%, which is the slowest annual increase since September 2021.

Investors see an August hike as more likely

With all that in mind, investors are confident that two more quarter-point hikes may be on the cards by this central bank, but they assign only a 37% chance for a hike at this gathering. The remaining 63% probability points to no action, which appears reasonable pricing given the abrupt slowdown in inflation in May. Although the headline CPI rate is still well above the upper bound of the RBA’s 2-3% target range, officials may prefer to wait for more data to see whether past hikes could still weigh on price pressures.

That said, a very slim majority of economists polled by Reuters are expecting a 25bps hike next week, while an August increase seems more sensible to the eyes of investors, who are nearly certain according to their implied rate path.

Asymmetrical risks surround the aussie

Therefore, should officials decide to take the sidelines, the aussie is unlikely to fall much, especially if they clearly telegraph an August hike. For the currency to fall sharply, the Bank may need to take the sidelines and adopt a softer language about its future plans than it did in June. Nonetheless, taking into account the data, this seems a very unlikely scenario.

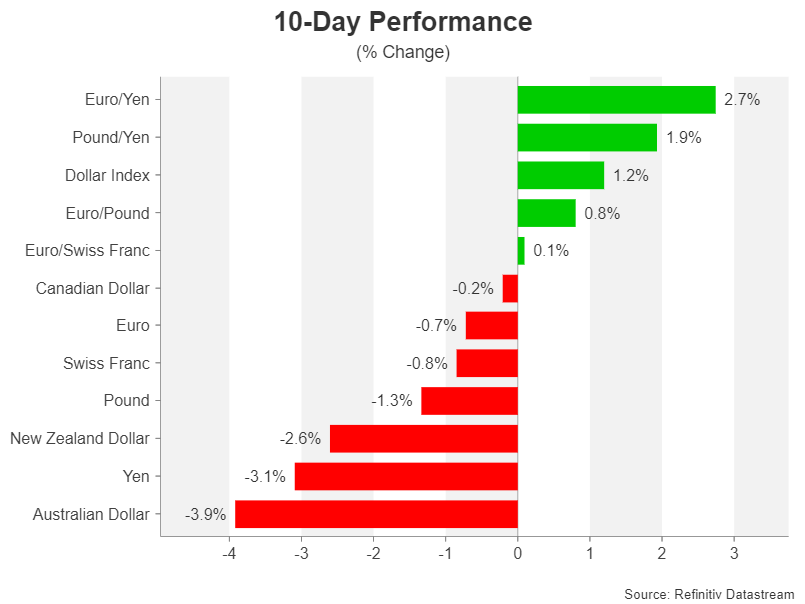

Now, in case the RBA does not hesitate to go against market bets for a third consecutive time and decides to press the hike button, the aussie is likely to rally. Given the current market pricing and the fact that the aussie has fallen around 4.5% against its US counterpart in the last two weeks, a rally due to a hike could be larger than a potential slide due to a hawkish pause. In other words, the risks may be asymmetrical.

Aussie/dollar trades within a range

Aussie/dollar fell sharply the last couple of weeks, returning within, and even approaching the lower bound of a sideways range that’s been containing most of the price action since February 24. A potential decline below that lower bound of the range at 0.6575 could paint a darker picture and perhaps set the stage for declines towards the 0.6490 barrier, which offered support in May.

On the upside, a potential rebound due to a hike could result in a test at the high of June 27 at 0.6720, but with the rate still within the aforementioned range, the outlook is unlikely to be considered bullish. For the picture to brighten a break above 0.6795 may be needed.

Week Ahead – Will US Nonfarm Payrolls and RBA Decision Rock the Boat?

Markets have been left somewhat bruised from a fresh round of hawkish gunfire from central bank chiefs, so nerves are running high ahead of the June jobs report out of America. The ISM PMIs and the Fed meeting minutes are also expected to send speculation about a July rate hike into overdrive. However, Australia’s Reserve Bank might decide against raising interest rates thrice in a row. The yen, meanwhile, will be hoping that Japanese data will provide some relief from its selloff.

Can NFP report and ISM PMIs lift the rate path fog?

Investors are being dragged kicking and screaming by policymakers to come round to the thinking that monetary policy tightening has still some way to go. But there was some progress over the last week for the Fed’s Jay Powell and his European counterparts, who once again made the case for ‘higher for longer’.

For Powell, the job of convincing the markets has been somewhat harder as inflation poses less of a threat in America right now than it does in Britain and the Eurozone. However, the Fed is unlikely to be satisfied until it sees clear signs that the labour market is becoming less tight and wage growth is slowing.

Nonfarm payrolls jumped by 339k in May, blowing past expectations, and even though the unemployment rate spiked up, all the indications are that the US labour market continues to sizzle. The projection for June is a figure of 200k – consistent with recent months’ forecast range. The jobless rate is expected to remain at 3.7%, while average hourly earnings are forecast to have risen by 0.3% m/m in June, unchanged from the prior month.

Unless there is a big shock in the data – either positive or negative, the report may not produce a decisive enough result that could steer policymakers in a specific direction. Hence, investors will also be looking at the other releases of the week, particularly the ISM manufacturing and non-manufacturing PMIs on Monday and Thursday, respectively. A further deterioration in the ISM surveys in June could revive recession fears after Powell played down the prospect in a panel discussion organized by the ECB in Portugal.

Factory orders due Wednesday and the ADP employment survey on Thursday will also be watched. US markets will be closed on Tuesday for the 4th of July Independence Day celebrations. The minutes of the Fed’s June policy meeting will be important too on Wednesday, although with Powell having made two major public appearances since, it’s unlikely the minutes will offer any new insight.

For the US dollar, which has retraced more than half of its June losses, it will be difficult to extend its recovery unless the data can boost the probability for additional rate hikes in 2023 more than Powell already has.

RBA might pause again

The Reserve Bank of Australia meets on Tuesday for its July policy decision and following the drop in the monthly consumer price index, there is less urgency for policymakers to increase borrowing costs for a third straight meeting. The RBA skipped a hike in April but resumed in May and June. The fall in the 12-month CPI rate to 5.6% in June, combined with soft PMI figures for the same month and ongoing doubts about the Chinese economy, suggests it’s time to pause this month.

However, a third consecutive hike cannot be completely ruled out as the labour market continues to tighten. Employment rose by an impressive 76k in May. Even if the RBA skips a move in July, it will likely maintain a hawkish stance, keeping the door open to further tightening in the future.

The net effect of the meeting outcome might therefore be neutral for the Australian dollar in the most dovish scenario and broader market risk sentiment will probably be a bigger driver for the currency.

Canadian jobs last big clue before next BoC decision

Another central bank that will be pondering whether its next move should be a pause or hike is the Bank of Canada. Next week’s employment report could be crucial in helping policymakers make up their minds before the July 12 decision. Employment in Canada unexpectedly fell in May so another weak report in June could almost certainly keep the BoC on hold in July, especially as there was a downside surprise in inflation too.

This would put the Canadian dollar at significant risk of paring back its month-long gains versus the US dollar.

German data may put euro bulls to the test

In the euro area, it will be a relatively quiet week, with May producer prices (Wednesday) and retail sales (Thursday) on the agenda. However, investors will also be keeping an eye on potential revisions to the June PMIs when the final prints are released on Monday and Wednesday. The flash PMIs were not very encouraging, raising question marks about how much longer the Eurozone economy can remain resilient in the face of rising interest rates and sluggish export markets such as China.

Moreover, key indicators out of Germany will likely attract some attention for traders as Europe’s largest economy is already in a recession and the outlook is not very bright either amid a European Central Bank determined to squash inflation with more rate increases. German trade figures are out on Tuesday, to be followed by industrial orders on Thursday and industrial production on Friday, all for May.

The euro, which has been more successful at fending off the dollar’s latest advances than other majors, could come under pressure if the incoming data keeps surprising to the downside.

Is there any hope for the battered yen?

The Japanese yen on the other hand has been badly beaten by the dollar’s resurgence, slumping to more than seven-month lows. The Bank of Japan is refusing to alter its policy course despite an improving economic backdrop and a pickup in underlying inflation. Whilst there have been some subtle shifts in the undertones, the BoJ has mostly maintained its ultra-dovish language and investors are betting that the status quo won’t change anytime soon, pushing the yen to multi-year lows against its main peers.

Next week’s data are not expected to turn the tide for the yen, although a broadly upbeat set of numbers might provide some support for the safe-haven currency.

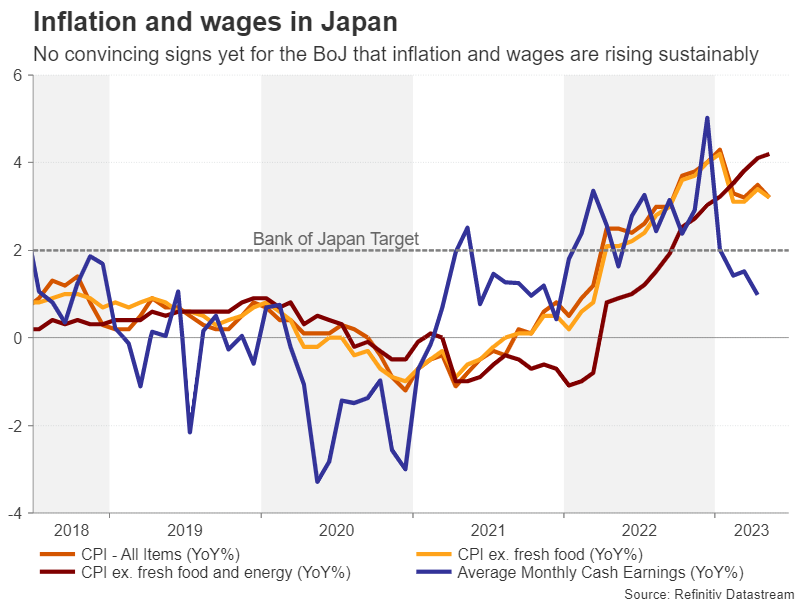

The Bank of Japan’s quarterly Tankan business survey will start the week on Monday. Forecasts point to growing optimism among businesses for the current and next quarters, as well as plans to increase capital expenditure. Household spending stats will be watched on Friday, along with average cash earnings for May.

Sustainably higher wage growth is a key criterion for the BoJ to begin unwinding its stimulus policies. However, despite reports of bumper pay deals in this year’s Spring wage negotiations, wage growth stood at just 0.8% year-on-year in April. An acceleration in May could increase speculation about a policy change by the Bank of Japan at its July policy meeting, potentially lifting the yen.

Weekly Focus – Two-Sided Risks Ahead for H2

The first half of 2023 was characterized by economic growth surprising to the upside, but also inflation proving stickier than expected. As such, when policymakers from around the world gathered in Sintra this week for the ECB's Forum on Central Banking, it was no surprise that (aside from Bank of Japan), central banks maintained a tightening bias towards H2.

ECB's Lagarde reiterated that a 25bp hike in July is almost given, and Fed's Powell noted that despite the pause in June, going back to consecutive hikes is not off the table. On Thursday, Riksbank hiked rates by 25bp and signalled at least one more 25bp hike going forward, in line with our expectations.

In July, markets' focus will revert back towards macro data. Recent releases have been mixed, with this week's German Ifo Business Climate cooling further in June, but US Conference Board's consumer confidence rebounding - defying contrasting signals from PMIs last week. We still think growth is set to remain weak across most developed economies for the remainder of the year, with the US headed for a modest recession.

Next week brings a series of important US data releases, including ISM, JOLTs and the June Jobs Report, which will be key to watch ahead of the upcoming FOMC meeting on 26 July. Following a positive revision to Q1 GDP figures and lower jobless claims, markets are pricing the peak Fed Funds Rate at 35bp above the current level by November, implying a 40% probability of two more hikes. We forecast June non-farm payrolls at 180k, and if we do see further signs of wage inflation cooling followed by a lower Core CPI release on 12 July, we think the Fed could still end up staying on hold in the next meeting.

Euro Area inflation cooled further to 5.5% in June. Core inflation ticked slightly higher to 5.4%, but part of the increase reflects base effect from the last year's German public transport subsidies. That said, we still think the ECB will hike both in July and September.

While Ueda refrained from hawkish hints in Sintra, we still think it is only a matter of time before the Bank of Japan will acknowledge the continuously building inflationary pressure in Japan by easing the yield curve control, which we expect to happen either at the next meeting on 28 July or in September. China is the only major economy where we expect further policy stimulus measures to be announced over summer.

After surprising both analysts and markets by hiking 50bp in June, we expect the Bank of England to hike by 25bp on 3 August. However, the return to smaller hikes depends on data not surprising significantly to the upside. BoE's focus remains on wages and services inflation, so job market report (11 July) and CPI (19 July) will be the key to watch.

Besides macro, geopolitics came back on the radar last weekend. In Russia, the attempted mutiny by Yevgeny Prigozhin, the leader of the Wagner mercenary group, ended as quickly as it began. But even so, Putin's position appears to have been weakened as his closest allies might not be as unified in support as previously thought. In our baseline expectation, we do not foresee major breakthroughs in the war in Ukraine over the coming weeks, but the Russian internal instability remains a key source of potential volatility for now.