Sample Category Title

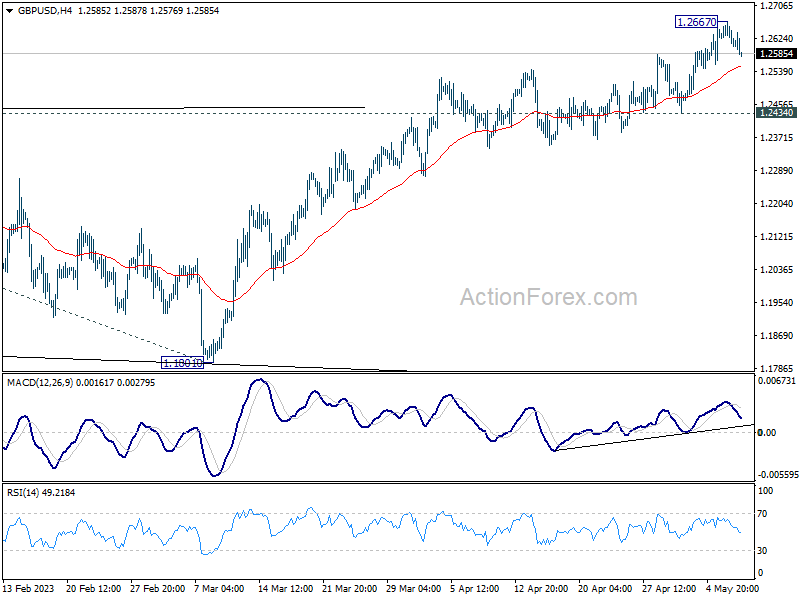

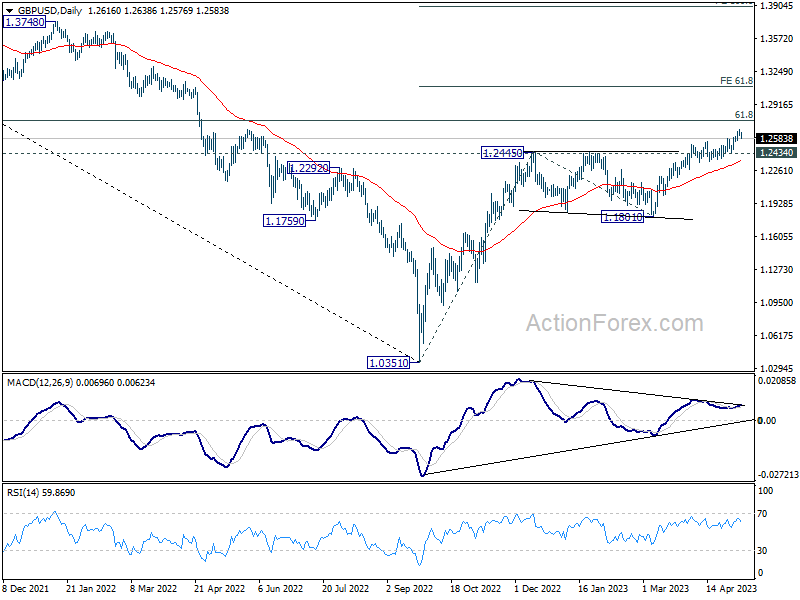

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2598; (P) 1.2634; (R1) 1.2654; More...

Intraday bias in GBP/USD stays neutral for consolidations below 1.2667. Near term outlook will stay bullish as long as 1.2434 support holds. Break of 1.2667 will resume larger up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

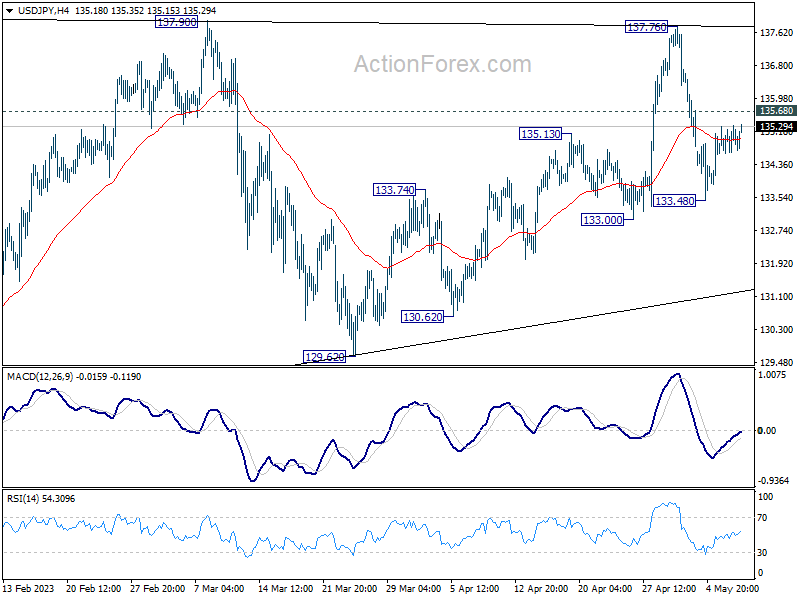

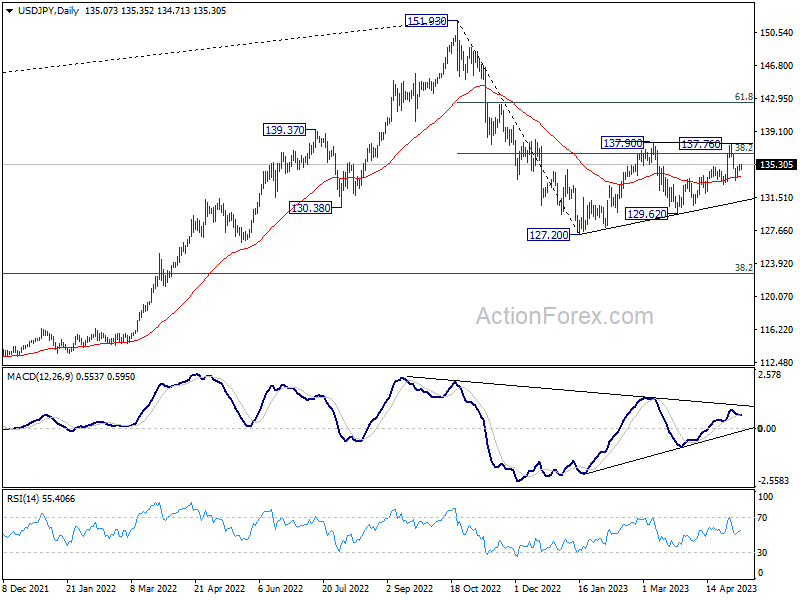

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 134.75; (P) 135.02; (R1) 135.40; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. Deeper decline is mildly in favor with 135.68 minor resistance intact. Fall from 137.76 is seen as the third leg of the pattern from 137.90. Below 133.48 will target 133.00 first, break will target 129.62 support. Still, as long as 129.62 holds, larger rebound from 127.20 is still in favor to resume at a later stage. On the upside, above 135.68 minor resistance will turn bias back to the upside for 137.76/90 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

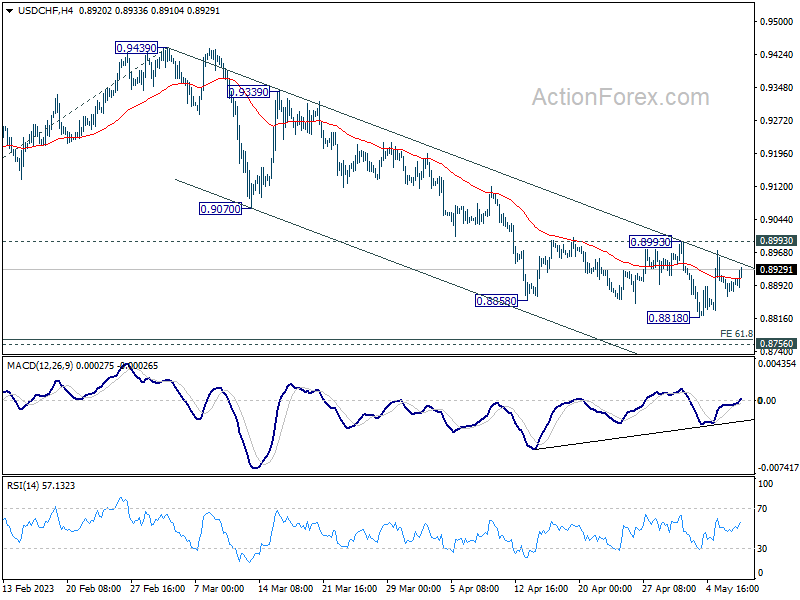

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8871; (P) 0.8892; (R1) 0.8915; More...

Range trading continues in USD/CHF and intraday bias remains neutral first. While down trend from 1.0146 could still extend lower, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound, at least on first attempt. On the upside, break of 0.8993 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Dollar and Yen Strike Back as Biden-McCarthy Meeting Eyed

Dollar and Yen are striking back on mild risk-off sentiment while Commodity currencies are paring some gains too. Eyes will be on the meeting between US President Joe Biden and Republican House Speaker Kevin McCarthy on debt ceiling. A final agreement on raising the debt limit is not expected today, but any rhetorics will be closely scrutinized, especially by American stocks and bonds investors.

Euro continues to be under broad based pressure today, shrugging off hawkish comments from ECB policymakers. Though, for now, Swiss Franc is slightly worse. Sterling is regaining some ground, with weak momentum, with traders largely holding their bets ahead of BoE rate decision and economic projections later this week.

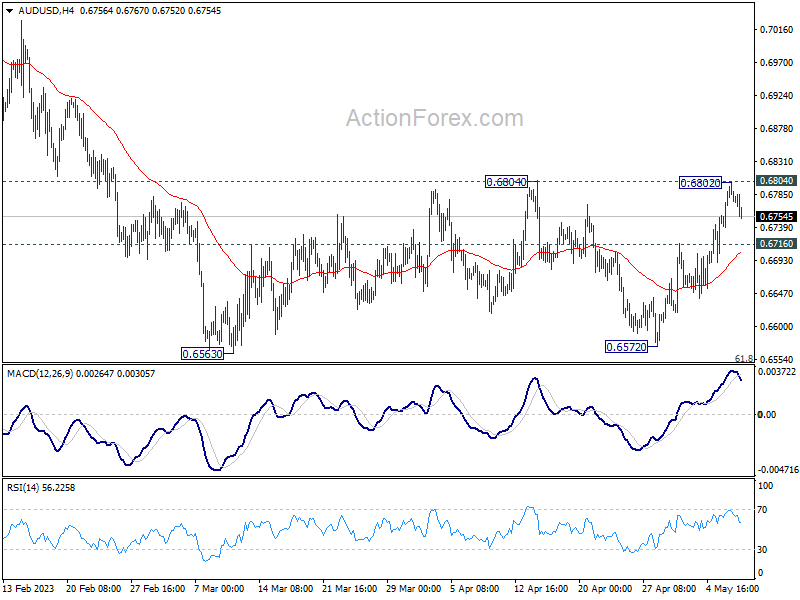

Technically, AUD/USD retreats just ahead of 0.6804 resistance. Break of 0.6716 support will turn near term bias back to the downside back towards 0.6563 low. Meanwhile, USD/CAD also recovers ahead of 1.3299 support. Reversal in risk sentiment could list USD/CAD back towards 1.3668 resistance.

In Europe, at the time of writing, FTSE is down -0.44%. DAX is down -0.38%. CAC is down -0.97%. Germany 10-year yield is down -0.0074 at 2.322. Earlier in Asia, Nikkei rose 1.01%. Hong Kong HSI dropped -2.12%. China Shanghai SSE dropped -1.10%. Singapore Strait Times dropped -0.45%. Japan 10-year JGB yield rose 0.0121 to 0.425.

ECB Kazaks asserts need for further rate hikes

In face of high inflation, ECB Governing Council member Martins Kazaks has voiced his belief that further interest rate hikes will be necessary to contain it. His remarks counter market expectations for borrowing costs to be cut as early as next spring, a notion Kazaks has described as "significantly premature."

He outlined a dual strategy to bring the current inflation rate of 7% back to ECB's target of 2%. "The first is raising the rates and of course we don't know where the terminal rate is," he commented. "Another thing is keeping those rates at elevated and sufficiently restrictive levels."

Despite concerns about potential economic risks from higher interest rates, Kazaks emphasized that the risk of doing too little to counter inflation was far greater than the risk of over-tightening. "Persistently high inflation is a bigger problem for society than a relatively short and shallow recession," he warned.

Underlining the importance of effective policy response, Kazaks cautioned, "Failing to contain inflation would be a failure because then the policy response in the second go would then need to be much tighter."

ECB Kazimir: We will have to keep raising interest rates for longer than anticipated

ECB might need to keep raising interest rates for longer than initially anticipated, according to Governing Council member Peter Kazimir. His comments indicate an evolving stance within ECB as it grapples with stubbornly high inflation in the Eurozone.

"Based on today's data, we will have to keep raising interest rates for longer than anticipated," Kazimir stated. He suggested a slower pace of rate hikes, at 25 basis points increments, as a measured approach that allows for longer-term adjustments, should incoming data warrant it. "So, slowing down the pace to 25 bps is a step that will allow us to go gradually higher for longer, should that be necessary and warranted by incoming data," he explained.

Kazimir pointed to core inflation trends, rising wage pressures, and high-profit margins as factors necessitating vigilance and the continued pursuit of ECB's current monetary policy trajectory. "The development of core inflation, the continued buildup of wage pressures, and high-profit margins call for vigilance and reconfirm the need to continue on our path," he said.

However, the true effectiveness of ECB's measures and the trajectory of inflation towards the target will not be fully assessed until the September forecast. "Our September forecast will be the earliest date to answer how effective our measures are and whether inflation is moving towards the target," Kazimir added.

BoJ Ueda sees position signs in trend inflation

BoJ Governor Kazuo Ueda pointed to encouraging signs in trend inflation during a recent parliamentary session. "We're seeing some positive signs in trend inflation, including inflation expectations," Ueda said. He added that once the BOJ could foresee inflation stably and sustainably meeting their 2% target, they would "abandon yield curve control and then move towards shrinking the bank's balance sheet."

Ueda also spoke about the upcoming monetary policy review, stating it would critically examine the benefits and side effects of past monetary policies. The review process will include workshops with private academics. However, the governor clarified that the central bank did not have any preconceived notions about how the review could influence future monetary policy decisions.

"We will take necessary policy steps at each of our rate reviews, with an eye on financial and price developments, even while we conduct the review," Ueda stated.

Australia sees second consecutive quarter of falling retail sales volume amidst rising living costs

Australia's retail sales volume declined by -0.6% qoq to AUD 96.17 billion in Q1 2023. Through the year, sales volume only managed to register a modest 0.3% yoy growth in the quarter.

ABS's head of retail statistics, Ben Dorber, noted that this marked the second consecutive quarter of falling retail sales volumes, primarily influenced by mounting cost of living pressures that continue to burden household spending.

"Outside of the COVID-19 pandemic period, this is the largest fall in retail sales volumes since the September quarter of 2009," Dorber stated, underlining the gravity of the situation.

Meanwhile, retail prices growth has slowed to 0.6% qoq in Q1. "Retail prices rose for the sixth straight quarter, but price growth this quarter is the smallest since September 2021," Dorber added.

He attributed the slowdown in price growth mainly to discounts on clothing and larger household items such as furniture and electronic goods. However, he noted that food retailing prices continued their upward trajectory.

China exports rose 8.5% yoy in Apr, exports to Russia surged 153% yoy

China's April exports outperformed expectations, growing by 8.5% yoy to reach USD 295.4B. This marked the second consecutive month of growth, exceeding anticipated 8.0% yoy. However, imports dropped by -7.9% yoy to USD 205.2B, falling short of expected 0.0% yoy. As a result, trade surplus widened from USD 88.2B to USD 90.2B, significantly surpassing the forecasted USD 69.0B.

Breaking down the numbers, exports to EU experienced a modest growth of 3.7% yoy, while imports from the bloc saw a slight decrease of -0.12% yoy. Trade with the US reflected a downturn, with exports dropping by -6.5% yoy and imports declining by -3.1% yoy.

Trade relations with ASEAN region were mixed, with exports increasing by 4.49% yoy, while imports fell by -6.25% yoy. Meanwhile, trade with Russia exhibited a significant surge. Chinese exports to Russia skyrocketed by a staggering 153.09% yoy, and imports also rose, though at a more modest rate of 8.06% yoy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8871; (P) 0.8892; (R1) 0.8915; More...

Range trading continues in USD/CHF and intraday bias remains neutral first. While down trend from 1.0146 could still extend lower, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound, at least on first attempt. On the upside, break of 0.8993 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 0.80% | 1.00% | 1.10% | |

| 23:30 | JPY | Overall Household Spending Y/Y Mar | -1.90% | 0.40% | 1.60% | |

| 03:00 | CNY | Trade Balance (USD) Apr | 90.2B | 69.0B | 88.2B | |

| 06:45 | EUR | France Trade Balance (EUR) Mar | -8.0B | -9.5B | -9.9B | -9.3B |

| 10:00 | USD | NFIB Business Optimism Index Apr | 89.0 | 89.6 | 90.1 |

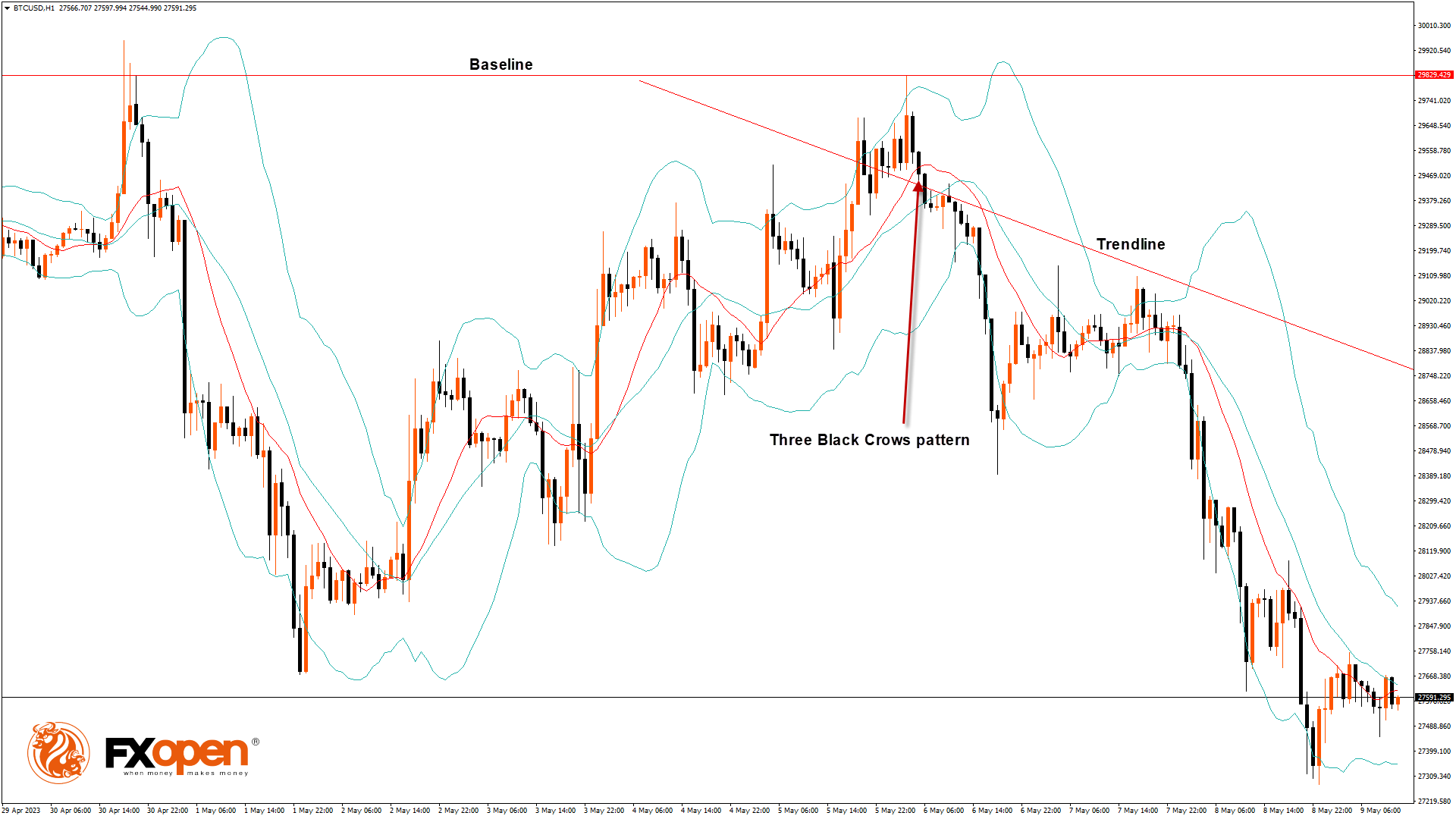

BTCUSD Analysis: Three Black Crows Pattern below $29,829

Bitcoin was unable to continue its bullish momentum from last week, and after touching a high of $29,829 on May 06, we can see a continuous decline in the bitcoin price, with immediate targets located in the range of $26500 and $27000.

We can clearly see a bearish three black crows pattern below the $29,829 handle on the H1 timeframe.

The price of Bitcoin continues to move in a bearish momentum, which is expected to continue towards the $27,000 handle.

Both the STOCH and Williams’s percent range indicate overbought levels, which means that in the immediate short term, a decline in the price is expected.

The Bitcoin chart is ranging near a new record low for 1 month.

The relative strength index is at 39.90, indicating a very weak demand for Bitcoin and the continuation of the selling pressure in the markets.

Bitcoin is now moving below its 100-hour exponential moving average and below its 200-hour exponential moving average.

Most of the major technical indicators are giving a bearish signal, which means that in the immediate short term, we are expecting targets of $26,500 and $27,000.

The average true range indicates less market volatility with mild bearish momentum.

- Bitcoin bearish reversal is seen below $29,829.

- The RSI remains below 50, indicating a bearish market.

- The price is now trading below its pivot level of $27,622.

- The short-term range is mildly bearish.

- The momentum indicator is back under zero.

Bitcoin Bearish Reversal Seen below $29,829

The price of Bitcoin entered into a consolidation zone above the $27,000 handle after which we can see the continuation of the bearish moves.

There is a bullish trend reversal pattern with adaptive moving average AMA-20 and AMA-50 in the daily timeframe.

We can see the formation of bearish engulfing lines in the 4-hourly timeframe.

We have also seen a bearish harami cross pattern located in the 15-minutes timeframe.

A support zone is located at $26,092, which is a 61.8% retracement from the 52 week low, and at $26,670, which is a 3-10 day MACD oscillator stalls .

BTCUSD is now facing its classic support level of $27,454 and Fibonacci resistance level of $27,583 breaking which the price will be able to move to $27,000.

There is an increase of 3.08% in the daily trading volume, which is normal. The short-term outlook for Bitcoin is bearish, the medium-term outlook has turned bearish, and the long-term outlook remains neutral under present market conditions.

The Week Ahead

We can see that Bitcoin price remains well supported above the $27,000 handle and the continuation pattern is seen, with the current support at $25,281, which is a 50% retracement from 13 week high/low.

The immediate expected target is $26,500, after which we may see some consolidation in the zone of the $27,000 level.

Monthly RSI is at 49.79, which indicates the Neutral market and the shift towards the consolidation zone in the medium-term range.

We can see the formation of a bearish trend line from $29,829 to $27,356.

The BTCUSD is now facing resistance at $28,051, which is a 14-3 day raw stochastic at 30%, and at 28,266 which is a 14 day RSI at 50%.

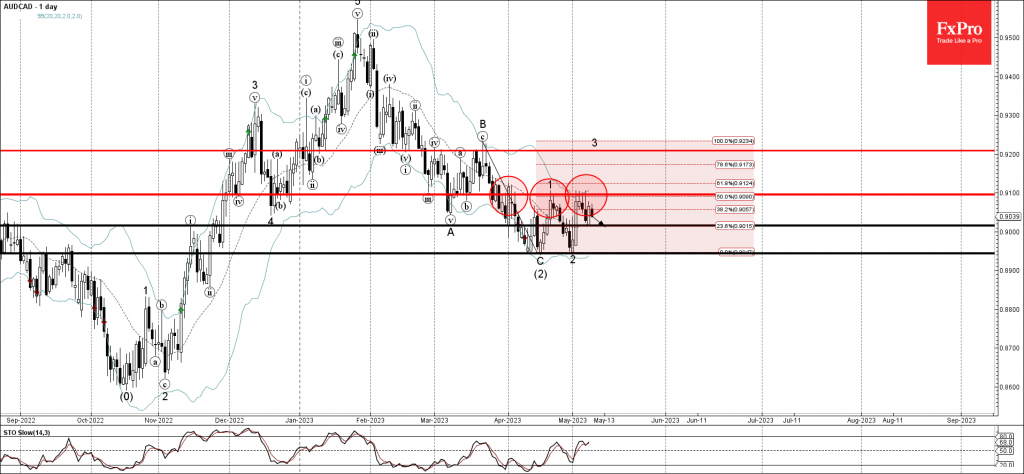

AUDCAD Wave Analysis

- AUDCAD reversed from resistance level 0.9100

- Likely to fall to support level 0.9015

AUDCAD earlier reversed down from the pivotal resistance level 0.9100 (which has been repeatedly reversing the price from the start of April).

The downward reversal from the resistance level 0.9100 is the 4th consecutive downward reversal from this price level – signalling its strength.

Given the strength of the resistance level 0.9100, AUDCAD can be expected to fall further toward the next support level 0.9015 (yesterday’s low).

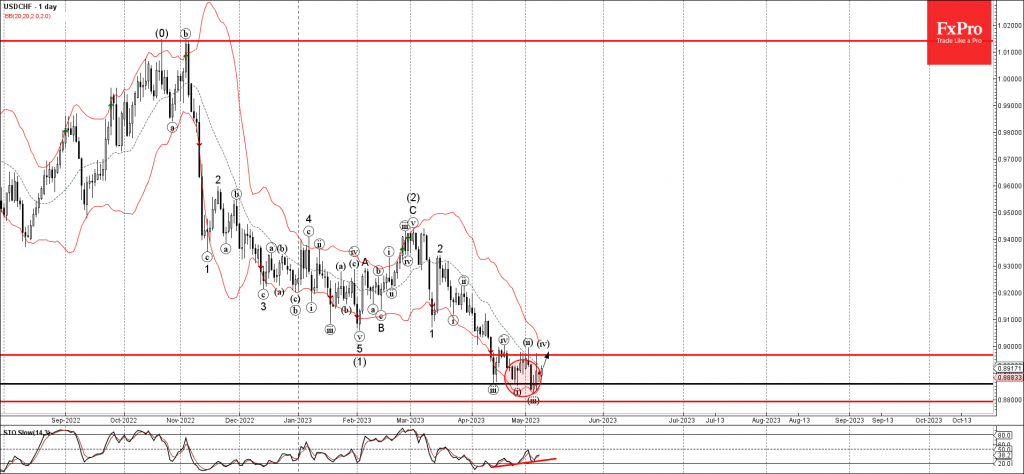

USDCHF Wave Analysis

- USDCHF reversed from key support level 0.8860

- Likely to rise to resistance level 0.8965

USDCHF currency pair recently reversed up from the key support level 0.8860 (which has been steadily reversing the pair from the middle of April).

The upward reversal from the support level 0.8860 follows the earlier upward reversal which created the daily Morning Star Doji.

Given the triple bullish divergence on the daily Stochastic, USDCHF can be expected to rise further toward the next resistance level 0.8965 (which stopped the earlier waves (iv) and (ii)).

Bitcoin Falls Under Pressure

Market picture

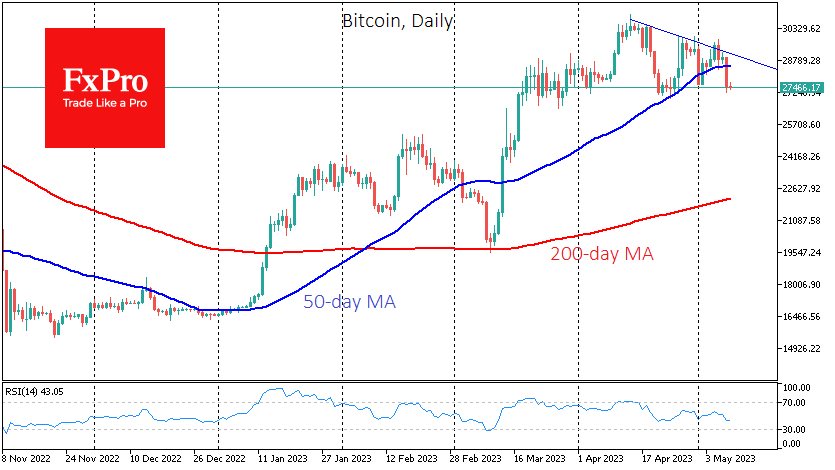

The total capitalisation of the cryptocurrency market fell by 2% to $1.14 trillion over the last 24 hours. Over the same period, bitcoin lost 2.6%, Ethereum lost 1.7%, and the top 10 altcoins lost between 1.4% (BNB) and 5% (Polygon).

Bitcoin lost around $1500 on Monday to $28.5K amid rumours of a possible collapse of Binance. The world’s largest cryptocurrency exchange twice suspended BTC withdrawals due to network congestion.

The technical picture shows local victory for the bears, as the sharp drop in price started from the downside resistance that has been in place since the middle of last month. In a strong move, the price broke below the 50-day moving average for the first time since March 13th. The price is testing support near $27K, from which the coin has been rallying for the past two months.

Fees on the Bitcoin network hit a record high on May 8th. In some cases, transaction fees on the BTC blockchain exceeded $10K, with block 788762 setting the record for the day costing $15,834. The BTC network processes around seven transactions per second and cannot quickly confirm payments when users are active, causing queues to form.

According to CryptoQuant, users withdrew over 195,000 BTC (over $5.6 billion) from Binance in one day. In addition, according to Bloomberg, the US Department of Justice has launched an investigation into the exchange, suspecting it of violating sanctions against Russia.

News background

YouTube analyst Jason Pizzino said that negative news failed to stop Bitcoin’s rally after a strong bearish signal after the $20K breakout failed in early March. He believes BTC should soon be in the $32K to $42K range.

According to Validus Power, investment in bitcoin, gold and real estate can protect investors against losses related to the banking crisis.

The prime minister of Liechtenstein said the country would allow citizens to pay for public services using Bitcoin. He also did not rule out the possibility of the state investing some of its reserves in BTC.

Famous investor and head of Berkshire Hathaway, Warren Buffett, said that people’s loss of confidence in the dollar does not mean that Bitcoin will become a global reserve currency.

Argentina’s central bank has banned the sale of cryptocurrencies through payment applications. The regulator said it was trying to reduce the financial risks that transactions in digital assets could pose.

AUD/USD Dips on Soft Retail Sales

- AUD/USD ends 6-day rally

- Australian retail sales decline

- Fed warns that banks are tightening credit

The Australian dollar is in negative territory, ending a rally of close to 200 points. In the European session, AUD/USD is trading at 0.6760, down 0.29% on the day.

Australian retail sales decline

Australian retail sales posted a decline of 0.6% in the first quarter, following a downwardly revised reading of -0.3% in Q4 2022. The reading matched the consensus, but investors were not pleased with a second straight decline and the Aussie has lost ground today. The National Australia Bank responded to the release by warning that a “consumer recession” had arrived.

Australians are holding tight onto their wallets due to the uncertainty in economic conditions. The cost-of-living crisis, driven by high inflation and rising interest rates, has driven down household spending. The new budget may help matters a little, but inflation will have to continue moving lower before consumers increase spending.

Australia will release consumer confidence for May on Wednesday, with the markets braced for a decline of -1.7% after a sharp gain of 9.4% in April.

The Federal Reserve has warned that the turbulence in the banking industry had led to tighter credit conditions which could slow down growth in the US economy. These concerns were highlighted in the Fed’s bi-annual financial stability report. The Fed’s quarterly Senior Loan Officer Opinion Survey noted that banks expected to continue tightening lending requirements and that bank officials expressed concerns about recession and deposit withdrawals.

The Fed isn’t about to pivot on its rate policy due to the stress in the banking sector. The financial stability report said that “a large majority of banks” were able handle the strain from higher rates and noted that banks were “well capitalised”. Still, the Fed will have to keep in mind the danger of contagion and give thought to cutting rates later in the year in order to minimize the chances of a recession.

AUD/USD Technical

- AUD/USD faces resistance at 0.6706 and 0.6803

- 0.6654 and 0.6557 are providing support

Will Bank of England Once Again Fail to Address the Inflation Problem?

Events elsewhere have been stealing the headlines lately, but this week’s focus will almost entirely be on the UK as the BoE is holding its rate setting meeting on Thursday. Will the BoE decision provide another boost to the pound against the euro?

BoE's inflation problem

Banking sector shenanigans in the US, the much-talked Chinese reopening and euro area developments have recently monopolized the market’s interest. But this week the BoE will be in the spotlight. This is the third meeting for 2023 and comes a week after the crucial Fed and ECB meetings. The market is pricing in a very strong probability of a 25bps move. Interestingly, the market is expecting a total of 65 bps of rate hikes (including Thursday’s move) until the November 2, 2023 meeting, contrary to the rate cuts expectations for the Fed.

We understand the reasons behind these market expectations, but we are not confident that the BoE members have taken seriously enough the inflation ravaging the UK economy. It remains the only developed economy with double digit inflation – the March CPI printed at 10.1% year-on-year change – but their rhetoric is less hawkish when compared to other top central banks that face lessened inflationary pressures.

We have commented in the past that the BoE was kind of hoping that a recession in the US would cause a slowdown in the UK and hence push inflation lower aggressively. This has not taken place, up to now, as the US economy continues to grow at a respectable rate.

Could the BoE hike by 50 bps?

The BoE hiked by 25 bps at the March 23 meeting following the 50 bps rate move at the February gathering. While the elevated outright inflation rate means that the BoE has to continue removing accommodation, the MPC members are expected to weigh the pros and cons of hiking rates more aggressively. From one side, the housing sector is clearly suffering from the higher rates, especially when examining the recent mortgage lending figures. On the other hand, the Services PMI figure stands at a 1-year high, and the average earnings are flirting with the 2021 highs.

Should the BoE opt for a stronger move, the focus would then turn to the Monetary Policy Statement (formerly Quarterly Inflation Report) published also on Thursday. At its February edition this Statement was forecasting 3% inflation for the fourth quarter of 2024. A stronger rate hike on Thursday would mean increased inflation projections at the famous Table 1.A.

Data calendar full

The week opened with the BRC retail sales printing stronger than expected and the Halifax House Price index returning to negative territory. On Friday and as the market digests the BoE announcement, we will get the preliminary GDP print for the first quarter of 2023 along with the March industrial and manufacturing industrial data. Following the downside surprise at the US advance GDP print, there is a growing risk for a similar outcome on Friday.

Euro/pound broke through a key area – will the breakout last?

The February high of 0.8978 seems to have energized the pound bulls as the euro/pound pair has been recording a series of lower highs. However, since the eve of 2023 their efforts for a sustainable drop have stopped at the 0.8720 area, forming a descending triangle pattern. Interestingly, the pair has just broken below this level, but it needs a push from the BoE for this move to count.

A stronger than expected rate hike or a 25 bps move accompanied with hawkish rhetoric has the potential to push the euro/pound pair towards the 0.8635 area and test the December 2022 lows. On the other hand, a confirmation of the market expectations and the usual dovish rhetoric from Bailey et al could allow the euro bulls to regain market control and aim for the 0.88 area.