Sample Category Title

Aussie Extended Gains after RBA

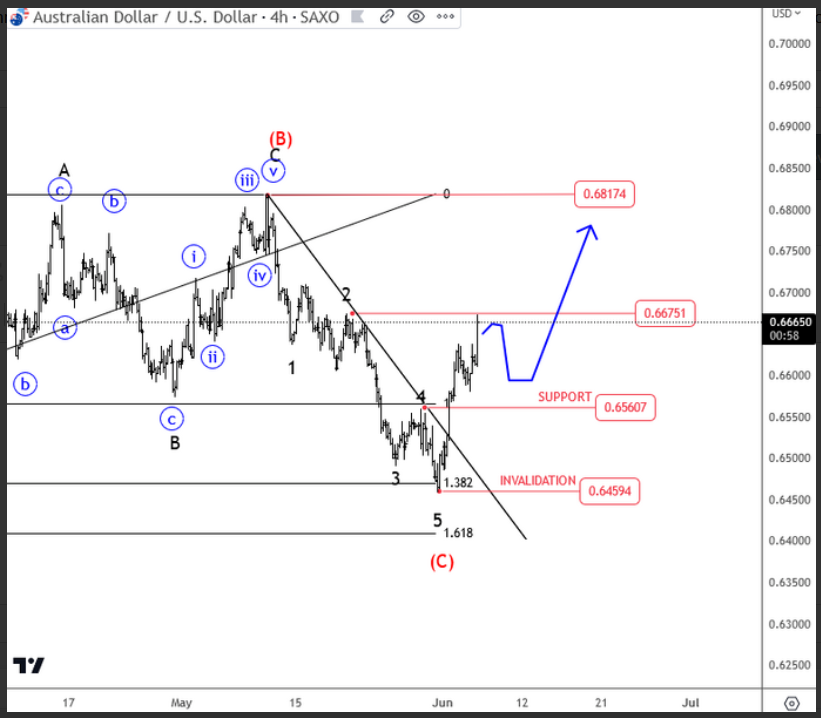

Move of the Asian session was Aussie because of RBA rate decision. AUD is up across the board after another rate hike by CB. They said that this hike will provide greater confidence that inflation would return to the target. More importantly, they added that some further tightening may be required. From an Elliott wave perspective, we see nice push higher, but ideally, that's still fifth wave of the first big impulse so possibly more gains after a pullback. Next pullback can be an opportunity for longs.

AUD/USD: Australian Dollar Rises to Three-Week High on RBA’s Hawkish Shift

Australian dollar rose to three-week high in early Wednesday, after RBA’s surprised by 25 basis points rate hike vs widely expected unchanged policy on today’s meeting.

Australia’s central bank lifted interest rates to 4.1%, the highest in eleven years and said that further rate hikes may be required to push inflation towards target.

Today’s decision was seen as a hawkish shift, after the RBA dropped its statement that medium term inflation expectations remain well anchored, pointing to growing concerns that inflation is still too high, which adds to signals about further hikes, as bets for July hike rose to 60%.

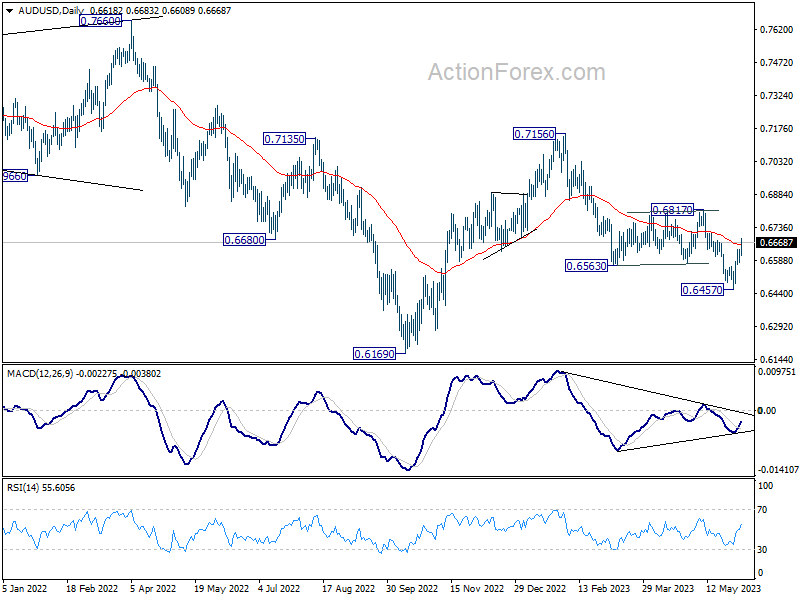

Hawkish RBA lifted the Aussie dollar, extending the latest bull-leg off 0.6458 (May 31 low) into fourth straight day, to crack strong resistances at 0.6680/91 (daily cloud base / Fibo 61.8% of 0.6818/0.6458 / 200DMA).

Offers may emerge at this zone as stochastic is overbought on daily chart and slow bulls for consolidation ahead of push higher, as daily studies are positive, and sentiment improved on RBA’s hawkish turn, while daily cloud shift later this week is also expected to be magnetic.

Broken Fibo 50%, reinforced by daily Kijun-sen (0.6638) should ideally contain and keep bulls firmly in play.

Sustained break of 0.6680/91 pivots to open way for test of targets at 0.6742/46 (daily cloud top / 100DMA) and unmask key resistance at 0.6818 (May 10 top).

Falling 20DMA (0.6611) marks pivotal support and break here would question bulls.

Res: 0.6691; 0.6733; 0.6746; 0.6771.

Sup: 0.6638; 0.6611; 0.6557; 0.6543.

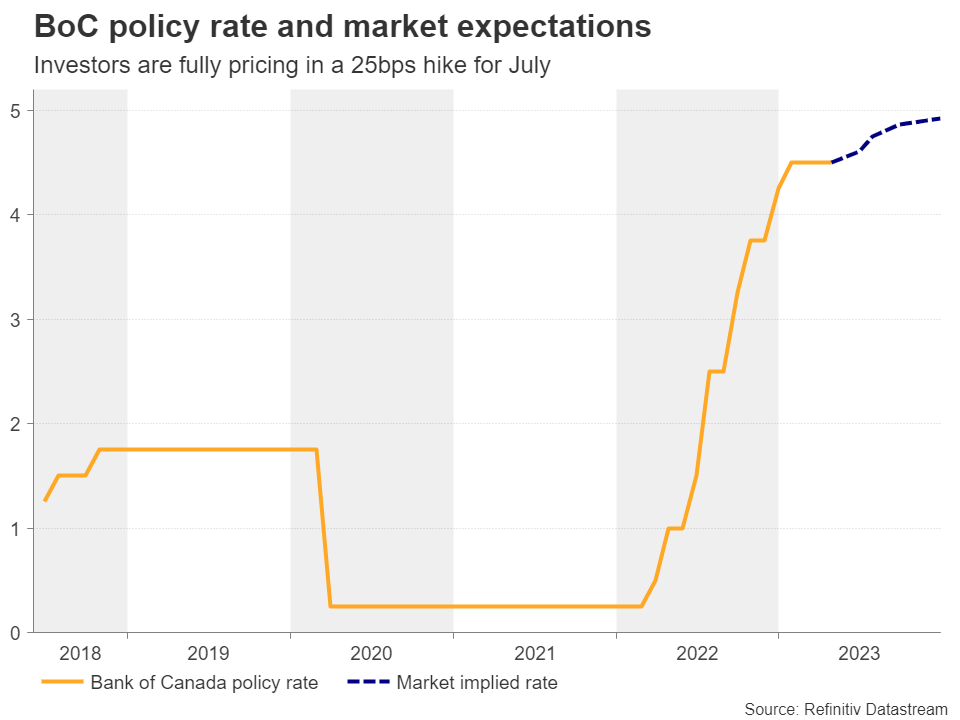

Will the BoC Resume Interest Rate Hikes?

After staying inactive for two consecutive meetings, the BoC is now expected by a decent percentage of market participants to raise interest rates when it meets on Wednesday at 14:00 GMT. The hype of another rate hike was bolstered by the much-better-than-expected GDP data for Q1. Will policymakers indeed press the button, or will they stay patient and wait for more incoming data before deciding whether raising interest rates further is appropriate?

Data keeps the hike door open

At its latest gathering, the Bank of Canada decided to stand pat for the second meeting in a row as it was largely anticipated. However, it did not satisfy those expecting a rate cut later this year, with the statement revealing that policymakers are still prepared to raise rates further if deemed necessary.

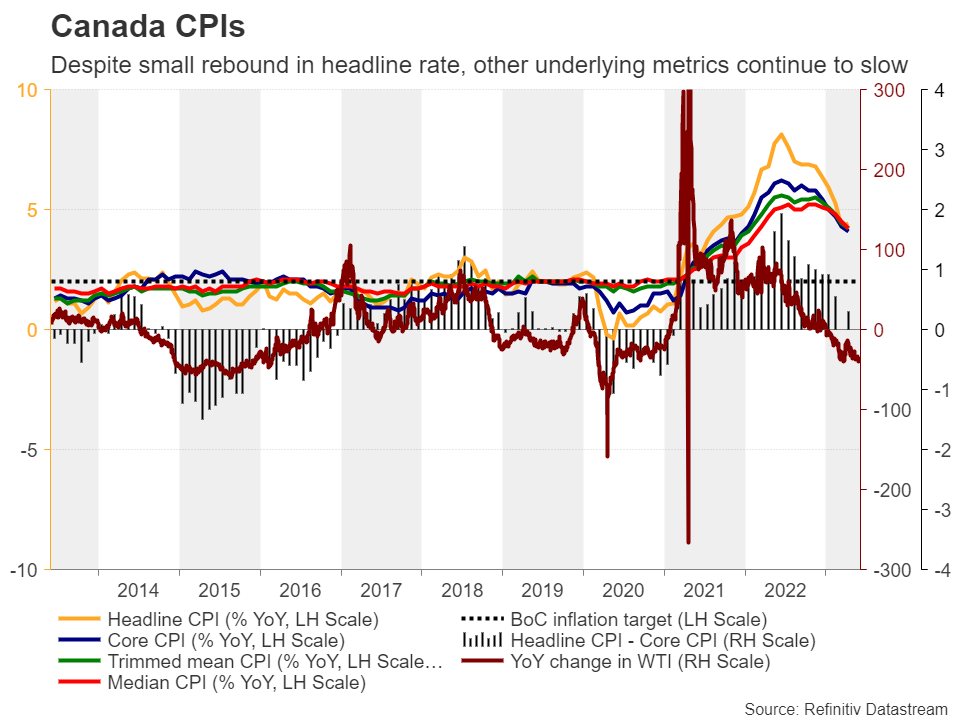

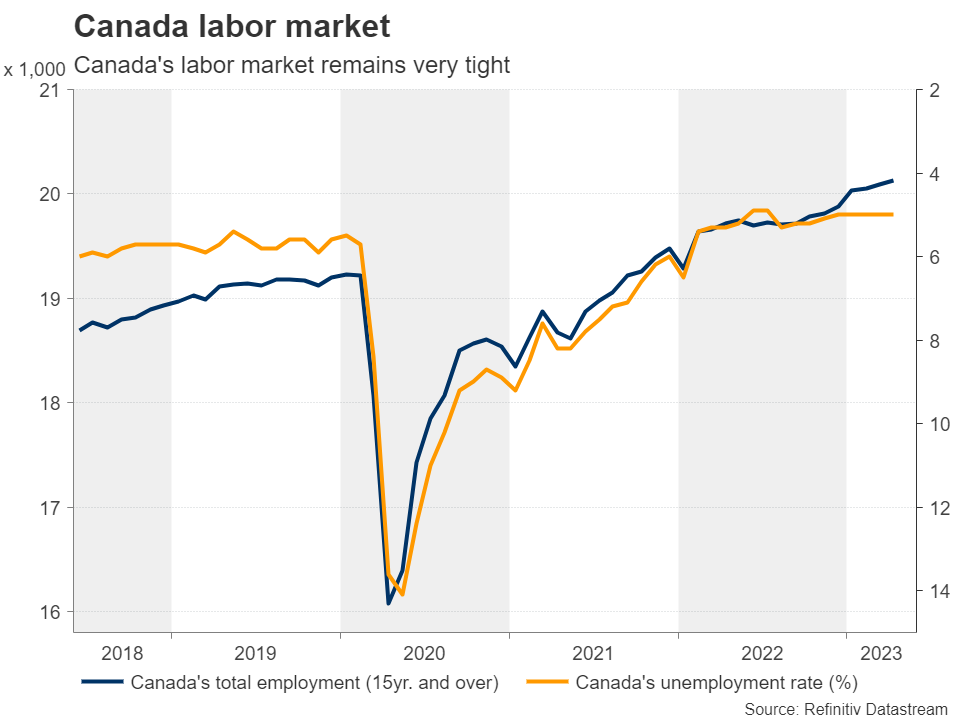

Data after the meeting have been adding credence to the Bank’s choice to leave the door to more hikes open. The April jobs report revealed that the unemployment rate held steady at 5.0%, just a tick above its lowest level in more than five decades, while the inflation data for the month showed that headline inflation accelerated in April, and although all the underlying metrics slowed, both the Trimmed mean and Common CPI rates slid by less than expected.

Most importantly, the economy grew by double the estimated pace during the first three months of the year after stagnating at the end of 2022, resulting in a skyrocketing quarter-on-quarter annualized rate to 3.1% from -0.1%.

But a hike more likely in July

Having said all that though, although market participants are convinced that another hike may be firmly on the table, they don’t see a high probability of this happening at this week’s gathering. They are assigning a 40% probability to the hike scenario, with the remaining 60% pointing to no action. They believe that a hike is more likely to be delivered in July and nearly another one by December.

Therefore, should policymakers stay sidelined and stick to their guns that they remain prepared to hike more if needed, the loonie is likely to slide but not much. For a noteworthy and sustained tumble in the Canadian currency, officials may need to stand pat and officially announce the end of this tightening crusade, which according to the aforementioned data appears to be the least likely scenario.

The former looks the wisest choice as it is too early to describe the latest rebound in the headline CPI rate as inflation getting out of control, and thus, officials may prefer to wait for more data before they hike again. They could do so at the July meeting, where updated macroeconomic projections will be available. Now, in the case of the Bank pressing the hike button this week and appearing willing to deliver more, the loonie could rally.

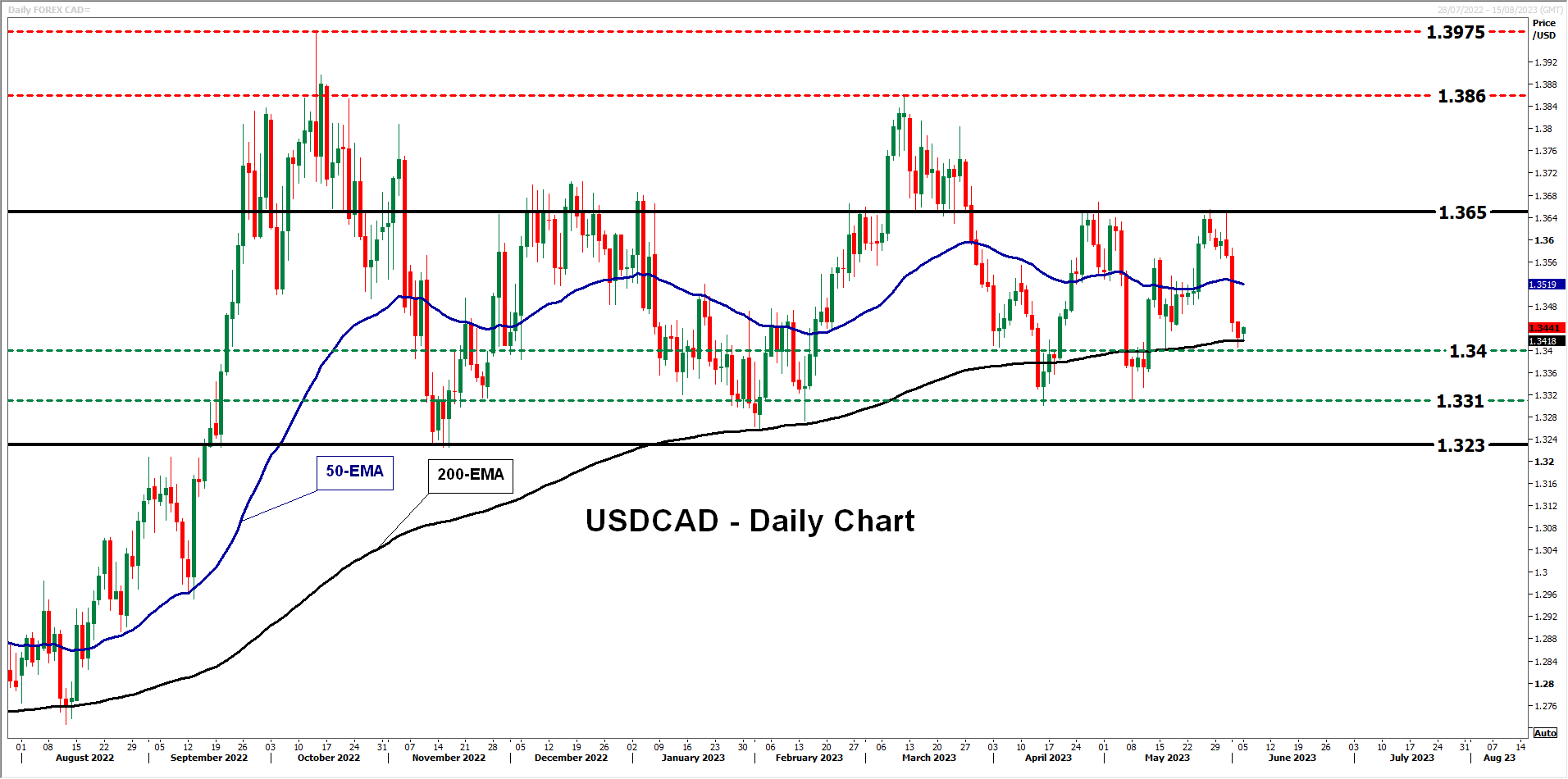

Dollar/loonie stays trapped within a wide range

Dollar/loonie has been trading in a trendless mode since November, with most of the price action being contained between the 1.3230 and 1.3650 barriers. Thus, the medium-term picture, at least from a technical perspective, looks neutral.

Currently, the pair is sitting slightly above the 1.3400 zone. If the BoC appears less hawkish than expected on Wednesday, dollar/loonie is likely to rebound and perhaps aim for another test at the upper bound of the range, at around 1.3650.

On the other hand, a potential hike could extend last week’s retreat, with a potential break below 1.3400 perhaps paving the way towards the lower bound of the aforementioned range, at around 1.3230.

Employment report also on tap

Having said all that though, apart from the BoC decision and the related market reaction, loonie traders will also have to evaluate the Canadian employment report for May, due out on Friday. Even if policymakers stay on hold, conditional upon leaving the door open to another hike, a strong employment report could prompt investors to add to their hike bets, adding more basis points worth of increments by the end of the year.

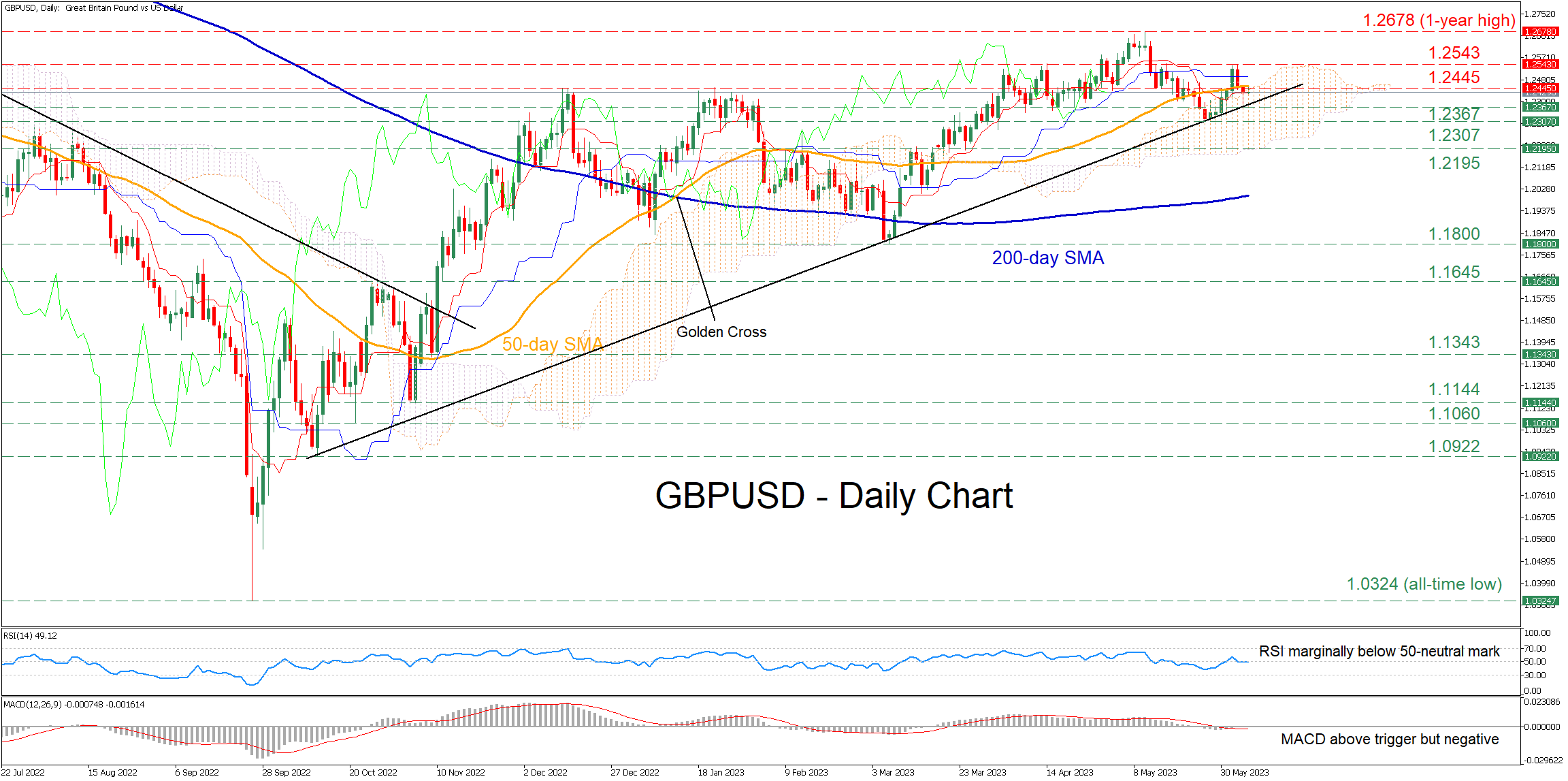

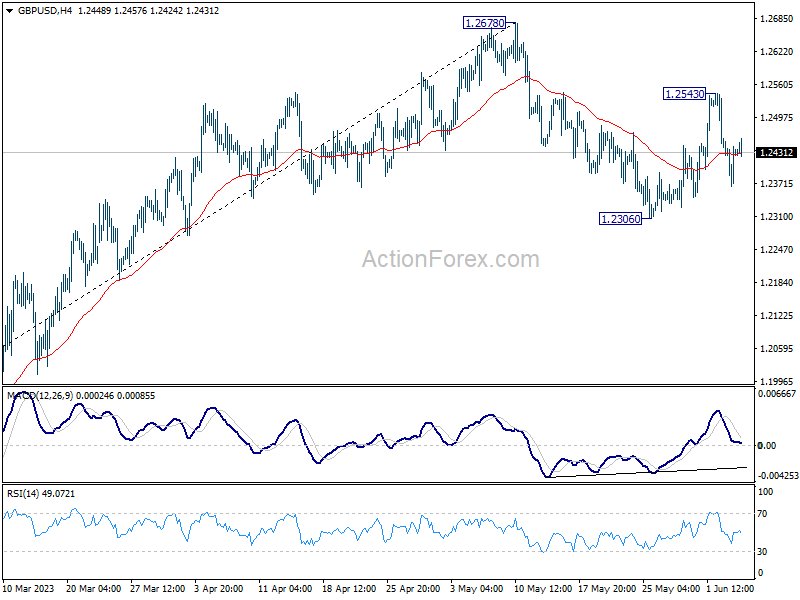

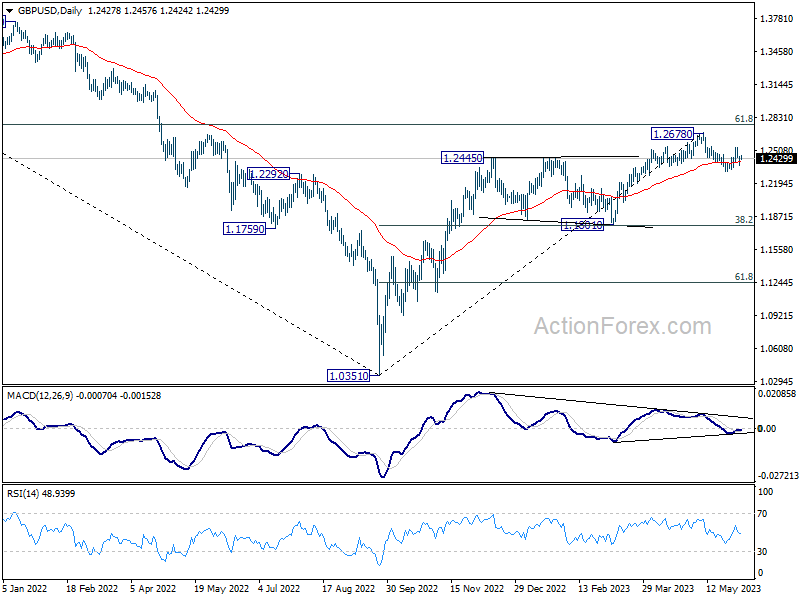

GBPUSD Battles With Crucial Technical Level

GBPUSD had been in a downside correction after peaking at the one-year high of 1.2678 on May 10. However, the pair retraced back higher when it found support at the long-term ascending trendline, while it is currently challenging a fortified zone that includes the 50-day simple moving average (SMA), the upper end of the Ichimoku cloud and a historical resistance level near 1.2445.

The momentum indicators currently suggest a neutral near-term bias. Specifically, the RSI is hovering around the 50-neutral mark and the MACD remains above its red signal line but in the negative territory.

Should buying pressures intensify, the bulls could initially attempt to overcome the congested technical region around 1.2445. Surpassing that zone, the price might ascend towards the recent resistance of 1.2543, which also provided upside protection in April. A violation of that region may set the stage for the one-year peak of 1.2678.

Alternatively, should the pair reverse lower to extend its short-term pullback towards the key support trendline, 1.2367 could act as the first line of defense. If that barrier fails, the May low of 1.2307 might appear on the radar. Further retreats could then cease at 1.2195, which served both as resistance and support in the past months.

In brief, GBPUSD is currently testing a very important technical region, where a failure to break above it could result in a downside breach of its long-term ascending trendline. Nevertheless, a jump above the fortified territory could enable the bulls to propel the price towards a fresh multi-month peak.

RBA Board Raises Cash Rate by 0.25% to 4.1% – A Further Hike Expected in July.

The Board has rebalanced its focus towards inflation and inflationary expectations. We expect there is more near-term work to be done to emphasise this message with another hike now likely in July.

The Reserve Bank Board raised the cash rate by 0.25% to 4.1% at its June Board meeting.

The Governor’s statement has rearranged the order of previous statements to put maximum emphasis on the damage associated with high inflation and inflationary expectations becoming entrenched in the economy. He points out that services price inflation is still very high and that unit labour costs are rising briskly with productivity growth remaining subdued. He also points out that public sector wages are expected to pick up further and that the annual increase in award wages was higher than last year.

He clearly now sees his dominant objective as being to contain inflation expectations and achieve the inflation objective which he now sees as associated with more risk.

The statement acknowledges “a substantial slowing in household spending” and “uncertainties regarding the global economy” but the emphasis has clearly pivoted away from concerns around domestic growth and maintaining the progress that has been achieved around the labour market since the pandemic, and towards ensuring that inflation returns to target, reflecting the rising risks around wages growth and inflationary expectations. He further emphasises that: “The Board remains alert to the risk that expectations of ongoing high inflation contribute to larger increases in both prices and wages”.

Our reading of the statement is that the Board believes that further work will need to be done in the near term to allay their concerns around inflationary expectations and wages growth.

Despite having increased the cash rate in both May and June we expect that a further rate hike will be required by the Board in July, to really emphasise their commitment to the inflation objective.

Thereafter the risk is that a further follow-up move may be required at the August meeting when the June quarter inflation report will be available. We expect that underlying inflation will have dropped from 6.6% to 6.1% but labour markets will remain tight and the ongoing concerns around wage pressures will persist.

The additional risk for the August meeting is that, due to these concerns around expectations, the staff may raise their inflation forecasts which would open the door to another rate increase.

Westpac has been expecting the first rate cut in the next easing cycle to come in February 2024 with at least 100bps of cuts over the course of next year. Since that call was made, the Board has now raised the cash rate by an additional 50bps with another 25bp move now expected in in July.

While this will put additional pressure on the Australian economy, particularly for households and eventually business, progress on reducing inflation and wages growth will not be sufficient to allow for a pivot to rate cuts any earlier than February.

Our current forecast for growth in the Australian economy in 2023 is 1%yr. Since that forecast was issued we have seen a lift in wages growth for certain sectors; higher immigration and a recovery in house prices. But the revised rate profile is certain to weigh even more heavily.

We expect the Australian economy grew by a very tepid 0.3% in the March quarter and further weakness is now almost certain through the remainder of the year. We will review our growth profile to take these major developments into account following the release of the national accounts.

Conclusion

The Board has become increasingly concerned around inflation risks. It has now raised the cash rate on two consecutive months following the pause in April.

We now expect a follow up move in July with risks of a further increase in August.

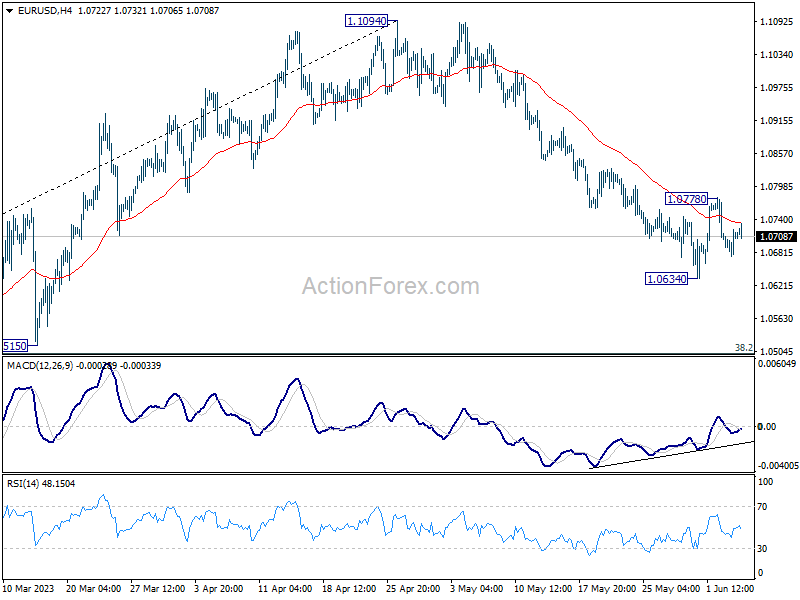

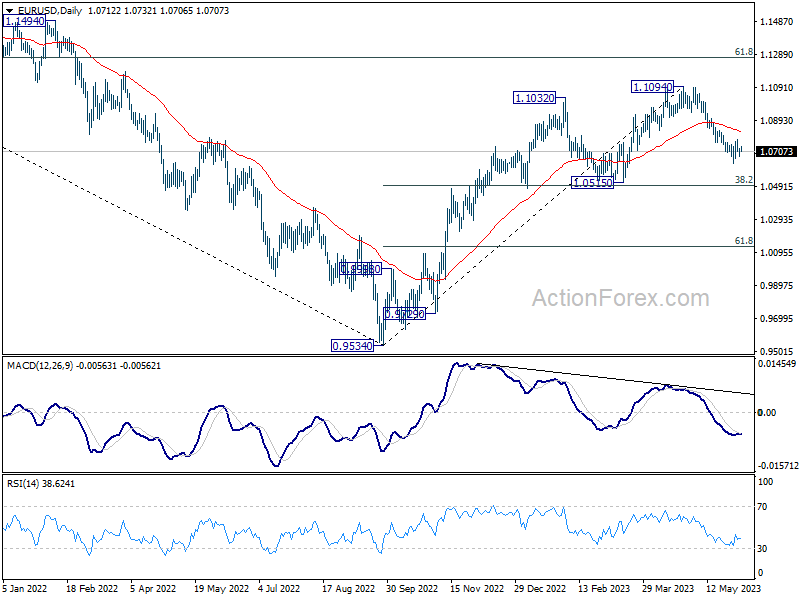

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0684; (P) 1.0703; (R1) 1.0731; More...

Intraday bias in EUR/USD stays neutral as consolidation continues above 1.0634. On the downside, break of 1.0634 will resume the corrective decline from 1.1094. Deeper fall should then be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0778 will resume the rebound from 1.0634 to 55 D EMA (now at 1.0829).

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2382; (P) 1.2420; (R1) 1.2472; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, break of 1.2306 will resume the correction from 1.2678. Deeper decline would then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, above 1.2543 will resume the rebound from 1.2306 to retest 1.2678 high.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

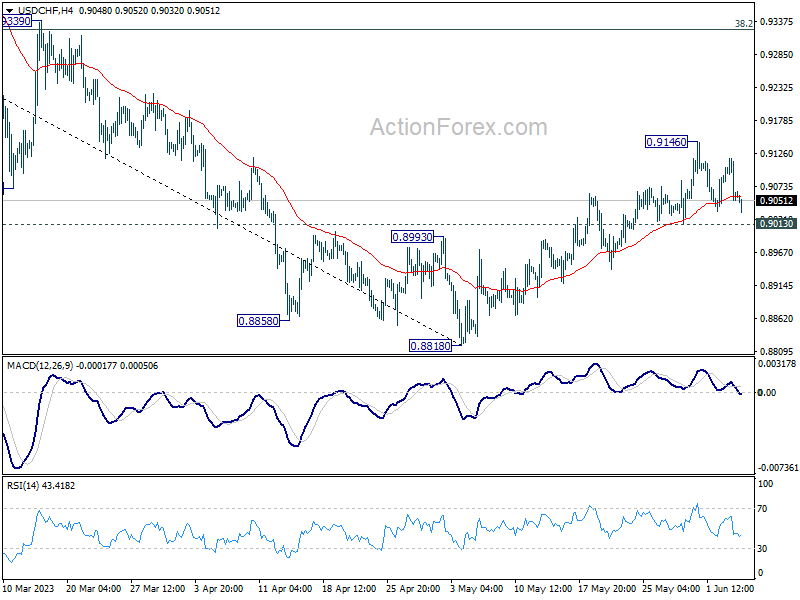

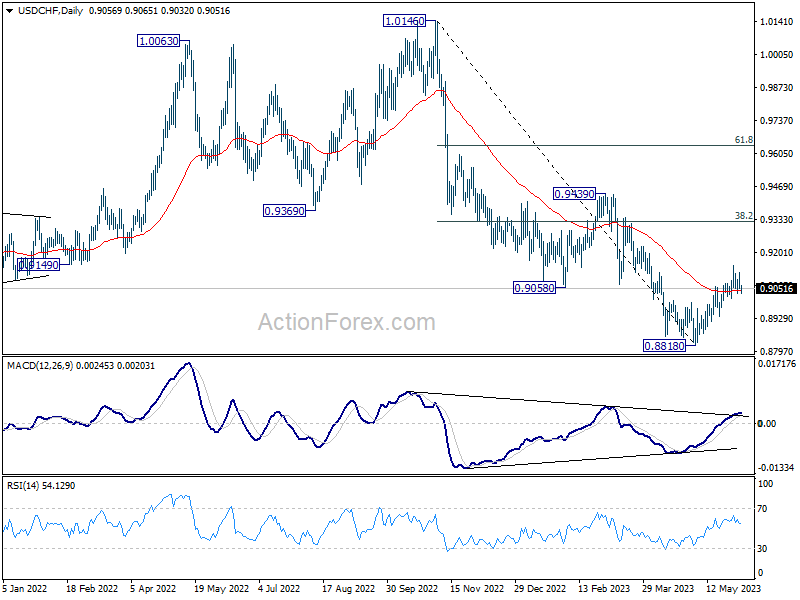

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9037; (P) 0.9078; (R1) 0.9105; More...

Intraday bias in USD/CHF remains neutral as consolidations continue, and further rally is expected with 0.9013 support intact. . Rise from 0.8818 short term bottom is seen as correcting whole down trend from 1.0146. Above 0.9146 will target 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, however, break of 0.9013 will turn bias back to the downside for retesting 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

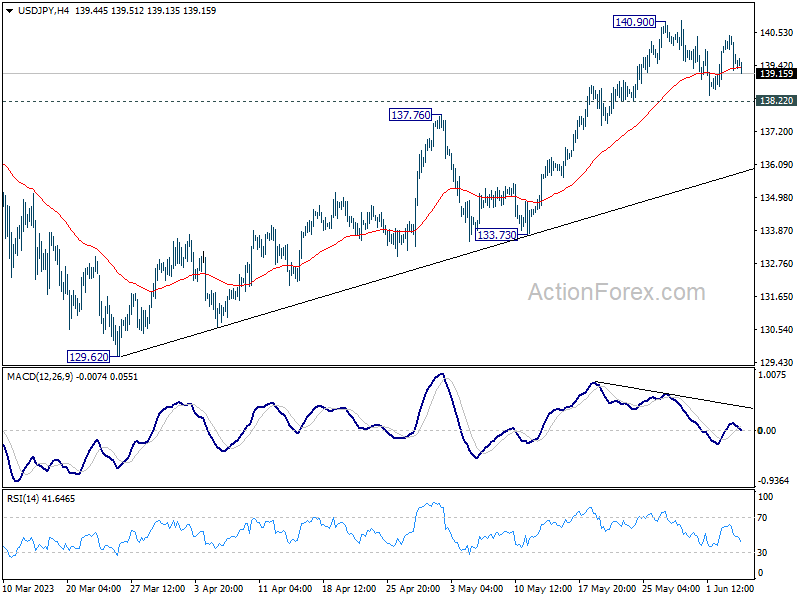

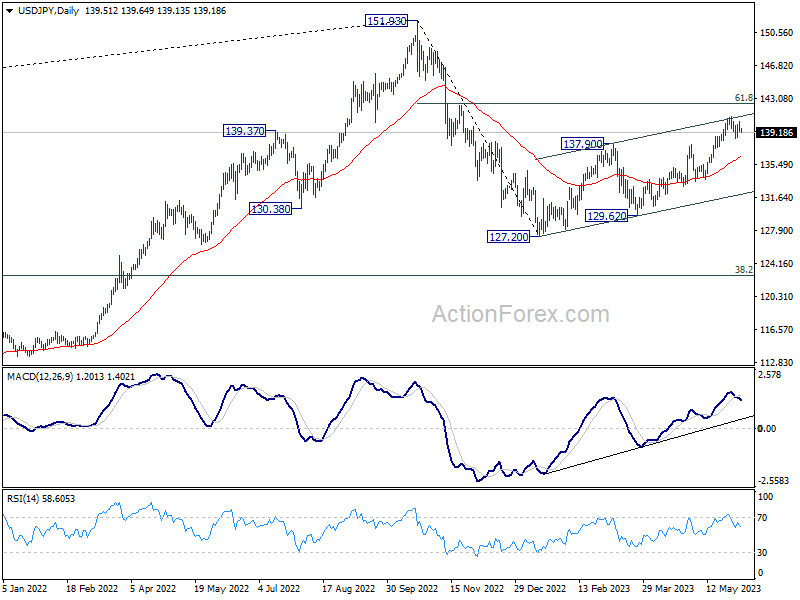

USD/JPY Daily Outlook

Daily Pivots: (S1) 139.07; (P) 139.76; (R1) 140.27; More...

Intraday bias in USD/JPY remains neutral as consolidation from 140.90 is extending. Further rally is expected as long as 138.22 minor support holds. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.35).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

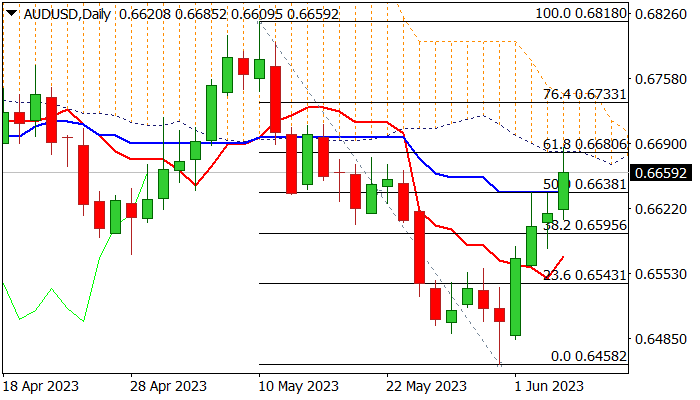

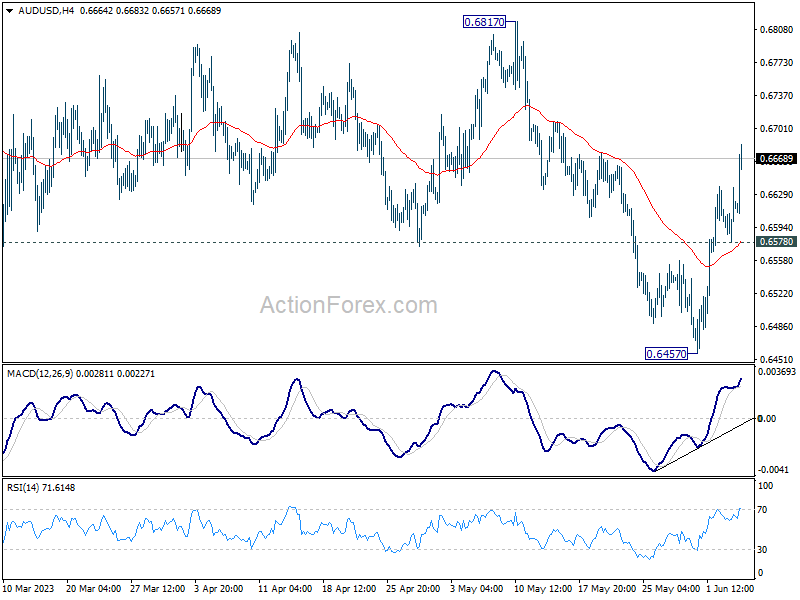

AUD/USD Daily Report

Daily Pivots: (S1) 0.6585; (P) 0.6611; (R1) 0.6644; More...

Intraday bias in AUD/USD remains on the upside as rebound from 0.6457 is extending today. Further rally would be seen to 0.6817 key structural resistance. On the downside, though, break of 0.6578 minor support will turn bias back to the downside for retesting 0.6457 low instead.

In the bigger picture, rejection by 55 W EMA (now at 0.6811) keeps medium term outlook bearish. Current development suggests that down trend from 0.8006 (2021 high) is possibly still in progress. Retest of 0.6169 (2022 low) should be seen next. Firm break there will confirm down trend resumption. For now, this will remain the favored case as long as 0.6817 resistance holds.