Sample Category Title

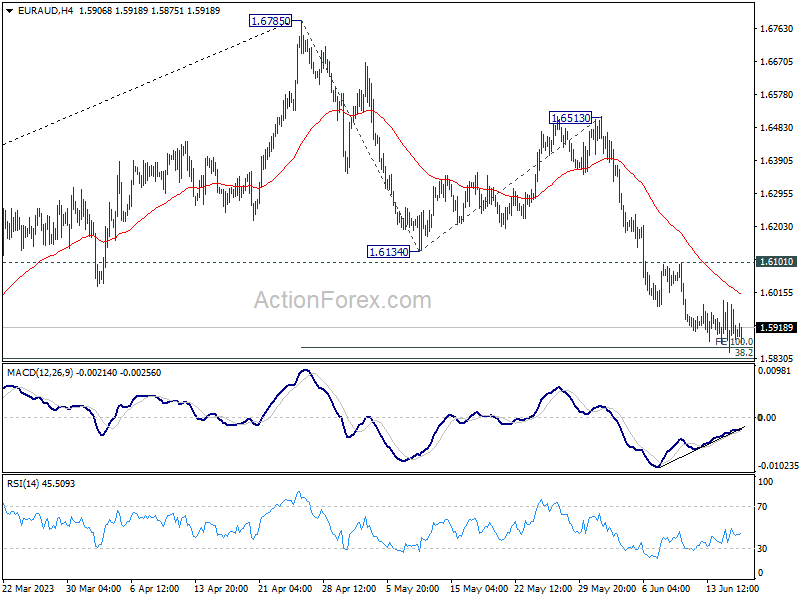

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5838; (P) 1.5914; (R1) 1.5980; More...

Intraday bias in EUR/AUD remains neutral for the moment. Strong support is still expected from around 100% projection of 1.6785 to 1.6134 from 1.6513 at 1.5862 to complete the fall from 1.6785. On the upside, break of 1.6101 resistance will confirm short term bottoming, and turn bias back to the upside for rebound.

In the bigger picture, a medium term is possibly in place at 1.6785 already, on bearish divergence condition in D MACD. Fall from there is seen as corrective whole up trend from 1.4281 (2022 low). Deeper decline is expected as long as 1.6513 resistance holds, to 38.2% retracement of 1.4281 to 1.6785 at 1.5828. Strong support could be seen there to complete the first leg of the corrective pattern.

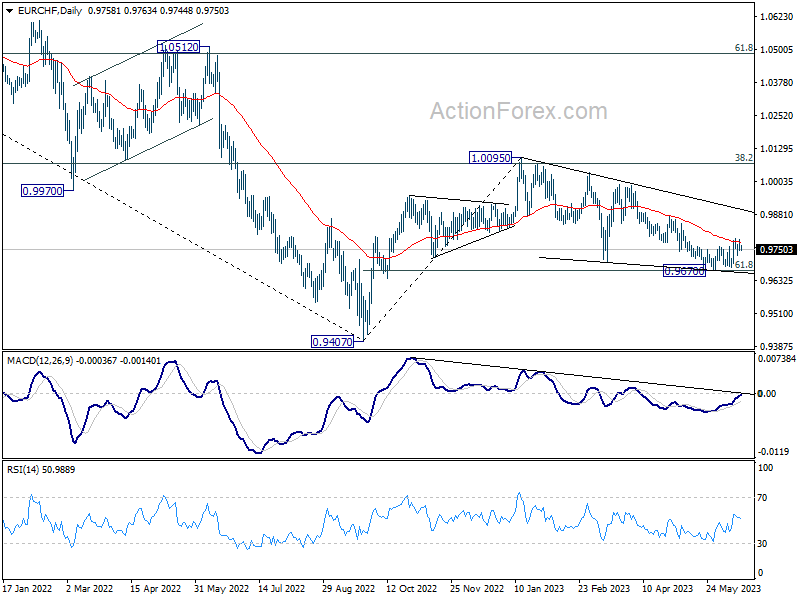

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9744; (P) 0.9767; (R1) 0.9784; More...

Intraday bias in EUR/CHF is turned neutral as it continued to lose upside momentum as seen in 4 H MACD. Risk stays on the upside as long a s0.9670 support holds. Sustained trading above 55 D EMA (now at 0.9778) will add to case that whole correction from 1.0095 has completed, after hitting 61.8% retracement of 0.9407 to 1.0095 at 0.9670. Further rise should then be seen to 0.9878 resistance next.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9929). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

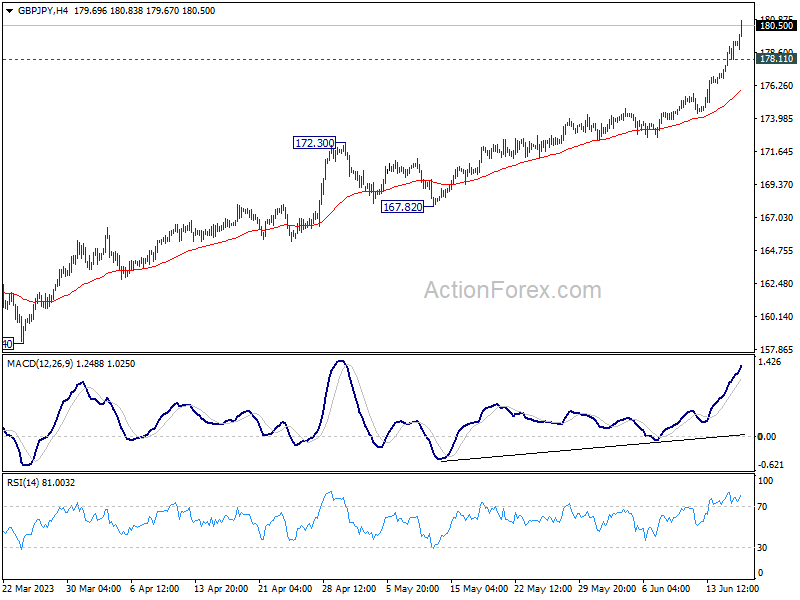

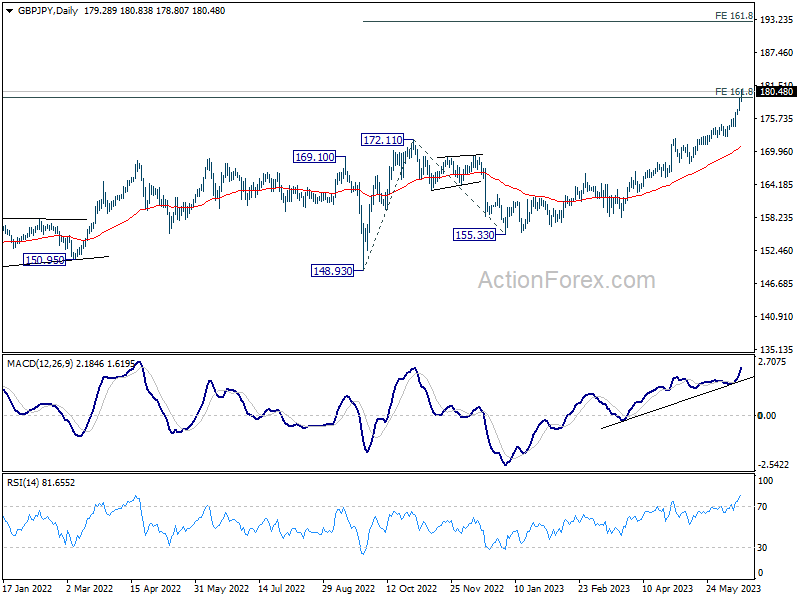

GBP/JPY Daily Outlook

Daily Pivots: (S1) 177.93; (P) 178.66; (R1) 180.08; More...

GBP/JPY surges to as high as 180.83 so far today as current rally accelerates. Intraday bias stays on the upside at this point. Next target is 161.8% projection of 148.93 to 172.11 from 155.33 at 192.83. On the downside, below 178.11 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) is extending. 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69 is already taken out. Sustained trading above there there will pave the way to 195.86 long term resistance (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

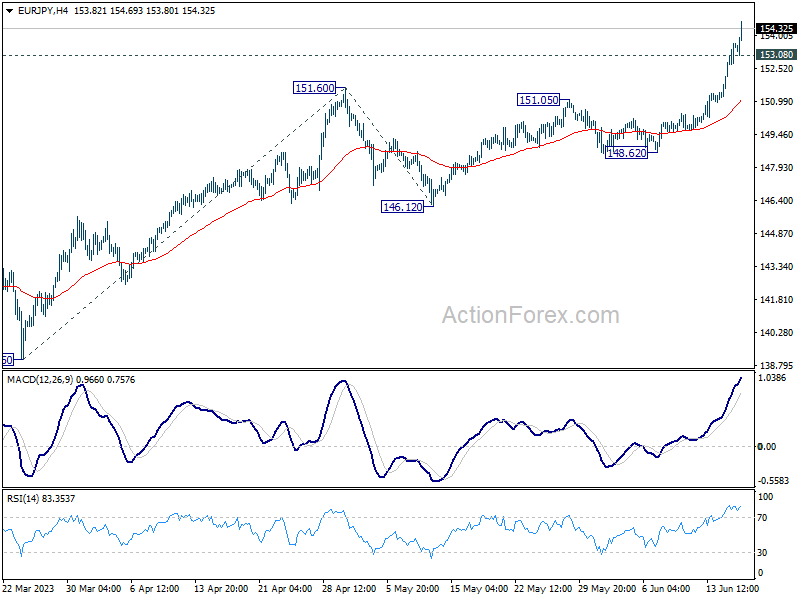

EUR/JPY Daily Outlook

Daily Pivots: (S1) 152.22; (P) 152.95; (R1) 154.29; More....

EUR/JPY accelerates to as high as 154.63 so far today. There is no sign of topping after breaking 153.63 medium term projection level. Intraday bias stays on the upside for 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64 is already met but there in no sign of topping. Further rally should be seen to 100% projection at 162.82 next. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

Yen Accelerates Down Again after BoJ, Dollar Staying Weak Too

In the wake of BoJ's decision to hold its monetary policy steady, we have seen an amplified sell-off in Yen, which is not surprising given the ongoing divergence in monetary policy with other major global central banks. The breaking of key levels in some crosses suggests that we might witness further declines in Yen, at least until Japanese authorities intervene once again.

Dollar, closely tailing Yen, is also displaying weakness and is ranked as the second poorest performer of the week. Nevertheless, it's yet to be ascertained if the greenback's trajectory is now inversely linked with risk sentiment, reverting to its norm.

On the other end of the spectrum, Australian Dollar is currently the week's top performer, but Euro is also trying to close the gap. The common currency has been buoyed by yesterday's rate hike by ECB and its hawkish economic projections. British Pound is holding up as the third strongest currency, as markets anticipate tightening by BoE next week. Meanwhile, Swiss Franc and New Zealand Dollar are showing a mixed performance, while Canadian Dollar is slightly on the softer side.

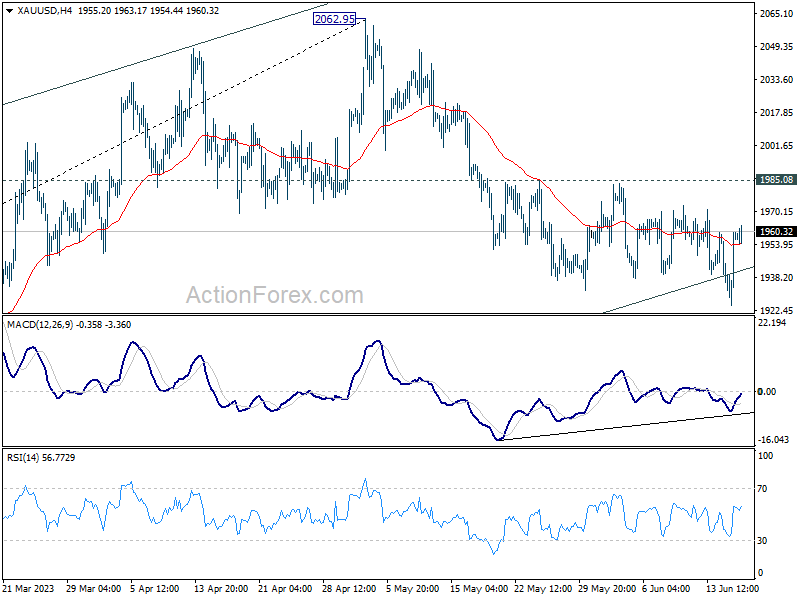

Technically, Gold recovered after just brief to 1924.61, back above medium term channel support. Bullish convergence is seen in 4H MACD. Break of 1985.08 resistance will argue that corrective fall from 2062.95 has completed. In this case, stronger rebound would be seen back to retest 2062.95 high. If realized, this could be a confirmation signal more deeper decline in Dollar elsewhere.

In Asia, Nikkei closed up 0.66%. Hong Kong HSI is up 1.00%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.57%. Japan 10-year JGB yield dropped -0.0187 to 0.413. Overnight, DOW rose 1.26%. S&P 500 rose 1.22%. NASDAQ rose 1.15%. 10-year yield dropped -0.068 to 3.728.

BoJ holds steady, core CPI to decelerate towards middle of fiscal 2023

In a widely expected move, BoJ today unanimously voted to maintain its existing ultra-loose monetary policy. The central bank kept short-term policy rate at -0.10% under its yield curve control. Yield target on 10-year JGB remains around 0%, with fluctuation band allowed also maintained at about plus and minus 0.50% from the target level. BoJ reiterated its commitment to carry on with its Quantitative and Qualitative Monetary Easing with Yield Curve Control "as long as it is necessary" and affirmed it "will not hesitate to take additional easing measures if necessary."

In its accompanying statement, BoJ noted that it anticipates Japan's economy to witness moderate recovery by around middle of the fiscal year 2023. "Thereafter, as a virtuous cycle from income to spending gradually intensifies, Japan's economy is projected to continue growing at a pace about its potential growth rate," the central bank said.

Discussing the inflation outlook, the bank stated: "The year-on-year rate of increase in the CPI (all items less fresh food) is likely to decelerate toward the middle of fiscal 2023, with a waning of the effects of the pass-through to consumer prices of cost increases led by the rise in import prices.

"Thereafter, the rate of increase is projected to accelerate again moderately, albeit with fluctuations, as the output gap improves and as medium- to long-term inflation expectations and wage growth rise, accompanied by changes in factors such as firms' price- and wage-setting behavior."

NZ BNZ PMI ticked up to 48.9, staying in relatively tight band of contraction

New Zealand BusinessNZ Performance of Manufacturing Index ticked up from 48.8 to 48.9 in May, staying well below long-term average activity rate of 53.0. Looking at some details, production dropped from 47.0 to 45.7. Employment rose from 47.7 to 49.5. New orders rose from 49.6 to 50.8. Finished stocks dropped from 52.5 to 51.5. Deliveries dropped from 50.7 to 46.0.

BusinessNZ's Director, Advocacy Catherine Beard said: "New Zealand's manufacturing sector has remained in a relatively tight band of contraction for the last three months. While the overall activity result has crept upwards over that time."

BNZ Senior Economist, Craig Ebert stated that "the range of results in the sub-components is mirrored in the breadth of issues manufacturers are now highlighting in the survey. Gone is the dominance of supply-side laments, especially regarding staff. But new negatives have arisen, for all of them to (still be) outnumbering the positive issues referenced".

Looking ahead

Eurozone CPI final and US U of Michigan consumer sentiment are the main features for the rest of the day.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 152.22; (P) 152.95; (R1) 154.29; More....

EUR/JPY accelerates to as high as 154.63 so far today. There is no sign of topping after breaking 153.63 medium term projection level. Intraday bias stays on the upside for 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64 is already met but there in no sign of topping. Further rally should be seen to 100% projection at 162.82 next. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 48.9 | 49.1 | ||

| 02:47 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 08:30 | GBP | Consumer Inflation Expectations | 3.90% | |||

| 09:00 | EUR | Eurozone CPI Y/Y May F | 6.10% | 6.10% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 5.30% | 5.30% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.00% | -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 60.2 | 59.2 |

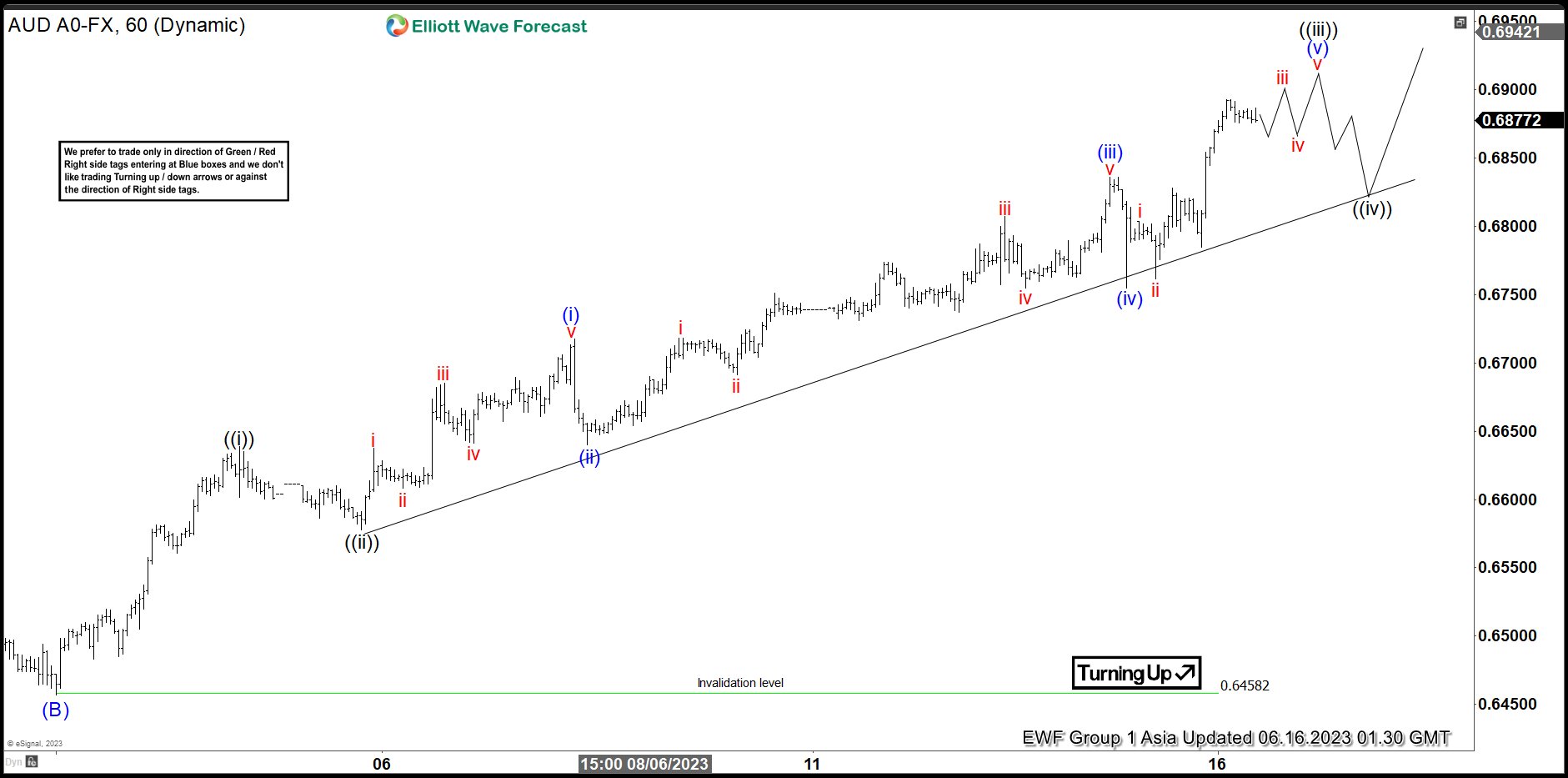

AUDUSD Starts New Elliott Wave Impulse Higher

Short Term Elliott Wave View in AUDUSD suggests the pair ended wave (B) at 0.6458. Pair has turned higher in wave (C) with subdivision as a 5 waves impulse Elliott Wave structure. Up from wave (B), wave ((i)) ended at 0.6638 and pullback in wave ((ii)) ended at 0.6578. Pair resumes higher in wave ((3)) and nesting in lesser impulsive structure. Up from wave ((ii)), wave (i) ended at 0.6717 and dips in wave (ii) ended at 0.664.

Pair resumes higher in wave (iii) towards 0.6835 and pullback in wave (iv) ended at 0.6755. Expect wave (v) to end soon which should complete wave ((iii)). Afterwards, pair should pullback in wave ((iv)) to correct cycle from 6.5.2023 low in 3, 7, or 11 swing before it resumes higher in wave ((v)). This should complete wave 1 of (C) in higher degree. Pair should then pullback again in larger degree wave 2 to correct the cycle from 6.1.2023 low before it resumes higher. Near term, as far as pivot at 0.6458 low stays intact, expect short term pullback to find support in 3, 7, or 11 swing and pair should continue to extend higher.

AUDUSD 1 Hour Elliott Wave Chart

AUDUSD Elliott Wave Video

https://www.youtube.com/watch?v=z1P8c-1GL5M

Welcome to a Bipolar World of Monetary Policies

- Monetary policies and guidance of the 4 major central banks are moving in the opposite direction.

- US Fed and Eurozone ECB are in the hawkish camp while Japan BoJ and China PBoC are still in accommodating mode.

- K-shaped performance in USD against key G-20 currencies; JPY remained weak and CNH sideways, in contrast, the rest has strengthened against the USD.

- G-10 JPY crosses are bursting up.

We have concluded three plus one monetary policy decisions outcome from four major G-20 central banks for this week; the US Federal Reserve (Fed), European Central Bank (ECB), Bank of Japan (BoJ), and People’s Bank of China (PBoC).

The latest monetary policies guidance from the Fed and ECB has been more skewed toward the hawkish side; despite the FOMC’s decision to skip a hike on the Fed funds rate this time round, the dot-plot projection has suggested two 25 basis points hike before 2023 ends to bring the terminal Fed funds rate of this current hiking cycle to a median level of 5.6%.

Over at the ECB, President Lagarde has hinted during the press conference that ECB is likely to hike by another 25 basis points (bps) in July after it raised its key policy deposit rate by 25 bps yesterday, 15 June to bring it to 3.5%, the highest level in more than 20 years. Expectations from money markets indicate that ECB may not be done hiking after July as traders’ positioning has implied an 80% probability of the ECB raising the deposit rate to 4% by October, an increase from 50% odds earlier.

In Asia, PBoC cut its one-year medium-term lending facility (MLF) interest rate yesterday which lends out funds to major China commercial banks by 10 bps to 2.65%, its first cut since August 2022. Hence, the expectations have now increased for more easing policies from PBoC to address the current slew of weak domestic/internal consumption data from China, a shift from its prior cautious targeted accommodating monetary policy stance.

Today, BoJ has maintained its ultra-easy monetary policy in place since the Great Financial Crisis of 2009, with no change in the band for the yield curve control program of the 10-year Japanese Government Bond at 0.50% on either side and short-term key policy interest rate stayed at -0.1%.

BoJ’s monetary policy statement cited Japan’s economy is picking up and likely to continue recovering moderately. But stated that the pace of core inflation is likely to slow down towards the middle of the current fiscal year with inflationary expectations moving sideways after an earlier increase. Therefore, this latest statement has suggested that BoJ is not in a “rush mode” to normalize its ultra-easy monetary policy due to an expected slowdown in inflationary pressures.

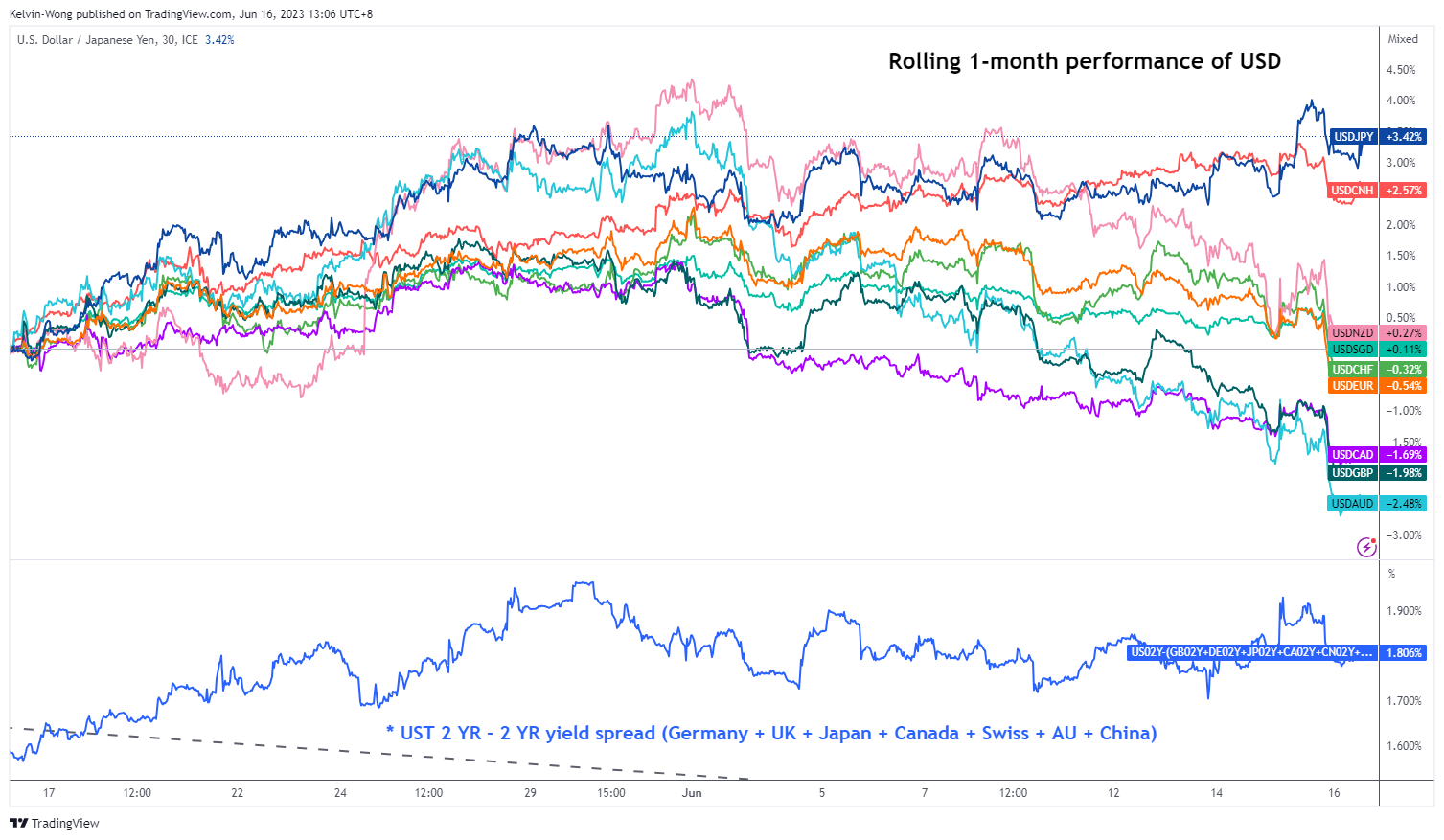

Impact on the FX market, USD outperformance against JPY but weaken significantly against the rest

Fig 1: USD against key G-20 currencies (including NZD) rolling 1-month performances as of 16 Jun 2023

(Source: TradingView, click to enlarge chart)

The rolling 1-month performances of the USD against the key G-20 currencies (inclusive of NZD) as of 16 June 2023 has shown a stark contrast driven by the current easy momentary policies mode of BoJ and PBoC. A “K-shaped” performance where the USD has strengthened against the JPY, sideways with CNH (offshore yuan) but weakened significantly against CAD, GBP, and AUD at this time of the writing.

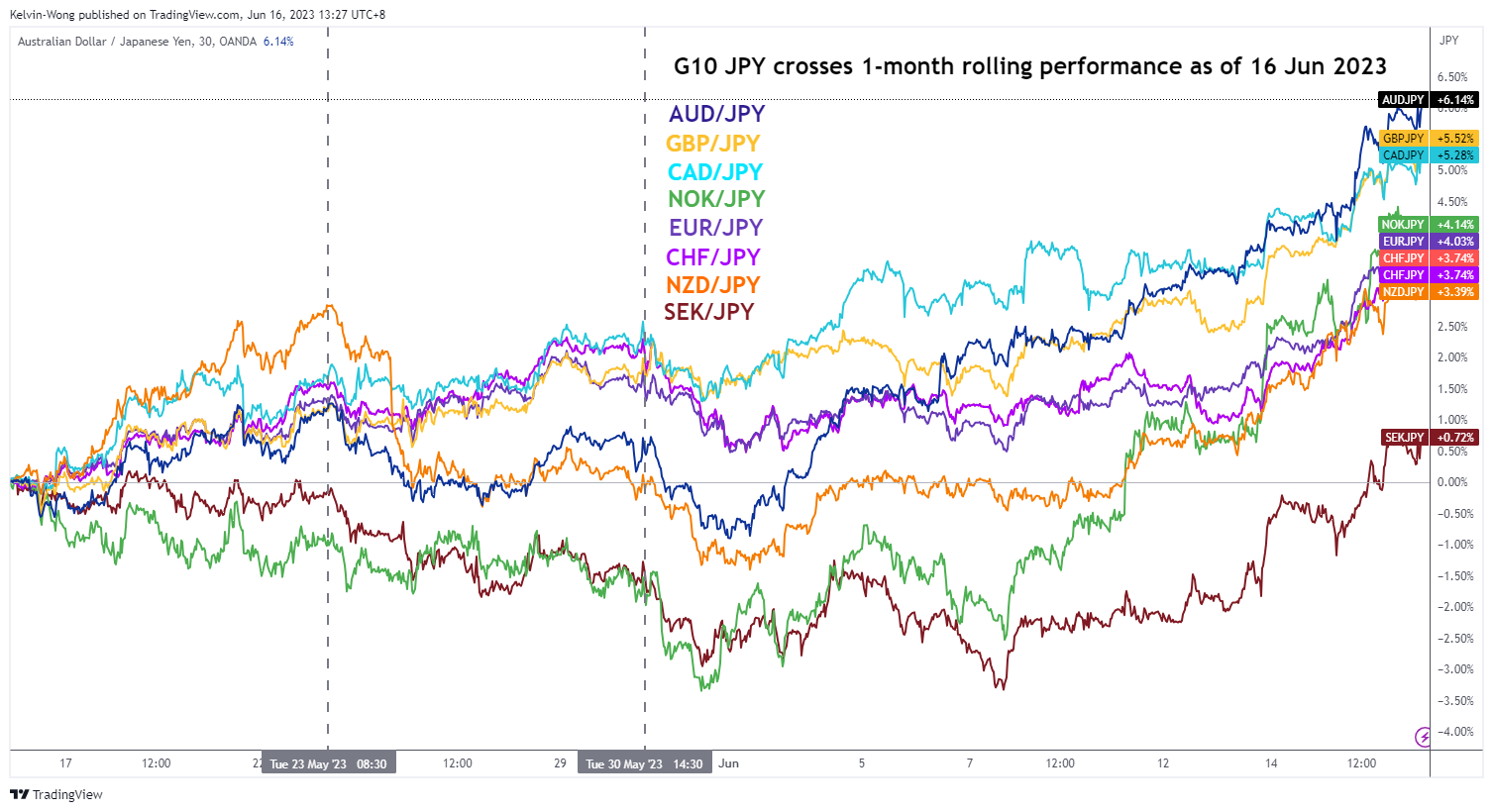

JPY crosses are now bursting upwards

Fig 2: G-10 JPY crosses rolling 1-month performances as of 16 Jun 2023 (Source: TradingView, click to enlarge chart)

The weakness seen in the JPY against the USD has led to the continuation of the JPY carry trade medium-term uptrend phase where the GBP/JPY and AUD/JPY are now trading close to a 9 and 10-month high respectively.

US Dollar Index is looking weak again for a retest on its 100.95 key near-term support

Fig 3: US Dollar Index medium-term trend as of 13 Jun 2023 (Source: TradingView, click to enlarge chart)

The US Dollar Index (a weighted average of 6 currencies, EUR, JPY, GBP, CAD, SEK & CHF where the EUR has the highest weightage of around 57%) has just broken below its 50-day moving average after it traded above it since 12 May 2023. Medium-term momentum has turned bearish as the daily RSI oscillator has reintegrated below its former corresponding support at the 50% level.

A break below the 100.95 key near-term support which the US Dollar Index has managed to hold on the previous five occasions since 2 February 2023 may resume its major downtrend movement with the next support coming in at 97.85 in the first step.

EUR Gains Momentum

EUR/USD surges towards recent peak

The euro soared after the ECB's eighth consecutive interest rate hike amid rising inflation forecasts. The pair has been inching up along a rising trend line from last week and a surge above the supply zone near 1.0900 in the shape of a former daily support has flushed out the remaining bearish interests, stirring up volatility in the process. 1.0960 is the next hurdle and as the RSI ventures again in the overbought area, a pullback would drive the price towards the trendline with 1.0820 as a key level to preserve the momentum.

AUD/USD breaks daily resistance

The US dollar continues to weaken across the board after the Fed paused its rate hikes. The current rebound from the base of last November’s momentum rally and a break above the top of a previous consolidation range (0.6800) are signs of renewed interest in the Aussie. Now that sellers are out of the picture, the path is mostly clear for an extension to 0.7000 with 0.6920 as an intermediate resistance. The two-week long rally might need some breathing room as the RSI grinds the overbought area and 0.6790 is a fresh support.

NAS 100 tests 15-month high

The Nasdaq 100 jumped as investors hope to see the Fed’s terminal rates soon. On the daily, the price is reaching its 15-month high of 15280 as bullish inertia keeps attracting buyers. However, a bearish RSI divergence indicates a deceleration in the rally and could lead to a pullback if traders start to take profit in the major supply zone. 14880 is the closest support and its breach would send the index to 14590 at the end of a previous consolidation. A close back above 15280 would resume the climb to the all-time high.

Bank of Japan Still Pushing Back Against Policy Normalization

Markets

The ECB hiked rates by 25 bps yesterday, bringing the deposit rate to 3.5%. In the base scenario, another 25 bps move follows in July. The full stop to APP reinvestments kicks in as planned, i.e. from July. The reason for further tightening even as past increases have yet to fully filter through is clear enough: “Inflation has been coming down but is projected to remain too high for too long.” Especially the upward revisions to core inflation (5.1% in 2023!) is worrying. Markets picked up Lagarde’s hawkish message. The front end of the German yield curve underperformed by adding 11 bps (2-y, surpassed the 3% barrier). The 10-y yield struggled with the 2.53-2.57% resistance area but finished 5.2 bps higher nonetheless. Moves were larger intraday but a mixed bag of US economic data interfered. A second straight 260k+ reading of US jobless claims caught markets off guard (245k expected). It helps explain the large outperformance of US Treasuries vs Bunds yesterday. Yields shed between 4.3 and 8 bps. That in turn lifted US equities more than 1% higher but weighed on the dollar. Combined with a touch of euro strength, EUR/USD surged from 1.083 to 1.0945. DXY fell towards the low 102 area. The yen slid, especially against the common currency. EUR/JPY skyrocketed towards a 15-yr high (153.55). A growing spread in central bank policy stance obviously doesn’t help either (see below). The yen loses further ground this morning against all major peers. USD/JPY is attacking recent highs in the 140.7 area. AUD/USD stabilizes near the highest level since February in the high 0.68 zone after a blow-out Australian payrolls report and USD weakness lifted the pair beyond strong 0.68 resistance yesterday. US yields recover a few bps from yesterday, with the front adding up to 3.4 bps. Bund futures deepen yesterday’s losses a bit, setting yields up for a higher open.

The economic calendar is slowly entering weekend mode. After the BoJ decision this morning, we only have U. of Michigan consumer sentiment left for release. The bar is set at a slight increase towards 60, a low level historically. The inflation expectations (1-yr and 5-10-yr ahead) part of the survey is worth mentioning separately. Barring a massive surprise we think the market impact will stay muted with the US readying for a long weekend (Juneteenth holiday on Monday). There may be some further repositioning in store for European markets in the wake of the ECB though. The technical charts, especially for short maturities, offer a helping hand as well. This also goes for EUR/USD. There’s a whole range of ECB and Fed speeches scheduled for today. Sterling is holding strong near the YtD highs. Next week is a pivotal one for the pound. Inflation numbers are due Wednesday with the Bank of England meeting scheduled a day later.

News and views

The EU Court of Justice yesterday ruled that EU law does not preclude customers from seeking compensation from banks going beyond reimbursement of the monthly installments paid after FX mortgage loan contracts are cancelled due to unfair terms. By contrast, it precludes the bank from relying on similar claims against consumers. The ruling came in the context of CHF-based mortgage loans by Polish banks. In a separate ruling, the EU court said that Polish courts can’t refuse customers a suspension of their obligation to make monthly mortgage payments in pending disputes over unfair terms in their contracts. The Polish financial regulator called on lenders to include the impact of the verdict in their provision models and that said that settlements are the most attractive and rational alternative to a costly and length legal path.

The Bank of Japan kept its monetary policy unchanged this morning, still pushing back against policy normalization even as inflation runs above the central bank’s 2% target. It has been at around 3.5% recently owing to the effects of a pass-through to consumer prices of cost increases led by a rise in import prices. The BoJ expects inflation to decelerate toward the middle of fiscal 2023. Japanese economic growth recently picked up and is likely to recover moderately supported by some pent-up demand. Risks to the outlook are extremely high with special attention needed to developments in financial and FX markets. Yen weakness recently became a topic again for Japanese officials as the currency slid to the weakest levels since just before last year’s interventions started. (USD/JPY > 140; EUR/JPY > 154, highest since 2008).

Bank of Japan Leaves Policy Unchanged While ECB Delivers More Tightening

Market movers today

Today, we get the Michigan consumer confidence survey in the US, which includes an inflation expectations component which the Fed is paying attention to. Year-ahead inflation expectations spiked to 4.6% in April but declined to 4.2% in May.

Fed Board Member Christopher Waller speaks in Oslo 13.45 on "financial stability and macroeconomic policy".

Final euro area inflation data for May is unlikely to be significantly different from the preliminary version, but will add more details.

The 60 second overview

ECB: The ECB meeting yesterday was according to expectations with its 25bp rate hike and a formal decision to end the APP reinvestments from July. The staff projections were revised higher for both underlying and headline inflation across the horizon with importantly the 2025 projection at 2.2%, above the ECB's target. Lagarde said that it's 'very likely' to hike again in July. Lagarde did not provide guidance for the rate path beyond that but reconfirmed the mantra of a known destination, but unknown journey. We continue to expect ECB to hike to 4% by September, and we reiterate our view that the burden of proof will reverse after July when we get two new inflation prints and new staff projections ahead of a September meeting, see more in Flash: ECB Review - 'Very likely' to hike again in July, 16 June.

Danmarks Nationalbank: Danmarks Nationalbank (DN) also announced a raise in its key policy rate 25bp to 3.10% and hence mirroring the ECB rate hike. DN thereby keeps the spread to ECB's policy rate unchanged at -40bp. EUR/DKK has traded towards the mid-point of the historical trading range in recent months with no need for DN to make interventions in the FX market. We expect this situation to prevail over the coming months and for DN to track future interest increases from ECB 1:1. Hence, we look for DN to hike 25bp again in July and September, which would bring its key policy rate to 3.60%.

Bank of Japan: Bank of Japan (BoJ) kept its yield curve control policy unchanged this morning as widely expected. The yen weakened further on the decision, with USD/JPY trading up around 140.7 levels. The BoJ continues to expect inflation to slow later this year. They pledge to "patiently continue with monetary easing while nimbly responding to developments in economic activity and prices as well as financial conditions". Markets will now turn focus to the press conference, not least for clues on what BoJ makes of the recent yen decline and what that means for inflation.

The economic recovery in Japan has been picking up speed recently, adding to the likelihood of a tightening move from the BoJ. May wage figures in three weeks will be key to watch ahead of the next BoJ meeting at the end of next month, in order to gauge broad wage pressures. We expect an increase in the tolerance band around the 0% 10-year yield target at that meeting or the one in September.

Energy prices. The European natural gas price has risen around 50% since the start of the month to around EUR40/Mwh - the highest level since the beginning of April. The price increase likely owes to a multitude of factors include weather-related drop in renewable power production, higher energy demand due to the dry and warm weather, the decision to close the Groningen gas field already this year, very low nuclear power production in France and finally, increased geopolitical risk to natural gas production in Europe following recent comments from Russia. Regardless of the reason, it serves as a reminder that the European energy situation is fragile and sensitive to many different factors that are hard to predict - most notably the weather. We do not think there is a big risk of sharp price increases. In particular, because European natural gas storages are 20% larger now compared to last year. Nevertheless, the increase in natural gas prices has spill-over to European power prices and coal prices.

Equities: Global equities higher again yesterday but with massive differences underneath. ECB's hawkish 25 bp hike, led yields massively higher with a stronger Euro. European equites were already lower going into the meeting but fell immediately after before recovering somewhat up to the close. Still at defensive rotation in Europe. In US it was a very different story where equities gained steadily during the session and closing around day high. S&P moved firmly above the 4400 level and on rack for a fifth straight week of gains, something that has not happened since November 2021. In US yesterday, Dow +1.3%, S&P 500 +1.2%, Nasdaq +1.2%, Russell 2000 +0.8%. Asian market grinding higher this morning while futures in Europe and US are more mixed.

FI: Yesterday's trading session was rather volatile as initially the FOMC's hawkish communication from Wednesday night took yields higher. The ECB meeting which saw an upward revision of the inflation projections across the forecast horizon initially sent rates higher as guidance for further tightening needed was given. The 10y point sold off by 5bp across most jurisdictions. The front-end led sell-off took the ECB policy peak rate 5bp higher to 3.91%, with markets bringing the September meeting into play. Bank of Japan kept its yield curve control policy unchanged this morning as widely expected.

FX: The last 24 hours in FX markets have been characterised by not least JPY weakness - on higher global yields and this morning's Bank of Japan 'unchanged' announcement - alongside the EUR gaining on a fairly hawkish ECB message yesterday. EUR/USD is back above the 1.09 level, while EUR/SEK and EUR/NOK trades around 11.60 and 11.50, respectively. EUR/GBP continues to trade around year-lows.

Credit: Credit markets continued to digest the implications of the Fed meeting as well as the rate hike from the ECB. This left credit markets with slow trading in secondary markets and relatively limited new issue supply. Overall, iTraxx Main was unchanged at 77bp while iTraxx Xover was 1bp wider at 405bp.