Sample Category Title

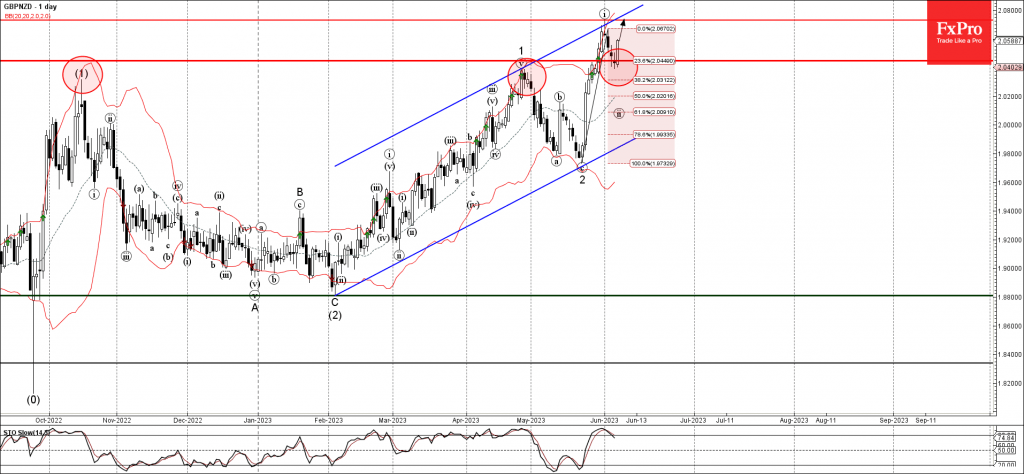

GBPNZD Wave Analysis

- GBPNZD reversed from support level 2.0390

- Likely to rise to resistance level 2.0730

GBPNZD recently reversed up sharply from the powerful support level 2.0390 (which stopped the two previous sharp upward impulses in October and April).

The upward reversal from the support level 2.0390 continues the clear multi-month uptrend from the start of this year.

Given the predominant uptrend, GBPNZD can be expected to rise further toward the next resistance level 2.0730 (top of the previous minor impulse wave (i)).

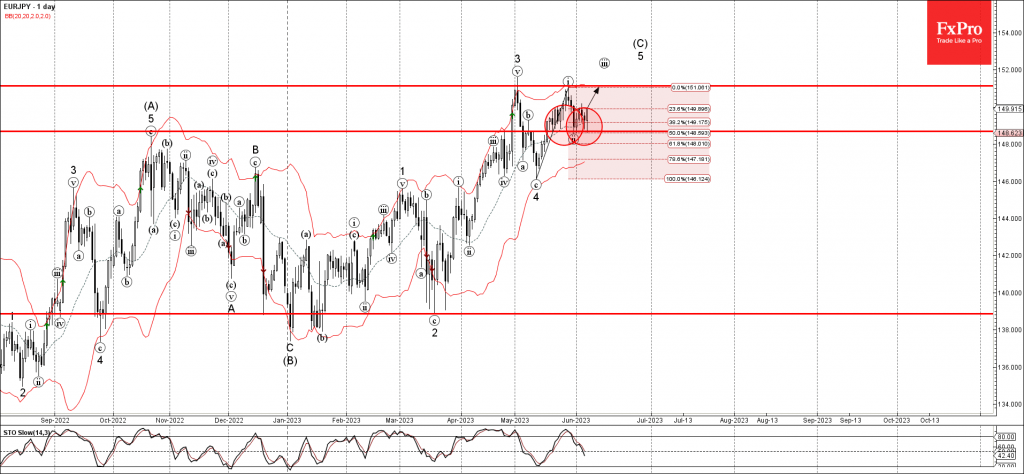

EURJPY Wave Analysis

- EURJPY under bullish pressure

- Likely to rise to resistance level 151.15

EURJPY under the bullish pressure after the price reversed up from the key support level 148.70 (which has been reversing the price from the middle of May).

The support level 148.70 was strengthened by the 20-day moving average and by the 50% Fibonacci correction of the previous sharp upward impulse wave (i).

Given the predominant uptrend, EURJPY can be expected to rise further toward the next resistance level 151.15 (top of the previous waves (v) and (i)).

Bank of Canada Delivers Surprise 25 Basis Point Hike

The Bank of Canada raised the overnight rate by 25 basis points, to 4.75%, while stating that it will continue with Quantitative Tightening (QT).

The bank highlighted the resurgence in economic momentum by stating, "Canada’s economy was stronger than expected in the first quarter of 2023, with GDP growth of 3.1%. Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains. Demand for services continued to rebound. In addition, spending on interest-sensitive goods increased and, more recently, housing market activity has picked up."

On rising prices, it stated that "prices for a broad range of goods and services coming in higher than expected. Goods price inflation increased, despite lower energy costs. Services price inflation remained elevated, reflecting strong demand and a tight labour market."

On the future path of policy, the Bank will "be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target."

Key Implications

The BoC leapt off the sidelines and jumped back in the game with a surprise rate hike. The Canadian economy has accelerated over 2023, with consumer spending leading the way. Robust employment gains and inflation-adjusted wage increases are enabling Canadians to keep spending in spite of high interest rates. With excess demand persisting, this will likely delay the timing of when inflation will be able to return to the 2% target.

There has also been a massive resurgence in the real estate market. Ever since the BoC paused on rate hikes earlier this year, the real estate market has returned to sellers' territory, with sales and prices soaring. That had to be worrying the BoC, which doesn't want to see financial imbalances balloon once again. We have highlighted the need for the BoC to actively lean against household imbalances when it sees them forming and the move today was a shot across the bow on that front.

Bet you can't have just one. With today's hike, the BoC is back in hiking mode. Economic data are pointing to more strength and the Bank has yet to see any sign from the labour market that the economy is turning. We expect the BoC to hike again in July, bringing the policy rate to 5%.

Bank of Canada Remains Proactive With 25 bp Rate Hike

- Following a two meeting pause, the BoC resumed tightening with a 25 bp hike lifting the overnight rate to 4.75%

- Today’s increase is hardly shocking given recent data flow but was only expected by a handful of analysts

- No clear tightening bias but a follow up hike in July is likely

There were plenty of reasons for the BoC to restart its tightening cycle today. GDP growth was stronger than expected in Q1 led by robust consumer spending, inflation surprised to the upside in April, unemployment has been steady near a record low for five straight months, and Canada’s housing correction appears to have run its course. We thought the BoC might wait until July to accumulate a few more data points and refresh its forecasts, but consistent with a proactive approach throughout this tightening cycle, Governing Council surprised the consensus (and us) with a 25 bp rate hike. While Governor Macklem sounded like he was in no rush to raise rates at his FSR press conference in mid-May—focusing on broader CPI trends rather than the April miss and downplaying the rebound in housing—today’s policy statement reads like there was little doubt that a hike was appropriate. The BoC’s key message is that “excess demand in the economy looks to be more persistent than anticipated” and there is growing risk that inflation “could get stuck materially above the 2% target.”

With Macklem’s “accumulation of evidence” criteria having been met, Governing Council determined monetary policy was not sufficiently restrictive to return inflation sustainably to target. The concluding statement doesn’t include a clear tightening bias but our expectation has been that if the BoC was coming off the sidelines, they would intend to hike more than once—if 4.50% wasn’t restrictive enough it’s hard to think 4.75% is. Governing Council laid out its now-familiar criteria for future policy decisions: the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour. It’s an unusually short five weeks until the July rate decision, but that period is packed with key releases including two employment reports, another CPI reading, an updated April GDP estimate and May flash, and the Q2 Business Outlook Survey. The onus is clearly on that data to soften broadly to preclude another rate hike, and timing a slowdown has been challenging. We’ll publish updated forecasts in our Macro & Provincial Outlook and Financial Markets Monthly tomorrow.

Sunset Market Commentary

Markets

We kick off today with the Turkish lira, in a separate bullet for the occasion. It’s as if the floor beneath it simply evaporated. TRY tanks about 7% against the US dollar and the euro to new record lows of USD/TRY 23.10 and EUR/TRY 24.92. This is however not part of an all-out Turkish asset crash. Stocks are easily rising 3% today. The Borsa Istanbul 100 since end May skyrocketed a stunning 25%. Turkey’s dollar bonds also extended their rally. And Turkish CDS (5-y), after surging to the highest since October 2022 in the wake of president Erdogan’s election victory, eased to the lowest level since end 2021. These moves follow the appointment of Mehmet Simsek as the new finance minister. Simsek pledged a return to “rational” economic policies. That prompted investor hopes of Turkey returning to more conventional policymaking. One of the key unorthodoxies were the massive FX interventions that have prevented the Turkish lira from declining uncontrollably. But Bloomberg today ran a story citing people familiar with the matter that Simsek had asked the central bank to ditch these operations, unshackling long-subdued strong TRY market forces that probably have additional room to run. Next on the agenda: higher (instead of lower) policy rates to finally address soaring inflation. President Erdogan for the past years twisted the central bank’s arm in lowering rates as he considered this the solution to the dramatic price surges. The policy rate currently is a mere 8.5% vs inflation of more than 40%. D-day is June 22.

Moves on other markets are miniscule compared to the hefty repositioning in Turkish assets. US yields nonetheless rise between 3.2 to 5.3 bps. The front-end underperforms with the US Treasury’s announcement weighing additionally. It expects to rebuild its cash buffer to around $425bn at the end of June. That’s up from an extremely low $50bn, give or take, currently. Expectations for a flood of T-bills in coming months have raised concerns here and there as it is seen sucking up liquidity in a relatively short period of time. That said, there’s still a huge amount of excess liquidity being parked at the Fed’s reserve repo facility every day (> $2000bn) that in theory could easily be redirected towards T-bills. German yields trade choppy and are on track to finish the day 2.9 bps higher at the front but a few bps lower at the longest tenor (30-y: -1.8 bps). Currencies trade muted. EUR/USD hit an intraday low of 1.067, this week’s low, before rebounding back north of 1.07(2). The trade-weighted DXY and EUR/GBP both ease to just south of 104 and 0.86 respectively in uninspired trading. The Canadian loonie awaits the Bank of Canada’s policy decision later today. It deserves some extra attention following the Reserve Bank of Australia’s unexpected rate hike earlier this week. Markets are almost evenly split between a hike and the status quo at 4.50%.

News & Views

The OECD updated its global economic outlook. It is improving, albeit from a weak recovery to a low growth recovery. The outlook projects a moderation of global GDP from 3.3% in 2022 to 2.7% this year, followed by 2.9% in 2024. Lower energy prices are easing the strain on household budgets, business and consumer sentiment are recovering, albeit from low levels, and the re-opening of China has provided a boost to global activity. On a country level, India is the growth engine with 6% and 7% respectively this year and next. OECD countries are projected to grow by 1.4% in 2023 and 2024. Headline inflation in the OECD is projected to decline from 9.4% in 2022 to 6.6% in 2023 and 4.3% in 2024. The decline in inflation is due to tighter monetary policy taking effect, lower energy and food prices and reduced supply bottlenecks. Monetary policy should remain restrictive until there are clear signs that underlying inflationary pressures are durably reduced. OECD Chief Economist called on fiscal policy to be scaled back, prioritizing productivity-enhancing public investments including those driving the green transition and boosting labour supply and skills.

Czech retail sales decreased by 0.3% M/M in April with the Y/Y-figure pointing to a 7.7% decline (from -9.5% Y/Y in March). The decrease of sales in retail trade was broad-based with the exception of sales of automotive fuels. Hungarian industrial production declined by 2.5% M/M in April (-5.8% Y/Y). Output increased in only two sectors: the manufacture of transport equipment and of electrical equipment. YTD, production was 4.3% lower compared to Jan-Apr of 2022. CZK and HUF both trade on the softer side today, respectively at EUR/CZK 23.62 and EUR/HUF 369.

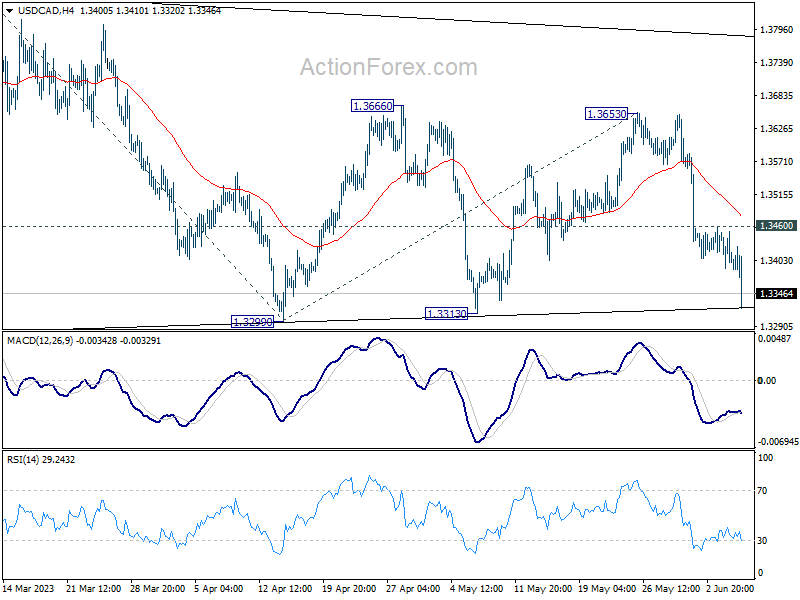

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3377; (P) 1.3415; (R1) 1.3439; More....

Immediate focus is now on 1.3299 support with today's decline. Strong support could still be seen there to rebound. Break of 1.3460 minor resistance will turn bias back to the upside for 1.3653 resistance, to extend the triangle consolidation pattern from 1.3976. However, sustained break of 1.3299 will indicate that larger corrective fall is underway, and target 100% projection of 1.3860 to 1.3299 from 1.3653 at 1.3092.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds. However, sustained break of 1.3233 will pave the way to 61.8% retracement at 1.2758.

BoC hikes 25bps, inflation concerns increased

BoC surprises the markets by raising the overnight rate by 25bps to 4.75% today. Correspondingly, the Bank Rate now sits at 5.00%, and deposit rate at 4.75%.

In the accompany statement, BoC noted that the "accumulation of evidence" reflected that monetary policy was "not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target".

The Governing Council will "continue to assess the dynamics of core inflation and the outlook for CPI inflation", in particular the "evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour".

The central bank also noted that the economy was "stronger than expected" in Q1, and " excess demand in the economy looks to be more persistent than anticipated."

Good price inflation "increased" while services price inflation "remained elevated". It continues to expect CPI inflation to east to around 3% in the summer.

However, "with three-month measures of core inflation running in the 3½-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target."

(BOC) Bank of Canada raises policy rate 25 basis points, continues quantitative tightening

The Bank of Canada today increased its target for the overnight rate to 4¾%, with the Bank Rate at 5% and the deposit rate at 4¾%. The Bank is also continuing its policy of quantitative tightening.

Globally, consumer price inflation is coming down, largely reflecting lower energy prices compared to a year ago, but underlying inflation remains stubbornly high. While economic growth around the world is softening in the face of higher interest rates, major central banks are signalling that interest rates may have to rise further to restore price stability. In the United States, the economy is slowing, although consumer spending remains surprisingly resilient and the labour market is still tight. Economic growth has essentially stalled in Europe but upward pressure on core prices is persisting. Growth in China is expected to slow after surging in the first quarter. Financial conditions have tightened back to those seen before the bank failures in the United States and Switzerland.

Canada's economy was stronger than expected in the first quarter of 2023, with GDP growth of 3.1%. Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains. Demand for services continued to rebound. In addition, spending on interest-sensitive goods increased and, more recently, housing market activity has picked up. The labour market remains tight: higher immigration and participation rates are expanding the supply of workers but new workers have been quickly hired, reflecting continued strong demand for labour. Overall, excess demand in the economy looks to be more persistent than anticipated.

CPI inflation ticked up in April to 4.4%, the first increase in 10 months, with prices for a broad range of goods and services coming in higher than expected. Goods price inflation increased, despite lower energy costs. Services price inflation remained elevated, reflecting strong demand and a tight labour market. The Bank continues to expect CPI inflation to ease to around 3% in the summer, as lower energy prices feed through and last year's large price gains fall out of the yearly data. However, with three-month measures of core inflation running in the 3½-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.

Based on the accumulation of evidence, Governing Council decided to increase the policy interest rate, reflecting our view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target. Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank's balance sheet. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is July 12, 2023. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the Monetary Policy Report at the same time.

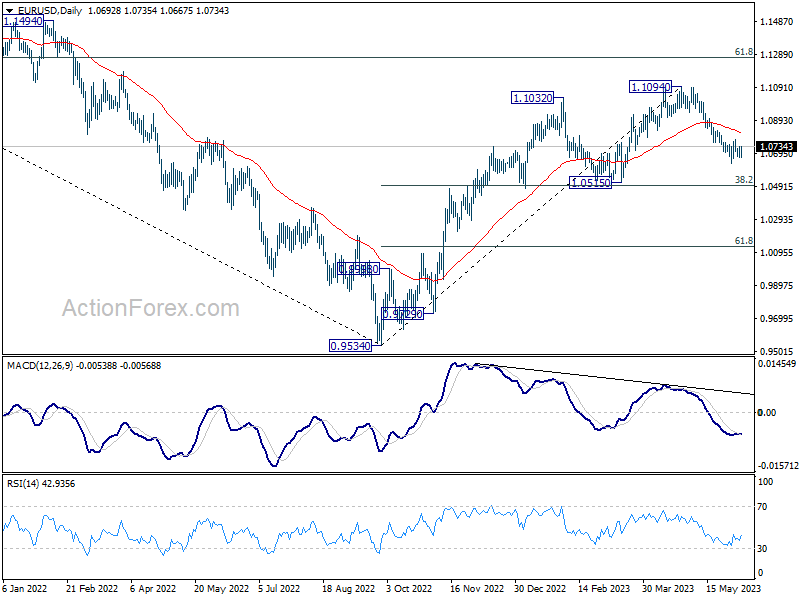

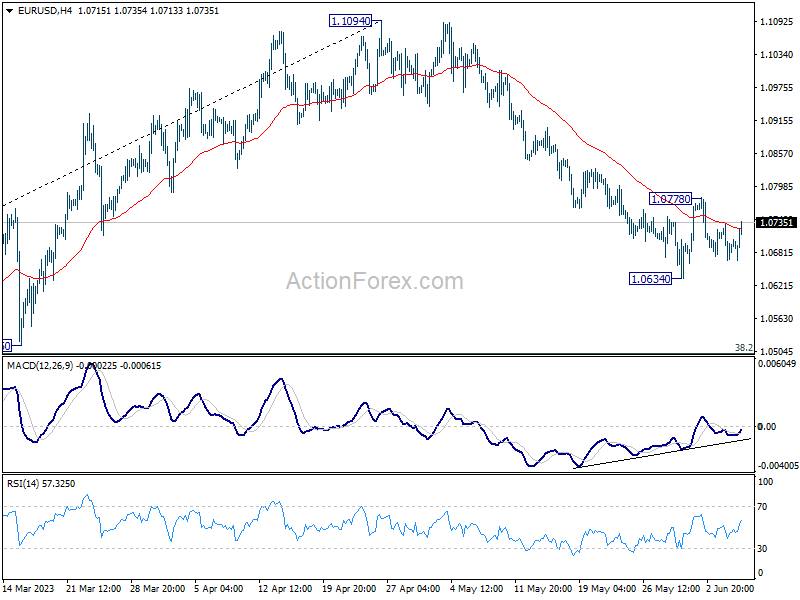

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0662; (P) 1.0698; (R1) 1.0728; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. On the downside, break of 1.0634 will resume the corrective decline from 1.1094. Deeper fall should then be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0778 will resume the rebound from 1.0634 to 55 D EMA (now at 1.0820).

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).