Sample Category Title

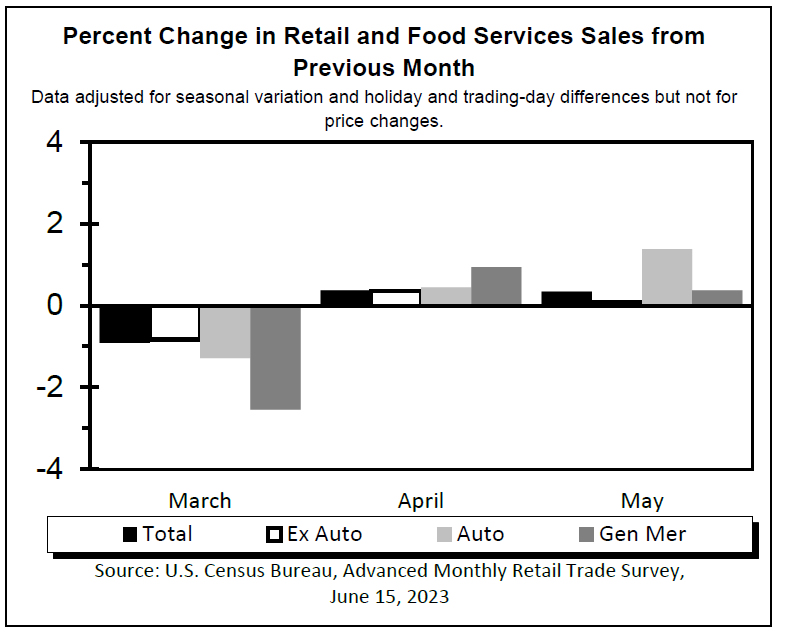

US retail sales rose 0.3% mom in May, ex-auto sales up 0.1% mom

US retail sales rose 0.3% mom to USD 686.6B in May, above expectation of 0.0% mom. Ex-auto sales rose 0.1% mom to USD 554.5B, matched expectations. Ex-gasoline sales rose 0.6% mom to USD 633.5B. Ex-auto and gasoline sales rose 0.4% mom to USD 501.5B

In the three months to may, sales were up 1.7% from the same period a year ago.

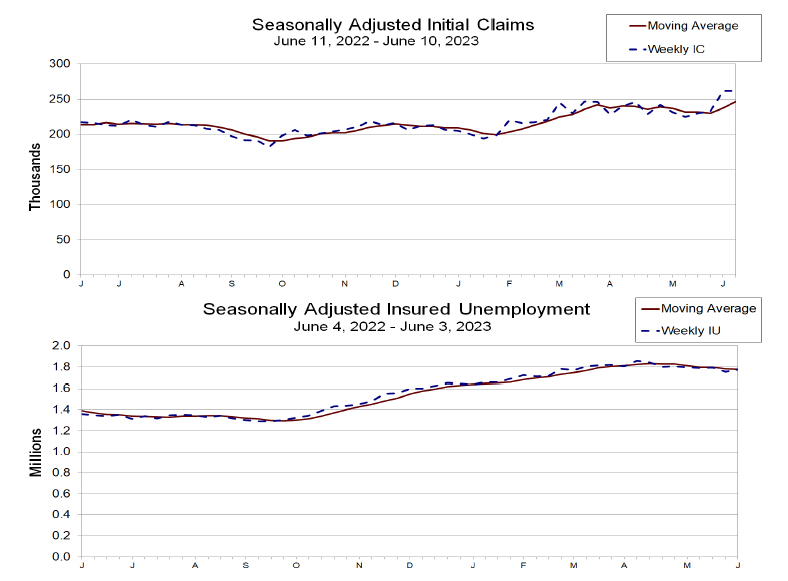

US initial jobless claims unchanged at 262k

US initial jobless claims was unchanged at 262k in the week ending June 10, well above expectation of 246k. Four-week moving average of initial claims rose 9k to 247k, highest since November 20, 2021 when it was 249k.

Continuing claims rose 20k to 1775k in the week ending June 3. Four-week moving average of continuing claims dropped -6k to 1778k.

(ECB) Monetary policy decisions

Inflation has been coming down but is projected to remain too high for too long. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It therefore today decided to raise the three key ECB interest rates by 25 basis points.

The rate increase today reflects the Governing Council's updated assessment of the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission. According to the June macroeconomic projections, Eurosystem staff expect headline inflation to average 5.4% in 2023, 3.0% in 2024 and 2.2% in 2025. Indicators of underlying price pressures remain strong, although some show tentative signs of softening. Staff have revised up their projections for inflation excluding energy and food, especially for this year and next year, owing to past upward surprises and the implications of the robust labour market for the speed of disinflation. They now see it reaching 5.1% in 2023, before it declines to 3.0% in 2024 and 2.3% in 2025. Staff have slightly lowered their economic growth projections for this year and next year. They now expect the economy to grow by 0.9% in 2023, 1.5% in 2024 and 1.6% in 2025.

At the same time, the Governing Council's past rate increases are being transmitted forcefully to financing conditions and are gradually having an impact across the economy. Borrowing costs have increased steeply and growth in loans is slowing. Tighter financing conditions are a key reason why inflation is projected to decline further towards target, as they are expected to increasingly dampen demand.

The Governing Council's future decisions will ensure that the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and will be kept at those levels for as long as necessary. The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will continue to be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.

The Governing Council confirms that it will discontinue the reinvestments under the asset purchase programme as of July 2023.

Key ECB interest rates

The Governing Council decided to raise the three key ECB interest rates by 25 basis points. Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be increased to 4.00%, 4.25% and 3.50% respectively, with effect from 21 June 2023.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem does not reinvest all of the principal payments from maturing securities. The decline will amount to €15 billion per month on average until the end of June 2023. The Governing Council will discontinue the reinvestments under the APP as of July 2023.

As concerns the PEPP, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

ECB hikes 25bps, core inflation forecast raised sharply higher

ECB raises its key interest rates by 25bps as widely expected. The main refinancing rate, marginal lending facility rate, and deposit rates will be 4.00%, 4.25% and 3.50% after the hike.

In the accompanying statement, it's reiterated that the Governing Council will continued to follow a "data-dependent approach" in future decisions, to bring rates to levels "sufficiently restrictive" to achieve timely return of inflation to 2% target. Rates will also be kept at that level "for as long as necessary".

In the updated economic projections, core inflation projection is revised up notably in 2023 and 2024, and slightly in 2025. Growth projection was revised down slightly in both 2023 and 2024.

- Inflation is projected to average 5.4% in 2023, 3.0% in 2024 and 2.2% in 2025. (March: 5.3% in 2023, 2.9% in 2024 and 2.1% in 2025).

- Core inflation is projected to reach 5.1% in 2023, before it declines to 3.0% in 2024 and 2.3% in 2025. (March: 4.6% in 2023, 2.5% in 2024 and 2.2% in 2025).

- Growth is projected to be at 0.9% in 2023, 1.5% in 2024 and 1.6% in 2025. (March: 1.0% in 2023, 1.6% in 2024, 1.6% in 2025).

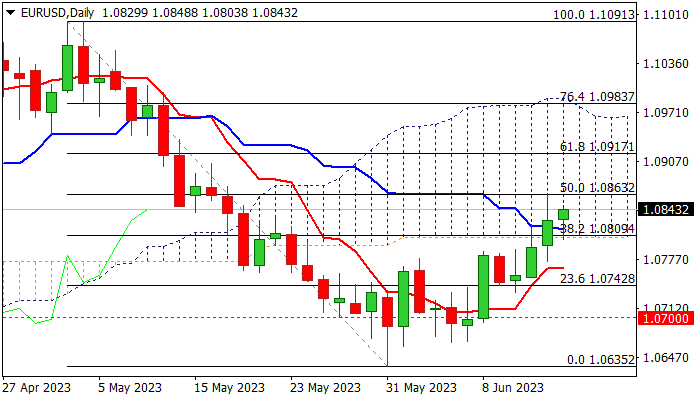

EUR/USD: Bulls Hold Grip Ahead of ECB Rate Decision

The Euro kept firm tone on Thursday despite strong upside rejection at 1.0863 (Fibo 50% of 1.1091/1.0635) on Wednesday, as dips were contained by former strong resistance at 1.0805 (daily cloud base) now reverted to solid support.

Hawkish Fed lifted dollar but so far did not manage to derail Euro’s bulls, although the action slowed and currently holding between two key levels, ahead of ECB rate decision.

The European Central Bank is widely expected to raise deposit rate by 25 basis points to 3.5% (the highest since 2001) today and likely to deliver another 0.25% raise in July, as inflation in the bloc remains unacceptably high (more than three times ECB’s 2% target) and underlying price growth is showing initial signs of easing, suggesting that the central bank would remain on tightening path for some time.

Markets will be focusing on ECB forward guidance which indicates central bank’s near future steps, with main question whether the ECB will pause after July’s hike or will continue with policy tightening, with prevailing expectations for more balanced message which will signal that further actions will be data dependent.

Daily studies remain positive with bullish bias expected above daily cloud base, though firm break of 1.0863 pivot required to signal bullish continuation.

Caution on return and close below daily cloud which would generate initial signal of recovery stall.

Res: 1.0863; 1.0904; 1.0917; 1.0980.

Sup: 1.0805; 1.0765; 1.0742; 1.0733.

BTCUSD Analysis: Bears Attack the Psychological Level

Last night, the price of bitcoin fell below USD 25k for the first time since mid-March. And the bitcoin chart this morning shows sellers breaking through yesterday's low.

There can be two fundamental reasons for the dominance of sellers:

→ yesterday's press conference of the head of the US Federal Reserve (more details in the next post);

→ claims against the Binance and Coinbase exchanges by the US SEC regulator, which declared about 60 crypto assets as securities.

We wrote on June 13 that after the bearish breakout of the ascending channel (1) and the test of this breakout (2), the price of bitcoin could break through the USD 25k support level from top to bottom.

Could the now-forming USD 25k bearish breakout be false?

There are 3 arguments in favor of this idea:

→ previously this level served as resistance – from the point of view of technical analysis, now it should support the market;

→ the price of bitcoin may receive support from the lower border of the channel shown in red;

→ for the price of bitcoin, punctures of psychological levels are quite typical (for example, punctures from bottom to top of USD 25k in the second half of February).

More confidence from the US authorities on this list could add confidence to the bulls, but so far the situation leaves much to be desired.

Market Reaction to Fed’s Decision

Yesterday the Fed (as expected) kept the interest rate unchanged (after a series of 10 increases). However, the opinion of market participants that the rate peak has been reached has been called into question. At the Jerome Powell's press conference, it became known that:

→ the majority of FOMC members are against the rate cut;

→ there may be another increase at the end of the year;

→ high inflation situation may last 2 years.

The markets reacted with a rise in the US dollar. Accordingly, the currencies fell in pairs with the US dollar. Gold also fell in price to a minimum in 3 months — like bitcoin, by the way, and this is not the only similarity in the behavior of the price of gold and the main cryptocurrency.

Note that on the XAU/USD chart, a picture is emerging that a few days ago was formed on the bitcoin price chart (see the previous post).

The price of gold has broken through the ascending channel (shown in blue), formed a breakout test and is moving within the descending channel (shown in red). If we see a continuation of the dynamics shown by bitcoin in the gold market, then XAU/USD may drop to the lower border of the descending channel.

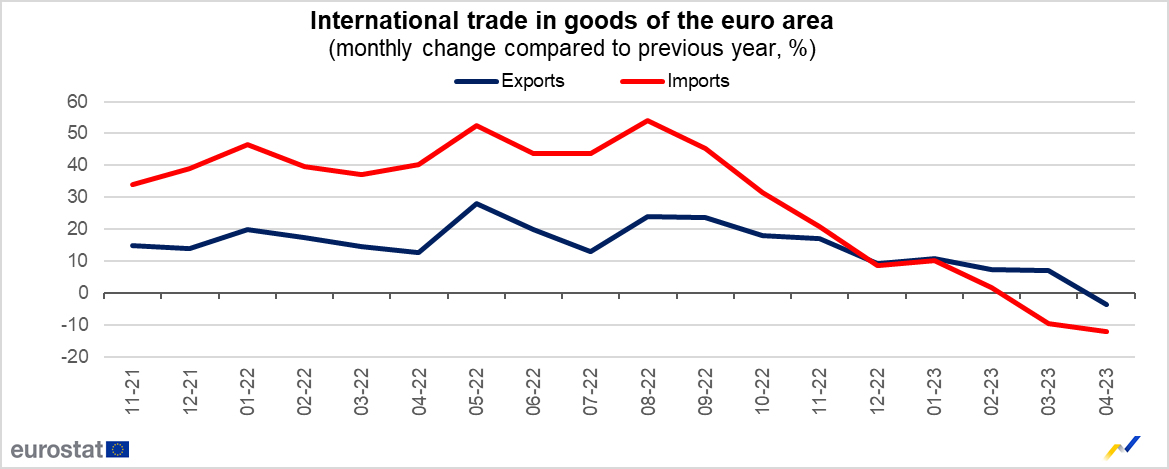

Eurozone exports down -3.6% yoy in Apr, imports down -11.9% yoy

Eurozone exports of goods to the rest of the world decreased -3.6% yoy in April to EUR 216.0B. Imports decreased -11.9% yoy to EUR 227.7B. A EUR -11.7B trade deficit was recorded. Intra-Eurozone trade was also down by -5.2% yoy to EUR 208.3B.

In seasonally adjusted term, exports fell -3.2% mom to EUR 234.5B. Imports rose 5.9% mom to EUR 241.5B. Trade balance turned into EUR -7.1B deficit, versus expectation of EUR 5.7B surplus. Intra-Eurozone trade fell from EUR 224.1B in March to 222.4B in April.

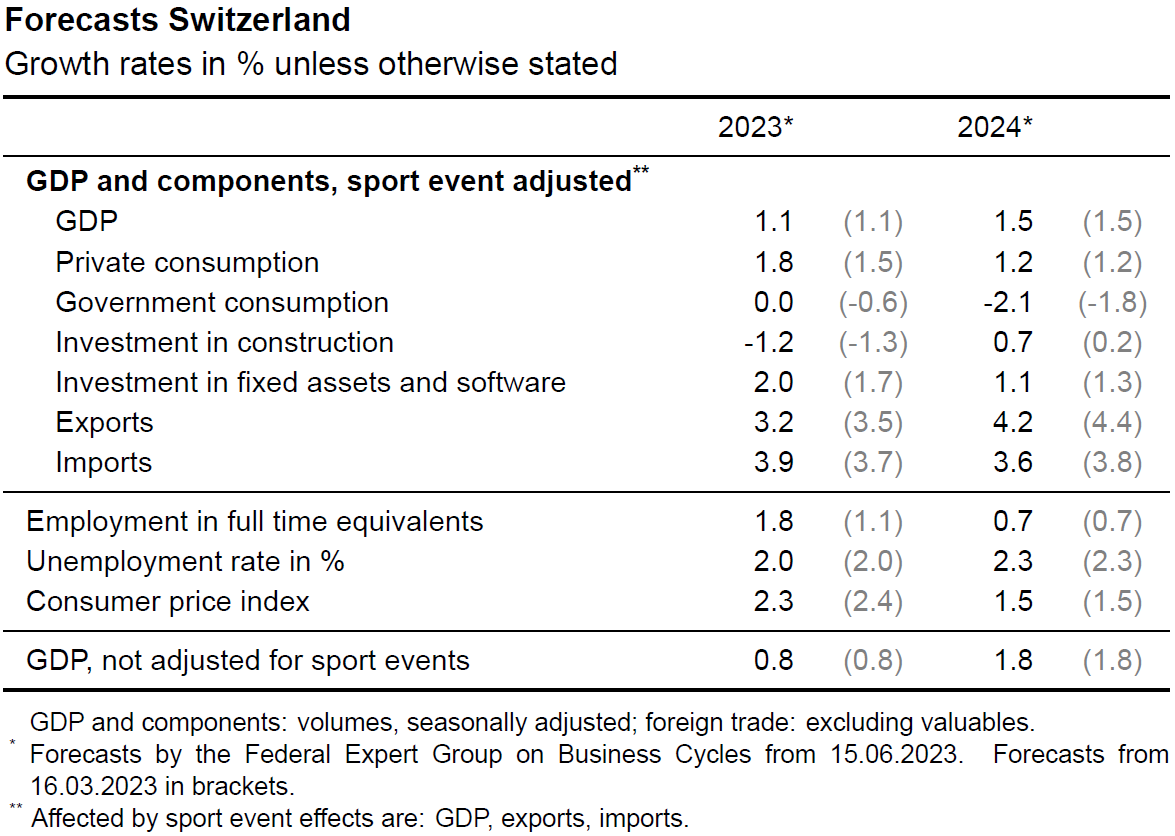

Swiss SECO: Economic growth to be significantly below average

Swiss SECO expert group on business cycles expect "significantly below average growth for the Swiss economy", at 1.1% in 2023, and then 1.5% in 2024. Both were unchanged from prior forecast in March. It added that while the economy started the year "vigorously", "inflationary pressures remain high internationally and there are pronounced economic risks".

Regarding inflation, the group expects inflation to stabilize at 2.3% in 2024 (down from March forecast of 2.4%), and then falls to 1.5% average in 2024 (unchanged from prior forecast). Unemployment rate is expected to average 2.0% in 2023, and then rise to 2.3% in 2024.

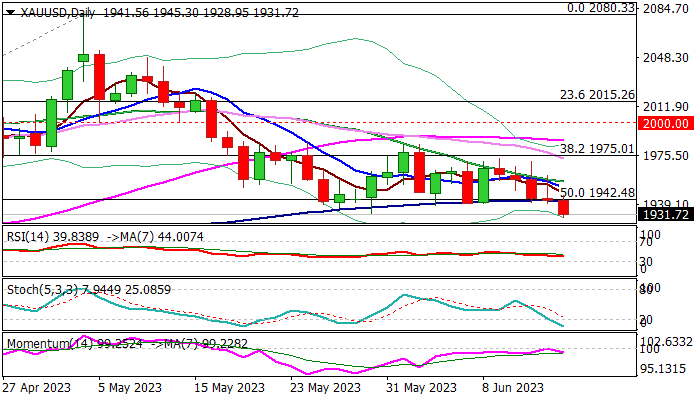

XAU/USD: Gold Falls to Three-month Low as Fed Signals More Rate Hikes

Gold fell to the lowest in almost three months on Thursday, after the Fed kept interest rates unchanged, as widely expected, but signaled more rate hikes towards the end of the year.

The central bank keeps focus on inflation, which still slows below expectations and will probably require more policy tightening in coming months, but stronger than expected performance of the US economy leave space for further rise in borrowing cost.

Hawkish signals from the Fed lifted dollar, making bullion less attractive for investors that increased pressure on gold price.

Fresh weakness broke through strong support provided by 100DMA ($1942) which contained a number of attacks in past weeks, adding to significance of support, also reinforced by the base of rising daily cloud.

Close below $1942 pivot to confirm fresh bearish signal and expose targets at $1909/$1900 (Fibo 61.8% of $1804/$2080 / psychological).

Bearish daily studies add to negative near-term outlook.

Broken $1942 pivot now acts as strong resistance, which should keep the upside protected to maintain fresh bearish bias.

Res: 1939; 1942; 1951; 1970.

Sup: 1918; 1909; 1900; 1871.