Sample Category Title

USD/CAD Weekly Outlook

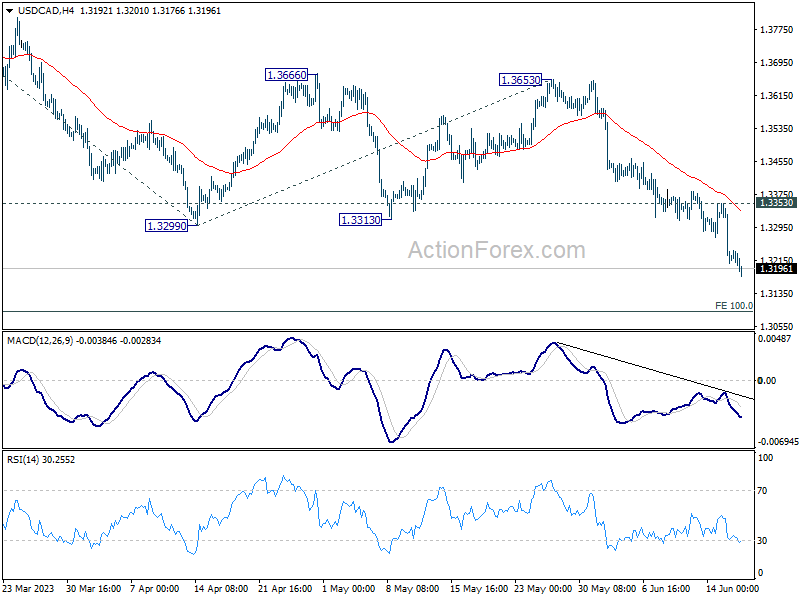

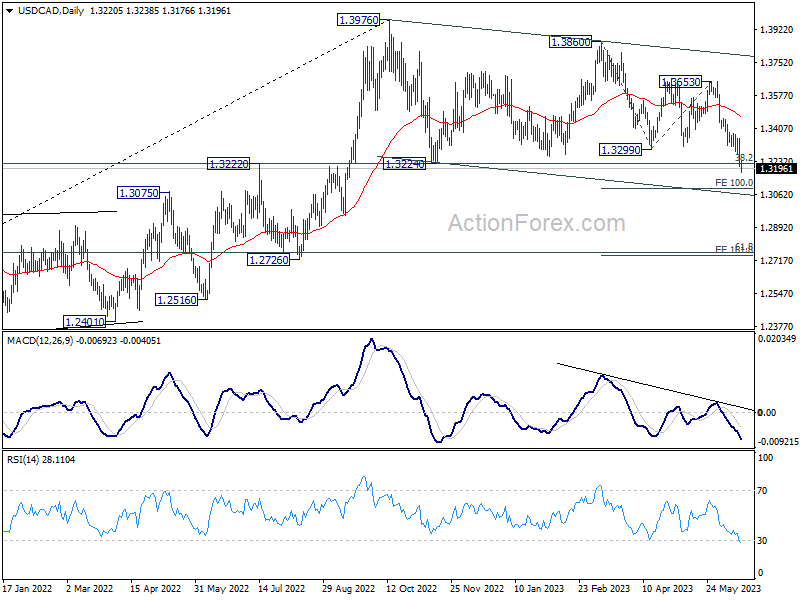

USD/CAD's break of 1.3224 support last week indicates that deeper correction is underway. Initial bias stays on the downside this week for 100% projection of 1.3860 to 1.3299 from 1.3653 at 1.3092 next. On the upside, above 1.3353 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low), but chance of trend reversal is increasing with current decline. But in either case, sustained trading below 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will pave the way to 61.8% retracement at 1.2758. Risk will stay on the downside as long as 1.3653 resistance holds, even in case of strong rebound.

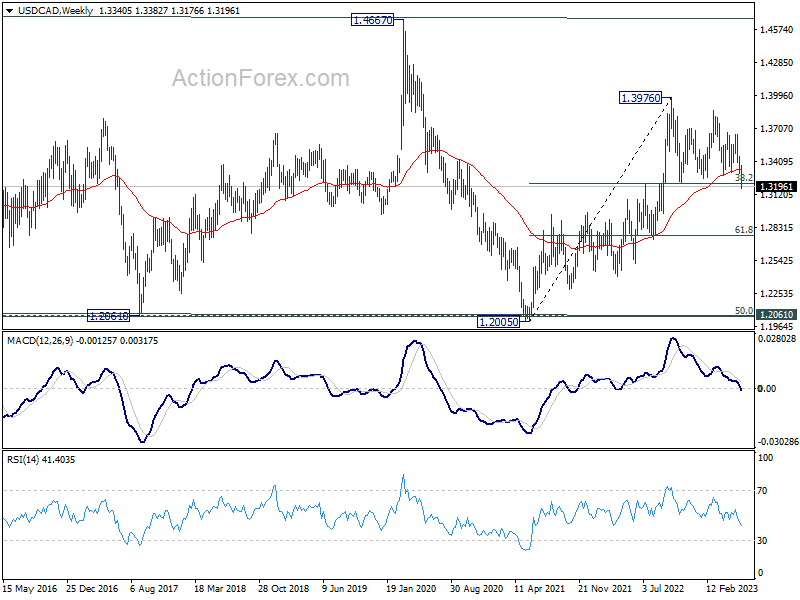

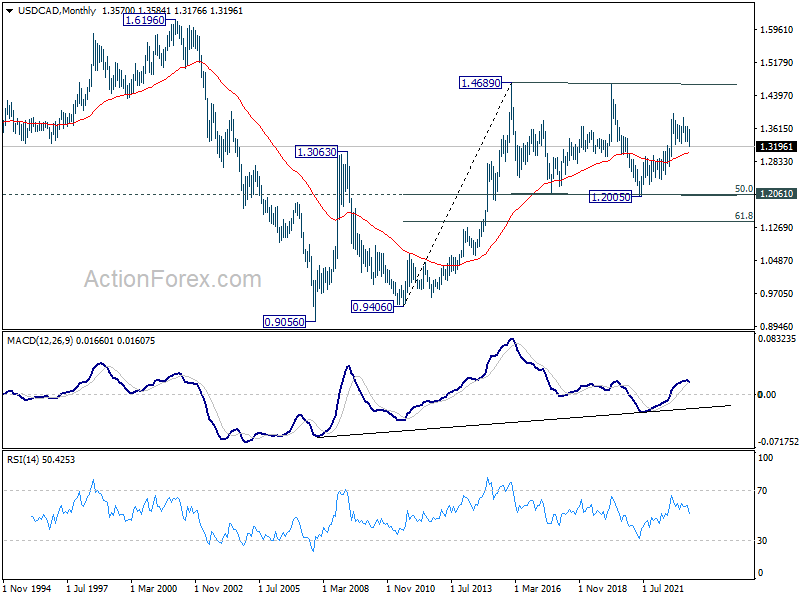

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3046) holds.

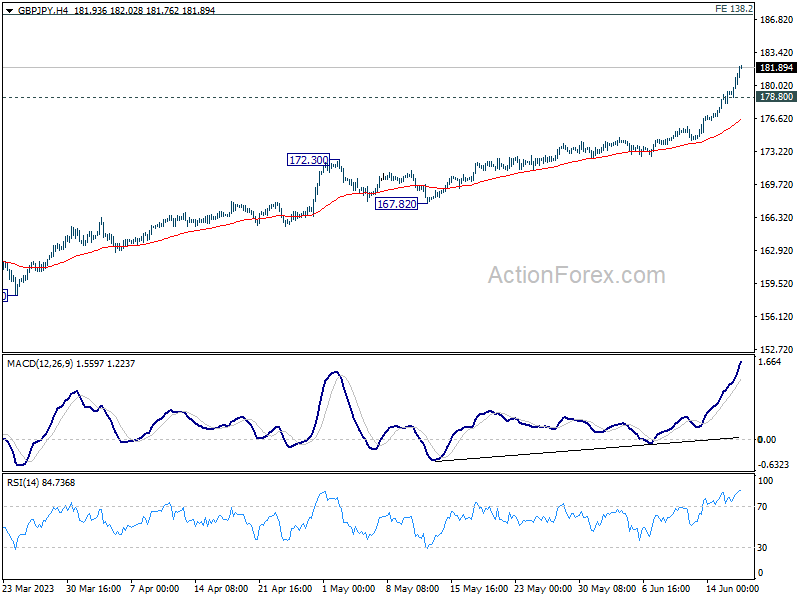

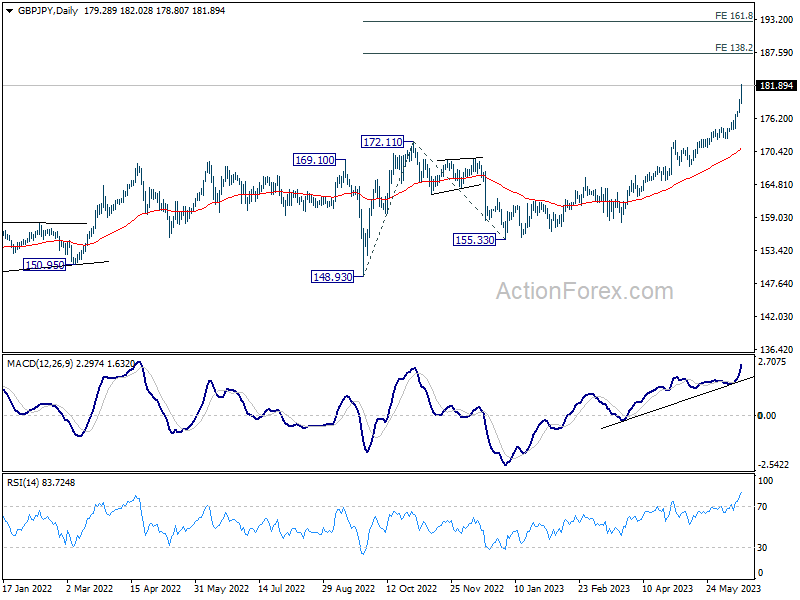

GBP/JPY Weekly Outlook

GBP/JPY surged to as high as 182.02 last week as up trend continued. Initial bias remains on the upside this week. Next target is 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36. On the downside, below 178.80 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

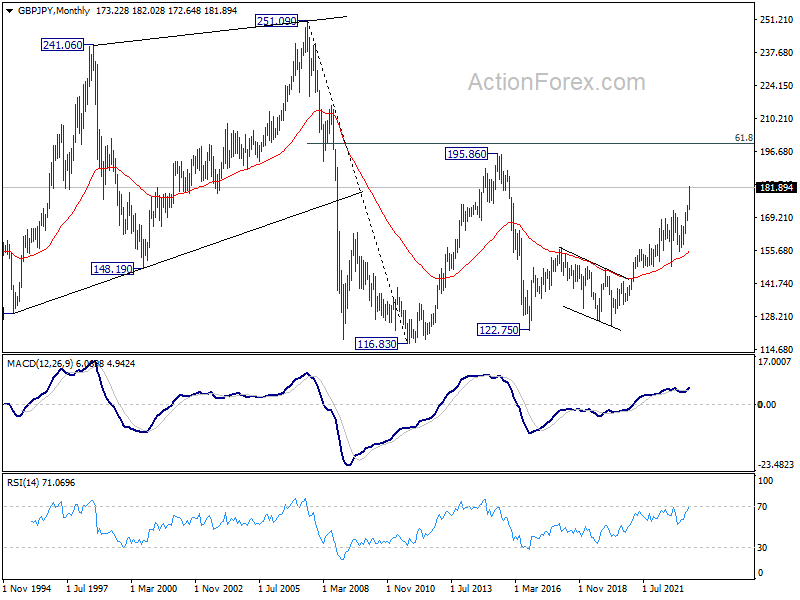

In the longer term picture, rise from 122.75 (2016 low) in still in progress to retest 195.86 (2015 high). Based on current momentum, break of 195.86 is in favor. But strong resistance could still be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 (2011 low) at 199.80 to limit upside on first attempt.

Global Markets Unfazed by Central Banks’ Moves, Risk-On Sentiment Prevails

Despite policy tightening from ECB and Fed's hawkish hold last week, global markets largely shrugged off the central banks' actions. Investors' sentiment remained buoyant, propelling many global markets to impressive rallies. Germany's DAX index even recorded a new all-time high.

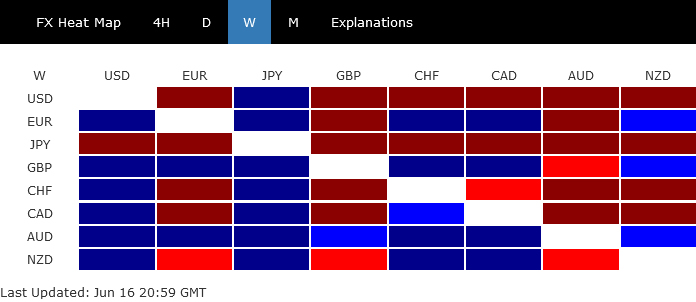

In the forex market, Yen took a significant hit and emerged as the week's worst performer by a mile. Policy divergence between BoJ and other central banks was a dominant factor led to the Yen's underperformance. Dollar wasn't far behind, sliding further as the correlation with risk sentiment seemed to invert once again. Swiss Franc, another traditional safe-haven currency, was the third weakest performer, further underscoring the prevailing risk-on environment.

Contrastingly, Australian Dollar outperformed, buoyed by robust domestic job data and expectations of further monetary tightening. Commodity prices also got a boost following China's decision to cut rates, providing an additional lift to the Aussie. British Pound secured the second strongest position, propelled by expectations of more rate hikes from BoE and significant buying against European majors. Euro, despite ECB's rate hike, lagged behind, only ended as the third strongest for the week.

US stocks extended rally, bullish investors skeptical on Fed's rate projections

Fed maintained interest rates at 5.00-5.25% during last week's FOMC meeting, an outcome that was in line with market expectations. However, it made a surprising upward adjustment in the median economic projections for the year, indicating that federal funds rate could peak at 5.60% instead of previously forecast 5.10%. This suggests two more 25bps rate hikes this year.

According to the new dot plot, twelve Fed members are now expecting rates to reach 5.50-5.75% or higher within the year. Also, the central bank foresees interest rates falling at a slower pace, dropping to 4.6% in 2024 (as opposed to the earlier forecast of 4.3%), and then to 3.4% in 2025 (versus t 3.1%).

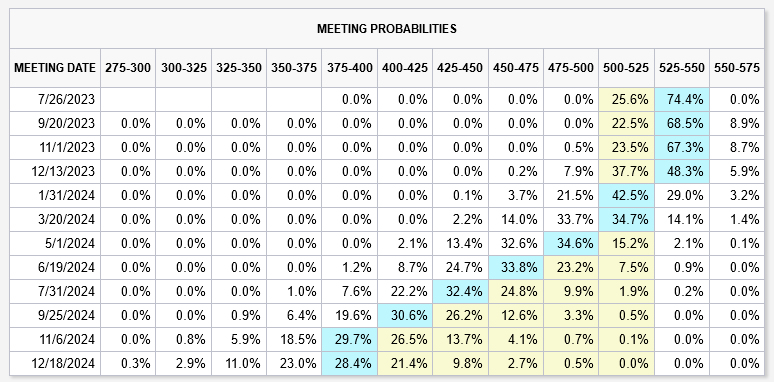

However, these hawkish projections appear not to have convinced the markets. Fed fund futures show a 74.4% likelihood of another 25bps hike in July, bringing rates to 5.25-5.50%. Yet, the probability of an additional hike for the remainder of the year stands at less than 10%. Though, expectations for the first rate cut are now pushed forward to January, with odds around 68%.

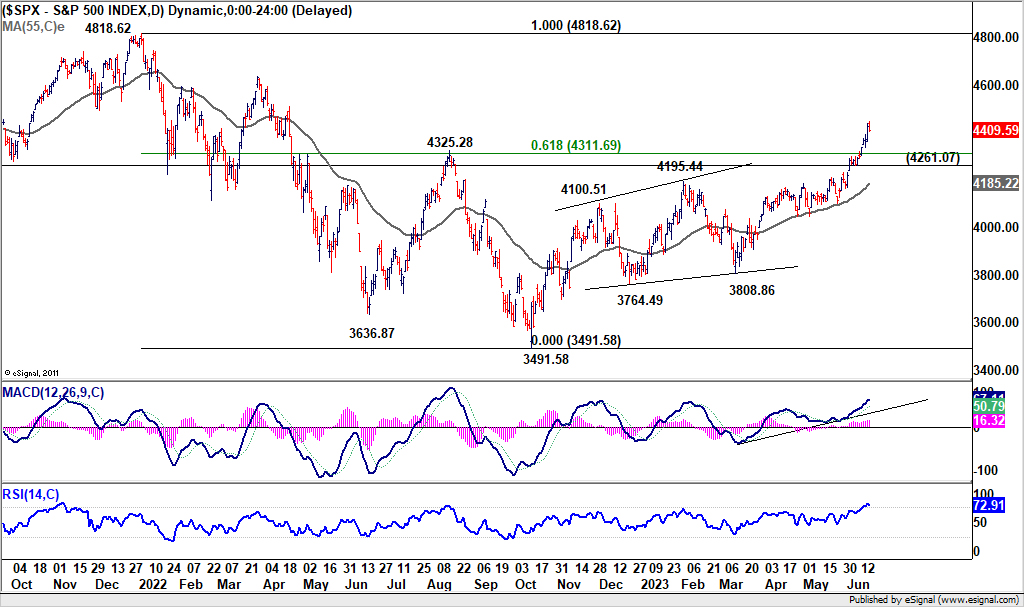

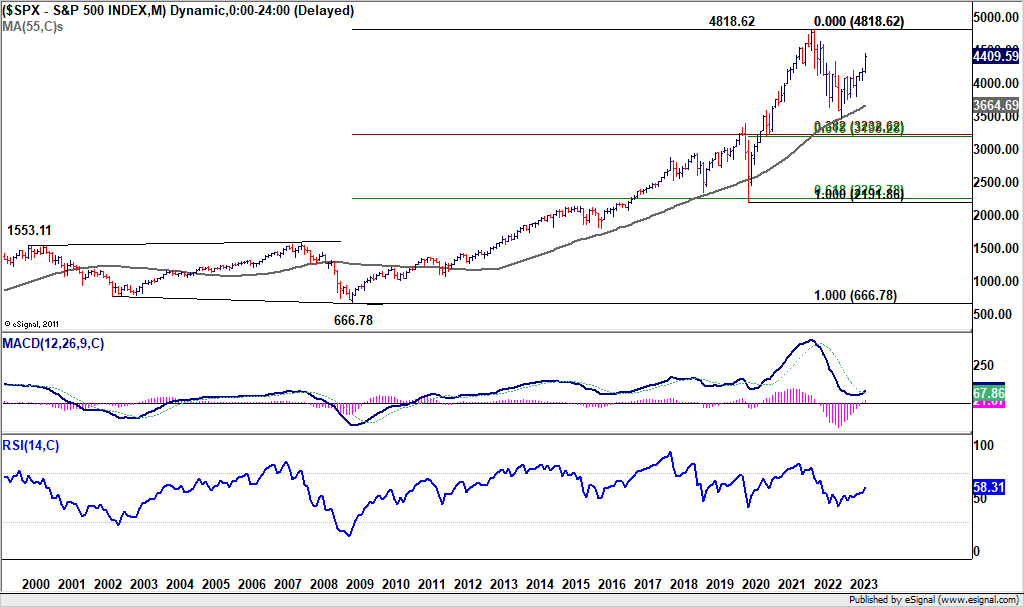

Interestingly, US stocks largely shrugged off Fed's more aggressive rate projections. The three major indexes ended the week on a higher note. S&P 500 convincingly surpassed key structural and cluster resistance at 4325.28 (61.8% retracement of 4818.62 to 3491.58 at 4311.69), to close at 4409.50.

This development should confirm that corrective fall from 4818.62 has concluded at 3491.58, after drawing support from 55 M EMA.

Whether the rise from 3491.58 marks the second leg of the corrective pattern from 4818.62 or signifies a resumption of the long-term uptrend remains to be seen. Regardless, as long as 4261.07 support holds, near-term outlook will remain bullish. Retest of 4818.62 high should be seen next.

DAX hit new record despite ECB hike and hawkish stance

ECB delivered on expectations by hiking interest rates by 25bps, elevating the main refinancing and deposit rates to 4.00% and 3.50% respectively. The decision came alongside a notable upward revision the core inflation forecast for 2023 and 2024, with a slight bump in 2025 projection. Concurrently, growth estimates were slightly reduced for 2023 and 2024.

In her post-meeting press conference, ECB President Christine Lagarde unequivocally underscored the hawkish stance. Lagarde emphasized that the central bank is not finished with its policy adjustments, stating, "Are we done? Have we finished the journey? No. We're not at our destination. Do we still have ground to cover? Yes, we still have ground to cover."

Lagarde explicitly indicated continued tightening trajectory in the near term, adding, "Barring a material change to our baseline, it is very likely that we will continue to increase rates at our next policy meeting in July." Thereafter, the central bank will continue to follow a "data-dependent approach".

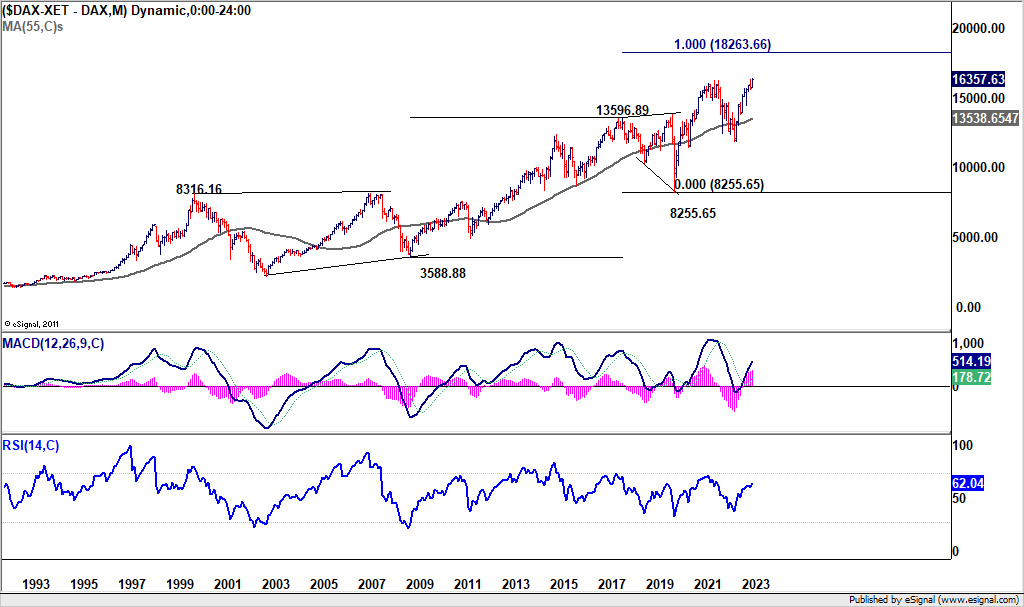

Yet European stock investors were not bothered by hawkish ECB. DAX has indeed extended its medium term up trend to close at new record high at 16357.53. For the near term, outlook will stay bullish as long as 55 D EMA holds (now at 15851.59). Next target is 61.8% projection of 11862.84 to 15658.56 from 14458.39 at 16804.14.

Depending on sustainability of buying momentum, there is prospect for DAX to target 61.8% projection of 3588.88 to 13596.89 from 8255.65 at 18263.66 in the medium term.

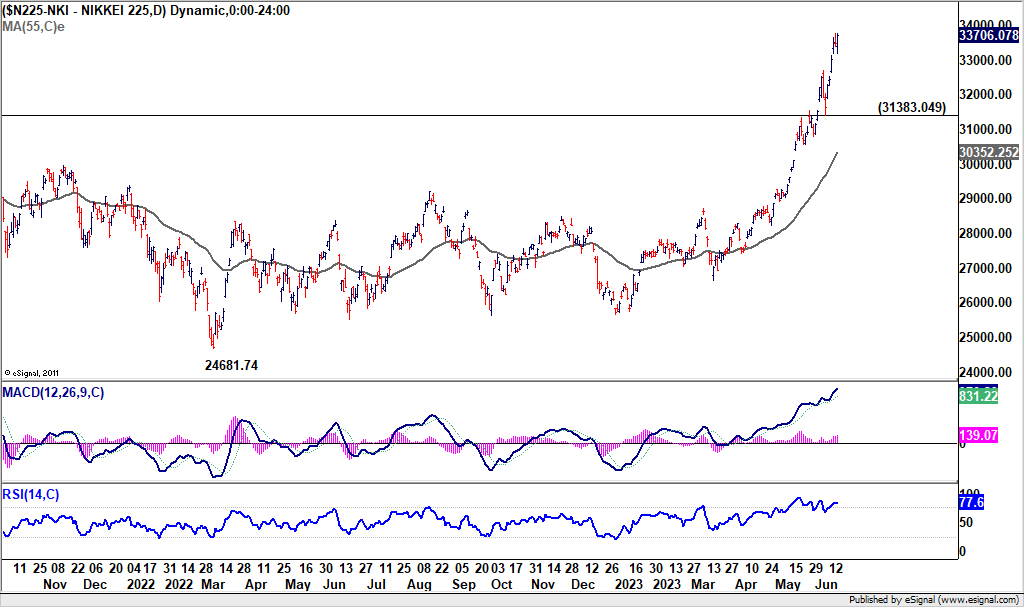

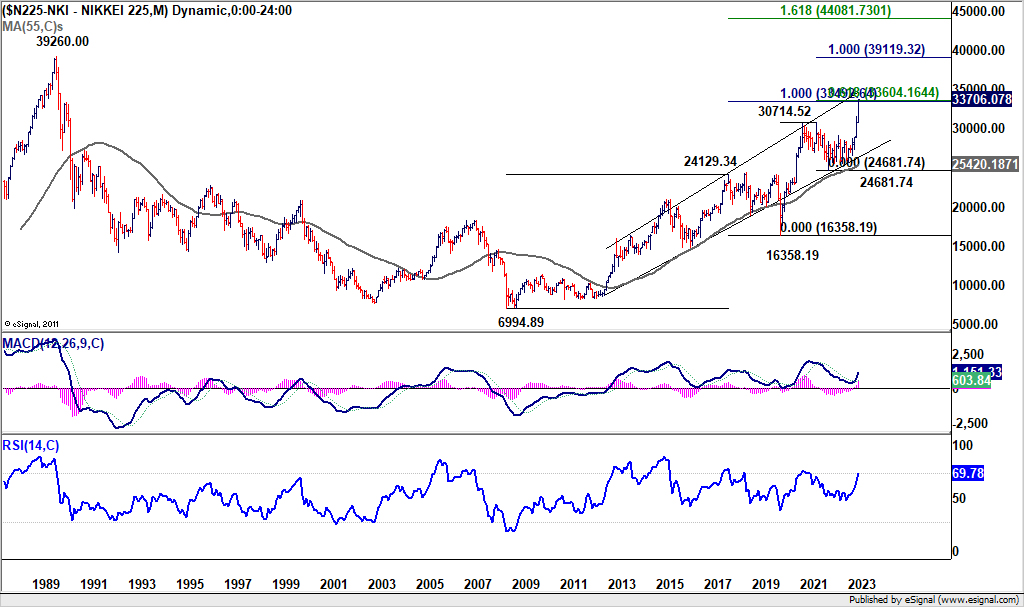

Nikkei surged as BoJ refrained from policy normalization, ready for record high?

The story in Japan was slightly different. BoJ continued to refrain from ending the ultra-loose monetary policy, stood pat last week. Governor Kazuo Ueda indicated clearly that inflation could fall below target ahead, and "that's why we are not normalizing monetary policy".

Nikkei surged earlier in the week and kept almost all of its gains after BoJ, closing at 33706.07, another three-decade high. Indeed, Nikkei has closed above a key cluster projection level at around 33500, including 61.8% projection of 16358.19 to 30714.52 from 24681.74 at 33533.95. and 100% projection of 6994.89 to 24129.34 from 16458.19 at 33492.64.

Near term outlook would stay bullish as long as 31383.05 support holds. Next target is 100% projection of 16358.16 to 30714.52 from 24681.74 at 39119.32, which is close to 1990 record high at 39260.00.

Meanwhile, it should be noted that Nikkei's momentum could depend on whether Japan would allow Yen to continue depreciation at the current pace.

Dollar index might be ready to break through 100

Dollar ended as the second worst in spite of hawkish Fed rate projections. Strong rally in global stock markets appeared to be the reason. But it's still certain if the inverse relationship between the greenback and risk sentiment is totally back.

In any case, Dollar index's rebound from 100.78 should have completed at 104.69. It's likely that the consolidation pattern from 100.82 has finished in a three-wave structure too. Risk will now be heavily on the downside as long as 55 D EMA (now at 103.05) holds. Retest of 100.78/82 support zone should be seen next. Decisive break there will confirm resumption of whole down trend from 114.77.

From a long term picture, ideally, 97/98 handle should provide strong enough support to DXY. The level represents 55 M EMA (now at 97.87) and 38.2% retracement of 70.69 to 114.77 at 97.93. Strong rebound from that level could complete the whole fall from 114.77, as the first leg of a long term corrective pattern. However, sustained break of 97 would pave the way to the second line of defense in channel support at around 93.00.

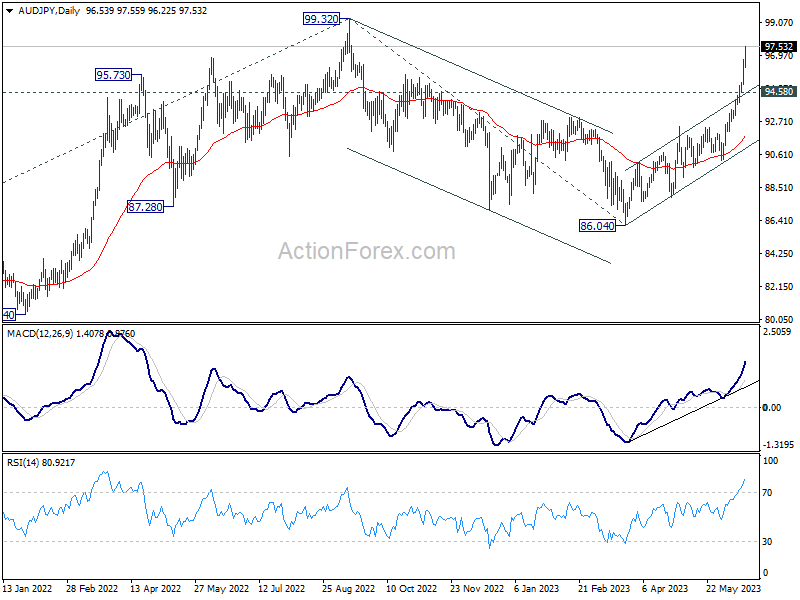

AUD/JPY's upside acceleration suggests up trend ready to resume

Yen was clearly even worse than Dollar, with AUD/JPY, GBP/JPY, EUR/JPY and NZD/JPY gaining more than 3.4% last week. AUD/JPY's upside acceleration, as seen is the strong break of near term channel resistance and D MACD, suggests that it's probably resuming the whole up trend from 59.85. In any case, outlook will stay bullish as long as 94.58 support holds. Retest of 99.32 should be seen next.

The question now is whether AUD/JPY would head to after breaking 99.32. The long term trend line resistance (now at around 100.34), could be a tough one to overcome. However, sustained trading above there could clear the way through 105.42 (2013 high) and even 107.88 (2007 high). In this case, next medium to long term target will be 61.8% projection of 59.85 to 99.32 from 86.04 at 110.43.

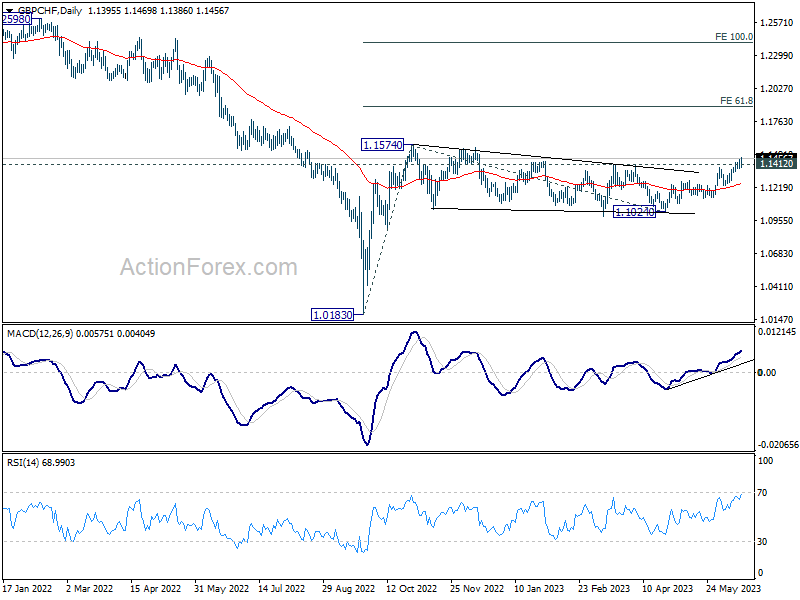

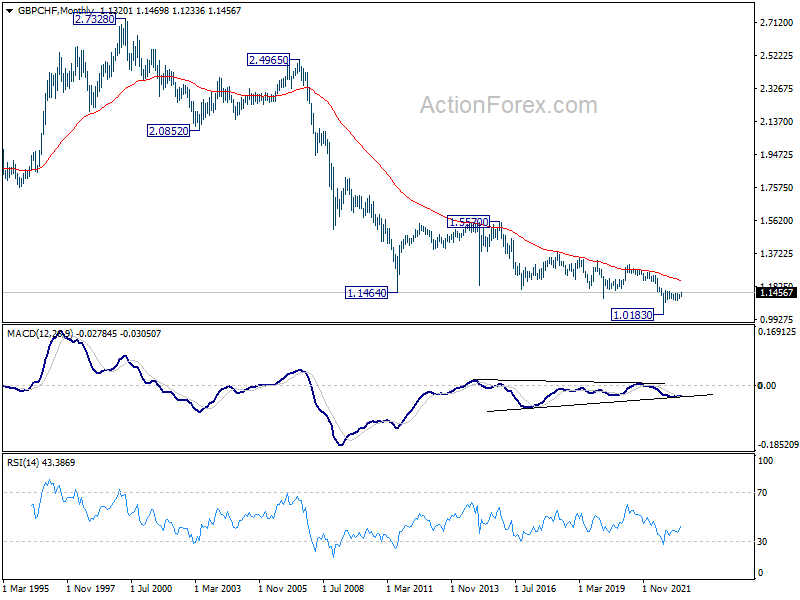

GBP/CHF heading for retesting 1.1574 resistance ahead of BoE and SNB

Looking ahead, GBP/CHF would be a pair to watch too with BoE and SNB rate decisions featured in the coming days. Last week's break of 1.1412 resistance argues that whole consolidation pattern from 1.1574 has completed at 1.1025. More importantly, rise from 1.0183 is ready to resume.

Sustained trading above 1.1412 this week will bring retest of 1.1574 first. Firm break there will confirm this bullish case and target 61.8% projection of 1.0183 to 1.1574 from 1.1024 at 1.1884.

From a long term point of view, it's too early to tell if trend reversal is underway. But bullish convergence condition in M MACD is a positive sign. A test on 55 M EMA (now at 1.2155) is possible if 1.1574 can be taken out decisively.

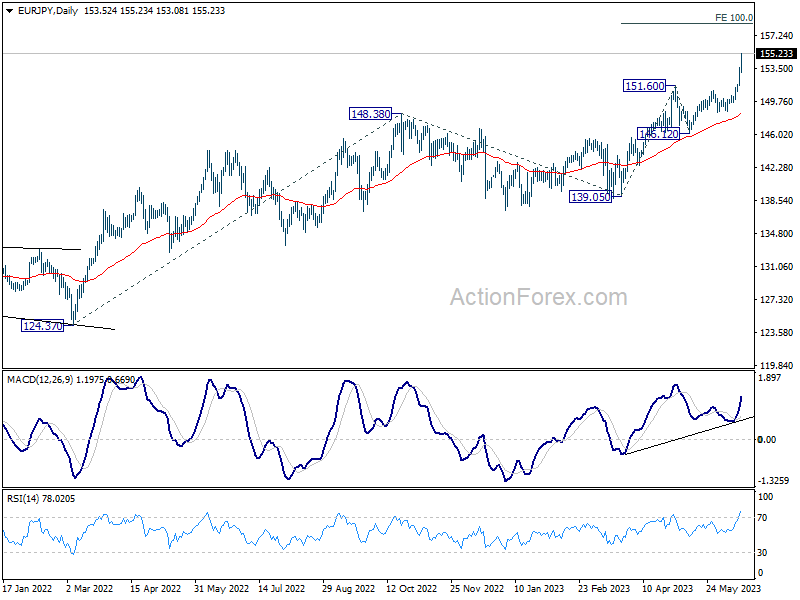

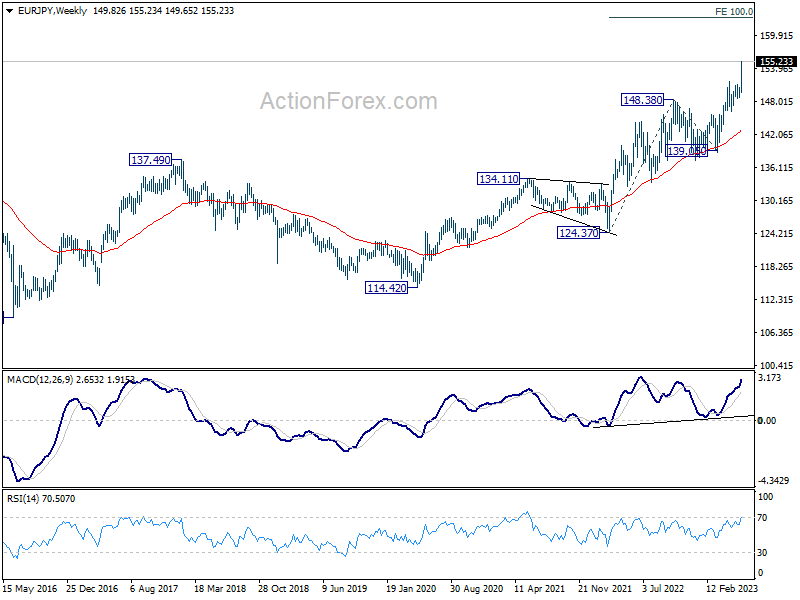

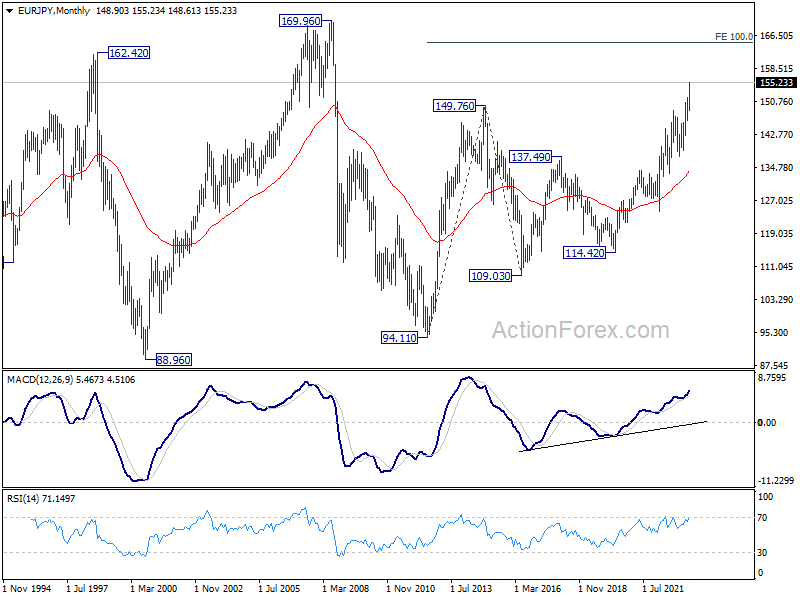

EUR/JPY Weekly Outlook

EUR/JPY's up trend resumed last week and surged to as high as 155.23. Initial bias stays on the upside this week for 100% projection of 139.05 to 151.60 from 146.12 at 158.67 next. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

EUR/JPY Weekly Outlook

EUR/JPY's up trend resumed last week and surged to as high as 155.23. Initial bias stays on the upside this week for 100% projection of 139.05 to 151.60 from 146.12 at 158.67 next. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

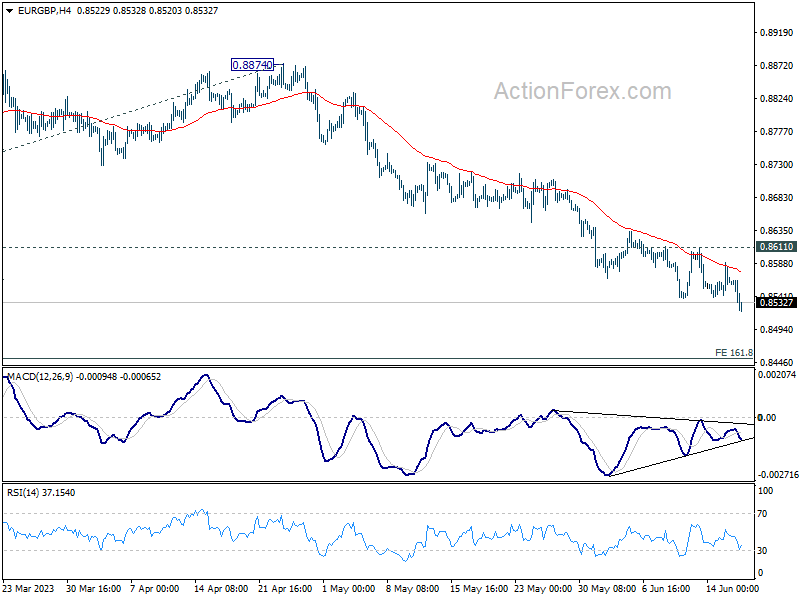

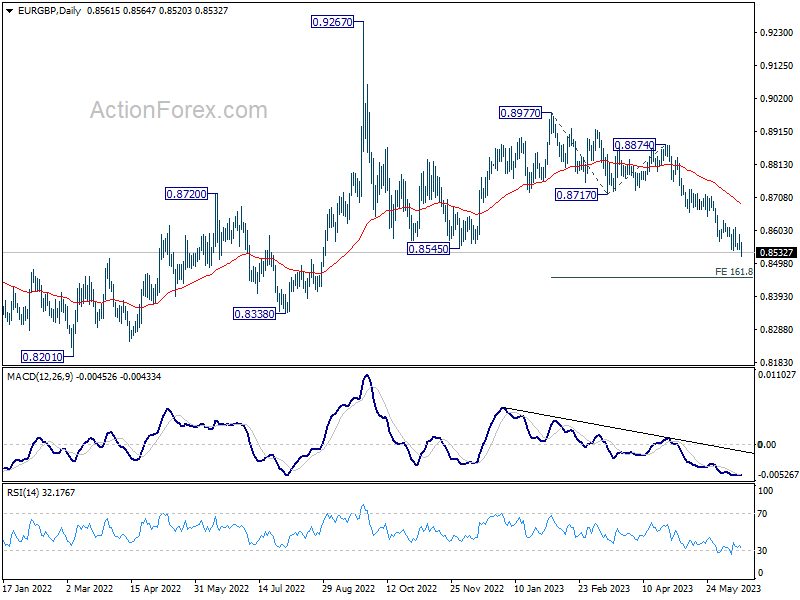

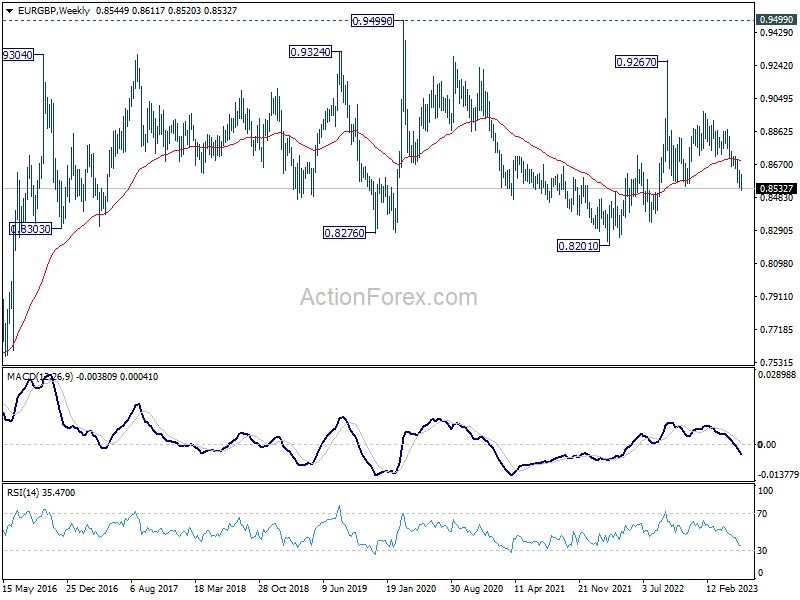

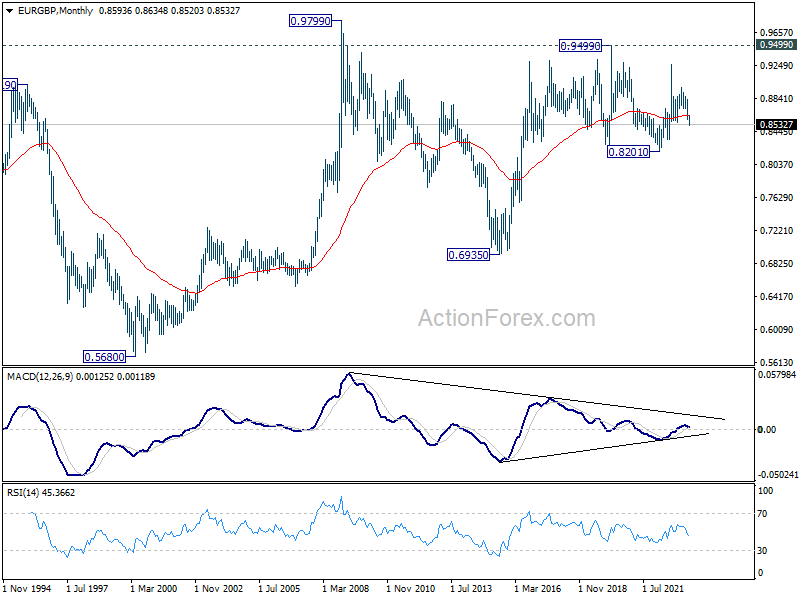

EUR/GBP Weekly Outlook

EUR/GBP's decline from 0.8977 continued last week and hit as low as 0.8520 so far. Initial bias is on the downside this week. Next target is 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. However, break of 0.8611 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

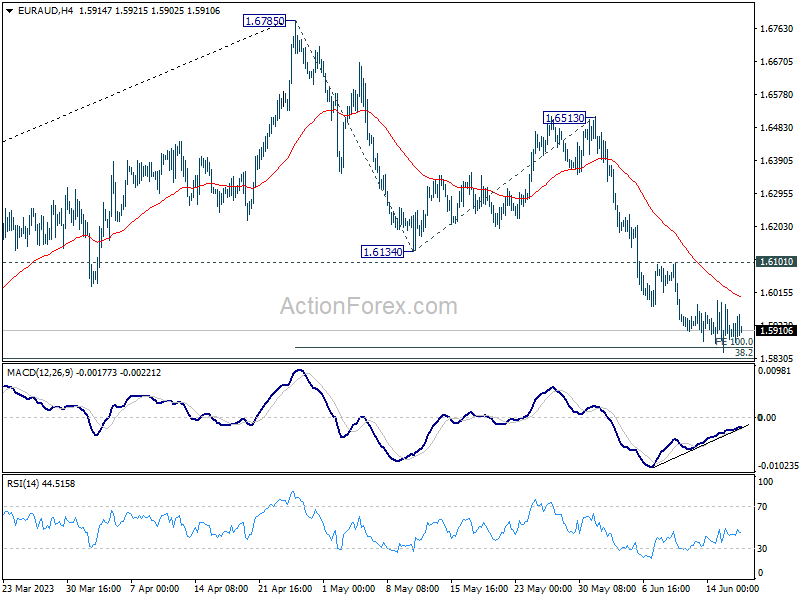

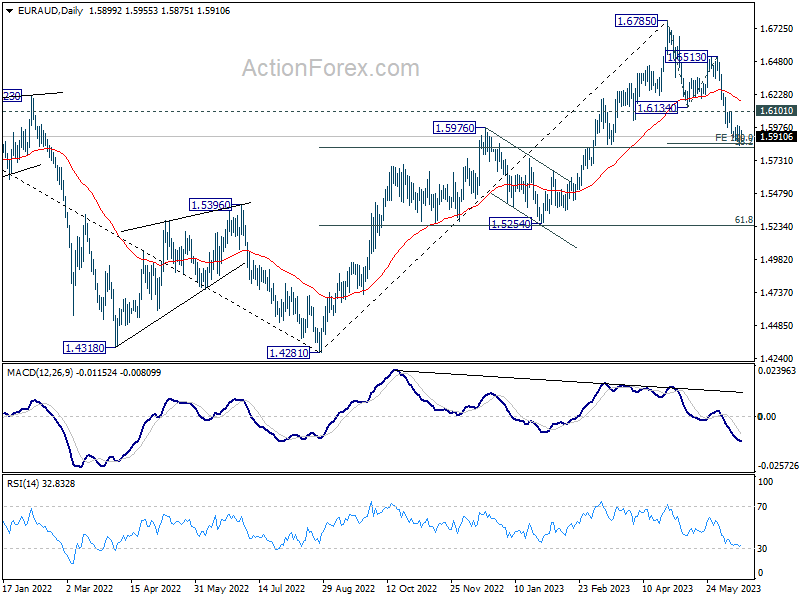

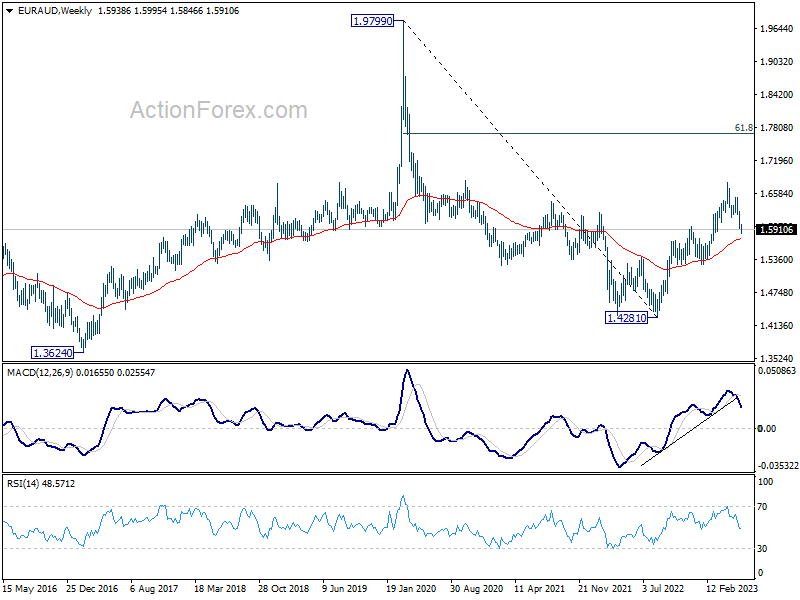

EUR/AUD Weekly Outlook

EUR/AUD continued to lose downside momentum last week, even though there was not solid bounce yet. Initial bias remains neutral this week first. Strong support is expected from around 100% projection of 1.6785 to 1.6134 from 1.6513 at 1.5862 to complete the fall from 1.6785. On the upside, break of 1.6101 resistance will confirm short term bottoming, and turn bias back to the upside for rebound.

In the bigger picture, price actions from 1.6785 are seen as a correction to up trend from 1.4281 (2022 low) only. Strong support should be seen around 38.2% retracement of 1.4281 to 1.6785 at 1.5828 to complete the first leg and bring rebound. However, sustained trading below 1.5828 will raise the chance of trend reversal and target 61.8% retracement at 1.5238.

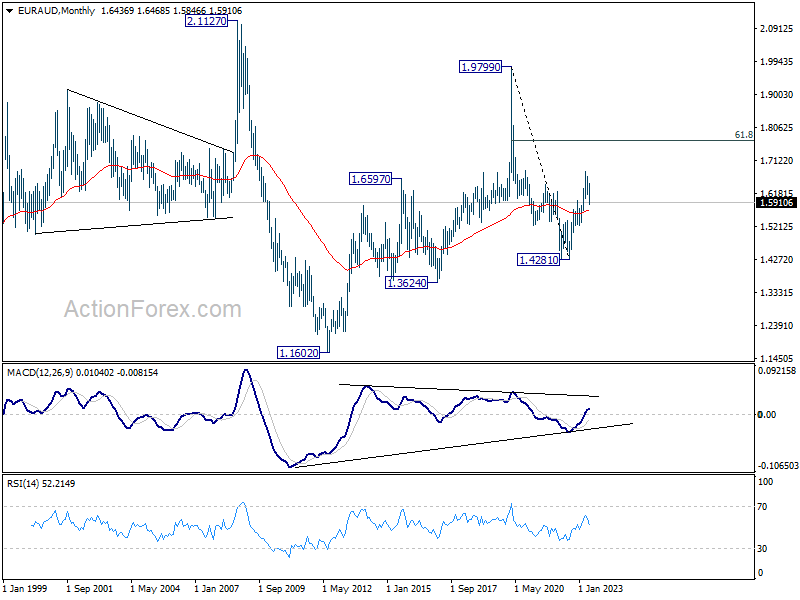

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

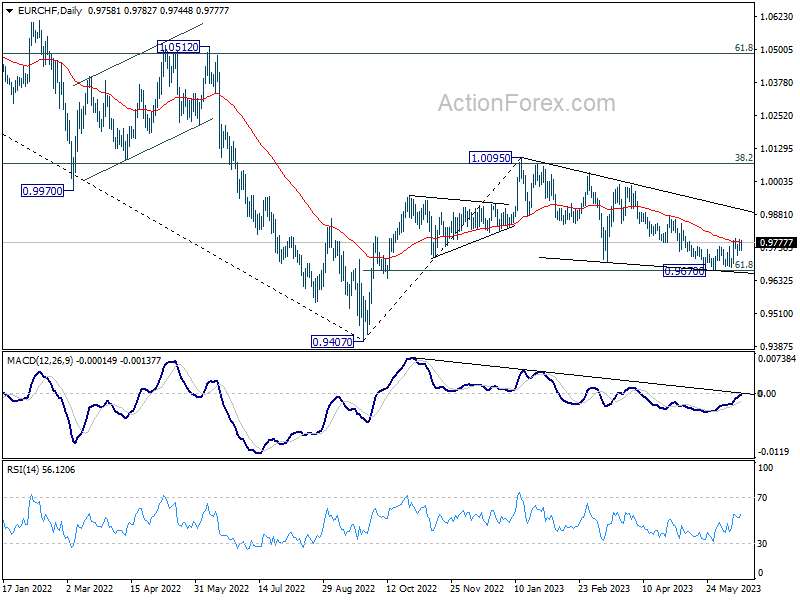

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9793 last week but turned sideway since then. Still, a short term bottom should be in place after hitting 61.8% retracement of 0.9407 to 1.0095 at 0.9670. Further rally is in favor. Break of 0.9793 and sustained trading above 55 D EMA (now at 0.9778) will add to case that whole correction from 1.0095 has completed Intraday bias will be back on the for 0.9878 resistance next.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9924). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0484) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Summary 6/19 – 6/23

Monday, Jun 19, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 49.8 | |

| 12:30 | CAD | Industrial Product Price M/M May | 0.20% | -0.20% |

| 12:30 | CAD | Raw Material Price Index M/M May | 2.40% | 2.90% |

| 14:00 | USD | NAHB Housing Market Index Jun | 50 | 50 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | |

| Forecast: | Previous: 49.8 | ||

| 12:30 | CAD | Industrial Product Price M/M May | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 12:30 | CAD | Raw Material Price Index M/M May | |

| Forecast: 2.40% | Previous: 2.90% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | |

| Forecast: 50 | Previous: 50 | ||

Tuesday, Jun 20, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes | ||

| 04:30 | JPY | Industrial Production M/M Apr F | -0.40% | -0.40% |

| 06:00 | CHF | Trade Balance (CHF) May | 3.45B | 2.60B |

| 06:00 | EUR | Germany PPI M/M May | 0.30% | |

| 06:00 | EUR | Germany PPI Y/Y May | 4.10% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 27.3B | 31.2B |

| 12:30 | USD | Housing Starts May | 1.40M | 1.40M |

| 12:30 | USD | Building Permits May | 1.43M | 1.42M |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Minutes | |

| Forecast: | Previous: | ||

| 04:30 | JPY | Industrial Production M/M Apr F | |

| Forecast: -0.40% | Previous: -0.40% | ||

| 06:00 | CHF | Trade Balance (CHF) May | |

| Forecast: 3.45B | Previous: 2.60B | ||

| 06:00 | EUR | Germany PPI M/M May | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | EUR | Germany PPI Y/Y May | |

| Forecast: | Previous: 4.10% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | |

| Forecast: 27.3B | Previous: 31.2B | ||

| 12:30 | USD | Housing Starts May | |

| Forecast: 1.40M | Previous: 1.40M | ||

| 12:30 | USD | Building Permits May | |

| Forecast: 1.43M | Previous: 1.42M | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Wednesday, Jun 21, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M May | -0.03% | |

| 06:00 | GBP | CPI M/M May | 0.40% | 1.20% |

| 06:00 | GBP | CPI Y/Y May | 8.50% | 8.70% |

| 06:00 | GBP | Core CPI Y/Y May | 6.80% | 6.80% |

| 06:00 | GBP | RPI M/M May | 0.50% | 1.50% |

| 06:00 | GBP | RPI Y/Y May | 11.10% | 11.40% |

| 06:00 | GBP | PPI Input M/M May | -0.60% | -0.30% |

| 06:00 | GBP | PPI Input Y/Y May | 2.40% | 3.90% |

| 06:00 | GBP | PPI Output M/M May | 0% | 0% |

| 06:00 | GBP | PPI Output Y/Y May | 4.10% | 5.40% |

| 06:00 | GBP | PPI Core Output M/M May | 0.10% | 0.00% |

| 06:00 | GBP | PPI Core Output Y/Y May | 4.70% | 6.00% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 20.3B | 24.7B |

| 12:30 | CAD | New Housing Price Index M/M May | 0.00% | -0.10% |

| 12:30 | CAD | Retail Sales M/M Apr | 0.30% | -1.40% |

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 0.30% | -0.30% |

| 22:45 | NZD | Trade Balance (NZD) May | 350M | 427M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M May | |

| Forecast: | Previous: -0.03% | ||

| 06:00 | GBP | CPI M/M May | |

| Forecast: 0.40% | Previous: 1.20% | ||

| 06:00 | GBP | CPI Y/Y May | |

| Forecast: 8.50% | Previous: 8.70% | ||

| 06:00 | GBP | Core CPI Y/Y May | |

| Forecast: 6.80% | Previous: 6.80% | ||

| 06:00 | GBP | RPI M/M May | |

| Forecast: 0.50% | Previous: 1.50% | ||

| 06:00 | GBP | RPI Y/Y May | |

| Forecast: 11.10% | Previous: 11.40% | ||

| 06:00 | GBP | PPI Input M/M May | |

| Forecast: -0.60% | Previous: -0.30% | ||

| 06:00 | GBP | PPI Input Y/Y May | |

| Forecast: 2.40% | Previous: 3.90% | ||

| 06:00 | GBP | PPI Output M/M May | |

| Forecast: 0% | Previous: 0% | ||

| 06:00 | GBP | PPI Output Y/Y May | |

| Forecast: 4.10% | Previous: 5.40% | ||

| 06:00 | GBP | PPI Core Output M/M May | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:00 | GBP | PPI Core Output Y/Y May | |

| Forecast: 4.70% | Previous: 6.00% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | |

| Forecast: 20.3B | Previous: 24.7B | ||

| 12:30 | CAD | New Housing Price Index M/M May | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 12:30 | CAD | Retail Sales M/M Apr | |

| Forecast: 0.30% | Previous: -1.40% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | |

| Forecast: 0.30% | Previous: -0.30% | ||

| 22:45 | NZD | Trade Balance (NZD) May | |

| Forecast: 350M | Previous: 427M | ||

Thursday, Jun 22, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:30 | CHF | SNB Rate Decision | 1.75% | 1.50% |

| 08:00 | CHF | SNB Press Conference | ||

| 11:00 | GBP | BoE Rate Decision | 4.75% | 4.50% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 7--0--2 |

| 12:30 | USD | Initial Jobless Claims (Jun 16) | 256K | 262K |

| 12:30 | USD | Current Account (USD) Q1 | -217B | -207B |

| 14:00 | USD | Existing Home Sales May | 4.25M | 4.28M |

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -17 | -17.4 |

| 14:30 | USD | Natural Gas Storage | 84B | |

| 15:00 | USD | Crude Oil Inventories | 7.9M | |

| 23:00 | AUD | Manufacturing PMI Jun P | 48.4 | |

| 23:00 | AUD | Services PMI Jun P | 52.1 | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -26 | -27 |

| 23:30 | JPY | National CPI Y/Y May | 3.50% | |

| 23:30 | JPY | National CPI Core Y/Y May | 3.10% | 3.40% |

| 23:30 | JPY | National CPI Core-Core Y/Y May | 4.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:30 | CHF | SNB Rate Decision | |

| Forecast: 1.75% | Previous: 1.50% | ||

| 08:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 11:00 | GBP | BoE Rate Decision | |

| Forecast: 4.75% | Previous: 4.50% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 7--0--2 | Previous: 7--0--2 | ||

| 12:30 | USD | Initial Jobless Claims (Jun 16) | |

| Forecast: 256K | Previous: 262K | ||

| 12:30 | USD | Current Account (USD) Q1 | |

| Forecast: -217B | Previous: -207B | ||

| 14:00 | USD | Existing Home Sales May | |

| Forecast: 4.25M | Previous: 4.28M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | |

| Forecast: -17 | Previous: -17.4 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 84B | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 7.9M | ||

| 23:00 | AUD | Manufacturing PMI Jun P | |

| Forecast: | Previous: 48.4 | ||

| 23:00 | AUD | Services PMI Jun P | |

| Forecast: | Previous: 52.1 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | |

| Forecast: -26 | Previous: -27 | ||

| 23:30 | JPY | National CPI Y/Y May | |

| Forecast: | Previous: 3.50% | ||

| 23:30 | JPY | National CPI Core Y/Y May | |

| Forecast: 3.10% | Previous: 3.40% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y May | |

| Forecast: | Previous: 4.10% | ||

Friday, Jun 23, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jun P | 50.2 | 50.6 |

| 06:00 | GBP | Retail Sales M/M May | -0.20% | 0.50% |

| 07:15 | EUR | France Manufacturing PMI Jun P | 45.2 | 45.7 |

| 07:15 | EUR | France Services PMI Jun P | 52.1 | 52.5 |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 43.6 | 43.2 |

| 07:30 | EUR | Germany Services PMI Jun P | 56.3 | 57.2 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 44.9 | 44.8 |

| 08:00 | EUR | Eurozone Services PMI Jun P | 54.5 | 55.1 |

| 08:30 | GBP | Manufacturing PMI Jun P | 46.8 | 47.1 |

| 08:30 | GBP | Services PMI Jun P | 54.9 | 55.2 |

| 13:45 | USD | Manufacturing PMI Jun P | 48.5 | 48.4 |

| 13:45 | USD | Services PMI Jun P | 54.0 | 54.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jun P | |

| Forecast: 50.2 | Previous: 50.6 | ||

| 06:00 | GBP | Retail Sales M/M May | |

| Forecast: -0.20% | Previous: 0.50% | ||

| 07:15 | EUR | France Manufacturing PMI Jun P | |

| Forecast: 45.2 | Previous: 45.7 | ||

| 07:15 | EUR | France Services PMI Jun P | |

| Forecast: 52.1 | Previous: 52.5 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | |

| Forecast: 43.6 | Previous: 43.2 | ||

| 07:30 | EUR | Germany Services PMI Jun P | |

| Forecast: 56.3 | Previous: 57.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | |

| Forecast: 44.9 | Previous: 44.8 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | |

| Forecast: 54.5 | Previous: 55.1 | ||

| 08:30 | GBP | Manufacturing PMI Jun P | |

| Forecast: 46.8 | Previous: 47.1 | ||

| 08:30 | GBP | Services PMI Jun P | |

| Forecast: 54.9 | Previous: 55.2 | ||

| 13:45 | USD | Manufacturing PMI Jun P | |

| Forecast: 48.5 | Previous: 48.4 | ||

| 13:45 | USD | Services PMI Jun P | |

| Forecast: 54.0 | Previous: 54.9 | ||

Week Ahead – A Huge Week for BoE, SNB to Keep Hiking, CBRT a Wildcard

US

It will be a quiet Monday as Wall Street observes Juneteenth. A week filled with economic releases will probably see the most attention go towards Fed speak. After the Fed’s hawkish skip, Wall Street wants to know if they can become convinced that we could see two more rate hikes. On Tuesday, Fed’s Bullard speaks at Barcelona School of Economics and Williams attends a NY Fed event. On Wednesday, Chair Powell appears before the House Financial Services Panel, while Goolsbee speaks at the Global Food Forum. On Thursday, Powell appears before the Senate Banking Panel. Mester and Barkin also make appearances on Thursday. Bullard and Mester also speak on Friday.

This week contains a lot of housing data, with building permits on Tuesday, weekly MBA mortgage applications on Wednesday, and existing home sales on Thursday. Housing data is expected to stabilize, but if we see strong demand for mortgages, that could unnerve the Fed. The end of the week contains the flash PMIs that should show manufacturing remains in contraction territory, while the service part of the economy softens.

Eurozone

The ECB made it very clear on Thursday that the tightening cycle is almost certainly not over and another 25 basis point hike is extremely likely. Markets had been pricing a small chance that the hike on Thursday will be the last – and interestingly, still are – which prompted questions and strong pushback from President Lagarde in the press conference. It would take “material change” for the committee to not raise rates, with a pause not even under consideration until now. The flash PMIs on Friday are unlikely to swing it one way or another but there isn’t much else of note next week.

UK

A lot of people in the UK are becoming anxious about remortgaging and wondering why, when the BoE was among the first to start raising rates, so many more hikes are expected over the rest of the year and even into the next. The economy has been more resilient than anticipated but inflation is much higher than we’re seeing elsewhere and hasn’t made nearly as much progress. The risk of it becoming embedded meaning higher rates for longer and an eventual economic slump is rising by the week.

People will be hoping for some good inflation news on Tuesday but if recent months are anything to go by, we should probably expect the worst and hope for the best. Another bad report could pile pressure on the BoE a day later to hike by 50 basis points. It’s only 12% priced in at the moment but that could change if the CPI data is ugly once again. And with 125 basis points of hikes priced in between now and February, there’s seemingly a lot of work still to do. Retail sales and flash PMIs are also due on Friday.

Russia

With the CBR warning that rate hikes may be next on the agenda rather than cuts due to higher-than-desired inflation expectations, all eyes will be on Wednesday’s PPI data. Previously it was -12.7% year on year but the more recent monthly data showed an uptick of 2.4% which suggests near-term trends are not favorable.

South Africa

Stagflation is a very real risk, with rolling blackouts exacerbating those fears by weighing on economic activity and adding to price pressures. The SARB has continued to raise rates despite inflation now not being far from target and it may be forced to continue if pressures don’t abate soon. CPI data on Wednesday will tell us if any further progress has been made. The rand has made strong gains in recent weeks buoyed by higher rates and data confirming the country avoided recession in the first quarter. But enormous challenges remain.

Turkey

The CBRT will announce its latest interest rate decision next week and frankly, no one knows what’s going to happen. Since being re-elected on the promise of defending lower interest rates, President Erdogan has replaced his finance minister and central bank governor with more respectable candidates in a sign of returning to more conventional policy. Under Erdogan, nothing is guaranteed and next week we’ll find out just how true that is.

Switzerland

The recent inflation report showed strong progress on getting inflation below 2% (2.2% in May) but that won’t be enough for the SNB to consider pausing on Thursday. In fact, markets are expecting the central bank to hike by 50 basis points, taking the policy rate to what Chairman Thomas Jordan suggested may be the neutral rate, of 2%.

China

In terms of economic data release, it will be a quiet week with only the 1-year and 5-year loan prime rates to be decided on Tuesday. Last week, the Chinese central bank, PBoC, finally decided to tweak its cautious targeted monetary policy stances by implementing cuts on its two interest rate policy tools; 10 bps cut to the 7-day reverse repo rate (1.9% from 2.0% previously) and the 1-year medium-term lending facility (2.65% from 2.75%), its first cut since August 2022.

Hence more monetary easing measures are now expected to help cushion the current pace of sluggishness seen in internal domestic demand where the 1-year and 5-year loan prime rates are forecasted to be cut by 10 bps cut each, bringing them to 3.55% and 4.2%, respectively. These prime rates are used to price corporate/consumer loans and mortgages.

Also do take note of a possible announcement of a new stimulus package under consideration that has been drafted by multiple government agencies to support areas such as real estate and domestic demand.

India

No key data releases.

Australia

Two key data to digest. Firstly, the release of the minutes of the recent RBA monetary policy decision on Tuesday; the RBA unexpectedly raised the policy cash rate by 25 bps to 4.1% on 6 June, an 11-year high. As of 16 June, the ASX 30-day interbank cash rate futures (July 2023 contract) has priced in a 53% chance of another 25 bps hike in the next RBA meeting to bring the cash rate to 4.35%.

On Friday, we get flash Manufacturing and Services PMIs for June; the manufacturing component is expected to contract further to 47.7 from 48.4 in May. If it turns out as forecasted, it will be the 4th consecutive month of deterioration in the manufacturing sector. The services sector is expected to decelerate to 51.5 from 52.1 in May.

New Zealand

On Monday, the services PMI for May is expected to slow slightly to 49.1 from 49.8 in April. Balance of trade data for May will be released on Thursday where a deficit of -NZ$0.3 billion is being forecasted after a surplus of NZ$0.427 billion was posted in April. Exports are expected to have decreased to NZ$6.6 billion from NZ$6.8 billion (April) and imports are forecast to increase to NZ$6.9 billion from NZ$6.38 billion.

Japan

The latest BoJ monetary policy decision to maintain its ultra-easy monetary policy on Friday coupled with Governor Ueda’s forecast for the country’s inflation trajectory – he expects pressures to slow down in the second half of the current fiscal year – has toned down market players’ expectation of an extension to the band of its yield curve control program at the next meeting.

Next up, the focus will be on the latest inflationary trends in Japan. May’s nationwide inflation data will be released on Friday. The core inflation rate (excluding fresh food) is expected to dip slightly to 3.1% year-on-year from 3.4% in April. In contrast, the core-core inflation rate (excluding fresh food & energy) is forecast to surge to 4.2% year-on-year from 4.1% in April.

Flash manufacturing and services PMIs will be released on Friday as well. Manufacturing activities are expected to be almost unchanged at 50 in June from 50.6 in May while the service sector is seen growing at a faster pace of 56.1, up from 55.9 in May.

Singapore

One key data point to focus on; inflation for May is expected to dip slightly to 5.5% year-on-year from 5.7% in April. The core inflation rate is also forecasted to ease to 4.9% year-on-year from 5% in April.

Economic Calendar

Saturday, June 17

Economic Events

- US Secretary of State Antony Blinken visits Beijing

- German Chancellor Scholz speaks at a ceremony commemorating the 1953 East Berlin uprising

Sunday, June 18

Economic Events

- EU foreign affairs chief Borrell meets Egyptian President Abdel-Fattah El-Sisi

Monday, June 19

Economic Data/Events

- US markets observe Juneteenth holiday

- Ukraine seeking to add Russia to money-laundering “black list” at meeting of Financial Action Task Force in Paris. Through June 23

- European Central Bank’s Francois Villeroy de Galhau speaks at conference in Paris

- Reserve Bank of Australia issues minutes of June’s policy meeting

- German President Frank-Walter hosts Chinese Premier Li Qiang in Berlin

- NATO Secretary General Stoltenberg and German Chancellor Scholz hold a news conference in Berlin

- EU energy ministers meet in Brussels

Tuesday, June 20

Economic Data/Events

- US housing starts

- China loan prime rates

- Hong Kong CPI

- Japan industrial production

- Mexico international reserves

- FedEx Corp reports earnings

- German Chancellor Scholz hosts Chinese Premier Li Qiang in Berlin

- Fed’s Bullard speak at Barcelona School of Economics Summer Forum

- Fed’s Williams speaks on leadership at Fed event

- RBA’s Kent participates in panel at ISDA/AFMA Derivatives Forum in Sydney

- RBA’s Michele Bullock at the AI Group in Newcastle

- RBA releases minutes of June policy meeting

- ECB’s Rehn speaks on outlook for Finnish economy

- ECB’s Gediminas Simkus speaks at the MNI event

Wednesday, June 21

Economic Data/Events

- Fed Chair Powell delivers semi-annual congressional testimony before the House Financial Services Committee

- Canada retail sales

- Eurozone new car registrations

- South Africa CPI

- UK CPI

- Indian PM Modi begins state visit to US. Will attend state dinner and address Congress during visit

- Fed’s Goolsbee speaks at Wall Street Journal Global Food Forum in Chicago

- Bank of Canada issues summary of June policy meeting

- Bank of Japan issues minutes of April policy meeting

Thursday, June 22

Economic Data/Events

- Fed Chair Powell delivers semi-annual testimony to Congress before the Senate Banking Committee

- US Conference Board leading index, initial jobless claims, current account, existing home sales

- Eurozone consumer confidence

- Mexico rate decision

- New Zealand trade

- Norway rate decision

- Switzerland rate decision

- UK BOE rate decision

- Fed’s Mester speaks at the bank’s annual policy summit

- Central Bank of Turkey rate decision (first meeting for Gov Hafize Gaye Erkan, Turkey’s first female central bank governor)

- French President Macron, German Chancellor Scholz, and Chinese Premier Li Qiang attend Summit for a New Global Financial Pact in Paris

- EU European affairs ministers meet in Stockholm

Friday, June 23

Economic Data/Events

- US June Prelim Manufacturing PMI, Services PMI

- European Flash PMIs: Eurozone, Germany, France, and the UK

- Japan CPI

- Singapore CPI

- Spain GDP

- Fed’s Bullard speaks at the Central Bank of Ireland and International Journal of Central Banking Research Conference

- ECB’s Vujcic delivers keynote lecture at 7th Annual Research Conference organized by central banks of Ukraine and Poland in Krakow

- ECB’s Cos speaks at an event for financial journalists in Santander, Spain

Sovereign Rating Updates

- Hungary (Fitch)

- Poland (Fitch)

- Ukraine (Fitch)

- Poland (S&P)

Weekly Economic & Financial Commentary: Fed Not on Summer Break Quite Yet

Summary

United States: Fed Not on Summer Break Quite Yet

- This was a busy week for markets and monetary policymakers alike, as a healthy slate of economic data was accompanied by an FOMC meeting. On balance, the data were consistent with slowing inflation and output growth, but at a gradual rather than sudden pace.

- Next week: Housing Starts (Tue), Existing Home Sales (Thu), Leading Economic Index (Thu)

International: China's Post-COVID Rebound Is Over, European Central Bank Remains Hawkish

- While the Chinese economy outperformed in Q1 after Zero-COVID measures were lifted, momentum from the first quarter has not been able to sustain itself and growth prospects are fading quickly. Elsewhere, European Central Bank policymakers lifted interest rates another 25 bps to the highest rate since the early 2000s. The message from ECB President Lagarde was quite clear. Inflation is still uncomfortably high, and more work needs to be done to bring it back to target.

- Next week: U.K. CPI (Wed), Brazilian Central Bank (Wed), Central Bank of Turkey (Thu)

Interest Rate Watch: FOMC Skips June, but Signals Hikes Not Done Yet

- As widely expected, the Federal Open Market Committee (FOMC) refrained from hiking rates at its policy meeting this week, which is the first time in 11 meetings that the committee left the fed funds rate unchanged. However, the decision to keep the fed funds rate unchanged was accompanied by signs that the FOMC is not done tightening policy yet.

Topic of the Week: Interstate-95 Collapse Brings Another Headache for Recovering Supply Chains

- On the morning of Monday, June 11, a vehicle fire broke out below an Interstate-95 overpass in Philadelphia. The blaze resulted in a partial collapse of a section of the East Coast’s primary north-south highway. While construction is under way to repair the damaged section, the disruption could lead to higher transportation costs in the region.