Sample Category Title

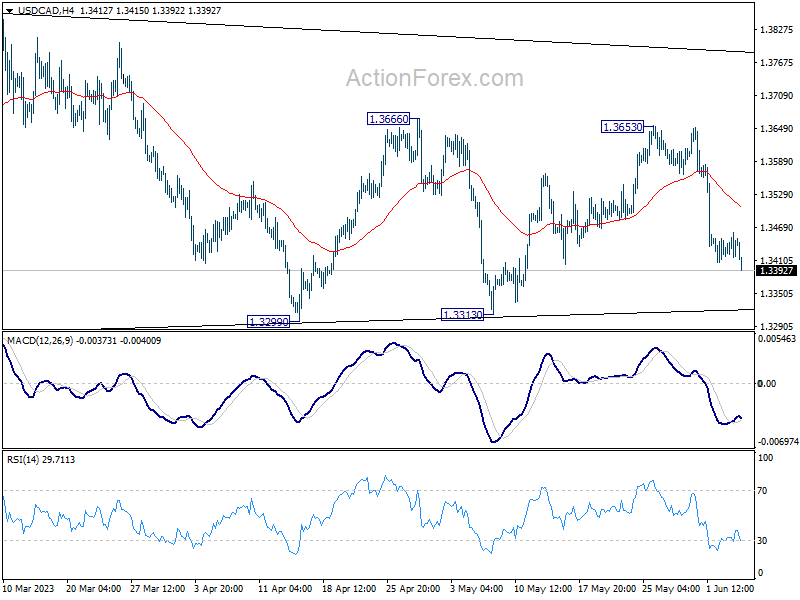

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3421; (P) 1.3441; (R1) 1.3465; More....

Range trading continues in USD/CAD and outlook is unchanged. Price actions from 1.3976 are seen as a triangle consolidation pattern. Above 1.3666 will target 1.3860 resistance first. Firm break of 1.3860 will argue that larger up trend is ready to resume through 1.3976 high. Nevertheless, sustained break of 1.3229 will dampen this view and turn near term outlook bearish.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds.

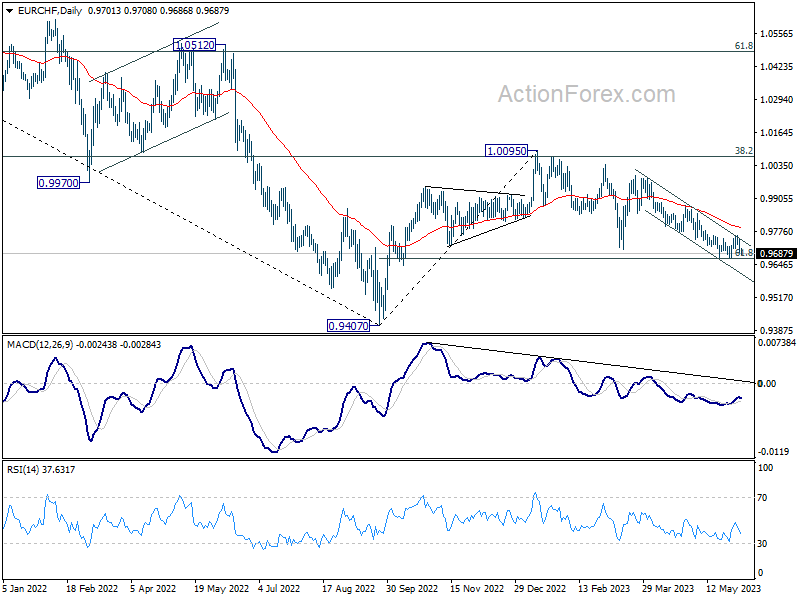

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9686; (P) 0.9719; (R1) 0.9740; More...

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. On the upside, firm break of 0.9760 should confirm short term bottoming after hitting 61.8% retracement of 0.9407 to 1.0095 at 0.9670. Intraday bias will be back on the upside for 0.9878 resistance next. However, sustained break of 0.9670 will extend the whole decline from 1.0095 towards 0.9407 low instead.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9938). Down trend from 1.2004 (2018 high) is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

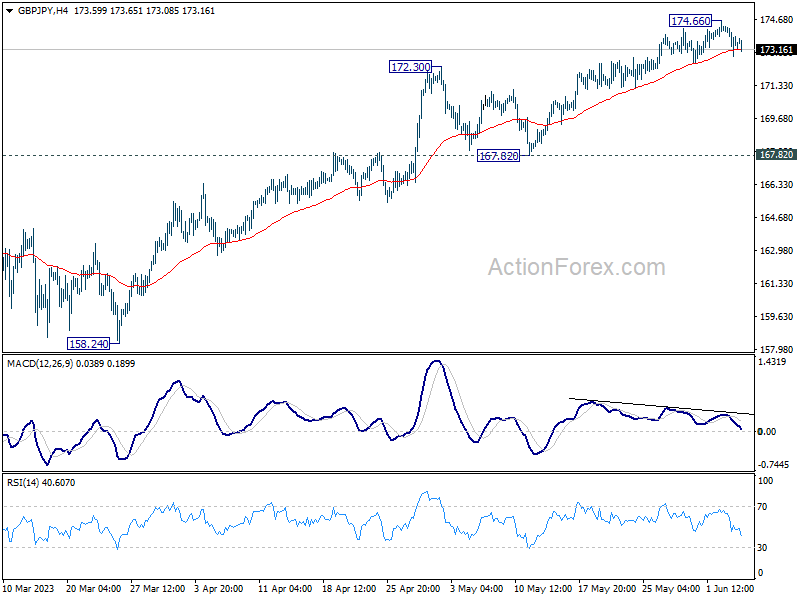

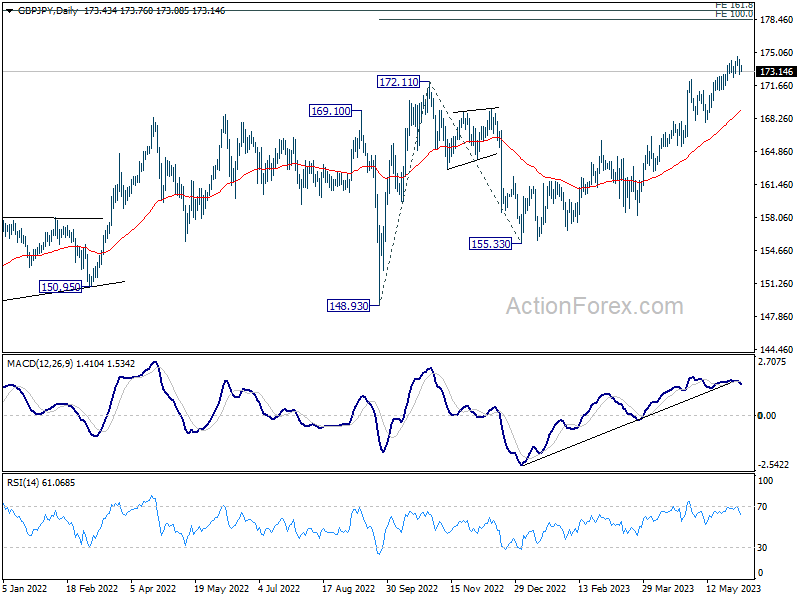

GBP/JPY Daily Outlook

Daily Pivots: (S1) 172.81; (P) 173.61; (R1) 174.35; More...

Intraday bias in GBP/JPY is turned neutral with current retreat. Deeper pull back cannot be ruled out, but outlook will stay bullish as long as 167.82 support holds. Break of 174.66 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. For now, medium term outlook will remain bullish as long as 165.99 resistance turned support holds, even in case of deep pull back.

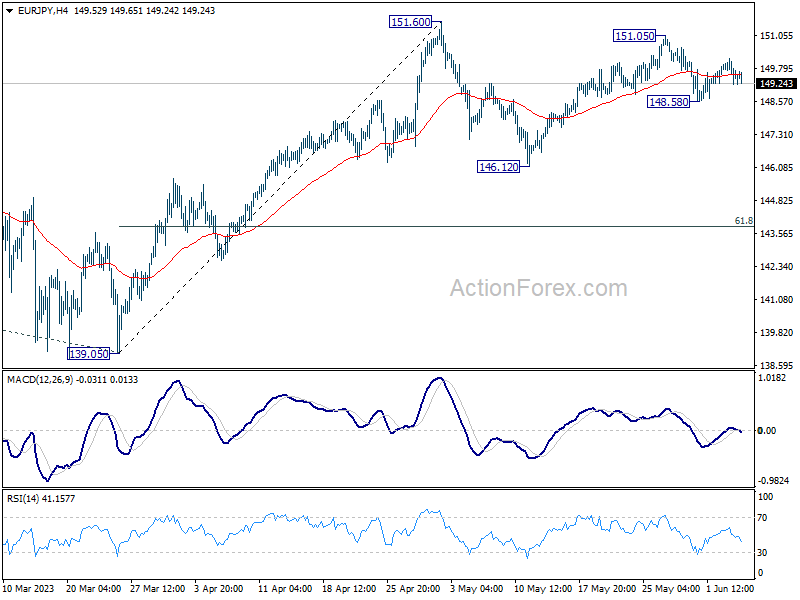

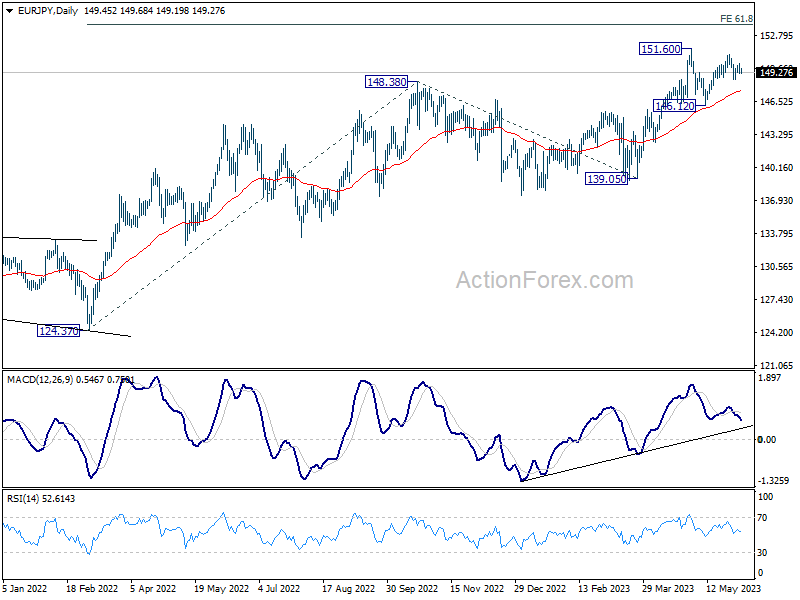

EUR/JPY Daily Outlook

Daily Pivots: (S1) 149.11; (P) 149.65; (R1) 150.07; More....

EUR/JPY is staying in tight range of 148.58/151.05 and intraday bias remains neutral first. On the downside, below 148.58 temporary low will extend the corrective pattern from 151.60 with another falling leg. Deeper fall would be seen to 146.12 support and possibly below. On the upside, however, above 151.05 will target 151.60 high. Firm break there will resume larger up trend to 153.64 projection level.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 139.05 support holds, even in case of deep pull back.

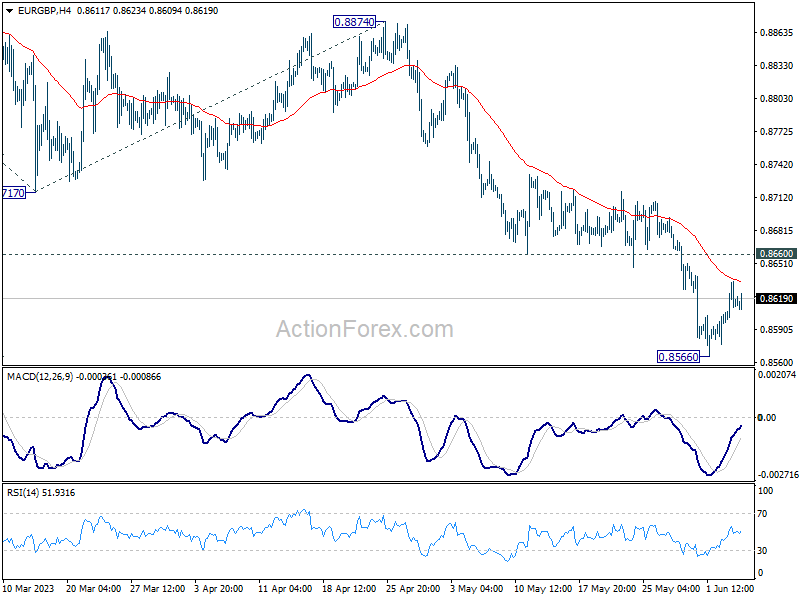

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8595; (P) 0.8615; (R1) 0.8637; More....

EUR/GBP's consolidation from 0.8566 is still extending and intraday bias remains neutral. Upside of recovery should be limited by 0.8660 support turned resistance and bring another fall. Break of 0.8566 will resume the fall from 0.8977, and target 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. Nevertheless, firm break of 0.8660 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, current development argues that whole decline from 0.9267 (2022 high) is still in progress. This is part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen through 0.8545 support. This will now remain the favored case as long as 0.8717 support turned resistance holds.

AUD Short-Term Bulls Supported by Hawkish RBA and China

- RBA surprised again with a 25-bps hike to raise the official cash rate to 4.10%

- Rumoured China’s property market stimulus measures also created a positive feedback loop back into AUD/USD.

- Short-term minor uptrend in place for AUD/USD with key resistance to watch at 0.6790.

The Aussie dollar has been resilient against the US dollar since last Friday, 2 June ex-post better the expected US non-farms payroll/jobs data for May. The AUD/USD has managed to stage a rally of +1.45% to today’s 6 June current intraday level of 0.6662 at this time of the writing from last Friday’s low that has outperformed the EUR/USD (+0.16%) and GBP/USD (+0.05%) over the same period.

There are several short-term positive factors that are supporting this minor AUD/USD resilient condition.

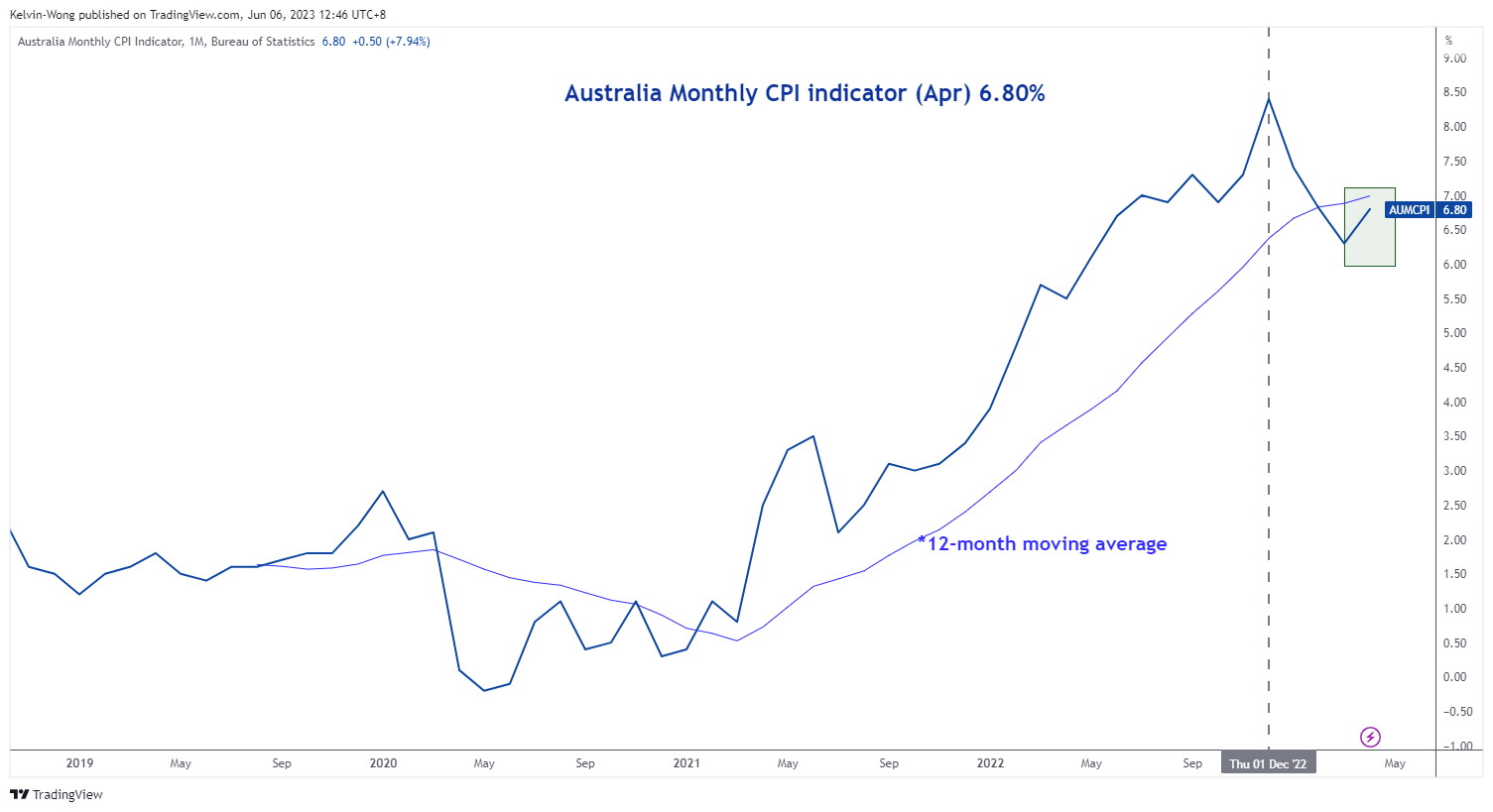

Australian inflation condition remains sticky

Fig 1: Australia’s Monthly CPI Indicator as of Apr 2023 (Source: TradingView, click to enlarge chart)

The recent release of a more advanced monthly CPI indicator for April released last week has indicated an uptick in inflationary pressures; accelerated to 6.8% in the year to April 2023 from a gain of 6.3% gain the year to March 2023, the first increase in annual inflation since last December 2022 and almost reverted back to the 12-month moving average now at 6.99%.

In addition, the latest Melbourne Institute Monthly Inflation Gauge report was released yesterday, 5 June showed prices accelerated to a four-month of 0.9% month-on-month in May, above 0.2% printed in April and 0.2% forecasted. This report estimates month-to-month price movements for a wide range of goods and services across the capital cities of Australia. It aims to provide financial markets and policymakers with regular updates on trends in inflation.

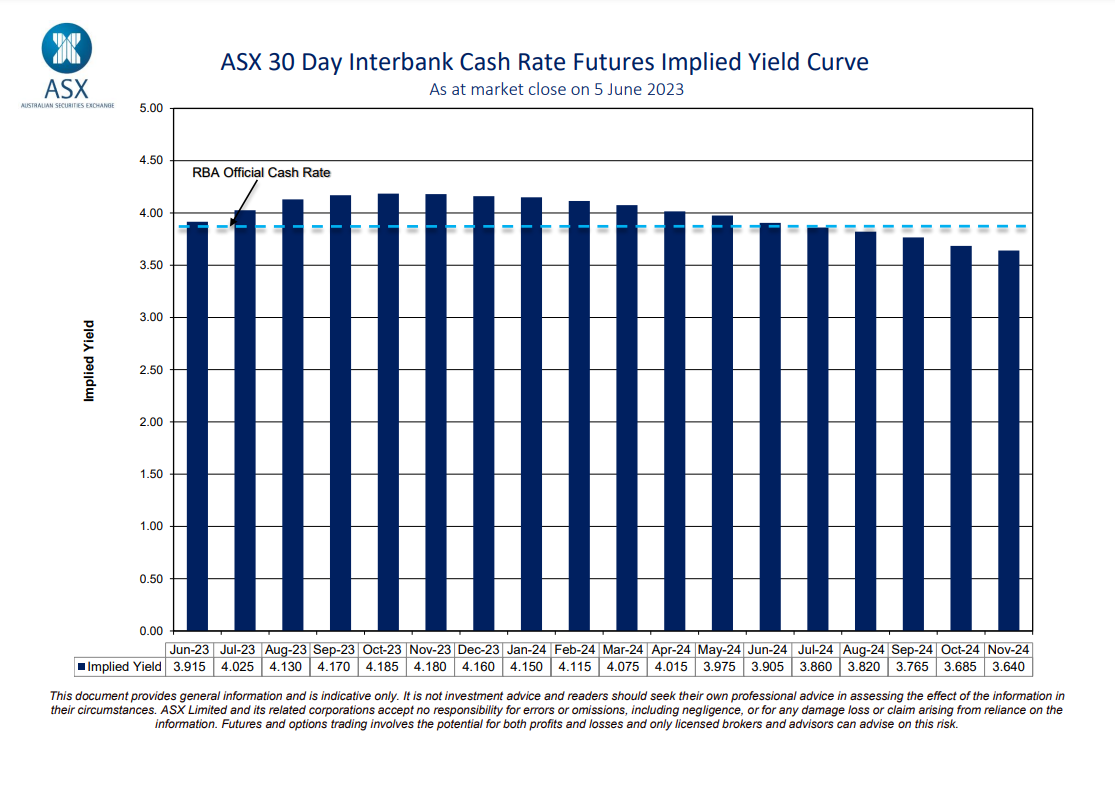

RBA surprised with a 25-bps rate hike again

Fig 2: ASX 30-day interbank cash futures implied yield curve as of 5 Jun 2023 (Source: ASX RBA Rate Tracker, click to enlarge chart)

Hence, this latest set of key economic data has shown that the inflation condition in Australia remains “hot” where the central bank, RBA may choose to maintain its restrictive and tight monetary policy.

As of 5 June, the ASX 30-day interbank cash rate futures for the June 2023 contract have priced in a 33% chance of a 25-bps hike today to the OCR which was a stark contrast to a week ago when the expectations were “no change”.

Indeed, the RBA has surprised the market again today (for the second consecutive month) with 25 basis points (bps) hike to bring the official cash rate to 4.10%; it has lifted rates for the 112th time in the past year and pushed borrowing costs to their highest level since April 2012.

The latest stance from RBA has indicated that rates are expected to stay longer than expected as sticky elevated inflationary concerns outweigh the risk of a liquidity crunch that can dampen growth prospects in the medium-term.

Positive animal spirits back in China’s stock market

In light of the recent dismal key leading economic data out from China, there have been media reports last Friday, 2 June that speculated that China’s top policymakers are working on a new basket of measures to support the faltering property market after existing policies failed to sustain a rebound and stabilize the property sector. Potential stimulative measures include a reduction in mortgage down payment in non-core neighbourhoods of major cities and further relaxation in the restrictions for residential purchases.

This potential impending stimulative measure has triggered a sudden positive reversal in China-related benchmark stock indices since last Friday. The Hong Kong China Enterprises Index (HSCEI) has rallied by +4% from last Friday’s low to today’s intraday level of 6,521 at this time of the writing and staged two consecutive prior weekly returns of +1.50% and +1.45% respectively, the best performance seen in the past two months.

Thus, this positive feedback loop has managed to spill over to the Aussie dollar given that Australia is one of the top trading partners of China.

AUD/USD Technical Analysis – Short-term minor bullish trend intact

Fig 3: AUD/USD minor trend as of 6 Jun 2023 (Source: TradingView, click to enlarge chart)

The price actions of AUD/USD have involved into a minor ascending channel in place since the 1 June 2023 minor swing low of 0.6460.

Short-term bullish momentum has resurfaced with a breakout above the 20-day moving average ex-post RBA monetary policy decision. Key short-term pivotal support to watch will be at 0.6600 and a clearance above 0.6710 sees the key medium-term range resistance coming in at 0.6790.

On the flip side, failure to hold above 0.6600 exposes the next support at 0.6460.

Reserve Bank of Australia Raised Policy Rate Further by 25 bps

Markets

A disappointing US non-manufacturing ISM was yesterday’s defining moment for FI and FX trading. Up until the release, the post-payrolls momentum still pushed US rates and the dollar gently higher. Afterwards, intraday fortunes changes, the first Pavlov reaction didn’t really gain traction afterwards. Turning to the data first, the ISM fell from 51.9 to 50.3, holding just north of the 50 boom/bust market. With the exception of Dec2022, it was the weakest reading since May 2020, undershooting the consensus estimate (pick-up to 52.4) as well. Deteriorating services sentiment is something to keep a close eye on as this sector kept global economies humming over the past months. Details didn’t offer much hope with inventory building (58.3 from 47.2) and inventory sentiment (61 from 48.9) being the sole factors preventing a drop in contraction territory. Overall business activity moderated from 52 to 51.5 with new orders down to 52.9 from 56.1. The order backlog is gone (40.9 from 49.7). Employment declined from 50.8 to 49.2. Prices paid extended their disinflationary trend (56.2 from 59.6). The market reaction was orderly overall. US yield lost 0.2 bps (30-yr) to 3.3 bps (2-yr) in the end, hiding an intraday decline in the high single digits. German Bunds underperformed significantly with yields adding 5.5 bps (30-yr) to 7.9 bps (2-yr). They had some catching up to do with the end of last week’s WS session, gapped higher at the open on rising energy prices and barely felt the impact from the non-manufacturing ISM. The trade-weighted dollar closed at 104 from an open at 104.04 and an intraday peak at 104.40. EUR/USD followed a similar intraday pattern eventually ending barely unchanged at 1.0713 coming off an intraday bottom at 1.0675.

This morning’s RBA decision (see below) was today’s main dish and a reminder to central banks and markets globally that the inflation battle isn’t easily won. It sets the tone for the start of trading with core bonds again trading on the weaker side. Mixed Asian risk sentiment offers little guidance further out. The single currency gets some interest rate backing which it missed for most of the month May. EUR/USD changes hands at 1.0729 with the May low/1st support (1.0635) starting to look more solid. Today’s eco calendar contains no events/data worth mentioning.

News and views

The Reserve Bank of Australia raised its policy rate further by 25 bps to 4.1%. A majority of analysts expected an unchanged decision after the RBA already restarted hiking rates last month. The RBA assumes that inflation has passed its peak, but at 7% it is still much too high. Recent data also indicated that upside risks to the inflation outlook have increased. Today’s hike should provide greater confidence that inflation will return to the target within a reasonable time frame. Growth in Australia has slowed and conditions on labour market have eased but remain very tight. Wage growth also has picked up in response to the tight labour market and high inflation. In this respect the RBA Board remains alert to the risk that expectations of ongoing high inflation contributes to larger increases in both prices and wages, especially given the limited spare capacity in the economy and the still very low rate of unemployment. The board concludes that some further tightening of monetary policy may be required. The 2-y Australian government yield jumps 9 bps, setting a new cycle top near 3.85%. The Aussie dollar gains about 1 bp after the decision with AUD/USD changing hands near 0.6675.

Japanese wages grew less than expected/hoped for in April. Labour Cash earning rose 1% Y/Y down from 1.3% Y/Y in March. The April data are the first wage data series after the labour spring negations (Shunto). However it might take some time to see the full impact of the wage negotiations in the coming months. Real cash earnings even were 3% lower compared to the same period last year. Consumer spending data for April also disappointed printing 4.4% lower compared to the same month last year. Today’s soft wage data probably won’t inspire the BOJ to change its easy policy anytime soon. The 10-y Japanese government bond yield trades little changed near 0.43%. USD/JPY is losing a few ticks, but this probably mainly mirrors USD softness

GBP Attempts to Bounce

GBP/USD tests support

The US dollar retreated after May’s services PMI came in short of expectations. The pair came under pressure at a 12-month high of 1.2670 then a series of lower lows led recent buyers to leave the market, leaving a dent on the upward impetus. The latest surge hit stiff selling pressure at 1.2540 and a drift below 1.2400 suggests weak follow-through interest, turning 1.2480 into a fresh resistance in the process. 1.2370 is a key zone to keep the price afloat as its breach would trigger a new round of sell-off below 1.2300.

EUR/JPY consolidate gains

The euro steadies as Christine Lagarde reiterated that inflationary pressures remained strong. A brief dip below 148.80 has shaken out some weak hands but sentiment remains rather solid. The price action on the daily chart indicates a lingering bullish pressure as it bounces off the 20-day SMA (148.60). 150.40 is the closest resistance and a breakout would lift offers to last month’s high peak of 151.50, potentially resuming the uptrend. On the downside, 148.60 is a major support in case the single currency struggles to bounce.

DAX 40 seeks support

The Dax 40 slipped after the ECB president signalled more rate increases to come. A swift rebound from the mid-April consolidation zone around 15700 has put the index back on track, with a break above the swing high of 16060 undercutting the short interests and prompting sellers to cover their positions. The support-turned-resistance of 16160 near the recent peak would be the last hurdle before a bullish continuation above the all-time high of 16330. 15860 is the first support as the RSI returns to the neutral area.

$3500 per Headset

Crude oil fully pared post-OPEC gains yesterday, as Saudi’s lonely production cuts and the quota transfer from African countries to UAE raised question about the hit-power and the health of the cartel.

As a result, the barrel of American crude fell below the $72pb mark. The risks are now tilted to the downside because the OPEC meeting was the major upside risk for oil bears and it’s cleared for now.

Oil stocks kicked off the week on a depressed note. Exxon tested the 200-DMA yesterday but failed to clear resistance amid the very short-lived post-OPEC oil rally. Exxon closed Monday’s session 0.44% lower, and Chevron lost 0.48%. Still, it’s more interesting to have a positive exposure to oil stocks than to oil itself, as oil companies accumulated a big amount of cash during the post-pandemic and Ukrainian war months, and they can simply acquire smaller rivals to boost revenue and growth.

$3500 per headset

Apple revealed its much-expected VR headset yesterday, just after its stock price hit a record, but the $3500 headset failed to convince investors that it will be the next big thing. It’s too expensive to democratize and rivals’ efforts haven’t paid much so far. Giving a fancy design to a product of little-interest may not be the next big thing for Apple.

Elsewhere in tech, Nasdaq 100 is up by more than 35% since the start of this year, and according to a Deutsche Bank report the volume of call-option buying in tech and Mega Cap Growth stocks is now approaching the highest levels of the pandemic era – despite the Federal Reserve’s (Fed) 500bp rate hike, and its pledge to do more. For now, there is no major sign of a reversal in appetite for Big Tech.

But we have signs that the major central banks are not done surprising to the hawkish side just yet. The Reserve Bank of Australia (RBA) hiked the interest rates by 25bp to 4.10% at today’s meeting, defying economists’ expectations of status quo. ‘Fighting inflation’ remains the primary focus, the bank said. The AUDUSD jumped past the minor 23.6% retracement on February-May retreat and cleared the 50-DMA at 0.6660. The surprise hawkish move, along with a rebound in iron ore price could further support the positive move and send the pair above its 200-DMA, which stands a touch below the 67 cents level.

Another scandal?

Bitcoin fell more than 5% yesterday after the SEC accused Binance and its CEO Zhao of being ‘engaged in an extensive web of deception, conflicts of interest, lack of disclosure and calculated evasion of the law’. Big cryptocurrency institutions’ misfortune could shake the market, but the cryptocurrencies, themselves, remain impressively resistant to scandals in crypto exchanges, and price dips could be interesting opportunities to buy the assets.

In the medium run, rising interest rates pause a higher risk to cryptocurrency valuations than another crypto-exchange scandal.

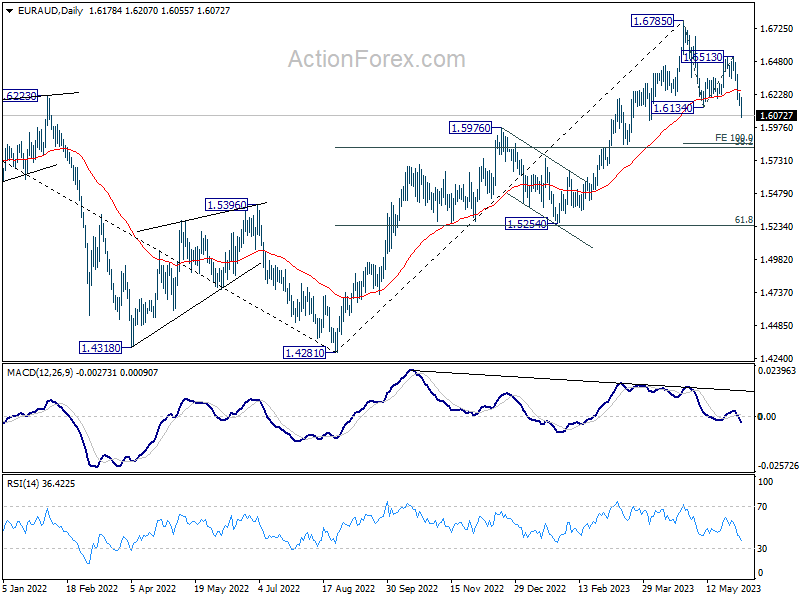

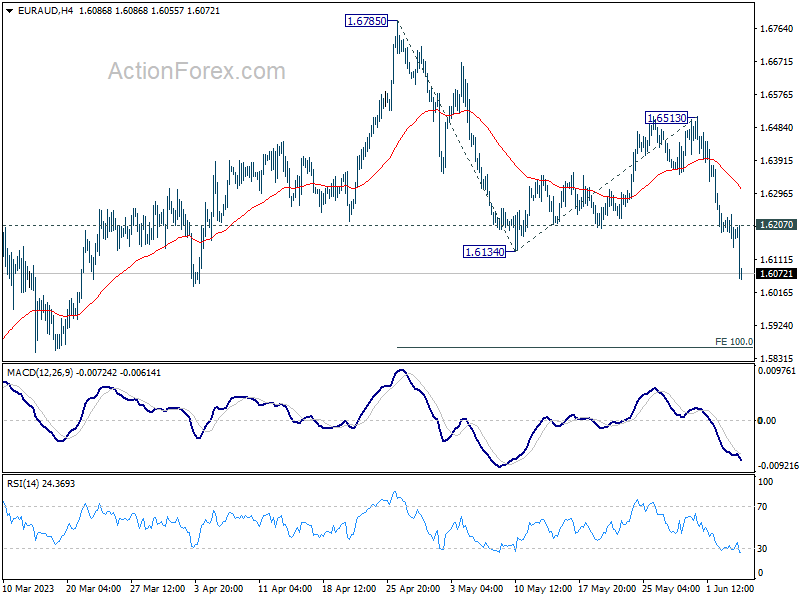

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6143; (P) 1.6191; (R1) 1.6237; More...

EUR/AUD's decline continues today and break of 1.6134 support confirms resumption of whole fall from 1.6785. Intraday bias stays on the downside for 100% projection of 1.6785 to 1.6134 from 1.6513 at 1.5862. On the upside, above 1.6207 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.6513 resistance holds, in case of recovery.

In the bigger picture, a medium term top is possibly in place at 1.6785 already, on bearish divergence condition in D MACD. Fall from there is seen as correcting whole up trend from 1.4281 (2022 low). Deeper decline is expected as long as 1.6513 resistance holds, to 38.2% retracement of 1.4281 to 1.6785 at 1.5828. Strong support could be seen there to complete the first leg of the corrective pattern.