Sample Category Title

Euro Extends Losses After Sizzling Nonfarm Payrolls

- ECB’s Lagarde hints at further rate hikes

- US nonfarm payrolls surges to 339,000

- US unemployment rises to 3.7%

The euro has extended its losses on Monday and is trading at 1.0686, down 0.21%.

It was a brutal month of May for the euro, which plunged 2.98%. The euro started the month above the 1.10 line but a hawkish Federal Reserve and solid US numbers have boosted the US dollar. The debt ceiling crisis also buoyed the greenback, as investors were nervous about a US default. This dampened risk appetite and pushed the safe-haven US dollar higher.

Lagarde stays hawkish

The ECB meets on June 15th and President Lagarde reiterated her hawkish stance earlier today. Lagarde noted that “price pressures remain strong”. She added that “there is no clear evidence that underlying inflation has peaked”, repeating what she said last week. An improvement in the eurozone inflation picture doesn’t seem to have softened Lagarde’s stance – last week’s April inflation report showed headline inflation falling from 7.0% to 6.1% and the core rate eased from 5.6% to 5.3%.

Lagarde said that future rate decisions would be data-dependent and strongly hinted that more rate hikes were coming. There are no tier-1 releases prior to the June meeting, and barring some unusual developments, the ECB is likely to raise rates by 25 basis points, which would bring the benchmark cash rate to an even 4.0%.

Nonfarm payrolls surge, but unemployment climbs as well

Last week ended with a scorching nonfarm payrolls report, a reminder that hiring and job growth remain resilient. Payrolls surged by 339,000 in May, crushing the estimate of 195,000. The April reading was revised upwards to 294,000 from 253,000, another sign of strong growth. However, there was more to the story. The unemployment rate surprised to the upside, rising from 3.4% to 3.7%, while wage growth ticked lower to 0.3%, down from 0.4%.

The mixed job report shows that job growth remains robust but the labour market is also showing signs of cooling down, which is what the Fed desperately needs to wind up the current rate-tightening cycle. If the Fed chooses to focus on the softer portions of the employment report, it could be enough for the Fed to take a pause at the meeting next week, after ten consecutive rate increases.

EUR/USD Technical

- 1.0707 is a weak support line. Below there is support at 1.0636

- 1.0780 and 1.0851 are the next resistance lines

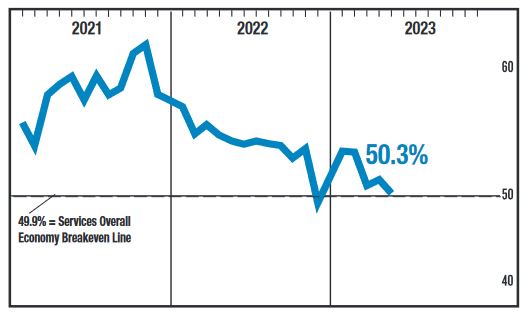

US: ISM Shows Services Sector Growth Slowed in May

The ISM Services PMI index pulled back to 50.3 in May from 51.9 in April. This falls well short of the 52.4 percent reading consensus was expecting. This is the fifth consecutive month of expansion for the services sector, but optimism has been steadily eroding since late 2022.

In line with the headline measure, the business activity sub-index cooled to 51.5, down from 52.0 in April.

The new orders fell 3.2 percentage points (pp) to 52.9, giving back most of April's gains and is now slightly higher than the 52.2 print in March. The new orders index is well below its 62.6 peak from February and reflects a significant moderation in growth.

The prices paid component fell again to 56.2 in May. This is the lowest reading since May 2020 and even below the average prints recorded in the 2017-2019 period before the pandemic.

Supplier delivery times registered 47.7, down from 48.6 in April, while the backlog of orders index plummeted 8.8 points to 40.9.

The employment sub-component tumbled into contractionary territory, and at 49.2 is at its lowest level since October 2022.

Eleven out of 18 industries expanded in May, down from fourteen in April.

Key Implications

May's services sector update reflects an economy that is gradually slowing down. Similar to the manufacturing sector's update last week, backlogs and supplier delivery times continue to improve as demand growth slows. The degree of improvement in supplier delivery times since February were last seen at the tail end of the recession during the Global Financial Crisis.

Taken with the ISM Manufacturing report from last week, businesses are signaling slowing demand growth. Combining this with improving supply chain conditions and easing price pressures, the Fed has some reassurance that the fight against inflation is gradually progressing – despite persistently strong jobs growth in the Nonfarm Payrolls Report.

ECB Lagarde: No clear evidence underlying inflation has peaked

Christine Lagarde, President of ECB, acknowledged the persistence of robust price pressures in her recent speech. She pointed out that both headline and core inflation continue to face "upside pressures... from the pass-through of past energy cost increases and supply bottlenecks."

Speaking on the current state of underlying inflation, Lagarde said, "The latest available data suggest that indicators of underlying inflationary pressures remain high and, although some are showing signs of moderation, there is no clear evidence that underlying inflation has peaked."

Lagarde also highlighted the intensifying wage pressures, noting that "wage pressures have strengthened further as employees recoup some of the purchasing power they have lost as a result of high inflation."

Lagarde also drew attention to the forceful impact of the central bank's rate hikes on financial conditions. "Our rate hikes are being transmitted forcefully to financing conditions for firms and households, as can be seen in rising lending rates and falling lending volumes," she stated.

Notably, she mentioned that "the full effects of our monetary policy measures are starting to materialise," adding that future ECB decisions are geared towards ensuring a "timely return of inflation to our 2% medium-term target." She asserted, "Our future decisions will ensure that the policy rates will be brought to levels sufficiently restrictive... and will be kept at those levels for as long as necessary."

US ISM services dropped to 50.3, corresponds to 0.2% annualized GDP growth

US ISM Services PMI dropped from 51.9 to 50.3 in May, below expectation of 52.6. Looking at some details, business activity/production dropped from 52.0 to 51.5. New orders dropped from 56.1 to 52.9. Employment dropped from 50.8 to 49.2. Prices dropped from 59.6 to 56.2.

ISM said, the May Services PMI indicates the overall economy is growing for the fifth consecutive month after one month of contraction in December.

The past relationship between the Services PMI and the overall economy indicates that the Services PMI for May (50.3 percent) corresponds to a 0.2-percent increase in real gross domestic product (GDP) on an annualized basis.

Sunset Market Commentary

Markets

With only the US services ISM as a really market relevant data series to be published after finishing this report, markets today mainly build the Friday’s post-payrolls narrative. Yields in the US, in Europe, but also in the UK are rebounding further. Ongoing labour market strength suggests that it’s premature to position for a (demand-driven) recession. To put it otherwise, (consumer) demand might stay stronger for longer than what is necessary for (core) inflation to quickly return to the central banks’ targets. Follow-though price action on Friday’s jump lifts US rates about 7.0/3.5 bps with the curve inverting further. The end of May peak yields (4.64% for the US 2-y vs 4.55% currently, 3,86% for the US 10-y yield vs 3.74% now) are again on the radar. Still a break won’t be that easy as the Fed’s ‘skip’ of a June rate hike still leaves plenty of eco data to finetune both the markets’ and the Fed’s assessment on what to do in July. European/German markets underperform. In a hearing before the EU Parliament, ECB Chair Lagarde reiterates that there is no clear evidence that underlying inflation has peaked, even as the effects of ECB policy start to materialize. German yields are gaining between 8 bps (2-y) and 6 bps (10-y). Similar narrative for UK markets (+8 bps 2-y, + 4bps 30-y). If the Saudi oil production cut would succeed to put the oil price again on an upward trajectory, over time it might also slow the decline of headline inflation. Admittedly, the jury is still out whether the trick will work this time. At $78 p/b, brent moves away from the low $70 p/b area. In this respect, also keep an eye at the rebound in the European reference Dutch natural Gas contract, jumping more than 15% from Friday’s cycle low. US and European equities are trading little changed (EuroStoxx -0.10%, S&P + 0.2%). After Friday’s substantial gains, this still might be labelled as ‘constructive’ price action.

On FX markets, the dollar outperforms most other majors. DXY trades near 104.3 (from 104.04) with last week’s correction top at about 104.7. EUR/USD is drifting below the 1.07 big figure (1.0685) with the correction low at 1.0635. USD/JPY regains the 140 barrier (140.25). For now, oil/commodity related currencies hardly profit from the Saudi oil production cut. USD/CAD trades marginally lower near 1.3435. EUR/NOK rises marginally to 11.82. The Aussie dollar (AUD/USD 0.6605) trades little changed as investors look out for tomorrow’s RBA policy decision. The Swedish krone (EUR/SEK 10.65) struggles to avoid returning to recent lows as markets continue to ponder the impact of real estate stress on Riksbank policy. Sterling is falling prey to profit taking with EUR/GBP returning to the 0.863 area. CE currencies remain in excellent shape (EUR/CZK 23,55, EURHUF 369,2). The zloty is even touched the strongest against the euro since June 2021.

News & Views

Turkish headline CPI in May fell from 43.68% to 39.59%, a little above the 39.2% consensus estimate. Inflation nearly flatlined M/M (0.04%), a direct consequence from president Erdogan offering natural gas to households for free last month in the run-up to the elections. The component ‘housing, water, electricity, gas and other fuels” dropped a whopping 13.79% m/m. Core inflation for the second months straight topped headline inflation and even reaccelerated from 45.48% to 46.62%,(43.70% expected). The data remain extremely troubling for a country reeling from a currency crisis amid very easy CB policy. President Erdogan appointed Mehmet Simsek as the new Treasury and Finance minister. In his first remarks, he signaled a return to conventional policies but market doubts remain. The Turkish Lira opened at a record low and extended losses after the data. USD/TRY trades near 21.24.

Czech wages grew by 8.6% y/y in the first quarter of this year. That’s an acceleration from a downwardly revised 6.6% in the final quarter of last year. It is, however, slower than the 9.1% the Czech central bank forecasted. In addition, real wages fell by -6.7%, a little over the -6% consensus estimate. The numbers serve as critical input to the CNB meeting June 21 and could ease hawkish policy makers’ concerns about the emergence of a wage-price spiral somewhat. The previous gathering was a close 4-3 call between the status quo (7%) and a rate hike. In combination with the Czech government’s determination to get the budget under control and disappointing growth details last week, it may settle the debate. Instead, the CNB could opt for keeping the policy rate at 7% for longer. One wildcard still remaining in the run-up to the meeting are Czech CPI numbers, due June 12. The Czech crown erased kneejerk losses shortly after today’s publication. EUR/CZK is trading around 23.54.

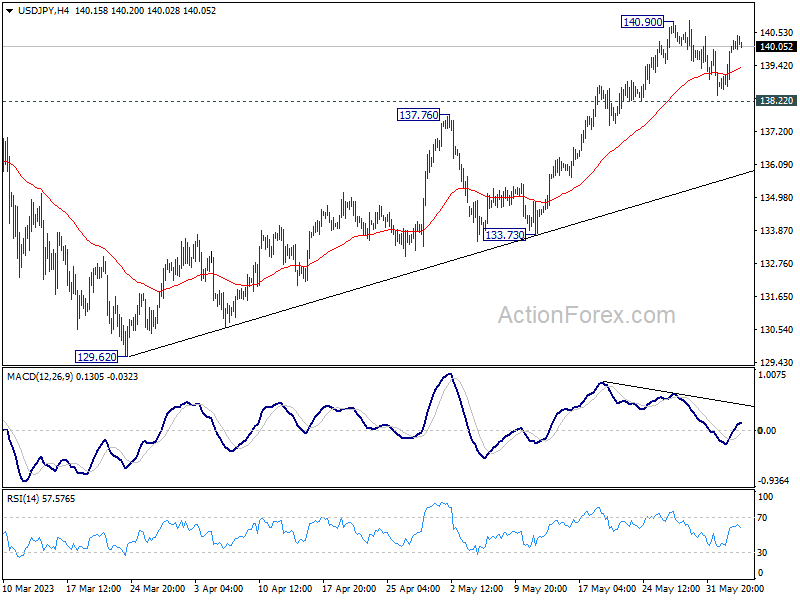

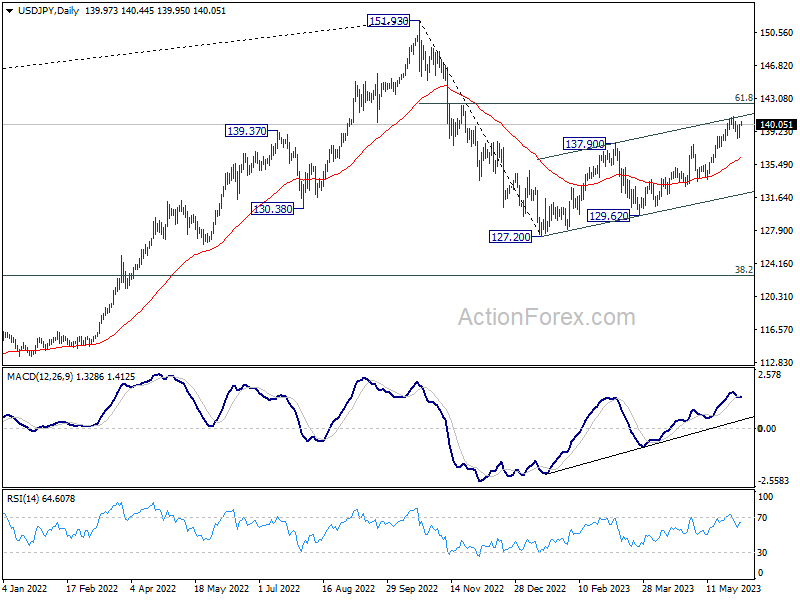

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.03; (P) 139.55; (R1) 140.49; More...

USD/JPY is staying in consolidation below 140.90 and intraday bias remains neutral. Further rally is expected as long as 138.22 minor support holds. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.27).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

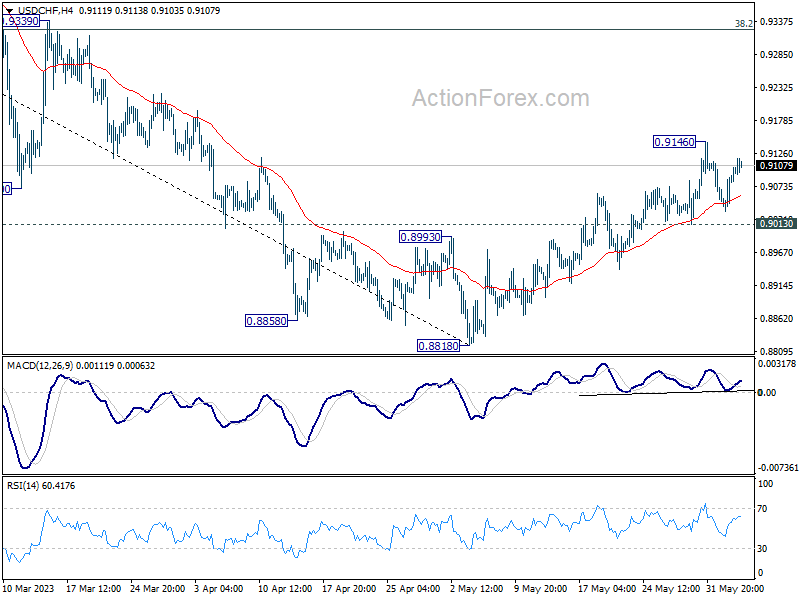

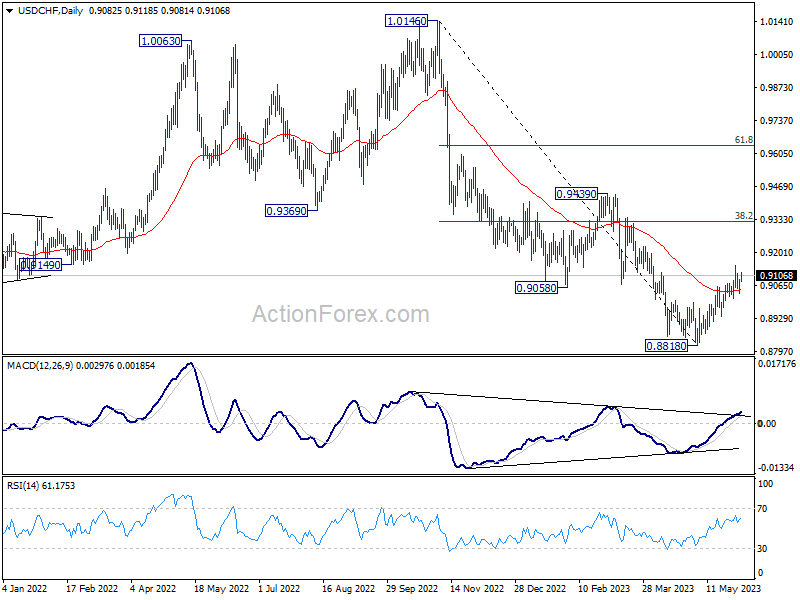

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9052; (P) 0.9072; (R1) 0.9110; More...

USD/CHF is staying in consolidation below 0.9146 and intraday bias remains neutral. Further rally is expected as long as 0.9013 minor support holds. Rise from 0.8818 short term bottom is seen as corrective whole down trend from 1.0146. Above 0.9146 will target 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, however, break of 0.9013 will turn bias back to the downside for retesting 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

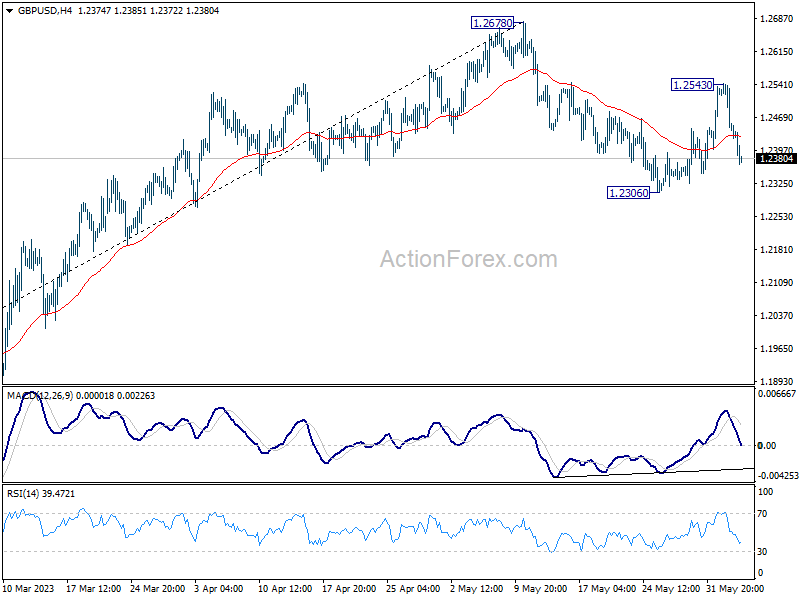

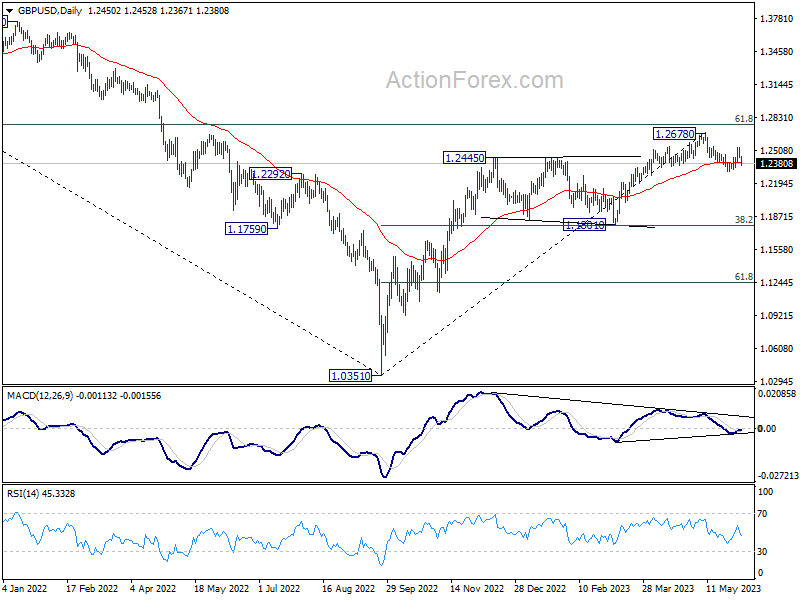

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2414; (P) 1.2480; (R1) 1.2517; More...

Intraday bias in GBP/USD stays neutral at this point. On the downside, break of 1.2306 will resume the correction from 1.2678. Deeper decline would then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, above 1.2543 will resume the rebound from 1.2306 to retest 1.2678 high.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

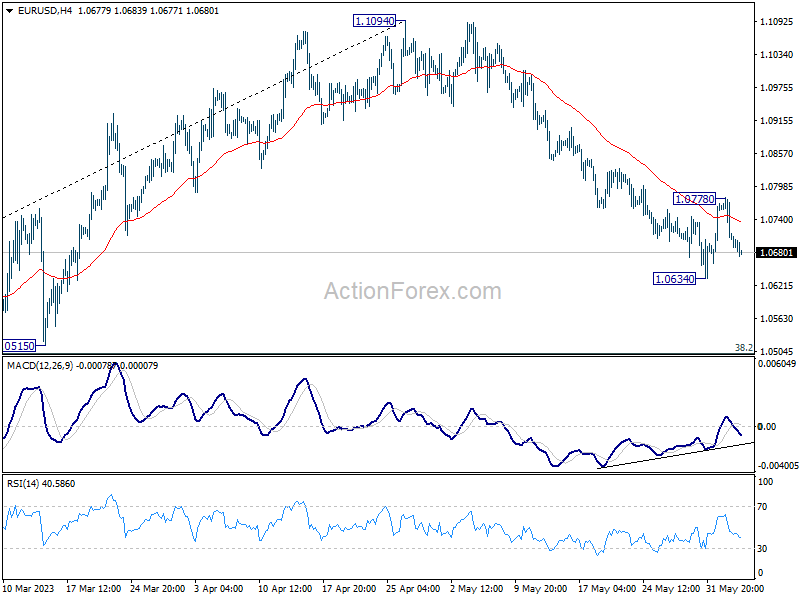

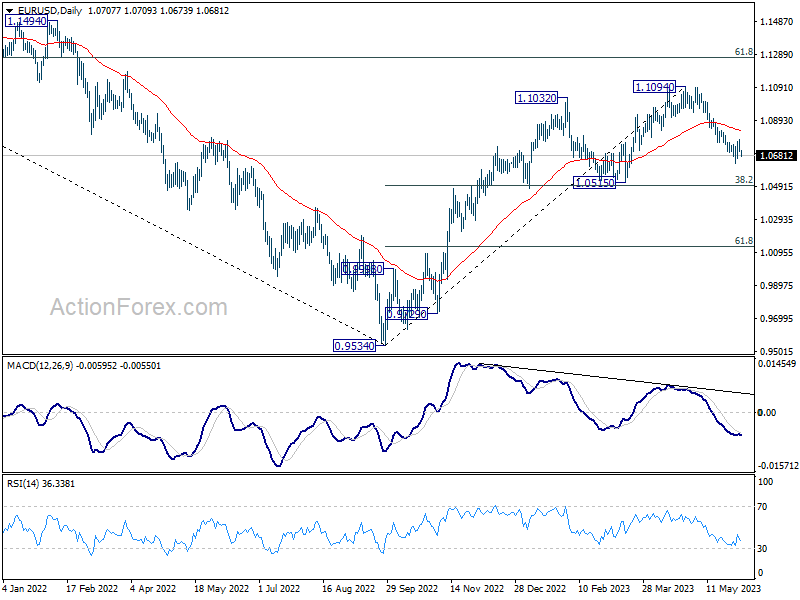

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0682; (P) 1.0731; (R1) 1.0756; More...

EUR/USD dips notably today but stays above 1.0634 support. Intraday bias remains neutral first. On the downside, break of 1.0634 will resume the corrective decline from 1.1094. Deeper fall should then be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0778 will resume the rebound from 1.0634 to 55 D EMA (now at 1.0829).

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

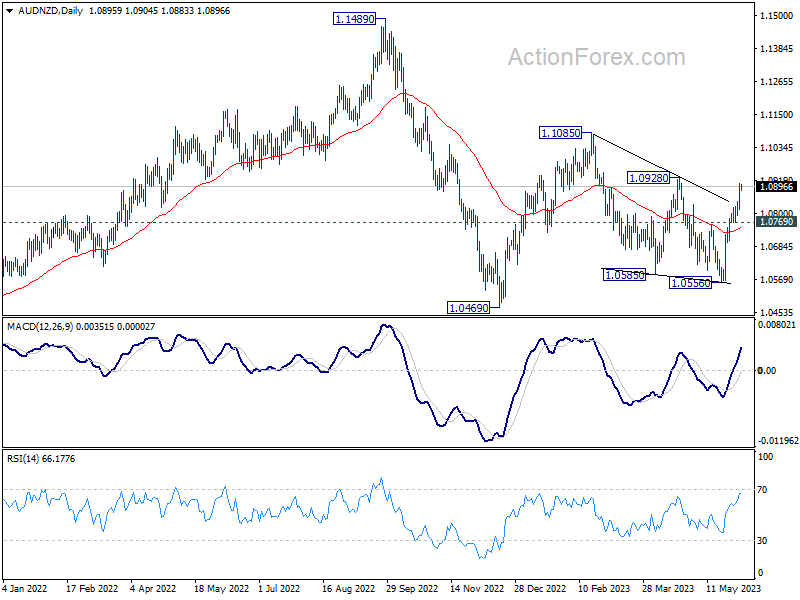

Euro Soft on Poor Investor Confidence, Aussie Range Bound ahead of RBA

Euro is experiencing some selling pressure today, brought on by discouraging investor confidence data, with other European currencies also showing signs of distress. Meanwhile, US Dollar is making strides, superseding commodity currencies as it rides the wave of last week's late rally.

Australian Dollar is trading within a narrow range against Canadian Dollar and New Zealand Dollar, as markets anticipate the outcome of tomorrow's RBA rate decision. On the other hand, the Japanese Yen presents a mixed picture as it continues in its near-term consolidation phase.

Technically, the strong rally in AUD/NZD in the last two weeks argues that corrective pattern from 1.1085 has completed with three waves down to 1.0556. Immediate focus is now on 1.0928 resistance in the coming session. Decisive break there will confirm this case and would probably prompt further rise through 1.1085, to resume the whole rebound from 1.0469. Nevertheless, break of 1.0769 minor support will revive some near term bearishness for deeper fall back to 1.0556.

RBA previews:

In Europe, at the time of writing, FTSE is up 0.49%. DAX is up 0.16%. CAC is down -0.16%. Germany 10-year yield is up 0.0067 at 2.383. Earlier in Asia, Nikkei rose 2.20%. Hong Kong HSI rose 0.84%. China Shanghai SSE rose 0.07%. Singapore Strait Times rose 0.72%. Japan 10-year JGB yield closed flat at 0.434.

Eurozone Sentix fell to -17, Germany the biggest problem child

Eurozone Sentix Investor Confidence dropped from -13.1 to -17 in June, well below expectation of -9.2. Current Situation index dropped from -7.0 to -15.8. But Expectations index ticked up from -19.0 to -18.3.

Sentix said, "Eurozone economy continues to send weak signals at the beginning of June", and "the clear slump in the assessment of the economic situation is particularly striking".

Meanwhile, inflation expectations rose to -6, comparing to -44.25 a year ago. "Thus, positive inflation surprises are on the horizon," Sentix said.

Sentix also noted: :The biggest problem child in the Eurozone remains Germany, which plummets dramatically in the sentix economic indices. The situation collapses to -22 points, expectations fall again slightly to -20.3 points. The overall index plunges to -21.1 points. All lows since Nov/Dec 2022."

Eurozone PPI at -3.2% mom, 1.0% yoy in Apr

Eurozone PPI came in at -3.2% mom, 1.0% yoy in April, versus expectation of -2.7% mom, 0.8% yoy. For the month, industrial producer prices decreased by 10.1% mom in the energy sector and by -0.6% mom for intermediate goods, while prices increased by 0.2% mom for durable consumer goods, by 0.3% mom for non-durable consumer goods and by 0.4% mom for capital goods. Prices in total industry excluding energy decreased by -0.1% mom.

EU PPI was at -2.9% mom, 2.3% yoy. The largest monthly decreases in industrial producer prices were recorded in Belgium (-9.1%), Italy (-6.5%) and Ireland (-6.3%), while increases were observed in Germany (+0.3%), Denmark (+0.2%) as well as Greece, Cyprus, Malta and Slovenia (all +0.1%).

Eurozone PMI composite finalized at 52.8, manufacturing downside to be reflected in services slowdown

Eurozone PMI Services was finalized at 55.1 in May, down from April's 56.2. PMI Composite was finalized at 52.8, down notably from April's 54.1. HCOB noted that services activity growth stayed strong, but factory output fell at the quickest pace in six months.

Looking at some countries, Spain PMI Composite (55.2), Italy (52.0) and France (51.2) were at 4-month low. Germany was at 53.9, a 2-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: "Relatively resilient services activity growth should ensure that the eurozone regains some footing and shows a positive rate of expansion in the second quarter after GDP stagnated in the October - March period.

"However, the downturn in manufacturing is a drag on economic growth and is likely to be reflected in a further slowdown in the services sector in the coming months. We do not anticipate an overall economic recession, though."

UK PMI services finalized at 55.2, strong growth so far in Q2

UK PMI Services was finalized at 55.2 in May, down slightly from April's 55.9. S&P Global said there were robust rises in output and incoming new work. Staffing numbers increased for the fifth month running. Wage pressures pushed up cost inflation to a new three-month high. PMI Composite was finalized at 54.0, down from prior month's 54.9.

Tim Moore, Economics Director at S&P Global Market Intelligence: "Service sector businesses have experienced strong growth so far in the second quarter of 2023... Rising export sales were also reported... Job creation was maintained... Intense wage pressures continued across the service economy... Average prices charged by service sector companies nonetheless increased at the second-weakest pace since August 2021."

Swiss CPI slowed to 2.2% yoy in May, slightly above expectations

Swiss CPI rose 0.3% mom in May, slightly below expectation of 0.4% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.2% mom. Domestic products prices rose 0.3% mom. Imported products prices rose 0.1% mom.

Comparing with May 2022, CPI slowed from 2.6% yoy to 2.2% yoy, above expectation of 2.1% yoy. Core CPI was unchanged at 2.2% yoy. Domestic products prices slowed from 2.6% yoy to 2.4% yoy. Imported products prices fell notably from 2.4% yoy to 1.4% yoy.

Japan PMI services finalized at record 55.9, overall growth accelerated in Q2

Japan PMI Services was finalized at 55.9 in May, up from April's 55.4, setting another fresh series record. PMI Composite was finalized at 54.3, up from April's 52.9, the second strongest reading since record began in 2007, after October 2013.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: "The record expansion in activity among service providers, coupled with a renewed increase in manufacturing production contributed to a stronger increase in overall private sector activity.

"The rate of expansion was solid and the second-strongest in the history of the series (behind October 2013). The upturn was led by the dominant services sector, although there was a renewed sense of optimism for private sector activity given the expansions in manufacturing output and new orders.

"Latest data also provides the indication economic growth has accelerated in the second quarter of the year, following the 1.3% year-on- year increase in growth in the first quarter of 2023, according to the latest official statistics."

China Caixin PMI services rose to 57.1, overall economy lacks internal drive

China Caixin PMI Services rose from 56.4 to 57.1 in May, above expectation of 55.2. The rate of expansion was the second-steepest seen over the past two-and-a-half years. PMI Composite rose from 53.6 to 55.6, highest since end of 2020.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In general, it remains a prominent feature of the Chinese economy that the services sector is stronger than manufacturing. In May, the Caixin China services PMI showed that services activity was picking up overall, but employment expansion and market optimism weakened. In the manufacturing sector, employment deteriorated, prices plunged, and manufacturers also became less optimistic toward the outlook, according to the Caixin China manufacturing PMI.

"This divergence highlights that economic growth is lacking internal drive and market entities lack sufficient confidence, underscoring the importance of expanding and restoring demand. Currently, stabilizing employment, increasing income and bolstering expectations through proactive fiscal policy should be prioritized given a dire job market and mounting deflationary pressure."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0682; (P) 1.0731; (R1) 1.0756; More...

EUR/USD dips notably today but stays above 1.0634 support. Intraday bias remains neutral first. On the downside, break of 1.0634 will resume the corrective decline from 1.1094. Deeper fall should then be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0778 will resume the rebound from 1.0634 to 55 D EMA (now at 1.0829).

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M May | 0.90% | 0.20% | ||

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q1 | 0.50% | 2.10% | 10.60% | 12.70% |

| 01:45 | CNY | Caixin Services PMI May | 57.1 | 55.2 | 56.4 | |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 18.4B | 16.1B | 16.7B | 14.9B |

| 06:30 | CHF | CPI M/M May | 0.30% | 0.40% | 0.00% | |

| 06:30 | CHF | CPI Y/Y May | 2.20% | 2.10% | 2.60% | |

| 07:45 | EUR | Italy Services PMI May | 54 | 53.7 | 57.6 | |

| 07:50 | EUR | France Services PMI May F | 52.5 | 52.8 | 52.8 | |

| 07:55 | EUR | Germany Services PMI May F | 57.2 | 57.8 | 57.8 | |

| 08:00 | EUR | Eurozone Services PMI May F | 55.1 | 55.9 | 55.9 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jun | -17 | -9.2 | -13.1 | |

| 08:30 | GBP | Services PMI May F | 55.2 | 55.1 | 55.1 | |

| 09:00 | EUR | Eurozone PPI M/M Apr | -3.20% | -2.70% | -1.60% | |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | 1.00% | 0.80% | 5.90% | |

| 13:45 | USD | Services PMI May F | 55.1 | 55.1 | ||

| 14:00 | USD | ISM Services PMI May | 52.6 | 51.9 | ||

| 14:00 | USD | Factory Orders M/M Apr | 0.80% | 0.90% |