Sample Category Title

The Weekly Bottom Line: Keepin’ At It… For Now

U.S. Highlights

- The Federal Reserve met expectations and held the policy rate steady at 5.0-5.25%, but left the door open to further rate hikes later this year.

- The Fed’s Summary of Economic Projections underscored a more optimistic outlook, and an upward revision on the future path of the fed funds rate to 5.75% (previously 5.25%).

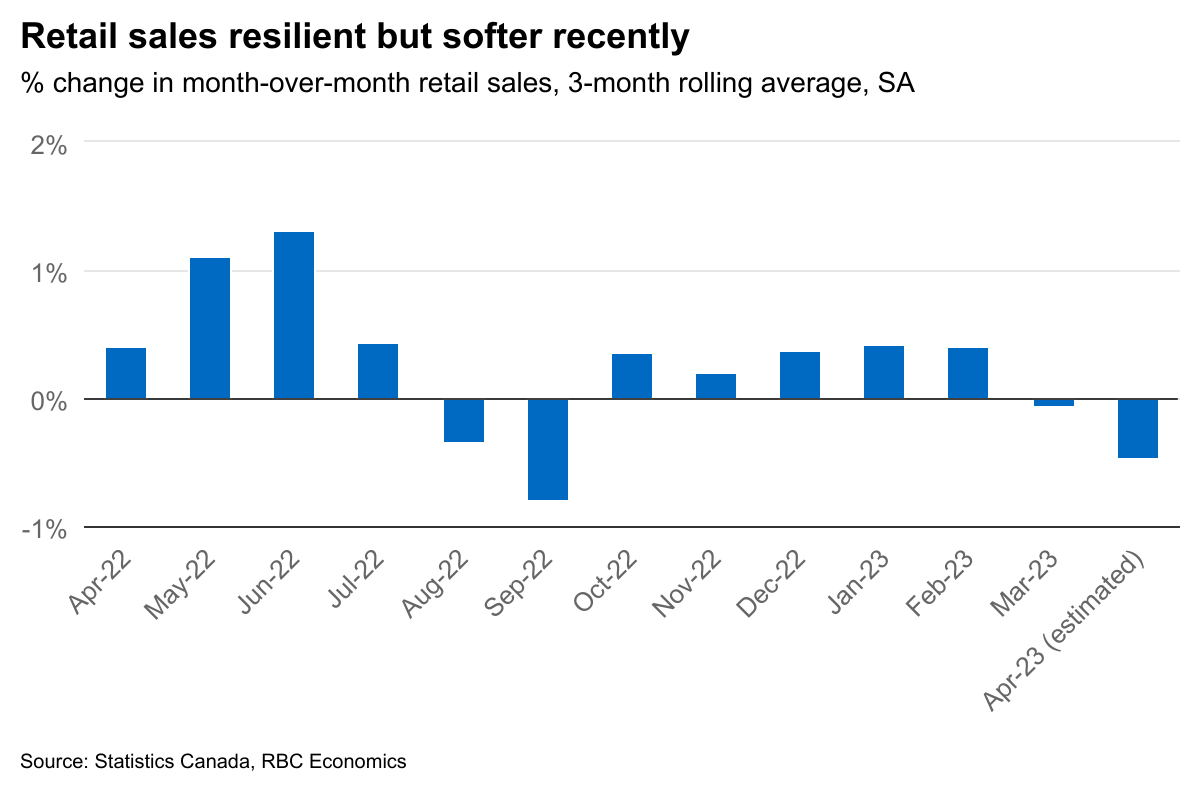

- Retail sales data for May came in stronger than expected, underscoring a still resilient consumer. Inflation data came in on expectations, with the headline and core measure up 4.0% and 5.3%, respectively.

Canadian Highlights

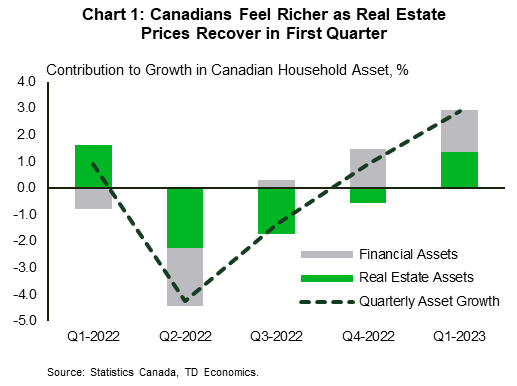

- Canadian households gained $520 billion as wealth growth accelerated in the first quarter of 2023.

- Wealth growth was supported by a rebound in real estate values as average home prices rose on the back of strong home sales and weak listings.

- Meanwhile, higher interest rates lifted the debt service ratio back to its pre-pandemic level. In response, Canadians extended the overall duration of their liabilities.

U.S. – Keepin’ At It… For Now

There were few surprises on the economic front this week. As widely expected, the Federal Reserve held the policy rate steady, after 10 consecutive increases over the past 15 months. Little changed in the statement, though the revised Summary of Economic Projections (SEP) underscored a more hawkish trajectory for the fed funds rate. And rightfully so. Retail sales and inflation data out this week continued to reflect a degree of inertia still present in the U.S. economy, which will likely necessitate a bit more ‘work’ from the FOMC through the remainder of this year.

Focusing on the major changes in the SEP, the FOMC revised its economic outlook higher for 2023. Real GDP growth is now expected to be 1.0% by year-end (previously 0.4%), and the unemployment rate was lowered to 4.1% (previously 4.5%). The inflation outlook was also revised higher, with the median forecast on core PCE now at 3.9% (previously 3.6%). With a stronger economic outlook and higher expected inflation, the median projection on the future path of the policy rate was raised by 50-bps to 5.6% – suggesting a terminal policy rate of 5.75%.

At the subsequent press conference, Fed Chair Powell was pressed on the timing of the potential future rate hikes. While remaining non-committal, Powell emphasized that the July meeting remained ‘live’, and the decision would ultimately be determined by the ‘totality’ of the data flow. From that perspective, a July hike seems more likely than not.

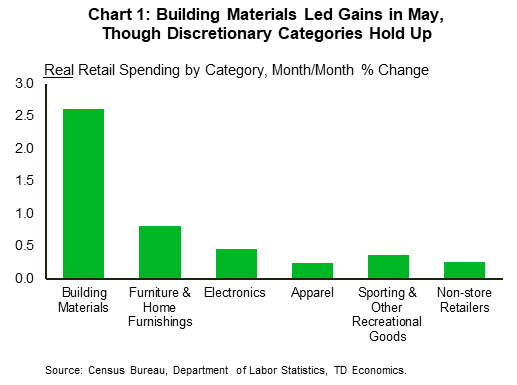

Data out this week on retail sales showed that consumer spending is still humming at a decent clip. Total retail sales rose 0.3% m/m in May, well ahead of the consensus forecast calling for a pullback of 0.2%. After stripping out food and gasoline, sales were even stronger – rising 0.4% m/m. While gains were led by building materials – an inherently volatile category – there was enough breadth across other discretionary categories to suggest that the ‘resilient’ narrative remains intact (Chart 1). Our current tracking for Q2 spending sits between 1.5%-2%. While this represents a deceleration from Q1’s 3.8%, spending is still running far too hot to meaningfully cool inflation. This was evident in the May inflation data.

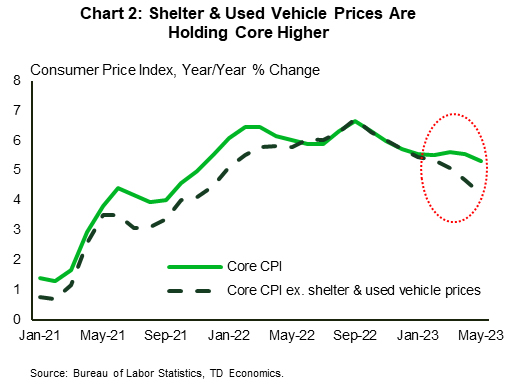

CPI rose by just 0.1% m/m, though the more subdued headline reading was the result of falling energy prices and slower food inflation. Core inflation (excludes food & energy), rose by a more notable 0.4% m/m with the 12-month change ticking down just 0.2%-pts to 5.3%. Sizeable contributions from both used vehicle prices and shelter were responsible for much of last month’s core gains. Excluding these two items shows a more subdued pace of price growth, with prices up just 0.1% m/m or 4.2% y/y (Chart 2). While stripping out individual categories is sometimes a dangerous game to play, there’s good reason to believe that both have downside over the coming months. This reinforces the notion that getting inflation down from today’s +5% reading to 3% over the next year is very feasible. It’s the last leg lower (from 3% to 2%) that will be the biggest challenge for the Fed, hence the need for policymakers to ‘keep at it’ for the time being.

Canada – Balancing Assets, Liabilities, and the Future

Canada – Balancing Assets, Liabilities, and the Future

Central banks' actions continued to underpin market sentiment this week with the Bank of Canada's surprise rate hike giving way to the Fed's hawkish tone as it kept rates unchanged. The news helped lift the Canadian dollar as the interest rate differential between the two countries tilted in loonie's favour. Meanwhile, S&P/TSX Composite index moved almost 1% higher (at the time of writing), with gains extending for the second consecutive week.

Monetary authorities prefer to remain hawkish as evidence of strong labour markets, sticky inflation, and a recovery in asset valuations continues to amass. This week's release of national balance sheet and financial flow accounts showed that national net worth (the sum of national wealth and Canada's net foreign asset position) rose 1.7% from the fourth quarter of 2022 to $17.1 trillion at the end of the first quarter of 2023. Canadian household net worth grew by $520 billion as wealth growth accelerated by 3.4% in Q1 from 0.9% in Q4 2022. These gains were preceded by two consecutive quarters of contraction, triggered by one of the most aggressive tightening cycles in the history of the Bank of Canada.

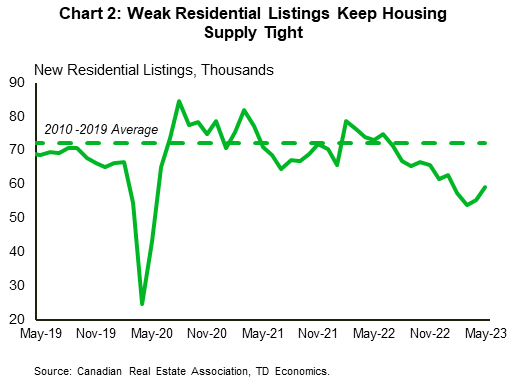

On the asset side of households' balance sheet, growth was supported by both a rebound in real estate and higher financial assets valuations. Indeed, average home prices turned the corner in February stepping on an upward trend, gaining 2.7% in the month of May and 14% since the beginning of the year. Home price gains have been driven by exceptionally tight supply dynamics, where home sales recovered more than 20% since the beginning of the year while listings remained weak at 16% below their post-Global Financial Crisis average (Chart 2). Despite these visible signs of a housing market resurrection, past declines in home sales continue to feed into falling construction, pushing housing starts lower in May. This is likely to reverse in the coming months, as more recent gains in sales reboot residential investment activity, supporting the overall economy.

As Canadians started buying homes again, the pace of accumulation in bank deposits slowed significantly in the first quarter of 2023, with the smallest gain since the third quarter of 2021. The pace of debt accumulation was also slower, with both mortgage and non-mortgage debt growth decelerating. This reflects the slow-moving nature of tighter monetary policy that also helped lift the debt service ratio (total debt payments as a share of personal disposable income) back to its pre-pandemic level. In response, Canadians lowered their debt principal repayments by 4% quarter-on-quarter, extending the overall duration of their liabilities.

This can have several implications for the Bank of Canada's future policy decisions. As a larger portion of individuals' income goes towards debt repayment, their disposable income for consumption and investment decreases. This should help slow demand, and in turn cool inflation. On the flip side, slower debt repayment leaves households more leveraged which weighs on consumption over the longer term.

Canadian Retail Sales Slowing, But Services Spending Remains Strong

We expect next week’s retail sales data to show further softening in consumer spending for April. The advance estimate for the month’s sales was for a slight 0.2% increase that likely reflected higher prices for gasoline rather than an increase in the quantity of purchases. Consumer spending was surprisingly resilient early in 2023, with a 5.7% annualized increase in the first quarter. But most of that boost came from strong spending in January. Recent monthly readings have been softer with declines in retail sales volumes (excluding price impacts) in both February and March.

Our own tracking of spending is pointing to a stronger increase May, and spending on services (not counted in the retail sales data) has remained firm. That resilience was cited by the Bank of Canada in its decision to hike interest rates in June for the first time since January. Still, the lagged impact of higher rates continues to feed through to household borrowing costs with a lag. Canada’s debt service ratio rose to 14.9% in Q1 , just one tenth of a percent shy of the pre-pandemic record high. Higher prices and debt payments already soaked up all of the increase in Canadian household after-tax income last year, and delinquency rates on credit cards and auto loans have ticked back above pre-pandemic levels. Meantime, signs of cracks have continued to surface in labour markets. We continue to expect spending to flag over the second half of this year, even with surprising resilience year-to-date.

Week ahead data watch

Next Tuesday, StatCan will release the 2023 CPI basket weights update, which reflects the consumer expenditures in 2022. The new weights will account for changes in consumer spending patterns by looking at expenditure data from Household Final Consumption Expenditures, Survey of Household Spending, and alternative data sources.

Gold Trapped in a Narrow Range, What’s Next?

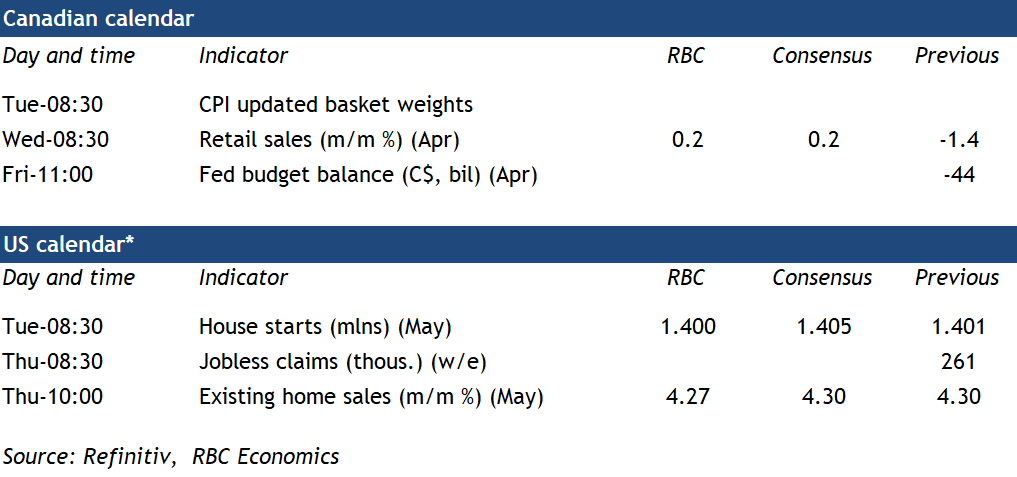

After almost touching a record high last month, gold prices have corrected lower, trampled under the weight of rising yields and a resurgent US dollar as markets priced in a higher-for-longer scenario for Fed rates. These forces could keep bullion under pressure for now, although in the bigger picture, the trend of sovereign buying by central banks and nerves around a recession might be enough to propel gold to new heights.

Behind the rally

Gold prices have staged a stunning recovery after bottoming out last year, rising more than 21% since November. Several elements fueled this powerful rally, including safe-haven demand after the collapse of several US regional banks, direct gold purchases by central banks, and hopes that the Fed’s tightening cycle is approaching its conclusion.

But the rally lost some steam lately. After getting rejected for a third time from the record high of $2,072, gold prices have declined by around 6% to settle in a narrow sideways range. The market has been trapped between $1,935 and $1,975 over the last month, waiting for a catalyst to break out.

This retreat and the ensuing consolidation phase reflect the latest developments in global markets. With fears about an imminent recession fading away, investors have recalibrated the Fed’s interest rate trajectory, pricing in higher rates for a longer period of time. This reassessment also helped to breathe some life back into the US dollar.

Interest rate expectations and movements in the dollar are critical for gold. The precious metal does not pay any interest to hold, so it becomes less attractive as yields rise and investors can earn higher returns in bonds.

Similarly, since gold is generally priced in US dollars, a stronger greenback makes it more expensive for foreign investors to buy the metal. The opposite effects are also true - gold becomes more attractive as yields fall and the dollar depreciates.

Geopolitics and central banks

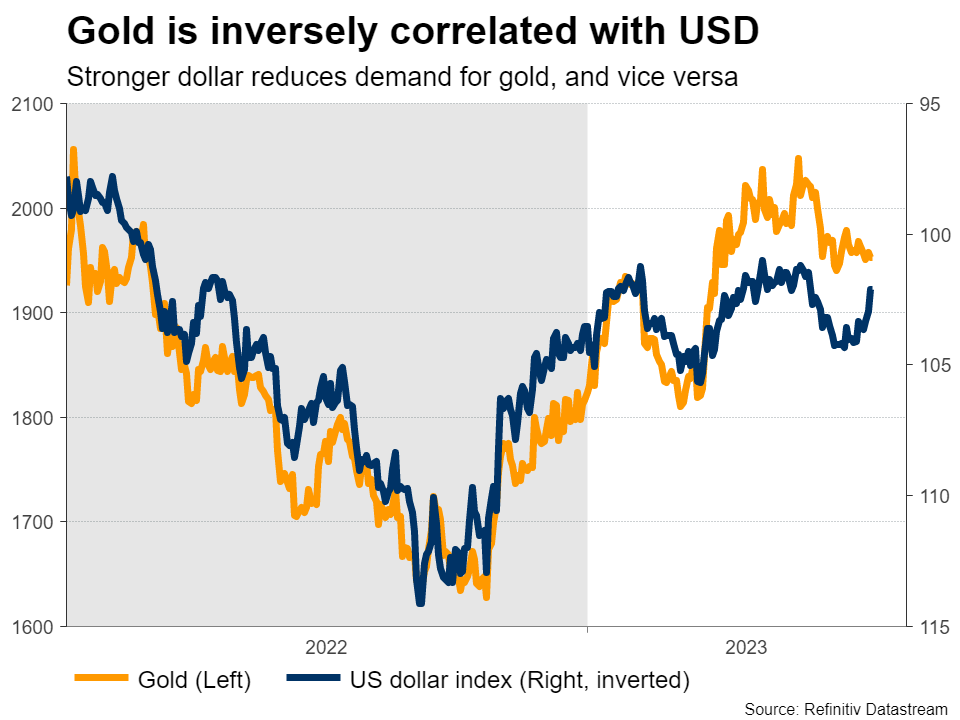

Beyond interest rates, the dollar, and safe-haven demand, the fourth variable that has emerged as a major driver of gold lately is the purchase of bullion by central banks to raise their reserves.

Geopolitics are behind this phenomenon. In the aftermath of the Ukraine invasion, the United States and Europe deployed crippling sanctions against Russia, which included the freezing of the FX reserves it held in dollars and euros. But its gold reserves that were held in Russia could not be frozen.

This helps to explain why China has been buying gold relentlessly over the past year. Beijing is trying to diversify its reserves, so it has been loading up on gold, which cannot be frozen if the geopolitical atmosphere turns colder. Other major sovereign buyers over the past year include Turkey and India.

Sovereign purchases are likely a game-changer for trading dynamics in gold. When there are such massive buyer whales lurking in the market, which are less sensitive to prices than other players because they also have political motives in mind, it almost establishes a soft floor under gold prices, preventing any massive selloffs.

New record highs? Maybe later on

Looking ahead, the central question for gold prices is whether a recession has been averted, or simply delayed. For now, the US economy remains fairly resilient. Economic growth is still solid and the labor market is in good shape, which suggests interest rates are likely to remain elevated for a longer period of time.

That’s a difficult environment for bullion, as it implies higher bond yields and a relatively strong US dollar. Hence, there is a clear risk that the recent consolidation phase in gold concludes with a break lower, in which case the focus would turn towards the $1,855 region that also encompasses the 200-day moving average.

For gold to resume its journey towards new record highs, it would likely require recession concerns to resurface. A weaker economic data pulse could see investors flirting with the idea of Fed rate cuts, pushing yields and the dollar lower.

With defensive demand also on the rise, such a scenario has the capacity to propel gold back towards the record high of $2,072 for a fourth time. That said, this is probably a longer-term story, perhaps around the end of this year or even beyond.

In other words, there isn’t much on the immediate horizon that can fuel upside in gold, as long as the Fed is keeping rates high and the economy is holding strong. This points to a sideways market over the next few months, with risks tilted to the downside.

Ultimately though, it is almost inevitable the economy will feel the burn of all the rapid-fire rate increases that have been rolled out over the past year. At that point, gold will most likely begin to shine once again.

Week Ahead – Can the BoE and SNB Hike by 50bps? Flash PMIs Incoming

The central bank theme will continue in the coming week with the Bank of England and Swiss National Bank next to announce their interest rate decisions. Both are expected to raise their policy rates but is there room for hawkish surprises? The flash PMIs for June will also be on investors’ radar as some regions such as the Eurozone grapple with a recession. Inflation data will be the highlight in Japan but it’s looking like a quieter period in the United States, allowing the US dollar to take a backseat after the Fed’s decision to pause.

BoE to likely play it safe despite inflation risks

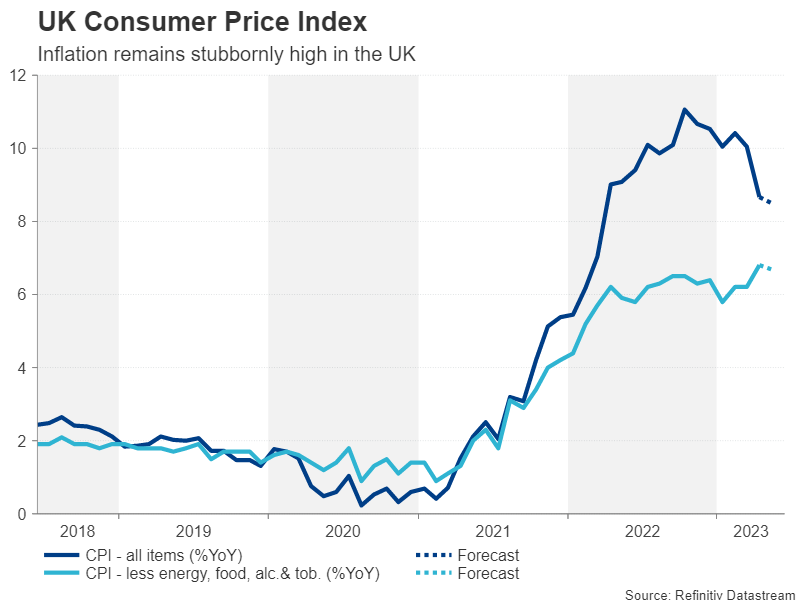

It is no secret that Britain has one of the highest inflation rates in the Western world, thanks to Brexit, high fuel prices and a tight labour market. The Bank of England has been trying to tame inflation for the past 18 months, but it has yet to cool off substantially.

Pressure is building on policymakers to get a grip on inflation fast after both wage growth and underlying prices pressures started to heat up again recently, dashing hopes for a pause. Fortunately for the Monetary Policy Committee (MPC), they will have some help on Wednesday before they vote when they get their hands on the latest CPI report.

Headline inflation is anticipated to have moderated further in May, declining to 8.5% y/y. However, even if there is another sizeable drop in headline CPI, policymakers will likely be more concerned about the core measure. After shooting up to 6.8% in April, core CPI is expected to have inched marginally lower to 6.7% in May, suggesting there is another wave of second-round effects underway.

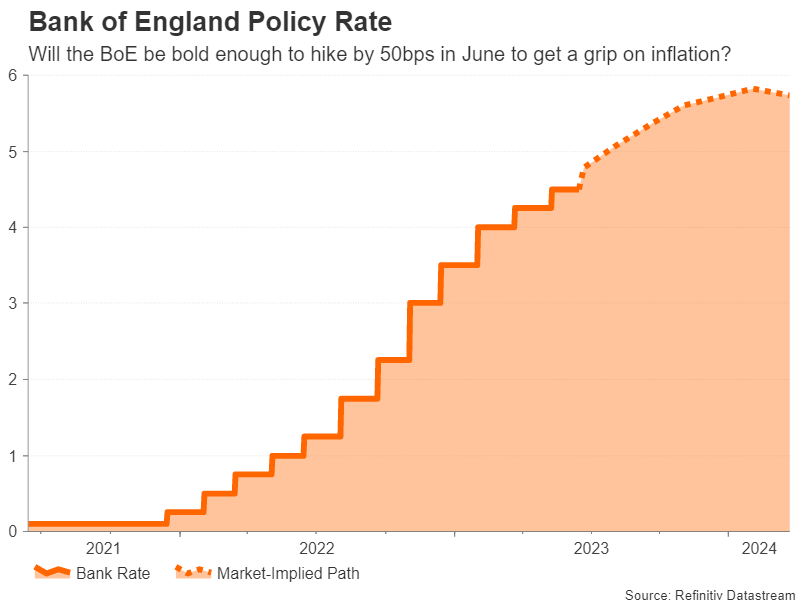

If the CPI figures are hotter-than-expected, which would come on the back of a strong employment report, the Bank of England might well decide to raise interest rates by a larger 50-basis-point increment. However, the chances of that are quite low. Investors have assigned just a 12% probability of a 50-bps hike and the BoE has not gone against the markets during the course of this tightening cycle except when it surprised at liftoff.

The MPC will probably point to the lag effect of its existing policy tightening as well as the risks to the housing market if it raises the Bank rate by only 25 bps as expected on Thursday. There is no press conference or updated forecasts at the June meeting but any changes to the language in the statement that flags additional rate increases would be positive for the pound.

Even if the BoE gives little away about its intentions at future meetings, sterling could benefit from a broadly positive set of data, as retail sales numbers for May are also due on Friday, along with the flash PMIs for June.

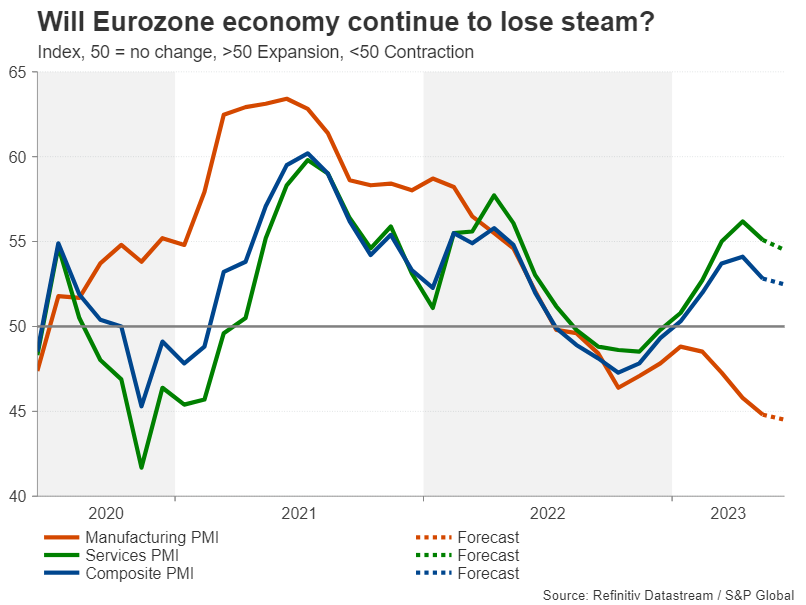

Will Eurozone PMIs soothe recession woes?

Across the channel, the flash PMIs will take centre stage in the euro area as doubts grow about the resilience of the bloc’s economy after revised GDP estimates put the Eurozone in a technical recession. So far, the recession tag hasn’t led to a significant shift in market expectations about further tightening from the European Central Bank as growth in Q1 was dragged lower by poor performance in a small number of countries, including Germany, but other economies continued to expand.

The preliminary PMI readings for June should give some idea as to whether this mild downturn is turning into something deeper or if economic activity in places like Germany is starting to rebound.

The euro could appreciate against the US dollar from any upside surprises in the manufacturing and services PMIs, especially after the ECB hiked rates this week and signalled they will have to go even higher, while the Fed kept its policy settings unchanged.

But against the Swiss franc, the single currency might struggle should the Swiss National Bank follow suit and lift rates next week.

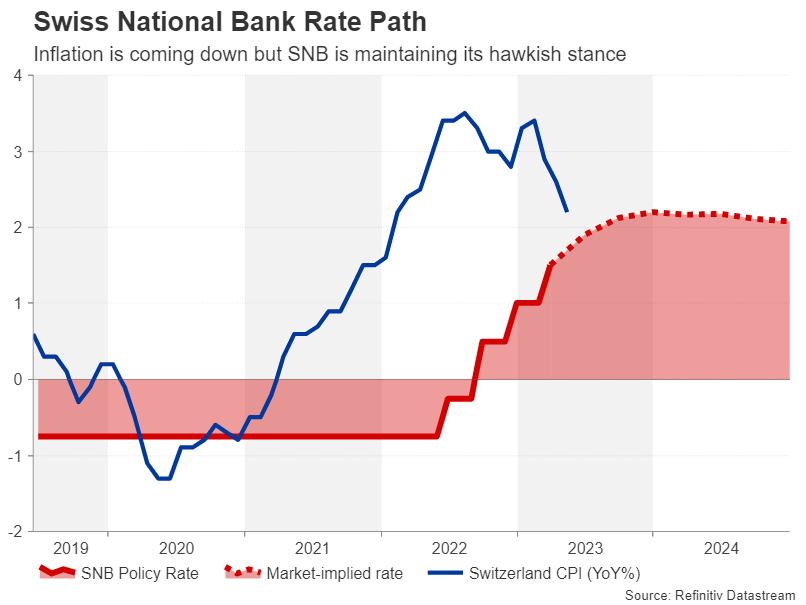

SNB not done raising rates

The odds of a 50-bps hike by the SNB on Thursday went up after unusually hawkish language from Chairman Thomas Jordan recently. The hawkish rhetoric comes despite the fact that inflation in Switzerland fell to 2.2% in May, much to the envy of other nations.

Nevertheless, the SNB doesn’t seem to think that policy is restrictive enough as it wants to see inflation fall below 2%. Policymakers might also be worried about the fall in CPI being temporary and considering that the SNB meets only four times a year, a 50-bps hike seems more likely.

If that turns out to be the case, the franc could enjoy strong gains as a 50-bps move is only about 60% priced in at the moment. Though the scale of the boost would depend on whether or not the SNB signals further tightening in the second half of the year.

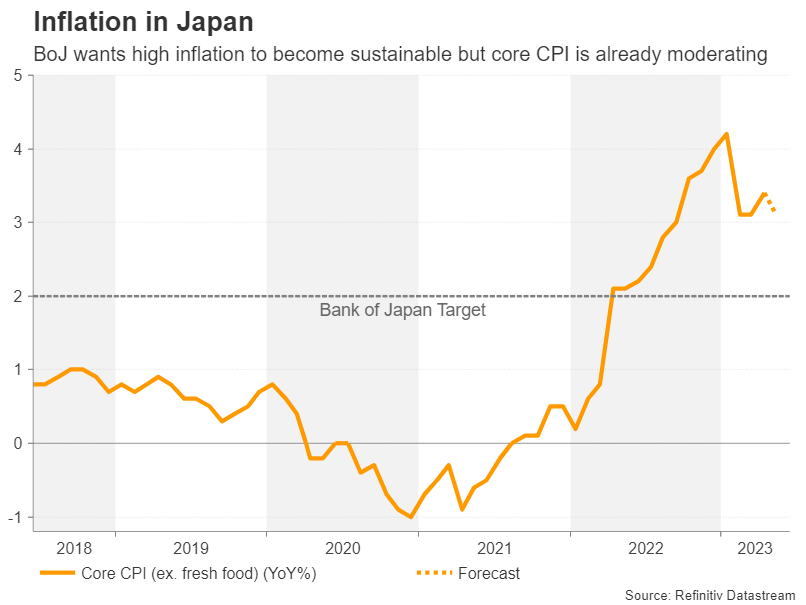

Japan’s reflation still has some way to go

Another country where the inflation problem has been more manageable is Japan. After peaking at 4.2% in January, core CPI has eased somewhat, although it did edge up to 3.4% in April. It is forecast to have eased to 3.1% y/y in May when the data is released on Friday. From a policy perspective, inflation does not necessarily have to climb to new peaks for the Bank of Japan to think about changing course and it only needs to stay above 2% for an extended period of time.

For the time being, however, the Bank of Japan is maintaining its easing stance as it wants to be certain that the pickup in prices and wages is sustainable. This is reflected in the Japanese yen, which has tumbled sharply against major currencies this month.

Yet, with many traders thinking that it’s only a matter of time before the BoJ starts unwinding its massive stimulus, the yen could begin to show signs of life should a clearer pattern of persistent inflation begin to form. Also to watch out of Japan next week are Friday’s flash PMIs amid an upturn in economic growth lately.

Minor risks for the aussie and greenback

Staying in the region, the Australian dollar will be keeping an eye on monetary policy in both China and Australia. The People’s Bank of China will decide on Tuesday whether to cut its loan prime rates, following the recent 10-bps cuts to its medium-term lending facility and seven-day reverse repo rate. The Reserve Bank of Australia, meanwhile, will publish the minutes of its June policy meeting the same day.

The aussie has been on a roll lately, as the RBA pivots further to the hawkish side and Beijing steps up its efforts to stimulate the Chinese economy, which is the biggest market for Australian exporters. Further gains could be in store for the currency if the minutes reinforce bets for further rate hikes by the RBA and China sticks to its pledge to boost growth.

Finally, over in the US, it’s going to be a relatively quieter week, allowing traders some time to process the Fed’s decision to temporarily pause but pencil in two additional rate increases before the year end. Markets are not convinced the Fed will be able to deliver on this but Fed Chair Jerome Powell will get another chance to get his message across to investors when he addresses lawmakers for his semi-annual testimonies on Wednesday and Thursday. In data, housing figures due on Tuesday and Thursday, as well as S&P Global’s manufacturing and services PMI prints on Friday might shed some useful light on these key sectors of the US economy.

Bank of England Preview – Look to Sell GBP on Aggressive BoE Pricing

- We expect the Bank of England (BoE) to hike the Bank Rate by 25bp on 22 June.

- While we now expect a peak in the Bank Rate of 5.00%, we see current market pricing of a peak in policy rates of 5.75% as too aggressive.

- EUR/GBP is set to move higher on the statement as we expect the BoE communication to fail to live up to market expectations.

BoE call. We expect the Bank of England (BoE) to hike the Bank Rate (key policy rate) by 25bp on 22 June, bringing it to 4.75%. This is in line with markets expectations. We expect a slight hawkish shift in communication given the latest releases showing increased persistence in inflation and a tight labour market. However, we do not expect it to live up to market expectations.

Since the last monetary policy decision in May, both wage growth and inflation releases have surprised to the upside. Likewise, other central banks, namely the Reserve Bank of Australia (RBA) and Bank of Canada (BoC) have gone against market expectation and further increased policy rates. Combined with the UK economy holding up much better than expected, this has increased the pressure on the BoE. As 25bp looks like a done deal for this meeting, focus will primarily turn to communication with respect to the future course of monetary policy action and language regarding the renewed surge in the persistence of inflation.

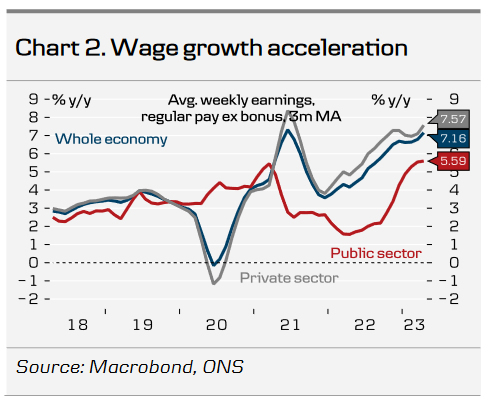

The latest labour market report was broadly stronger than expected and highlights that the UK labour market remains under immense pressure. Wage growth excluding bonuses increased to 7.2% (up from 6.7%) with wage growth accelerating in the private sector. Likewise, unemployment ticked lower to 3.8% following increases the past months.

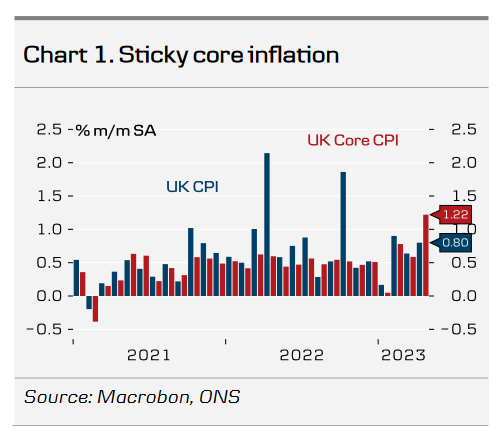

Although inflation figures for May will not be published until the day before the rate announcement, the April figures exceeded the consensus expectation for both headline and core inflation. The core inflation recorded a significant month-on-month growth of 1.22%, marking the highest increase in decades. While the headline inflation fell 0.2 percentage points below the BoE's forecast, we anticipate that BoE will place greater emphasis on wage growth and persistent core inflation. This is particularly noteworthy as the contribution from services rose to 3.2% from a previous 3.1%. Likewise, the latest BoE's monthly Decision Maker Panel survey showed that inflation expectations ticked higher in May, with both 1Y- and 3Y ahead CPI inflation expectations increasing.

On the back of recent events we add an additional 25bp hike in August to our forecast profile and thus see the Bank Rate peaking at 5.00%. This is significantly less than market pricing, which has increased the previous months to a peak rate of 5.75%, up from 4.80% in May. We expect no rate cuts until 2024.

FX. In our base case of a 25bp hike, we expect EUR/GBP to move higher. While we expect the BoE to highlight that inflation has proven more persistent than previously expected, we believe that they will fail to live up to market expectation of a hawkish pivot. On balance, we increasingly see relative rates as a positive for EUR/GBP from here, which is one of several reasons behind our fundamental predisposition of buying EUR/GBP dips.

Weekly Focus – Hawkish Messages from the Fed and ECB

In a big central bank week, the ECB delivered a 25bp hike, which was no surprise, but an upward revision to the 2025 inflation forecast to 2.2% from 2.1% clearly indicated that the ECB has more work to do. ECB President Lagarde confirmed that the hiking journey is not over yet and that a rate increase in July was "very likely". As expected she left little guidance beyond July as uncertainty is high and they take a meeting-by-meeting approach. However, we continue to expect the ECB to reach the rate peak in September at 4.0% as there are no signs that the super tight labour market is easing in the coming months, see ECB Review - 'Very likely to hike again in July', 15 June.

The Fed on the other hand paused its rate hiking cycle on Wednesday as widely anticipated, but they delivered a hawkish message as the updated median rate projection signalled two more 25bp rate hikes by the end of 2023. The 2023 GDP forecast was lifted to 1.1% (from 0.4%), suggesting that the outlook for more rate hikes relies on a fairly optimistic growth assumption. As we remain more pessimistic on the macro outlook for H2, we also think that the projected rate hikes will not end up materializing, and stick to our previous forecast of no rate changes by the Fed for the remainder of the year, read more from our Fed review: Powell's hawkish bluff, 14 June, and see also our thoughts on the latest inflation data and outlook from Global Inflation Watch - Euro area inflation pressures remain sticky, 14 June.

The Chinese central bank is going against the global trend and cut the policy rate by 10bp this week. It follows signs of a sputtering recovery and data on Thursday confirmed weakness in housing and manufacturing in May, while the service sector is holding up still. We expect to see a broader stimulus package soon aimed at providing more support to housing and sustaining demand from consumers. Bank of Japan did not make any changes on Friday but we expect to see a moderate tightening in July or September.

Bond yields trended higher this week on the back of the hawkish signals from the Fed and ECB with especially short end yields rising. The central banks didn't scare stock markets, though, which saw further upside taking S&P500 to the highest level in more than a year, not least driven by a strong rally in tech stocks. EUR/USD also rebounded again lifted by a stronger rise in euro short end rates relative to the US.

Next week the key focus will be Flash PMI's for May in US and the Euro zone. Manufacturing has been weak lately while service has been strong. Will we see some convergence this month? We also have a range of Fed speakers that may cast more light over Fed's view on future tightening. Inflation data in Japan will be key to gauge the outlook for a possible tightening of monetary policy. In Emerging markets, the central bank meeting in Turkey on Thursday will be interesting following new appointments of Simsek as finance minister and Erkan as central bank governor. Also look out for possible stimulus announcements in China. On Tuesday we will publish Nordic Outlook with updated macro forecasts for the Nordics as well as the global economy.

China’s Sluggish—Short & Long-Term—Growth Outlook

Summary

China's post-COVID rebound has now fully matured as the latest batch of activity data reinforced a slowdown is under way across the Chinese economy. As a result, we have revised our 2023 GDP forecast lower, and now believe China's economy will grow 5.7% this year. Waning economic momentum has prompted easier monetary policy from the People's Bank of China (PBoC), and we believe further easing is imminent as authorities are likely to lower bank Reserve Requirement Ratios in Q3-2023. Diverging paths for monetary policy between the Fed and PBoC have weighed on the renminbi, and while we are not adjusting our renminbi forecasts, we believe tactical opportunities exist to take advantage of potential renminbi underperformance.

Short-term growth prospects are now under pressure; however, China's longer-term growth potential also faces robust challenges as structural issues persist and have arguably worsened. These structural hurdles stem from worsening demographic trends, an over-leveraged non-financial sector, and geopolitical developments that are more likely to suppress than enhance future economic growth prospects.

The Post-COVID Rebound In China Is Over

“Zero-COVID” protocols weighed on China's economy for a good part of the past three years. COVID mutations and rising case burdens were met with harsh mobility restrictions that upended China's economy, disruptions that trickled across Asia and other parts of the world. Eventually lifting COVID containment measures brought about an optimism that China's economy would flourish. In fairness, the Chinese economy did outperform in Q1. China's economy grew 2.2% quarter-over-quarter, a more robust pace of growth than we along with consensus forecast expected. However, the momentum from the first quarter has not been able to sustain itself and growth prospects for China's economy are fading quickly. Currently, the May non-manufacturing PMI sits at 54.5, down from 58.2 in March, while the manufacturing PMI slipped deeper into contraction territory in May. Perhaps most concerning is that the April and May manufacturing and services PMIs fell more than consensus expected. In fact, underperforming sentiment as well as activity data have been a theme in China over the past few months. To that point, the economic surprise index—designed to measure whether data are outperforming or underperforming relative to expectations as well as the magnitude of performance—has declined rapidly since the end of March (Figure 1). Meaning, not only are data out of China suggesting the economy is slowing, but the deceleration is occurring at a quicker pace than initially expected. The latest batch of activity data for May, particularly retail sales, confirms China's post-COVID economic rebound has fully matured. As a result, we are revising our GDP forecast lower, and now forecast China's economy to grow 5.7% this year, down from 6% previously. Following this downward revision, risks around our forecast are now balanced.

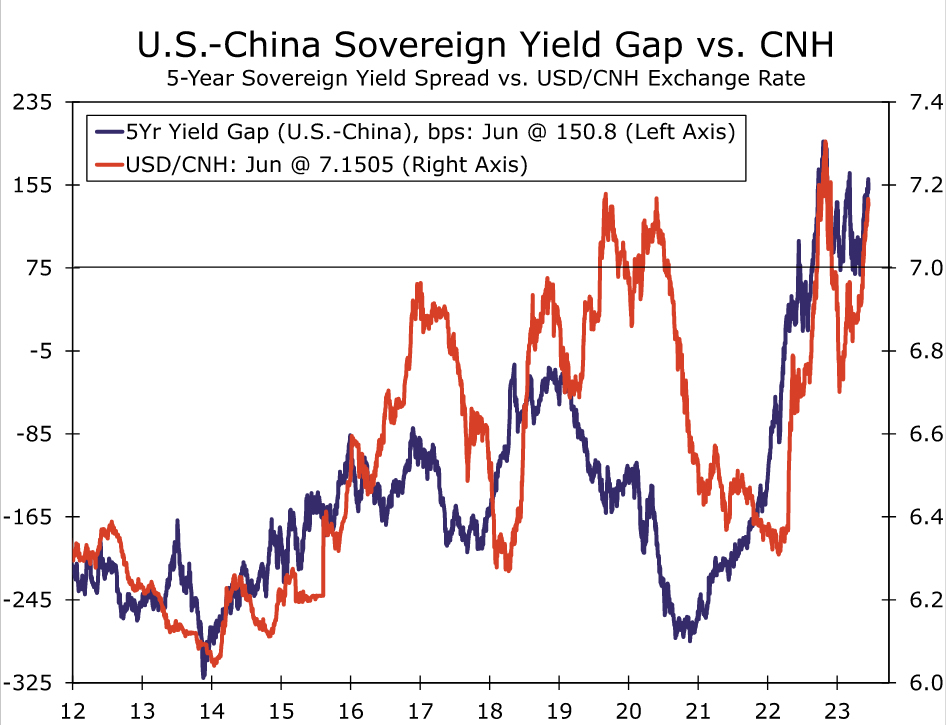

Recent actions and communications from Chinese authorities also suggest they are concerned with the overall health of the economy. Just recently, the People's Bank of China (PBoC) lowered short- and medium-term lending rates to encourage borrowing and support broader economic activity. Media reports also suggest authorities are considering deploying new fiscal stimulus, likely targeted at propping up the real estate sector, but also to possibly spark domestic consumption. While deploying fiscal stimulus is a possibility, we can say more confidently that we believe additional PBoC monetary easing will be the primary policy lever authorities use to support the economy and that further easing is likely forthcoming. In that sense, we believe PBoC policymakers will follow up their decision to cut lending rates with a decision to lower the Reserve Requirement Ratio (RRR) for local banks, and we reiterate our view that the major bank RRR will be lowered 25 bps to 10.50% in Q3-2023. Further easing will keep the PBoC and Federal Reserve on diverging paths for monetary policy, a dynamic that has historically applied depreciation pressure on the renminbi, and has resulted in a weaker Chinese currency more recently. While we baked widening interest rate differentials into our renminbi forecasts and forecast a weaker currency through Q2-2023, renminbi depreciation has been more pronounced than we expected to this point. However, the current sovereign yield spread between similar tenor Chinese government bonds and U.S. Treasuries suggests renminbi depreciation against the dollar may be topping out (Figure 2). While our forecast is for the renminbi to end Q2-2023 at 7.10, we opt to exercise caution and believe a renminbi recovery against the greenback is more likely to materialize than further depreciation based on medium-term yield differentials.

With that said, there are still tactical opportunities to position for renminbi underperformance. The RMB’s recent underperformance suggests a weakening linkage with the U.S. dollar and tighter linkage to the trade-weighted basket. With additional policy easing in China tilted toward monetary channels, we remain of the view that these are more likely to fuel outflows than change the broader narrative on economic growth. Real rates in China (1y FX forward implied rates less consensus inflation expectations) have continued to head lower against both developed and emerging market countries. Furthermore, we note that Chinese policymakers have not stepped in to stem FX weakness, suggesting a revealed preference for a weaker FX. In that sense, we like being short the CNH against currencies that are highly sensitive to a weakening trend in the RMB trade-weighted exchange rate (CFETS basket). The Wells Fargo Macro Strategy team recently recommended extending targets on long SGDCNH spot. Macro strategists will keep a close eye on the CNY’s fixing behavior, FX intervention activity and prospects for fiscal stimulus and/or broader credit easing for signs of a change in the currency’s weakening trend.

Future Growth Rates Are Not Promising Either

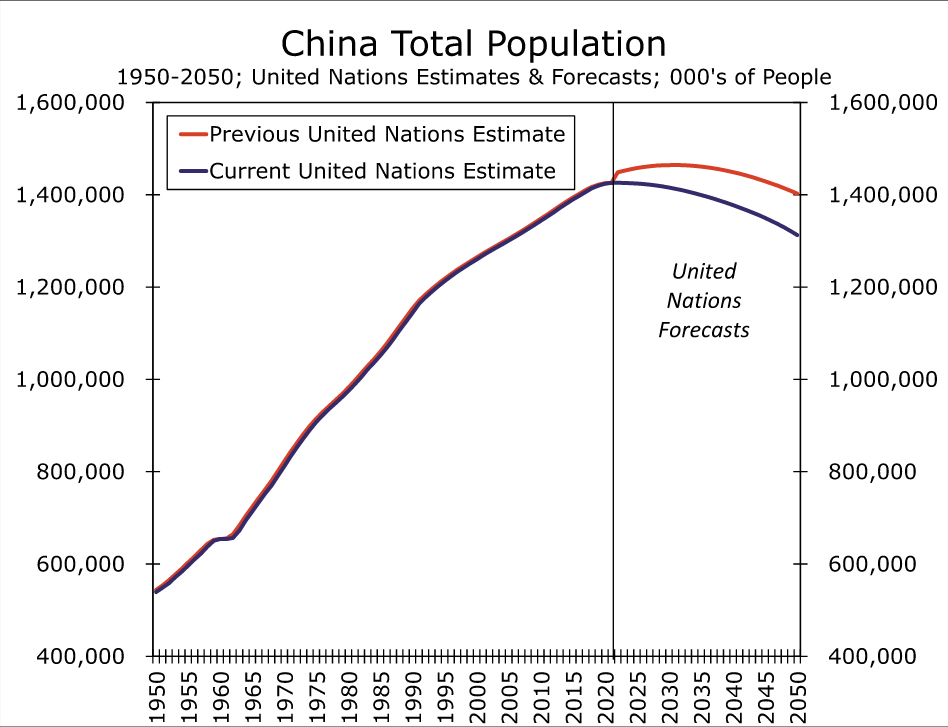

China's economic slowdown is not just a short-term phenomenon, but a theme that should also play out over the longer term. We have commented on China's structural challenges in the past and how these hurdles will place downward pressure on the Chinese economy's long-term growth potential. Not only are these issues still present, but China's structural challenges have worsened. To that point, China's demographic profile has deteriorated in the past year. Slowing population growth has been a hurdle for some time; however, China's population declined for the first time in decades at the end of last year. The outright population decline came 10 years earlier than the United Nations initially forecast (Figure 3), and with China's working age population already shrinking, China's potential growth is on a rapidly downward trajectory purely from a demographics perspective.

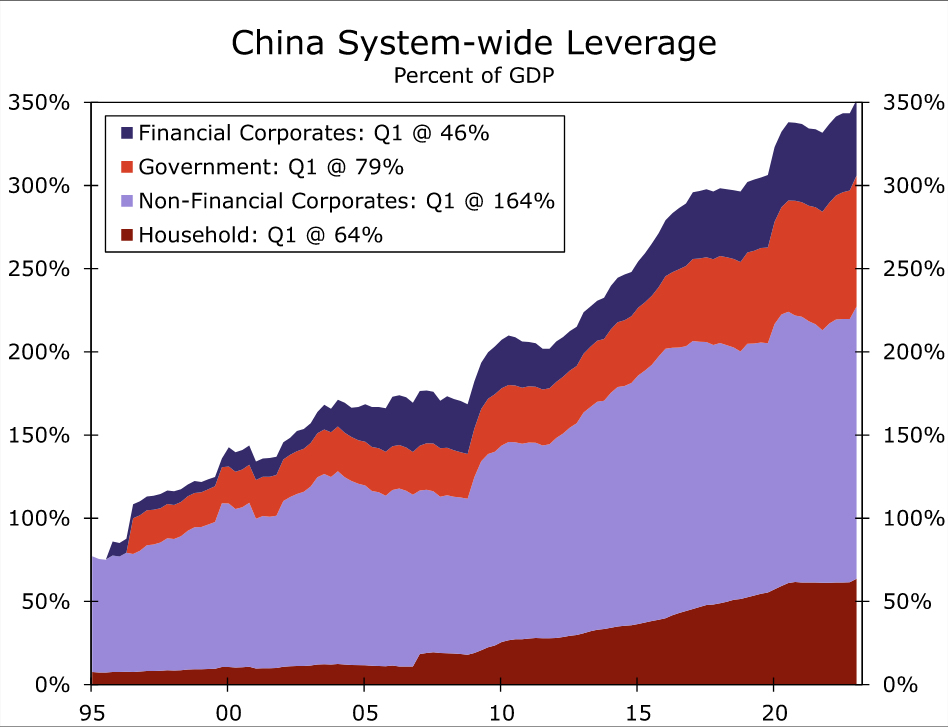

Compounding poor demographics is China's debt problem, particularly leverage within the non-financial corporate sector. Since the 2008-2009 Global Financial Crisis, most of China's growth has been driven by credit expansion. This credit growth has been directed toward the real estate industry and infrastructure spending has been critical to China's growth story for the past 15 years. As a result, China's non-financial corporate sector, mostly real estate firms, has amassed a debt burden worth 164% of GDP (Figure 4). This debt burden is more of a vulnerability; however, cracks in the real estate sector have formed over the past few years, most notably with the collapse of Evergrande and other large local property developers. State support has also been limited recently and “bail out's” for over-leveraged firms have been rebuffed by Chinese authorities, leading to the possibility of a financial crisis unfolding in China. Two scenarios exist for China's debt burden going forward, both of which are likely to result in suppressed potential growth rates. In the first scenario, the sovereign allows property developer defaults and bankruptcies, which can spill over to China's banking sector and reduce confidence in the country's financial system. Or, China actively tries to deleverage the economy, similar to efforts in 2015-2016. As mentioned, credit expansion has been key to China's growth, should borrowing slow and leverage stabilize, future growth rates will be negatively affected.

And finally, geopolitical developments represent a structural issue that could weigh on China's future growth rates over the long term. Supply chain diversification, tariffs, export restrictions, sanctions risk, and a somewhat elevated possibility of military conflict—intentional or accidental—in the Taiwan Strait could all individually and collectively have negative implications for China's economy. As far as tariffs, Trump administration tariffs remain in place and are likely to remain in place going forward. Western allies have also imposed restrictions on intellectual property that can be exported to China, most notably microchips, in an effort to limit the nation's technological advancements and steps toward a more digital economy. China's coziness with Russia also keeps the risk of sanctions very much a possibility. And given China's flurry of activity in the Taiwan Strait as well as commentary around reuniting the mainland and Taiwan at the 20th National Party Congress, the probability of military conflict in the South China Sea is higher relative to recent history. While we are not assuming any type of conflict, multiple flashpoints and event risks exist over the next few years that could lead to an escalation in geopolitical tensions between China, the United States and other economic powerhouses around the world. Next year, Taiwan will host presidential elections with pro-democracy and pro-sovereignty candidates seeing a fair amount of momentum early in the election cycle. China may look to disrupt next year's election and could look to become more assertive in interrupting the democratic process in the United States around the time of the U.S. election in 2024. China also has stated its goal for technological independence by 2025—”Made in China 2025”—which could mean turning more aggressive toward Taiwan's semi-conductor and technology capabilities. Also, the 21st National Party Congress will take place in 2027. In our view, one of President Xi's potential motivations could be to cement his legacy within Chinese history. And securing that legacy could, hypothetically, even potentially mean unifying mainland China with Taiwan before the 21st National Party Congress meets in 2027. Point being, geopolitical risks involving China seem more likely to weigh on future growth than enhance growth prospects. While we will refrain from making any assumptions around geopolitical developments at this point, should any of these risks materialize, China's economy would likely be negatively affected and place additional downward pressure on potential growth.

The End of China’s Recovery?

Over the last week, Chinese authorities have taken a series of measures to prop up the economy. That could be seen initially as a good sign for the global economy and commodity prices. But if the economy is doing well, then it typically doesn't need extraordinary measures of support. Which could indicate a more long-term worry, and ultimately hurt commodities as well as their respective currencies.

There were a lot of hopes pinned on China's post-covid recovery. The initial thought was that the draconian measures implemented last year by China to control the spread of the virus had depressed the economy. The first sign of trouble was when Q4 GDP came in not as bad as expected.

The good news is isn't good in the long run

But if the economy hadn't been depressed as much, it means that there was less pent-up demand for a rebound. Q1 saw China's economy returning to growth, but not as much as anticipated. Since then, preliminary measures for Q2 have soured, with PMIs returning contraction. The massive rebound hasn't materialized, and China's domestic economy is once again sputtering.

Some analysts remain optimistic that the rebound might still come, and is being simply delayed by global worries. But that view does not appear to be shared by the PBOC, which recently cut the reserve requirement ratio (RRR) and major lending facility (MLF) in a bid to prop up the economy. This is equivalent in effect to an interest rate cut in other economies, and implies that China's central bank is not the least bit worried about the economy overheating.

Where to from here?

Further signs of the weak domestic situation is that the Chinese government has announced new measures to spur consumer demand. That includes offering incentives to buy cars and household appliances. With the housing market still on shaky footing, Chinese consumers are hesitant to open their pocketbooks. Even if industrial production and exports remain steady and the people still have jobs, the reluctance to spend could keep the economy depressed.

The Chinese government's efforts to boost the domestic economy means that the consumer sector is taking a bigger role in growth. Chinese consumers are notoriously frugal, with China having among the highest personal savings rates in the world. This puts a crimp on expecting outsized growth in the economy based on domestic consumer demand.

The weaker yuan and global growth

The weakness in the Chinese currency might help reactivate the export-driven industrial base, thanks to being more competitive. By extension, it could even help reduce global inflationary pressures, and contribute to less monetary tightening. In the medium term, that might help avoid a deeper recession.

But, for the moment, Chinese firms have less purchasing power on the global scene and could be less willing to pay for commodities. This even includes crude, which could lead to a reversion in the latest CAD strength thanks to the BOC's surprise action. Unless the government's drive to support the domestic economy starts to bear fruits, commodity currencies could be under pressure through the summer.

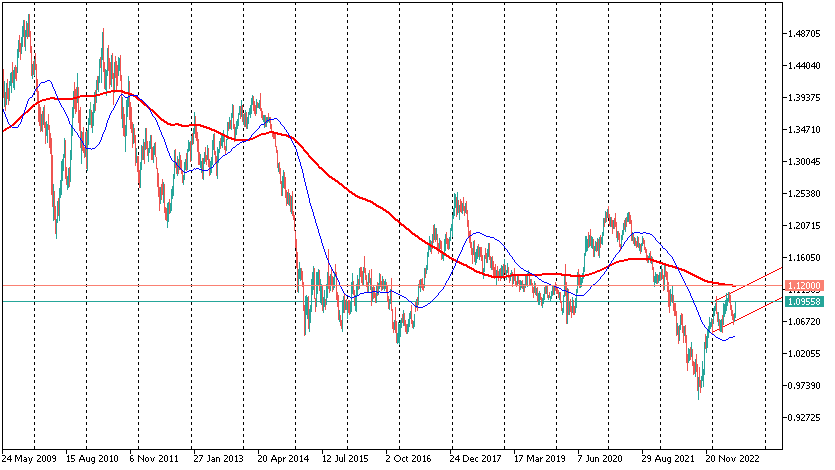

EURUSD Targets 1.11; 1.12 Won’t be Easy to Overcome

On Thursday, the ECB raised three key interest rates by 25 basis points, taking the benchmark lending rate to 4%, the highest since 2008. It also confirmed its intention to refuse to refinance coupons and maturing bonds, accelerating quantitative easing – another parameter of policy tightening.

Markets had anticipated this move, so the attention of traders and journalists was, as usual, focused on the comments that would determine the trajectory of future actions.

In contrast to Fed Chairman Powell, ECB President Lagarde was much more reassuring about future moves. She confidently stated that a few more hikes would be needed, leaving little doubt about a hike at the next meeting. This sharply contrasted with Powell, who highlighted a July hike as the more likely scenario but did not rule out the possibility of no hike.

Lagarde pointed to the strength of the labour market and rising core inflation as factors in domestic price pressures. Despite the reversal to a lower inflation trend, she maintained that the ECB still has ground to cover to contain inflation.

It took some time for the markets to appreciate the seriousness of the ECB’s stance. An initial 0.5% rise in EURUSD on the release of the commentary, which did not soften the tone significantly from May, picked up after the press conference and continued for the rest of the day, giving EURUSD a 1.1% gain, with the pair stabilising around 1.0950.

The pair’s technical disposition should also be considered, as it adds to the amplitude. After rising above 1.0880, the EURUSD crossed the 50-day moving average, and a decisive take of this level further supports the buyers’ resolve.

The EURUSD has been trading in a broad bullish corridor since the beginning of the year after bouncing off its lower boundary earlier this month and confirming the seriousness of the short-term uptrend with yesterday’s strong move. The bulls are now focusing on the 1.1050 area, the April high.

However, given the upward bias of the move, the pair could be as high as 1.1100 by the end of the month. The 1.1200 area will be the next major milestone, through which the ultra-long 200-week moving average trend passes, and many pivot points are concentrated. The dollar will struggle there.

Ending the Week on a Positive Note, More Central Banks Next Week

Markets are ending the week on a positive note but there remains enormous uncertainty around inflation and interest rates that looks set to continue throughout the summer.

Expectations are changing considerably on a very regular basis, with markets now pricing in no rate cuts in the US this year but a strong chance of one more hike, which still falls short of the median two from the Fed dot plot. The central bank opted to buy itself time on Wednesday which may prove to be a good decision given the scale of tightening already seen and the progress we're seeing across a selection of indicators.

The ECB on the other hand believes there's still more to do, so much so that it insisted that barring material change, another 25 basis point hike will follow in July. Investors mostly took this on board but perhaps not as strongly as President Lagarde would have liked.

There are a number of other interest rate decisions to come next week, with the Bank of England being the standout considering its one of the few central banks that appears to have achieved very little in its battle with inflation. CPI data released the day before may deliver another hammer blow to ambitions to pause the tightening cycle, bringing the UK another step closer to recession. Could the central bank move back to super-sized hikes?

Oil steadies but further volatility may be in store

Oil prices are steady at the end of the week, the rest of which has been anything but. There’s been a lot to factor in recently from OPEC+ (Saudi) output cuts to higher interest rate expectations, deteriorating economic prospects, and rate cuts in China.

In all of that, the price has held in its lower 2023 range - roughly $70-$80 in Brent - but it did test the lower end of this earlier in the week. Going forward, the focus will likely remain on interest rates and just how much they will threaten economies into year-end and perhaps what else China has up its sleeve to support the economy.

There was a brief surge in the price of natural gas on Thursday, apparently triggered by plans in the Netherlands to close a field. It may be that this was a knee-jerk reaction to what shouldn’t be big news but it perhaps highlights how sensitive the market remains to outages given it triggered a 30% rally at one stage.

Gold rebounds strongly despite Fed rate cuts being priced out this year

The slide in the dollar in recent days, alongside US yields since the Fed pause on Wednesday, has given gold a boost going into the end of the week. Since breaking below the lower end of its recent trading range - roughly between $1,940 and $1,980 - the yellow metal has rebounded strongly and now finds itself not far from the upper end of the range.

With the Fed far from convinced that its tightening cycle is over - quite the opposite in fact, the median estimate is that there’ll be two more hikes this year and one policymaker thinks four - and markets having now priced out those rate cuts this year, it may take something significant to sway gold one way or another. No further hikes looks much more likely after the pause, regardless of the dot plot, but it will require convincing data over the coming weeks.

Bitcoin near lows despite Blackrock SEC filing

Another fascinating week in the crypto space, which ends with Blackrock filing for a spot Bitcoin ETF with the SEC, using Coinbase as Custodian. The same Coinbase that is currently being sued by the SEC for running unregistered securities exchanges. While this may be a big move over the longer term, you can imagine it won’t be a quick process which may be why bitcoin traders haven’t got too excited at this stage. In fact, it hit three-month lows on Thursday before rebounding to trade just below $26,000.