Sample Category Title

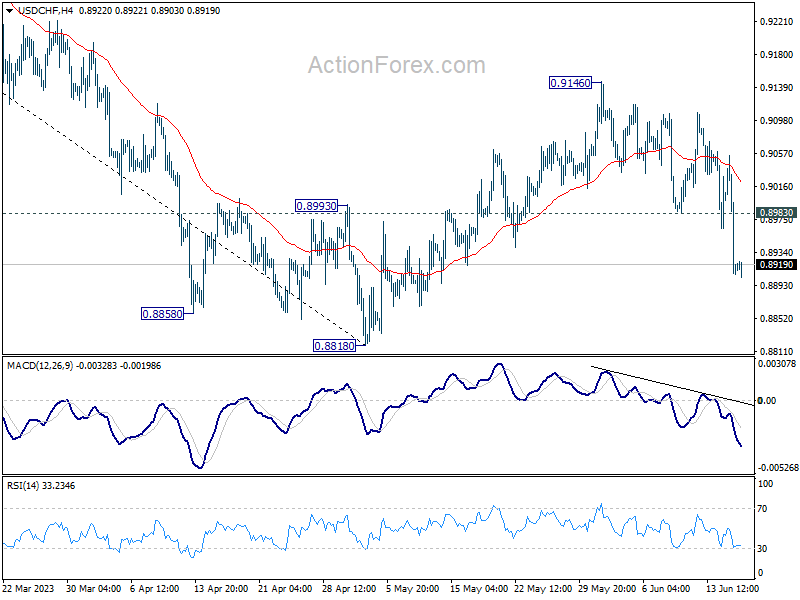

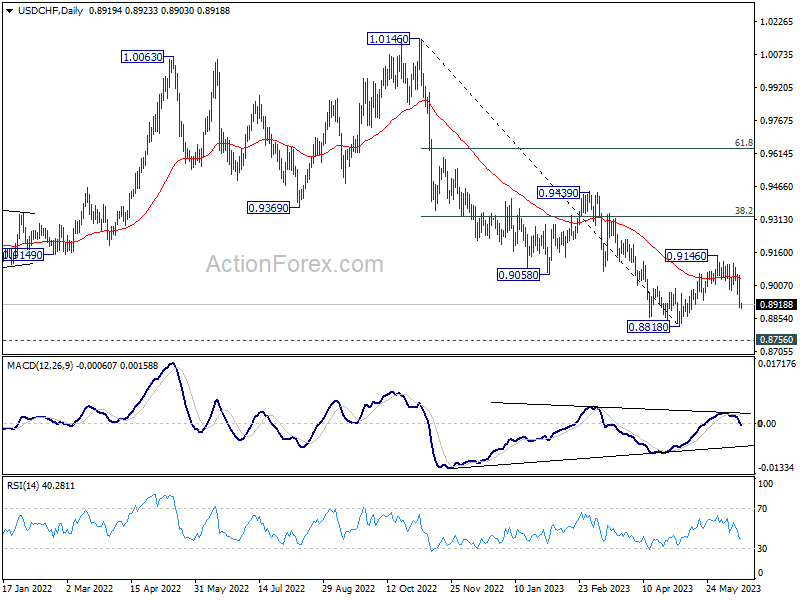

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8864; (P) 0.8960; (R1) 0.9013; More...

Intraday bias in USD/CHF remains on the downside for the moment. Fall from 0.9146 would extend to 0.8818 support and possibly below. Still, strong support is still expected from 0.8756 to bring reversal. On the upside, above 0.8983 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

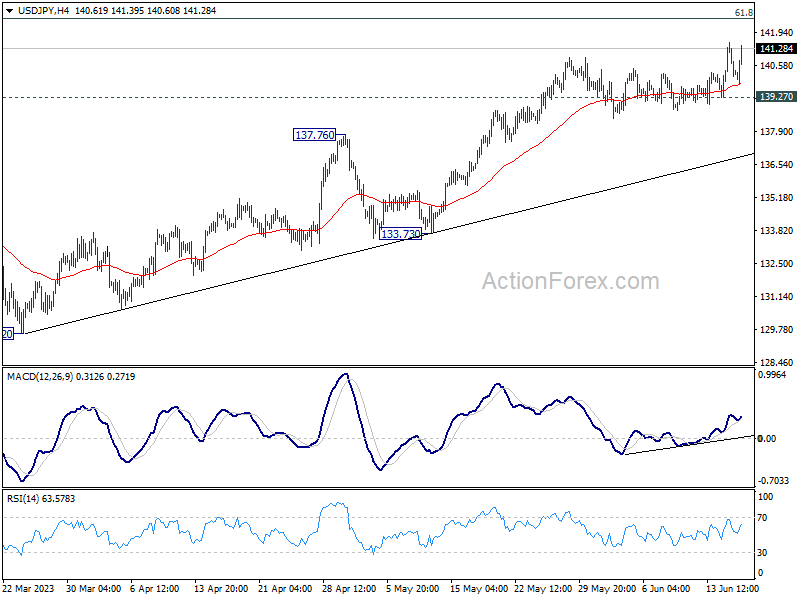

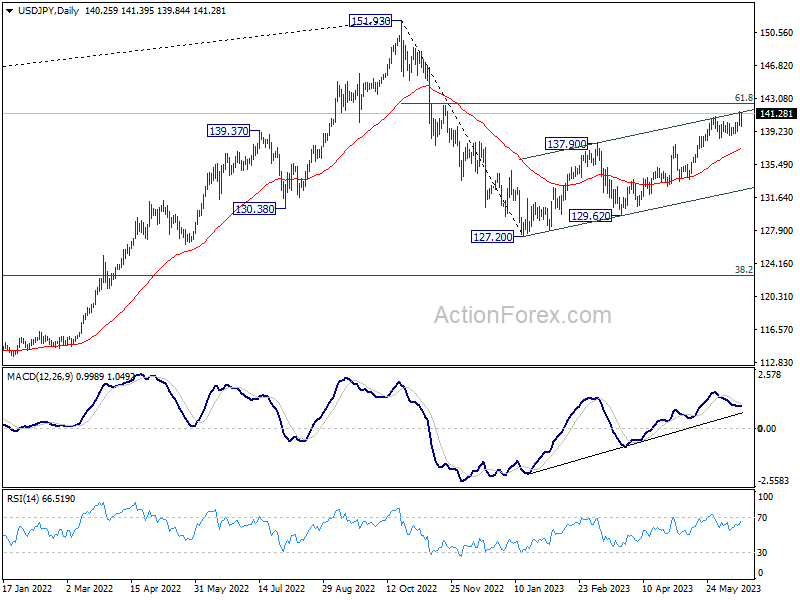

USD/JPY Daily Outlook

Daily Pivots: (S1) 139.65; (P) 140.57; (R1) 141.21; More...

No change in USD/JPY's outlook and further rise expected with 139.27 support intact. Current rise from 127.20 should now target 142.48 fibonacci level next. Nevertheless, break of 139.27 will now indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 142.48. Sustained break there will pave the way back to retest 151.93. On the downside, however, decisive break of 137.90 resistance turned support will now be the first indicate that this rebound from 127.20 has completed already.

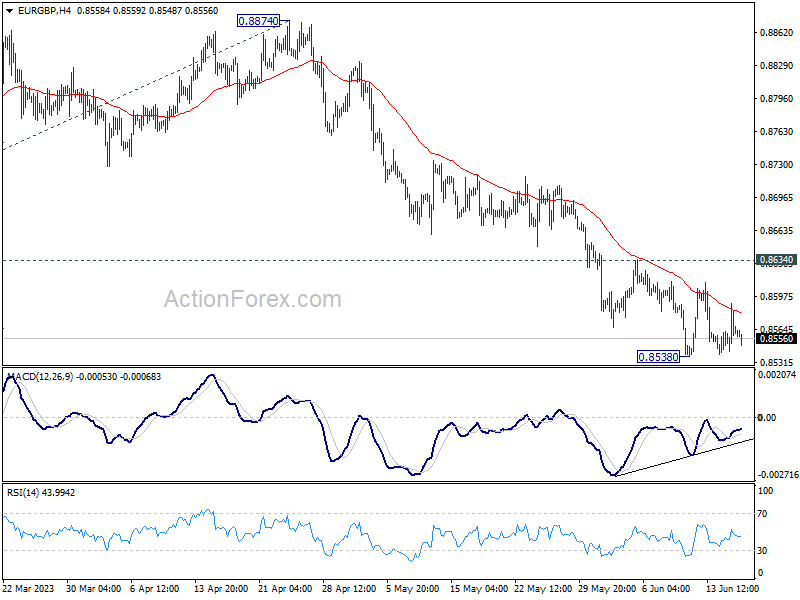

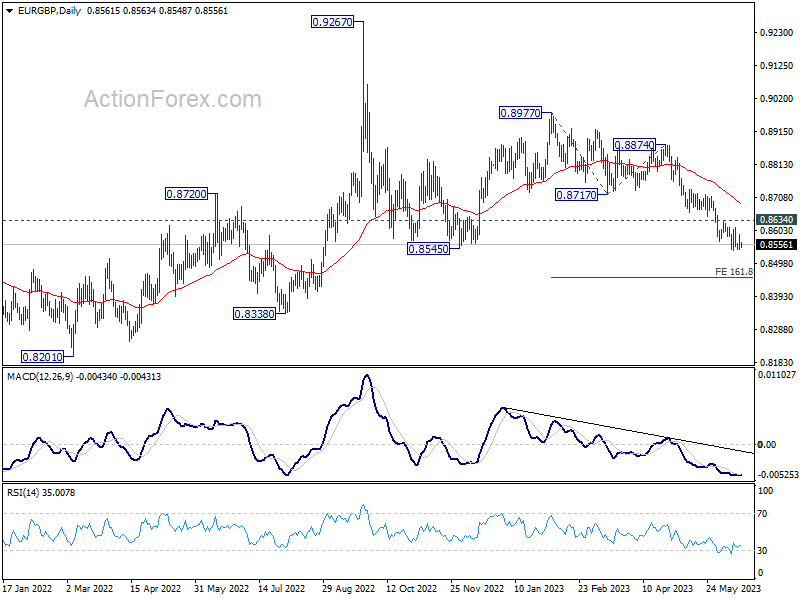

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8540; (P) 0.8566; (R1) 0.8588; More...

Intraday bias in EUR/GBP remains neutral and outlook stays bearish with 0.8634 resistance intact. Break of 0.8538 will resume larger decline from 0.8977 to 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. However, considering bullish convergence condition in 4H MACD, firm break of 0.8634 will indicate short term bottoming and turn bias to the upside for stronger rebound.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

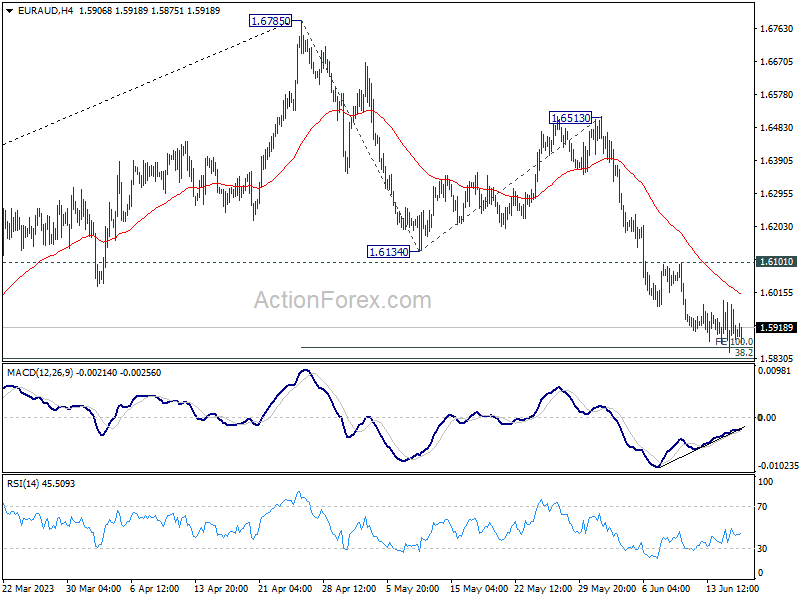

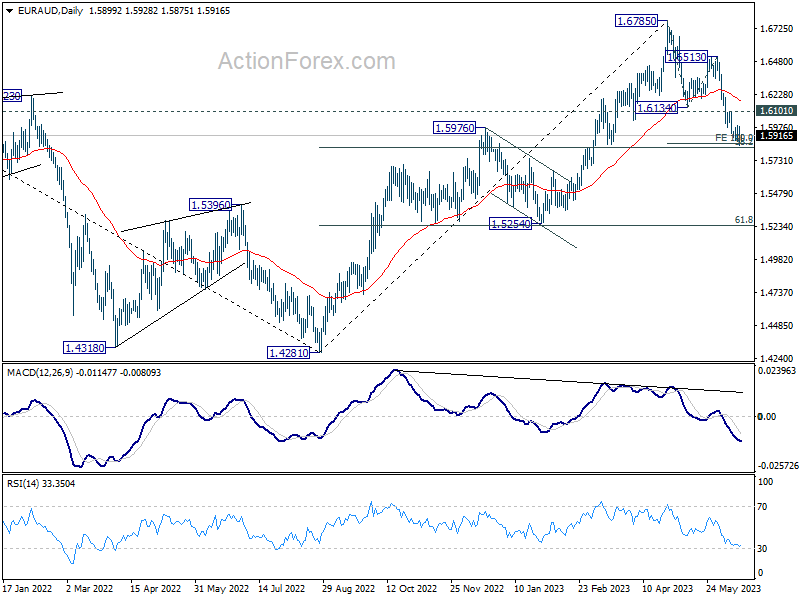

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5838; (P) 1.5914; (R1) 1.5980; More...

Intraday bias in EUR/AUD remains neutral for the moment. Strong support is still expected from around 100% projection of 1.6785 to 1.6134 from 1.6513 at 1.5862 to complete the fall from 1.6785. On the upside, break of 1.6101 resistance will confirm short term bottoming, and turn bias back to the upside for rebound.

In the bigger picture, a medium term is possibly in place at 1.6785 already, on bearish divergence condition in D MACD. Fall from there is seen as corrective whole up trend from 1.4281 (2022 low). Deeper decline is expected as long as 1.6513 resistance holds, to 38.2% retracement of 1.4281 to 1.6785 at 1.5828. Strong support could be seen there to complete the first leg of the corrective pattern.

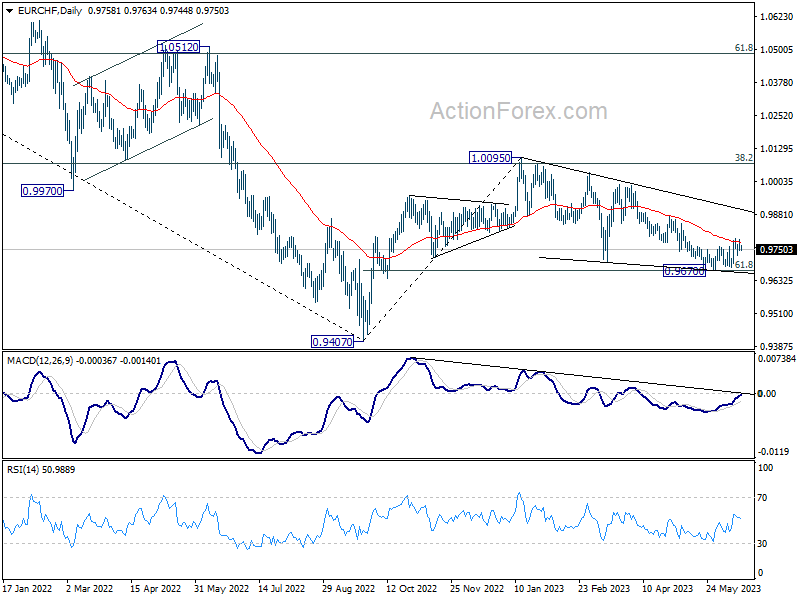

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9744; (P) 0.9767; (R1) 0.9784; More...

Intraday bias in EUR/CHF is turned neutral as it continued to lose upside momentum as seen in 4 H MACD. Risk stays on the upside as long a s0.9670 support holds. Sustained trading above 55 D EMA (now at 0.9778) will add to case that whole correction from 1.0095 has completed, after hitting 61.8% retracement of 0.9407 to 1.0095 at 0.9670. Further rise should then be seen to 0.9878 resistance next.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9929). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

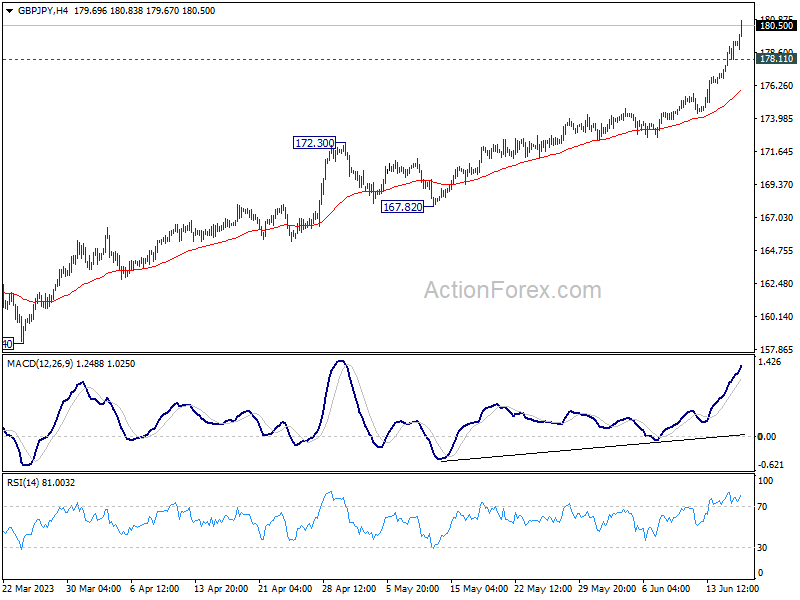

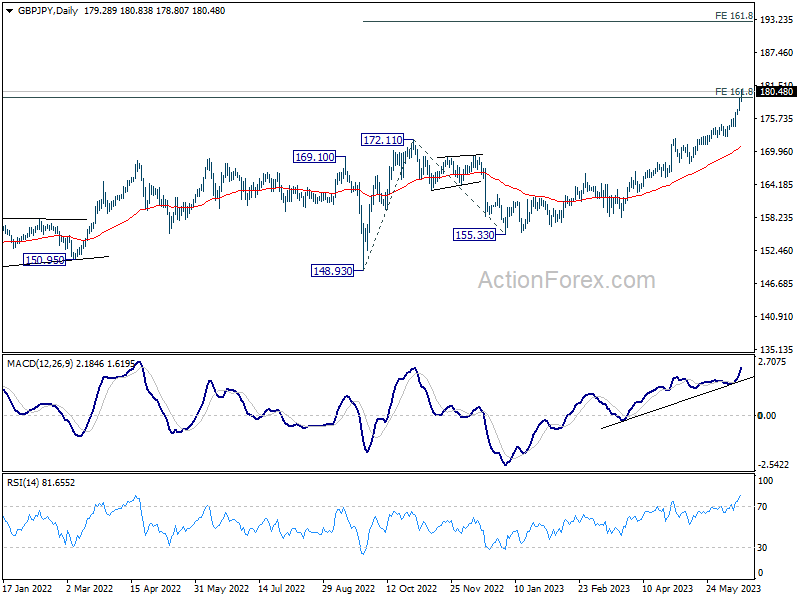

GBP/JPY Daily Outlook

Daily Pivots: (S1) 177.93; (P) 178.66; (R1) 180.08; More...

GBP/JPY surges to as high as 180.83 so far today as current rally accelerates. Intraday bias stays on the upside at this point. Next target is 161.8% projection of 148.93 to 172.11 from 155.33 at 192.83. On the downside, below 178.11 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) is extending. 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69 is already taken out. Sustained trading above there there will pave the way to 195.86 long term resistance (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

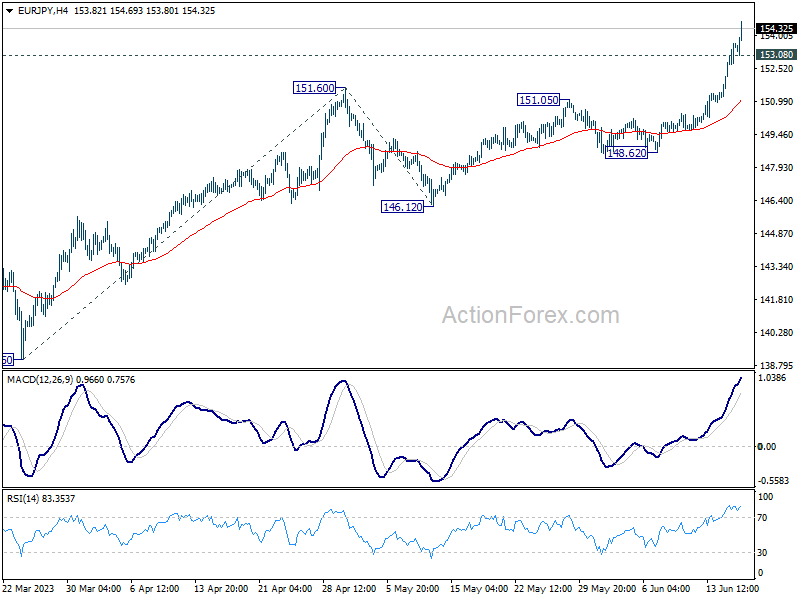

EUR/JPY Daily Outlook

Daily Pivots: (S1) 152.22; (P) 152.95; (R1) 154.29; More....

EUR/JPY accelerates to as high as 154.63 so far today. There is no sign of topping after breaking 153.63 medium term projection level. Intraday bias stays on the upside for 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64 is already met but there in no sign of topping. Further rally should be seen to 100% projection at 162.82 next. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

Yen Accelerates Down Again after BoJ, Dollar Staying Weak Too

In the wake of BoJ's decision to hold its monetary policy steady, we have seen an amplified sell-off in Yen, which is not surprising given the ongoing divergence in monetary policy with other major global central banks. The breaking of key levels in some crosses suggests that we might witness further declines in Yen, at least until Japanese authorities intervene once again.

Dollar, closely tailing Yen, is also displaying weakness and is ranked as the second poorest performer of the week. Nevertheless, it's yet to be ascertained if the greenback's trajectory is now inversely linked with risk sentiment, reverting to its norm.

On the other end of the spectrum, Australian Dollar is currently the week's top performer, but Euro is also trying to close the gap. The common currency has been buoyed by yesterday's rate hike by ECB and its hawkish economic projections. British Pound is holding up as the third strongest currency, as markets anticipate tightening by BoE next week. Meanwhile, Swiss Franc and New Zealand Dollar are showing a mixed performance, while Canadian Dollar is slightly on the softer side.

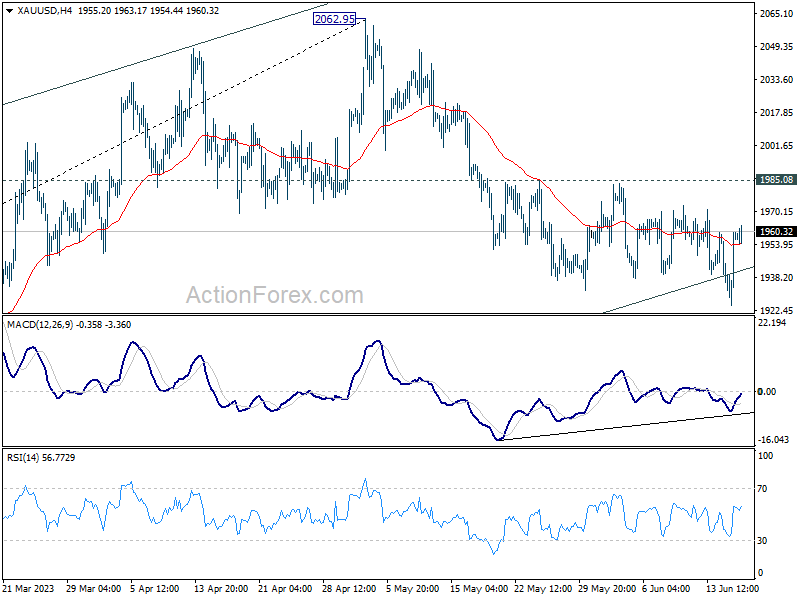

Technically, Gold recovered after just brief to 1924.61, back above medium term channel support. Bullish convergence is seen in 4H MACD. Break of 1985.08 resistance will argue that corrective fall from 2062.95 has completed. In this case, stronger rebound would be seen back to retest 2062.95 high. If realized, this could be a confirmation signal more deeper decline in Dollar elsewhere.

In Asia, Nikkei closed up 0.66%. Hong Kong HSI is up 1.00%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.57%. Japan 10-year JGB yield dropped -0.0187 to 0.413. Overnight, DOW rose 1.26%. S&P 500 rose 1.22%. NASDAQ rose 1.15%. 10-year yield dropped -0.068 to 3.728.

BoJ holds steady, core CPI to decelerate towards middle of fiscal 2023

In a widely expected move, BoJ today unanimously voted to maintain its existing ultra-loose monetary policy. The central bank kept short-term policy rate at -0.10% under its yield curve control. Yield target on 10-year JGB remains around 0%, with fluctuation band allowed also maintained at about plus and minus 0.50% from the target level. BoJ reiterated its commitment to carry on with its Quantitative and Qualitative Monetary Easing with Yield Curve Control "as long as it is necessary" and affirmed it "will not hesitate to take additional easing measures if necessary."

In its accompanying statement, BoJ noted that it anticipates Japan's economy to witness moderate recovery by around middle of the fiscal year 2023. "Thereafter, as a virtuous cycle from income to spending gradually intensifies, Japan's economy is projected to continue growing at a pace about its potential growth rate," the central bank said.

Discussing the inflation outlook, the bank stated: "The year-on-year rate of increase in the CPI (all items less fresh food) is likely to decelerate toward the middle of fiscal 2023, with a waning of the effects of the pass-through to consumer prices of cost increases led by the rise in import prices.

"Thereafter, the rate of increase is projected to accelerate again moderately, albeit with fluctuations, as the output gap improves and as medium- to long-term inflation expectations and wage growth rise, accompanied by changes in factors such as firms' price- and wage-setting behavior."

NZ BNZ PMI ticked up to 48.9, staying in relatively tight band of contraction

New Zealand BusinessNZ Performance of Manufacturing Index ticked up from 48.8 to 48.9 in May, staying well below long-term average activity rate of 53.0. Looking at some details, production dropped from 47.0 to 45.7. Employment rose from 47.7 to 49.5. New orders rose from 49.6 to 50.8. Finished stocks dropped from 52.5 to 51.5. Deliveries dropped from 50.7 to 46.0.

BusinessNZ's Director, Advocacy Catherine Beard said: "New Zealand's manufacturing sector has remained in a relatively tight band of contraction for the last three months. While the overall activity result has crept upwards over that time."

BNZ Senior Economist, Craig Ebert stated that "the range of results in the sub-components is mirrored in the breadth of issues manufacturers are now highlighting in the survey. Gone is the dominance of supply-side laments, especially regarding staff. But new negatives have arisen, for all of them to (still be) outnumbering the positive issues referenced".

Looking ahead

Eurozone CPI final and US U of Michigan consumer sentiment are the main features for the rest of the day.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 152.22; (P) 152.95; (R1) 154.29; More....

EUR/JPY accelerates to as high as 154.63 so far today. There is no sign of topping after breaking 153.63 medium term projection level. Intraday bias stays on the upside for 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64 is already met but there in no sign of topping. Further rally should be seen to 100% projection at 162.82 next. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 48.9 | 49.1 | ||

| 02:47 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 08:30 | GBP | Consumer Inflation Expectations | 3.90% | |||

| 09:00 | EUR | Eurozone CPI Y/Y May F | 6.10% | 6.10% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 5.30% | 5.30% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.00% | -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 60.2 | 59.2 |

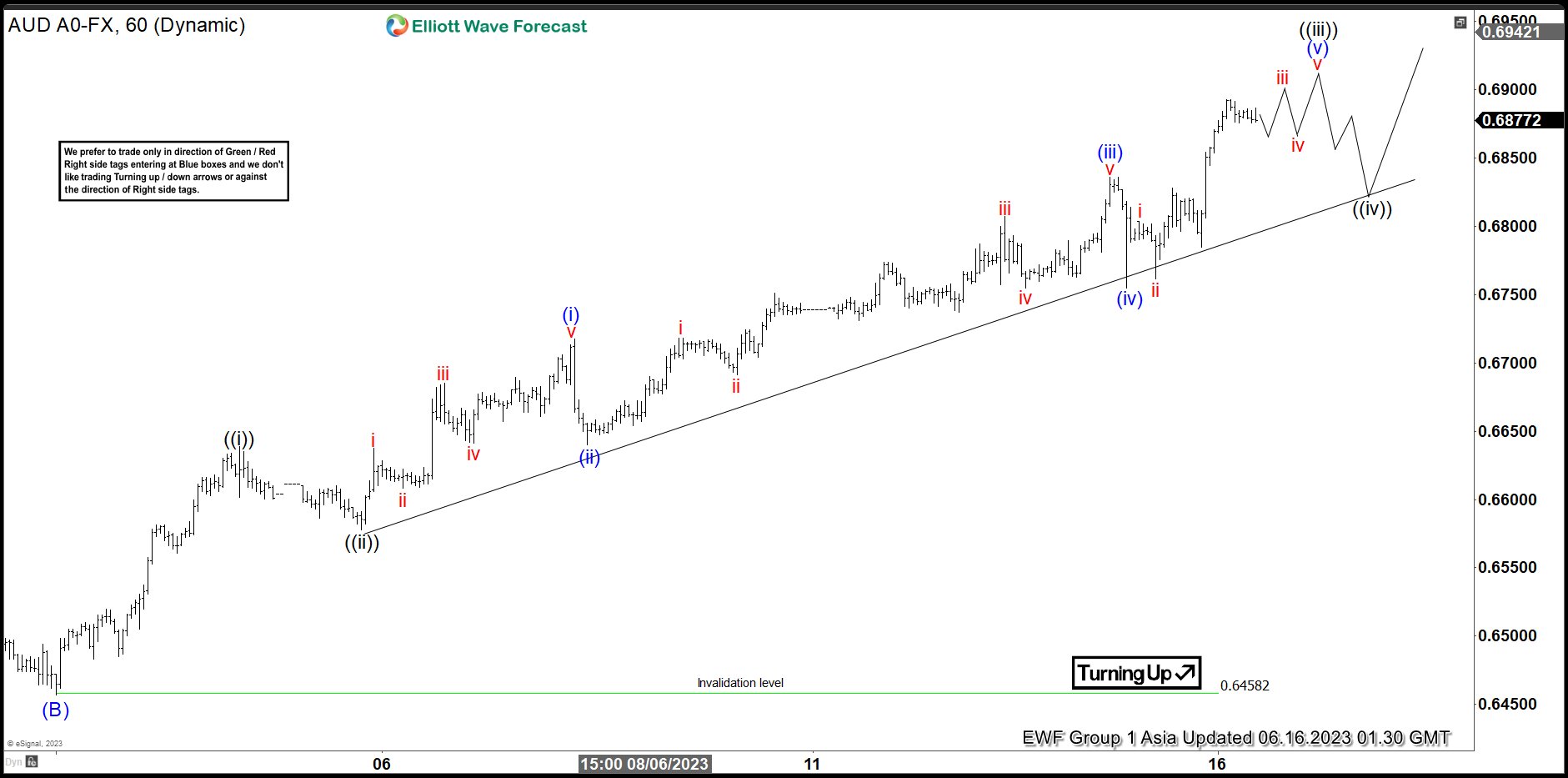

AUDUSD Starts New Elliott Wave Impulse Higher

Short Term Elliott Wave View in AUDUSD suggests the pair ended wave (B) at 0.6458. Pair has turned higher in wave (C) with subdivision as a 5 waves impulse Elliott Wave structure. Up from wave (B), wave ((i)) ended at 0.6638 and pullback in wave ((ii)) ended at 0.6578. Pair resumes higher in wave ((3)) and nesting in lesser impulsive structure. Up from wave ((ii)), wave (i) ended at 0.6717 and dips in wave (ii) ended at 0.664.

Pair resumes higher in wave (iii) towards 0.6835 and pullback in wave (iv) ended at 0.6755. Expect wave (v) to end soon which should complete wave ((iii)). Afterwards, pair should pullback in wave ((iv)) to correct cycle from 6.5.2023 low in 3, 7, or 11 swing before it resumes higher in wave ((v)). This should complete wave 1 of (C) in higher degree. Pair should then pullback again in larger degree wave 2 to correct the cycle from 6.1.2023 low before it resumes higher. Near term, as far as pivot at 0.6458 low stays intact, expect short term pullback to find support in 3, 7, or 11 swing and pair should continue to extend higher.

AUDUSD 1 Hour Elliott Wave Chart

AUDUSD Elliott Wave Video

https://www.youtube.com/watch?v=z1P8c-1GL5M

Welcome to a Bipolar World of Monetary Policies

- Monetary policies and guidance of the 4 major central banks are moving in the opposite direction.

- US Fed and Eurozone ECB are in the hawkish camp while Japan BoJ and China PBoC are still in accommodating mode.

- K-shaped performance in USD against key G-20 currencies; JPY remained weak and CNH sideways, in contrast, the rest has strengthened against the USD.

- G-10 JPY crosses are bursting up.

We have concluded three plus one monetary policy decisions outcome from four major G-20 central banks for this week; the US Federal Reserve (Fed), European Central Bank (ECB), Bank of Japan (BoJ), and People’s Bank of China (PBoC).

The latest monetary policies guidance from the Fed and ECB has been more skewed toward the hawkish side; despite the FOMC’s decision to skip a hike on the Fed funds rate this time round, the dot-plot projection has suggested two 25 basis points hike before 2023 ends to bring the terminal Fed funds rate of this current hiking cycle to a median level of 5.6%.

Over at the ECB, President Lagarde has hinted during the press conference that ECB is likely to hike by another 25 basis points (bps) in July after it raised its key policy deposit rate by 25 bps yesterday, 15 June to bring it to 3.5%, the highest level in more than 20 years. Expectations from money markets indicate that ECB may not be done hiking after July as traders’ positioning has implied an 80% probability of the ECB raising the deposit rate to 4% by October, an increase from 50% odds earlier.

In Asia, PBoC cut its one-year medium-term lending facility (MLF) interest rate yesterday which lends out funds to major China commercial banks by 10 bps to 2.65%, its first cut since August 2022. Hence, the expectations have now increased for more easing policies from PBoC to address the current slew of weak domestic/internal consumption data from China, a shift from its prior cautious targeted accommodating monetary policy stance.

Today, BoJ has maintained its ultra-easy monetary policy in place since the Great Financial Crisis of 2009, with no change in the band for the yield curve control program of the 10-year Japanese Government Bond at 0.50% on either side and short-term key policy interest rate stayed at -0.1%.

BoJ’s monetary policy statement cited Japan’s economy is picking up and likely to continue recovering moderately. But stated that the pace of core inflation is likely to slow down towards the middle of the current fiscal year with inflationary expectations moving sideways after an earlier increase. Therefore, this latest statement has suggested that BoJ is not in a “rush mode” to normalize its ultra-easy monetary policy due to an expected slowdown in inflationary pressures.

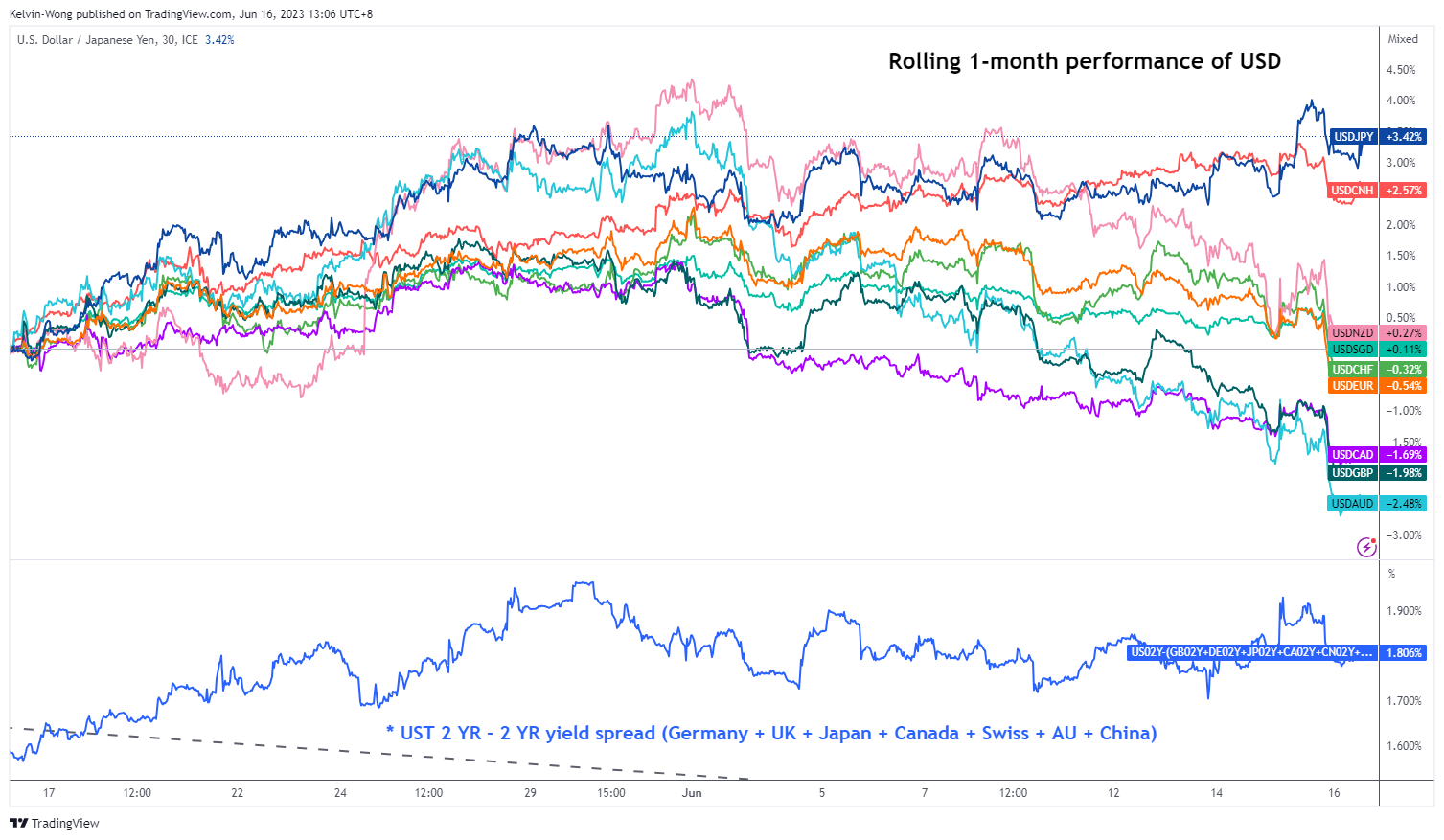

Impact on the FX market, USD outperformance against JPY but weaken significantly against the rest

Fig 1: USD against key G-20 currencies (including NZD) rolling 1-month performances as of 16 Jun 2023

(Source: TradingView, click to enlarge chart)

The rolling 1-month performances of the USD against the key G-20 currencies (inclusive of NZD) as of 16 June 2023 has shown a stark contrast driven by the current easy momentary policies mode of BoJ and PBoC. A “K-shaped” performance where the USD has strengthened against the JPY, sideways with CNH (offshore yuan) but weakened significantly against CAD, GBP, and AUD at this time of the writing.

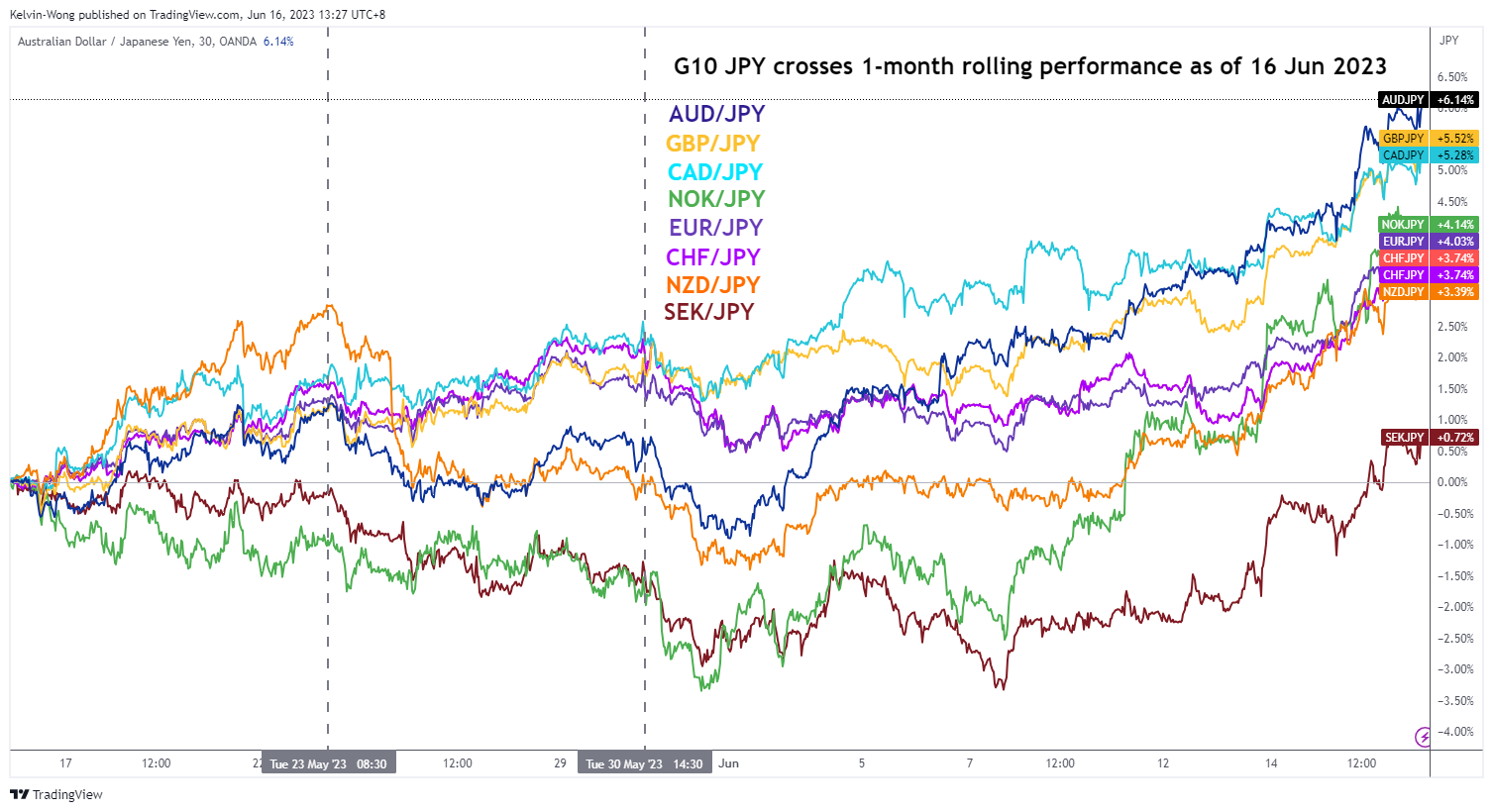

JPY crosses are now bursting upwards

Fig 2: G-10 JPY crosses rolling 1-month performances as of 16 Jun 2023 (Source: TradingView, click to enlarge chart)

The weakness seen in the JPY against the USD has led to the continuation of the JPY carry trade medium-term uptrend phase where the GBP/JPY and AUD/JPY are now trading close to a 9 and 10-month high respectively.

US Dollar Index is looking weak again for a retest on its 100.95 key near-term support

Fig 3: US Dollar Index medium-term trend as of 13 Jun 2023 (Source: TradingView, click to enlarge chart)

The US Dollar Index (a weighted average of 6 currencies, EUR, JPY, GBP, CAD, SEK & CHF where the EUR has the highest weightage of around 57%) has just broken below its 50-day moving average after it traded above it since 12 May 2023. Medium-term momentum has turned bearish as the daily RSI oscillator has reintegrated below its former corresponding support at the 50% level.

A break below the 100.95 key near-term support which the US Dollar Index has managed to hold on the previous five occasions since 2 February 2023 may resume its major downtrend movement with the next support coming in at 97.85 in the first step.