Sample Category Title

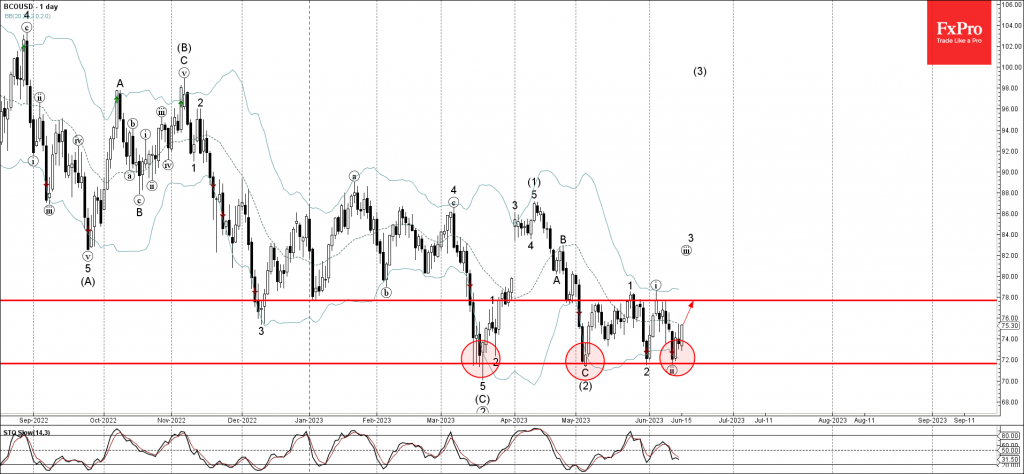

Brent Wave Analysis

- Brent reversed from key support level 72.00

- Likely to rise to resistance level 78.00

Brent crude oil recently reversed up from the key support level 72.00 (which has been repeatedly reversing the price from the middle of March), coinciding with the lower daily Bollinger Band.

The upward reversal from the support level 72.00 started the active minor impulse wave (iii).

Given the strength of the nearby support level 72.00, Brent crude oil can be expected to rise further toward the next resistance level 78.00 (which has been reversing the price from the end of May).

Stocks Suffering from a Fed Hangover, ECB Signals a July Hike

US stocks held onto losses after a data dump didn’t really give a clear signal about the economy. Wall Street is suffering from a Fed hangover that won’t go away anytime soon as the economy will remain vulnerable as further tightening seems likely. The US consumer remains robust, the labor market is slowly weakening, and the manufacturing sector is full of mixed signals. This morning’s data won’t move any Fed members, but if we continue to see healthy spending throughout the summer, the Fed will need to deliver on that dot plot forecast that has penciled in two hikes.

Now that we’ve seen so many mega-cap tech stocks overextend themselves, traders are reassessing some of the high-flying stocks, like Tesla. Tesla’s 13-day surge couldn’t last forever and that is leading to some profit-taking. Tesla’s pullback may have been triggered by the Fed’s hawkish pause, but it could also be a sign that some momentum behind the AI boon could be running out of steam for now.

US Data

Retail spending is not cooling and should keep Wall Street nervous that the disinflation process could struggle going forward. Strong buying confirms what everyone knows about the job market… it is too strong. Retail sales in May rose 0.3%, much better than the expected decline of 0.2%. Americans are buying everything from cars, furniture, electronics, and building materials.

Weekly jobless claims were unchanged at 262,000, a high print compared to the consensus estimate range of 230-268K. The labor market is still slowly weakening here.

A couple Fed regional surveys painted a mixed picture. The Empire manufacturing report posted an impressive rebound, while the Philly Fed outlook remained deeply in contraction territory. The manufacturing part of the US economy is stabilizing here, but not at a level that is triggering inflation worries for goods pricing.

FX

The Japanese yen is approaching the danger zone as FX traders anticipate the BOJ will disappoint in tightening when compared to the US. Betting on the yen has been painful and if dollar-yen falls to 145, that could trigger action by Japan.

ECB

THE ECB raised rates by a quarter percentage point and raised their inflation forecasts for the next couple of years. The statement noted that the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and will be kept at those levels for as long as necessary. They confirmed that they will discontinue the reinvestments under the asset purchase program.

The euro initially rallied on the raised inflation forecasts but that doesn’t change expectations that they are getting close to the end of this rate hiking campaign. Lagarde signaled a hike in July and more importantly a determination to get inflation down. The euro is now trending above all three key (200-, 100-, and 50-day) SMAs. Critical resistance doesn’t emerge until 1.10 region.

ECB as Expected Lifted Key Policy Rates by 25 bps

Markets

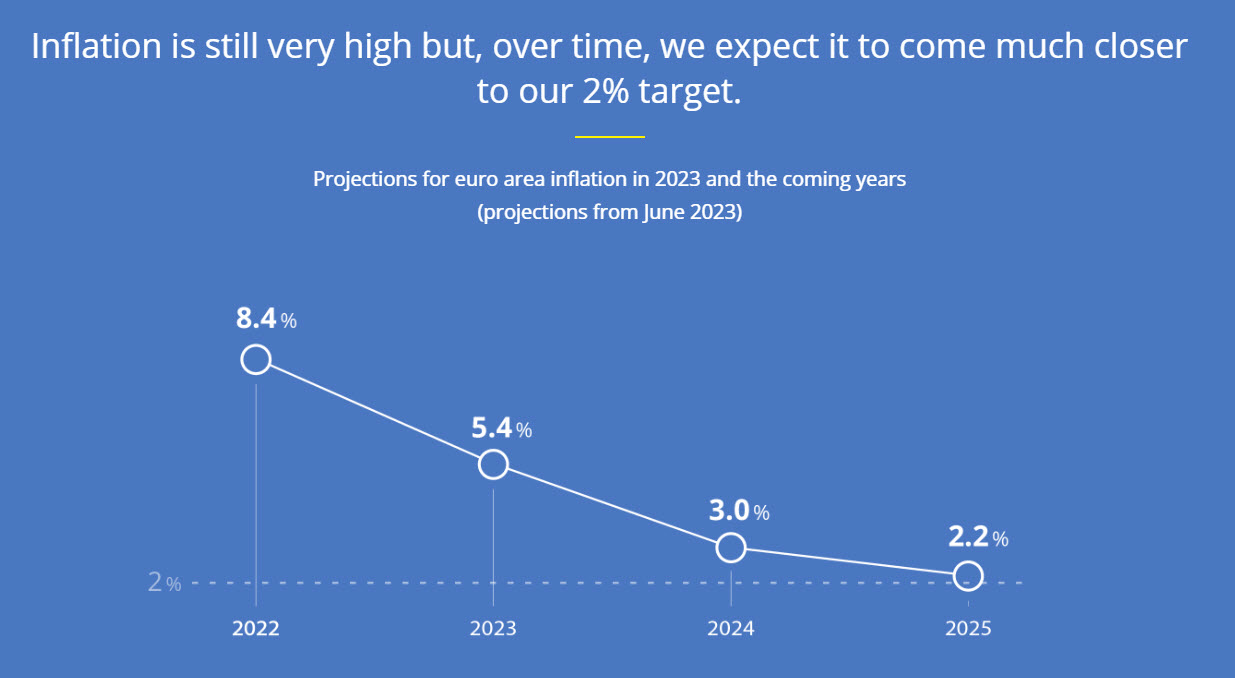

The ECB as expected lifted its key policy rates by 25 bps. The deposit rate now stands at 3.5%. The opening statement starts with the observation that inflation has been coming down combined with the confession that it is projected to remain too high for too long. Inflation forecasts faced a new upward revision compared to March. Changes to the headline figure are tiny: 5.4% for this year (from 5.3%), 3% next year (from 2.9%) and 2.2% for 2025 (from 2.1%). This hides a forceful increases in underlying core inflation though, which is the needle in the ECB’s compass: 5.1% for this year (from 4.6%), 3% for next year (from 2.5%) and 2.3% (from 2.2%) for 2025. In both cases, the ECB doesn’t expect inflation to drop sustainably to/below its 2% inflation target. Upside risks to inflation remain via both energy/food (Russia-related), wage agreements and rising inflation expectations while lower demand could have a dampening effect. The Governing Council remains inclined to extend its tightening cycle. Future decisions will ensure that key rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-target and will be kept at those levels for as long as necessary. Higher for longer is also for the ECB the key message. “Are we done? Have we finished the journey? No we’re not at our destination! We have more ground to cover! In the base scenario, we will hike the policy rate again by 25 bps in July.” ECB President Lagarde didn’t want to namedrop the September meeting yet, given the updated monetary policy report they’ll be receiving by then. “The terminal rate is something we’ll now once we’ll get there. The ultimate goal is bringing inflation down to 2%”. All else equal, we believe another 25 bps rate hike is our base case. To take attention away from the upwardly revised inflation path, the ECB said that past rate increases are being transmitted forcefully, that growth in loans is slowing and that tighter financial conditions will increasingly dampen demand.

European and US yields were rising in the wake of yesterday’s hawkish skip by the Fed and following the upward ECB CPI revisions. During the Q&A session, the tide turned completely. ECB Lagarde kept to the expected script (she had already pre-announced the July move back in May) but we think that especially mixed US eco data are to blame. Rising weekly jobless claims (2nd week running) left a sour taste while import and export prices fell faster than expected. EUR/USD accelerated its upleg, closing in on 1.09. US Treasuries outperform German Bunds.

News & Views

Dutch TTF gas prices (€42/MWh) since June have started to bottom out from the lowest levels since April 2021 between €20-25/MWh. Air-conditioning demand has risen sharply as Europe continues to be in the grip of a heatwave. Today’s price surge of more than 30% at some point, however, was supply driven. The Netherlands is set to close Europe’s biggest gas field from October 1, Bloomberg reported citing sources. The field has been a critical source of gas, especially since Russia basically cut off all supplies in response to western sanctions. Closing it means one option less to ramp up flows should the energy crisis resurface next winter. The decision isn’t fully irrevocable though, the people said. In case of high need, wells can be reopened in about two weeks. The gas field has long been controversial as its extraction caused earthquakes and damaged homes in the area. PM Rutte just one week ago narrowly survived a vote of no-confidence with his handling of the topic at the center of the debate.

Switzerland’s State Secretariat for Economic Affairs (SECO) said consumer prices will rise 2.3% this year, after 2.8% in 2022. The new prediction is a tad lower than the 2.4% in March but nevertheless above the 2% target of the Swiss National Bank. It sees inflation easing to 1.5% in 2024 while the economy should grew at a 1.1% and 1.4% clip this year and the next. The Swiss National Bank meets next week (June 22). Its president Jordan was quoted in an interview published last Saturday as saying that the fight against inflation is not over yet and further tightening of monetary policy cannot be excluded. The SNB has raised the policy rate from -0.75% to 1.5% currently. Markets expect at least a 25 bps move next week with a 40% chance discounted for a hike double that size. On the Swiss franc, Jordan said the SNB has already allowed CHF to strengthen but he doesn’t want it “to appreciate too much”. EUR/CHF since May traded a tight range between 0.97/0.98.

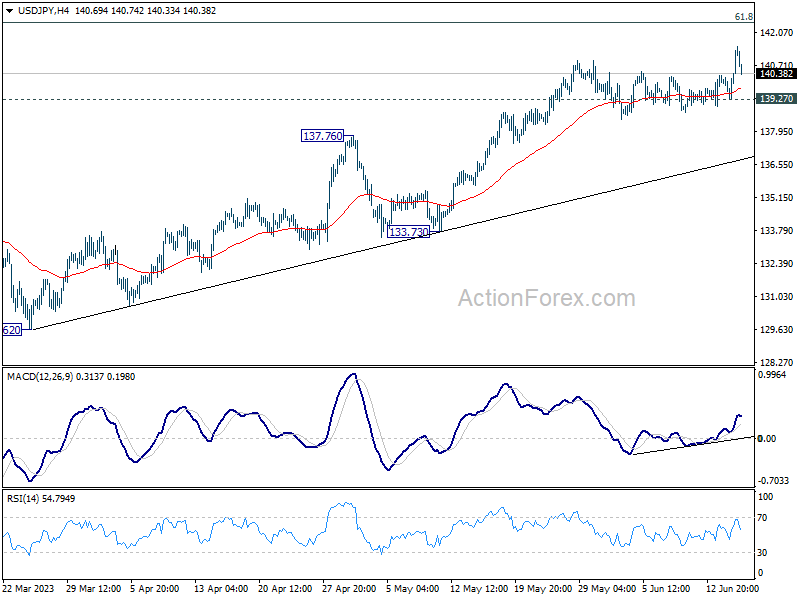

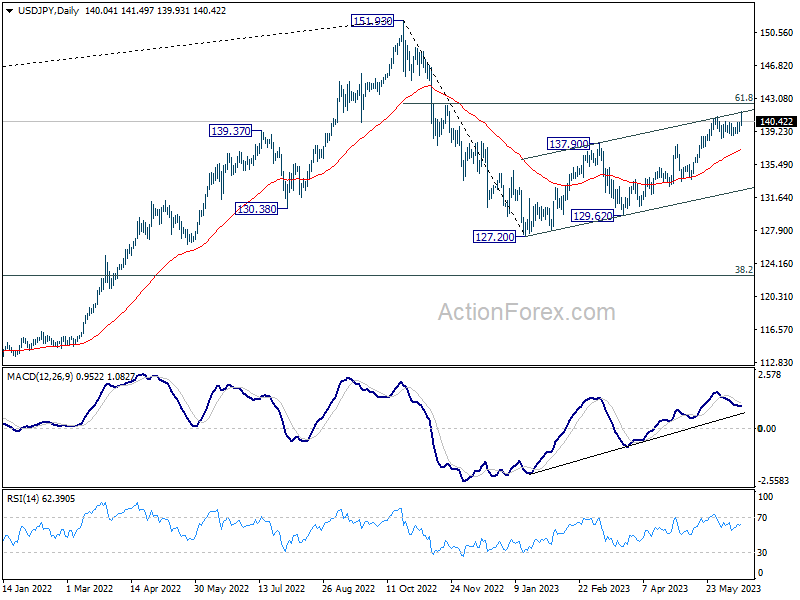

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.50; (P) 139.89; (R1) 140.49; More...

USD/JPY retreats notably in early US session. But further rally is still expected as long as 139.27 support holds. Current rise from 127.20 should now target 142.48 fibonacci level next. Nevertheless, break of 139.27 will now indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 142.48. Sustained break there will pave the way back to retest 151.93. On the downside, however, decisive break of 137.90 resistance turned support will now be the first indicate that this rebound from 127.20 has completed already.

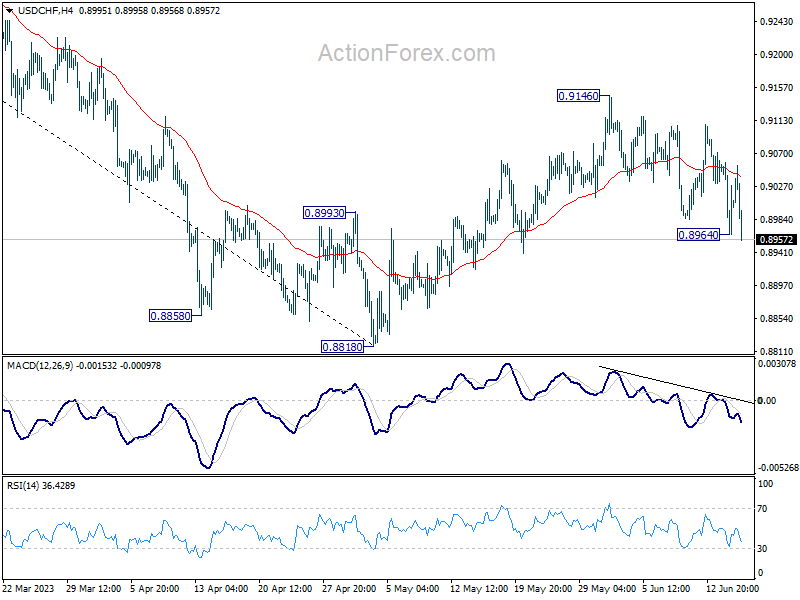

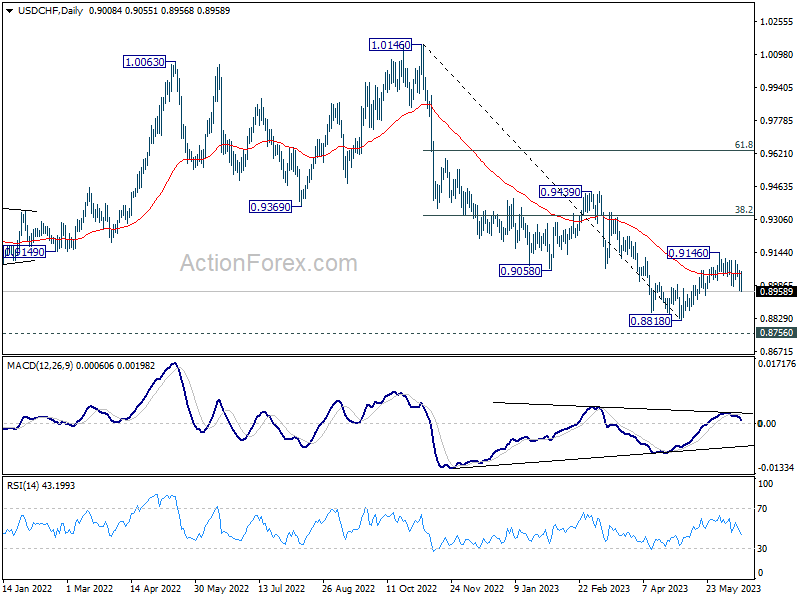

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8965; (P) 0.9012; (R1) 0.9059; More...

USD/CHF's fall from 0.9146 resumed after brief recovery and intraday bias is back on the downside for 0.8818 support. For now, strong support is still expected from 0.8756 to bring reversal. But risk will stay on the downside as long as 0.9146 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

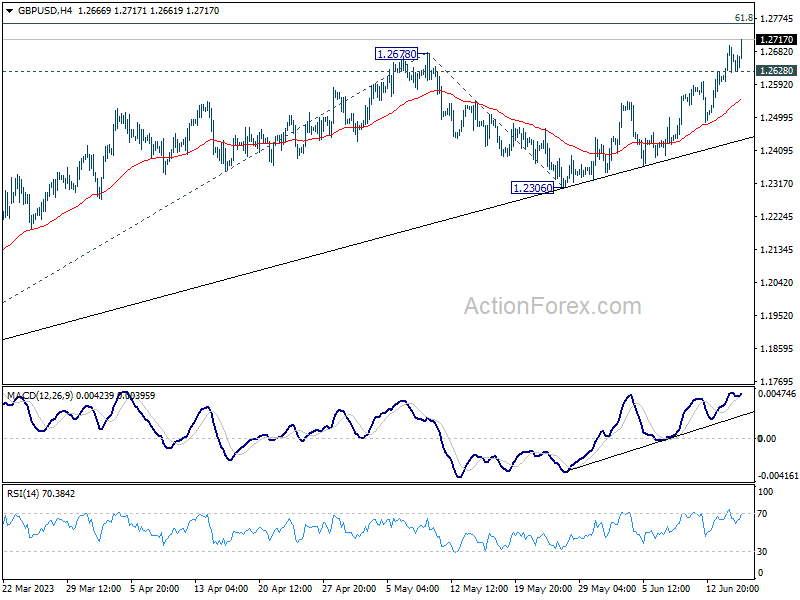

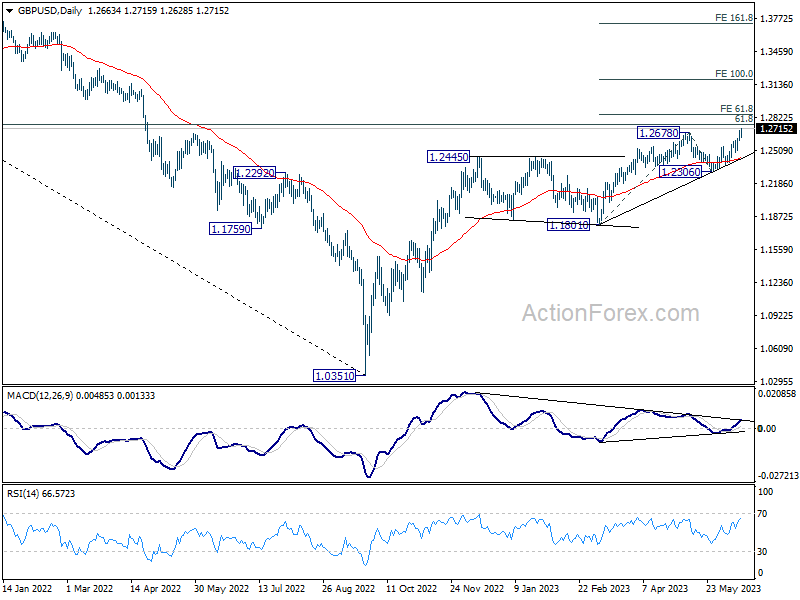

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2609; (P) 1.2654; (R1) 1.2707; More...

GBP/USD's rally continues today and the firm break of 1.2678 resistance should confirm resumption of whole up trend from 1.0351. Intraday bias stays on the upside for 1.2759 fibonacci level, and then 61.8% projection of 1.1801 to 1.2678 from 1.2306 at 1.2848. On the downside, below 1.2628 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 1.2306 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.2306 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

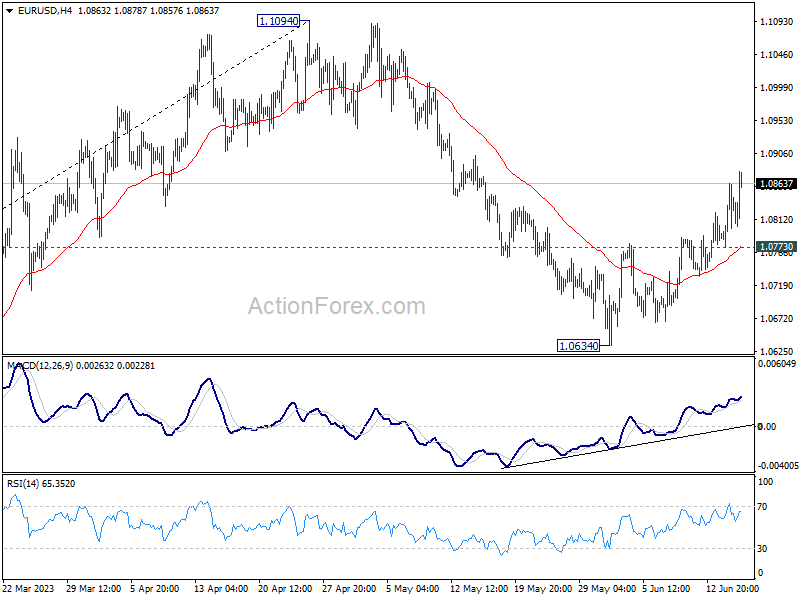

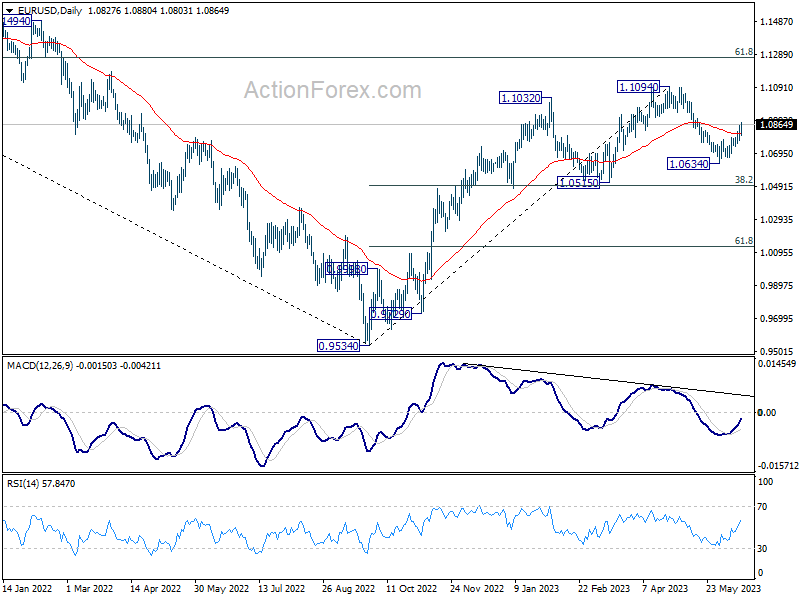

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0823; (R1) 1.0872; More...

EUR/USD's rally from 1.0634 short term bottom continues today and intraday bias stays on the upside. Corrective fall from 1.1094 could have completed already. Further rally would be seen back to retest 1.1094 high. On the downside, though, below 1.0773 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Euro Soars as ECB Hikes Rates Amid Upgraded Core Inflation Forecasts

Euro is making notable gains following ECB's decision to increase interest rates by a widely anticipated 25bps. The real kicker, however, is the significant upward revision of core inflation forecasts for both the current and following years, pushing the common currency up across the board. Swiss Franc capitalized on Euro's rally, securing its spot as the day's next strongest performer. Sterling, on the other hand, delivered a mixed performance, selloff against Euro. Australian Dollar emerges as the third strongest player, buoyed by robust jobs data released earlier in Asian trading session.

On the flip side, Japanese Yen continues to languish as the weakest performer, with verbal interventions from Japanese officials having done little to stem its downward trajectory. There was, however, a slight recovery during early US session, likely attributable to traders engaging in short covering in advance of BoJ rate decision in the upcoming Asian session. New Zealand Dollar is the day's second weakest currency, followed closely by Canadian Dollar. Dollar, meanwhile, exhibited a mixed performance, largely brushing off the retail sales and jobless claims data.

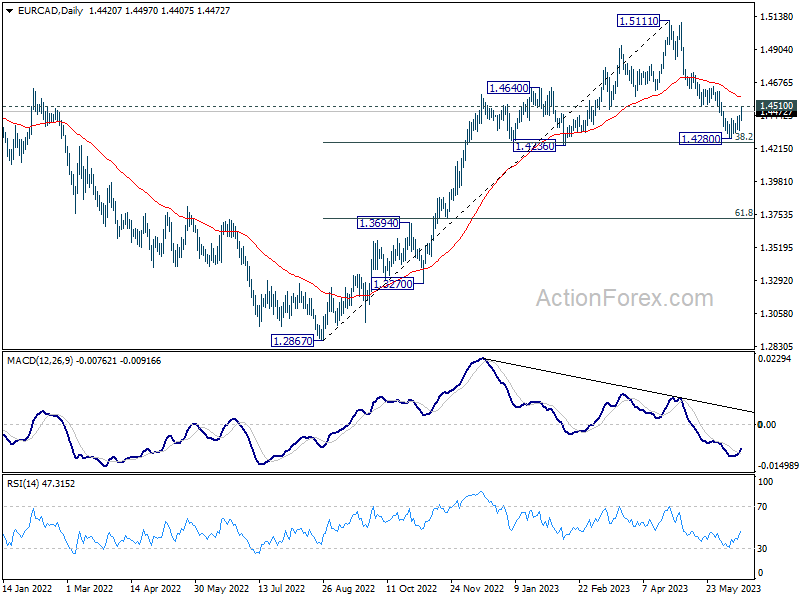

Technically, EUR/CAD's rebound from 1.4280 is finally taking up some momentum. Immediate focus is now on 145.10 support turned resistance. Decisive break there should confirm that corrective fall from 1.5111 has completed, just ahead of 1.4236 cluster support (38.2% retracement of 1.2867 to 1.5111 at 1.4254). Stronger rally should then be seen through 55 D EMA (now at 1.4570). If realized, the rally in EUR/CAD could also be accompanied by break of 1.6101 resistance in EUR/AUD.

In Europe, the time of writing, FTSE is up 0.01%. DAX is down -0.72%. CAC is down -0.95%. Germany 10-year yield is up 0.047 at 2.500. Earlier in Asia, Nikkei dropped -0.05%. Hong Kong HSI surged 2.17%. China Shanghai SSE rose 0.74%. Singapore Strait Times rose 0.77%. Japan 10-year JGB yield rose 0.0009 to 0.432.

US retail sales rose 0.3% mom in May, ex-auto sales up 0.1% mom

US retail sales rose 0.3% mom to USD 686.6B in May, above expectation of 0.0% mom. Ex-auto sales rose 0.1% mom to USD 554.5B, matched expectations. Ex-gasoline sales rose 0.6% mom to USD 633.5B. Ex-auto and gasoline sales rose 0.4% mom to USD 501.5B

In the three months to may, sales were up 1.7% from the same period a year ago.

US initial jobless claims unchanged at 262k

US initial jobless claims was unchanged at 262k in the week ending June 10, well above expectation of 246k. Four-week moving average of initial claims rose 9k to 247k, highest since November 20, 2021 when it was 249k.

Continuing claims rose 20k to 1775k in the week ending June 3. Four-week moving average of continuing claims dropped -6k to 1778k.

ECB hikes 25bps, core inflation forecast raised sharply higher

ECB raises its key interest rates by 25bps as widely expected. The main refinancing rate, marginal lending facility rate, and deposit rates will be 4.00%, 4.25% and 3.50% after the hike.

In the accompanying statement, it's reiterated that the Governing Council will continued to follow a "data-dependent approach" in future decisions, to bring rates to levels "sufficiently restrictive" to achieve timely return of inflation to 2% target. Rates will also be kept at that level "for as long as necessary".

In the updated economic projections, core inflation projection is revised up notably in 2023 and 2024, and slightly in 2025. Growth projection was revised down slightly in both 2023 and 2024.

- Inflation is projected to average 5.4% in 2023, 3.0% in 2024 and 2.2% in 2025. (March: 5.3% in 2023, 2.9% in 2024 and 2.1% in 2025).

- Core inflation is projected to reach 5.1% in 2023, before it declines to 3.0% in 2024 and 2.3% in 2025. (March: 4.6% in 2023, 2.5% in 2024 and 2.2% in 2025).

- Growth is projected to be at 0.9% in 2023, 1.5% in 2024 and 1.6% in 2025. (March: 1.0% in 2023, 1.6% in 2024, 1.6% in 2025).

Eurozone exports down -3.6% yoy in Apr, imports down -11.9% yoy

Eurozone exports of goods to the rest of the world decreased -3.6% yoy in April to EUR 216.0B. Imports decreased -11.9% yoy to EUR 227.7B. A EUR -11.7B trade deficit was recorded. Intra-Eurozone trade was also down by -5.2% yoy to EUR 208.3B.

In seasonally adjusted term, exports fell -3.2% mom to EUR 234.5B. Imports rose 5.9% mom to EUR 241.5B. Trade balance turned into EUR -7.1B deficit, versus expectation of EUR 5.7B surplus. Intra-Eurozone trade fell from EUR 224.1B in March to 222.4B in April.

Swiss SECO: Economic growth to be significantly below average

Swiss SECO expert group on business cycles expect "significantly below average growth for the Swiss economy", at 1.1% in 2023, and then 1.5% in 2024. Both were unchanged from prior forecast in March. It added that while the economy started the year "vigorously", "inflationary pressures remain high internationally and there are pronounced economic risks".

Regarding inflation, the group expects inflation to stabilize at 2.3% in 2024 (down from March forecast of 2.4%), and then falls to 1.5% average in 2024 (unchanged from prior forecast). Unemployment rate is expected to average 2.0% in 2023, and then rise to 2.3% in 2024.

Australia employment grew 75.6k in May, unemployment rate back to 3.6%

Australia employment rose 75.6k in May, well above expectation of 16.5k. Full time jobs grew 61.7k while part-time jobs grew 14.3k.

Unemployment rate dropped from 3.7% to 3.6%, below expectation of 3.7%. Participation rate rose from 66.7% to 66.9%. Monthly hours worked dropped -1.8% mom. Employment-to-population ratio rose 0.2% to 64.5%, a record high.

Bjorn Jarvis, ABS head of labour statistics, said: "Looking over the past two months, the employment increases average out to around 36,000 extra employed people each month. This is still around the average over the past year of 39,000 people a month."

"Just before the start of the pandemic almost 13 million people were employed in Australia. In May 2023, this had risen to just over 14 million people."

NZ GDP down -0.1% qoq in Q1, driven by inventory rundown and services exports

New Zealand GDP contracted -0.1% qoq in Q1 as expected. Primary industries fell -0.5%. Service industries fell -0.6%. Goods producing industries fell -0.4%.

StatsNZ noted, "The expenditure measure of GDP fell 0.2 percent this quarter. This decline was driven by run downs in inventories held by businesses, and a fall in exports of services."

"A 2.4 percent increase in household consumption expenditure and 2.0 percent growth in investment in fixed assets partially offset the falls."

China production and investment data show struggling private sector

China's industrial production growth for May came in at 3.5% yoy, aligning with market expectations. However, a discrepancy was observed in growth rates of private and state-owned businesses. Industrial output from private businesses only managed to expand by 0.7% yoy, a stark contrast to the 4.4% yoy growth posted by state-owned enterprises.

Furthermore, China's fixed asset investment rose 4.0% ytd yoy, a figure falling short of the anticipated 4.4% and a marked deceleration from 4.7% recorded during the first four months of 2023. Notably, private businesses experienced a dip in their fixed asset investment by -0.1% ytd yoy, while state-owned enterprises reported robust growth of 8.4%.

Meanwhile, retail sales failed to meet expectations, recording a rise of 12.7% yoy, lower expectation of 13.9% yoy increase.

In a separate but related development, People's Bank of China announced a cut in rate on its one-year medium-term lending facility loans to financial institutions. The rate was lowered from 2.75% to 2.65%, following the bank's decision to cut seven-day reverse repo and standing lending facility rate earlier this week.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0823; (R1) 1.0872; More...

EUR/USD's rally from 1.0634 short term bottom continues today and intraday bias stays on the upside. Corrective fall from 1.1094 could have completed already. Further rally would be seen back to retest 1.1094 high. On the downside, though, below 1.0773 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q1 | -0.10% | -0.10% | -0.60% | |

| 23:50 | JPY | Trade Balance (JPY) May | -0.78T | -0.78T | -1.02T | -1.04T |

| 23:50 | JPY | Machinery Orders M/M Apr | 5.50% | 3.00% | -3.90% | |

| 01:00 | AUD | Consumer Inflation Expectations Jun | 5.20% | 5.00% | ||

| 01:30 | AUD | Employment Change May | 75.9K | 16.5K | -4.3K | -4.0K |

| 01:30 | AUD | Unemployment Rate May | 3.60% | 3.70% | 3.70% | |

| 02:00 | CNY | Retail Sales Y/Y May | 12.70% | 13.90% | 18.40% | |

| 02:00 | CNY | Industrial Production Y/Y May | 3.50% | 3.50% | 5.60% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 4.00% | 4.40% | 4.70% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.20% | 0.50% | -1.70% | |

| 06:30 | CHF | Producer and Import Prices M/M May | -0.30% | 0.10% | 0.20% | |

| 06:30 | CHF | Producer and Import Prices Y/Y May | -0.30% | -0.20% | 1.00% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | -7.1B | 5.7B | 17.0B | 14.0B |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.00% | 4.00% | 3.75% | |

| 12:30 | CAD | Manufacturing Sales M/M Apr | 0.30% | -0.20% | 0.70% | 0.80% |

| 12:30 | USD | Empire State Manufacturing Index Jun | 6.6 | -14.6 | -31.8 | |

| 12:30 | USD | Retail Sales M/M May | 0.30% | 0.00% | 0.40% | |

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.10% | 0.10% | 0.40% | |

| 12:30 | USD | Initial Jobless Claims (Jun 9) | 262K | 248K | 261K | 262K |

| 12:30 | USD | Import Price Index M/M May | -0.60% | -0.10% | 0.40% | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | -13.7 | -12.7 | -10.4 | |

| 12:45 | EUR | ECB Press Conference | ||||

| 13:15 | USD | Industrial Production M/M May | 0.10% | 0.50% | ||

| 13:15 | USD | Capacity Utilization May | 79.70% | 79.70% | ||

| 14:00 | USD | Business Inventories Apr | 0.20% | -0.10% | ||

| 14:30 | USD | Natural Gas Storage | 97B | 104B |

ECB Lagarde press conference live stream

https://www.youtube.com/watch?v=EwwxwdgZaNw