Sample Category Title

RBA Lowe: Some further tightening of monetary policy may be required

In a speech, RBA Governor Philip Lowe revealed further insight into the central bank's decision-making process and concerns regarding inflation. Lowe underscored RBA's decision to raise interest rates once more yesterday as an effort to confidently bring inflation back to target within a reasonable timeframe.

Governor Lowe said, "Yesterday's decision to increase interest rates again was taken to provide greater confidence that inflation will return to target within a reasonable timeframe."

He attributed this decision to a recent influx of data, suggesting "greater upside risks" to the Bank's inflation outlook. Persistent inflation in services prices, both domestically and abroad, combined with recent data on inflation, wages, and housing prices outpacing forecasts, were contributing factors.

The Governor noted, "Given this shift in risks and the already fairly drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted."

However, he also highlighted various factors the Board will monitor closely in the coming months, including developments in the global economy, domestic household spending, the growth rate in unit labour costs, and inflation expectations.

While acknowledging that the RBA remains on a narrow path, Lowe pointed out "significant risks", particularly the possibility that "inflation stays too high for too long".

He concluded, "Some further tightening of monetary policy may be required, but that will depend upon how the economy and inflation evolve. The Board will continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market."

First Impressions: Australian Q1 GDP

Australia’s economy grew by a tepid 0.2% in the quarter. Consumer spending remains soft, up 0.2%, with high inflation and higher interest rates leading to a fall in real household disposable income, down 0.3%. Domestic demand rose 0.6%, led by business investment and public demand.

The Australian economy expanded by a tepid 0.2% in the March quarter.

That was broadly as anticipated, Westpac 0.3% and market median 0.3%, range (0.1% to 0.6%).

Annual growth is 2.3%. The level of activity is 7.4% above that prior to the pandemic, at the end of 2019.

Key surprise: The key downside surprise, the statistical discrepancy subtracted 0.1ppt from activity in the period – i.e. the income and production estimates of GDP at 0.2% were a fraction softer than the expenditure measure, which grew by 0.3%, meeting expectations.

Total inventories were also a fraction softer, printing flat, with a slightly larger drag from farm than allowed for (-0.1ppt vs a forecast -0.05ppt). While domestic demand was a little stronger, at +0.6% vs an expected +0.4%.

Consumer spending grew by a sluggish 0.2% in the quarter, little changed from the 0.3% increase the period prior. That represents a slight upside surprise from our latest expectation for a flat result.

The detail shows the gain centred on services with other components recording declines.

Around incomes, the picture was mixed.

Nominal wage incomes grew by a robust 2.4%; nominal gross household income increased by 1.7%; nominal gross disposable income (after interest payments and taxes etc) expanded by 0.8% (a rebound from the -0.7% decline the quarter prior); and real gross disposable income is weak, declining by 0.3%, but again that was a marked improvement on a -2.2% for the December quarter. Consumer prices increased by 1.2%, a moderation on 1.5% for the previous quarter.

The household saving ratio continues to trend lower, declining from 7.1% in the September quarter to 4.4% in December and then 3.7% in March – with the past two outcomes below the “equilibrium”, judged to be around 6%. The period of “excess savings”, which was a feature during the pandemic, has ended. Households are now drawing down on the savings buffer to support spending.

Hours worked: The National Accounts estimate that hours worked expanded by 0.6%qtr and 7.1%yr. The Labour Force survey estimated that hours work declined by -0.2% in the March quarter.

Expenditure detail:

Domestic demand grew by 0.6% in the March quarter, representing an upside surprise and a rebound from the broadly flat outcome for the December quarter (a +0.1%, revised up from flat).

Net exports subtracted a modest 0.2% from activity, with strong imports, +3.2%, outpacing a 1.5% lift in exports (centred on services).

Total inventories were neutral in the period, with a 0.3ppt contribution from private non-farm offset by farm and public authorities.

Home building activity declined by -1.2%, with falls in new dwelling construction and renovations (with the latter weaker than the quarterly partial).

The real estate sector – in the form of Ownership Transfer Costs (turnover in the property sector) – declined by a further 5%, to be 22% lower over the year as rapid interest rate rises bite.

Business investment increased by solid 2.9%, including a 4.9% increase in equipment spending and a 3.1% rise in infrastructure (with the growing pipeline pointing to some further upside in this segment).

Public demand has been cresting at a high level as the spike in covid related spending unwinds. In the March quarter, on a strong showing from investment (centred on construction, which has further upside) +4%, total public demand grew by 0.8%.

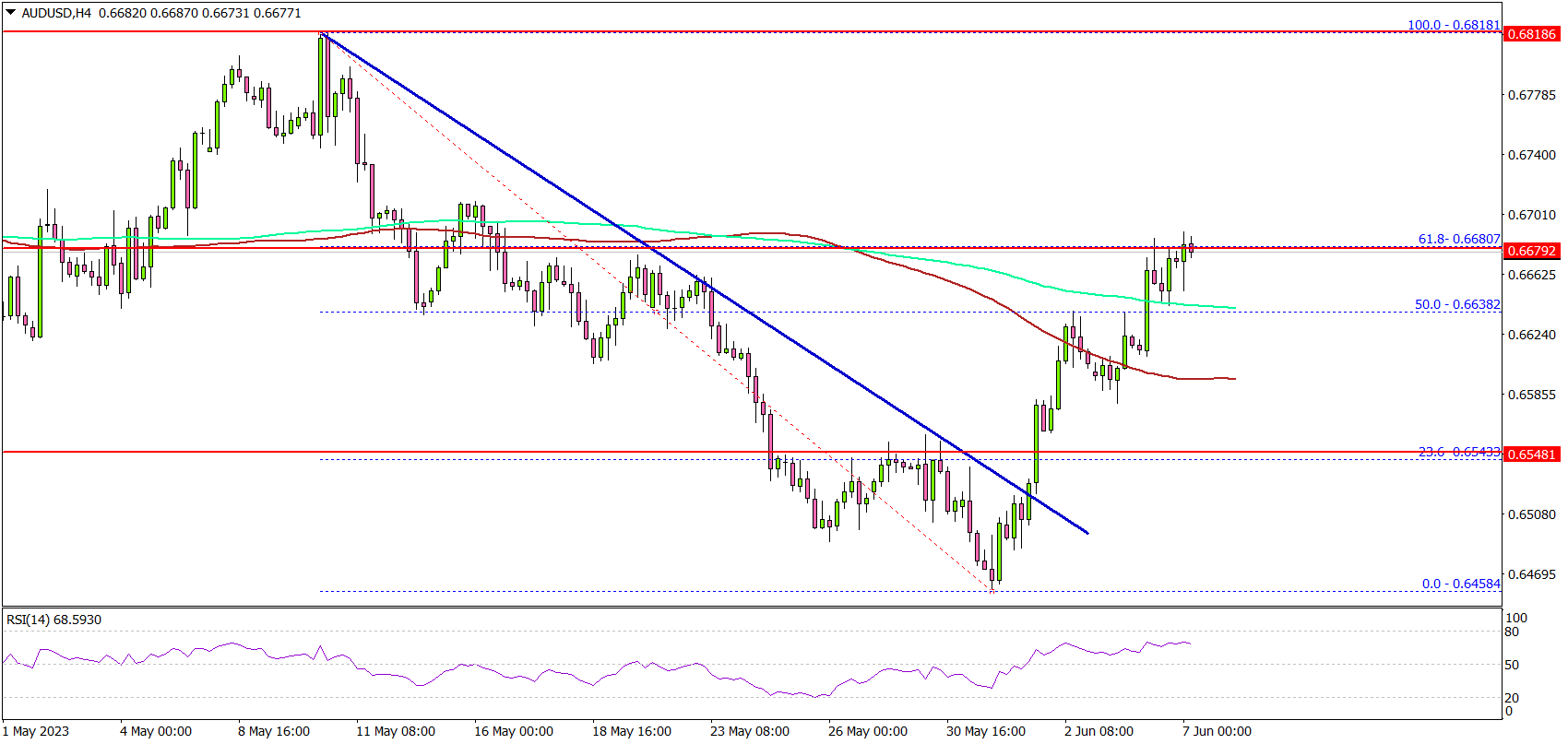

AUD/USD Eyes Steady Increase To 0.6800

Key Highlights

- AUD/USD is moving higher above the 0.6550 resistance.

- It broke a major bearish trend line with resistance near 0.6510 on the 4-hour chart.

- EUR/USD is still struggling to start a recovery wave above the 1.0780 resistance.

- The BoC interest rate decision is scheduled today (forecast 4.5%, versus 4.5% previous).

AUD/USD Technical Analysis

The Aussie Dollar found support near the 0.6460 zone against the US Dollar. AUD/USD started a fresh increase and was able to clear the 0.6500 resistance.

Looking at the 4-hour chart, the pair broke a major bearish trend line with resistance near 0.6510. There was a close above the 100 simple moving average (red, 4 hours). The bulls pushed the pair above the 50% Fib retracement level of the downward move from the 0.6818 swing high to the 0.6458 low.

It is now trading above the 200 simple moving average (green, 4 hours) and testing the 76.4% Fib retracement level of the downward move from the 0.6818 swing high to the 0.6458 low.

If there is a move above the 0.6680 resistance, the pair could drift toward 0.6750. The main resistance is near 0.6800, above which the pair might rise steadily.

If there is no wave above 0.6680, the pair could dip toward 0.6620. The next major support is near the 0.6550 level. If there is a downside break below the 0.6550 support, the pair could decline toward the 0.6500 support.

Looking at EUR/USD, the pair is now consolidating losses and still facing a lot of hurdles near the 1.0780 level.

Economic Releases

BoC Interest Rate Decision – Forecast 4.5%, versus 4.5% previous.

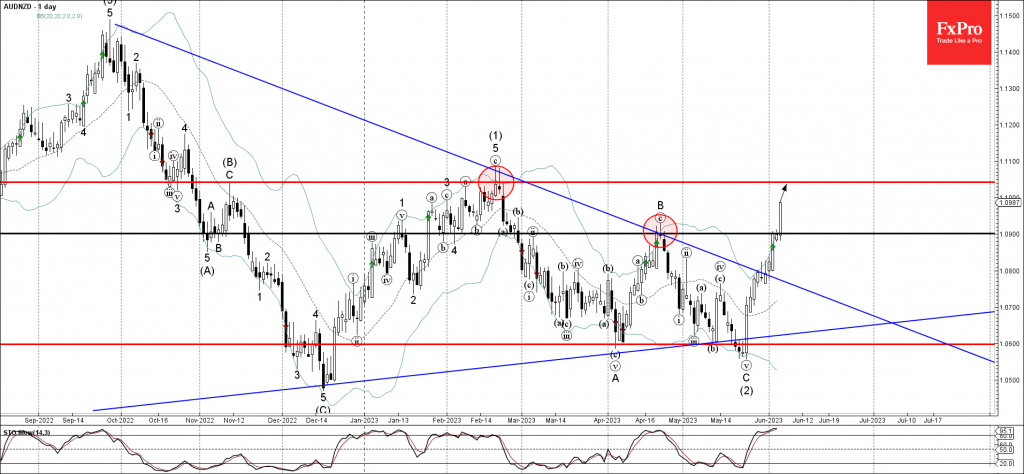

AUDNZD Wave Analysis

- AUDNZD broke resistance level 1,0900

- Likely to rise to resistance level 1.1045

AUDNZD under the bullish pressure after the price broke above the pivotal resistance level 1,0900 (which has been reversing the price from the start of March).

The breakout of the resistance level 1,0900 was preceded by the breakout of the weekly Triangle from last September.

AUDNZD can be expected to rise further toward the next resistance level 1.1045 (top of the previous waves (B) and (1)).

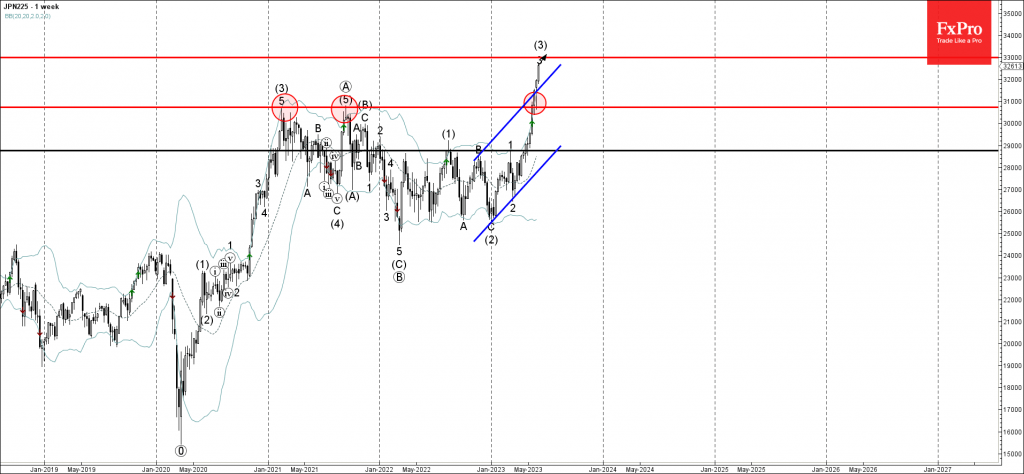

Nikkei 225 Wave Analysis

- Nikkei 225 broke long-term resistance level 30735.00

- Likely to rise to resistance level 33000.00

Nikkei 225 index continues to rise sharply after the price broke through the major long-term resistance level 30735.00 (former Double Top from 2021).

The breakout of the resistance level 30735.00 coincided with the breakout of the weekly up channel from last year, which accelerated the active impulse waves 3 and (3).

Given the strong weekly uptrend, Nikkei 225 can be expected to rise further toward the next resistance level 33000.00.

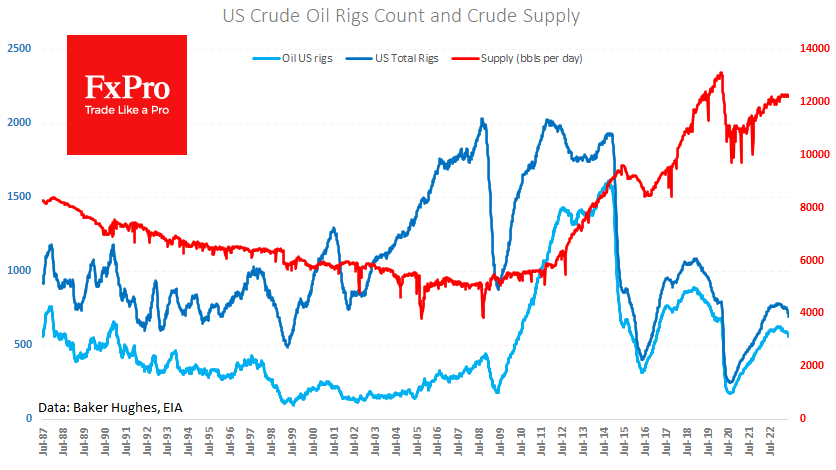

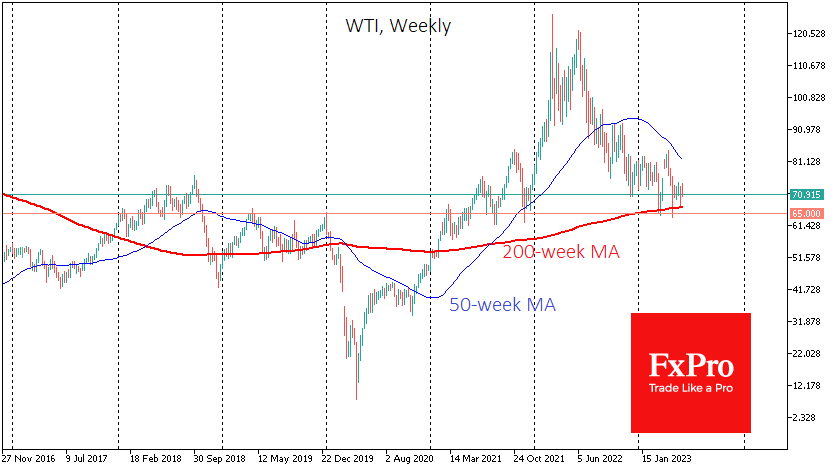

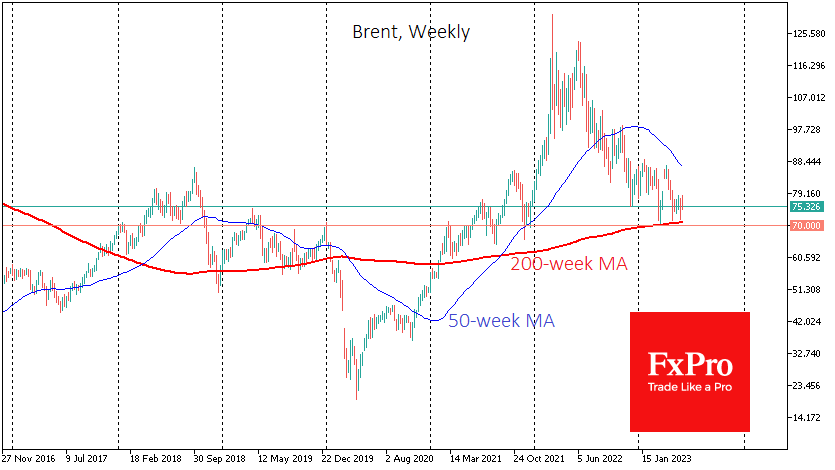

Is a Big Oil Slump Brewing?

Oil started the week with a 2.5% jump, picking up on news of Saudi Arabia’s surprise decision to voluntarily cut production by 1M BPD. In addition, OPEC+ agreed to Russia’s production cut from next year.

These measures look like an impressive attempt to increase energy prices, giving traders a sense of increased energy shortages for at least the coming quarters.

On the US side, news on production levels is also working to support this perception. The latest data from Baker Hughes noted a drop of 15 oil production rigs to 555 – the lowest since April 2022.

Since the start of the year, US production has been close to 12.2M BPD, which is only a modest 2.5% higher than exactly a year ago. Thus, US producers are in no hurry to take the market share that Saudi Arabia and Russia are willing to give up. There are two reasons for this.

Firstly, producers need to be more impressed by prices. Technically, they are near the 2018 peak, which is not low by historical standards. But here, one must add significantly higher market interest rates and a pronounced green agenda of financial institutions.

Secondly, the apathy of the major oil producers could result from lower demand in key areas, forming a bearish market environment.

Judging by the fact that WTI closed the gap before the end of Monday and lost another 1.8% on Tuesday, traders in the market are leaning towards the second scenario, which makes us assume a further downside in the price.

On the other hand, Saudi Arabia has stepped up its efforts to cut production as soon as the price of Brent drops to around $71 and WTI touches $65. Therefore, downside play is worth being cautious when approaching these levels.

That said, a breakout of these levels could look like a capitulation and trigger a big sell-off, like those in 2014 and 2020, when oil producers lost coordination. Technically, these levels coincided with price consolidation under the 200-week average. The market has already tested these levels ($67/bbl. WTI and 70.80/bbl. Brent) but bounced back.

Sunset Market Commentary

Markets

This morning’s hawkish rate hike by the Reserve Bank of Australia was set to be today’s sole highlight. The central bank unexpectedly raised its policy rate for a second meeting running by 25 bps after installing a pause back in April (Fed, are you listening?). On top, they worry more over upside inflation risks. This might even require some further tightening of policy in the future. The market impact remained restricted to Australian markets despite potentially being a global example. AUD/USD reached its strongest level since the start of the USD-comeback mid-May (0.6685). AUD swap yields added up to 7.4 bps at the front end (2y) with money markets almost completely discounting another 25 bps rate hike by the September meeting.

The eco & event calendar looked extremely dull in Europe and the US, but the ECB’s April Consumer Expectations’ Survey results caught investors by surprise. Although outdated, they managed to nonetheless trigger a market reaction as consumer inflation expectations decreased significantly, reversing most of the increases seen in Q1 this year. The median rate of perceived inflation over the previous 12 months decreased to 8.9% in April 2023, from 9.9% in March. Median expectations for inflation over the next 12 months decreased to 4.1% in April, from 5% in March, and those for inflation three years ahead decreased to 2.5%, from 2.9% in March. Uncertainty about inflation expectations 12 months ahead also decreased. Economic growth expectations for the next 12 months were less negative in April, standing at -0.8% compared with -1% in March. Expectations for the unemployment rate 12 months ahead decreased to 11.2% in April, from 11.7% in March. In the run-up to next week’s ECB meeting, markets obviously zoomed in on the inflation expectations component. While they don’t doubt the ECB’s commitment at the June and July policy meetings, it could result in a more balanced tone by ECB Lagarde at the Q&A session afterwards. German Bunds outperform US Treasuries today with German yields losing up to 4.7 bps at the front end of the curve. Daily US yield changes vary between +1.1 bp (30-yr) and +3.8 bps (2-yr). Loss of interest rate support pulls EUR/USD back below 1.07 (1.0677 currently) with EUR/GBP copying the move to a lesser extend (0.8608). Risk sentiment on stock markets is mildly negative.

News & Views

According to Czech statistical office (CZSO), industrial production in real terms declined 1.9% M/M to be 1.2% higher compared to the same month last year (WDA). According to CZSO ‘the April result of industry was mainly influenced by last year’s low comparison basis in manufacture of motor vehicles. The number of economic activities of industry in which production increased, year-on-year, decreased again. Manufacturing of motor vehicles and trailers increased by 30% Y/Y, but declined 5% M/M. Y/Y production also increased in electrical equipment, in repair and installation of machinery and equipment and in pharmaceutical products. New orders at current prices increased 2.7% Y/Y. Non-domestic orders declined 1.6% Y/Y, but domestic orders increased by 11.3%. Again the rise was mainly due to a low comparison base in the automotive industry last year. The average registered number of employees in industry decreased by 1.7% Y/Y. Their average gross monthly nominal wage increased 9.6% Y/Y. Other data also showed a further decline in construction output (-3.4% M/M and 6.4% Y/Y). Despite mediocre activity data, the Czech koruna remains well bid near EUR/CZK 23.51.

Hungarian retail sales suggest ongoing sluggish domestic demand. Alongside a significant base effect from last year, sales were 12.6% lower in April compared to the same month last year. Sales declined 8.6% Y/Y in food shops, by 10.7% in non-food shops and by 22.9% in automotive fuel retailing. Despite the domestic slowdown, the Hungarian forint holds near recent peak levels (EUR/HUF 368.5). The MNB last month started reducing the O/N deposit rate from 18% to 17%. In the view of the Hungarian central bank this was mainly inspired by a return of financial stability on Hungarian markets (including a solid performance of the forint) rather than by monetary policy considerations (inflation) or as a means to support demand.

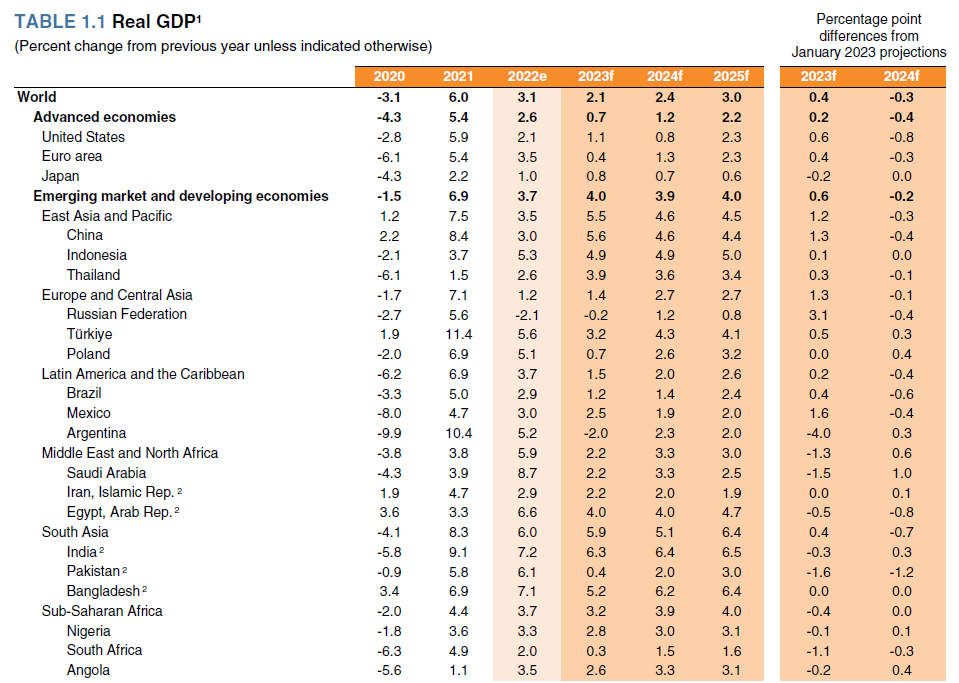

World bank upgrades 2023 global growth forecast to 2.1%

In the latest Global Economic Prospects, World Bank raised 2023 global growth forecast to 2.1%, from January's projection of 1.7%. Nevertheless, growth forecast for 2024 was downgraded from 2.7% to 2.4%. Growth is expected to accelerate further to 3.0% in 2025.

"Growth over the rest of 2023 is set to slow substantially as it is weighed down by the lagged and ongoing effects of monetary tightening, and more restrictive credit conditions," the report said.

"These factors are envisaged to continue to affect activity heading into next year, leaving global growth below previous projections."

EUR/USD Recovers Amid U.S. Debt and Employment Shifts

The most heavily traded currency pair, EUR/USD, experienced a rebound to 1.0720 following a significant downturn.

The concerns about U.S. public debt subsided after the proposal to increase the debt limit was endorsed first by the House of Representatives, followed by the Senate and the White House. This resolution was widely anticipated and successfully prevented a halt to federal government operations.

U.S. employment statistics for May presented a mixed picture. Non-farm payrolls (NFP) rose more than expected, surging by 339 thousand, which was welcome news. However, the average wage increase was modest, ticking up by a mere 0.3% month on month. This modest wage growth served to limit market dynamics.

Currency markets are now focusing their attention on the upcoming Federal Reserve meeting scheduled for next week. Investors are eager to know the Fed's stance: Will it pause its interest rate hike, or will the cycle continue? The market consensus on this matter remains divided.

On a 4-hour chart (H4), EUR/USD corrected to 1.0762. The market is currently forming a downward impulse to 1.0666. Once this level is reached, an uptick towards 1.0735 may occur. Essentially, a consolidation range could form above 1.0666. An upward breakout from this range could trigger a correction towards 1.0830. Alternatively, a downward breakout could continue the bearish trend down to 1.0596. This technical scenario is supported by the Moving Average Convergence Divergence (MACD) indicator. Its signal line is below zero and poised for an upward move to test from below, followed by a potential drop to new lows.

On the 1-hour chart (H1), EUR/USD is forming a downward wave structure towards 1.0666. Upon reaching this level, a corrective move towards 1.0700 may occur, followed by a drop to 1.0616. From this point, the bearish trend could persist down to 1.0573. This technical scenario is validated by the Stochastic oscillator. Its signal line is currently near the 50 level and could break lower, potentially declining to 20.